Accounting for Managers Report: IFRS, Stakeholders, and Decisions

VerifiedAdded on 2021/04/24

|13

|1379

|55

Report

AI Summary

This report provides an in-depth analysis of International Financial Reporting Standards (IFRS) and their crucial role in financial reporting. It begins by defining IFRS and outlining its objectives, emphasizing the importance of fair presentation in financial statements to accurately reflect an organization's financial position, performance, and cash flow. The report highlights the standard's guidelines for financial statement preparation, ensuring comparability and transparency. It then explores how financial statements are used by various stakeholders, including investors, creditors, employees, and government entities, in making informed decisions. The report also delves into common accounting ratios and the significance of financial information for small business owners and potential investors. Finally, it emphasizes the role of financial statements in assessing an organization's profitability, stability, and ability to meet its obligations, making it an essential tool for decision-making across multiple stakeholder groups. The report also includes a reference list of sources consulted.

Running head: ACCOUNTING FOR MANAGERS

Accounting for Managers

Name of the Student

Name of the University

Authors Note

Course ID

Accounting for Managers

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING FOR MANAGERS

Table of Contents

Requirement 1:...........................................................................................................................2

Requirement 2:...........................................................................................................................3

Requirement 3:...........................................................................................................................6

Requirement 4:...........................................................................................................................7

Requirement 5:...........................................................................................................................7

Requirement 6:...........................................................................................................................9

Reference list:...........................................................................................................................12

Table of Contents

Requirement 1:...........................................................................................................................2

Requirement 2:...........................................................................................................................3

Requirement 3:...........................................................................................................................6

Requirement 4:...........................................................................................................................7

Requirement 5:...........................................................................................................................7

Requirement 6:...........................................................................................................................9

Reference list:...........................................................................................................................12

2ACCOUNTING FOR MANAGERS

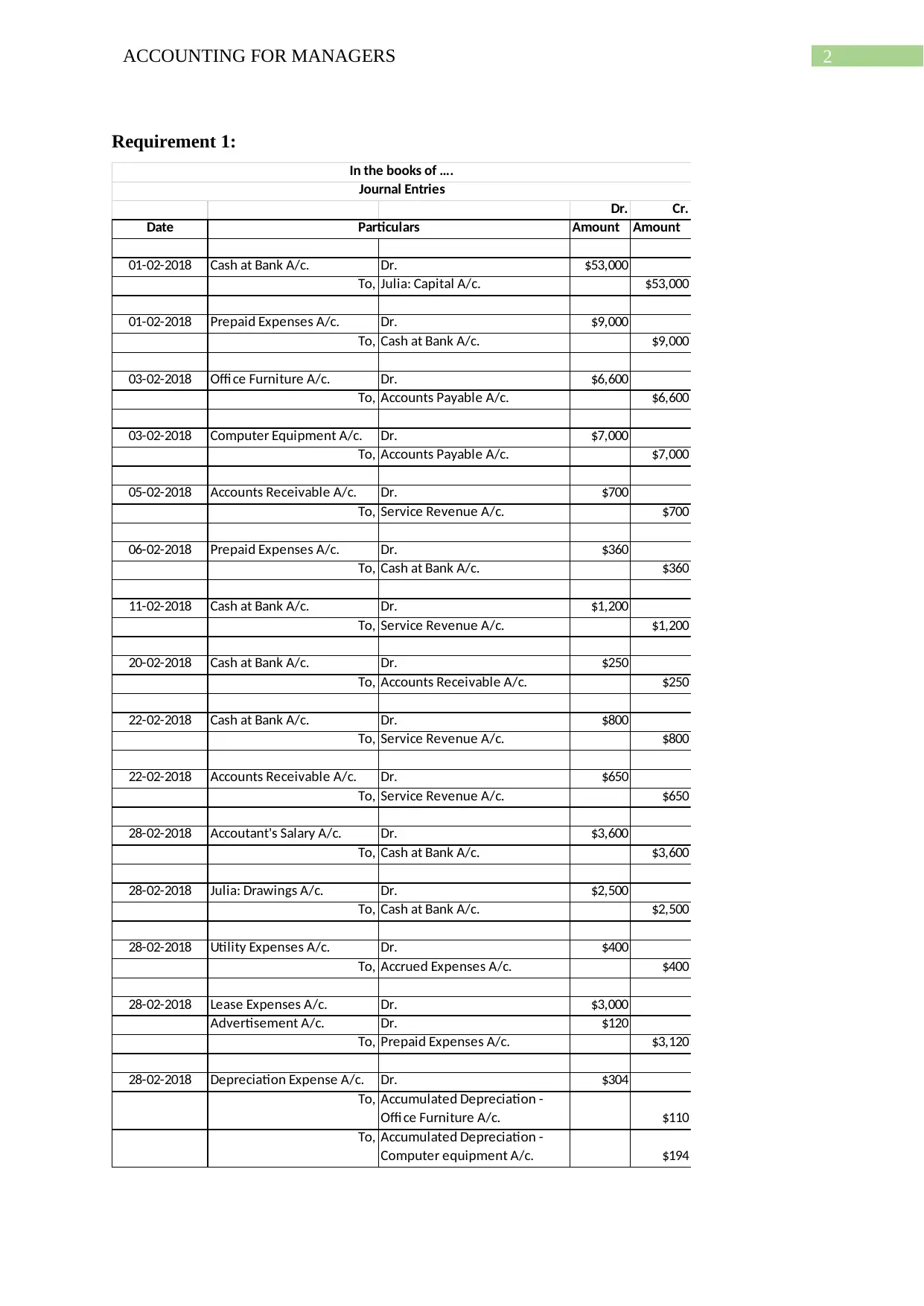

Requirement 1:

Dr. Cr.

Date Amount Amount

01-02-2018 Cash at Bank A/c. Dr. $53,000

To, Julia: Capital A/c. $53,000

01-02-2018 Prepaid Expenses A/c. Dr. $9,000

To, Cash at Bank A/c. $9,000

03-02-2018 Offi ce Furniture A/c. Dr. $6,600

To, Accounts Payable A/c. $6,600

03-02-2018 Computer Equipment A/c. Dr. $7,000

To, Accounts Payable A/c. $7,000

05-02-2018 Accounts Receivable A/c. Dr. $700

To, Service Revenue A/c. $700

06-02-2018 Prepaid Expenses A/c. Dr. $360

To, Cash at Bank A/c. $360

11-02-2018 Cash at Bank A/c. Dr. $1,200

To, Service Revenue A/c. $1,200

20-02-2018 Cash at Bank A/c. Dr. $250

To, Accounts Receivable A/c. $250

22-02-2018 Cash at Bank A/c. Dr. $800

To, Service Revenue A/c. $800

22-02-2018 Accounts Receivable A/c. Dr. $650

To, Service Revenue A/c. $650

28-02-2018 Accoutant's Salary A/c. Dr. $3,600

To, Cash at Bank A/c. $3,600

28-02-2018 Julia: Drawings A/c. Dr. $2,500

To, Cash at Bank A/c. $2,500

28-02-2018 Utility Expenses A/c. Dr. $400

To, Accrued Expenses A/c. $400

28-02-2018 Lease Expenses A/c. Dr. $3,000

Advertisement A/c. Dr. $120

To, Prepaid Expenses A/c. $3,120

28-02-2018 Depreciation Expense A/c. Dr. $304

To, Accumulated Depreciation -

Offi ce Furniture A/c. $110

To, Accumulated Depreciation -

Computer equipment A/c. $194

Particulars

In the books of ….

Journal Entries

Requirement 1:

Dr. Cr.

Date Amount Amount

01-02-2018 Cash at Bank A/c. Dr. $53,000

To, Julia: Capital A/c. $53,000

01-02-2018 Prepaid Expenses A/c. Dr. $9,000

To, Cash at Bank A/c. $9,000

03-02-2018 Offi ce Furniture A/c. Dr. $6,600

To, Accounts Payable A/c. $6,600

03-02-2018 Computer Equipment A/c. Dr. $7,000

To, Accounts Payable A/c. $7,000

05-02-2018 Accounts Receivable A/c. Dr. $700

To, Service Revenue A/c. $700

06-02-2018 Prepaid Expenses A/c. Dr. $360

To, Cash at Bank A/c. $360

11-02-2018 Cash at Bank A/c. Dr. $1,200

To, Service Revenue A/c. $1,200

20-02-2018 Cash at Bank A/c. Dr. $250

To, Accounts Receivable A/c. $250

22-02-2018 Cash at Bank A/c. Dr. $800

To, Service Revenue A/c. $800

22-02-2018 Accounts Receivable A/c. Dr. $650

To, Service Revenue A/c. $650

28-02-2018 Accoutant's Salary A/c. Dr. $3,600

To, Cash at Bank A/c. $3,600

28-02-2018 Julia: Drawings A/c. Dr. $2,500

To, Cash at Bank A/c. $2,500

28-02-2018 Utility Expenses A/c. Dr. $400

To, Accrued Expenses A/c. $400

28-02-2018 Lease Expenses A/c. Dr. $3,000

Advertisement A/c. Dr. $120

To, Prepaid Expenses A/c. $3,120

28-02-2018 Depreciation Expense A/c. Dr. $304

To, Accumulated Depreciation -

Offi ce Furniture A/c. $110

To, Accumulated Depreciation -

Computer equipment A/c. $194

Particulars

In the books of ….

Journal Entries

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING FOR MANAGERS

Requirement 2:

Cash at Bank A/c.

Date Particulars Amount Amount Balance

01-02-2018 Julia: Capital A/c. $53,000 $53,000 Dr.

01-02-2018 Prepaid Expenses A/c. $9,000 $44,000 Dr.

06-02-2018 Prepaid Expenses A/c. $360 $43,640 Dr.

11-02-2018 Service Revenue A/c. $1,200 $44,840 Dr.

20-02-2018 Accounts Receivable A/c. $250 $45,090 Dr.

22-02-2018 Service Revenue A/c. $800 $45,890 Dr.

28-02-2018 Accoutant's Salary A/c. $3,600 $42,290 Dr.

28-02-2018 Julia: Drawings A/c. $2,500 $39,790 Dr.

Accounts Receivable A/c.

Date Particulars Amount Amount Balance

05-02-2018 Service Revenue A/c. $700 $700 Dr.

20-02-2018 Cash at Bank A/c. $250 $450 Dr.

22-02-2018 Service Revenue A/c. $650 $1,100 Dr.

Prepaid Expenses A/c.

Date Particulars Amount Amount Balance

01-02-2018 Cash at Bank A/c. $9,000 $9,000 Dr.

06-02-2018 Cash at Bank A/c. $360 $9,360 Dr.

28-02-2018 Lease Expenses A/c. $3,000 $6,360 Dr.

Advertisement A/c. $120 $6,240 Dr.

Office Furniture A/c.

Date Particulars Amount Amount Balance

03-02-2018 Accounts Payable A/c. $6,600 $6,600 Dr.

Computer Equipment A/c.

Date Particulars Amount Amount Balance

03-02-2018 Accounts Payable A/c. $7,000 $7,000 Dr.

Requirement 2:

Cash at Bank A/c.

Date Particulars Amount Amount Balance

01-02-2018 Julia: Capital A/c. $53,000 $53,000 Dr.

01-02-2018 Prepaid Expenses A/c. $9,000 $44,000 Dr.

06-02-2018 Prepaid Expenses A/c. $360 $43,640 Dr.

11-02-2018 Service Revenue A/c. $1,200 $44,840 Dr.

20-02-2018 Accounts Receivable A/c. $250 $45,090 Dr.

22-02-2018 Service Revenue A/c. $800 $45,890 Dr.

28-02-2018 Accoutant's Salary A/c. $3,600 $42,290 Dr.

28-02-2018 Julia: Drawings A/c. $2,500 $39,790 Dr.

Accounts Receivable A/c.

Date Particulars Amount Amount Balance

05-02-2018 Service Revenue A/c. $700 $700 Dr.

20-02-2018 Cash at Bank A/c. $250 $450 Dr.

22-02-2018 Service Revenue A/c. $650 $1,100 Dr.

Prepaid Expenses A/c.

Date Particulars Amount Amount Balance

01-02-2018 Cash at Bank A/c. $9,000 $9,000 Dr.

06-02-2018 Cash at Bank A/c. $360 $9,360 Dr.

28-02-2018 Lease Expenses A/c. $3,000 $6,360 Dr.

Advertisement A/c. $120 $6,240 Dr.

Office Furniture A/c.

Date Particulars Amount Amount Balance

03-02-2018 Accounts Payable A/c. $6,600 $6,600 Dr.

Computer Equipment A/c.

Date Particulars Amount Amount Balance

03-02-2018 Accounts Payable A/c. $7,000 $7,000 Dr.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING FOR MANAGERS

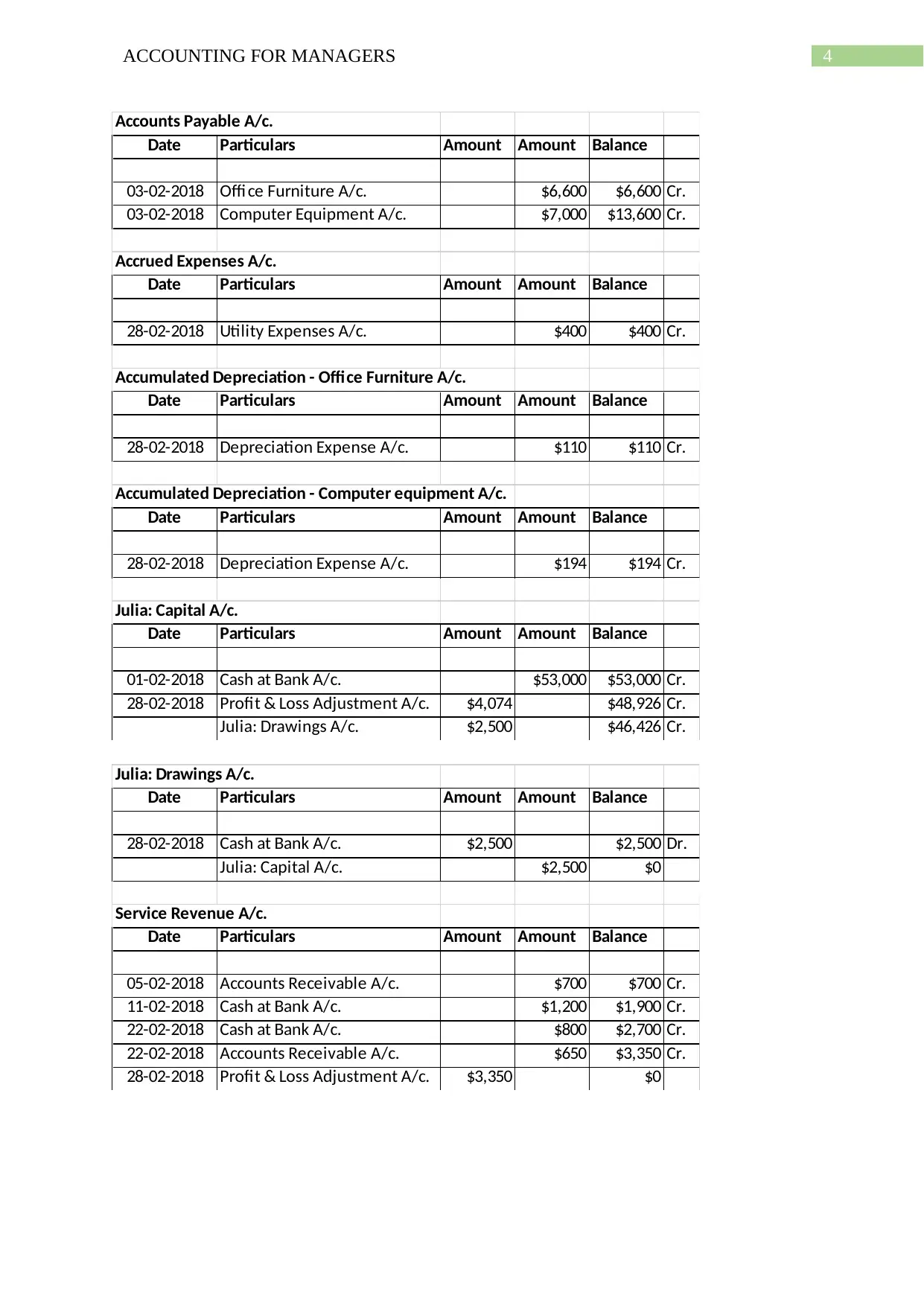

Accounts Payable A/c.

Date Particulars Amount Amount Balance

03-02-2018 Offi ce Furniture A/c. $6,600 $6,600 Cr.

03-02-2018 Computer Equipment A/c. $7,000 $13,600 Cr.

Accrued Expenses A/c.

Date Particulars Amount Amount Balance

28-02-2018 Utility Expenses A/c. $400 $400 Cr.

Accumulated Depreciation - Office Furniture A/c.

Date Particulars Amount Amount Balance

28-02-2018 Depreciation Expense A/c. $110 $110 Cr.

Accumulated Depreciation - Computer equipment A/c.

Date Particulars Amount Amount Balance

28-02-2018 Depreciation Expense A/c. $194 $194 Cr.

Julia: Capital A/c.

Date Particulars Amount Amount Balance

01-02-2018 Cash at Bank A/c. $53,000 $53,000 Cr.

28-02-2018 Profit & Loss Adjustment A/c. $4,074 $48,926 Cr.

Julia: Drawings A/c. $2,500 $46,426 Cr.

Julia: Drawings A/c.

Date Particulars Amount Amount Balance

28-02-2018 Cash at Bank A/c. $2,500 $2,500 Dr.

Julia: Capital A/c. $2,500 $0

Service Revenue A/c.

Date Particulars Amount Amount Balance

05-02-2018 Accounts Receivable A/c. $700 $700 Cr.

11-02-2018 Cash at Bank A/c. $1,200 $1,900 Cr.

22-02-2018 Cash at Bank A/c. $800 $2,700 Cr.

22-02-2018 Accounts Receivable A/c. $650 $3,350 Cr.

28-02-2018 Profit & Loss Adjustment A/c. $3,350 $0

Accounts Payable A/c.

Date Particulars Amount Amount Balance

03-02-2018 Offi ce Furniture A/c. $6,600 $6,600 Cr.

03-02-2018 Computer Equipment A/c. $7,000 $13,600 Cr.

Accrued Expenses A/c.

Date Particulars Amount Amount Balance

28-02-2018 Utility Expenses A/c. $400 $400 Cr.

Accumulated Depreciation - Office Furniture A/c.

Date Particulars Amount Amount Balance

28-02-2018 Depreciation Expense A/c. $110 $110 Cr.

Accumulated Depreciation - Computer equipment A/c.

Date Particulars Amount Amount Balance

28-02-2018 Depreciation Expense A/c. $194 $194 Cr.

Julia: Capital A/c.

Date Particulars Amount Amount Balance

01-02-2018 Cash at Bank A/c. $53,000 $53,000 Cr.

28-02-2018 Profit & Loss Adjustment A/c. $4,074 $48,926 Cr.

Julia: Drawings A/c. $2,500 $46,426 Cr.

Julia: Drawings A/c.

Date Particulars Amount Amount Balance

28-02-2018 Cash at Bank A/c. $2,500 $2,500 Dr.

Julia: Capital A/c. $2,500 $0

Service Revenue A/c.

Date Particulars Amount Amount Balance

05-02-2018 Accounts Receivable A/c. $700 $700 Cr.

11-02-2018 Cash at Bank A/c. $1,200 $1,900 Cr.

22-02-2018 Cash at Bank A/c. $800 $2,700 Cr.

22-02-2018 Accounts Receivable A/c. $650 $3,350 Cr.

28-02-2018 Profit & Loss Adjustment A/c. $3,350 $0

5ACCOUNTING FOR MANAGERS

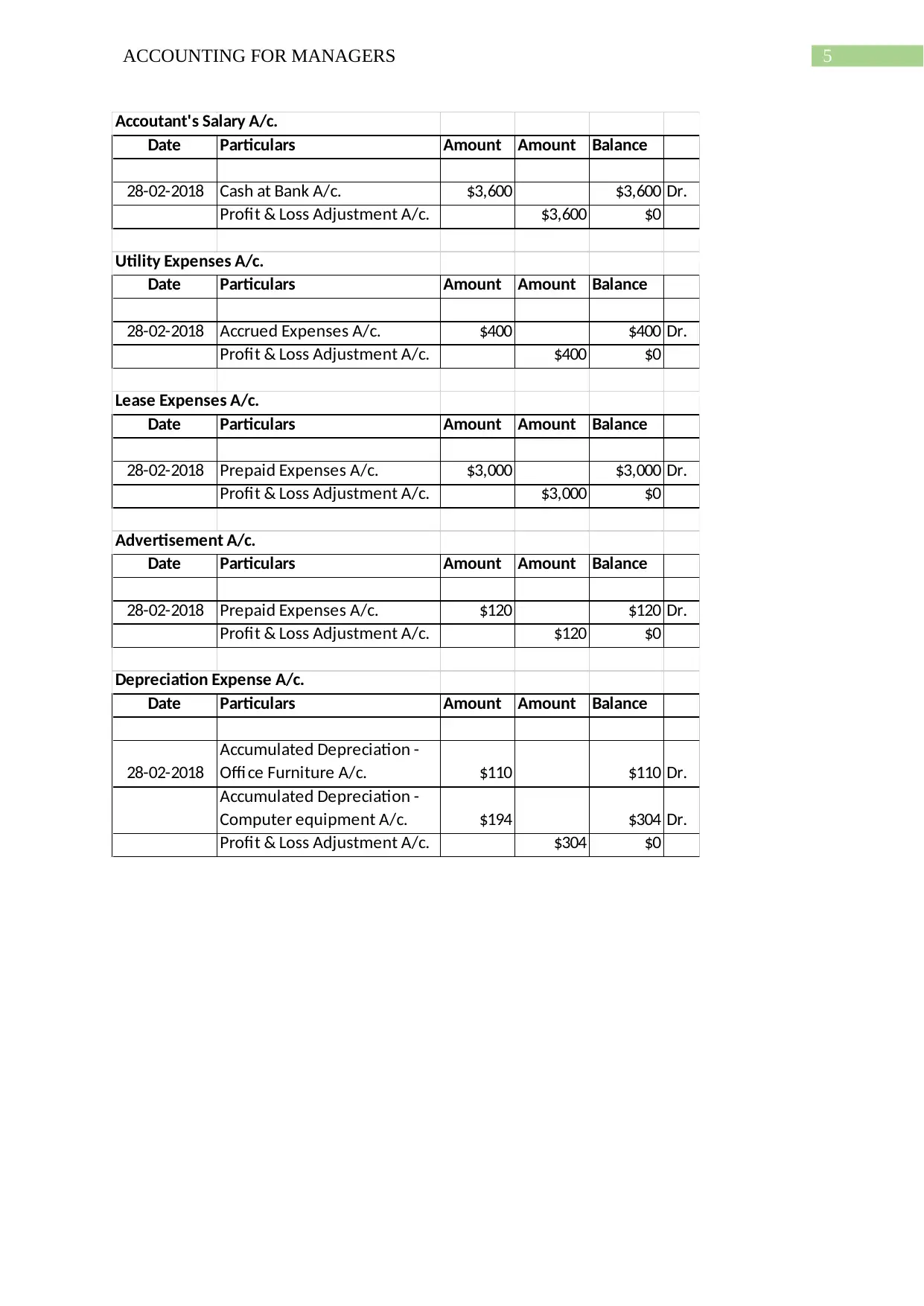

Accoutant's Salary A/c.

Date Particulars Amount Amount Balance

28-02-2018 Cash at Bank A/c. $3,600 $3,600 Dr.

Profit & Loss Adjustment A/c. $3,600 $0

Utility Expenses A/c.

Date Particulars Amount Amount Balance

28-02-2018 Accrued Expenses A/c. $400 $400 Dr.

Profit & Loss Adjustment A/c. $400 $0

Lease Expenses A/c.

Date Particulars Amount Amount Balance

28-02-2018 Prepaid Expenses A/c. $3,000 $3,000 Dr.

Profit & Loss Adjustment A/c. $3,000 $0

Advertisement A/c.

Date Particulars Amount Amount Balance

28-02-2018 Prepaid Expenses A/c. $120 $120 Dr.

Profit & Loss Adjustment A/c. $120 $0

Depreciation Expense A/c.

Date Particulars Amount Amount Balance

28-02-2018

Accumulated Depreciation -

Offi ce Furniture A/c. $110 $110 Dr.

Accumulated Depreciation -

Computer equipment A/c. $194 $304 Dr.

Profit & Loss Adjustment A/c. $304 $0

Accoutant's Salary A/c.

Date Particulars Amount Amount Balance

28-02-2018 Cash at Bank A/c. $3,600 $3,600 Dr.

Profit & Loss Adjustment A/c. $3,600 $0

Utility Expenses A/c.

Date Particulars Amount Amount Balance

28-02-2018 Accrued Expenses A/c. $400 $400 Dr.

Profit & Loss Adjustment A/c. $400 $0

Lease Expenses A/c.

Date Particulars Amount Amount Balance

28-02-2018 Prepaid Expenses A/c. $3,000 $3,000 Dr.

Profit & Loss Adjustment A/c. $3,000 $0

Advertisement A/c.

Date Particulars Amount Amount Balance

28-02-2018 Prepaid Expenses A/c. $120 $120 Dr.

Profit & Loss Adjustment A/c. $120 $0

Depreciation Expense A/c.

Date Particulars Amount Amount Balance

28-02-2018

Accumulated Depreciation -

Offi ce Furniture A/c. $110 $110 Dr.

Accumulated Depreciation -

Computer equipment A/c. $194 $304 Dr.

Profit & Loss Adjustment A/c. $304 $0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING FOR MANAGERS

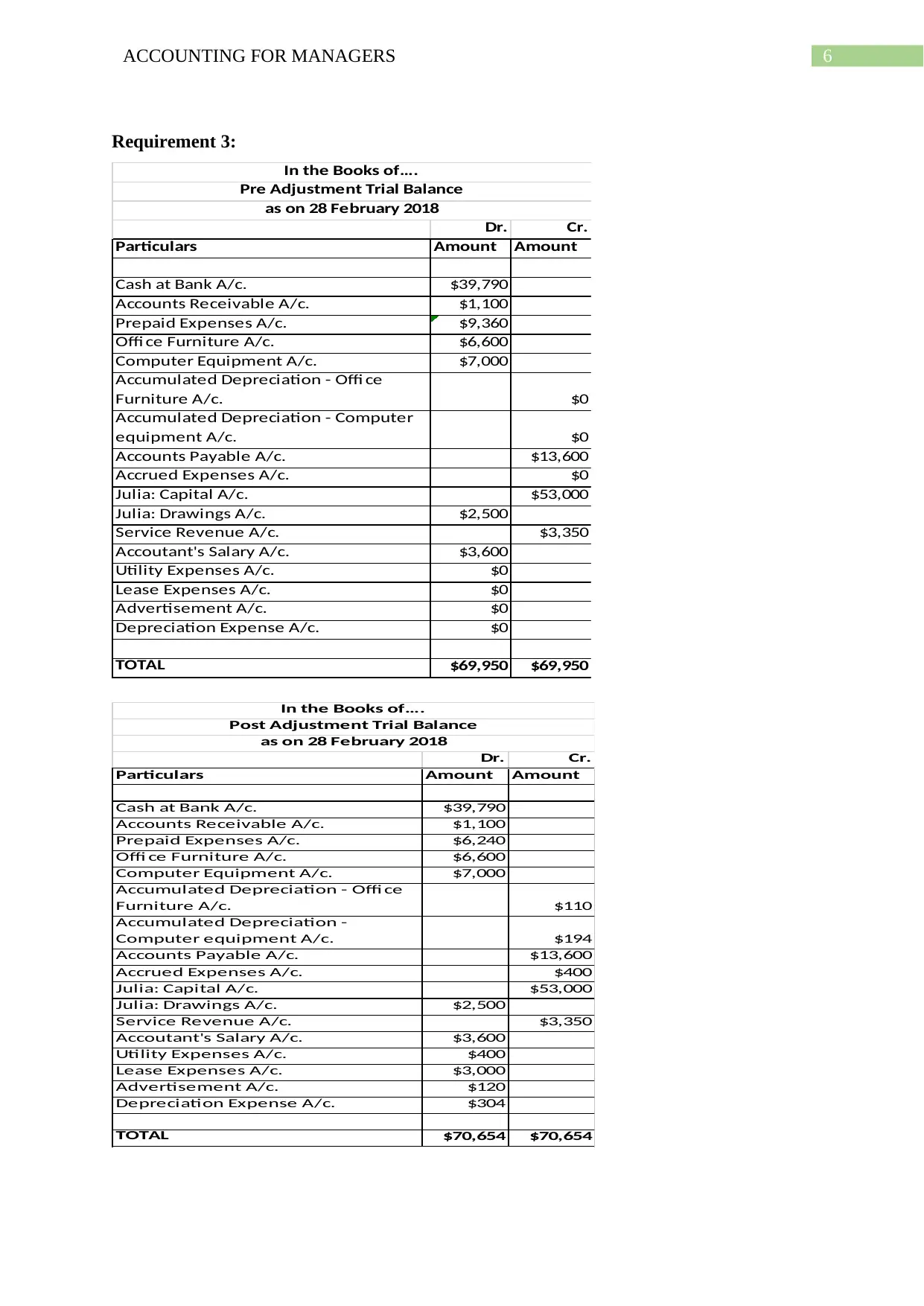

Requirement 3:

Dr. Cr.

Particulars Amount Amount

Cash at Bank A/c. $39,790

Accounts Receivable A/c. $1,100

Prepaid Expenses A/c. $9,360

Offi ce Furniture A/c. $6,600

Computer Equipment A/c. $7,000

Accumulated Depreciation - Offi ce

Furniture A/c. $0

Accumulated Depreciation - Computer

equipment A/c. $0

Accounts Payable A/c. $13,600

Accrued Expenses A/c. $0

Julia: Capital A/c. $53,000

Julia: Drawings A/c. $2,500

Service Revenue A/c. $3,350

Accoutant's Salary A/c. $3,600

Utility Expenses A/c. $0

Lease Expenses A/c. $0

Advertisement A/c. $0

Depreciation Expense A/c. $0

TOTAL $69,950 $69,950

In the Books of….

Pre Adjustment Trial Balance

as on 28 February 2018

Dr. Cr.

Particulars Amount Amount

Cash at Bank A/c. $39,790

Accounts Receivable A/c. $1,100

Prepaid Expenses A/c. $6,240

Offi ce Furniture A/c. $6,600

Computer Equipment A/c. $7,000

Accumulated Depreciation - Offi ce

Furniture A/c. $110

Accumulated Depreciation -

Computer equipment A/c. $194

Accounts Payable A/c. $13,600

Accrued Expenses A/c. $400

Julia: Capital A/c. $53,000

Julia: Drawings A/c. $2,500

Service Revenue A/c. $3,350

Accoutant's Salary A/c. $3,600

Utility Expenses A/c. $400

Lease Expenses A/c. $3,000

Advertisement A/c. $120

Depreciation Expense A/c. $304

TOTAL $70,654 $70,654

In the Books of….

Post Adjustment Trial Balance

as on 28 February 2018

Requirement 3:

Dr. Cr.

Particulars Amount Amount

Cash at Bank A/c. $39,790

Accounts Receivable A/c. $1,100

Prepaid Expenses A/c. $9,360

Offi ce Furniture A/c. $6,600

Computer Equipment A/c. $7,000

Accumulated Depreciation - Offi ce

Furniture A/c. $0

Accumulated Depreciation - Computer

equipment A/c. $0

Accounts Payable A/c. $13,600

Accrued Expenses A/c. $0

Julia: Capital A/c. $53,000

Julia: Drawings A/c. $2,500

Service Revenue A/c. $3,350

Accoutant's Salary A/c. $3,600

Utility Expenses A/c. $0

Lease Expenses A/c. $0

Advertisement A/c. $0

Depreciation Expense A/c. $0

TOTAL $69,950 $69,950

In the Books of….

Pre Adjustment Trial Balance

as on 28 February 2018

Dr. Cr.

Particulars Amount Amount

Cash at Bank A/c. $39,790

Accounts Receivable A/c. $1,100

Prepaid Expenses A/c. $6,240

Offi ce Furniture A/c. $6,600

Computer Equipment A/c. $7,000

Accumulated Depreciation - Offi ce

Furniture A/c. $110

Accumulated Depreciation -

Computer equipment A/c. $194

Accounts Payable A/c. $13,600

Accrued Expenses A/c. $400

Julia: Capital A/c. $53,000

Julia: Drawings A/c. $2,500

Service Revenue A/c. $3,350

Accoutant's Salary A/c. $3,600

Utility Expenses A/c. $400

Lease Expenses A/c. $3,000

Advertisement A/c. $120

Depreciation Expense A/c. $304

TOTAL $70,654 $70,654

In the Books of….

Post Adjustment Trial Balance

as on 28 February 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING FOR MANAGERS

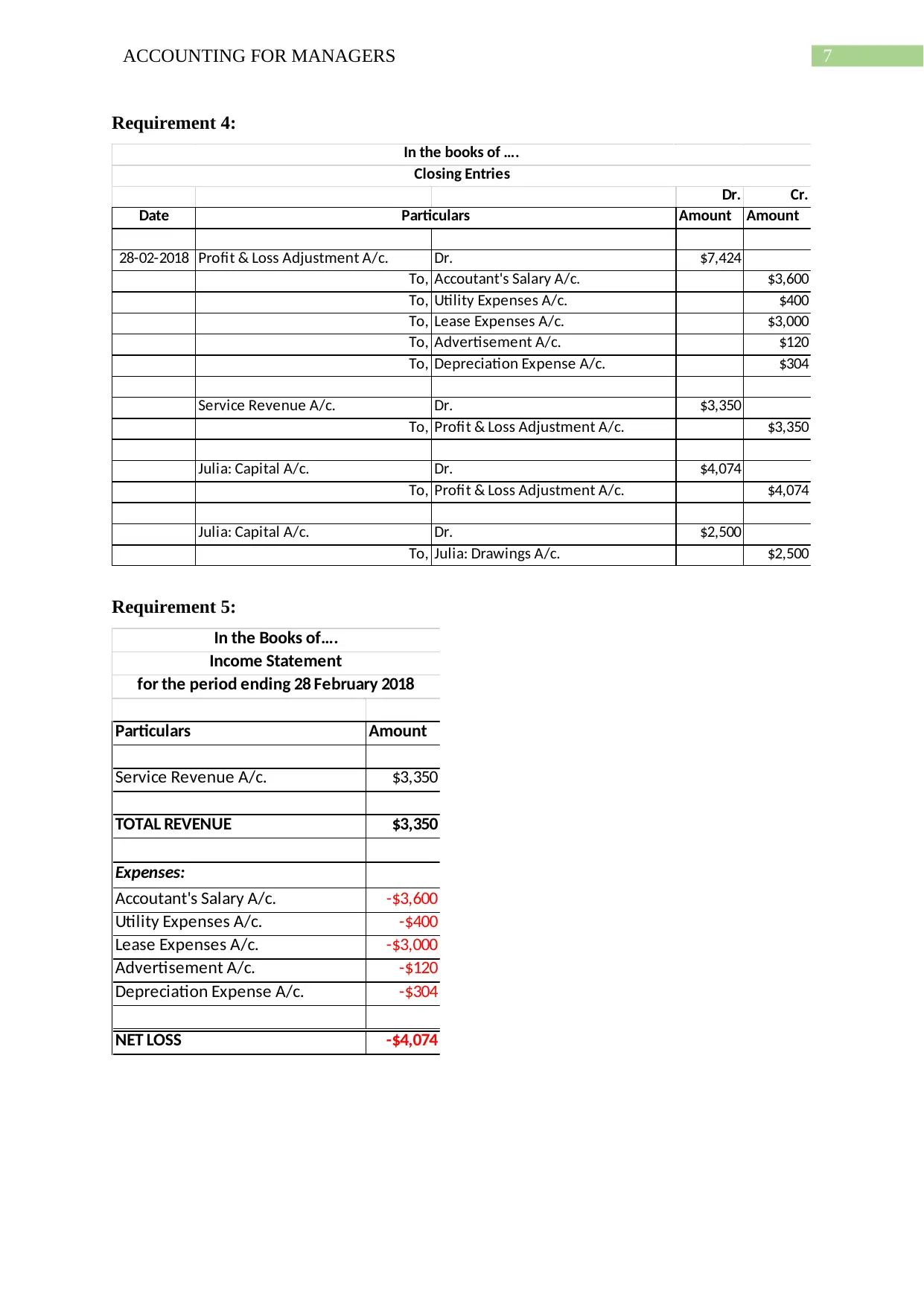

Requirement 4:

Dr. Cr.

Date Amount Amount

28-02-2018 Profit & Loss Adjustment A/c. Dr. $7,424

To, Accoutant's Salary A/c. $3,600

To, Utility Expenses A/c. $400

To, Lease Expenses A/c. $3,000

To, Advertisement A/c. $120

To, Depreciation Expense A/c. $304

Service Revenue A/c. Dr. $3,350

To, Profit & Loss Adjustment A/c. $3,350

Julia: Capital A/c. Dr. $4,074

To, Profit & Loss Adjustment A/c. $4,074

Julia: Capital A/c. Dr. $2,500

To, Julia: Drawings A/c. $2,500

In the books of ….

Closing Entries

Particulars

Requirement 5:

Particulars Amount

Service Revenue A/c. $3,350

TOTAL REVENUE $3,350

Expenses:

Accoutant's Salary A/c. -$3,600

Utility Expenses A/c. -$400

Lease Expenses A/c. -$3,000

Advertisement A/c. -$120

Depreciation Expense A/c. -$304

NET LOSS -$4,074

In the Books of….

Income Statement

for the period ending 28 February 2018

Requirement 4:

Dr. Cr.

Date Amount Amount

28-02-2018 Profit & Loss Adjustment A/c. Dr. $7,424

To, Accoutant's Salary A/c. $3,600

To, Utility Expenses A/c. $400

To, Lease Expenses A/c. $3,000

To, Advertisement A/c. $120

To, Depreciation Expense A/c. $304

Service Revenue A/c. Dr. $3,350

To, Profit & Loss Adjustment A/c. $3,350

Julia: Capital A/c. Dr. $4,074

To, Profit & Loss Adjustment A/c. $4,074

Julia: Capital A/c. Dr. $2,500

To, Julia: Drawings A/c. $2,500

In the books of ….

Closing Entries

Particulars

Requirement 5:

Particulars Amount

Service Revenue A/c. $3,350

TOTAL REVENUE $3,350

Expenses:

Accoutant's Salary A/c. -$3,600

Utility Expenses A/c. -$400

Lease Expenses A/c. -$3,000

Advertisement A/c. -$120

Depreciation Expense A/c. -$304

NET LOSS -$4,074

In the Books of….

Income Statement

for the period ending 28 February 2018

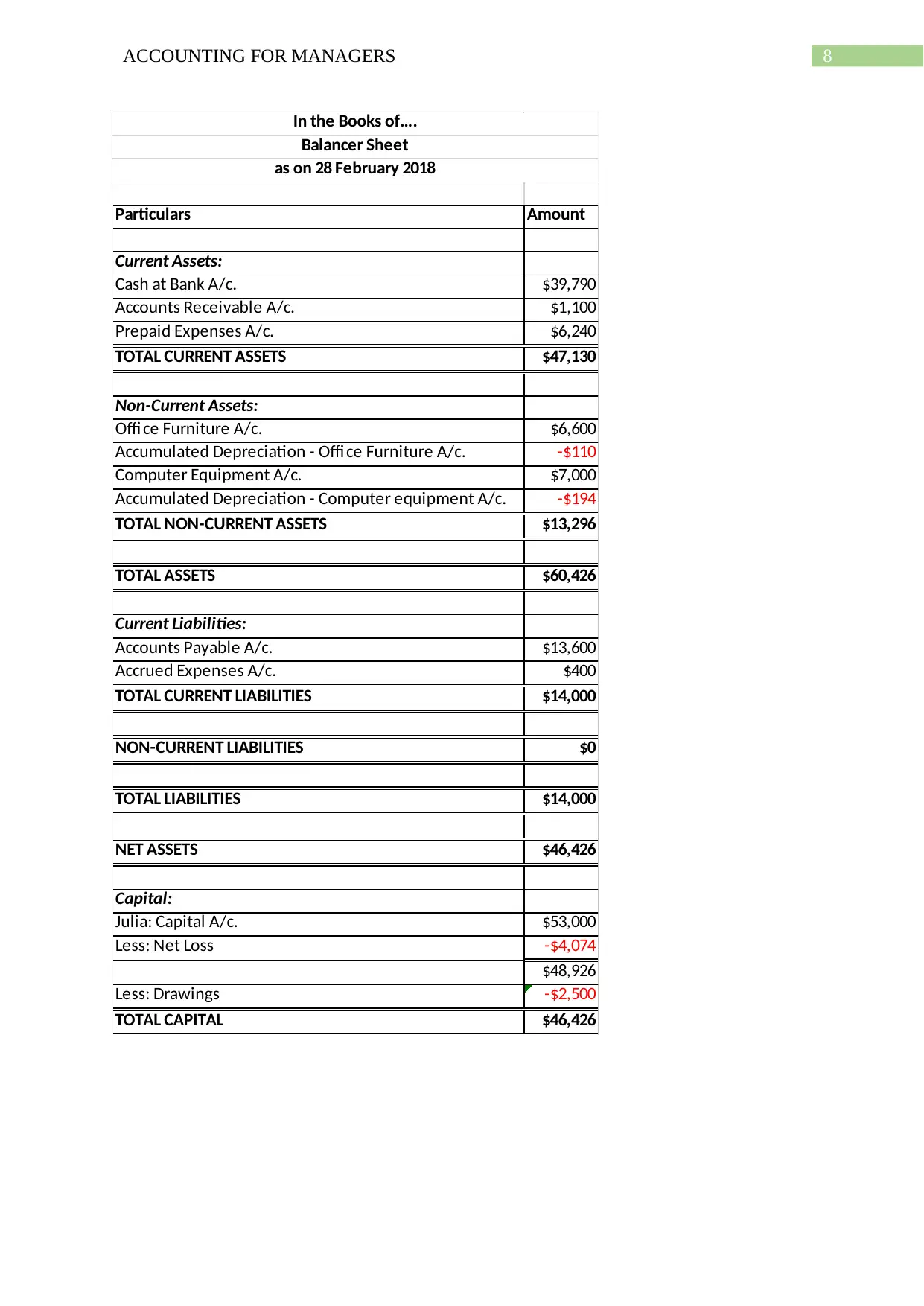

8ACCOUNTING FOR MANAGERS

Particulars Amount

Current Assets:

Cash at Bank A/c. $39,790

Accounts Receivable A/c. $1,100

Prepaid Expenses A/c. $6,240

TOTAL CURRENT ASSETS $47,130

Non-Current Assets:

Offi ce Furniture A/c. $6,600

Accumulated Depreciation - Offi ce Furniture A/c. -$110

Computer Equipment A/c. $7,000

Accumulated Depreciation - Computer equipment A/c. -$194

TOTAL NON-CURRENT ASSETS $13,296

TOTAL ASSETS $60,426

Current Liabilities:

Accounts Payable A/c. $13,600

Accrued Expenses A/c. $400

TOTAL CURRENT LIABILITIES $14,000

NON-CURRENT LIABILITIES $0

TOTAL LIABILITIES $14,000

NET ASSETS $46,426

Capital:

Julia: Capital A/c. $53,000

Less: Net Loss -$4,074

$48,926

Less: Drawings -$2,500

TOTAL CAPITAL $46,426

In the Books of….

Balancer Sheet

as on 28 February 2018

Particulars Amount

Current Assets:

Cash at Bank A/c. $39,790

Accounts Receivable A/c. $1,100

Prepaid Expenses A/c. $6,240

TOTAL CURRENT ASSETS $47,130

Non-Current Assets:

Offi ce Furniture A/c. $6,600

Accumulated Depreciation - Offi ce Furniture A/c. -$110

Computer Equipment A/c. $7,000

Accumulated Depreciation - Computer equipment A/c. -$194

TOTAL NON-CURRENT ASSETS $13,296

TOTAL ASSETS $60,426

Current Liabilities:

Accounts Payable A/c. $13,600

Accrued Expenses A/c. $400

TOTAL CURRENT LIABILITIES $14,000

NON-CURRENT LIABILITIES $0

TOTAL LIABILITIES $14,000

NET ASSETS $46,426

Capital:

Julia: Capital A/c. $53,000

Less: Net Loss -$4,074

$48,926

Less: Drawings -$2,500

TOTAL CAPITAL $46,426

In the Books of….

Balancer Sheet

as on 28 February 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING FOR MANAGERS

Requirement 6:

The international financial reporting standard can be defined as the standard and

interpretation that is adopted by the international accounting standard board. The standard lay

down the guidelines that is required to be used by the companies in the preparation and

presentation of the financial statements in order to make sure that the financial statements of

the organizations are comparable with the previous year’s financial statements and with the

statement of the other entity (Christensen et al. 2015). The objective of the international

financial reporting standard in the preparation and presentation of financial statement is to lay

down the overall requirements relating to the structure and contents of the financial statement

together with some general functions. The requirements of the standard is generally

applicable to the general purpose financial statements that are presented and prepared in

compliance with the international financial reporting standard.

The standard requires the financial statements must be presented fairly in order to

reflect the financial position, financial performance and cash flow of the organization. Fair

presentation needs faithful presentation of the effects of transactions and conditions that are

in compliance with the definition and identification criteria for assets, liabilities, income and

expenditure that are set out under the framework (Nobes 2014). The international financial

reporting standard is laid down by the international accounting standard board. The objective

of the IASB is to create the standard in the best interest of the public. It requires presentation

of financial statements with understandable quality.

According to the international financial reporting standard the financial performance

and financial position and the cash flow of the organization should be presented in the fairly

manner (Flower 2015). The fair presentation of the financial statements, events and

transactions must be fairly reported to the financial report in compliance with the recognition

and measurement values for the components of financial report. The IFRS provides that

entity should prepare the financial statement in compliance with the guidelines of the related

disclosure requirements. To attain the fair presentation the entity must make sure that the

selection and application of the accounting policies should in compliance with the

International Accounting Standard 8. The information that is provided in the financial

statement must contain all the necessary qualitative aspects of the financial statements (Li

2015). A commercial entity is required to provide complete and fair disclosure as per the

rules of the IFRS.

Requirement 6:

The international financial reporting standard can be defined as the standard and

interpretation that is adopted by the international accounting standard board. The standard lay

down the guidelines that is required to be used by the companies in the preparation and

presentation of the financial statements in order to make sure that the financial statements of

the organizations are comparable with the previous year’s financial statements and with the

statement of the other entity (Christensen et al. 2015). The objective of the international

financial reporting standard in the preparation and presentation of financial statement is to lay

down the overall requirements relating to the structure and contents of the financial statement

together with some general functions. The requirements of the standard is generally

applicable to the general purpose financial statements that are presented and prepared in

compliance with the international financial reporting standard.

The standard requires the financial statements must be presented fairly in order to

reflect the financial position, financial performance and cash flow of the organization. Fair

presentation needs faithful presentation of the effects of transactions and conditions that are

in compliance with the definition and identification criteria for assets, liabilities, income and

expenditure that are set out under the framework (Nobes 2014). The international financial

reporting standard is laid down by the international accounting standard board. The objective

of the IASB is to create the standard in the best interest of the public. It requires presentation

of financial statements with understandable quality.

According to the international financial reporting standard the financial performance

and financial position and the cash flow of the organization should be presented in the fairly

manner (Flower 2015). The fair presentation of the financial statements, events and

transactions must be fairly reported to the financial report in compliance with the recognition

and measurement values for the components of financial report. The IFRS provides that

entity should prepare the financial statement in compliance with the guidelines of the related

disclosure requirements. To attain the fair presentation the entity must make sure that the

selection and application of the accounting policies should in compliance with the

International Accounting Standard 8. The information that is provided in the financial

statement must contain all the necessary qualitative aspects of the financial statements (Li

2015). A commercial entity is required to provide complete and fair disclosure as per the

rules of the IFRS.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING FOR MANAGERS

Financial statements are regarded as the structured representation of the financial

position and financial performance of an organization. An organization is required to present

the financial report with equal prominence as the complete set of financial report. An

organization whose financial report are in agreement with the IFRS standard is required to

make an explicit and unreserved statements of notes (Scott 2015). In virtual circumstances an

organization attains the fair presentation by complying with the applicable standards of IFRS.

The fair presentation also requires an organization to present the financial information by

taking into the considerations the accounting policies in such a way that it provides, relevant,

reliable and understandable information to the users.

The objective of the accounting is to offer information to the users of the financial

statement for the purpose of making decision. There are namely three areas where the users

of financial statement makes decision. The financial statement offers the investors with the

baseline of analysis for and comparison among the financial health of security issuing

instructions (Schaltegger and Burritt 2017). The financial accounting provides assistance to

the creditors in making decision regarding solvency, liquidity and creditworthiness of an

organization. The financial statement are used by the stakeholders in making decisions

regarding the allocation of the scare resources.

The stakeholders of the organization requires financial statement to assist them in

making decisions on what is to be done with the investment. The statement helps the

stakeholders in understanding whether they should hold, sell or buy the stocks more. The

perspective investors requires the financial information to provide access to the organizations

potential for success and generating profits (Wang 2014). Similarly the small business

owners should focus on the financial information in order to ascertain whether the business is

profitable or whether to continue the business, improve or drop it.

Stakeholders are reliant on the financial statement for making decisions regarding the

lending. There are numerous common accounting ratios that are relied upon by the creditors

namely the debt to equity ratio and the times interest earned ratio that are generally derived

from the financial statements (Warren and Jones 2018). Even for the business that are

privately owned that don’t generally follow the guidelines of the FASB no credit lending

institute considers the liability of the huge business loan without obtaining information from

the financial accounting techniques.

Financial statements are regarded as the structured representation of the financial

position and financial performance of an organization. An organization is required to present

the financial report with equal prominence as the complete set of financial report. An

organization whose financial report are in agreement with the IFRS standard is required to

make an explicit and unreserved statements of notes (Scott 2015). In virtual circumstances an

organization attains the fair presentation by complying with the applicable standards of IFRS.

The fair presentation also requires an organization to present the financial information by

taking into the considerations the accounting policies in such a way that it provides, relevant,

reliable and understandable information to the users.

The objective of the accounting is to offer information to the users of the financial

statement for the purpose of making decision. There are namely three areas where the users

of financial statement makes decision. The financial statement offers the investors with the

baseline of analysis for and comparison among the financial health of security issuing

instructions (Schaltegger and Burritt 2017). The financial accounting provides assistance to

the creditors in making decision regarding solvency, liquidity and creditworthiness of an

organization. The financial statement are used by the stakeholders in making decisions

regarding the allocation of the scare resources.

The stakeholders of the organization requires financial statement to assist them in

making decisions on what is to be done with the investment. The statement helps the

stakeholders in understanding whether they should hold, sell or buy the stocks more. The

perspective investors requires the financial information to provide access to the organizations

potential for success and generating profits (Wang 2014). Similarly the small business

owners should focus on the financial information in order to ascertain whether the business is

profitable or whether to continue the business, improve or drop it.

Stakeholders are reliant on the financial statement for making decisions regarding the

lending. There are numerous common accounting ratios that are relied upon by the creditors

namely the debt to equity ratio and the times interest earned ratio that are generally derived

from the financial statements (Warren and Jones 2018). Even for the business that are

privately owned that don’t generally follow the guidelines of the FASB no credit lending

institute considers the liability of the huge business loan without obtaining information from

the financial accounting techniques.

11ACCOUNTING FOR MANAGERS

The lenders of the funds namely the banks and the other financial institutions are keen

on obtaining the knowledge regarding the ability of the organization in meeting its debt

obligations upon the maturity of loan. Similar to lenders, the trade creditors and the supplier

are interested in understanding the capability of the organization to pay the obligations as and

when they become payable (Schaltegger and Burritt 2017). They are generally interested in

understanding the capability of the organization regarding its ability to meet the short term

debt obligations.

Stakeholders such as employees are keen on the financial statement to understand the

profitability and stability of the organization. They are generally reliant on the ability of the

organization to pay the salaries and give the employee benefit (Li 2015). The employees are

dependent on the financial position and performance of the organization to determine the

possibility of organization expansion and future growth. Government as the stakeholder are

interested on the organization financial statements for the purpose of taxation and regulatory

requirement purpose. The taxes are determined based on the outcome of the operating profit

and other base of tax. In general the government would like to understand the ability of the

entity as the taxpayer to ascertain the tax dues thereon. Hence, financial statement serves as

the important tool in decision making for several stakeholders.

The lenders of the funds namely the banks and the other financial institutions are keen

on obtaining the knowledge regarding the ability of the organization in meeting its debt

obligations upon the maturity of loan. Similar to lenders, the trade creditors and the supplier

are interested in understanding the capability of the organization to pay the obligations as and

when they become payable (Schaltegger and Burritt 2017). They are generally interested in

understanding the capability of the organization regarding its ability to meet the short term

debt obligations.

Stakeholders such as employees are keen on the financial statement to understand the

profitability and stability of the organization. They are generally reliant on the ability of the

organization to pay the salaries and give the employee benefit (Li 2015). The employees are

dependent on the financial position and performance of the organization to determine the

possibility of organization expansion and future growth. Government as the stakeholder are

interested on the organization financial statements for the purpose of taxation and regulatory

requirement purpose. The taxes are determined based on the outcome of the operating profit

and other base of tax. In general the government would like to understand the ability of the

entity as the taxpayer to ascertain the tax dues thereon. Hence, financial statement serves as

the important tool in decision making for several stakeholders.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.