ACC00724: Managerial Accounting - Pacific Telemet Ltd Proposals

VerifiedAdded on 2023/04/23

|10

|1339

|197

Report

AI Summary

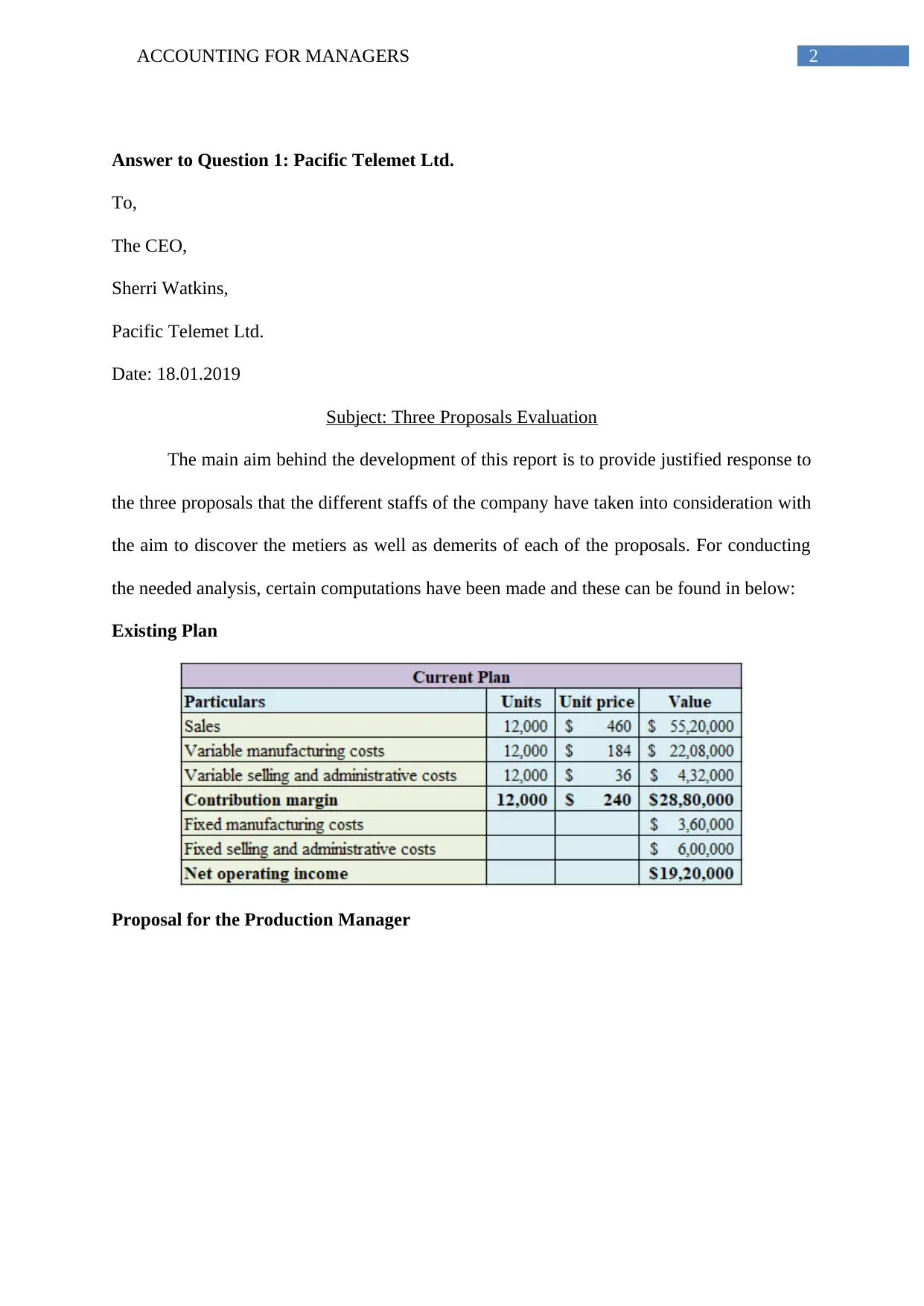

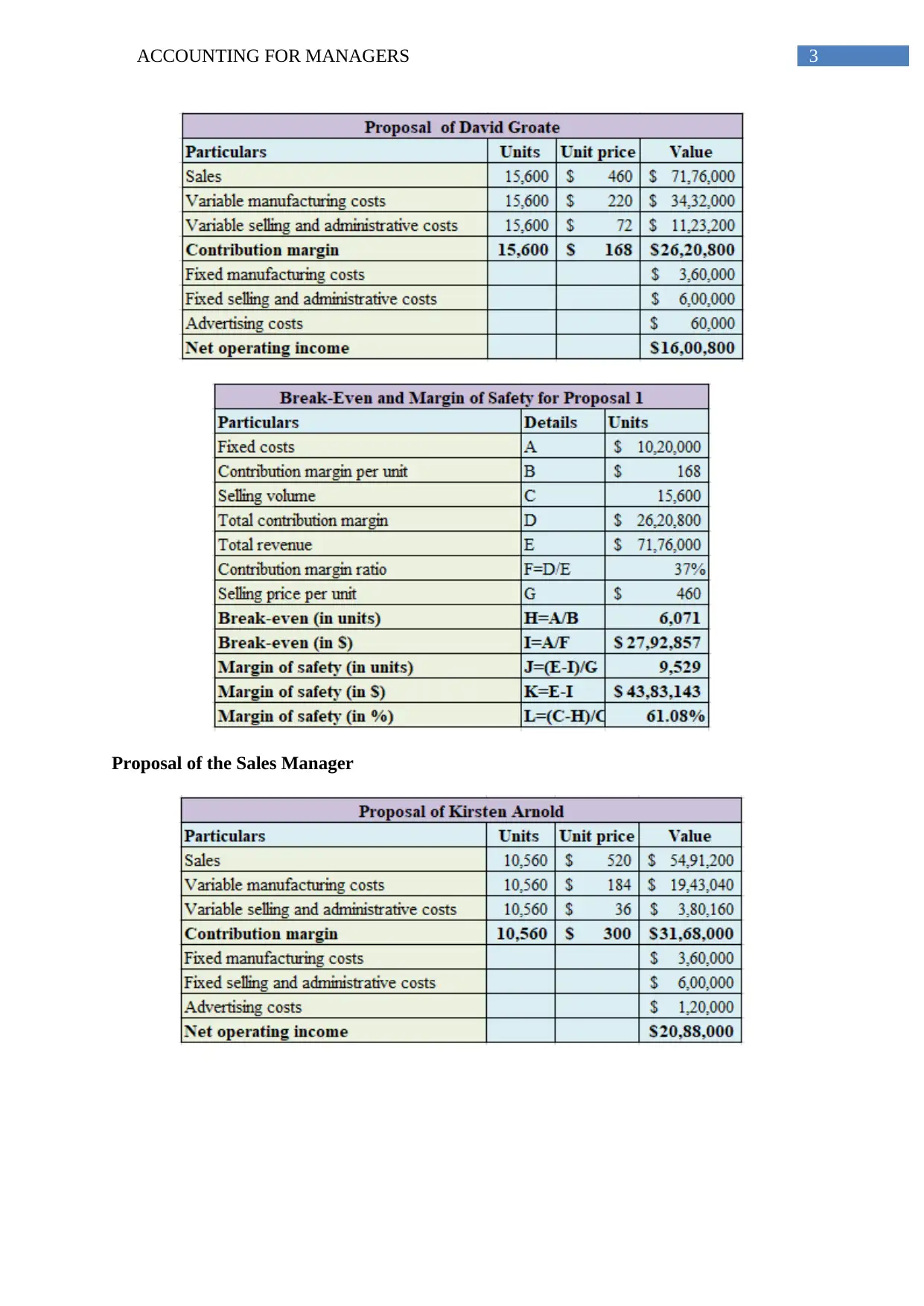

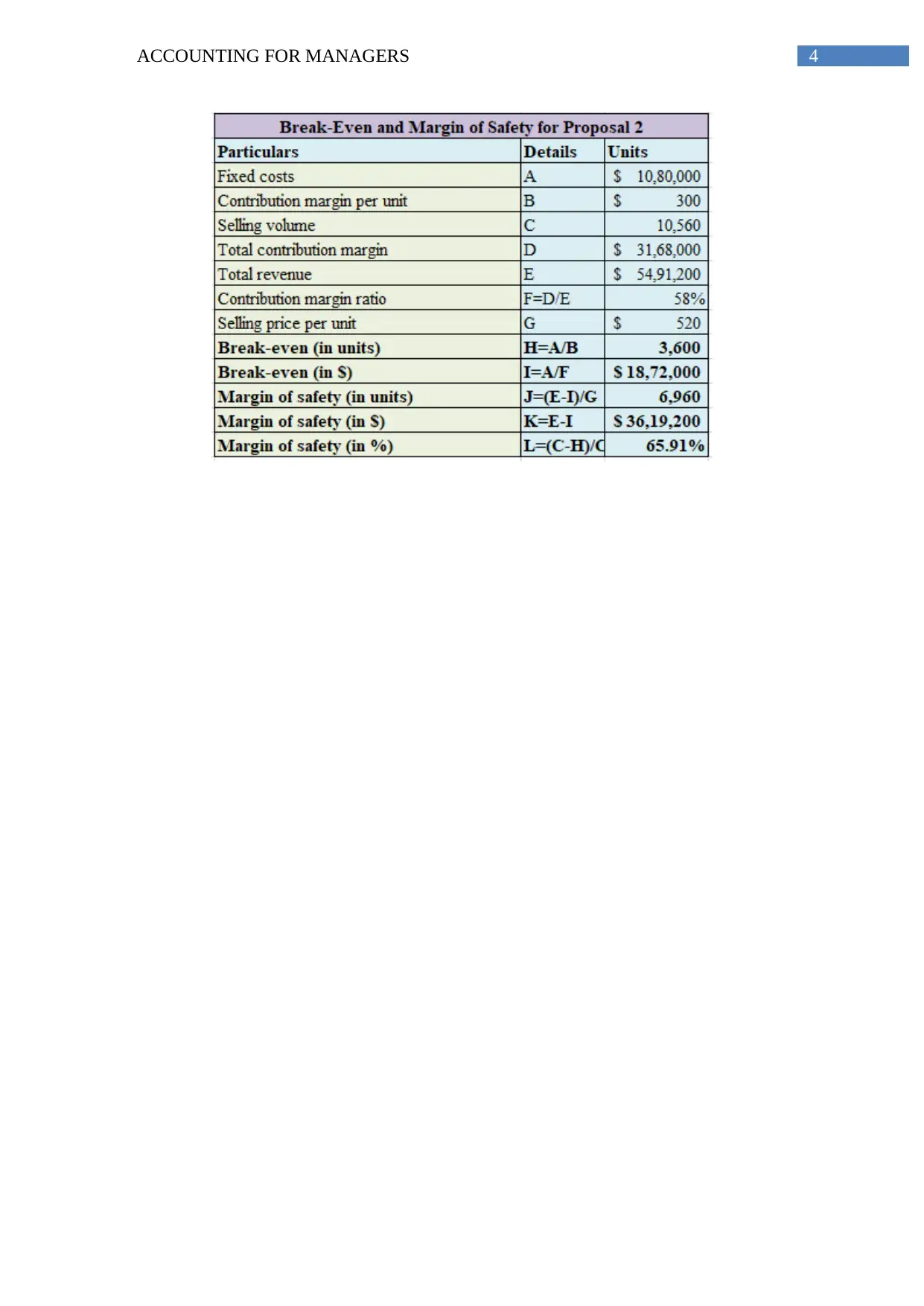

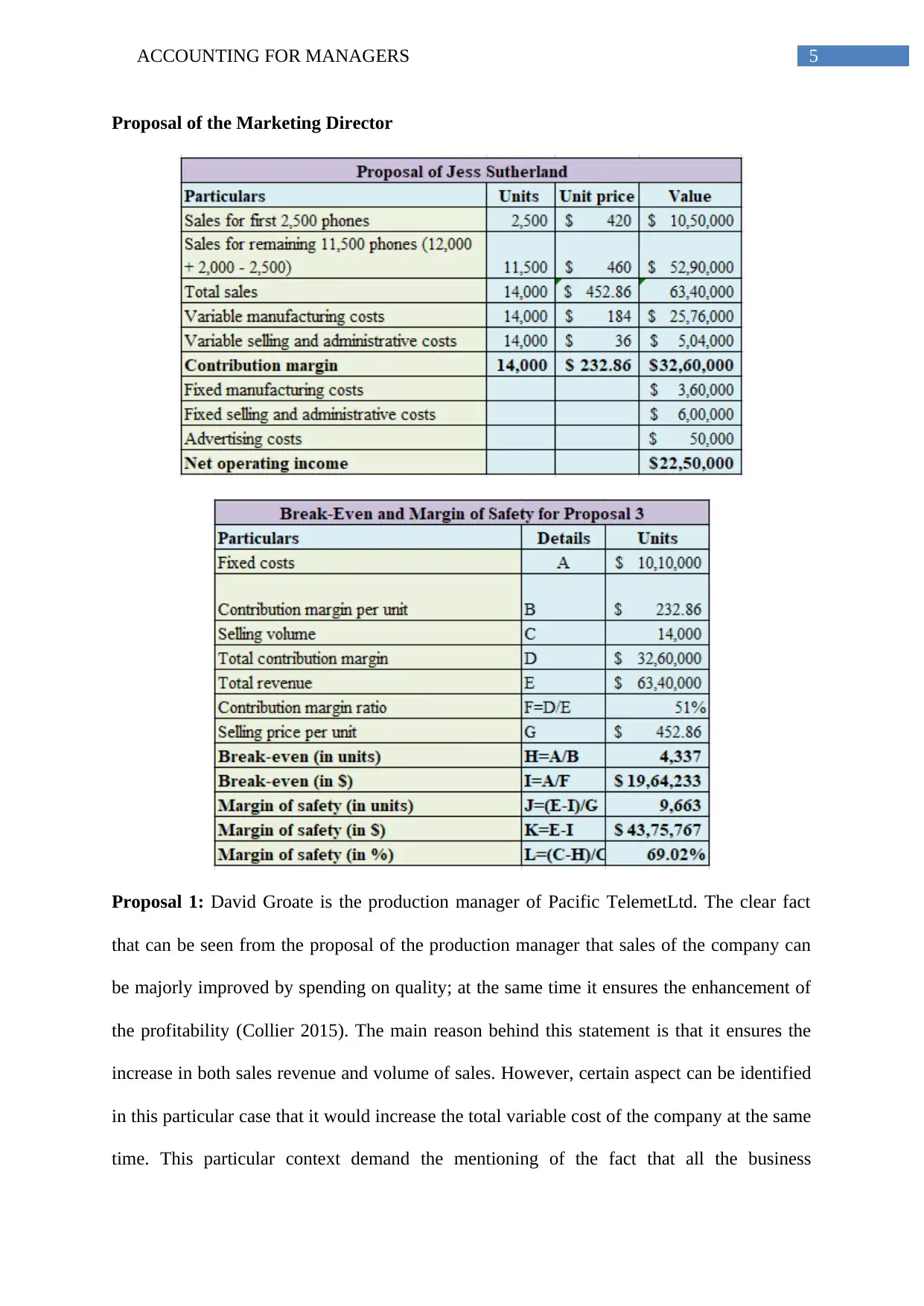

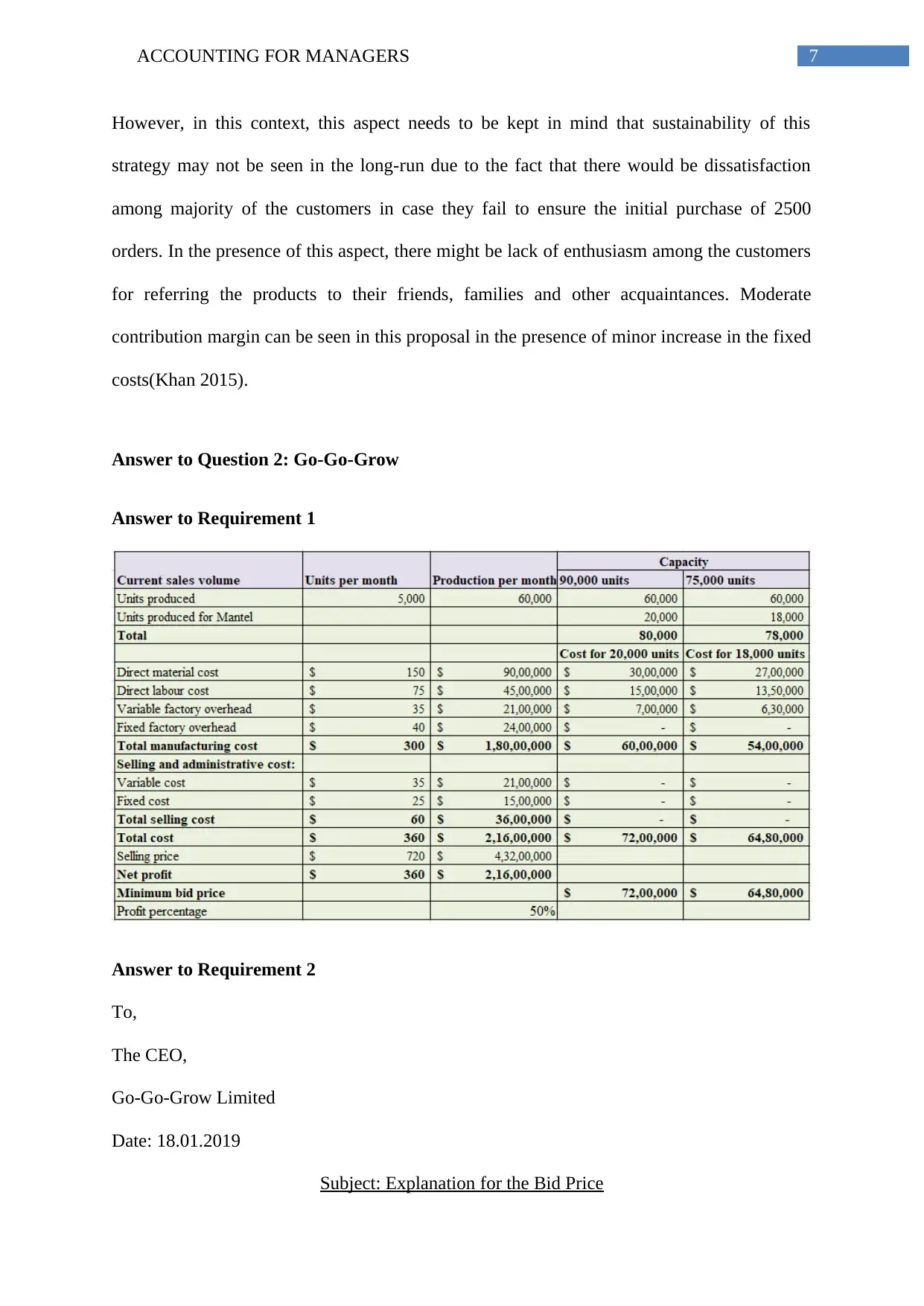

This document presents a student's solution to an accounting for managers assignment, focusing on the evaluation of proposals for Pacific Telemet Ltd. The report analyzes three different proposals from the production manager, sales manager, and marketing director, assessing their potential impact on sales, profitability, and overall business strategy. Additionally, the solution includes an explanation of bid pricing for Go-Go-Grow Limited and a reflection on the student's personal background and how their education has prepared them for a future accounting career. Desklib offers a wide range of study resources, including past papers and solved assignments, to support students in their academic endeavors.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.