Accounting for Managers: Financial Analysis and Recommendations

VerifiedAdded on 2020/05/28

|9

|1507

|86

Report

AI Summary

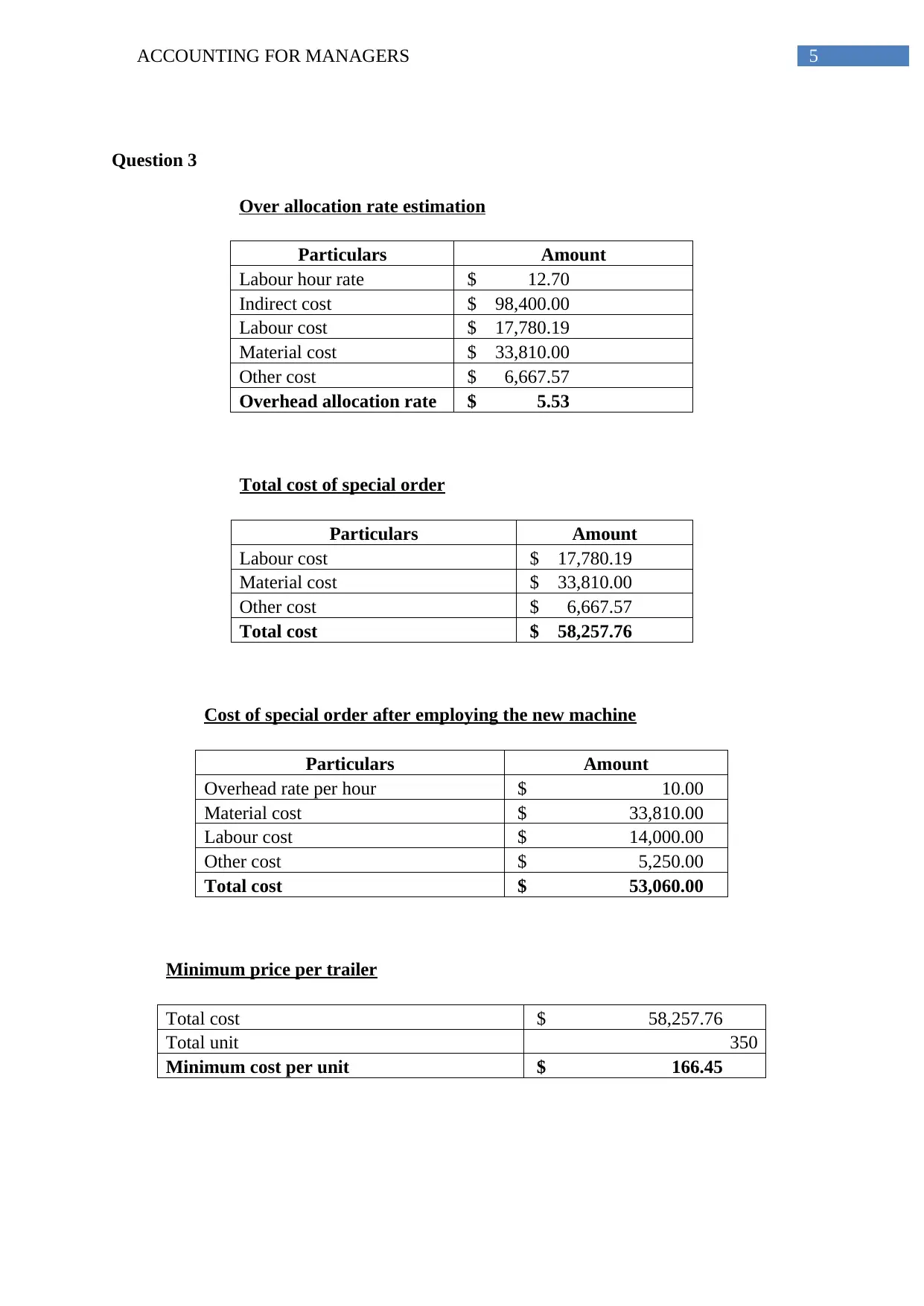

This report provides a comprehensive analysis of accounting for managers, addressing key financial concepts through various scenarios and calculations. The report begins with a comparative analysis of three sales proposals, evaluating their impact on profit margins considering factors like variable and fixed costs, advertising expenses, and potential sales increases. The report then delves into a unit-based cost analysis, comparing different situations to assess profit changes based on sales volume, selling price, and total costs. Furthermore, the report explores overhead allocation, including the estimation of overhead rates, and a detailed cost breakdown of a special order, along with the minimum price per unit. The report concludes with a discussion of overhead allocation methods, the importance of cost segmentation, and the application of Activity-Based Costing (ABC) for effective cost management. It emphasizes the significance of accurate overhead allocation for informed decision-making, profit calculation, and effective business planning.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.