ACC00724 Accounting for Managers: Profitability Enhancement Report

VerifiedAdded on 2023/04/23

|11

|1559

|53

Report

AI Summary

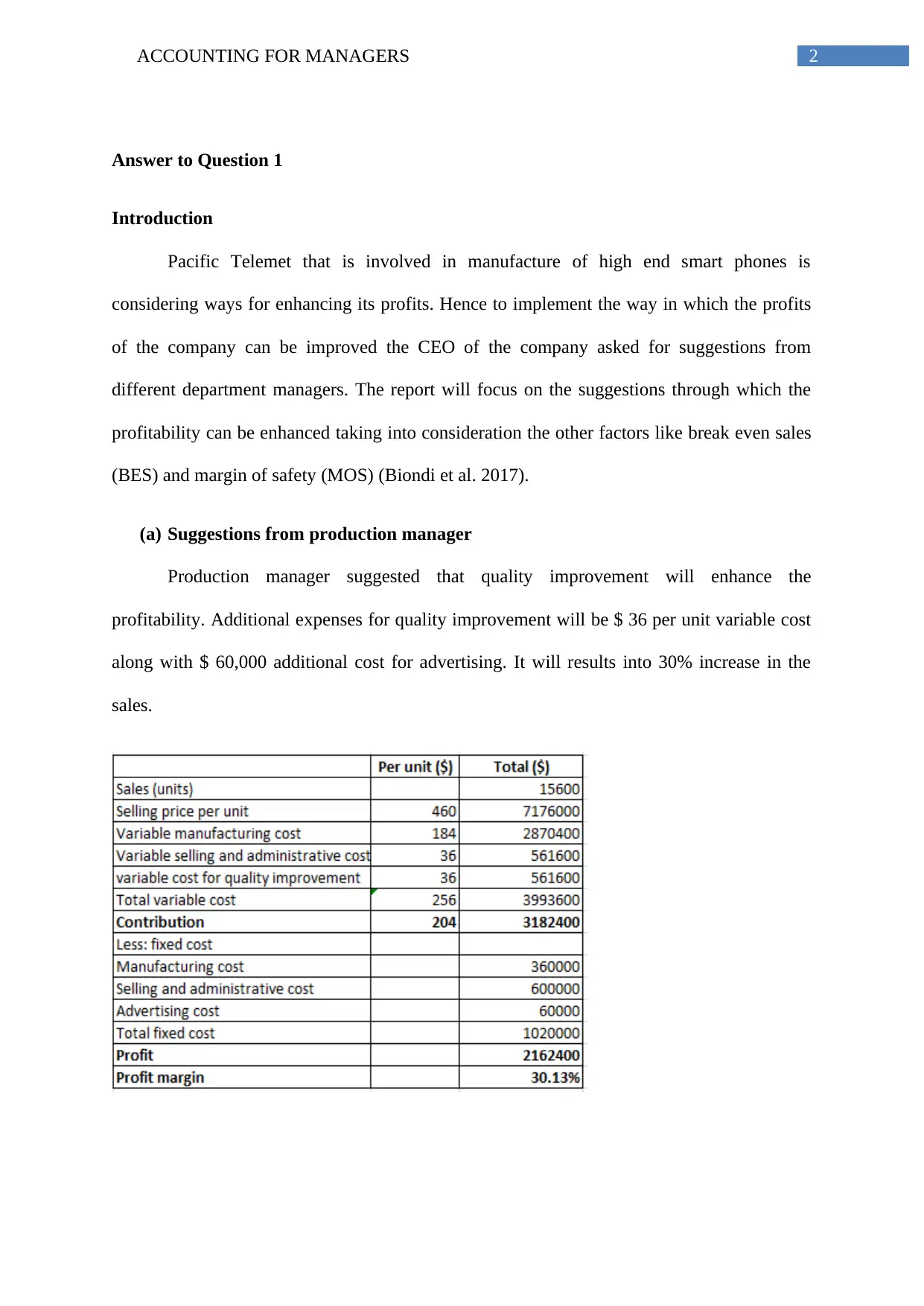

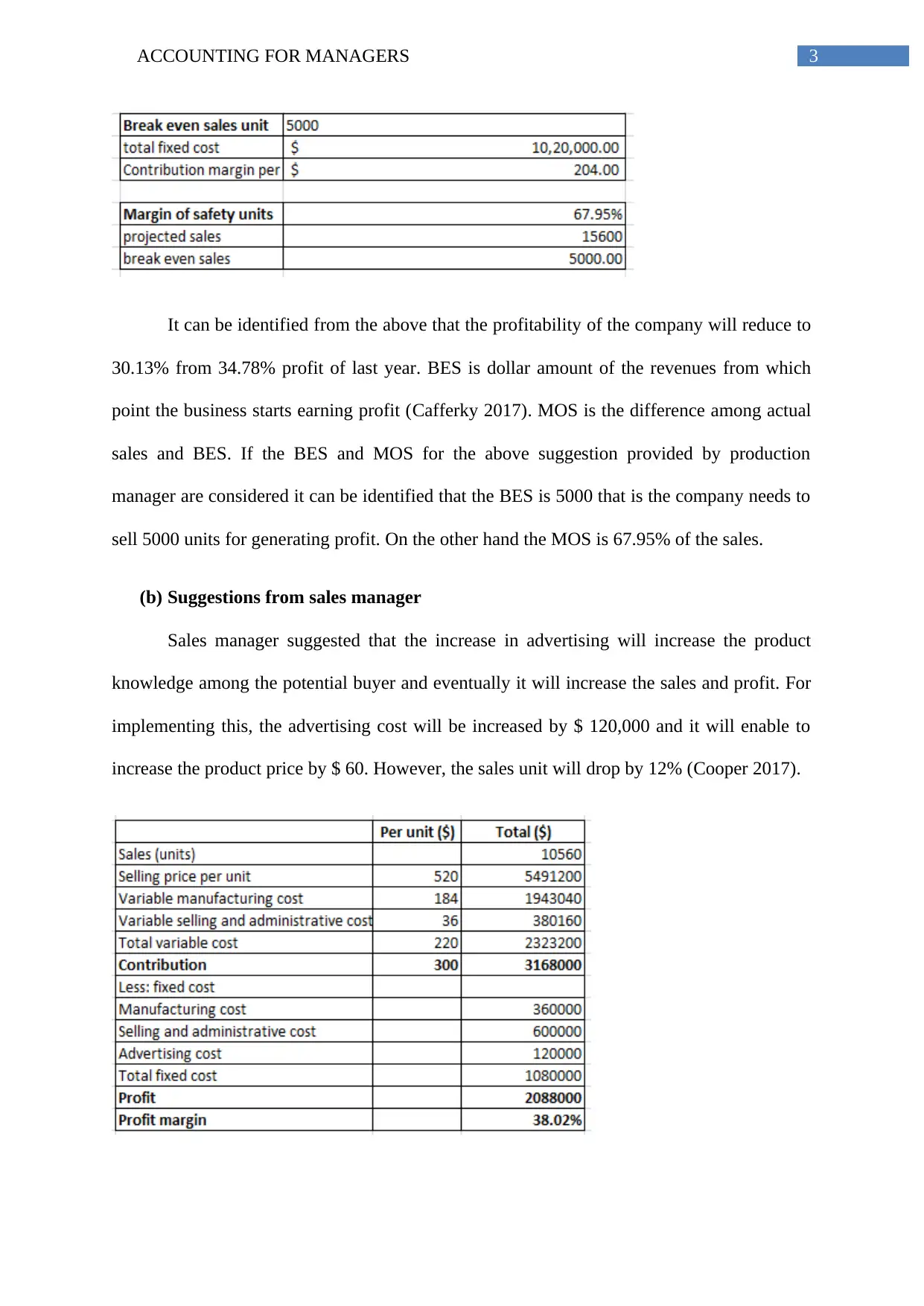

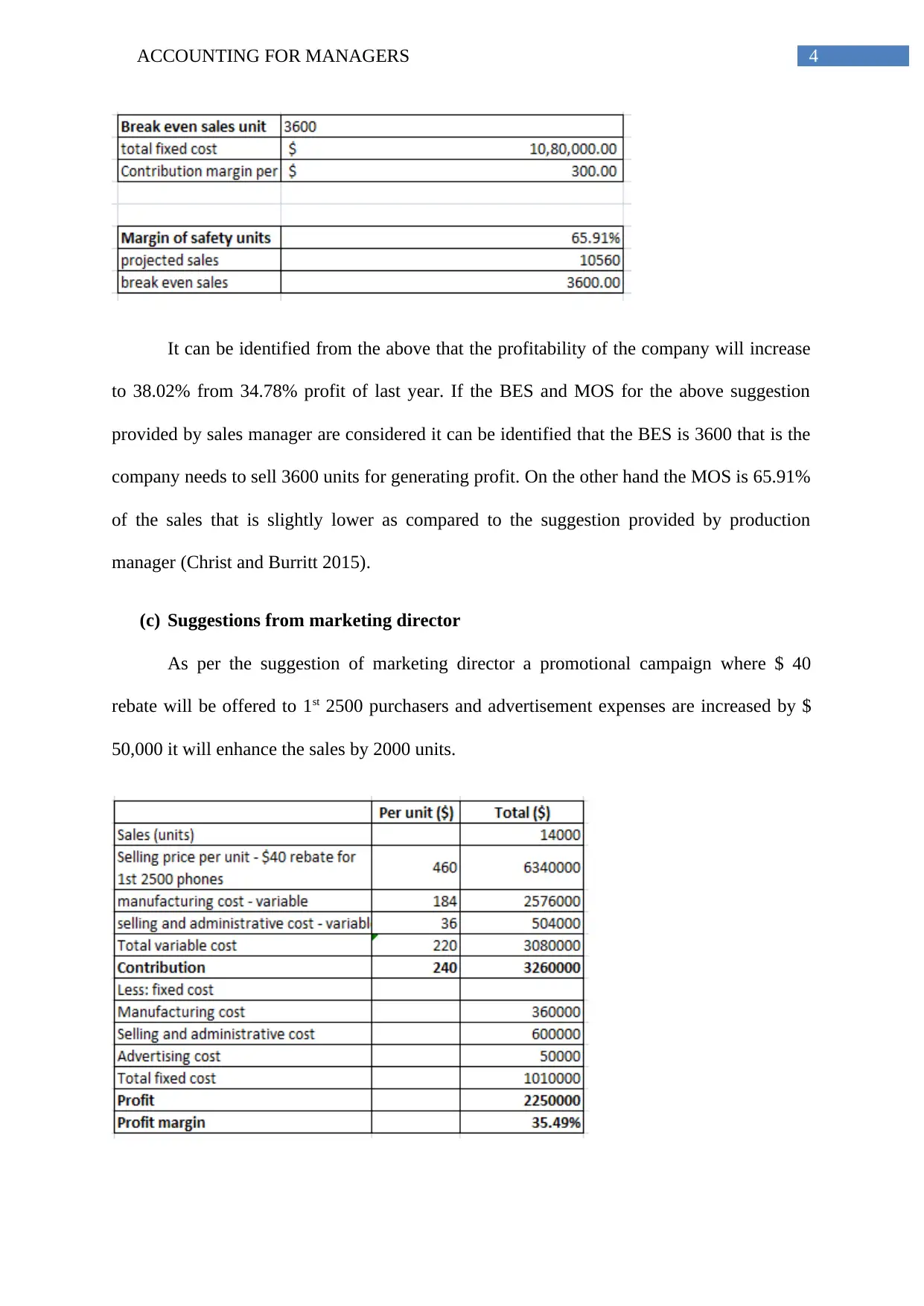

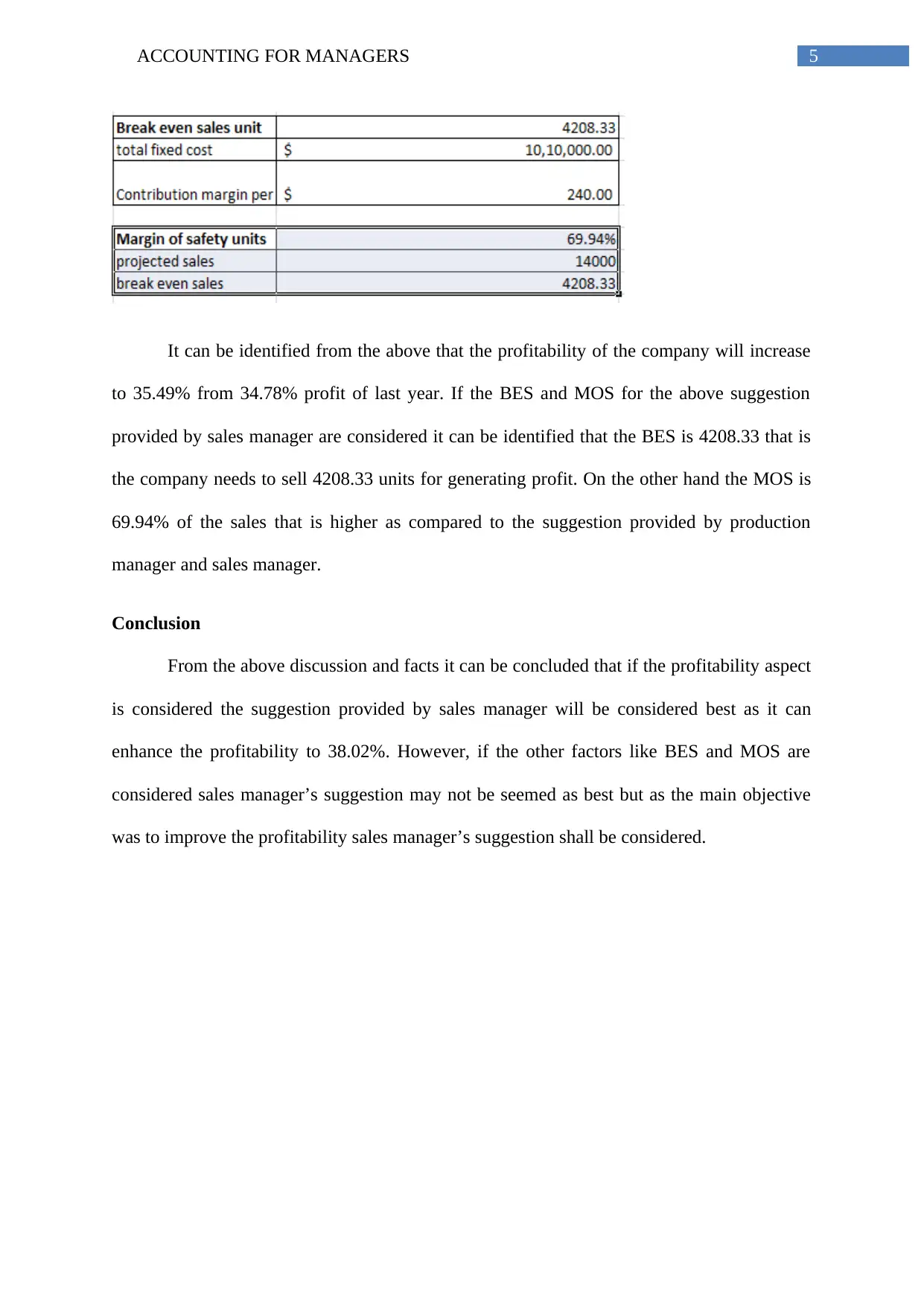

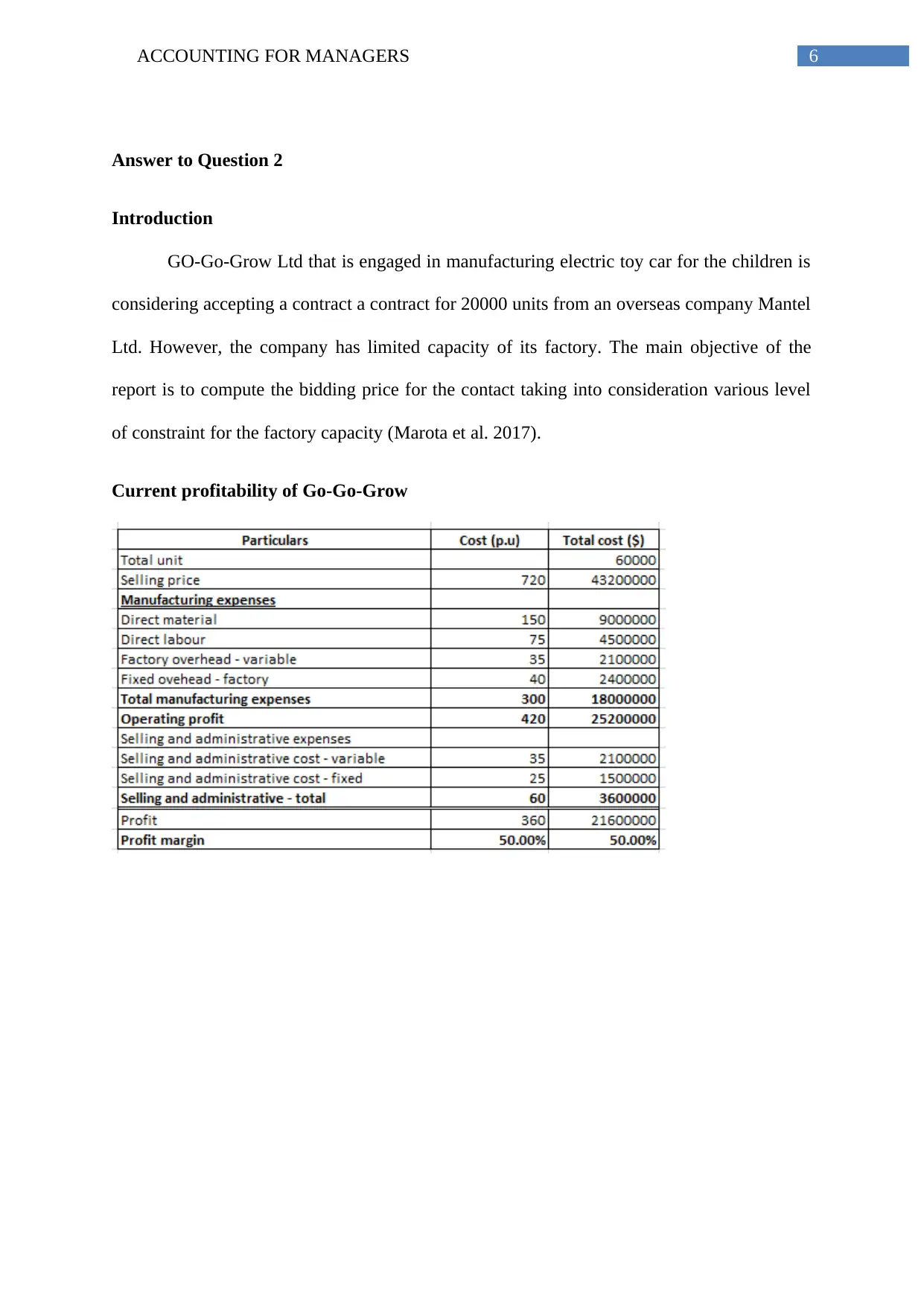

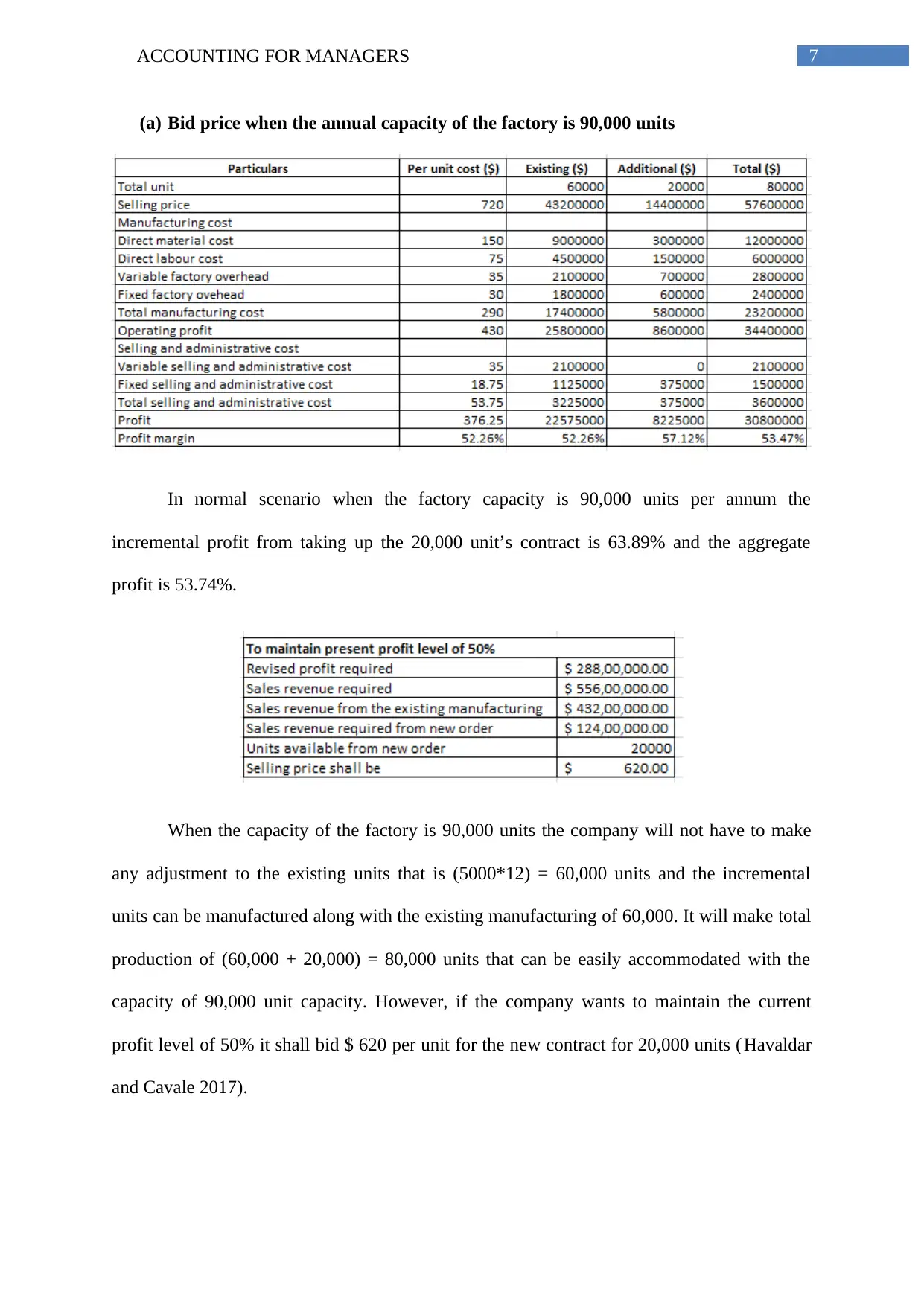

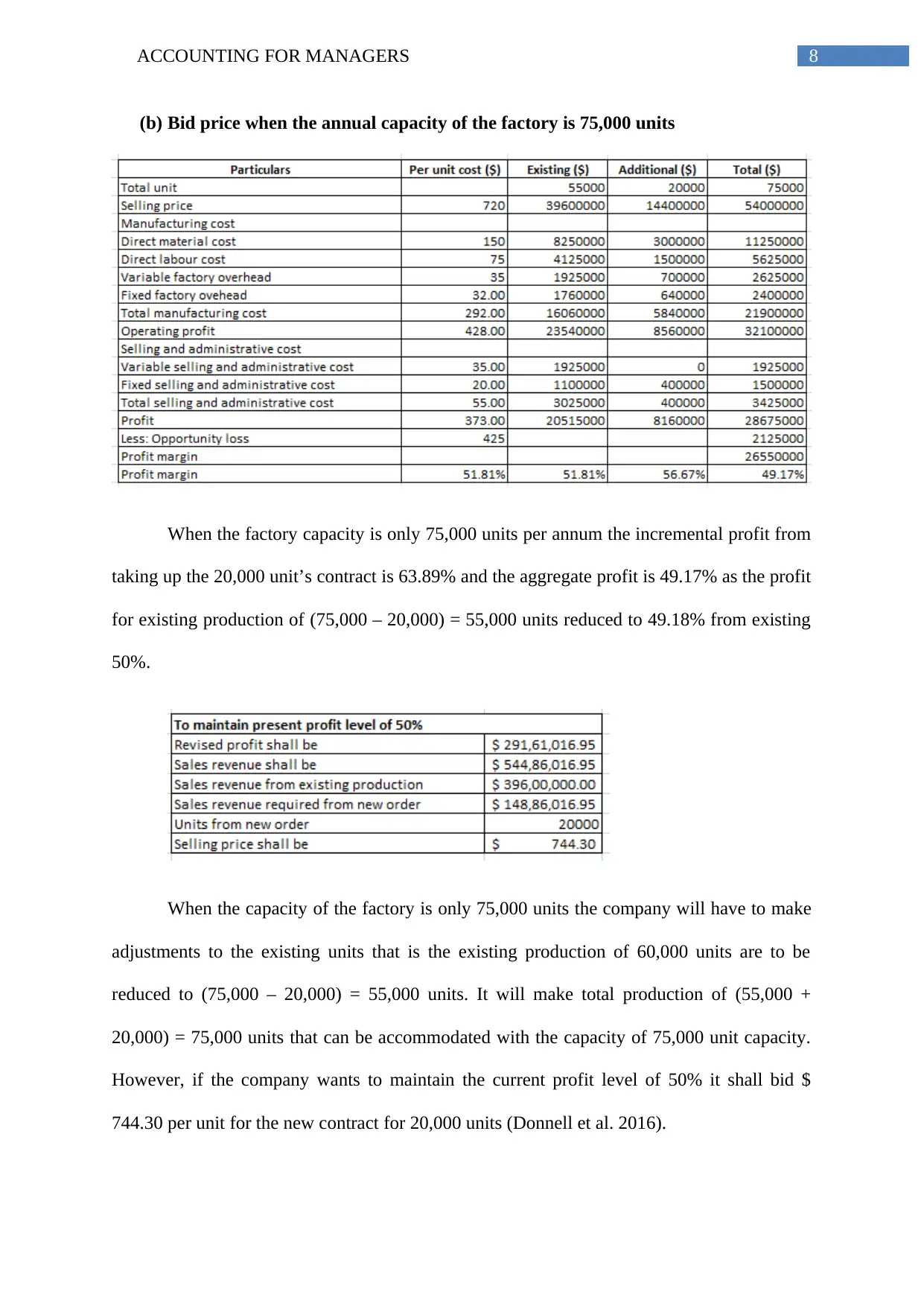

This report evaluates strategies to enhance profitability for Pacific Telemet Ltd., a smartphone manufacturer, based on suggestions from the production, sales, and marketing departments. It analyzes the impact of quality improvements, increased advertising, and promotional campaigns on profitability, break-even sales, and margin of safety. The report concludes that the sales manager's suggestion offers the highest potential profitability. Additionally, the report computes bid prices for Go-Go-Grow Ltd., an electric toy car manufacturer, considering factory capacity constraints, determining the optimal bid price to maintain current profit levels under different production scenarios. Desklib is a platform where students can find similar solved assignments and study resources.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.