Finance Module: Accounting for Managers Report on Proposals

VerifiedAdded on 2020/03/07

|14

|2113

|252

Report

AI Summary

This report, titled "Accounting for Managers," analyzes various financial proposals and cost structures within a company. It begins by evaluating three proposals from senior staff, considering their impact on sales, costs, and profit. The report then delves into detailed cost calculations, including direct materials, labor, and overhead, to determine bid prices for government contracts under different capacity scenarios. Furthermore, it explores the implications of different capacity levels on pricing and profitability. The report also addresses the treatment of costs in a balance sheet and calculates overhead allocation rates and total costs for special orders using both traditional and machine hour rate methods. Finally, it highlights the advantages of segmented overhead cost pools and activity-based costing (ABC) in accurately determining production costs and supporting effective pricing strategies. The report concludes with a bibliography of relevant accounting literature.

Running head: ACCOUNTING FOR MANAGERS

Accounting for Managers

Name of the Student:

Name of the University:

Author’s Note:

Accounting for Managers

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING FOR MANAGERS

Table of Contents

Answer to Question No.1:...............................................................................................................2

Proposal of Accountant:-.............................................................................................................3

Proposal of Production Manager:................................................................................................4

Proposal of Sales Manager:-........................................................................................................5

Answer to Question No.2:-..............................................................................................................6

a) Capacity of 200000 units:-....................................................................................................7

b) Capacity of 180000 units:-................................................................................................8

Answer to Question 3:-....................................................................................................................9

Answer to Question No.4:-............................................................................................................10

a) Calculation of Overhead Allocation Rate:-........................................................................10

b) Calculation of Total Cost for Special Order:-.................................................................10

c) Calculation of Total Cost for Special Order under Machine Hour Rate:-..........................10

d) Calculation of Minimum Price:-.....................................................................................11

e) Advantages of Segmented Overhead Cost Pool & ABC Costing:-....................................11

Bibliography:-................................................................................................................................13

Table of Contents

Answer to Question No.1:...............................................................................................................2

Proposal of Accountant:-.............................................................................................................3

Proposal of Production Manager:................................................................................................4

Proposal of Sales Manager:-........................................................................................................5

Answer to Question No.2:-..............................................................................................................6

a) Capacity of 200000 units:-....................................................................................................7

b) Capacity of 180000 units:-................................................................................................8

Answer to Question 3:-....................................................................................................................9

Answer to Question No.4:-............................................................................................................10

a) Calculation of Overhead Allocation Rate:-........................................................................10

b) Calculation of Total Cost for Special Order:-.................................................................10

c) Calculation of Total Cost for Special Order under Machine Hour Rate:-..........................10

d) Calculation of Minimum Price:-.....................................................................................11

e) Advantages of Segmented Overhead Cost Pool & ABC Costing:-....................................11

Bibliography:-................................................................................................................................13

2ACCOUNTING FOR MANAGERS

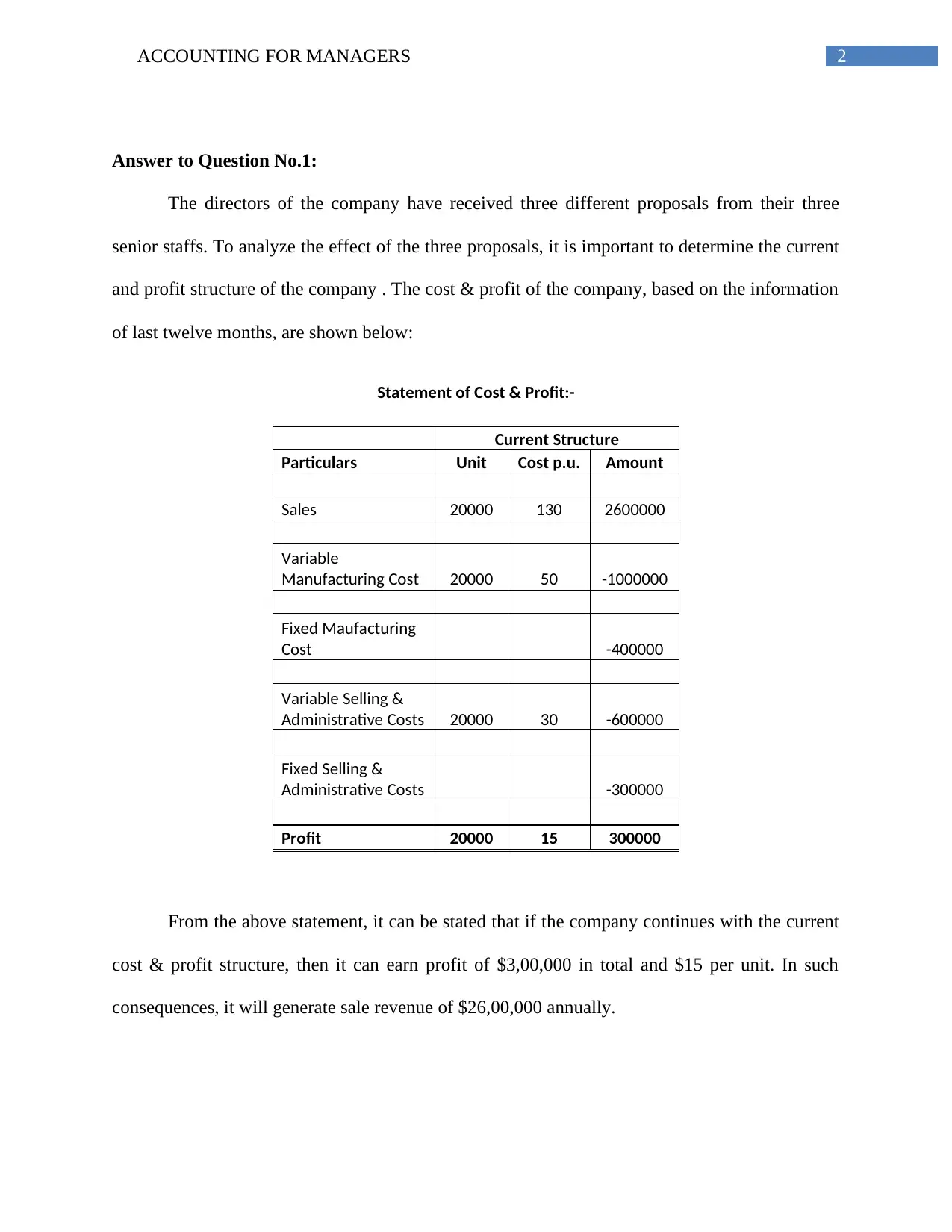

Answer to Question No.1:

The directors of the company have received three different proposals from their three

senior staffs. To analyze the effect of the three proposals, it is important to determine the current

and profit structure of the company . The cost & profit of the company, based on the information

of last twelve months, are shown below:

Statement of Cost & Profit:-

Current Structure

Particulars Unit Cost p.u. Amount

Sales 20000 130 2600000

Variable

Manufacturing Cost 20000 50 -1000000

Fixed Maufacturing

Cost -400000

Variable Selling &

Administrative Costs 20000 30 -600000

Fixed Selling &

Administrative Costs -300000

Profit 20000 15 300000

From the above statement, it can be stated that if the company continues with the current

cost & profit structure, then it can earn profit of $3,00,000 in total and $15 per unit. In such

consequences, it will generate sale revenue of $26,00,000 annually.

Answer to Question No.1:

The directors of the company have received three different proposals from their three

senior staffs. To analyze the effect of the three proposals, it is important to determine the current

and profit structure of the company . The cost & profit of the company, based on the information

of last twelve months, are shown below:

Statement of Cost & Profit:-

Current Structure

Particulars Unit Cost p.u. Amount

Sales 20000 130 2600000

Variable

Manufacturing Cost 20000 50 -1000000

Fixed Maufacturing

Cost -400000

Variable Selling &

Administrative Costs 20000 30 -600000

Fixed Selling &

Administrative Costs -300000

Profit 20000 15 300000

From the above statement, it can be stated that if the company continues with the current

cost & profit structure, then it can earn profit of $3,00,000 in total and $15 per unit. In such

consequences, it will generate sale revenue of $26,00,000 annually.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING FOR MANAGERS

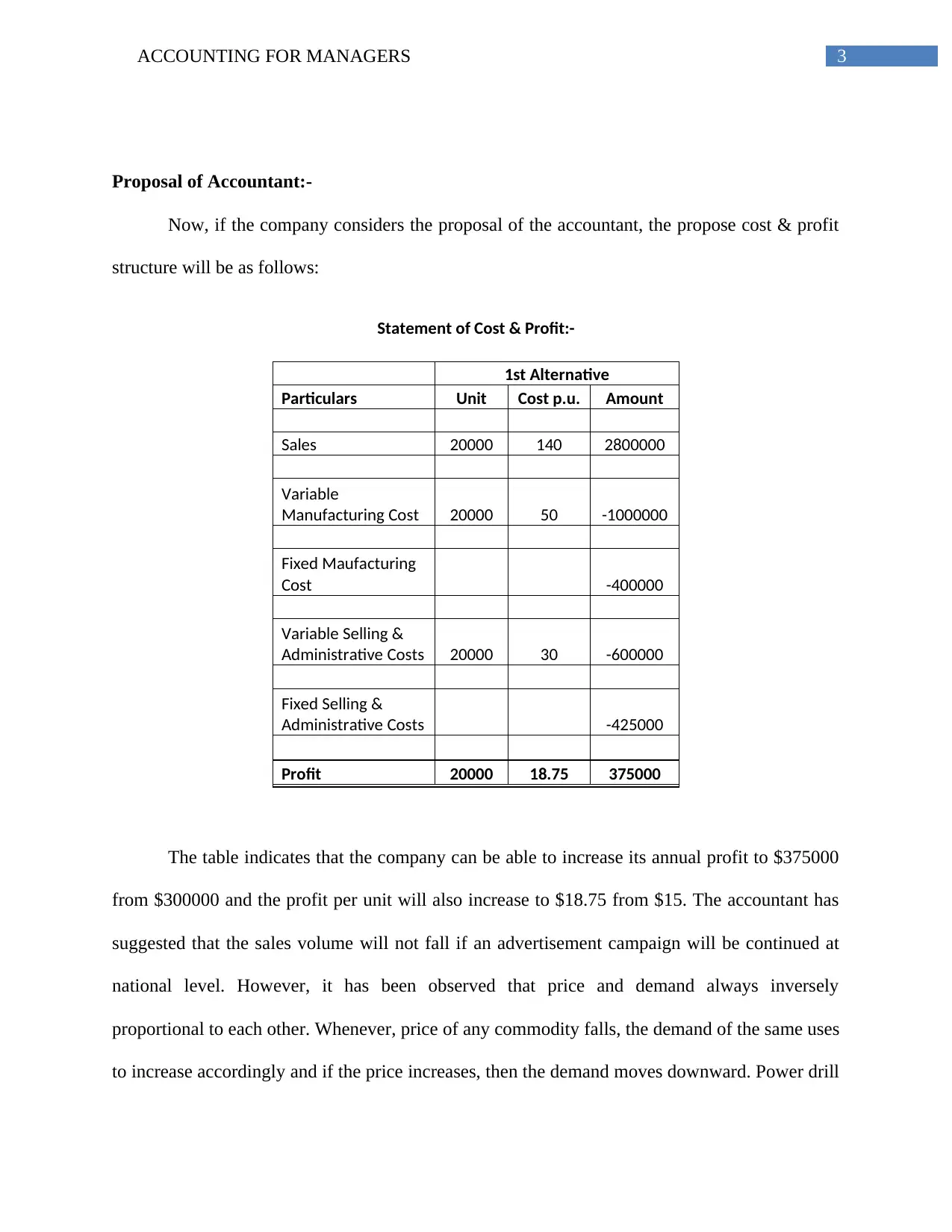

Proposal of Accountant:-

Now, if the company considers the proposal of the accountant, the propose cost & profit

structure will be as follows:

Statement of Cost & Profit:-

1st Alternative

Particulars Unit Cost p.u. Amount

Sales 20000 140 2800000

Variable

Manufacturing Cost 20000 50 -1000000

Fixed Maufacturing

Cost -400000

Variable Selling &

Administrative Costs 20000 30 -600000

Fixed Selling &

Administrative Costs -425000

Profit 20000 18.75 375000

The table indicates that the company can be able to increase its annual profit to $375000

from $300000 and the profit per unit will also increase to $18.75 from $15. The accountant has

suggested that the sales volume will not fall if an advertisement campaign will be continued at

national level. However, it has been observed that price and demand always inversely

proportional to each other. Whenever, price of any commodity falls, the demand of the same uses

to increase accordingly and if the price increases, then the demand moves downward. Power drill

Proposal of Accountant:-

Now, if the company considers the proposal of the accountant, the propose cost & profit

structure will be as follows:

Statement of Cost & Profit:-

1st Alternative

Particulars Unit Cost p.u. Amount

Sales 20000 140 2800000

Variable

Manufacturing Cost 20000 50 -1000000

Fixed Maufacturing

Cost -400000

Variable Selling &

Administrative Costs 20000 30 -600000

Fixed Selling &

Administrative Costs -425000

Profit 20000 18.75 375000

The table indicates that the company can be able to increase its annual profit to $375000

from $300000 and the profit per unit will also increase to $18.75 from $15. The accountant has

suggested that the sales volume will not fall if an advertisement campaign will be continued at

national level. However, it has been observed that price and demand always inversely

proportional to each other. Whenever, price of any commodity falls, the demand of the same uses

to increase accordingly and if the price increases, then the demand moves downward. Power drill

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING FOR MANAGERS

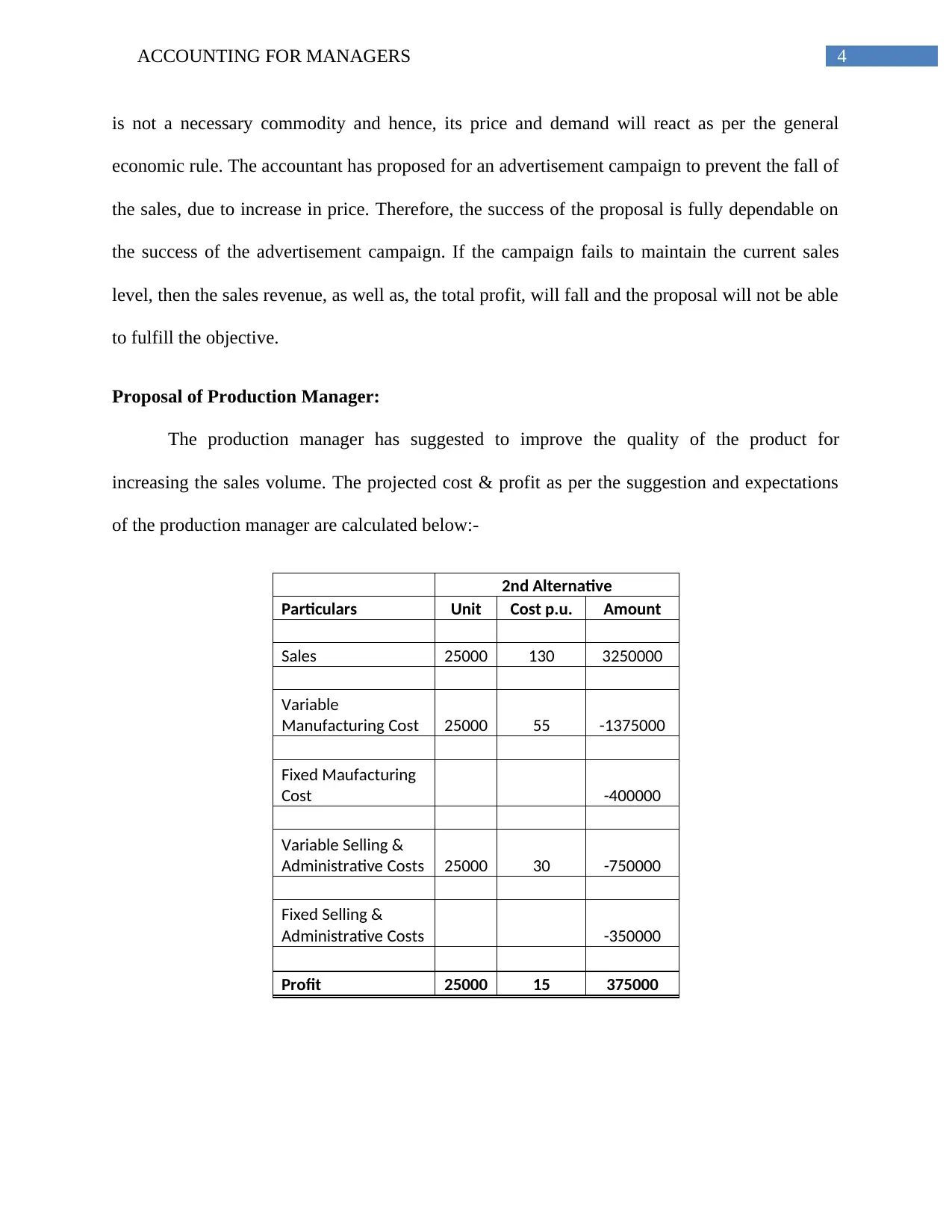

is not a necessary commodity and hence, its price and demand will react as per the general

economic rule. The accountant has proposed for an advertisement campaign to prevent the fall of

the sales, due to increase in price. Therefore, the success of the proposal is fully dependable on

the success of the advertisement campaign. If the campaign fails to maintain the current sales

level, then the sales revenue, as well as, the total profit, will fall and the proposal will not be able

to fulfill the objective.

Proposal of Production Manager:

The production manager has suggested to improve the quality of the product for

increasing the sales volume. The projected cost & profit as per the suggestion and expectations

of the production manager are calculated below:-

2nd Alternative

Particulars Unit Cost p.u. Amount

Sales 25000 130 3250000

Variable

Manufacturing Cost 25000 55 -1375000

Fixed Maufacturing

Cost -400000

Variable Selling &

Administrative Costs 25000 30 -750000

Fixed Selling &

Administrative Costs -350000

Profit 25000 15 375000

is not a necessary commodity and hence, its price and demand will react as per the general

economic rule. The accountant has proposed for an advertisement campaign to prevent the fall of

the sales, due to increase in price. Therefore, the success of the proposal is fully dependable on

the success of the advertisement campaign. If the campaign fails to maintain the current sales

level, then the sales revenue, as well as, the total profit, will fall and the proposal will not be able

to fulfill the objective.

Proposal of Production Manager:

The production manager has suggested to improve the quality of the product for

increasing the sales volume. The projected cost & profit as per the suggestion and expectations

of the production manager are calculated below:-

2nd Alternative

Particulars Unit Cost p.u. Amount

Sales 25000 130 3250000

Variable

Manufacturing Cost 25000 55 -1375000

Fixed Maufacturing

Cost -400000

Variable Selling &

Administrative Costs 25000 30 -750000

Fixed Selling &

Administrative Costs -350000

Profit 25000 15 375000

5ACCOUNTING FOR MANAGERS

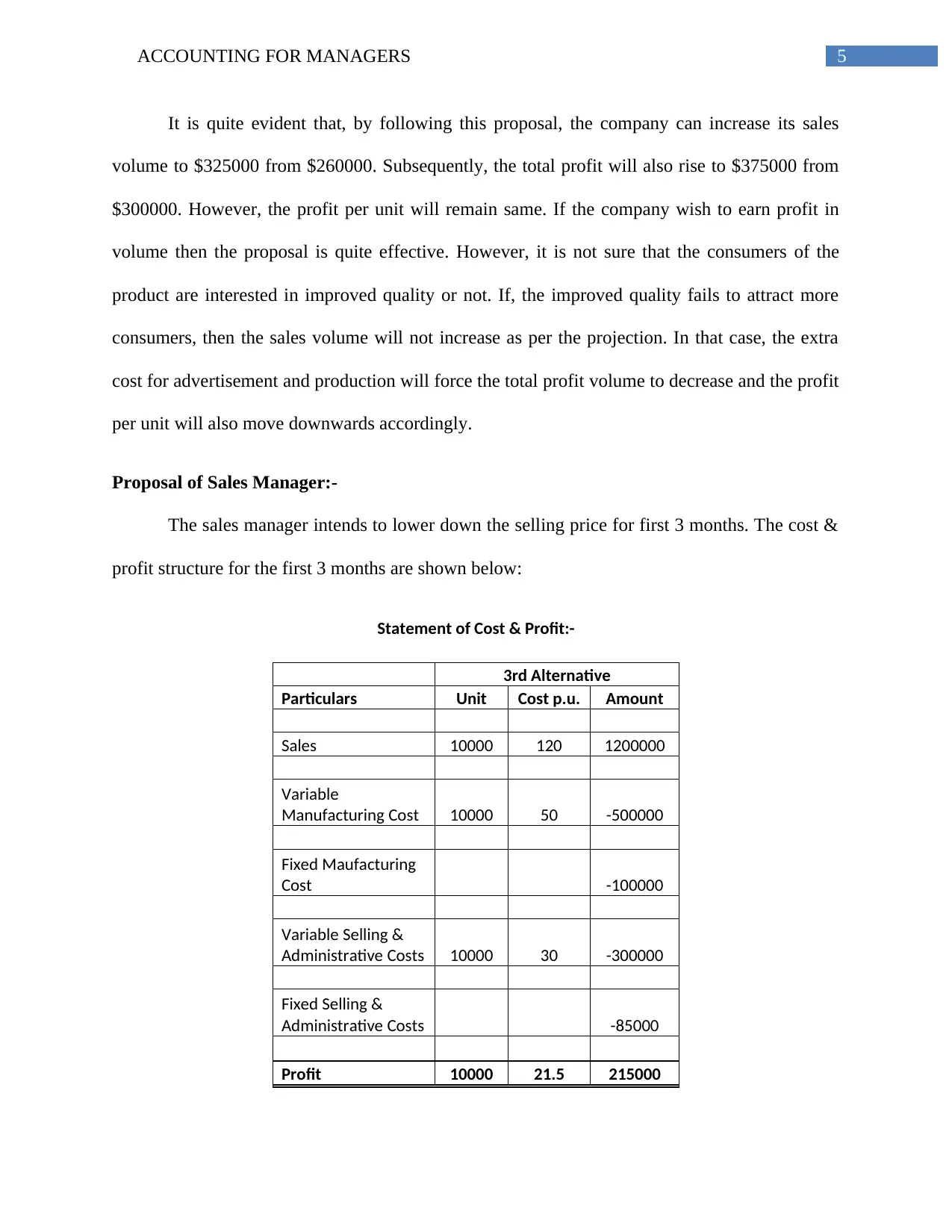

It is quite evident that, by following this proposal, the company can increase its sales

volume to $325000 from $260000. Subsequently, the total profit will also rise to $375000 from

$300000. However, the profit per unit will remain same. If the company wish to earn profit in

volume then the proposal is quite effective. However, it is not sure that the consumers of the

product are interested in improved quality or not. If, the improved quality fails to attract more

consumers, then the sales volume will not increase as per the projection. In that case, the extra

cost for advertisement and production will force the total profit volume to decrease and the profit

per unit will also move downwards accordingly.

Proposal of Sales Manager:-

The sales manager intends to lower down the selling price for first 3 months. The cost &

profit structure for the first 3 months are shown below:

Statement of Cost & Profit:-

3rd Alternative

Particulars Unit Cost p.u. Amount

Sales 10000 120 1200000

Variable

Manufacturing Cost 10000 50 -500000

Fixed Maufacturing

Cost -100000

Variable Selling &

Administrative Costs 10000 30 -300000

Fixed Selling &

Administrative Costs -85000

Profit 10000 21.5 215000

It is quite evident that, by following this proposal, the company can increase its sales

volume to $325000 from $260000. Subsequently, the total profit will also rise to $375000 from

$300000. However, the profit per unit will remain same. If the company wish to earn profit in

volume then the proposal is quite effective. However, it is not sure that the consumers of the

product are interested in improved quality or not. If, the improved quality fails to attract more

consumers, then the sales volume will not increase as per the projection. In that case, the extra

cost for advertisement and production will force the total profit volume to decrease and the profit

per unit will also move downwards accordingly.

Proposal of Sales Manager:-

The sales manager intends to lower down the selling price for first 3 months. The cost &

profit structure for the first 3 months are shown below:

Statement of Cost & Profit:-

3rd Alternative

Particulars Unit Cost p.u. Amount

Sales 10000 120 1200000

Variable

Manufacturing Cost 10000 50 -500000

Fixed Maufacturing

Cost -100000

Variable Selling &

Administrative Costs 10000 30 -300000

Fixed Selling &

Administrative Costs -85000

Profit 10000 21.5 215000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING FOR MANAGERS

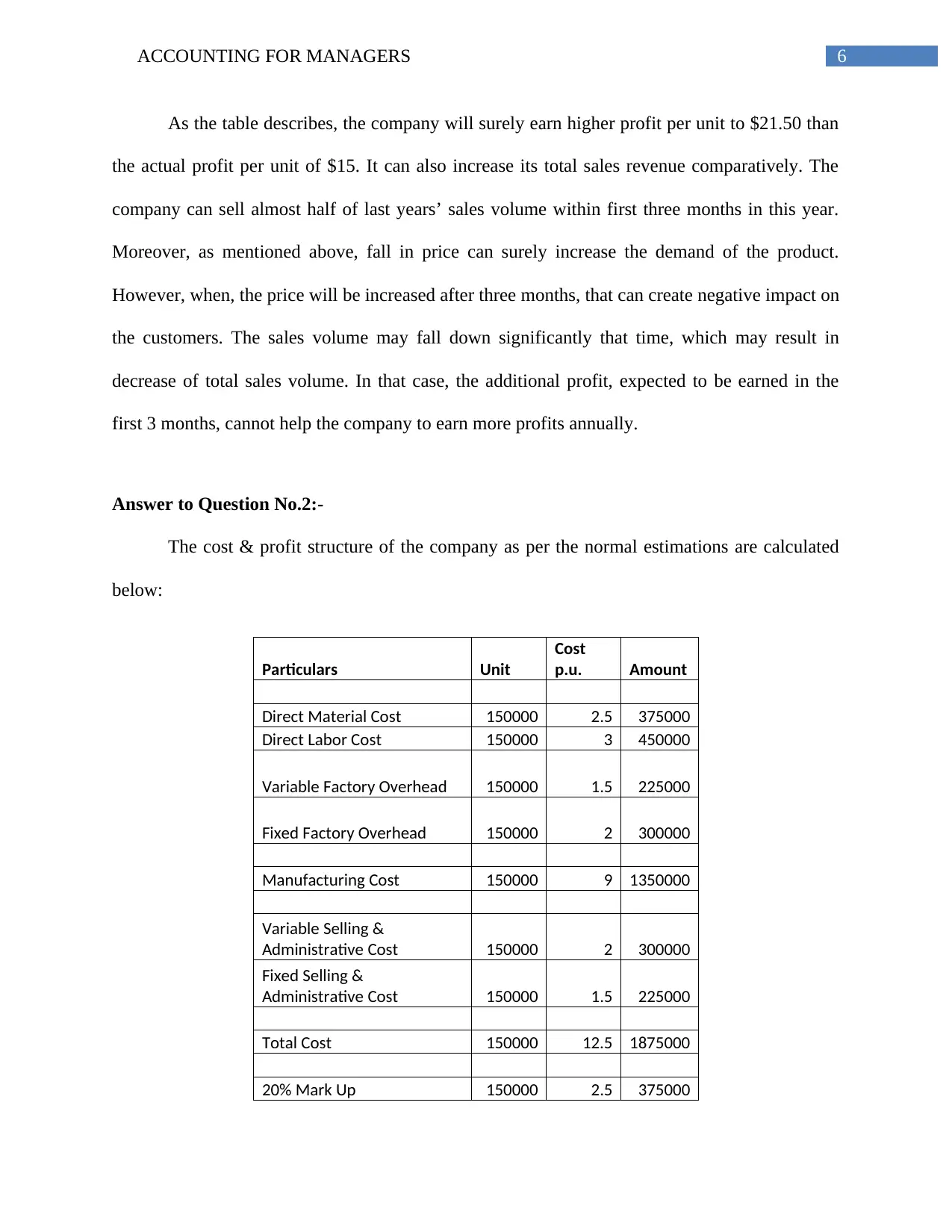

As the table describes, the company will surely earn higher profit per unit to $21.50 than

the actual profit per unit of $15. It can also increase its total sales revenue comparatively. The

company can sell almost half of last years’ sales volume within first three months in this year.

Moreover, as mentioned above, fall in price can surely increase the demand of the product.

However, when, the price will be increased after three months, that can create negative impact on

the customers. The sales volume may fall down significantly that time, which may result in

decrease of total sales volume. In that case, the additional profit, expected to be earned in the

first 3 months, cannot help the company to earn more profits annually.

Answer to Question No.2:-

The cost & profit structure of the company as per the normal estimations are calculated

below:

Particulars Unit

Cost

p.u. Amount

Direct Material Cost 150000 2.5 375000

Direct Labor Cost 150000 3 450000

Variable Factory Overhead 150000 1.5 225000

Fixed Factory Overhead 150000 2 300000

Manufacturing Cost 150000 9 1350000

Variable Selling &

Administrative Cost 150000 2 300000

Fixed Selling &

Administrative Cost 150000 1.5 225000

Total Cost 150000 12.5 1875000

20% Mark Up 150000 2.5 375000

As the table describes, the company will surely earn higher profit per unit to $21.50 than

the actual profit per unit of $15. It can also increase its total sales revenue comparatively. The

company can sell almost half of last years’ sales volume within first three months in this year.

Moreover, as mentioned above, fall in price can surely increase the demand of the product.

However, when, the price will be increased after three months, that can create negative impact on

the customers. The sales volume may fall down significantly that time, which may result in

decrease of total sales volume. In that case, the additional profit, expected to be earned in the

first 3 months, cannot help the company to earn more profits annually.

Answer to Question No.2:-

The cost & profit structure of the company as per the normal estimations are calculated

below:

Particulars Unit

Cost

p.u. Amount

Direct Material Cost 150000 2.5 375000

Direct Labor Cost 150000 3 450000

Variable Factory Overhead 150000 1.5 225000

Fixed Factory Overhead 150000 2 300000

Manufacturing Cost 150000 9 1350000

Variable Selling &

Administrative Cost 150000 2 300000

Fixed Selling &

Administrative Cost 150000 1.5 225000

Total Cost 150000 12.5 1875000

20% Mark Up 150000 2.5 375000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING FOR MANAGERS

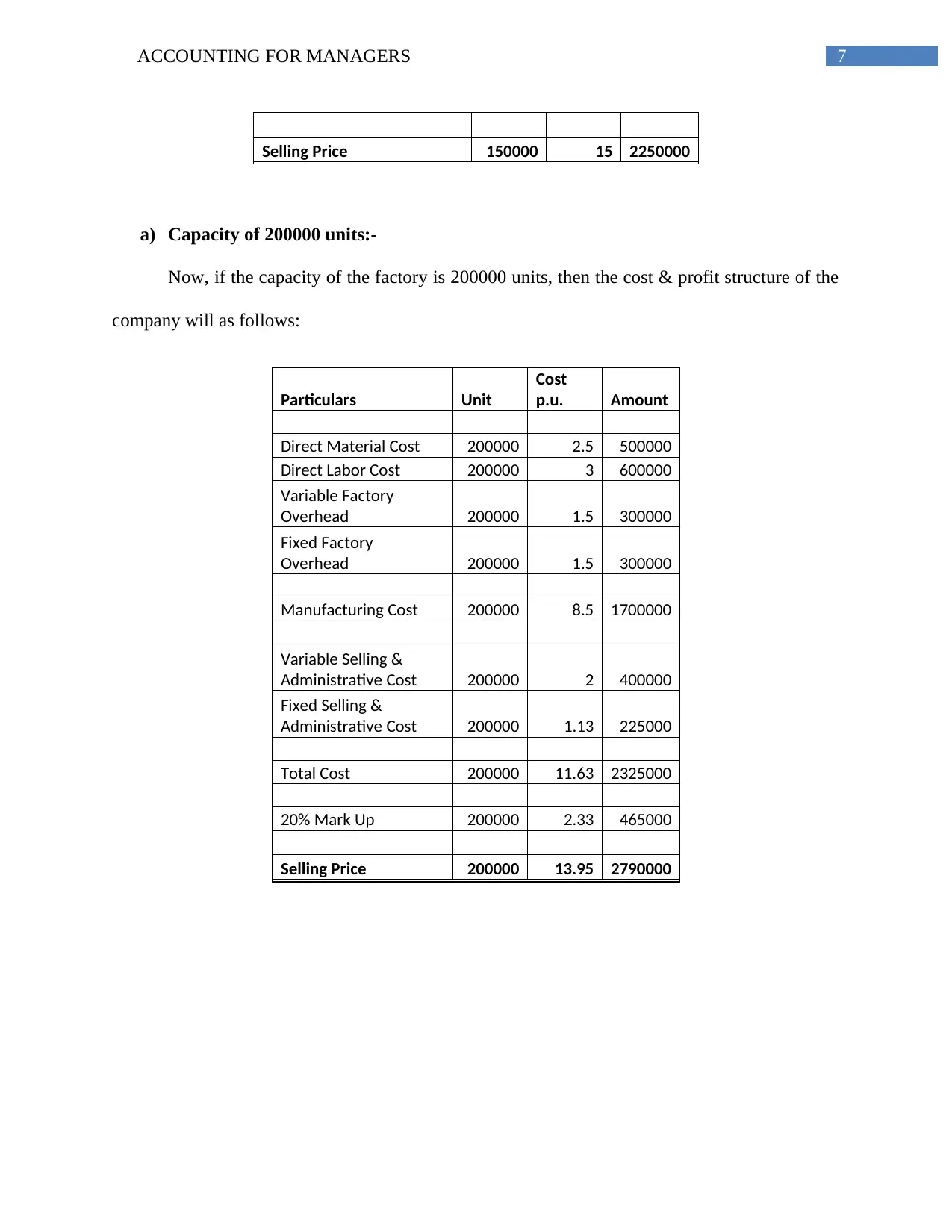

Selling Price 150000 15 2250000

a) Capacity of 200000 units:-

Now, if the capacity of the factory is 200000 units, then the cost & profit structure of the

company will as follows:

Particulars Unit

Cost

p.u. Amount

Direct Material Cost 200000 2.5 500000

Direct Labor Cost 200000 3 600000

Variable Factory

Overhead 200000 1.5 300000

Fixed Factory

Overhead 200000 1.5 300000

Manufacturing Cost 200000 8.5 1700000

Variable Selling &

Administrative Cost 200000 2 400000

Fixed Selling &

Administrative Cost 200000 1.13 225000

Total Cost 200000 11.63 2325000

20% Mark Up 200000 2.33 465000

Selling Price 200000 13.95 2790000

Selling Price 150000 15 2250000

a) Capacity of 200000 units:-

Now, if the capacity of the factory is 200000 units, then the cost & profit structure of the

company will as follows:

Particulars Unit

Cost

p.u. Amount

Direct Material Cost 200000 2.5 500000

Direct Labor Cost 200000 3 600000

Variable Factory

Overhead 200000 1.5 300000

Fixed Factory

Overhead 200000 1.5 300000

Manufacturing Cost 200000 8.5 1700000

Variable Selling &

Administrative Cost 200000 2 400000

Fixed Selling &

Administrative Cost 200000 1.13 225000

Total Cost 200000 11.63 2325000

20% Mark Up 200000 2.33 465000

Selling Price 200000 13.95 2790000

8ACCOUNTING FOR MANAGERS

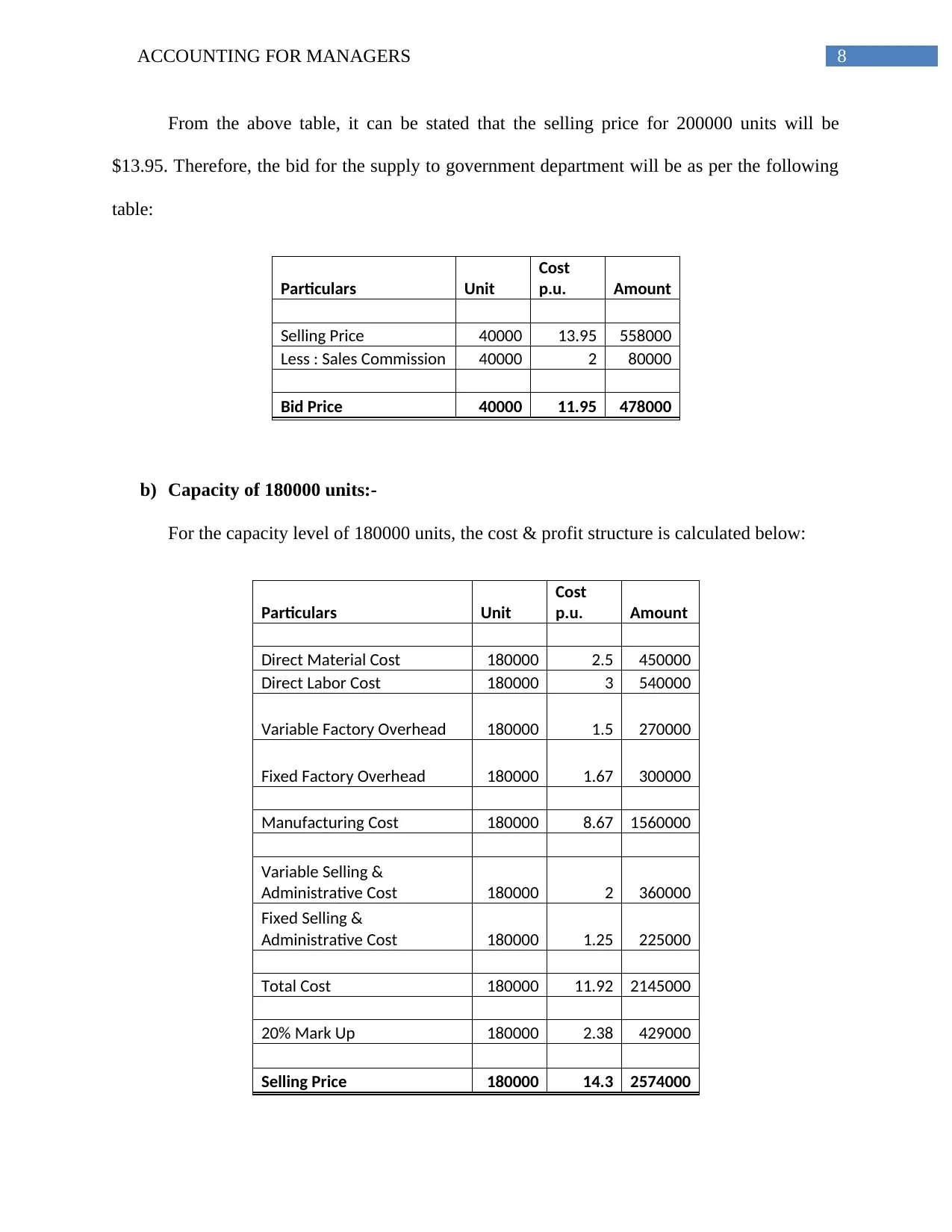

From the above table, it can be stated that the selling price for 200000 units will be

$13.95. Therefore, the bid for the supply to government department will be as per the following

table:

Particulars Unit

Cost

p.u. Amount

Selling Price 40000 13.95 558000

Less : Sales Commission 40000 2 80000

Bid Price 40000 11.95 478000

b) Capacity of 180000 units:-

For the capacity level of 180000 units, the cost & profit structure is calculated below:

Particulars Unit

Cost

p.u. Amount

Direct Material Cost 180000 2.5 450000

Direct Labor Cost 180000 3 540000

Variable Factory Overhead 180000 1.5 270000

Fixed Factory Overhead 180000 1.67 300000

Manufacturing Cost 180000 8.67 1560000

Variable Selling &

Administrative Cost 180000 2 360000

Fixed Selling &

Administrative Cost 180000 1.25 225000

Total Cost 180000 11.92 2145000

20% Mark Up 180000 2.38 429000

Selling Price 180000 14.3 2574000

From the above table, it can be stated that the selling price for 200000 units will be

$13.95. Therefore, the bid for the supply to government department will be as per the following

table:

Particulars Unit

Cost

p.u. Amount

Selling Price 40000 13.95 558000

Less : Sales Commission 40000 2 80000

Bid Price 40000 11.95 478000

b) Capacity of 180000 units:-

For the capacity level of 180000 units, the cost & profit structure is calculated below:

Particulars Unit

Cost

p.u. Amount

Direct Material Cost 180000 2.5 450000

Direct Labor Cost 180000 3 540000

Variable Factory Overhead 180000 1.5 270000

Fixed Factory Overhead 180000 1.67 300000

Manufacturing Cost 180000 8.67 1560000

Variable Selling &

Administrative Cost 180000 2 360000

Fixed Selling &

Administrative Cost 180000 1.25 225000

Total Cost 180000 11.92 2145000

20% Mark Up 180000 2.38 429000

Selling Price 180000 14.3 2574000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING FOR MANAGERS

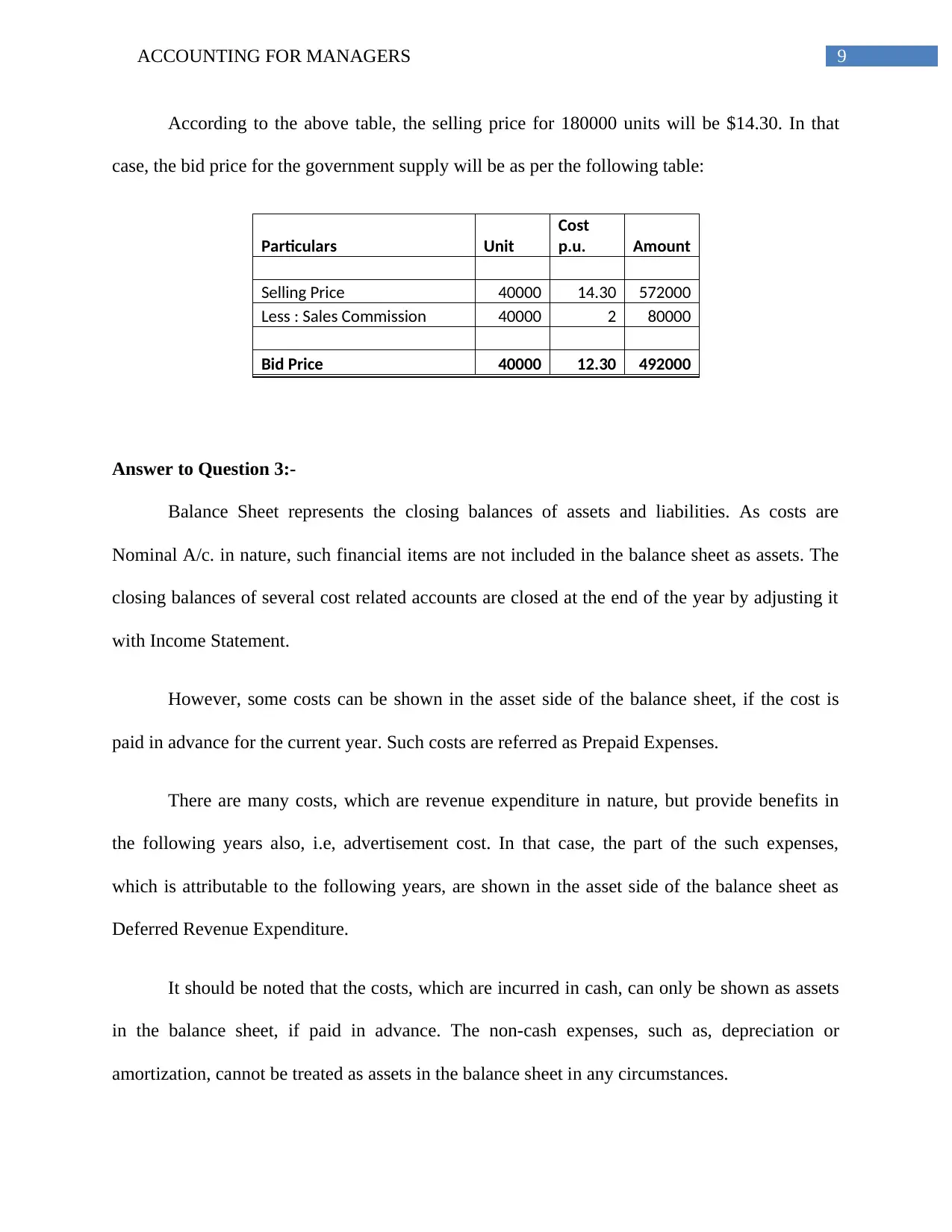

According to the above table, the selling price for 180000 units will be $14.30. In that

case, the bid price for the government supply will be as per the following table:

Particulars Unit

Cost

p.u. Amount

Selling Price 40000 14.30 572000

Less : Sales Commission 40000 2 80000

Bid Price 40000 12.30 492000

Answer to Question 3:-

Balance Sheet represents the closing balances of assets and liabilities. As costs are

Nominal A/c. in nature, such financial items are not included in the balance sheet as assets. The

closing balances of several cost related accounts are closed at the end of the year by adjusting it

with Income Statement.

However, some costs can be shown in the asset side of the balance sheet, if the cost is

paid in advance for the current year. Such costs are referred as Prepaid Expenses.

There are many costs, which are revenue expenditure in nature, but provide benefits in

the following years also, i.e, advertisement cost. In that case, the part of the such expenses,

which is attributable to the following years, are shown in the asset side of the balance sheet as

Deferred Revenue Expenditure.

It should be noted that the costs, which are incurred in cash, can only be shown as assets

in the balance sheet, if paid in advance. The non-cash expenses, such as, depreciation or

amortization, cannot be treated as assets in the balance sheet in any circumstances.

According to the above table, the selling price for 180000 units will be $14.30. In that

case, the bid price for the government supply will be as per the following table:

Particulars Unit

Cost

p.u. Amount

Selling Price 40000 14.30 572000

Less : Sales Commission 40000 2 80000

Bid Price 40000 12.30 492000

Answer to Question 3:-

Balance Sheet represents the closing balances of assets and liabilities. As costs are

Nominal A/c. in nature, such financial items are not included in the balance sheet as assets. The

closing balances of several cost related accounts are closed at the end of the year by adjusting it

with Income Statement.

However, some costs can be shown in the asset side of the balance sheet, if the cost is

paid in advance for the current year. Such costs are referred as Prepaid Expenses.

There are many costs, which are revenue expenditure in nature, but provide benefits in

the following years also, i.e, advertisement cost. In that case, the part of the such expenses,

which is attributable to the following years, are shown in the asset side of the balance sheet as

Deferred Revenue Expenditure.

It should be noted that the costs, which are incurred in cash, can only be shown as assets

in the balance sheet, if paid in advance. The non-cash expenses, such as, depreciation or

amortization, cannot be treated as assets in the balance sheet in any circumstances.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING FOR MANAGERS

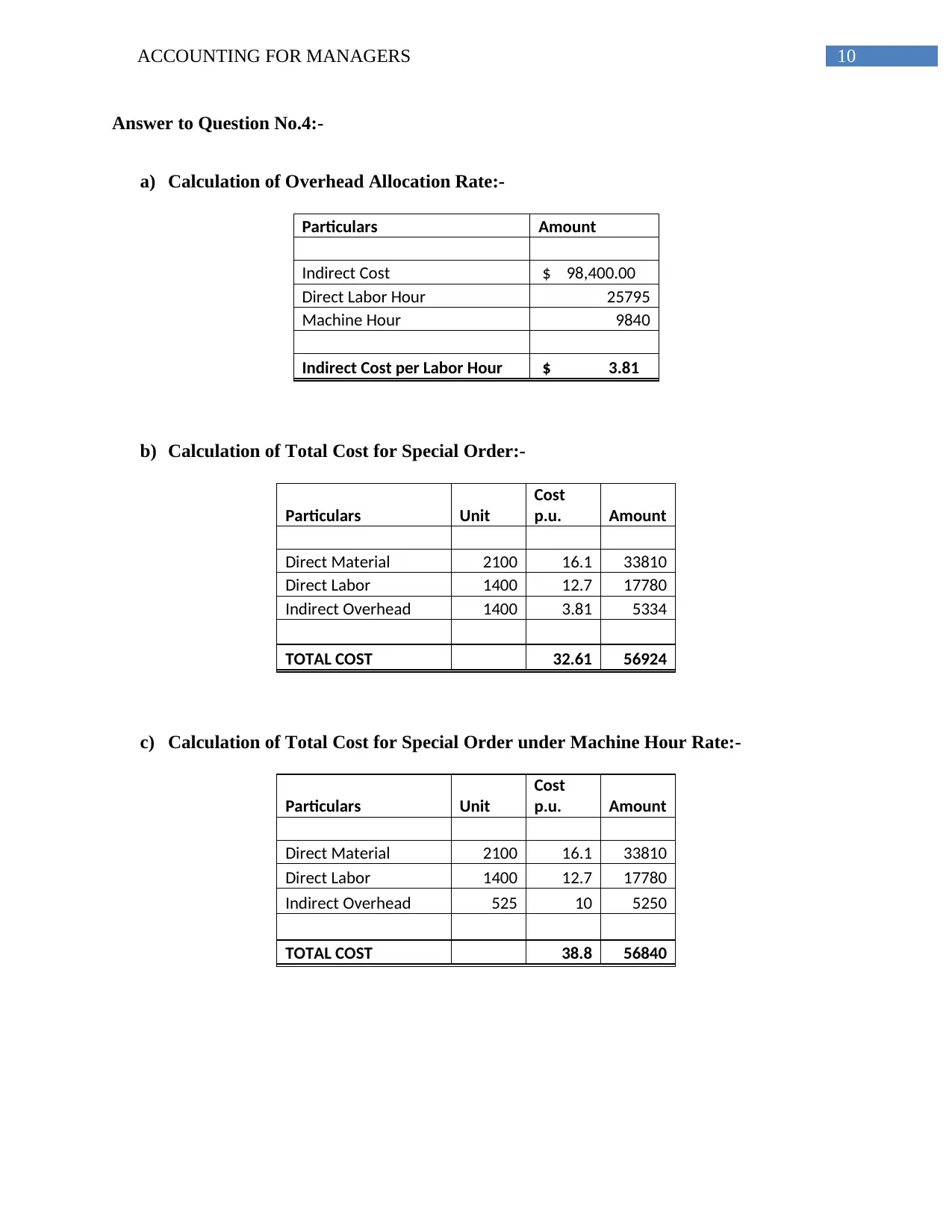

Answer to Question No.4:-

a) Calculation of Overhead Allocation Rate:-

Particulars Amount

Indirect Cost $ 98,400.00

Direct Labor Hour 25795

Machine Hour 9840

Indirect Cost per Labor Hour $ 3.81

b) Calculation of Total Cost for Special Order:-

Particulars Unit

Cost

p.u. Amount

Direct Material 2100 16.1 33810

Direct Labor 1400 12.7 17780

Indirect Overhead 1400 3.81 5334

TOTAL COST 32.61 56924

c) Calculation of Total Cost for Special Order under Machine Hour Rate:-

Particulars Unit

Cost

p.u. Amount

Direct Material 2100 16.1 33810

Direct Labor 1400 12.7 17780

Indirect Overhead 525 10 5250

TOTAL COST 38.8 56840

Answer to Question No.4:-

a) Calculation of Overhead Allocation Rate:-

Particulars Amount

Indirect Cost $ 98,400.00

Direct Labor Hour 25795

Machine Hour 9840

Indirect Cost per Labor Hour $ 3.81

b) Calculation of Total Cost for Special Order:-

Particulars Unit

Cost

p.u. Amount

Direct Material 2100 16.1 33810

Direct Labor 1400 12.7 17780

Indirect Overhead 1400 3.81 5334

TOTAL COST 32.61 56924

c) Calculation of Total Cost for Special Order under Machine Hour Rate:-

Particulars Unit

Cost

p.u. Amount

Direct Material 2100 16.1 33810

Direct Labor 1400 12.7 17780

Indirect Overhead 525 10 5250

TOTAL COST 38.8 56840

11ACCOUNTING FOR MANAGERS

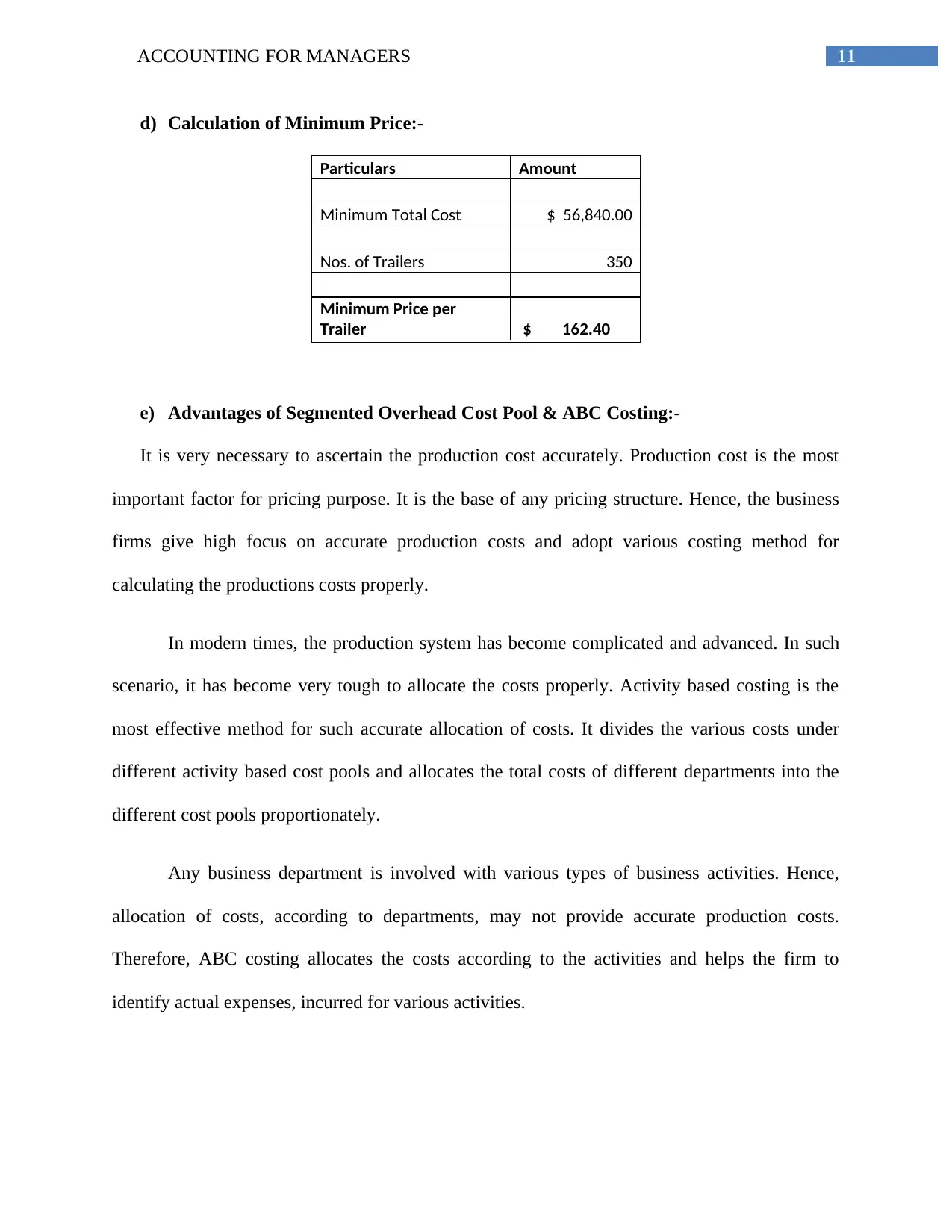

d) Calculation of Minimum Price:-

Particulars Amount

Minimum Total Cost $ 56,840.00

Nos. of Trailers 350

Minimum Price per

Trailer $ 162.40

e) Advantages of Segmented Overhead Cost Pool & ABC Costing:-

It is very necessary to ascertain the production cost accurately. Production cost is the most

important factor for pricing purpose. It is the base of any pricing structure. Hence, the business

firms give high focus on accurate production costs and adopt various costing method for

calculating the productions costs properly.

In modern times, the production system has become complicated and advanced. In such

scenario, it has become very tough to allocate the costs properly. Activity based costing is the

most effective method for such accurate allocation of costs. It divides the various costs under

different activity based cost pools and allocates the total costs of different departments into the

different cost pools proportionately.

Any business department is involved with various types of business activities. Hence,

allocation of costs, according to departments, may not provide accurate production costs.

Therefore, ABC costing allocates the costs according to the activities and helps the firm to

identify actual expenses, incurred for various activities.

d) Calculation of Minimum Price:-

Particulars Amount

Minimum Total Cost $ 56,840.00

Nos. of Trailers 350

Minimum Price per

Trailer $ 162.40

e) Advantages of Segmented Overhead Cost Pool & ABC Costing:-

It is very necessary to ascertain the production cost accurately. Production cost is the most

important factor for pricing purpose. It is the base of any pricing structure. Hence, the business

firms give high focus on accurate production costs and adopt various costing method for

calculating the productions costs properly.

In modern times, the production system has become complicated and advanced. In such

scenario, it has become very tough to allocate the costs properly. Activity based costing is the

most effective method for such accurate allocation of costs. It divides the various costs under

different activity based cost pools and allocates the total costs of different departments into the

different cost pools proportionately.

Any business department is involved with various types of business activities. Hence,

allocation of costs, according to departments, may not provide accurate production costs.

Therefore, ABC costing allocates the costs according to the activities and helps the firm to

identify actual expenses, incurred for various activities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.