Accounting for Managers Homework Solution - Semester 1, 2024

VerifiedAdded on 2020/03/07

|15

|3174

|39

Homework Assignment

AI Summary

This document presents a complete solution to an Accounting for Managers assignment, addressing key concepts in financial and management accounting. The solution begins by comparing and contrasting financial and management accounting reports, classifying items as assets, liabilities, or equity, and distinguishing between cash flow budgets and statements. It then delves into depreciation, owner's equity changes, and the implications of bad debt. Ratio calculations for profitability, liquidity, and solvency are provided, along with a short report analyzing the business's financial health. The assignment further explores break-even analysis, special order decisions, and profit/loss calculations. It concludes with a discussion on factors influencing cash holdings, the costs of low inventory, and the pros and cons of retained earnings. The solution also includes a price quotation for a specific job and considers non-financial information relevant to venture capitalists, offering a comprehensive overview of accounting principles and their practical application.

Running head: ACCOUNTING FOR MANAGERS

Accounting for Managers

Name of the University:

Name of the Student:

Authors Note:

Accounting for Managers

Name of the University:

Name of the Student:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING FOR MANAGERS

Table of Contents

Question 1:.................................................................................................................................3

a) Comparing and contrasting financial accounting reports with management accounting

reports:........................................................................................................................................3

b) Depicting relevant question regarding public listed company:.............................................3

c) Classifying whether the item falls under asset, liability or equity:........................................3

d) Distinguishing a cash flow budget with statement of cash flow:..........................................4

e) Explaining the term depreciation by using practice examples:..............................................4

f) Depicting whether which part of the pair would be expected be larger:................................5

Question 2:.................................................................................................................................5

a) Discussing the major changes that could increase or decrease the owner’s equity:..............5

b) Depicting the reason why business owners would leave retained earnings in the business:.6

c) Discussing whether financial performance could be affected by not considering bad debt:. 7

d) Depicting the reason behind companies operating cash flow showing negative balance and

whether the company’s management needs to be alarmed:.......................................................7

Question 3:.................................................................................................................................8

a) Calculating ratios for 2015 and 2016:....................................................................................8

b) Writing a short report on profitability, short-term liquidity, and long-term solvency of the

business:.....................................................................................................................................8

Question 4:.................................................................................................................................9

a) Calculating the variable cost per pot for Fancy Terracotta pots:...........................................9

b) Depicting the contribution cost per pot for Fancy Terracotta pots:.......................................9

c) Calculating the breakeven point per month if only plain black pots are made:...................10

d) Depicting whether the order should be accepted or not:.....................................................10

e) Depicting the circumstance, this could change the conclusion for part d:...........................10

ACCOUNTING FOR MANAGERS

Table of Contents

Question 1:.................................................................................................................................3

a) Comparing and contrasting financial accounting reports with management accounting

reports:........................................................................................................................................3

b) Depicting relevant question regarding public listed company:.............................................3

c) Classifying whether the item falls under asset, liability or equity:........................................3

d) Distinguishing a cash flow budget with statement of cash flow:..........................................4

e) Explaining the term depreciation by using practice examples:..............................................4

f) Depicting whether which part of the pair would be expected be larger:................................5

Question 2:.................................................................................................................................5

a) Discussing the major changes that could increase or decrease the owner’s equity:..............5

b) Depicting the reason why business owners would leave retained earnings in the business:.6

c) Discussing whether financial performance could be affected by not considering bad debt:. 7

d) Depicting the reason behind companies operating cash flow showing negative balance and

whether the company’s management needs to be alarmed:.......................................................7

Question 3:.................................................................................................................................8

a) Calculating ratios for 2015 and 2016:....................................................................................8

b) Writing a short report on profitability, short-term liquidity, and long-term solvency of the

business:.....................................................................................................................................8

Question 4:.................................................................................................................................9

a) Calculating the variable cost per pot for Fancy Terracotta pots:...........................................9

b) Depicting the contribution cost per pot for Fancy Terracotta pots:.......................................9

c) Calculating the breakeven point per month if only plain black pots are made:...................10

d) Depicting whether the order should be accepted or not:.....................................................10

e) Depicting the circumstance, this could change the conclusion for part d:...........................10

2

ACCOUNTING FOR MANAGERS

f) Calculating the profit and loss for the month of May:.........................................................10

a) Depicting the factors that influence how much cash a business should hold:.....................12

b) Depicting the cost that might be faced by the business by holding to low inventory:........12

c) Explaining pros and cons of retained earnings:...................................................................12

d) Depicting the non-financial information that would concern a venture capitalist:..............13

Reference and Bibliography:....................................................................................................14

ACCOUNTING FOR MANAGERS

f) Calculating the profit and loss for the month of May:.........................................................10

a) Depicting the factors that influence how much cash a business should hold:.....................12

b) Depicting the cost that might be faced by the business by holding to low inventory:........12

c) Explaining pros and cons of retained earnings:...................................................................12

d) Depicting the non-financial information that would concern a venture capitalist:..............13

Reference and Bibliography:....................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING FOR MANAGERS

Question 1:

a) Comparing and contrasting financial accounting reports with management

accounting reports:

The financial accounting report mainly summarizes about the financial position of the

company. On the other hand, management accounting report provides a detailed and

complete report regarding various information of the organisation. The reports provide by

financial accounting consists of the annual report, while the report provided by the

management accounting directly consists details about specific areas in business (Drury

2013).

b) Depicting relevant question regarding public listed company:

The company is mainly owned by shareholders, the person holding the maximum

shares of the company is considered to be the owner.

Apart from shareholders, employees, creditors, suppliers, stakeholders, analyst,

investors and financial institutions are interest in the contents of the financial accounting

report of an organisation (Lobo and Zhao 2013).

c) Classifying whether the item falls under asset, liability or equity:

Items Classification

Paid up capital Equity

Bank loan Liability

Provision for annual leave Liability

Brand names and intellectual property Asset

ACCOUNTING FOR MANAGERS

Question 1:

a) Comparing and contrasting financial accounting reports with management

accounting reports:

The financial accounting report mainly summarizes about the financial position of the

company. On the other hand, management accounting report provides a detailed and

complete report regarding various information of the organisation. The reports provide by

financial accounting consists of the annual report, while the report provided by the

management accounting directly consists details about specific areas in business (Drury

2013).

b) Depicting relevant question regarding public listed company:

The company is mainly owned by shareholders, the person holding the maximum

shares of the company is considered to be the owner.

Apart from shareholders, employees, creditors, suppliers, stakeholders, analyst,

investors and financial institutions are interest in the contents of the financial accounting

report of an organisation (Lobo and Zhao 2013).

c) Classifying whether the item falls under asset, liability or equity:

Items Classification

Paid up capital Equity

Bank loan Liability

Provision for annual leave Liability

Brand names and intellectual property Asset

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING FOR MANAGERS

Accounts receivable Asset

Prepaid insurance premiums Asset

Deposit paid by a customer for work yet to be done Liability

Retained profit Liability

d) Distinguishing a cash flow budget with statement of cash flow:

Cash low budget is mainly prepared for the forthcoming year as a planning exercise,

whereas cash flow statement is mainly post-mortem of the past activities conducted by the

organisation.

Cash budget is mainly prepared based on requirements, which could be monthly, half

yearly, quarterly and yearly. On the contrary, cash flow statement is mainly prepared for a

financial account year (Megginson, Ullah and Wei 2014).

There is no specific format that is descried for cash budget companies mainly prepare

the cash budget according to their requirements. On the other hand, cash flow statement is

mainly prepared according to the provisions laid down by accounting standard-3.

e) Explaining the term depreciation by using practice examples:

Depreciation is mainly a method, which is used by the organisation for reducing ht tax

by declining value of the assets (Becker 2015). For example, a company buys a machine for

$60,000, which is expected to last for 5 years with no scrap value. This mainly allows the

company to calculate the deprecation amount each year at $12,000, which could be deducted

from the taxable amount and increase profit retention of the organisation.

ACCOUNTING FOR MANAGERS

Accounts receivable Asset

Prepaid insurance premiums Asset

Deposit paid by a customer for work yet to be done Liability

Retained profit Liability

d) Distinguishing a cash flow budget with statement of cash flow:

Cash low budget is mainly prepared for the forthcoming year as a planning exercise,

whereas cash flow statement is mainly post-mortem of the past activities conducted by the

organisation.

Cash budget is mainly prepared based on requirements, which could be monthly, half

yearly, quarterly and yearly. On the contrary, cash flow statement is mainly prepared for a

financial account year (Megginson, Ullah and Wei 2014).

There is no specific format that is descried for cash budget companies mainly prepare

the cash budget according to their requirements. On the other hand, cash flow statement is

mainly prepared according to the provisions laid down by accounting standard-3.

e) Explaining the term depreciation by using practice examples:

Depreciation is mainly a method, which is used by the organisation for reducing ht tax

by declining value of the assets (Becker 2015). For example, a company buys a machine for

$60,000, which is expected to last for 5 years with no scrap value. This mainly allows the

company to calculate the deprecation amount each year at $12,000, which could be deducted

from the taxable amount and increase profit retention of the organisation.

5

ACCOUNTING FOR MANAGERS

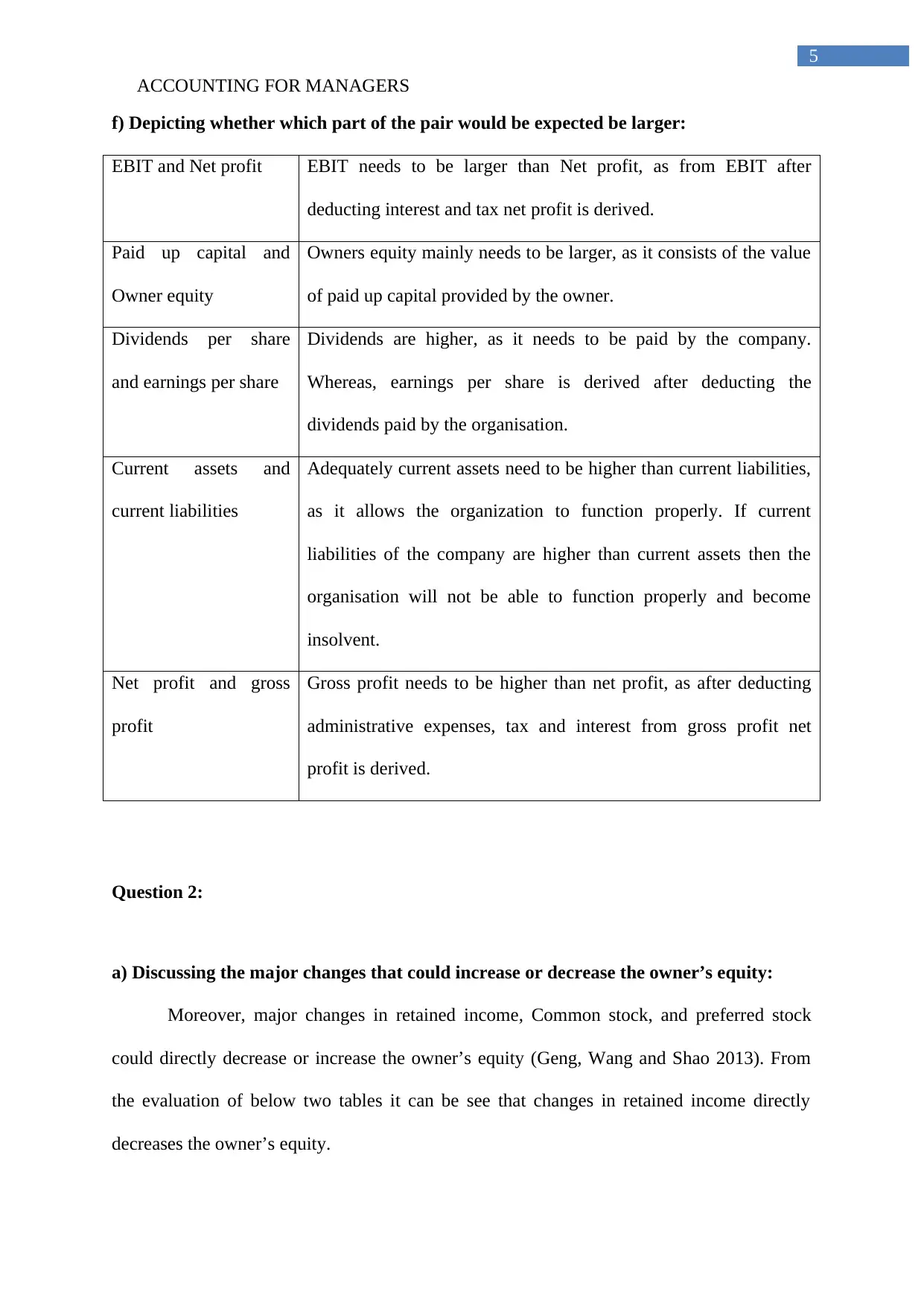

f) Depicting whether which part of the pair would be expected be larger:

EBIT and Net profit EBIT needs to be larger than Net profit, as from EBIT after

deducting interest and tax net profit is derived.

Paid up capital and

Owner equity

Owners equity mainly needs to be larger, as it consists of the value

of paid up capital provided by the owner.

Dividends per share

and earnings per share

Dividends are higher, as it needs to be paid by the company.

Whereas, earnings per share is derived after deducting the

dividends paid by the organisation.

Current assets and

current liabilities

Adequately current assets need to be higher than current liabilities,

as it allows the organization to function properly. If current

liabilities of the company are higher than current assets then the

organisation will not be able to function properly and become

insolvent.

Net profit and gross

profit

Gross profit needs to be higher than net profit, as after deducting

administrative expenses, tax and interest from gross profit net

profit is derived.

Question 2:

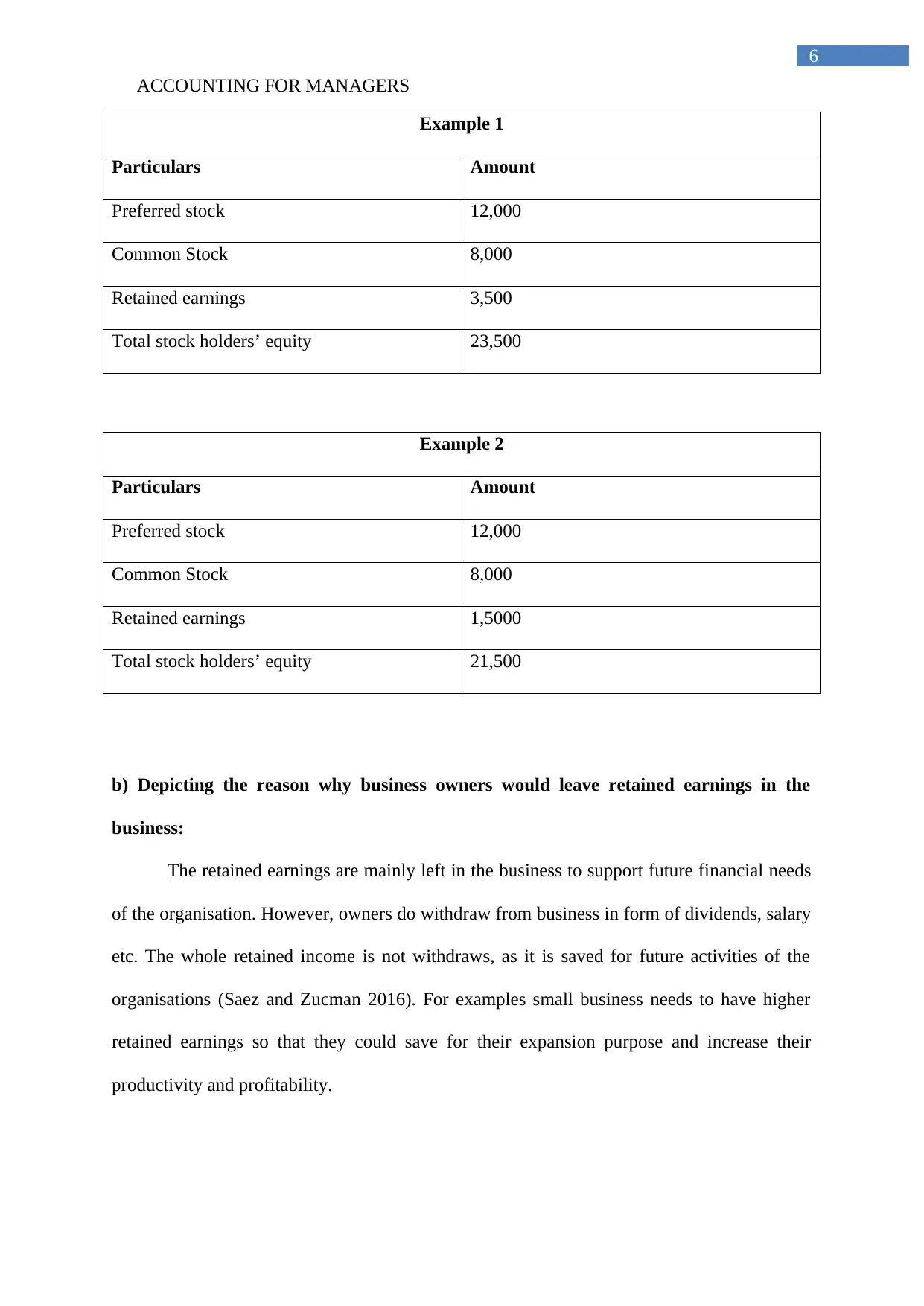

a) Discussing the major changes that could increase or decrease the owner’s equity:

Moreover, major changes in retained income, Common stock, and preferred stock

could directly decrease or increase the owner’s equity (Geng, Wang and Shao 2013). From

the evaluation of below two tables it can be see that changes in retained income directly

decreases the owner’s equity.

ACCOUNTING FOR MANAGERS

f) Depicting whether which part of the pair would be expected be larger:

EBIT and Net profit EBIT needs to be larger than Net profit, as from EBIT after

deducting interest and tax net profit is derived.

Paid up capital and

Owner equity

Owners equity mainly needs to be larger, as it consists of the value

of paid up capital provided by the owner.

Dividends per share

and earnings per share

Dividends are higher, as it needs to be paid by the company.

Whereas, earnings per share is derived after deducting the

dividends paid by the organisation.

Current assets and

current liabilities

Adequately current assets need to be higher than current liabilities,

as it allows the organization to function properly. If current

liabilities of the company are higher than current assets then the

organisation will not be able to function properly and become

insolvent.

Net profit and gross

profit

Gross profit needs to be higher than net profit, as after deducting

administrative expenses, tax and interest from gross profit net

profit is derived.

Question 2:

a) Discussing the major changes that could increase or decrease the owner’s equity:

Moreover, major changes in retained income, Common stock, and preferred stock

could directly decrease or increase the owner’s equity (Geng, Wang and Shao 2013). From

the evaluation of below two tables it can be see that changes in retained income directly

decreases the owner’s equity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING FOR MANAGERS

Example 1

Particulars Amount

Preferred stock 12,000

Common Stock 8,000

Retained earnings 3,500

Total stock holders’ equity 23,500

Example 2

Particulars Amount

Preferred stock 12,000

Common Stock 8,000

Retained earnings 1,5000

Total stock holders’ equity 21,500

b) Depicting the reason why business owners would leave retained earnings in the

business:

The retained earnings are mainly left in the business to support future financial needs

of the organisation. However, owners do withdraw from business in form of dividends, salary

etc. The whole retained income is not withdraws, as it is saved for future activities of the

organisations (Saez and Zucman 2016). For examples small business needs to have higher

retained earnings so that they could save for their expansion purpose and increase their

productivity and profitability.

ACCOUNTING FOR MANAGERS

Example 1

Particulars Amount

Preferred stock 12,000

Common Stock 8,000

Retained earnings 3,500

Total stock holders’ equity 23,500

Example 2

Particulars Amount

Preferred stock 12,000

Common Stock 8,000

Retained earnings 1,5000

Total stock holders’ equity 21,500

b) Depicting the reason why business owners would leave retained earnings in the

business:

The retained earnings are mainly left in the business to support future financial needs

of the organisation. However, owners do withdraw from business in form of dividends, salary

etc. The whole retained income is not withdraws, as it is saved for future activities of the

organisations (Saez and Zucman 2016). For examples small business needs to have higher

retained earnings so that they could save for their expansion purpose and increase their

productivity and profitability.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING FOR MANAGERS

c) Discussing whether financial performance could be affected by not considering bad

debt:

Organisation mainly use allowance for doubtful debts for making the required

provisions of the bad debt. If the bad debt is not recorded as the expenses of the organisation

in the financial account then it will directly increase its performance. This is mainly because

expense is not recorded, while adequate revenues are been stated, which will improve

financial performance of the organization (Saeidi et al. 2015). For example a bad debt of

$10,000 is generated from customer, which is not recorded in the financial account. The sales

will show the increased revenue, whereas the actual payment from the customer is not

received. This directly increases the overall profits and improves performance of the

organisation

d) Depicting the reason behind companies operating cash flow showing negative balance

and whether the company’s management needs to be alarmed:

The negative cash from operating activities mainly indicates that the cash balance of

the company is going to be negative, which is why the management needs to have positive

financing or investing activities cash flow. This will mainly nullify the negative cash balance

from operating activities. Moreover, the management needs to be concerned regarding the

negative cash balance, as it might directly affects its cash at hand balance (Collins, Hribar

and Tian 2014). For example an organisation having negative operating cash flow, will have

paid more cash than it has received, which is why it mainly needs to sells its current assets to

support the short term obligations.

ACCOUNTING FOR MANAGERS

c) Discussing whether financial performance could be affected by not considering bad

debt:

Organisation mainly use allowance for doubtful debts for making the required

provisions of the bad debt. If the bad debt is not recorded as the expenses of the organisation

in the financial account then it will directly increase its performance. This is mainly because

expense is not recorded, while adequate revenues are been stated, which will improve

financial performance of the organization (Saeidi et al. 2015). For example a bad debt of

$10,000 is generated from customer, which is not recorded in the financial account. The sales

will show the increased revenue, whereas the actual payment from the customer is not

received. This directly increases the overall profits and improves performance of the

organisation

d) Depicting the reason behind companies operating cash flow showing negative balance

and whether the company’s management needs to be alarmed:

The negative cash from operating activities mainly indicates that the cash balance of

the company is going to be negative, which is why the management needs to have positive

financing or investing activities cash flow. This will mainly nullify the negative cash balance

from operating activities. Moreover, the management needs to be concerned regarding the

negative cash balance, as it might directly affects its cash at hand balance (Collins, Hribar

and Tian 2014). For example an organisation having negative operating cash flow, will have

paid more cash than it has received, which is why it mainly needs to sells its current assets to

support the short term obligations.

8

ACCOUNTING FOR MANAGERS

Question 3:

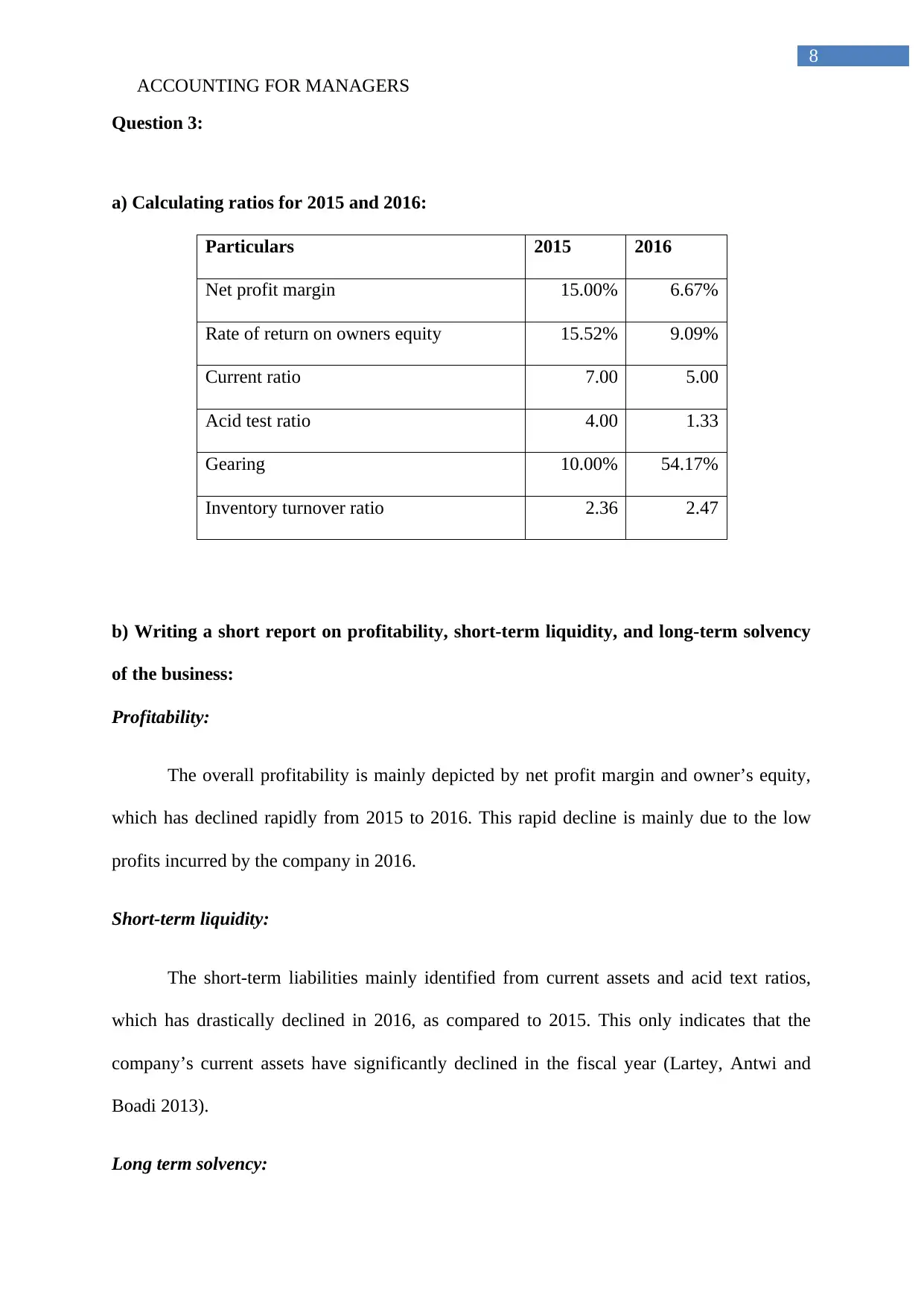

a) Calculating ratios for 2015 and 2016:

Particulars 2015 2016

Net profit margin 15.00% 6.67%

Rate of return on owners equity 15.52% 9.09%

Current ratio 7.00 5.00

Acid test ratio 4.00 1.33

Gearing 10.00% 54.17%

Inventory turnover ratio 2.36 2.47

b) Writing a short report on profitability, short-term liquidity, and long-term solvency

of the business:

Profitability:

The overall profitability is mainly depicted by net profit margin and owner’s equity,

which has declined rapidly from 2015 to 2016. This rapid decline is mainly due to the low

profits incurred by the company in 2016.

Short-term liquidity:

The short-term liabilities mainly identified from current assets and acid text ratios,

which has drastically declined in 2016, as compared to 2015. This only indicates that the

company’s current assets have significantly declined in the fiscal year (Lartey, Antwi and

Boadi 2013).

Long term solvency:

ACCOUNTING FOR MANAGERS

Question 3:

a) Calculating ratios for 2015 and 2016:

Particulars 2015 2016

Net profit margin 15.00% 6.67%

Rate of return on owners equity 15.52% 9.09%

Current ratio 7.00 5.00

Acid test ratio 4.00 1.33

Gearing 10.00% 54.17%

Inventory turnover ratio 2.36 2.47

b) Writing a short report on profitability, short-term liquidity, and long-term solvency

of the business:

Profitability:

The overall profitability is mainly depicted by net profit margin and owner’s equity,

which has declined rapidly from 2015 to 2016. This rapid decline is mainly due to the low

profits incurred by the company in 2016.

Short-term liquidity:

The short-term liabilities mainly identified from current assets and acid text ratios,

which has drastically declined in 2016, as compared to 2015. This only indicates that the

company’s current assets have significantly declined in the fiscal year (Lartey, Antwi and

Boadi 2013).

Long term solvency:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING FOR MANAGERS

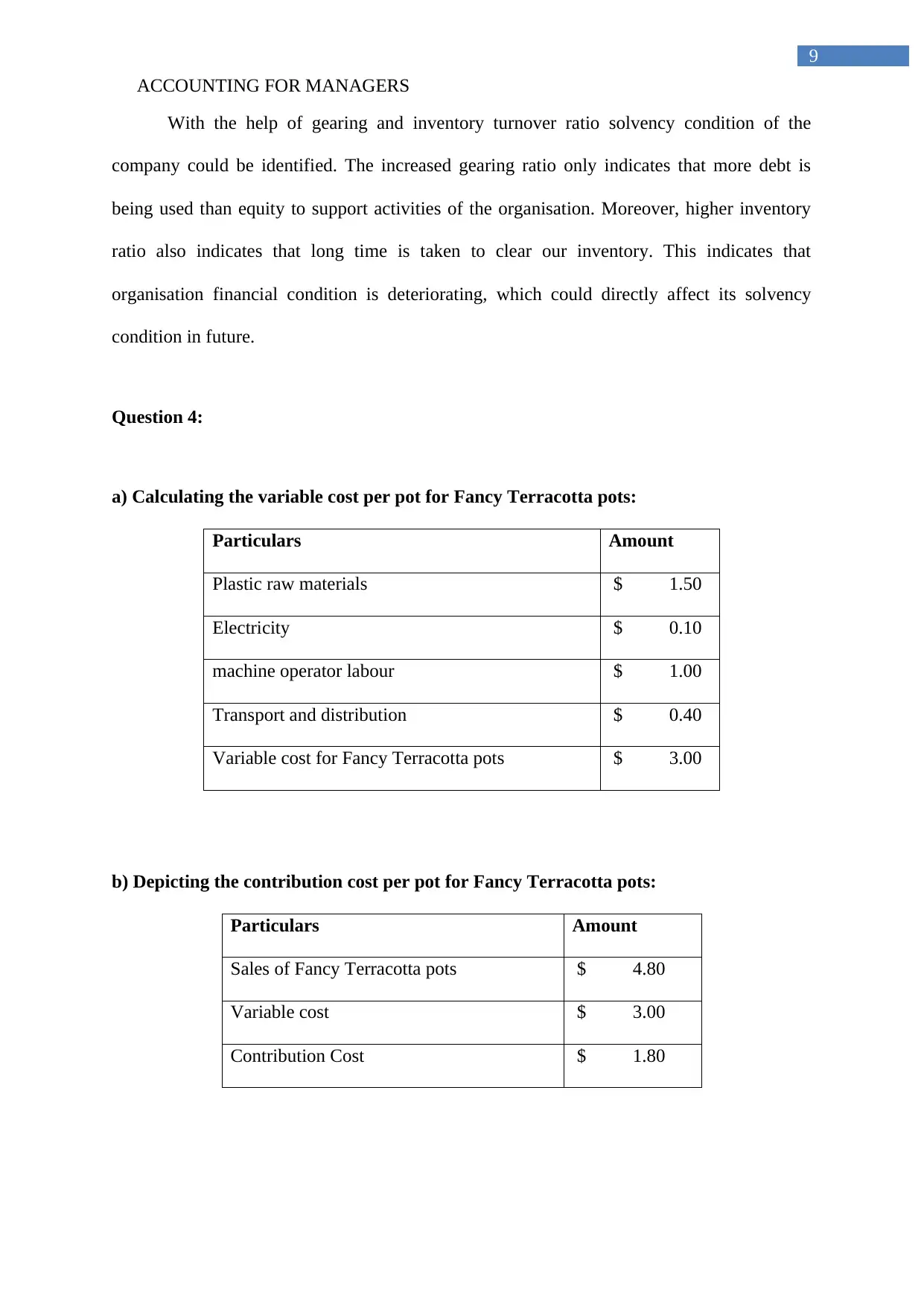

With the help of gearing and inventory turnover ratio solvency condition of the

company could be identified. The increased gearing ratio only indicates that more debt is

being used than equity to support activities of the organisation. Moreover, higher inventory

ratio also indicates that long time is taken to clear our inventory. This indicates that

organisation financial condition is deteriorating, which could directly affect its solvency

condition in future.

Question 4:

a) Calculating the variable cost per pot for Fancy Terracotta pots:

Particulars Amount

Plastic raw materials $ 1.50

Electricity $ 0.10

machine operator labour $ 1.00

Transport and distribution $ 0.40

Variable cost for Fancy Terracotta pots $ 3.00

b) Depicting the contribution cost per pot for Fancy Terracotta pots:

Particulars Amount

Sales of Fancy Terracotta pots $ 4.80

Variable cost $ 3.00

Contribution Cost $ 1.80

ACCOUNTING FOR MANAGERS

With the help of gearing and inventory turnover ratio solvency condition of the

company could be identified. The increased gearing ratio only indicates that more debt is

being used than equity to support activities of the organisation. Moreover, higher inventory

ratio also indicates that long time is taken to clear our inventory. This indicates that

organisation financial condition is deteriorating, which could directly affect its solvency

condition in future.

Question 4:

a) Calculating the variable cost per pot for Fancy Terracotta pots:

Particulars Amount

Plastic raw materials $ 1.50

Electricity $ 0.10

machine operator labour $ 1.00

Transport and distribution $ 0.40

Variable cost for Fancy Terracotta pots $ 3.00

b) Depicting the contribution cost per pot for Fancy Terracotta pots:

Particulars Amount

Sales of Fancy Terracotta pots $ 4.80

Variable cost $ 3.00

Contribution Cost $ 1.80

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING FOR MANAGERS

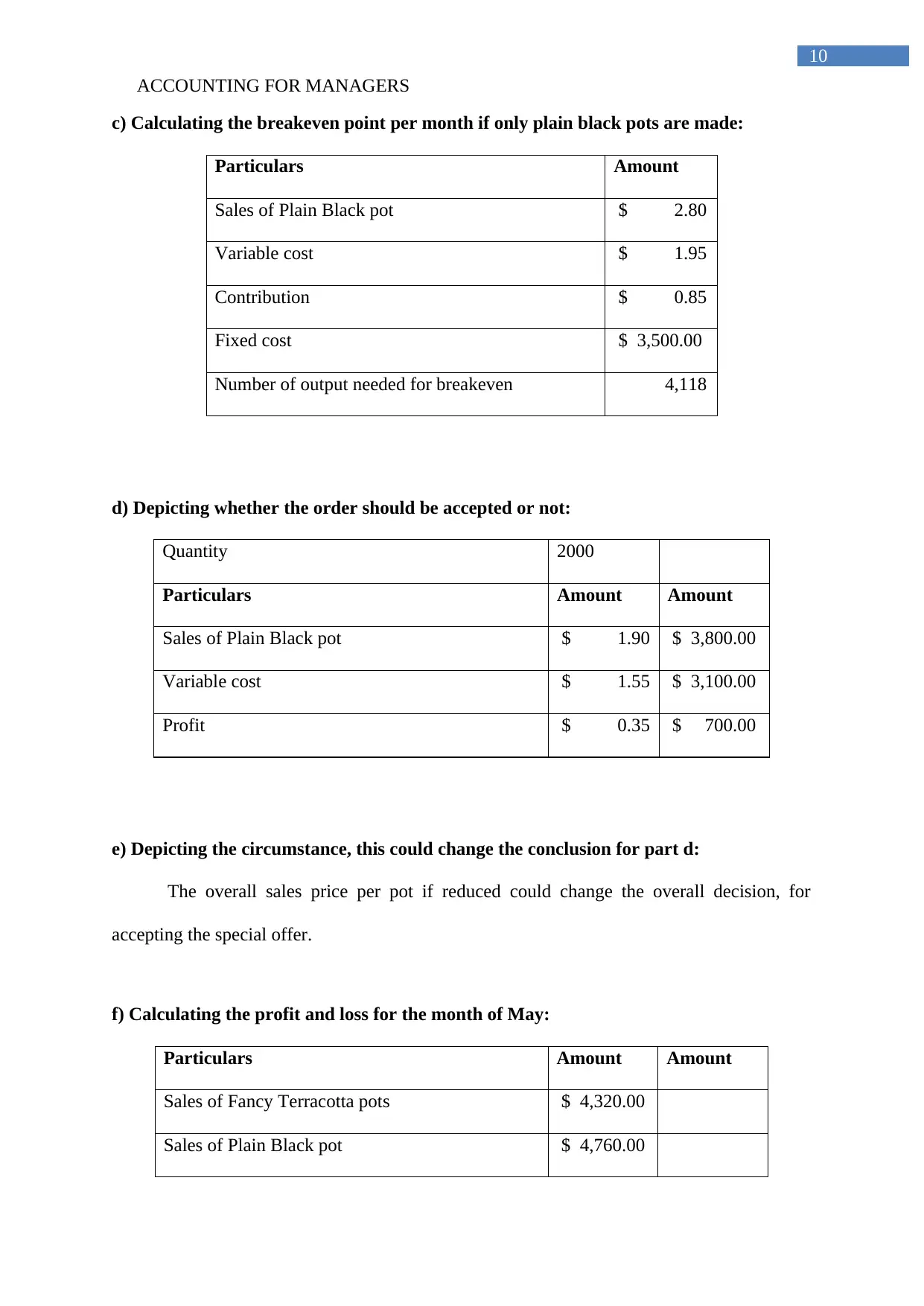

c) Calculating the breakeven point per month if only plain black pots are made:

Particulars Amount

Sales of Plain Black pot $ 2.80

Variable cost $ 1.95

Contribution $ 0.85

Fixed cost $ 3,500.00

Number of output needed for breakeven 4,118

d) Depicting whether the order should be accepted or not:

Quantity 2000

Particulars Amount Amount

Sales of Plain Black pot $ 1.90 $ 3,800.00

Variable cost $ 1.55 $ 3,100.00

Profit $ 0.35 $ 700.00

e) Depicting the circumstance, this could change the conclusion for part d:

The overall sales price per pot if reduced could change the overall decision, for

accepting the special offer.

f) Calculating the profit and loss for the month of May:

Particulars Amount Amount

Sales of Fancy Terracotta pots $ 4,320.00

Sales of Plain Black pot $ 4,760.00

ACCOUNTING FOR MANAGERS

c) Calculating the breakeven point per month if only plain black pots are made:

Particulars Amount

Sales of Plain Black pot $ 2.80

Variable cost $ 1.95

Contribution $ 0.85

Fixed cost $ 3,500.00

Number of output needed for breakeven 4,118

d) Depicting whether the order should be accepted or not:

Quantity 2000

Particulars Amount Amount

Sales of Plain Black pot $ 1.90 $ 3,800.00

Variable cost $ 1.55 $ 3,100.00

Profit $ 0.35 $ 700.00

e) Depicting the circumstance, this could change the conclusion for part d:

The overall sales price per pot if reduced could change the overall decision, for

accepting the special offer.

f) Calculating the profit and loss for the month of May:

Particulars Amount Amount

Sales of Fancy Terracotta pots $ 4,320.00

Sales of Plain Black pot $ 4,760.00

11

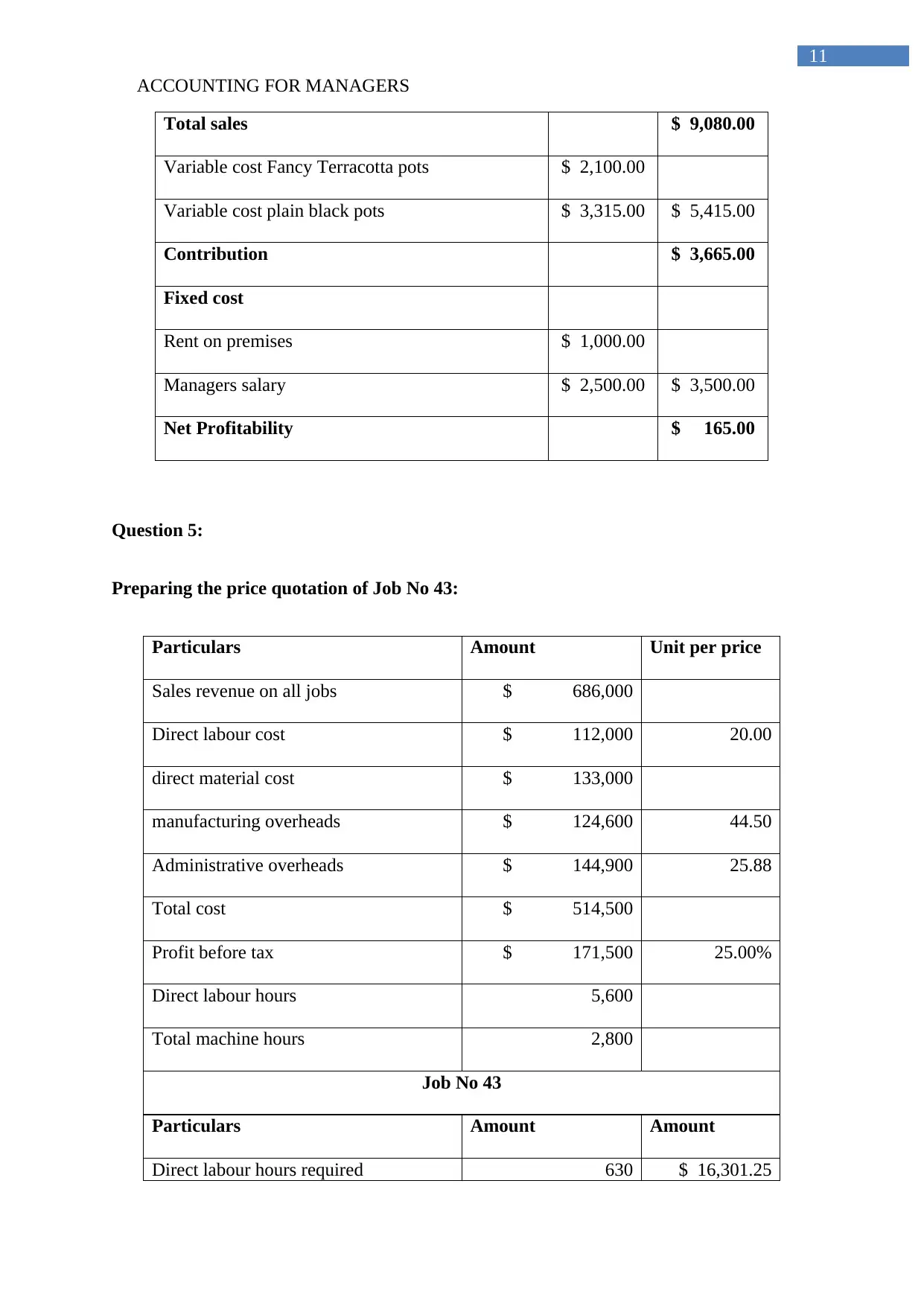

ACCOUNTING FOR MANAGERS

Total sales $ 9,080.00

Variable cost Fancy Terracotta pots $ 2,100.00

Variable cost plain black pots $ 3,315.00 $ 5,415.00

Contribution $ 3,665.00

Fixed cost

Rent on premises $ 1,000.00

Managers salary $ 2,500.00 $ 3,500.00

Net Profitability $ 165.00

Question 5:

Preparing the price quotation of Job No 43:

Particulars Amount Unit per price

Sales revenue on all jobs $ 686,000

Direct labour cost $ 112,000 20.00

direct material cost $ 133,000

manufacturing overheads $ 124,600 44.50

Administrative overheads $ 144,900 25.88

Total cost $ 514,500

Profit before tax $ 171,500 25.00%

Direct labour hours 5,600

Total machine hours 2,800

Job No 43

Particulars Amount Amount

Direct labour hours required 630 $ 16,301.25

ACCOUNTING FOR MANAGERS

Total sales $ 9,080.00

Variable cost Fancy Terracotta pots $ 2,100.00

Variable cost plain black pots $ 3,315.00 $ 5,415.00

Contribution $ 3,665.00

Fixed cost

Rent on premises $ 1,000.00

Managers salary $ 2,500.00 $ 3,500.00

Net Profitability $ 165.00

Question 5:

Preparing the price quotation of Job No 43:

Particulars Amount Unit per price

Sales revenue on all jobs $ 686,000

Direct labour cost $ 112,000 20.00

direct material cost $ 133,000

manufacturing overheads $ 124,600 44.50

Administrative overheads $ 144,900 25.88

Total cost $ 514,500

Profit before tax $ 171,500 25.00%

Direct labour hours 5,600

Total machine hours 2,800

Job No 43

Particulars Amount Amount

Direct labour hours required 630 $ 16,301.25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.