Accounting for Managers: Financial Analysis of Pacific Telemet Ltd

VerifiedAdded on 2021/11/01

|12

|1438

|102

Report

AI Summary

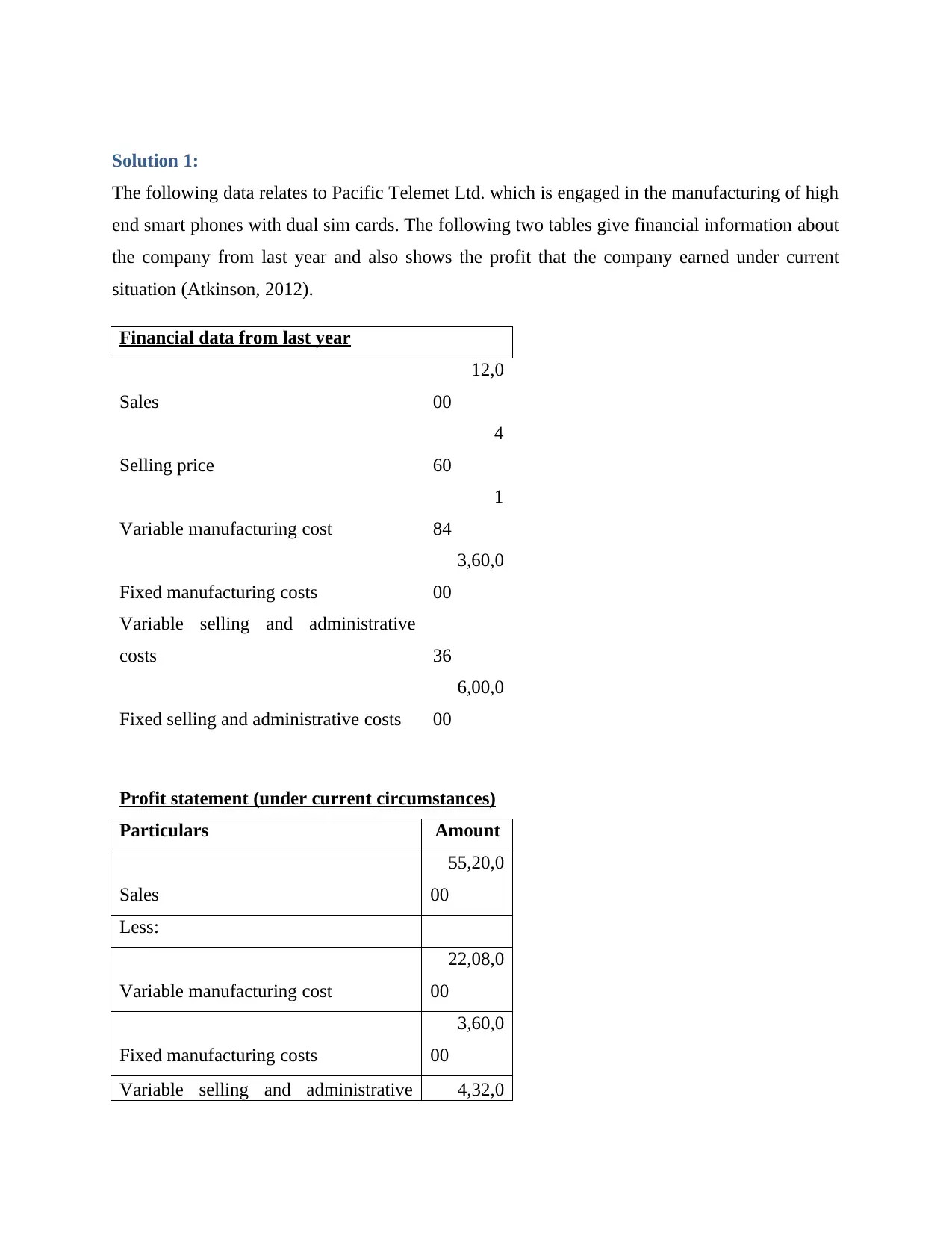

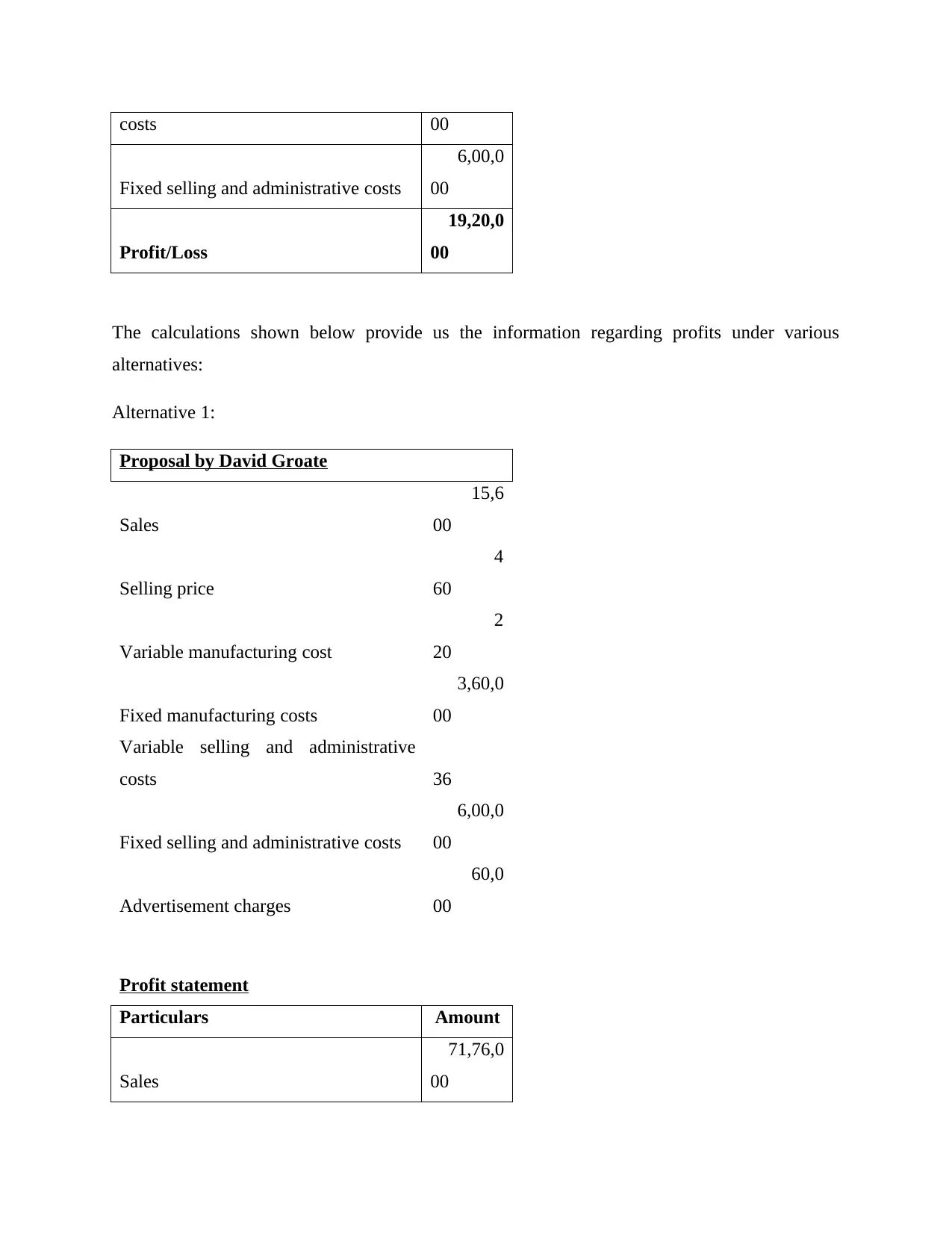

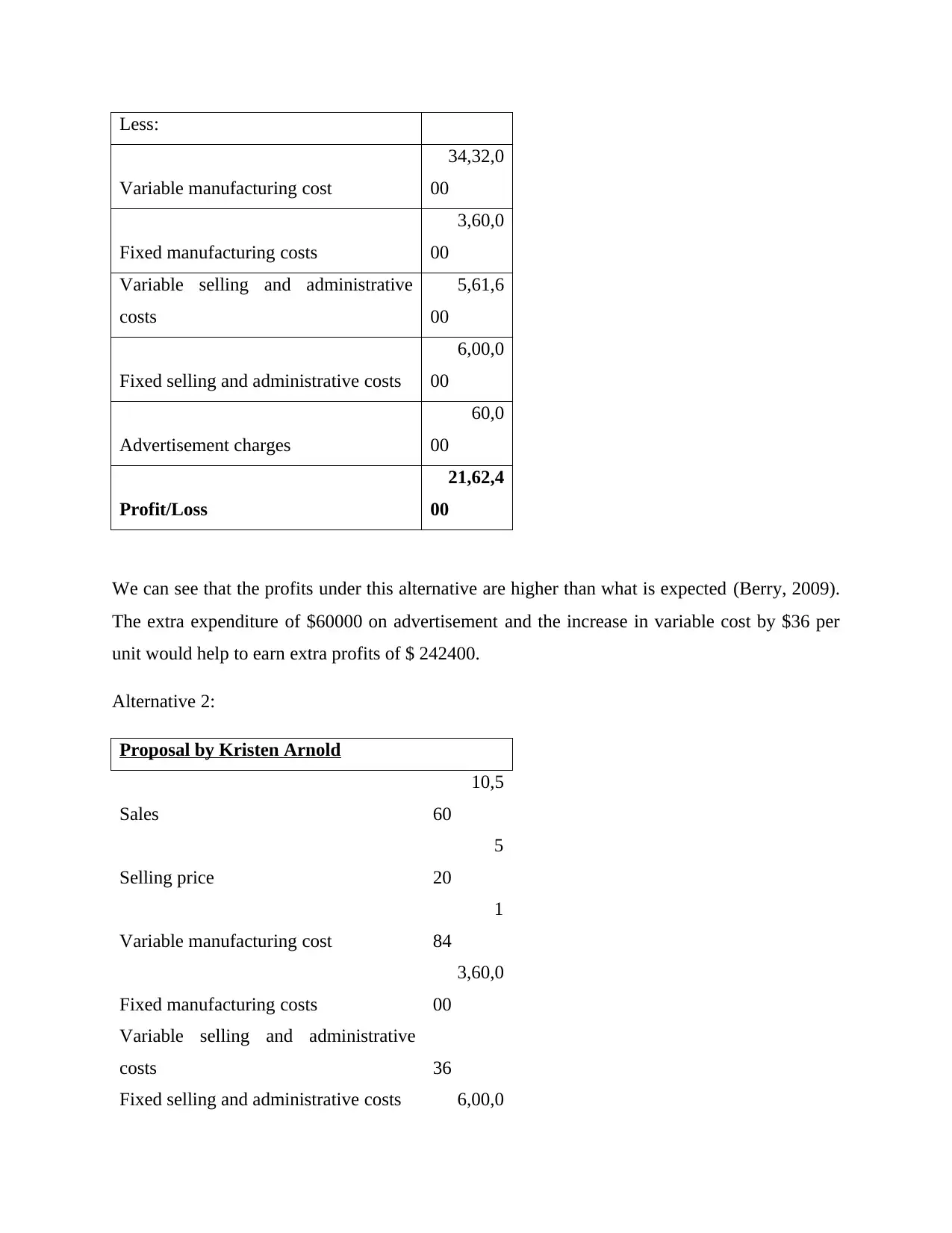

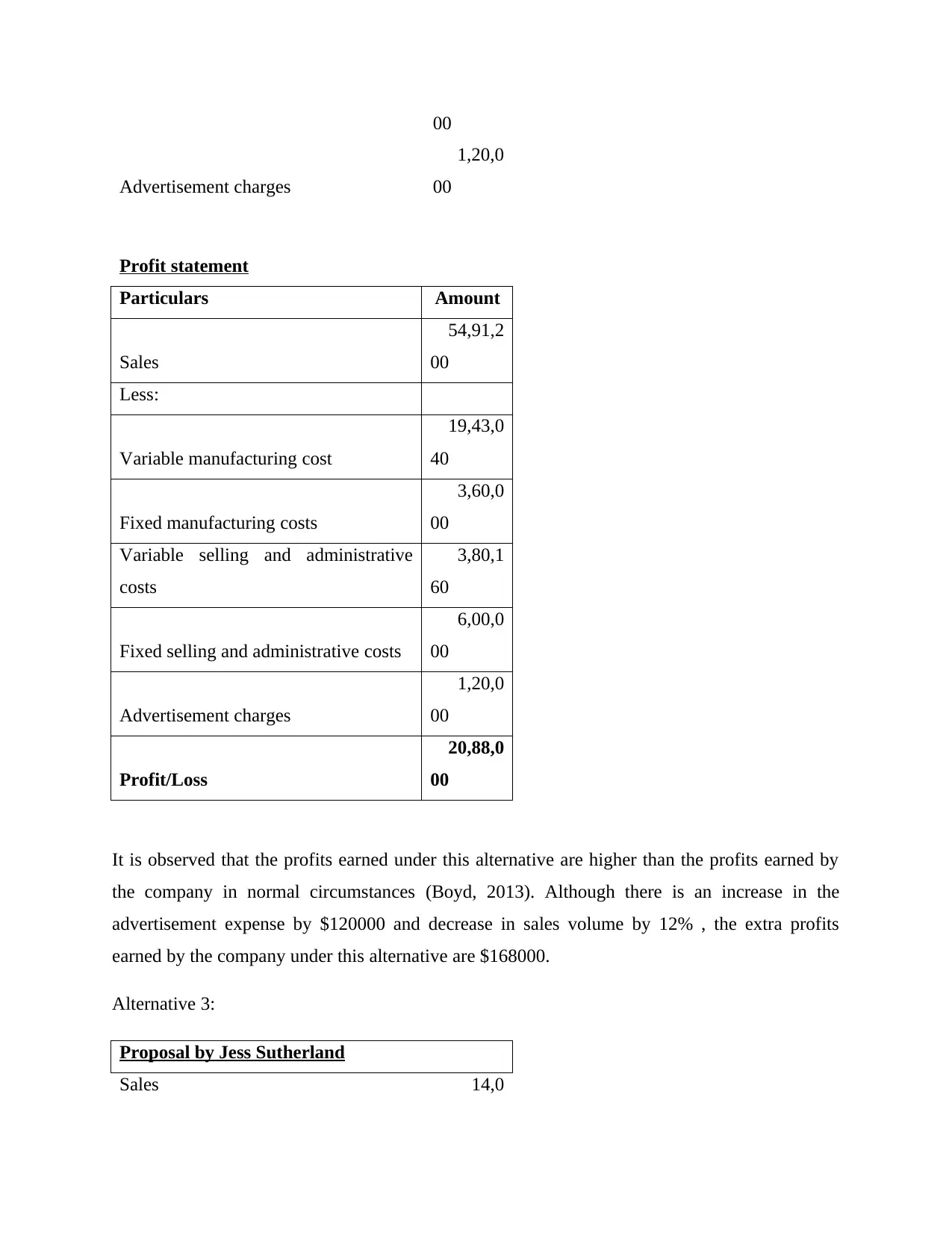

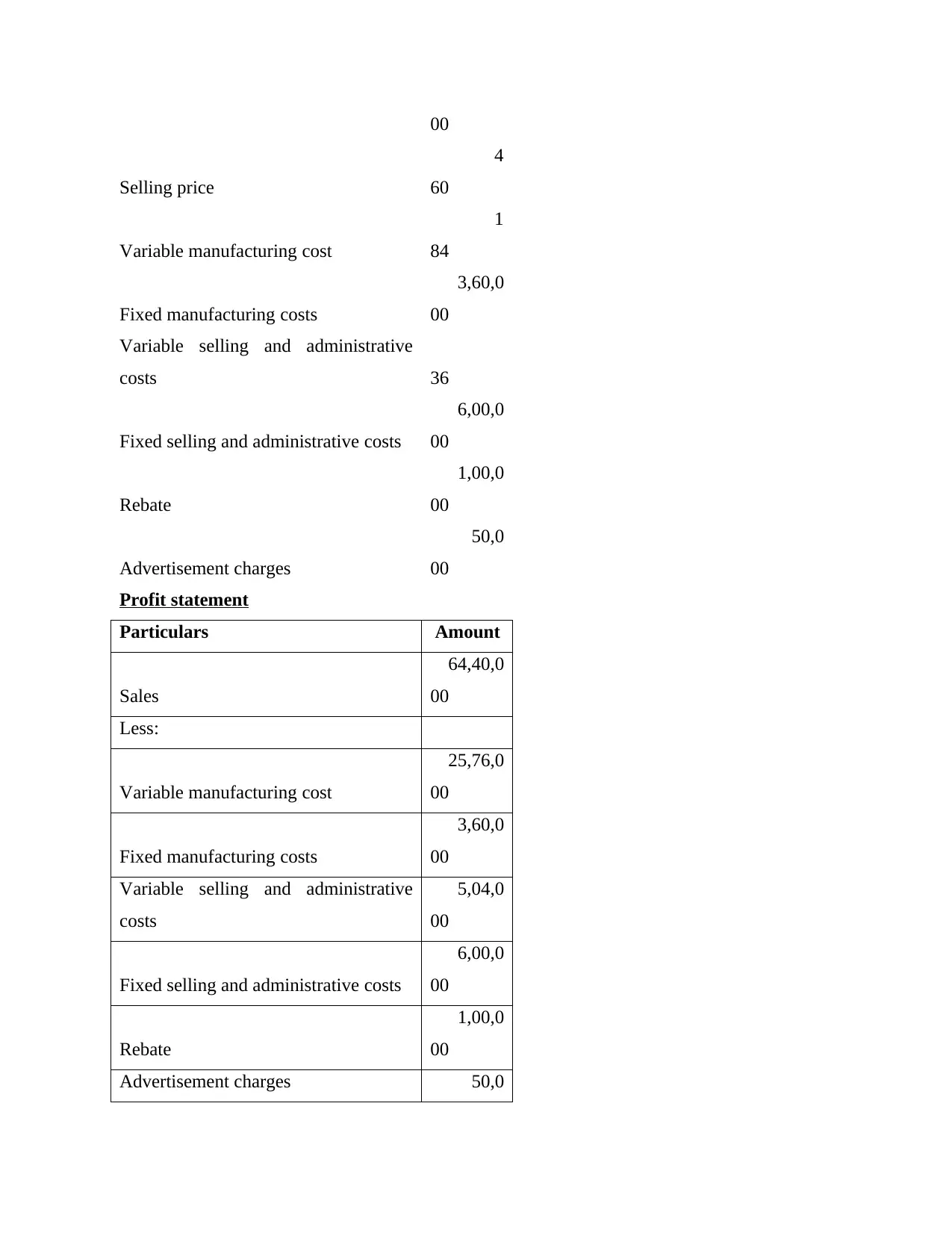

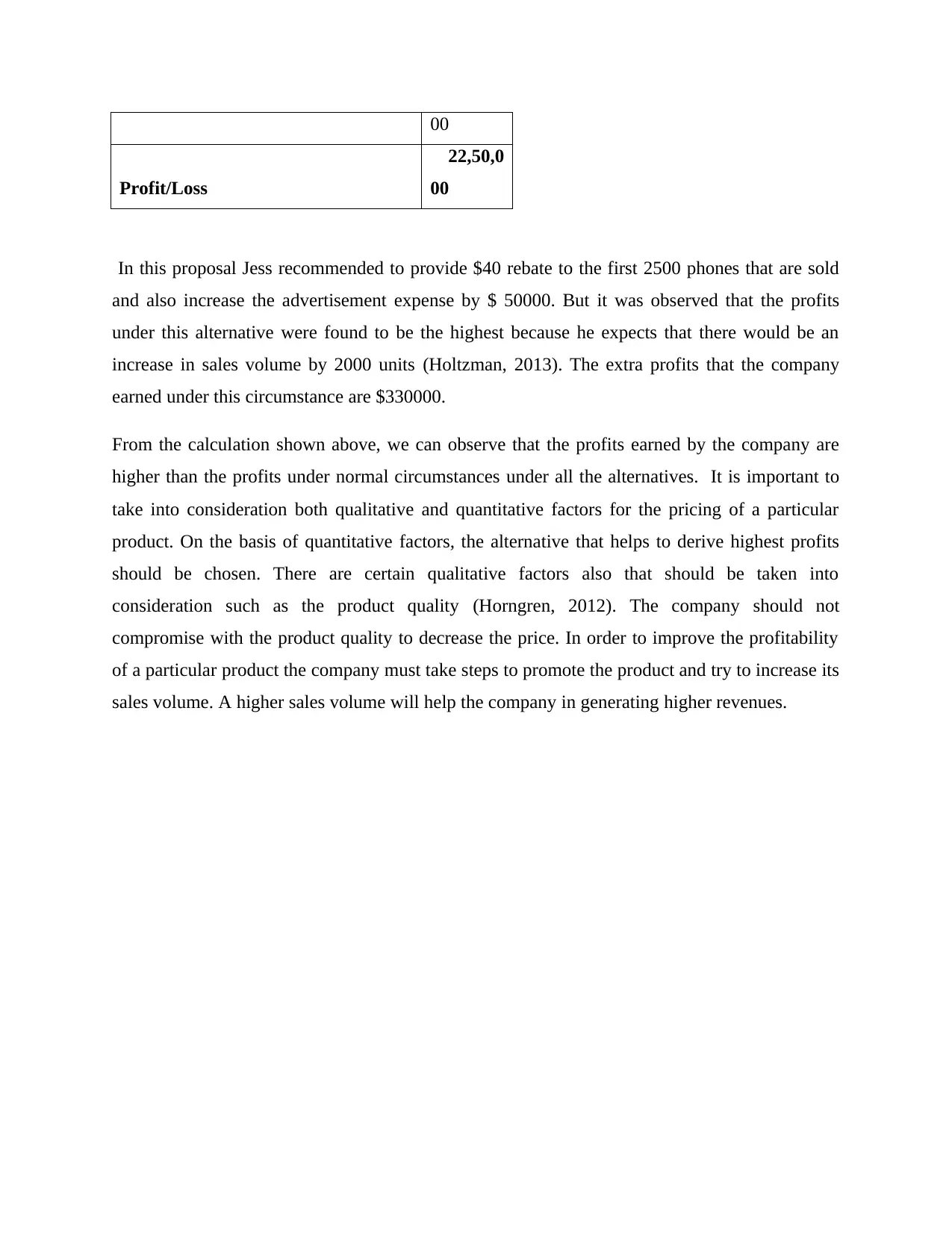

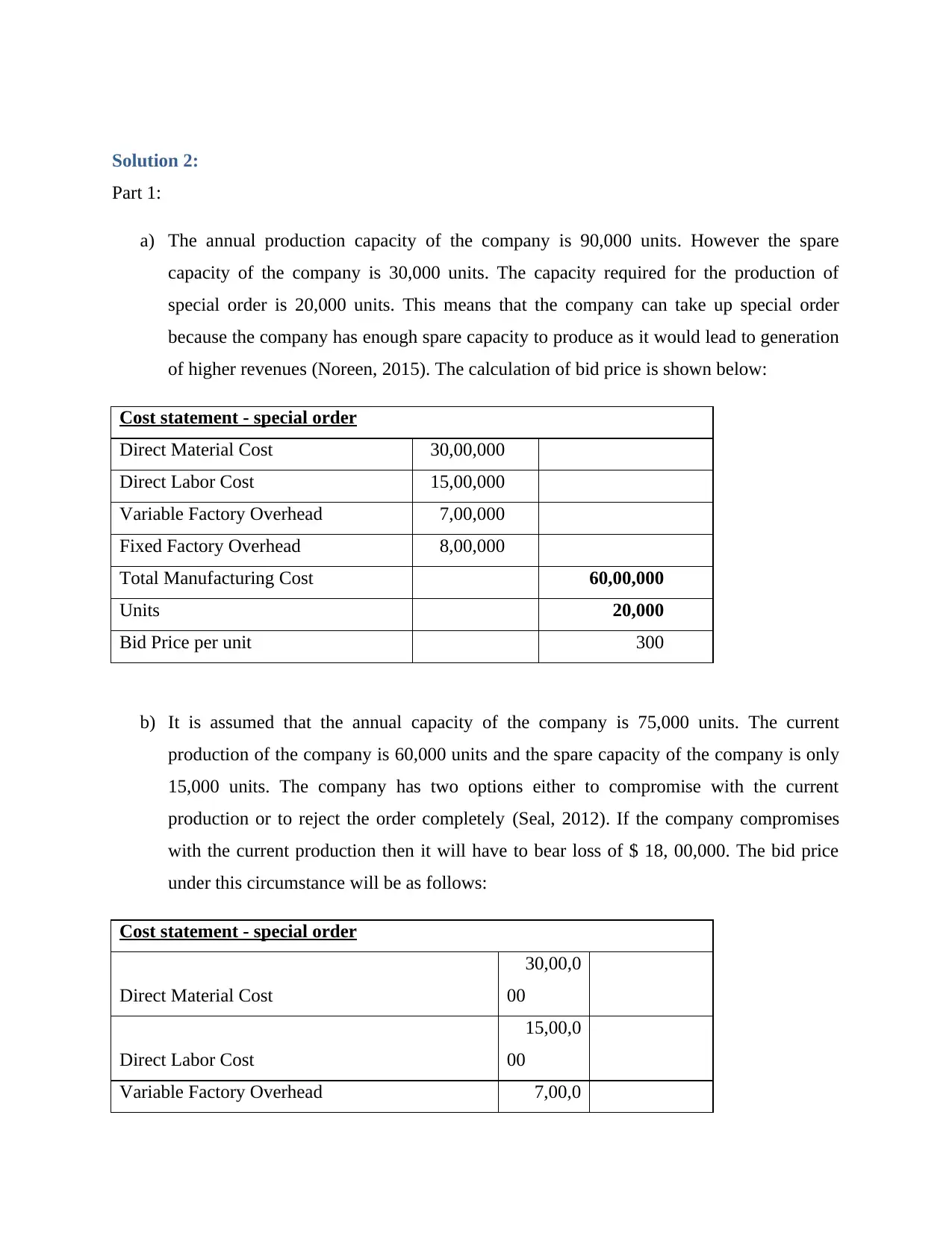

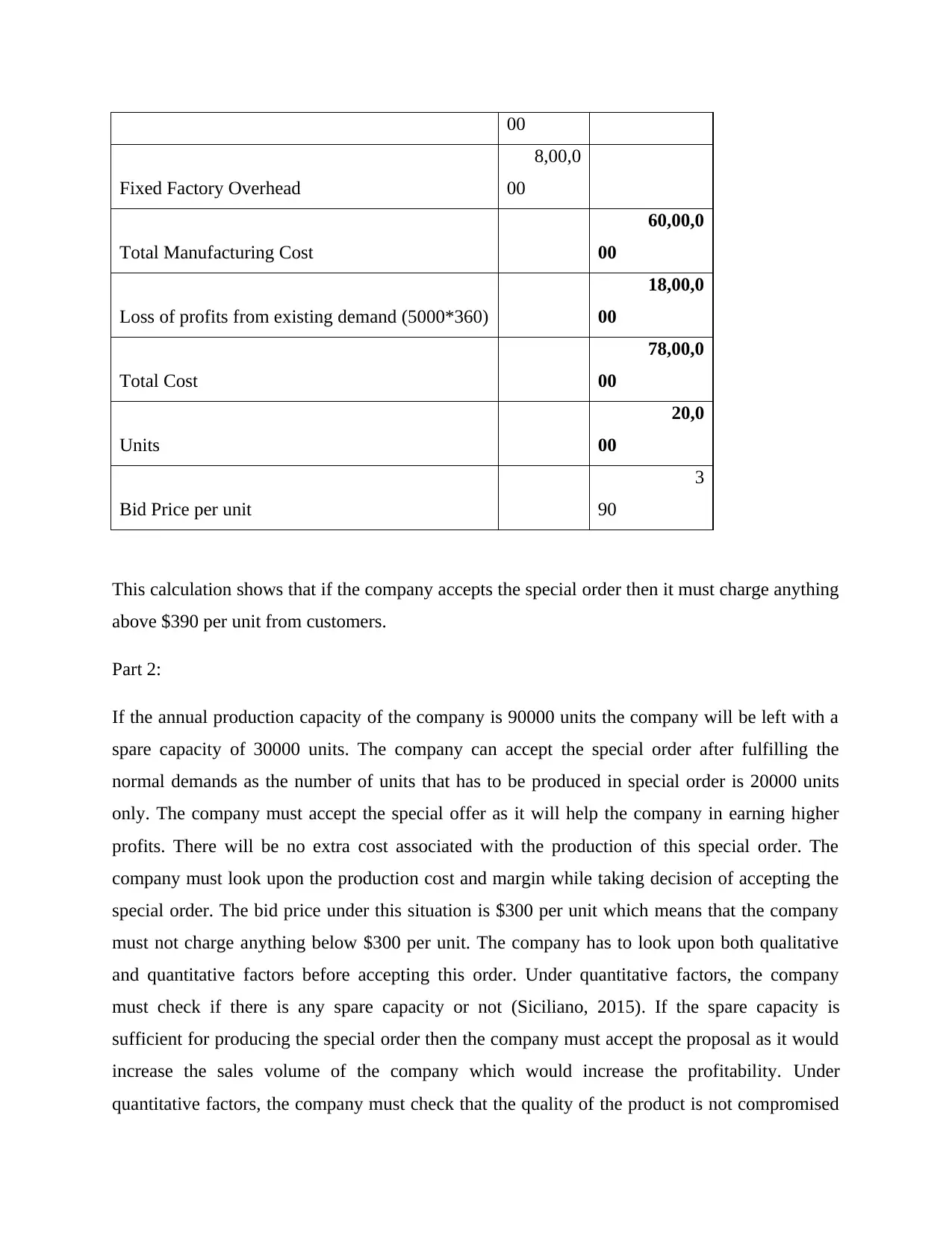

This report analyzes financial data for Pacific Telemet Ltd., focusing on accounting for managers. It examines three proposals for increasing profitability, evaluating sales, costs, and profits under each scenario. The report calculates profits under current circumstances and compares them to the proposed alternatives, considering factors like selling price, variable costs, and advertisement expenses. It also addresses special order decisions, calculating bid prices based on spare capacity and potential profit or loss, considering both quantitative and qualitative factors. The analysis includes cost statements and emphasizes the importance of balancing profitability with product quality and customer satisfaction. The report provides insights into financial decision-making, highlighting the impact of various strategies on the company's financial performance and the importance of considering both quantitative and qualitative factors in pricing and production decisions.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.