Cost Accounting Report: Budgeting, Variance Analysis, and Methods

VerifiedAdded on 2020/01/07

|24

|6987

|215

Report

AI Summary

This report delves into the intricacies of cost accounting, offering a comprehensive overview of various cost types, including material, labor, and overheads, categorized by cost elements and behavior. It examines different costing methods such as job costing, contract costing, and process costing, with a focus on calculating the cost of goods sold using relevant formulas. The report further explores data analysis techniques, specifically highlighting the LIFO (Last-In-First-Out) method for inventory valuation, and provides variance analysis to identify deviations from set targets and suggest remedial actions. Furthermore, the report discusses the significance of budgeting processes, appropriate budgeting methods, and the preparation of cash budgets. It also covers the calculation of variances, the creation of operating statements to reconcile budgeted and actual results, and the presentation of reports to management, culminating in a comprehensive understanding of cost accounting principles and practices for effective financial management.

Question Answer

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................4

TASK 1.................................................................................................................................................4

1.1 Cost types..................................................................................................................................4

1.2 Costing methods........................................................................................................................6

1.3 Calculation of cost of goods sold...............................................................................................6

1.4 Analysis data using appropriate technique.................................................................................7

TASK 2.................................................................................................................................................9

2.1 Cost reports................................................................................................................................9

2.2 Use performance indicators to identify improvements..............................................................9

2.3 Suggest improvement to minimize cost and maximize value and quality...............................11

TASK 3...............................................................................................................................................14

3.1 Nature and purpose of budgeting process................................................................................14

3.2 Appropriate method of budgeting............................................................................................15

3.3 Budget preparation...................................................................................................................16

3.4 Cash budget..............................................................................................................................16

TASK 4...............................................................................................................................................18

4.1 Calculation of variances, reasons and remedial actions..........................................................18

4.2 Operating statement reconciling the budgeted and actual results............................................20

4.3 Presenting report to the management.......................................................................................20

CONCLUSION..................................................................................................................................21

REFERENCES...................................................................................................................................22

2

INTRODUCTION................................................................................................................................4

TASK 1.................................................................................................................................................4

1.1 Cost types..................................................................................................................................4

1.2 Costing methods........................................................................................................................6

1.3 Calculation of cost of goods sold...............................................................................................6

1.4 Analysis data using appropriate technique.................................................................................7

TASK 2.................................................................................................................................................9

2.1 Cost reports................................................................................................................................9

2.2 Use performance indicators to identify improvements..............................................................9

2.3 Suggest improvement to minimize cost and maximize value and quality...............................11

TASK 3...............................................................................................................................................14

3.1 Nature and purpose of budgeting process................................................................................14

3.2 Appropriate method of budgeting............................................................................................15

3.3 Budget preparation...................................................................................................................16

3.4 Cash budget..............................................................................................................................16

TASK 4...............................................................................................................................................18

4.1 Calculation of variances, reasons and remedial actions..........................................................18

4.2 Operating statement reconciling the budgeted and actual results............................................20

4.3 Presenting report to the management.......................................................................................20

CONCLUSION..................................................................................................................................21

REFERENCES...................................................................................................................................22

2

Table of index

Table 1 Inventory valuation through FIFO...........................................................................................6

Table 2 Inventory valuation through FIFO...........................................................................................7

Table 3 Inventory valuation through weighted average method..........................................................7

Table 4 Schedule for expected cash collection for September...........................................................15

Table 5 Expected cash disbursement schedule...................................................................................16

Table 6 Cash budget of Calgon Products for the month of September..............................................16

Table 7 Calculation of variances........................................................................................................18

3

Table 1 Inventory valuation through FIFO...........................................................................................6

Table 2 Inventory valuation through FIFO...........................................................................................7

Table 3 Inventory valuation through weighted average method..........................................................7

Table 4 Schedule for expected cash collection for September...........................................................15

Table 5 Expected cash disbursement schedule...................................................................................16

Table 6 Cash budget of Calgon Products for the month of September..............................................16

Table 7 Calculation of variances........................................................................................................18

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In the present era of competitive age, all the companies either commercial or service-

rendering needs to formulate effective strategies, set policies and targets and make decisions to

sustain in the market. The aim of present assignment is to identify various costs and its accounting

practices to determine total cost. Moreover, the report will present the role of budgetary framework

like production, purchase and cash budget to achieve success. In addition to this, various inventory

valuation techniques like LIFO, FIFO and weighted average will be applied for the valuation of

ending stock. At the end, variance analysis technique will be opted to determine deviations and

make remedial actions to drive success.

TASK 1

1.1 Cost types

The amount of money that G. Chemical Company pays to manufacture, produce and sell its

goods and services into the market is called cost. In other words, cost is the value of sacrifice that

company made to acquire specific quantity of goods in the business (Kaplan. and Atkinson, 2015).

There are different types of costs which can be classified or grouped on different basis,

demonstrated below:

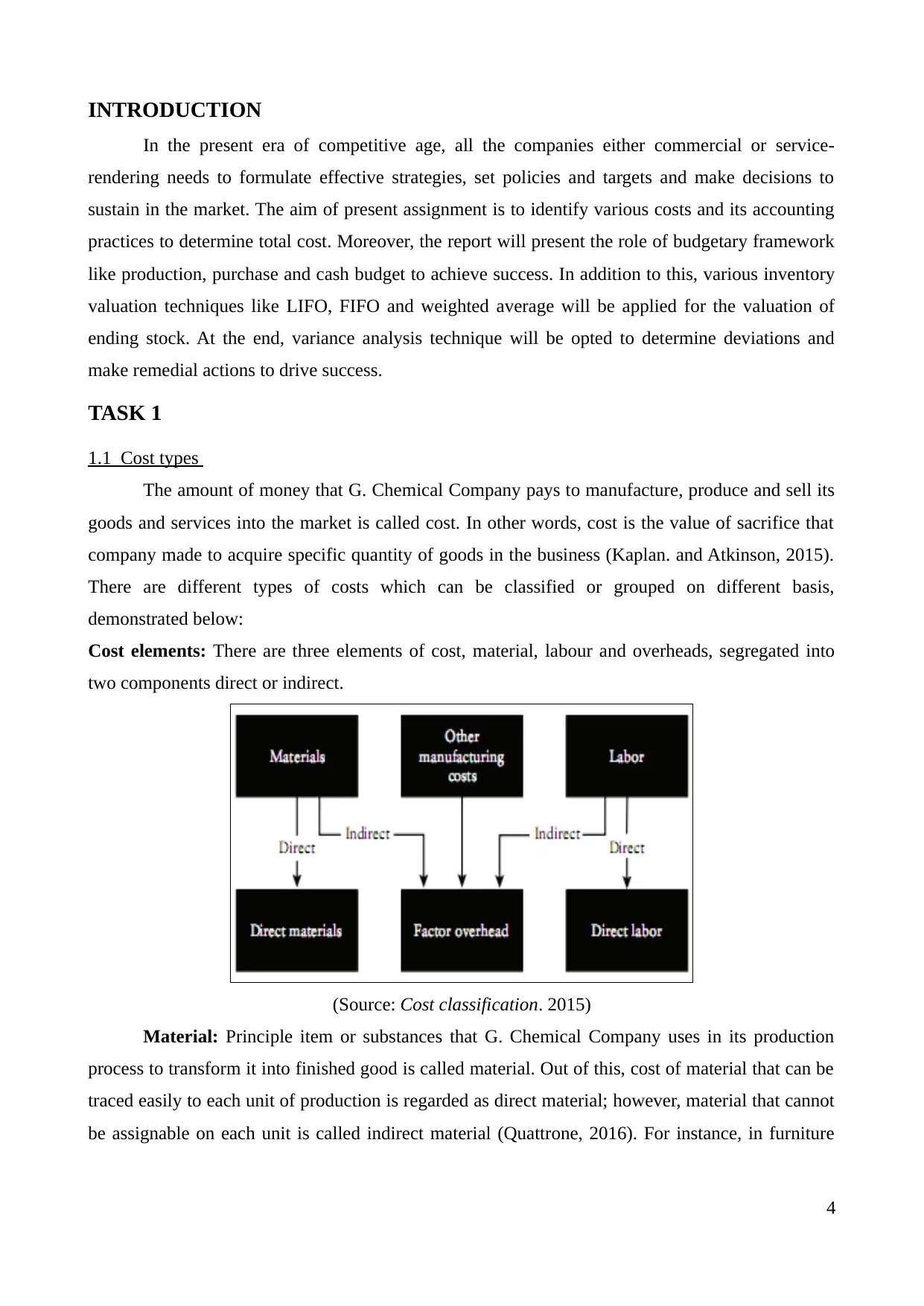

Cost elements: There are three elements of cost, material, labour and overheads, segregated into

two components direct or indirect.

(Source: Cost classification. 2015)

Material: Principle item or substances that G. Chemical Company uses in its production

process to transform it into finished good is called material. Out of this, cost of material that can be

traced easily to each unit of production is regarded as direct material; however, material that cannot

be assignable on each unit is called indirect material (Quattrone, 2016). For instance, in furniture

4

In the present era of competitive age, all the companies either commercial or service-

rendering needs to formulate effective strategies, set policies and targets and make decisions to

sustain in the market. The aim of present assignment is to identify various costs and its accounting

practices to determine total cost. Moreover, the report will present the role of budgetary framework

like production, purchase and cash budget to achieve success. In addition to this, various inventory

valuation techniques like LIFO, FIFO and weighted average will be applied for the valuation of

ending stock. At the end, variance analysis technique will be opted to determine deviations and

make remedial actions to drive success.

TASK 1

1.1 Cost types

The amount of money that G. Chemical Company pays to manufacture, produce and sell its

goods and services into the market is called cost. In other words, cost is the value of sacrifice that

company made to acquire specific quantity of goods in the business (Kaplan. and Atkinson, 2015).

There are different types of costs which can be classified or grouped on different basis,

demonstrated below:

Cost elements: There are three elements of cost, material, labour and overheads, segregated into

two components direct or indirect.

(Source: Cost classification. 2015)

Material: Principle item or substances that G. Chemical Company uses in its production

process to transform it into finished good is called material. Out of this, cost of material that can be

traced easily to each unit of production is regarded as direct material; however, material that cannot

be assignable on each unit is called indirect material (Quattrone, 2016). For instance, in furniture

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

industry, wood will be a direct material, however, screw, bolt, glue will be the part of indirect

material.

Labour: Financial reward for the physical or mental effort put by the labourers to produce a

specified item is called cost of labour (Pettinger, 2012). People who are directly involved in the

manufacturing process is called direct labour, like machine operators. In contrast to this, payments

to labourers that are not directly engaged in production process are known as indirect labour such as

remuneration to supervisor.

Factory Overheads: It includes all the cost pool that G. Chemical Company used to

accumulate indirect material, labour and all the indirect expenses (overheads) which cannot be

traced to specific product such as depreciation, insurance, non-manufacturing overheads, factory

lighting, rent and so on.

Cost behaviour:

Fixed cost: Expenditures that remains constant or do not volatile with the change in output

is called fixed cost, however, with the higher production level, its allocation to each unit got

decreases (Strumickas. and Valanciene, 2015). For instance, insurance, depreciation, office rent and

so on.

Semi-variable cost: Cost of items which represents a minimum fees upto a fixed output and

beyond that level, cost goes increase with the more quantity of production is called semi-variable

cost. For instance, telephone and electricity charges

Variable cost: It directly moves with the same direction of changes in production level is

called variable cost (Cost classification, 2015). For instance, in order to produce more quantity of

item, G. Chemical Company will be require to purchase more material as a variable cost.

Step cost: Cost which fixed proportion rises abruptly at different level of activity is called

step cost. For instance, with the increase in number of subordinates, supervisor will demand more

salary for additional work and increase business cost.

Cost function: In this, expenditures are grouped according to the activity performed, enumerated

hereunder:

Production/manufacturing cost: It consist of expenditures paid for manufacturing a

specified item includes direct material, labour and factory overhead (Messner, 2016).

Administration cost: Payment made by G. Chemical Company to direct, control and

operate regular functioning is called office/administration cost. For instance, staff salary, manager

remuneration, printing, stationery etc.

Marketing: Expenditures which incur by the firm to promote and encourage consumers to

make excessive quantity of purchase is called marketing cost i.e. advertisement and promotional

5

material.

Labour: Financial reward for the physical or mental effort put by the labourers to produce a

specified item is called cost of labour (Pettinger, 2012). People who are directly involved in the

manufacturing process is called direct labour, like machine operators. In contrast to this, payments

to labourers that are not directly engaged in production process are known as indirect labour such as

remuneration to supervisor.

Factory Overheads: It includes all the cost pool that G. Chemical Company used to

accumulate indirect material, labour and all the indirect expenses (overheads) which cannot be

traced to specific product such as depreciation, insurance, non-manufacturing overheads, factory

lighting, rent and so on.

Cost behaviour:

Fixed cost: Expenditures that remains constant or do not volatile with the change in output

is called fixed cost, however, with the higher production level, its allocation to each unit got

decreases (Strumickas. and Valanciene, 2015). For instance, insurance, depreciation, office rent and

so on.

Semi-variable cost: Cost of items which represents a minimum fees upto a fixed output and

beyond that level, cost goes increase with the more quantity of production is called semi-variable

cost. For instance, telephone and electricity charges

Variable cost: It directly moves with the same direction of changes in production level is

called variable cost (Cost classification, 2015). For instance, in order to produce more quantity of

item, G. Chemical Company will be require to purchase more material as a variable cost.

Step cost: Cost which fixed proportion rises abruptly at different level of activity is called

step cost. For instance, with the increase in number of subordinates, supervisor will demand more

salary for additional work and increase business cost.

Cost function: In this, expenditures are grouped according to the activity performed, enumerated

hereunder:

Production/manufacturing cost: It consist of expenditures paid for manufacturing a

specified item includes direct material, labour and factory overhead (Messner, 2016).

Administration cost: Payment made by G. Chemical Company to direct, control and

operate regular functioning is called office/administration cost. For instance, staff salary, manager

remuneration, printing, stationery etc.

Marketing: Expenditures which incur by the firm to promote and encourage consumers to

make excessive quantity of purchase is called marketing cost i.e. advertisement and promotional

5

activities.

1.2 Costing methods

Costing methods: Cost accounting refers to the process of measuring production cost so as

to report accurate amount in the financial statements. It aids in making effective business decisions

to control expenditures and maximizing profitability (Tappura. and et.al., 2015). There is variety of

costing techniques and methods available to G. Chemcial Company to determine their production

cost that are enumerated below:

Job costing: This method is generally used by those organizations who work on number of

jobs and each has unique specification and scope. This method is helpful to measure cost of each

job by accumulating fixed as well as variable expenses. For instance, car repairers and decorators

measure cost by applying this method.

Contract costing: Companies who perform big jobs and require huge money to complete

the contract within a longer period use this method to measure their cost, also called terminal

costing. Constructors who construct bridges, roads, railway platform, apartment and building use

this method.

Batch costing: This method is used to determine the cost of each batch which is uniform in

both the terms of design and nature (Abdelaty. and et.al., 2016). In this, each batch is treated as

separate unit and covering a number of units. For instance, pharmaceutical firms often use this

technique to determine the cost of every batch.

Process costing: Business units in which production of finish goods go through number of

processes used this costing method to examine the cost of each process and transfer it to the next

one to determine their total cost. For instance, clothing industry includes number of stages or

processes like spinning, weaving and converting applied this method.

Unit costing: Organizations which carry out production activities consistently throughout

the year and produce also identical goods prefer unit costing to determine cost of each unit such as

mines and cement works.

1.3 Calculation of cost of goods sold

In manufacturing industry, companies produce goods and services on their own basis and

distribute it into the market to meet their client expectation (Aksenov. and et.al., 2015). Cost of

goods sold includes only the direct expenditures paid for manufacturing a specified quantity of

items, calculated here as under:

COGS = Beginning/opening inventory + purchase – closing inventory

Alternatively, we can say, COGS = Purchase of direct material – purchase return + direct expenses

6

1.2 Costing methods

Costing methods: Cost accounting refers to the process of measuring production cost so as

to report accurate amount in the financial statements. It aids in making effective business decisions

to control expenditures and maximizing profitability (Tappura. and et.al., 2015). There is variety of

costing techniques and methods available to G. Chemcial Company to determine their production

cost that are enumerated below:

Job costing: This method is generally used by those organizations who work on number of

jobs and each has unique specification and scope. This method is helpful to measure cost of each

job by accumulating fixed as well as variable expenses. For instance, car repairers and decorators

measure cost by applying this method.

Contract costing: Companies who perform big jobs and require huge money to complete

the contract within a longer period use this method to measure their cost, also called terminal

costing. Constructors who construct bridges, roads, railway platform, apartment and building use

this method.

Batch costing: This method is used to determine the cost of each batch which is uniform in

both the terms of design and nature (Abdelaty. and et.al., 2016). In this, each batch is treated as

separate unit and covering a number of units. For instance, pharmaceutical firms often use this

technique to determine the cost of every batch.

Process costing: Business units in which production of finish goods go through number of

processes used this costing method to examine the cost of each process and transfer it to the next

one to determine their total cost. For instance, clothing industry includes number of stages or

processes like spinning, weaving and converting applied this method.

Unit costing: Organizations which carry out production activities consistently throughout

the year and produce also identical goods prefer unit costing to determine cost of each unit such as

mines and cement works.

1.3 Calculation of cost of goods sold

In manufacturing industry, companies produce goods and services on their own basis and

distribute it into the market to meet their client expectation (Aksenov. and et.al., 2015). Cost of

goods sold includes only the direct expenditures paid for manufacturing a specified quantity of

items, calculated here as under:

COGS = Beginning/opening inventory + purchase – closing inventory

Alternatively, we can say, COGS = Purchase of direct material – purchase return + direct expenses

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Octroi, customer duty, carriage inward)

For instance,

Opening stock – 25,000

Purchase – 100,000

Closing stock – 30000

COGS = 25,000 + 100,000 – 30,000

= 95,000

It is important for the company to measure COGS so as to determine gross margin by

subtracting it from the total turnover. G. Chemcial Company needs to execute effective control over

direct spending so as to maximize their gross profit.

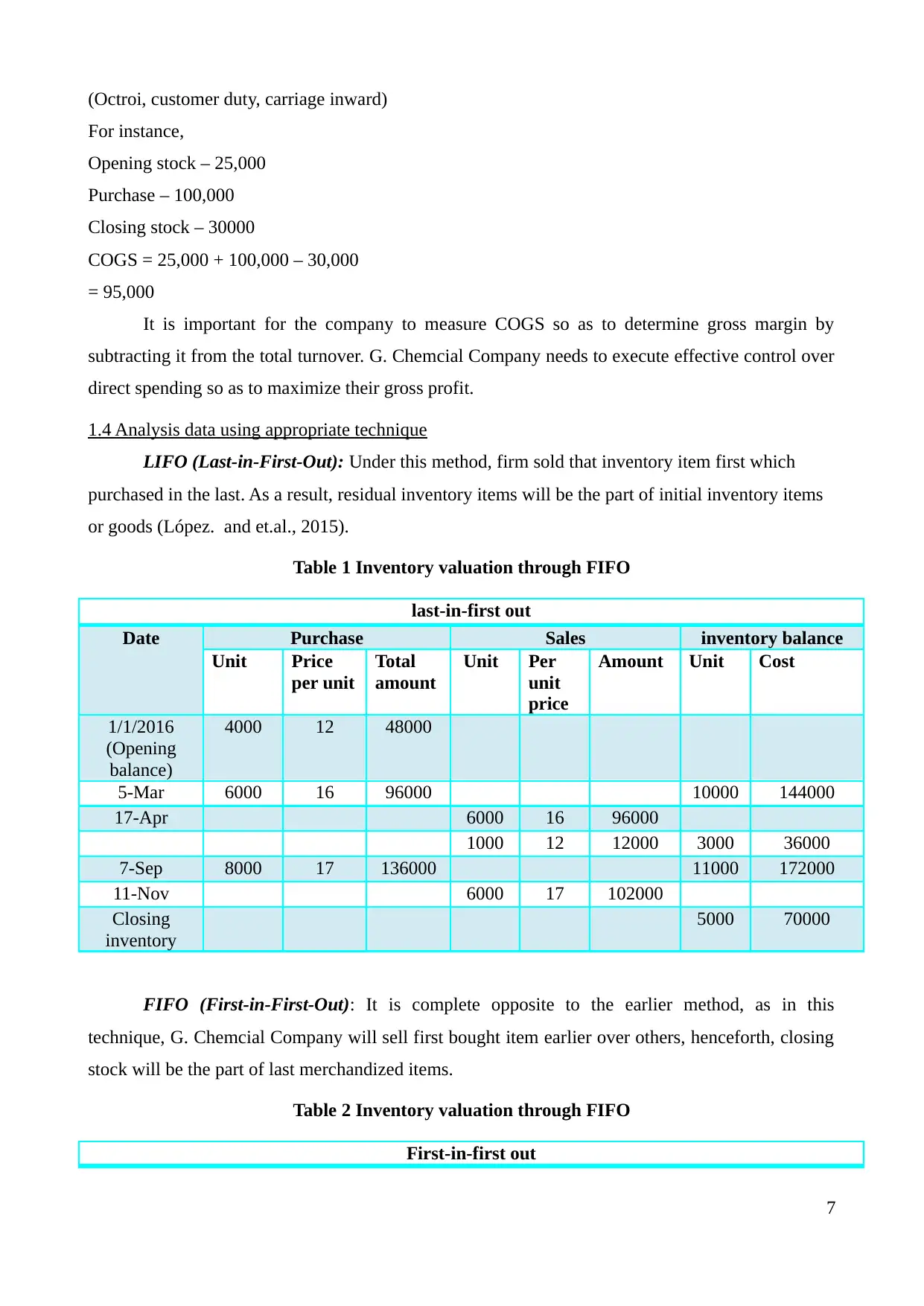

1.4 Analysis data using appropriate technique

LIFO (Last-in-First-Out): Under this method, firm sold that inventory item first which

purchased in the last. As a result, residual inventory items will be the part of initial inventory items

or goods (López. and et.al., 2015).

Table 1 Inventory valuation through FIFO

last-in-first out

Date Purchase Sales inventory balance

Unit Price

per unit

Total

amount

Unit Per

unit

price

Amount Unit Cost

1/1/2016

(Opening

balance)

4000 12 48000

5-Mar 6000 16 96000 10000 144000

17-Apr 6000 16 96000

1000 12 12000 3000 36000

7-Sep 8000 17 136000 11000 172000

11-Nov 6000 17 102000

Closing

inventory

5000 70000

FIFO (First-in-First-Out): It is complete opposite to the earlier method, as in this

technique, G. Chemcial Company will sell first bought item earlier over others, henceforth, closing

stock will be the part of last merchandized items.

Table 2 Inventory valuation through FIFO

First-in-first out

7

For instance,

Opening stock – 25,000

Purchase – 100,000

Closing stock – 30000

COGS = 25,000 + 100,000 – 30,000

= 95,000

It is important for the company to measure COGS so as to determine gross margin by

subtracting it from the total turnover. G. Chemcial Company needs to execute effective control over

direct spending so as to maximize their gross profit.

1.4 Analysis data using appropriate technique

LIFO (Last-in-First-Out): Under this method, firm sold that inventory item first which

purchased in the last. As a result, residual inventory items will be the part of initial inventory items

or goods (López. and et.al., 2015).

Table 1 Inventory valuation through FIFO

last-in-first out

Date Purchase Sales inventory balance

Unit Price

per unit

Total

amount

Unit Per

unit

price

Amount Unit Cost

1/1/2016

(Opening

balance)

4000 12 48000

5-Mar 6000 16 96000 10000 144000

17-Apr 6000 16 96000

1000 12 12000 3000 36000

7-Sep 8000 17 136000 11000 172000

11-Nov 6000 17 102000

Closing

inventory

5000 70000

FIFO (First-in-First-Out): It is complete opposite to the earlier method, as in this

technique, G. Chemcial Company will sell first bought item earlier over others, henceforth, closing

stock will be the part of last merchandized items.

Table 2 Inventory valuation through FIFO

First-in-first out

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Date Purchase Sales Inventory balance

Unit Price per

unit

Total

amount

Unit Per

unit

pric

e

Amou

nt

Unit Cost

1/1/2016

(Opening

balance)

4000 12 48000

5-Mar 6000 16 96000 10000 144000

17-Apr 4000 12 48000

3000 16 48000 3000 48000

7-Sep 8000 17 136000 11000 184000

11-Nov 3000 16 48000

3000 17 51000

Closing

inventory

5000 85000

Weighted Average method: This inventory method is considered more suitable and

appropriate as this method consider all the quantity purchased along with their respective prices and

use weighted cost per unit for inventory valuation (Duan. and Ding, 2016).

Table 3 Inventory valuation through weighted average method

Weighted average method

Date Purchase Sales Inventory

balance

Unit Price

per

unit

Total

amount

Unit Per

unit

price

Amount Unit WACC

per unit

Weighted

average cost

1/1/2016

(Opening

balance)

4000 12 48000

5-Mar 6000 16 96000 10000 14.4 144000

17-Apr 7000 14.4 100800 3000 14.4 43200

7-Sep 8000 17 136000 11000 16.29 179200

11-Nov 6000 16.29 97745.45

Closing inventory 5000 34.84 174200

TASK 2

2.1 Cost reports

Cost reports represent a summary of key statistics about different types of variable and

fixed cost such as material, labour, variable and fixed overheads, prepared underneath:

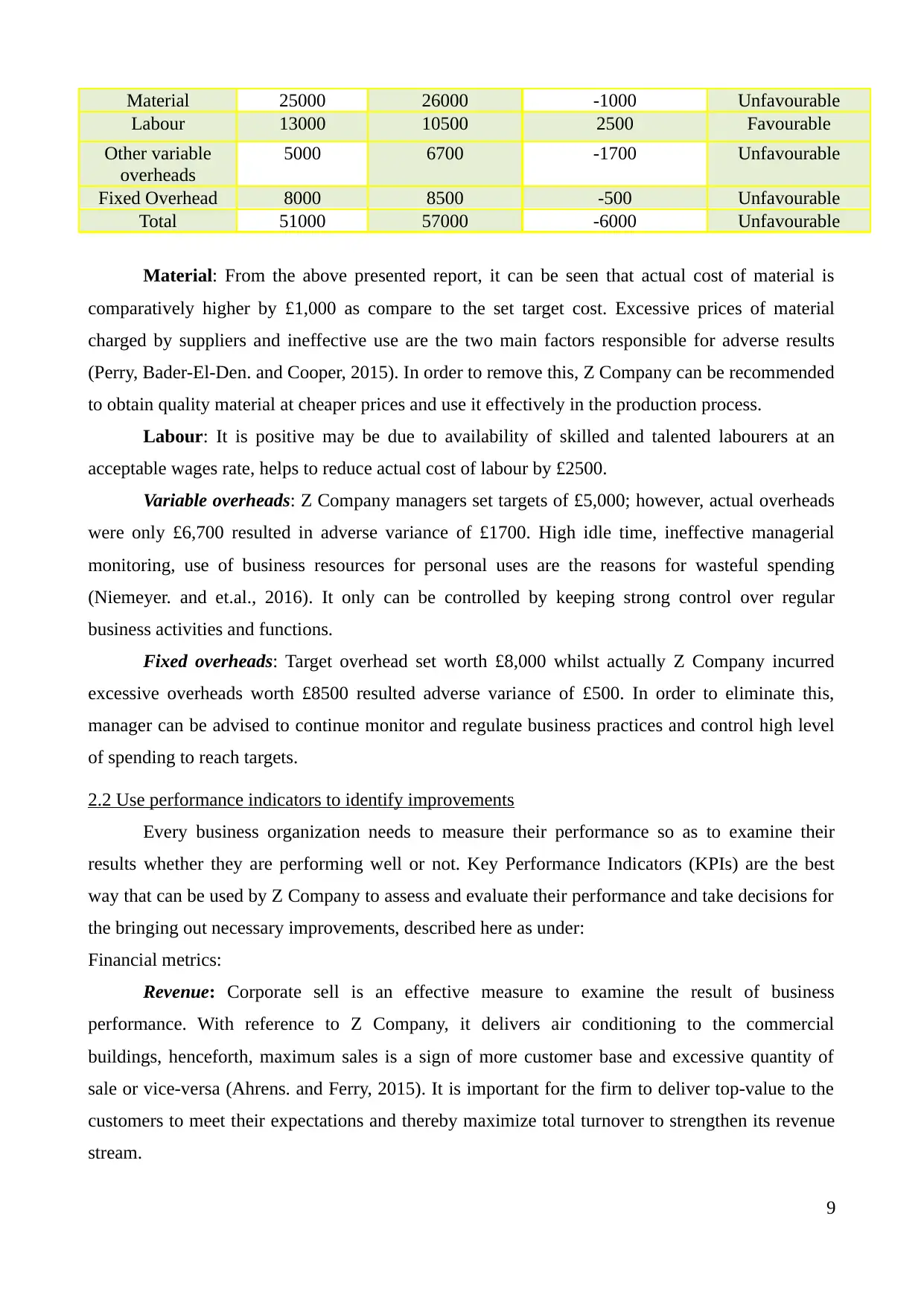

Particular Budgeted cost Actual cost Variance Type

8

Unit Price per

unit

Total

amount

Unit Per

unit

pric

e

Amou

nt

Unit Cost

1/1/2016

(Opening

balance)

4000 12 48000

5-Mar 6000 16 96000 10000 144000

17-Apr 4000 12 48000

3000 16 48000 3000 48000

7-Sep 8000 17 136000 11000 184000

11-Nov 3000 16 48000

3000 17 51000

Closing

inventory

5000 85000

Weighted Average method: This inventory method is considered more suitable and

appropriate as this method consider all the quantity purchased along with their respective prices and

use weighted cost per unit for inventory valuation (Duan. and Ding, 2016).

Table 3 Inventory valuation through weighted average method

Weighted average method

Date Purchase Sales Inventory

balance

Unit Price

per

unit

Total

amount

Unit Per

unit

price

Amount Unit WACC

per unit

Weighted

average cost

1/1/2016

(Opening

balance)

4000 12 48000

5-Mar 6000 16 96000 10000 14.4 144000

17-Apr 7000 14.4 100800 3000 14.4 43200

7-Sep 8000 17 136000 11000 16.29 179200

11-Nov 6000 16.29 97745.45

Closing inventory 5000 34.84 174200

TASK 2

2.1 Cost reports

Cost reports represent a summary of key statistics about different types of variable and

fixed cost such as material, labour, variable and fixed overheads, prepared underneath:

Particular Budgeted cost Actual cost Variance Type

8

Material 25000 26000 -1000 Unfavourable

Labour 13000 10500 2500 Favourable

Other variable

overheads

5000 6700 -1700 Unfavourable

Fixed Overhead 8000 8500 -500 Unfavourable

Total 51000 57000 -6000 Unfavourable

Material: From the above presented report, it can be seen that actual cost of material is

comparatively higher by £1,000 as compare to the set target cost. Excessive prices of material

charged by suppliers and ineffective use are the two main factors responsible for adverse results

(Perry, Bader-El-Den. and Cooper, 2015). In order to remove this, Z Company can be recommended

to obtain quality material at cheaper prices and use it effectively in the production process.

Labour: It is positive may be due to availability of skilled and talented labourers at an

acceptable wages rate, helps to reduce actual cost of labour by £2500.

Variable overheads: Z Company managers set targets of £5,000; however, actual overheads

were only £6,700 resulted in adverse variance of £1700. High idle time, ineffective managerial

monitoring, use of business resources for personal uses are the reasons for wasteful spending

(Niemeyer. and et.al., 2016). It only can be controlled by keeping strong control over regular

business activities and functions.

Fixed overheads: Target overhead set worth £8,000 whilst actually Z Company incurred

excessive overheads worth £8500 resulted adverse variance of £500. In order to eliminate this,

manager can be advised to continue monitor and regulate business practices and control high level

of spending to reach targets.

2.2 Use performance indicators to identify improvements

Every business organization needs to measure their performance so as to examine their

results whether they are performing well or not. Key Performance Indicators (KPIs) are the best

way that can be used by Z Company to assess and evaluate their performance and take decisions for

the bringing out necessary improvements, described here as under:

Financial metrics:

Revenue: Corporate sell is an effective measure to examine the result of business

performance. With reference to Z Company, it delivers air conditioning to the commercial

buildings, henceforth, maximum sales is a sign of more customer base and excessive quantity of

sale or vice-versa (Ahrens. and Ferry, 2015). It is important for the firm to deliver top-value to the

customers to meet their expectations and thereby maximize total turnover to strengthen its revenue

stream.

9

Labour 13000 10500 2500 Favourable

Other variable

overheads

5000 6700 -1700 Unfavourable

Fixed Overhead 8000 8500 -500 Unfavourable

Total 51000 57000 -6000 Unfavourable

Material: From the above presented report, it can be seen that actual cost of material is

comparatively higher by £1,000 as compare to the set target cost. Excessive prices of material

charged by suppliers and ineffective use are the two main factors responsible for adverse results

(Perry, Bader-El-Den. and Cooper, 2015). In order to remove this, Z Company can be recommended

to obtain quality material at cheaper prices and use it effectively in the production process.

Labour: It is positive may be due to availability of skilled and talented labourers at an

acceptable wages rate, helps to reduce actual cost of labour by £2500.

Variable overheads: Z Company managers set targets of £5,000; however, actual overheads

were only £6,700 resulted in adverse variance of £1700. High idle time, ineffective managerial

monitoring, use of business resources for personal uses are the reasons for wasteful spending

(Niemeyer. and et.al., 2016). It only can be controlled by keeping strong control over regular

business activities and functions.

Fixed overheads: Target overhead set worth £8,000 whilst actually Z Company incurred

excessive overheads worth £8500 resulted adverse variance of £500. In order to eliminate this,

manager can be advised to continue monitor and regulate business practices and control high level

of spending to reach targets.

2.2 Use performance indicators to identify improvements

Every business organization needs to measure their performance so as to examine their

results whether they are performing well or not. Key Performance Indicators (KPIs) are the best

way that can be used by Z Company to assess and evaluate their performance and take decisions for

the bringing out necessary improvements, described here as under:

Financial metrics:

Revenue: Corporate sell is an effective measure to examine the result of business

performance. With reference to Z Company, it delivers air conditioning to the commercial

buildings, henceforth, maximum sales is a sign of more customer base and excessive quantity of

sale or vice-versa (Ahrens. and Ferry, 2015). It is important for the firm to deliver top-value to the

customers to meet their expectations and thereby maximize total turnover to strengthen its revenue

stream.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost: Total corporate spending or expenditures for producing, distributing and marketing the

goods or services is regarded as business cost. Continuous cost increase without any increase in

production volume or slightly improvement is a sign of poor performance; however, effective

control is a sign of stronger managerial control.

Profitability: Surplus remains after subtracting total cost from the revenue generated is also

an effective measure (Parmenter, 2015). Rapid growth is considered good as it indicates that Z

Company is carrying out their regular functioning in well manner and acquiring better yield or vice-

versa.

Customer Metrics:

Customer satisfaction and retention rate: Every company operates in the market to satisfy

their target customer demand and thereby gain maximum return. Regular buying, repetitive

purchasing and customer loyalty deliberately indicates that use group are satisfied. It help firm to

retain their existing consumer base for a longer duration and attract potential clients as well.

Consumer lifetime value: CLV helps to measure total worth to establish a long-term

relationship with the target audiences (Johnes, 2016). It facilitates managers to gain loyal

customers at best prices.

Number of customers: It is a straightforward indicator that can be used by Z Company to

determine their target customers. Rising or rapid growth in domestic as well as foreign customers is

a sign of performance improvement, however, in case of declined customer base; managers need to

make better policies and decisions for enhancing their user group.

People Metrics:

Employee Turnover rate: Employees are the base of business success as they drive more

customers by delivering excellent and top quality services (Feiz, and et.al., 2015). High turnover is

a negative indicator towards performance makes it essential for the business unit to examine their

workplace culture, staff salary, motivation practices and individual behaviour so as to eliminate

adverse situations.

Employee satisfaction: Highly-motivated and committed workers work hard and put their

increased efforts to complete assigned duties in the best possible manner. Satisfied employees work

with greater efficiency and have capability to render best services to the final users. Thus, it

becomes essential for the Z Company to satisfy their workers to drive stronger revenue stream by

offering them better salary, motivation, training and welfare activities.

Process Metrics:

Product defects: Rising consumer complaints about defective items and worst quality of

goods is an indicator of poor performance (Podgórski, 2015). However, minimizing defect rate

10

goods or services is regarded as business cost. Continuous cost increase without any increase in

production volume or slightly improvement is a sign of poor performance; however, effective

control is a sign of stronger managerial control.

Profitability: Surplus remains after subtracting total cost from the revenue generated is also

an effective measure (Parmenter, 2015). Rapid growth is considered good as it indicates that Z

Company is carrying out their regular functioning in well manner and acquiring better yield or vice-

versa.

Customer Metrics:

Customer satisfaction and retention rate: Every company operates in the market to satisfy

their target customer demand and thereby gain maximum return. Regular buying, repetitive

purchasing and customer loyalty deliberately indicates that use group are satisfied. It help firm to

retain their existing consumer base for a longer duration and attract potential clients as well.

Consumer lifetime value: CLV helps to measure total worth to establish a long-term

relationship with the target audiences (Johnes, 2016). It facilitates managers to gain loyal

customers at best prices.

Number of customers: It is a straightforward indicator that can be used by Z Company to

determine their target customers. Rising or rapid growth in domestic as well as foreign customers is

a sign of performance improvement, however, in case of declined customer base; managers need to

make better policies and decisions for enhancing their user group.

People Metrics:

Employee Turnover rate: Employees are the base of business success as they drive more

customers by delivering excellent and top quality services (Feiz, and et.al., 2015). High turnover is

a negative indicator towards performance makes it essential for the business unit to examine their

workplace culture, staff salary, motivation practices and individual behaviour so as to eliminate

adverse situations.

Employee satisfaction: Highly-motivated and committed workers work hard and put their

increased efforts to complete assigned duties in the best possible manner. Satisfied employees work

with greater efficiency and have capability to render best services to the final users. Thus, it

becomes essential for the Z Company to satisfy their workers to drive stronger revenue stream by

offering them better salary, motivation, training and welfare activities.

Process Metrics:

Product defects: Rising consumer complaints about defective items and worst quality of

goods is an indicator of poor performance (Podgórski, 2015). However, minimizing defect rate

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

helps to increase satisfaction level of the users and meet people desires and expectations.

Technological advancement: Better and advanced use of technological equipments,

machinery and other helps to maximize operational efficiency and minimize cost.

2.3 Suggest improvement to minimize cost and maximize value and quality

Looking at the modern era of changing market conditions and intense competitive edge,

companies like Z Company and other requires reducing their business cost and improving quality

and worth to sustain in the market.

Ways to minimize cost:

One of the best ways to curtail business cost is to execute effective managerial control and

monitoring over regular business activities and operations (Bahadur, and et.al., 2016). With

the help of this, managers can easily identify the responsible reasons for higher cost and take

immediate actions to mitigate the same.

Z Company’s purchase departmental manager should search for suppliers either domestic or

international so as to bought material at cheaper rates.

Company also can be advised to recruit highly-committed, motivated, talented and capable

workforce to deliver best value to the customers at an affordable cost of wages.

Technological advancement is also an effective way to maximize operational efficiency and

reduce cost (Bieńkowska, Kral. and Zabłocka-Kluczka, 201).

Managers need to effectively allocate their business resource in various functional areas and

also execute effective control to manage it.

Recycling wastage and scrap by reuse also helps to eliminate excessive wastage and curtail

cost. Various cost-management strategies can be used such as increasing the level of output helps

to reduce allocation of cost to each unit and maximize return on each item.

Ways to maximize value and quality: Investment in training: Z Company’s executives and directors can conduct training and

development sessions for maximizing their workers skills and competency level and thereby

deliver top-quality value to the users. Quality improvement techniques: Firm can opt for Total Quality Management (TQM)

approach, in which, it can focuses on each activity, production process and functions and

bring significant level of improvements to improve quality. Moreover, quality circles and six

sigma techniques are also some alternatives available to the firm to remove defects and

perform quality work to meet people demand.

11

Technological advancement: Better and advanced use of technological equipments,

machinery and other helps to maximize operational efficiency and minimize cost.

2.3 Suggest improvement to minimize cost and maximize value and quality

Looking at the modern era of changing market conditions and intense competitive edge,

companies like Z Company and other requires reducing their business cost and improving quality

and worth to sustain in the market.

Ways to minimize cost:

One of the best ways to curtail business cost is to execute effective managerial control and

monitoring over regular business activities and operations (Bahadur, and et.al., 2016). With

the help of this, managers can easily identify the responsible reasons for higher cost and take

immediate actions to mitigate the same.

Z Company’s purchase departmental manager should search for suppliers either domestic or

international so as to bought material at cheaper rates.

Company also can be advised to recruit highly-committed, motivated, talented and capable

workforce to deliver best value to the customers at an affordable cost of wages.

Technological advancement is also an effective way to maximize operational efficiency and

reduce cost (Bieńkowska, Kral. and Zabłocka-Kluczka, 201).

Managers need to effectively allocate their business resource in various functional areas and

also execute effective control to manage it.

Recycling wastage and scrap by reuse also helps to eliminate excessive wastage and curtail

cost. Various cost-management strategies can be used such as increasing the level of output helps

to reduce allocation of cost to each unit and maximize return on each item.

Ways to maximize value and quality: Investment in training: Z Company’s executives and directors can conduct training and

development sessions for maximizing their workers skills and competency level and thereby

deliver top-quality value to the users. Quality improvement techniques: Firm can opt for Total Quality Management (TQM)

approach, in which, it can focuses on each activity, production process and functions and

bring significant level of improvements to improve quality. Moreover, quality circles and six

sigma techniques are also some alternatives available to the firm to remove defects and

perform quality work to meet people demand.

11

Maximize yield: Loyal customers are willing to pay higher or premium charges for the

supplied goods and services and help Z Company to maximize their net earnings. With the

help of getting more and more return, entities will be able to deliver improved return to the

investors and satisfying their expectation about return. Product differentiation, strong

revenue stream, controlled cost, existence into foreign market, introduction of unique

product and services are the best strategies available to company to enhance their net yield

or earnings (Lanis. and Richardson, 2016).

Competitive advantage, strategic capabilities and sustainable benefits also assist business

unit to fulfill investors’ expectations by delivering them increased value and worth.

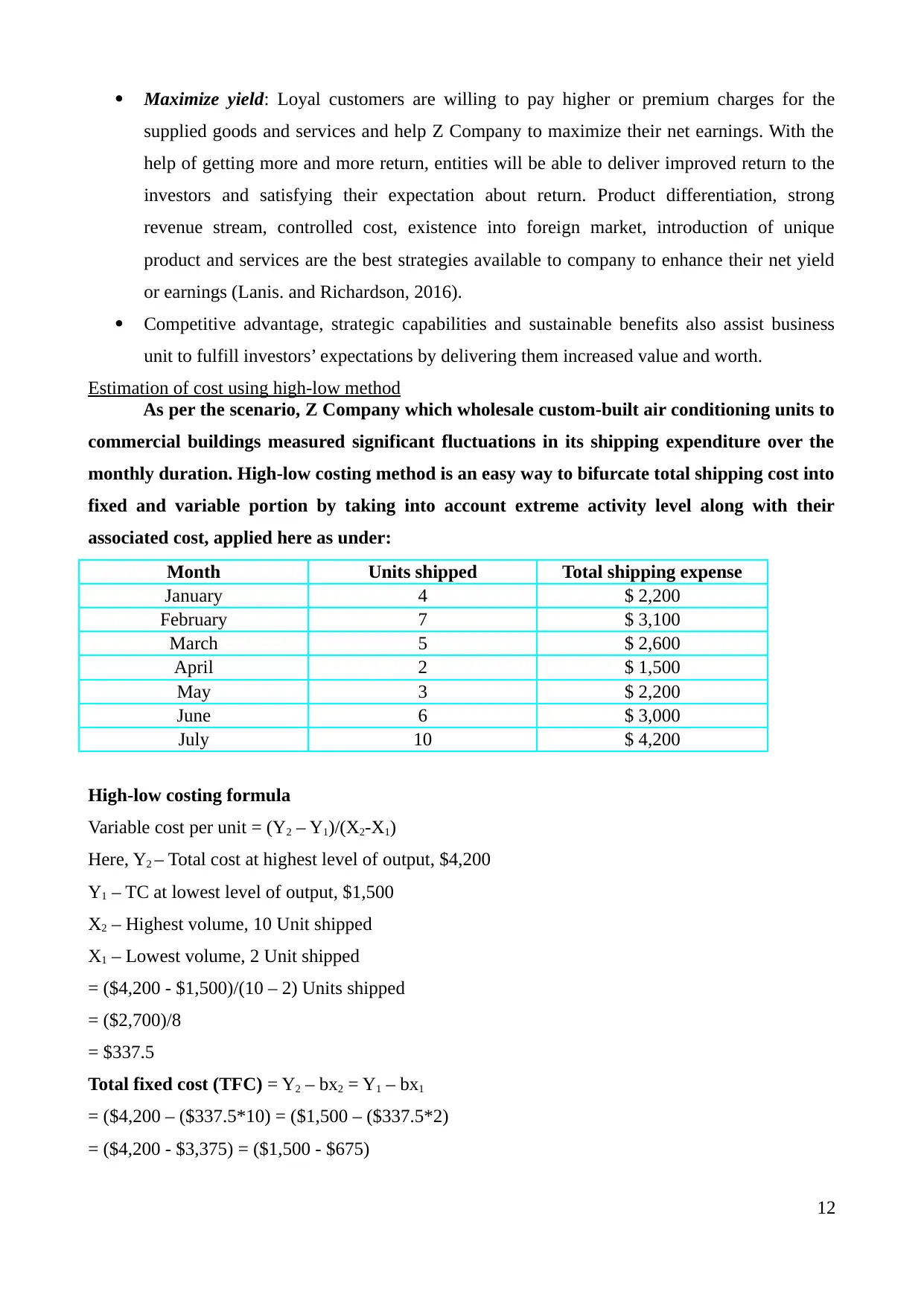

Estimation of cost using high-low method

As per the scenario, Z Company which wholesale custom-built air conditioning units to

commercial buildings measured significant fluctuations in its shipping expenditure over the

monthly duration. High-low costing method is an easy way to bifurcate total shipping cost into

fixed and variable portion by taking into account extreme activity level along with their

associated cost, applied here as under:

Month Units shipped Total shipping expense

January 4 $ 2,200

February 7 $ 3,100

March 5 $ 2,600

April 2 $ 1,500

May 3 $ 2,200

June 6 $ 3,000

July 10 $ 4,200

High-low costing formula

Variable cost per unit = (Y2 – Y1)/(X2-X1)

Here, Y2 – Total cost at highest level of output, $4,200

Y1 – TC at lowest level of output, $1,500

X2 – Highest volume, 10 Unit shipped

X1 – Lowest volume, 2 Unit shipped

= ($4,200 - $1,500)/(10 – 2) Units shipped

= ($2,700)/8

= $337.5

Total fixed cost (TFC) = Y2 – bx2 = Y1 – bx1

= ($4,200 – ($337.5*10) = ($1,500 – ($337.5*2)

= ($4,200 - $3,375) = ($1,500 - $675)

12

supplied goods and services and help Z Company to maximize their net earnings. With the

help of getting more and more return, entities will be able to deliver improved return to the

investors and satisfying their expectation about return. Product differentiation, strong

revenue stream, controlled cost, existence into foreign market, introduction of unique

product and services are the best strategies available to company to enhance their net yield

or earnings (Lanis. and Richardson, 2016).

Competitive advantage, strategic capabilities and sustainable benefits also assist business

unit to fulfill investors’ expectations by delivering them increased value and worth.

Estimation of cost using high-low method

As per the scenario, Z Company which wholesale custom-built air conditioning units to

commercial buildings measured significant fluctuations in its shipping expenditure over the

monthly duration. High-low costing method is an easy way to bifurcate total shipping cost into

fixed and variable portion by taking into account extreme activity level along with their

associated cost, applied here as under:

Month Units shipped Total shipping expense

January 4 $ 2,200

February 7 $ 3,100

March 5 $ 2,600

April 2 $ 1,500

May 3 $ 2,200

June 6 $ 3,000

July 10 $ 4,200

High-low costing formula

Variable cost per unit = (Y2 – Y1)/(X2-X1)

Here, Y2 – Total cost at highest level of output, $4,200

Y1 – TC at lowest level of output, $1,500

X2 – Highest volume, 10 Unit shipped

X1 – Lowest volume, 2 Unit shipped

= ($4,200 - $1,500)/(10 – 2) Units shipped

= ($2,700)/8

= $337.5

Total fixed cost (TFC) = Y2 – bx2 = Y1 – bx1

= ($4,200 – ($337.5*10) = ($1,500 – ($337.5*2)

= ($4,200 - $3,375) = ($1,500 - $675)

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.