Comparative Study: Cost Accounting Methods in Manufacturing Companies

VerifiedAdded on 2023/05/27

|26

|8219

|162

Report

AI Summary

This report examines the transition from traditional to modern cost accounting methods within manufacturing companies. It begins by outlining the limitations of traditional methods, which were developed in the mid-20th century and focused on manufacturing costs and overhead allocation, in the face of modern challenges such as technological advancements, changing consumer preferences, and global competition. The paper then introduces modern cost accounting methods, emphasizing their focus on cost rationalization and reduction. It highlights the importance of these methods in providing management with accurate information on product, project, and activity effectiveness. The report discusses Activity-Based Costing (ABC) as a key modern method, emphasizing its role in more accurately determining product profitability. Furthermore, it stresses that modern methods should be applied alongside traditional methods for a comprehensive understanding of costs across both short-term and long-term perspectives, including the entire product life cycle. The report also touches upon the core elements of costing systems, different types of costing systems like job order, process, and ABC, and the cost allocation in both traditional and ABC systems, including the importance of selecting appropriate cost drivers.

155

Movement From Traditional to Modern

Cost Accounting Methods in

Manufacturing Companies (*)

Hrvoje Perčević

University of Zagreb, Croatia

Mirjana Hladika

University of Zagreb, Croatia

Abstract

Significant changes in business environment at the e

the beginning of 21st century enable the development and

cost accounting methods which main purpose is to give

management regarding the effectiveness of certain products,

consumers, responsibility centres etc. Traditional cost accounting

developed in the middle of 20th century due to the

focus of traditional cost accounting methods was on

of indirect manufacturing costs allocation to products or

development of technology, changes in consumer’s preferences, g

face modern manufacturing companies with permanent challenges

the global market. Traditional cost accounting methods are no l

modern business conditions, because cost accounting methods

potential areas in companies where are possible cost savings. Therefor

cost accounting methods are focused on cost rationalization

since modern manufacturing companies cannot effect on market prices

effect on their costs. In current business conditions, modern cost a

(*) Bu Araştırma, 19-22 Haziran 2013 tarihinde İstanbul’da yapılan 3rd

International Conference on Luca Pacioli in Accounting History’de ve 3rd Balkans

and Middle East Countries Conference on Accounting and Accounting History

(3 BMAC) Konferansı’nda bildiri olarak sunulmuştur.

Movement From Traditional to Modern

Cost Accounting Methods in

Manufacturing Companies (*)

Hrvoje Perčević

University of Zagreb, Croatia

Mirjana Hladika

University of Zagreb, Croatia

Abstract

Significant changes in business environment at the e

the beginning of 21st century enable the development and

cost accounting methods which main purpose is to give

management regarding the effectiveness of certain products,

consumers, responsibility centres etc. Traditional cost accounting

developed in the middle of 20th century due to the

focus of traditional cost accounting methods was on

of indirect manufacturing costs allocation to products or

development of technology, changes in consumer’s preferences, g

face modern manufacturing companies with permanent challenges

the global market. Traditional cost accounting methods are no l

modern business conditions, because cost accounting methods

potential areas in companies where are possible cost savings. Therefor

cost accounting methods are focused on cost rationalization

since modern manufacturing companies cannot effect on market prices

effect on their costs. In current business conditions, modern cost a

(*) Bu Araştırma, 19-22 Haziran 2013 tarihinde İstanbul’da yapılan 3rd

International Conference on Luca Pacioli in Accounting History’de ve 3rd Balkans

and Middle East Countries Conference on Accounting and Accounting History

(3 BMAC) Konferansı’nda bildiri olarak sunulmuştur.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

156

are more appropriate while they are focused on the total

product life cycle. This paper deals with the modern cost accounti

their application in manufacturing companies. The results are s

cost accounting methods enables more confidential determination of t

profitability. But it is also important to state that r

cost accounting methods should be applied together with traditional c

methods. Traditional cost accounting methods give informat

short term, while modern methods are orientated on longer period (

product life cycle).

Key words: Traditional Cost AccountingMethods, Modern Cost Accounting

Methods, ABC, Target Costing, Life Cycle Costing, Product Profitability.

Jel Classificiation: M21, M4A, M51

1. Introduction

The basic purpose of costing systems is to

product or service by assigning manufacturing costs to products

that company produces or provides. Costing system

accounting methods used in order to define the cost

methods used in costing system enable the evaluation of p

from the manufacturing process. It is important to

costing systems differently affect the product evaluation.

costing system was based on the type of the production p

job order costing was used in job order production, while

was applied in process or mass production. Today, these two c

are considered as traditional costing systemswhich are no l

use in modern operating conditions. Business conditions a

becoming more and more complex. Manufacturing processes

production companies are almost fully automated and compute

process of manufacturing automation and computerization causes s

change in manufacturing cost structure. The most important c

modern manufacturing cost structure becomes indirect manufac

are more appropriate while they are focused on the total

product life cycle. This paper deals with the modern cost accounti

their application in manufacturing companies. The results are s

cost accounting methods enables more confidential determination of t

profitability. But it is also important to state that r

cost accounting methods should be applied together with traditional c

methods. Traditional cost accounting methods give informat

short term, while modern methods are orientated on longer period (

product life cycle).

Key words: Traditional Cost AccountingMethods, Modern Cost Accounting

Methods, ABC, Target Costing, Life Cycle Costing, Product Profitability.

Jel Classificiation: M21, M4A, M51

1. Introduction

The basic purpose of costing systems is to

product or service by assigning manufacturing costs to products

that company produces or provides. Costing system

accounting methods used in order to define the cost

methods used in costing system enable the evaluation of p

from the manufacturing process. It is important to

costing systems differently affect the product evaluation.

costing system was based on the type of the production p

job order costing was used in job order production, while

was applied in process or mass production. Today, these two c

are considered as traditional costing systemswhich are no l

use in modern operating conditions. Business conditions a

becoming more and more complex. Manufacturing processes

production companies are almost fully automated and compute

process of manufacturing automation and computerization causes s

change in manufacturing cost structure. The most important c

modern manufacturing cost structure becomes indirect manufac

157

(manufacturing overheads). This change in manufacturing cost

found traditional costing systems inappropriate for product evaluation.

In order to avoid the inaccuracy of traditional costing

evaluation, the new costing system, based on activities, has b

This costing system is known as Activity based costing.

2. The Types of Costing Systems

Costing system can be defined as a system used

cost objects (products or services). The main purposeof c

enable cost assignment. Cost assignment is the process

and indirect costs to products or servicesin order to d

product or service.

Each costing system consists of five basic elements:1

1. cost object – anything for which a

desired. Usually, cost objects are products or services

manufactures or provides.

2. direct costs of a cost object – these are costs that c

a particular product or service

3. indirect costs of a cost object – these are costs that c

to a particular product or service. Indirect costs need to b

objects using a proper cost allocation method.

4. cost pool – a grouping of individual c

formed when company uses more cost allocation bases. In A

pools are identified activities to which indirect costs are a

5. cost allocation base – the factor that links in a

indirect cost (or group of indirect cost) to a particular c

1) Horngren, C.T., Datar, S.M., Foster, G. (2003), Cost Accounting – A

Managerial Emphasis, Prentice Hall, New Jersey, p. 96-97.

(manufacturing overheads). This change in manufacturing cost

found traditional costing systems inappropriate for product evaluation.

In order to avoid the inaccuracy of traditional costing

evaluation, the new costing system, based on activities, has b

This costing system is known as Activity based costing.

2. The Types of Costing Systems

Costing system can be defined as a system used

cost objects (products or services). The main purposeof c

enable cost assignment. Cost assignment is the process

and indirect costs to products or servicesin order to d

product or service.

Each costing system consists of five basic elements:1

1. cost object – anything for which a

desired. Usually, cost objects are products or services

manufactures or provides.

2. direct costs of a cost object – these are costs that c

a particular product or service

3. indirect costs of a cost object – these are costs that c

to a particular product or service. Indirect costs need to b

objects using a proper cost allocation method.

4. cost pool – a grouping of individual c

formed when company uses more cost allocation bases. In A

pools are identified activities to which indirect costs are a

5. cost allocation base – the factor that links in a

indirect cost (or group of indirect cost) to a particular c

1) Horngren, C.T., Datar, S.M., Foster, G. (2003), Cost Accounting – A

Managerial Emphasis, Prentice Hall, New Jersey, p. 96-97.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

158

These five elements are using to design an adequate

There are three basic costing systems used in

manufacturing companies in order to determine the cost of

a particular product or to evaluate product profitability:2

1. job order costing,

2. process costing,

3. activity based costing.

The first two costing systems are known as tradition

systems. While the appliance of traditional costing systems

type of a manufacturing process, activity based costing system c

regardless the type of manufacturing process. The main i

when is convenient to use traditional costing systemsand w

costing system should be applied? To answer on this question

conditions and the manufacturing cost structure should be c

2.1. Cost allocation in traditional costing systems

The basic distinction between job costing and process c

is in determination of cost object. In job costing cost

consistsof a unit or multiple units of distinct products

costing cost object is masses of identical or similar units o

Therefore, job costing can be applied in manufacturing which i

customer’s order, while process costing can be used in mass p

is continually performing and is not initiated by a

Cost allocation is similar in job costing and in

both costing systems direct manufacturing costs are traced to

services. These costs are directly assigned to particular p

which cause their appearance. Direct manufacturing costs include direct

material costs and direct labour costs. The main problem

system is indirect manufacturing costs allocation. Because these c

2) Lucey, T. (1996), Costing, DP Publications, London, p. 175-176.

These five elements are using to design an adequate

There are three basic costing systems used in

manufacturing companies in order to determine the cost of

a particular product or to evaluate product profitability:2

1. job order costing,

2. process costing,

3. activity based costing.

The first two costing systems are known as tradition

systems. While the appliance of traditional costing systems

type of a manufacturing process, activity based costing system c

regardless the type of manufacturing process. The main i

when is convenient to use traditional costing systemsand w

costing system should be applied? To answer on this question

conditions and the manufacturing cost structure should be c

2.1. Cost allocation in traditional costing systems

The basic distinction between job costing and process c

is in determination of cost object. In job costing cost

consistsof a unit or multiple units of distinct products

costing cost object is masses of identical or similar units o

Therefore, job costing can be applied in manufacturing which i

customer’s order, while process costing can be used in mass p

is continually performing and is not initiated by a

Cost allocation is similar in job costing and in

both costing systems direct manufacturing costs are traced to

services. These costs are directly assigned to particular p

which cause their appearance. Direct manufacturing costs include direct

material costs and direct labour costs. The main problem

system is indirect manufacturing costs allocation. Because these c

2) Lucey, T. (1996), Costing, DP Publications, London, p. 175-176.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

159

be directly identified to particular product or service, indirect m

costs need to be allocated to products or serviceso

which correctly present the relationship between indirect

costs and certain product. This relationship is often very difficult to

express by a single allocation base. It is important

is no allocation base which can accurately provide

to products. Chosen cost allocation base can be more

but it can’t be 100% accurate. Indirect manufacturing

assigned to products or services using the followin3

1. direct labour hours,

2. machine hours,

3. direct material costs,

4. total direct costs,

5. quantity of production.

Indirect manufacturing costs are assigned to cost

overhead allocation rate which is computing on the c4

total indirect manufacturing costs

OAR = --------------------------------------------

cost allocation base

Companies can use either one or more overhead

assigning indirect manufacturing costs to products or services.

that the more overhead allocation rates are used the

accurate and the product profitability evaluation is

objective for decision making.

3) Engler, C. (1988), Managerial Accounting, Irwin, Homewood, Illinois,

p. 427

4) Lucey, T. (1996), Costing, DP Publications, London, p. 88

be directly identified to particular product or service, indirect m

costs need to be allocated to products or serviceso

which correctly present the relationship between indirect

costs and certain product. This relationship is often very difficult to

express by a single allocation base. It is important

is no allocation base which can accurately provide

to products. Chosen cost allocation base can be more

but it can’t be 100% accurate. Indirect manufacturing

assigned to products or services using the followin3

1. direct labour hours,

2. machine hours,

3. direct material costs,

4. total direct costs,

5. quantity of production.

Indirect manufacturing costs are assigned to cost

overhead allocation rate which is computing on the c4

total indirect manufacturing costs

OAR = --------------------------------------------

cost allocation base

Companies can use either one or more overhead

assigning indirect manufacturing costs to products or services.

that the more overhead allocation rates are used the

accurate and the product profitability evaluation is

objective for decision making.

3) Engler, C. (1988), Managerial Accounting, Irwin, Homewood, Illinois,

p. 427

4) Lucey, T. (1996), Costing, DP Publications, London, p. 88

160

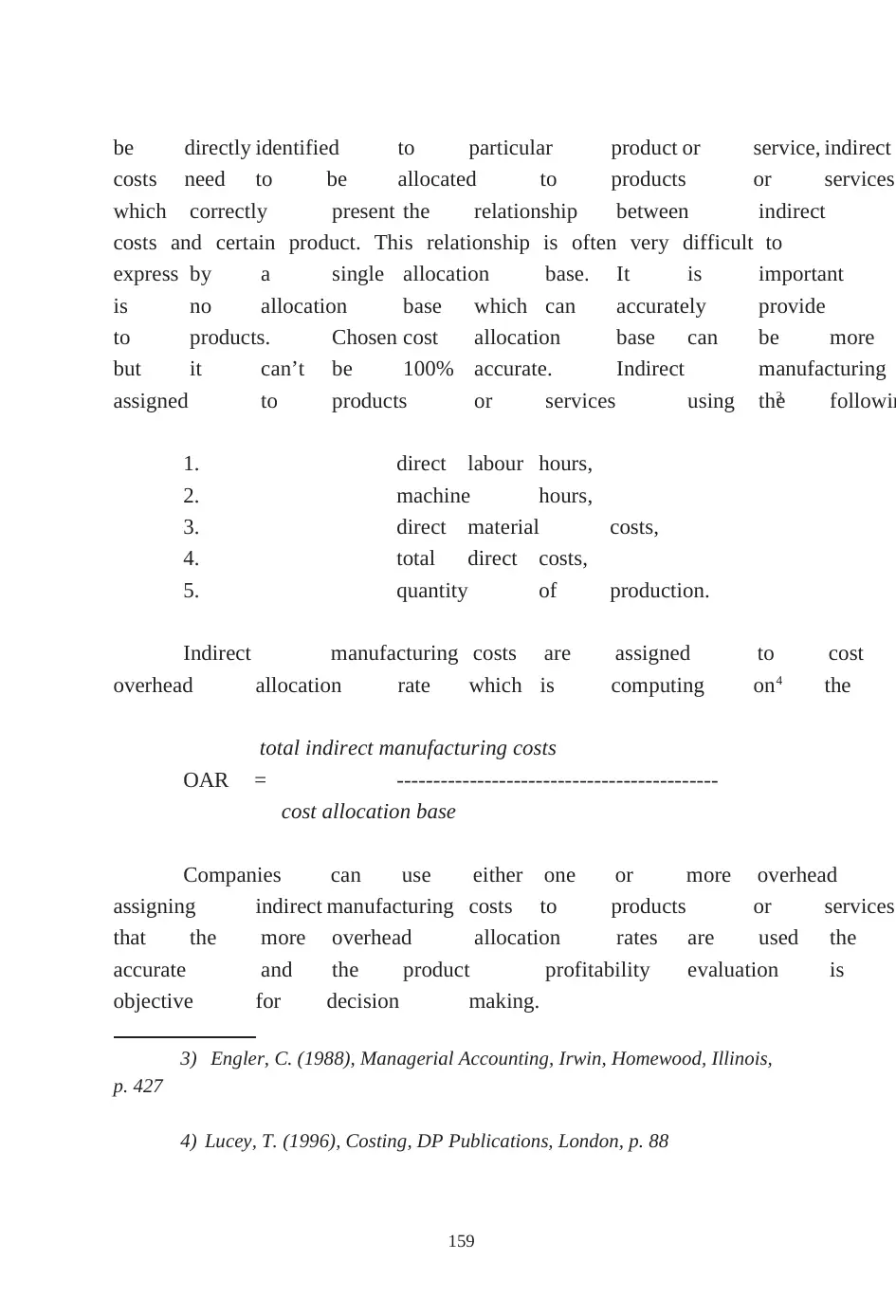

Figure 1. Cost allocation in traditional costing systems

In traditional costing systems the indirect manufac

allocated to cost objects on arbitrary bases which could

profitability evaluation. The impact of traditional costing systemsa

on product profitability evaluation depends on certain

which is manufacturing cost structure considered as the

indirect manufacturing costs participate significantly in total manufac

costs, traditional costing system may cause the wrong picture of

profitability evaluation. Otherwise, traditional costing system can

relatively objective product profitability evaluation.

2.2. Cost allocation in Activity Based Costing System

Activity Based Costing system (ABC system) was

order to correct the deficiencies of traditional costing

purpose of ABC system is to provide the fair and

Cost allocation base

Overhead allocation rate

COST OBJECT –

Direct material costs Direct labour costs

Manufacturing overheads

Figure 1. Cost allocation in traditional costing systems

In traditional costing systems the indirect manufac

allocated to cost objects on arbitrary bases which could

profitability evaluation. The impact of traditional costing systemsa

on product profitability evaluation depends on certain

which is manufacturing cost structure considered as the

indirect manufacturing costs participate significantly in total manufac

costs, traditional costing system may cause the wrong picture of

profitability evaluation. Otherwise, traditional costing system can

relatively objective product profitability evaluation.

2.2. Cost allocation in Activity Based Costing System

Activity Based Costing system (ABC system) was

order to correct the deficiencies of traditional costing

purpose of ABC system is to provide the fair and

Cost allocation base

Overhead allocation rate

COST OBJECT –

Direct material costs Direct labour costs

Manufacturing overheads

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

161

and therefore product profitability evaluation also. Accordin

system focuses attention on indirect manufacturing costs. The aim i

the most appropriate way for indirect manufacturing costs a

objects.

The main assumption

consume activities and activities consume resources.5 The more

activities are set up, the more complex is ABCsystem. An activity

is defined as any event, action, transaction

incurs cost when producing a product or providing a service.6

In ABCsystem direct manufacturing costs are also directly traced to

products or services, so the main attention is p

costs which are allocated to activities instead to departments or jobs

(like in traditional systems). Basically, the application

going through two main phases. In the first phase indirect

costs are allocated to activity cost pools. It is

correlation between particular indirect manufacturing cost

activity. Every indirect manufacturing cost must be assigned

activity which causes its occurrence. The second phase in ABC

is assigning indirect manufacturing costs from activity cost pools to

products using defined cost drivers. A cost driver

that has a direct cause – effect relationship with the7

ABC system uses multiple cost allocation bases to assign i

costs to products or services. The usage of multiple

provide a more accurate and objective product profitability e

5) Horngren, C.T., Datar, S.M., Foster, G. (2003), Cost Accounting – A

Managerial Emphasis, Prentice Hall, New Jersey, p. 141.

6) Horngren, C.T., Datar, S.M., Foster, G. (2003), Cost Accounting – A

Managerial Emphasis,Prentice Hall,New Jersey, p. 141 or Weygandt, J.J., Kieso,

D.E.,Kimmel, P.D. (2005), Managerial Accounting, John Wiley & Sons, USA, p. 144.

7) Weygandt, J.J., Kieso, D.E., Kimmel, P.D. (2005), Managerial Accounting,

John Wiley & Sons, USA, p. 144.

and therefore product profitability evaluation also. Accordin

system focuses attention on indirect manufacturing costs. The aim i

the most appropriate way for indirect manufacturing costs a

objects.

The main assumption

consume activities and activities consume resources.5 The more

activities are set up, the more complex is ABCsystem. An activity

is defined as any event, action, transaction

incurs cost when producing a product or providing a service.6

In ABCsystem direct manufacturing costs are also directly traced to

products or services, so the main attention is p

costs which are allocated to activities instead to departments or jobs

(like in traditional systems). Basically, the application

going through two main phases. In the first phase indirect

costs are allocated to activity cost pools. It is

correlation between particular indirect manufacturing cost

activity. Every indirect manufacturing cost must be assigned

activity which causes its occurrence. The second phase in ABC

is assigning indirect manufacturing costs from activity cost pools to

products using defined cost drivers. A cost driver

that has a direct cause – effect relationship with the7

ABC system uses multiple cost allocation bases to assign i

costs to products or services. The usage of multiple

provide a more accurate and objective product profitability e

5) Horngren, C.T., Datar, S.M., Foster, G. (2003), Cost Accounting – A

Managerial Emphasis, Prentice Hall, New Jersey, p. 141.

6) Horngren, C.T., Datar, S.M., Foster, G. (2003), Cost Accounting – A

Managerial Emphasis,Prentice Hall,New Jersey, p. 141 or Weygandt, J.J., Kieso,

D.E.,Kimmel, P.D. (2005), Managerial Accounting, John Wiley & Sons, USA, p. 144.

7) Weygandt, J.J., Kieso, D.E., Kimmel, P.D. (2005), Managerial Accounting,

John Wiley & Sons, USA, p. 144.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

162

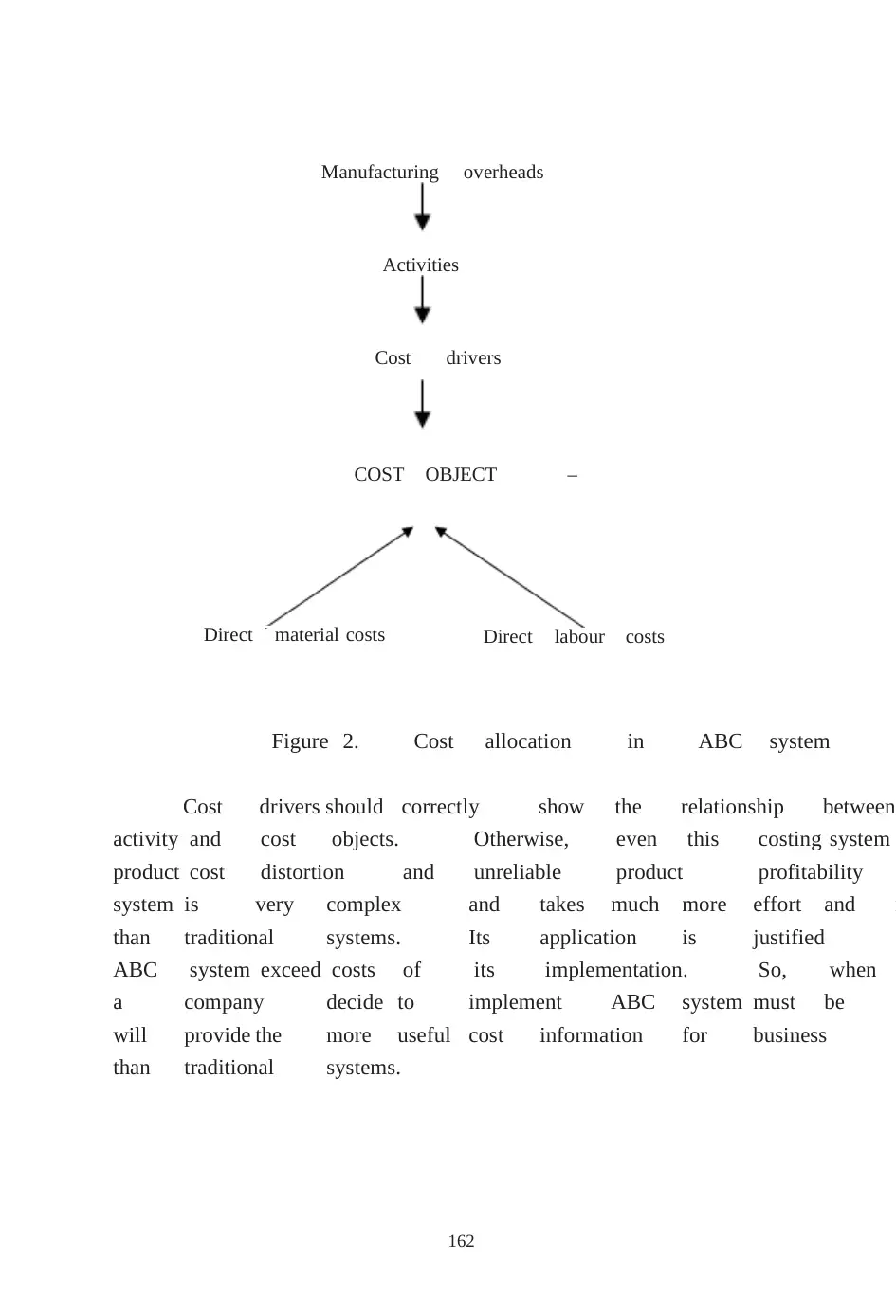

Manufacturing overheads

Figure 2. Cost allocation in ABC system

Cost drivers should correctly show the relationship between

activity and cost objects. Otherwise, even this costing system

product cost distortion and unreliable product profitability

system is very complex and takes much more effort and r

than traditional systems. Its application is justified o

ABC system exceed costs of its implementation. So, when

a company decide to implement ABC system must be s

will provide the more useful cost information for business d

than traditional systems.

Activities

Cost drivers

COST OBJECT –

Direct material costs Direct labour costs

Manufacturing overheads

Figure 2. Cost allocation in ABC system

Cost drivers should correctly show the relationship between

activity and cost objects. Otherwise, even this costing system

product cost distortion and unreliable product profitability

system is very complex and takes much more effort and r

than traditional systems. Its application is justified o

ABC system exceed costs of its implementation. So, when

a company decide to implement ABC system must be s

will provide the more useful cost information for business d

than traditional systems.

Activities

Cost drivers

COST OBJECT –

Direct material costs Direct labour costs

163

2.3. Traditional systems vs. ABC system – the impact on product

profitability evaluation

The main dilemma which many manufacturing companies

is the choice of costing system. Traditional costing systems

deficiencies in product profitability evaluation especially

allocation bases are not in direct correlation with indirect

costs. Today’s manufacturing environment characterizes automat

computerized manufacturing processes, technological innovations and g

competition.8 As a result of these changes, indirect

significantly increased, while direct labour costs are dramatically d

In these conditions, traditional costing systemscannot provide objective

accurate product profitability evaluation becausetypical cost allocatio

in traditional system (which are direct labour hours and machine

longer in correlation with indirect manufacturing costs appearance. T

the new approach for cost allocation needs to be

more appropriate costing system in modern manufacturing conditions. M

surveys conducted in modern manufacturing companies worldwide i

the factors which directs to ABC system application. These factors9

1. product lines differ greatly in volume and manufacturing

complexity;

2. product lines are numerous, diverse and require differing

of support services;

3. overhead costs constitute a significant portion o

4. the manufacturing process or the number of products

significantly – for example, from labour-intensive t

intensive due to automation;

8) Ibid.

9) Ibid, p. 154

2.3. Traditional systems vs. ABC system – the impact on product

profitability evaluation

The main dilemma which many manufacturing companies

is the choice of costing system. Traditional costing systems

deficiencies in product profitability evaluation especially

allocation bases are not in direct correlation with indirect

costs. Today’s manufacturing environment characterizes automat

computerized manufacturing processes, technological innovations and g

competition.8 As a result of these changes, indirect

significantly increased, while direct labour costs are dramatically d

In these conditions, traditional costing systemscannot provide objective

accurate product profitability evaluation becausetypical cost allocatio

in traditional system (which are direct labour hours and machine

longer in correlation with indirect manufacturing costs appearance. T

the new approach for cost allocation needs to be

more appropriate costing system in modern manufacturing conditions. M

surveys conducted in modern manufacturing companies worldwide i

the factors which directs to ABC system application. These factors9

1. product lines differ greatly in volume and manufacturing

complexity;

2. product lines are numerous, diverse and require differing

of support services;

3. overhead costs constitute a significant portion o

4. the manufacturing process or the number of products

significantly – for example, from labour-intensive t

intensive due to automation;

8) Ibid.

9) Ibid, p. 154

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

164

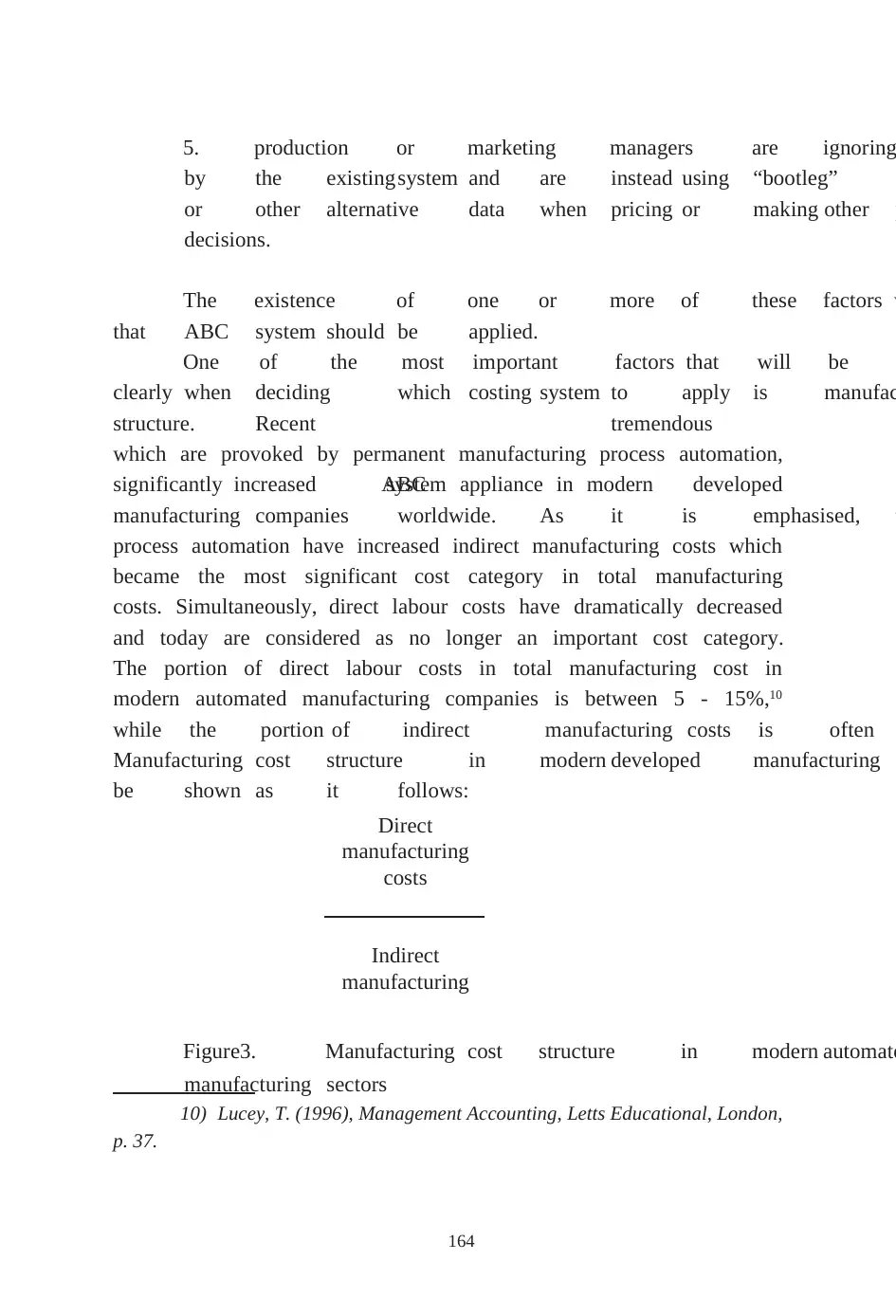

5. production or marketing managers are ignoring

by the existingsystem and are instead using “bootleg” c

or other alternative data when pricing or making other p

decisions.

The existence of one or more of these factors w

that ABC system should be applied.

One of the most important factors that will be

clearly when deciding which costing system to apply is manufac

structure. Recent tremendous c

which are provoked by permanent manufacturing process automation,

significantly increased ABCsystem appliance in modern developed

manufacturing companies worldwide. As it is emphasised, t

process automation have increased indirect manufacturing costs which

became the most significant cost category in total manufacturing

costs. Simultaneously, direct labour costs have dramatically decreased

and today are considered as no longer an important cost category.

The portion of direct labour costs in total manufacturing cost in

modern automated manufacturing companies is between 5 - 15%,10

while the portion of indirect manufacturing costs is often

Manufacturing cost structure in modern developed manufacturing s

be shown as it follows:

Figure3. Manufacturing cost structure in modern automate

manufacturing sectors

10) Lucey, T. (1996), Management Accounting, Letts Educational, London,

p. 37.

Direct

manufacturing

costs

Indirect

manufacturing

5. production or marketing managers are ignoring

by the existingsystem and are instead using “bootleg” c

or other alternative data when pricing or making other p

decisions.

The existence of one or more of these factors w

that ABC system should be applied.

One of the most important factors that will be

clearly when deciding which costing system to apply is manufac

structure. Recent tremendous c

which are provoked by permanent manufacturing process automation,

significantly increased ABCsystem appliance in modern developed

manufacturing companies worldwide. As it is emphasised, t

process automation have increased indirect manufacturing costs which

became the most significant cost category in total manufacturing

costs. Simultaneously, direct labour costs have dramatically decreased

and today are considered as no longer an important cost category.

The portion of direct labour costs in total manufacturing cost in

modern automated manufacturing companies is between 5 - 15%,10

while the portion of indirect manufacturing costs is often

Manufacturing cost structure in modern developed manufacturing s

be shown as it follows:

Figure3. Manufacturing cost structure in modern automate

manufacturing sectors

10) Lucey, T. (1996), Management Accounting, Letts Educational, London,

p. 37.

Direct

manufacturing

costs

Indirect

manufacturing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

165

When indirect manufacturing costs take the significant portion

of total manufacturing costs, more objective and more accurate

profitability evaluation can be achieved by using ABC s

manufacturing costs take the significant portion of total manufac

then even traditional costing systems can provide relativel

accurate product profitability evaluation. In these circumstances u

system wouldn’t contribute to more objective and more

profitability evaluation.

3. Dynamic Approach of Cost Management

Dynamic approach of cost management enables

product profitability through the entire product life cycle.

approach is oriented to the long run decisions r

forming the adequate product mix, eliminating the non-pro

introducing the new product line etc. But, in order to p

with relevant information regarding product profitability evaluation,

accounting function in companies need to combine

dynamic approach of cost management e.g. need t

product profitability in the short run and in the long r

of these two cost management approaches can give the o

picture regarding product profitability.

While static cost management approach is based on

cost accounting methods which are focused mainly on

towardsthe determination of the manufacturing cost per unit, d

management approach involves modern managerial account

focused on the total costs through the whole product

managerial accounting literature recognizes several costing methods

on the whole product life cycle. The most important methods

theory of constraints, life-cycle costing and long-term pricing11. These four

11) Blocher, E.J., Chen, K.H., Cokins, G., Lin, T.W. (2005), Cost Management

– A Strategic Emphasis, McGraw Hill – Irwin, New York.

When indirect manufacturing costs take the significant portion

of total manufacturing costs, more objective and more accurate

profitability evaluation can be achieved by using ABC s

manufacturing costs take the significant portion of total manufac

then even traditional costing systems can provide relativel

accurate product profitability evaluation. In these circumstances u

system wouldn’t contribute to more objective and more

profitability evaluation.

3. Dynamic Approach of Cost Management

Dynamic approach of cost management enables

product profitability through the entire product life cycle.

approach is oriented to the long run decisions r

forming the adequate product mix, eliminating the non-pro

introducing the new product line etc. But, in order to p

with relevant information regarding product profitability evaluation,

accounting function in companies need to combine

dynamic approach of cost management e.g. need t

product profitability in the short run and in the long r

of these two cost management approaches can give the o

picture regarding product profitability.

While static cost management approach is based on

cost accounting methods which are focused mainly on

towardsthe determination of the manufacturing cost per unit, d

management approach involves modern managerial account

focused on the total costs through the whole product

managerial accounting literature recognizes several costing methods

on the whole product life cycle. The most important methods

theory of constraints, life-cycle costing and long-term pricing11. These four

11) Blocher, E.J., Chen, K.H., Cokins, G., Lin, T.W. (2005), Cost Management

– A Strategic Emphasis, McGraw Hill – Irwin, New York.

166

methods enable a comprehensive analysis of product

through the whole product life cycle. Target costing emphasizes the r

product design in reducing costs in the manufacturing and d

of the product life cycle.12 Theory of constraints includes methods used

identify and to manage (or eliminate if possible) bottlenec

process in order to reduce manufacturing costs and to increase

income13. Life-cycle costing tracks and accumulates all costs

the each product through its whole life cycle14 enabling a complete

of product profitability through its life cycle. Thus, long-term pricin

life-cycle costing in long-term pricing decisions.15

In further chapters of this paper, target costing and life-cycle

costing will be analysed, because these two methods

used by manufacturing companies, especially the ones where

development, manufacturing speed and efficiency are important.

3.1. The Characteristics and Implementation of Target Costing

3.1.1. The Characteristics and Reasons of Target Costing

Application

Target costing is a specific approach developed

combines market and accounting information. Target costing can b

as the process of determining the maximum allowab

product and then developing a prototype that can be p

12) Ibid.

13) Horngren, C.T., Datar, S.M., Foster, G. (2003), Cost Accounting – AHorngren, C.T., Datar, S.M., Foster, G. (2003), Cost Accounting – A

Managerial Emphasis, Prentice Hall, New Jersey.

14) Ibid.

15) Blocher, E.J., Chen, K.H., Cokins, G., Lin, T.W. (2005), Cost Management

– A Strategic Emphasis, McGraw Hill – Irwin, New York.

methods enable a comprehensive analysis of product

through the whole product life cycle. Target costing emphasizes the r

product design in reducing costs in the manufacturing and d

of the product life cycle.12 Theory of constraints includes methods used

identify and to manage (or eliminate if possible) bottlenec

process in order to reduce manufacturing costs and to increase

income13. Life-cycle costing tracks and accumulates all costs

the each product through its whole life cycle14 enabling a complete

of product profitability through its life cycle. Thus, long-term pricin

life-cycle costing in long-term pricing decisions.15

In further chapters of this paper, target costing and life-cycle

costing will be analysed, because these two methods

used by manufacturing companies, especially the ones where

development, manufacturing speed and efficiency are important.

3.1. The Characteristics and Implementation of Target Costing

3.1.1. The Characteristics and Reasons of Target Costing

Application

Target costing is a specific approach developed

combines market and accounting information. Target costing can b

as the process of determining the maximum allowab

product and then developing a prototype that can be p

12) Ibid.

13) Horngren, C.T., Datar, S.M., Foster, G. (2003), Cost Accounting – AHorngren, C.T., Datar, S.M., Foster, G. (2003), Cost Accounting – A

Managerial Emphasis, Prentice Hall, New Jersey.

14) Ibid.

15) Blocher, E.J., Chen, K.H., Cokins, G., Lin, T.W. (2005), Cost Management

– A Strategic Emphasis, McGraw Hill – Irwin, New York.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.