Analysis of MFRS for Savings Deposits Contracts: A Financial Report

VerifiedAdded on 2020/06/05

|11

|1800

|32

Report

AI Summary

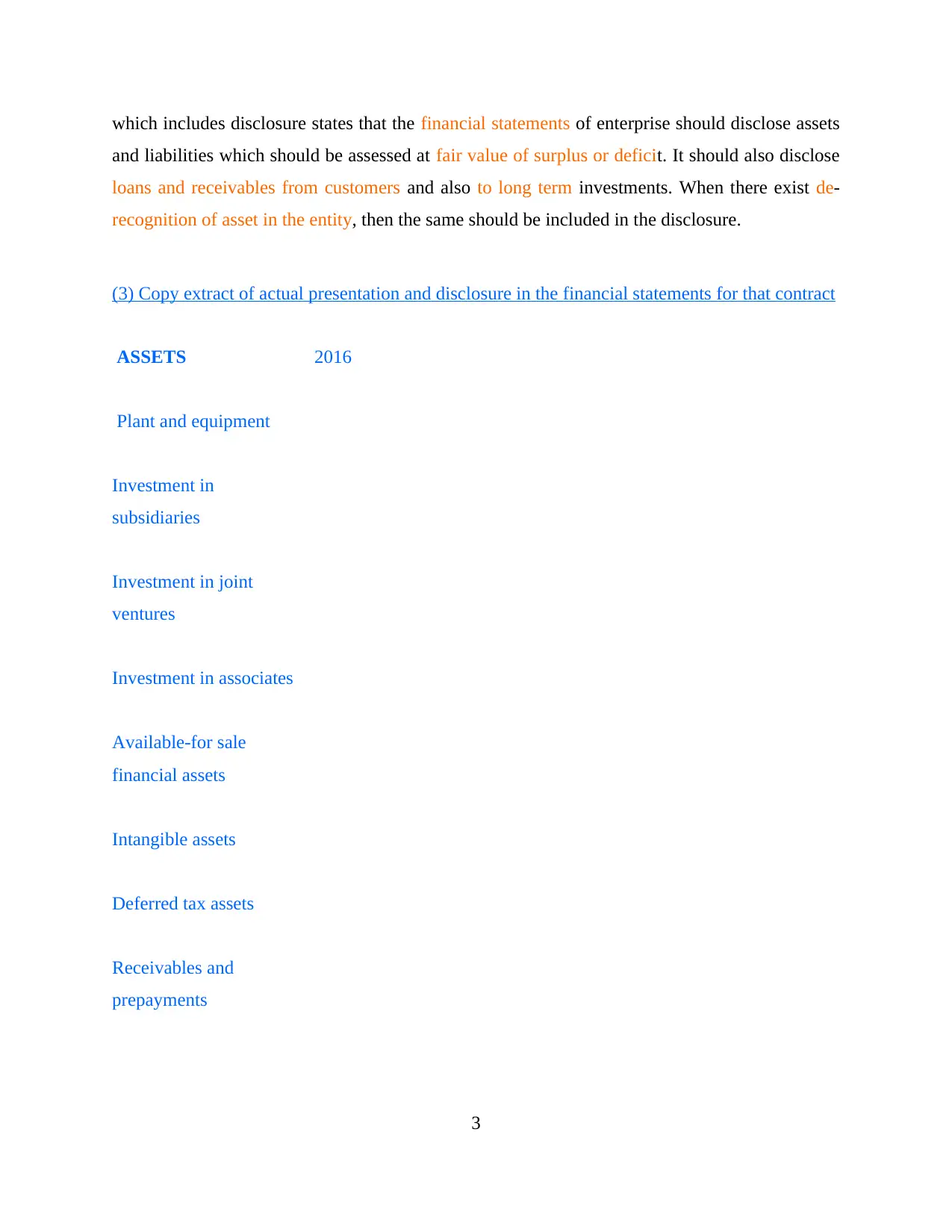

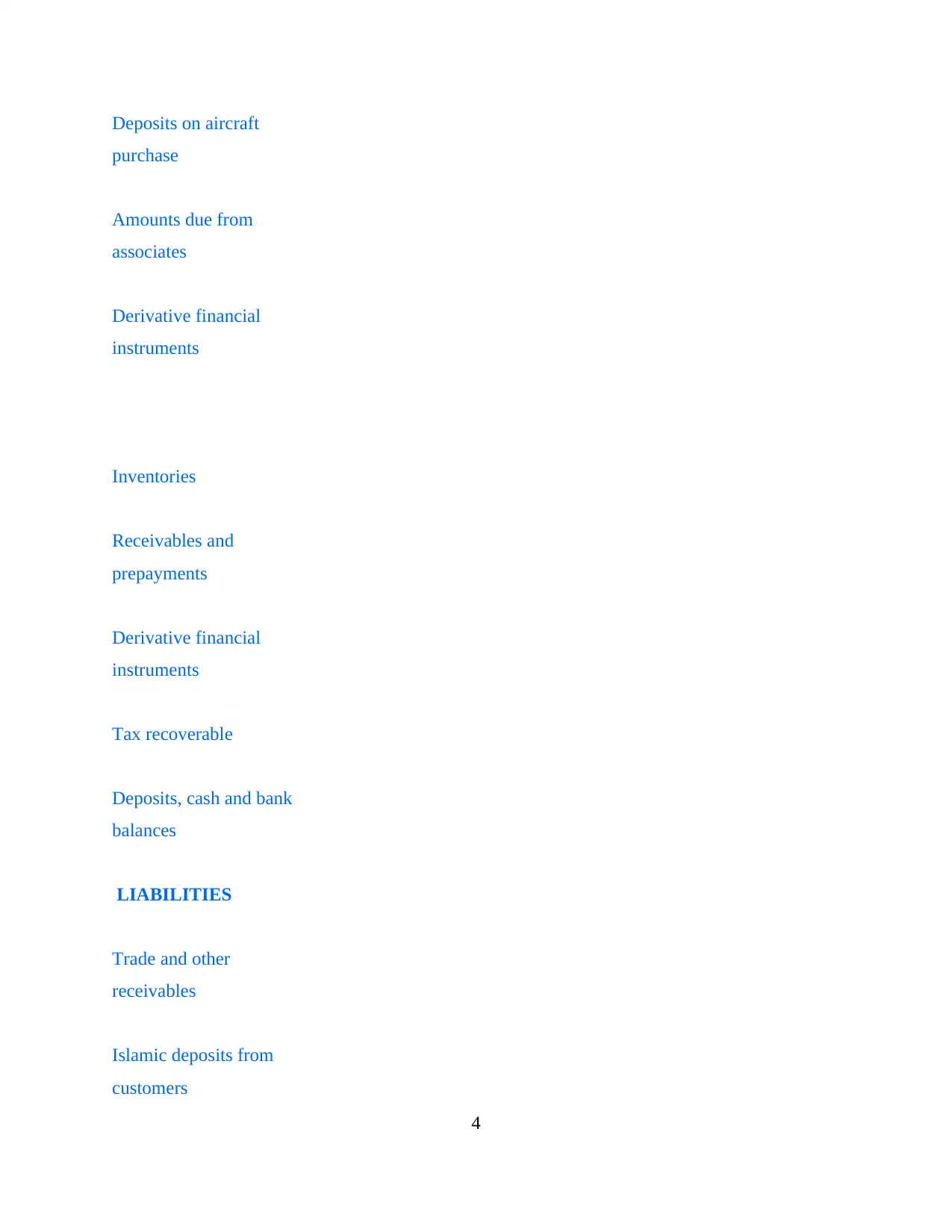

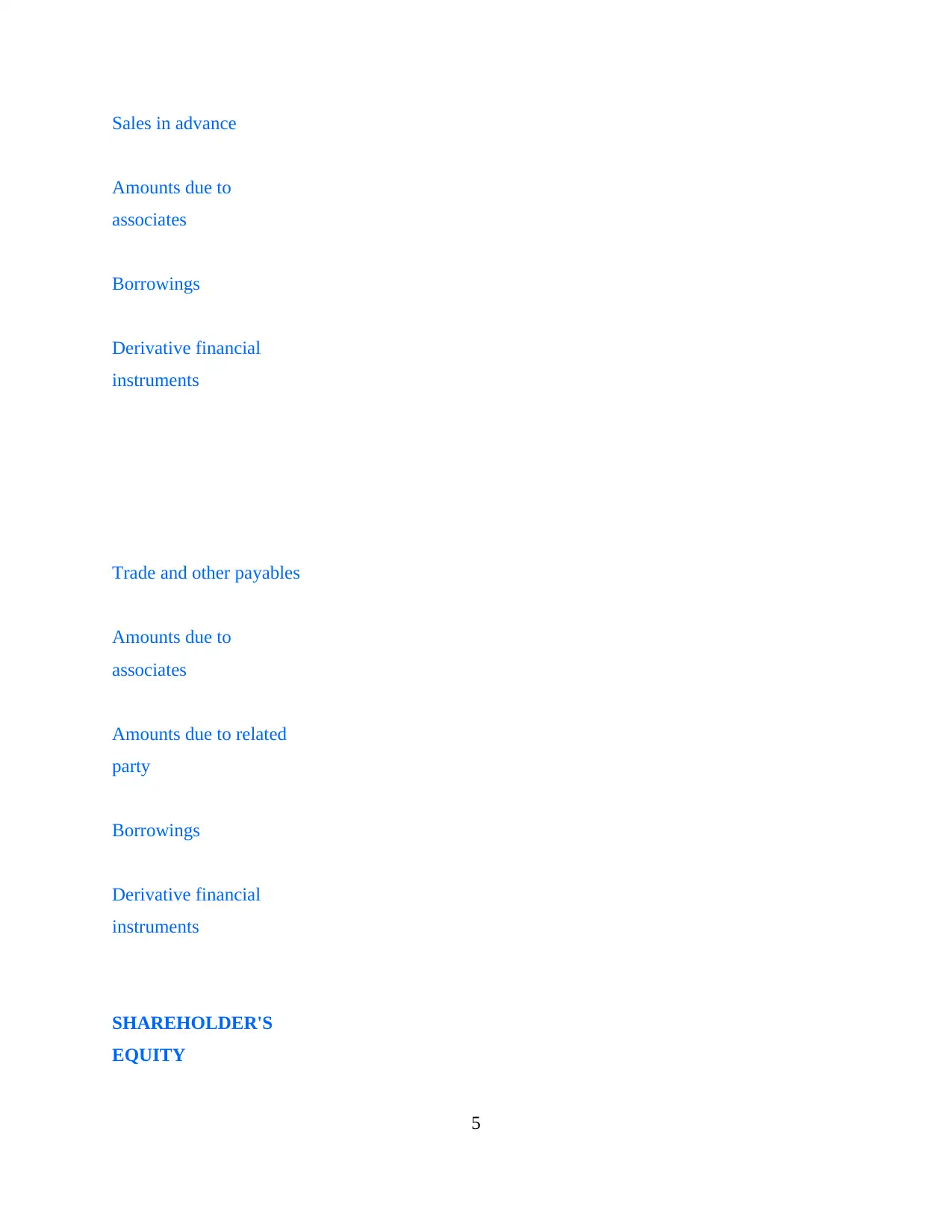

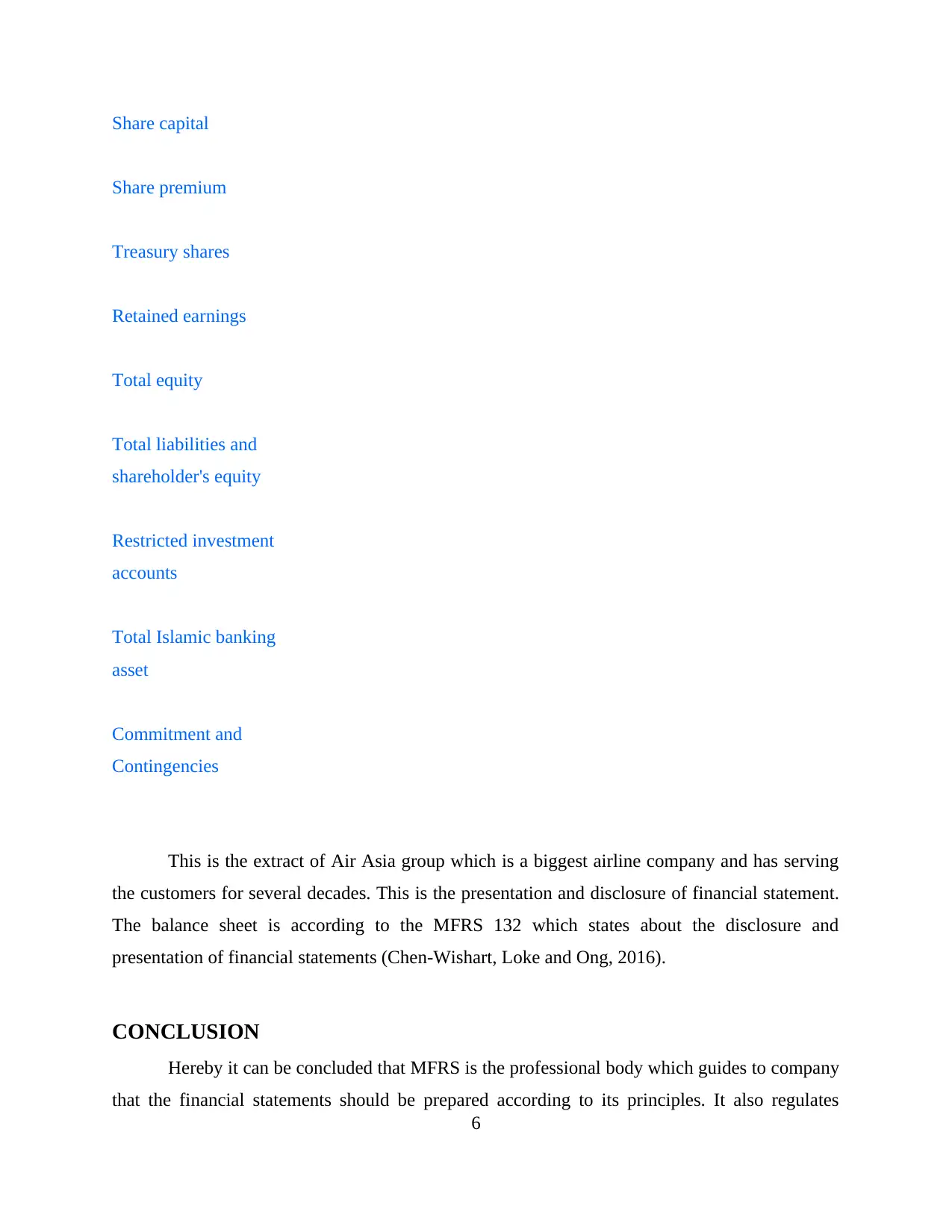

This report provides an overview of Malaysian Financial Reporting Standards (MFRS) as they relate to savings deposits contracts. It begins by identifying the relevant MFRS, focusing on revenue recognition, including Tawarruq, Murabahah, Musyarakah Mutanaqisah, and Qard contracts. The report then discusses how MFRS standards address the recognition, measurement, presentation, and disclosure of these contracts, with specific reference to MFRS 139 and MFRS 132. The document includes an extract of the actual presentation and disclosure of financial statements related to savings deposits, using AirAsia's financial statements as an example. The conclusion emphasizes the role of MFRS in ensuring the financial statements are prepared according to its principles and in regulating contracts. The report is supported by multiple references to accounting and legal literature.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.