Organisational Performance of NAB: HC1010 Accounting for Business

VerifiedAdded on 2023/06/12

|20

|4418

|95

Report

AI Summary

This report provides a comprehensive financial analysis of National Australia Bank (NAB), examining its profitability, financial position, and cash flow statements. It includes a comparative analysis of NAB's performance against a competitor, Commonwealth Bank of Australia (CBA), using key profitability ratios such as return on equity and profit margin. The analysis covers the years 2016 and 2017, evaluating changes in interest income, net profit, and various balance sheet components like assets and liabilities. Additionally, the report calculates and interprets ratios like return on assets, quick ratio, and price-earnings ratio for the years 2015-2017, offering insights into the bank's financial health and operational efficiency. The study concludes with an assessment of management's role in safeguarding the corporation's interests.

Running head: ACCOUNTING FOR BUSINESS

Accounting for Business

University Name

Student Name

Authors’ Note

Accounting for Business

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

ACCOUNTING FOR BUSINESS

Executive Summary

The study at hand intends to present financial standing of the firm by means of thorough

comparative analysis of profitability, investigation of financial assertions of the firm and

analysis of financial position from balance sheet statement. Moving further, this study

presents analysis of key ratio of three financial years that can aid understanding financial

health as well as soundness of organizational position. In the end, based on report announced

by the firm, this current study discusses in detail about the way management works for the

best interest of the entire corporation.

ACCOUNTING FOR BUSINESS

Executive Summary

The study at hand intends to present financial standing of the firm by means of thorough

comparative analysis of profitability, investigation of financial assertions of the firm and

analysis of financial position from balance sheet statement. Moving further, this study

presents analysis of key ratio of three financial years that can aid understanding financial

health as well as soundness of organizational position. In the end, based on report announced

by the firm, this current study discusses in detail about the way management works for the

best interest of the entire corporation.

3

ACCOUNTING FOR BUSINESS

Table of Contents

Introduction................................................................................................................................3

Section 1:....................................................................................................................................3

Section 2:..................................................................................................................................11

Section 3:..................................................................................................................................13

Conclusion................................................................................................................................17

References................................................................................................................................19

ACCOUNTING FOR BUSINESS

Table of Contents

Introduction................................................................................................................................3

Section 1:....................................................................................................................................3

Section 2:..................................................................................................................................11

Section 3:..................................................................................................................................13

Conclusion................................................................................................................................17

References................................................................................................................................19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

ACCOUNTING FOR BUSINESS

Introduction

For the purpose of the current study on analysis of organizational performance of the

company National Australian Bank (NAB) is selected. NAB is a Melbourne based Australian

bank that is necessarily a different financial services group, conventionally focussed on

banking business with presence in segment of wealth. In essence, National Australia Bank is

presently the third largest bank in terms of market capitalisation as well as benefits from a

huge national branch network and enhancing market share in both home loans as well as

retail deposits.

Section 1:

Evaluation of financial standing of the allocated company National Australian Bank

(NAB)

Analysis of profitability of the company

Profitability of the company National Australia Bank (NAB) can be analysed from the

income statement of the firm. The total interest income of the corporation is recorded to be

$27403 million in the year 2017 whereas the same was recorded to be $27629 in the year

2016 (Nab.com.au 2018). This reflects a decrease in the interest income of the firm. Again,

interest expense of the firm is said to have increased to $14699 million in 2017 in comparison

to $14221 million in 2016. Therefore, decrease in interest income along with the increase in

the interest expense of the firm reflects an overall decrease in the net interest income acquired

by the firm (Rakićević et al. 2016). The net interest income of the firm is registered to be

$13182 million in 2017 while the same is recorded to be $12930 million in the year 2016.

ACCOUNTING FOR BUSINESS

Introduction

For the purpose of the current study on analysis of organizational performance of the

company National Australian Bank (NAB) is selected. NAB is a Melbourne based Australian

bank that is necessarily a different financial services group, conventionally focussed on

banking business with presence in segment of wealth. In essence, National Australia Bank is

presently the third largest bank in terms of market capitalisation as well as benefits from a

huge national branch network and enhancing market share in both home loans as well as

retail deposits.

Section 1:

Evaluation of financial standing of the allocated company National Australian Bank

(NAB)

Analysis of profitability of the company

Profitability of the company National Australia Bank (NAB) can be analysed from the

income statement of the firm. The total interest income of the corporation is recorded to be

$27403 million in the year 2017 whereas the same was recorded to be $27629 in the year

2016 (Nab.com.au 2018). This reflects a decrease in the interest income of the firm. Again,

interest expense of the firm is said to have increased to $14699 million in 2017 in comparison

to $14221 million in 2016. Therefore, decrease in interest income along with the increase in

the interest expense of the firm reflects an overall decrease in the net interest income acquired

by the firm (Rakićević et al. 2016). The net interest income of the firm is registered to be

$13182 million in 2017 while the same is recorded to be $12930 million in the year 2016.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

ACCOUNTING FOR BUSINESS

Analysis of the financial statement of the firm National Australia Bank reveals the fact that

the net profit of the firm is recorded to be $5288 million in the year 2017 whereas the same

was documented to be $357 million in the year 2016. Thus, it replicates a sharp enhancement

in net income of the corporation. This net income is said to enhance during the year 2017 as

interest expense is said to have decreased and the net loss from different discontinued

operations of the firm is said to have lessened during the current year. Thus, based on

analysis of prior year, it can be hereby mentioned that net income or in other words net profit

of the firm has improved during the specified period of time, reflecting desirable financial

condition (Rakićević et al. 2016).

However, in terms of the competitor of the firm that is the Commonwealth Bank of Australia

(CBA), it can be said that during the same period of time, the net revenue of the firm was

registered to be $25089 million in 2017. This replicates the fact that net revenue of the

competitor firm Commonwealth Bank was comparatively higher in the year 2017 as

compared to the figure registered by the National Australia Bank (NAB).

Essentially, the profitability of the firm can also be analysed by application of certain key

profitability ratio (Omar et al. 2014)

Return on equity: As rightly indicated by Zainudin and Hashim (2016), the return on equity

refers to a profitability ratio that enumerates capability of a corporation to acquire profits

from particularly investments of the shareholders in the business concern. In essence, the

return on equity reflects the way profit of each dollar is generated from the equity of the

common shareholders of the firm (Alin-Eliodor 2014). The same is calculated by means of

dividing the net income of the company by the equity contribution of the firm’s shareholders.

Comparative analysis of NAB and its competitor’s profitability over the time period 2016 and

2017 is hereby presented below:

ACCOUNTING FOR BUSINESS

Analysis of the financial statement of the firm National Australia Bank reveals the fact that

the net profit of the firm is recorded to be $5288 million in the year 2017 whereas the same

was documented to be $357 million in the year 2016. Thus, it replicates a sharp enhancement

in net income of the corporation. This net income is said to enhance during the year 2017 as

interest expense is said to have decreased and the net loss from different discontinued

operations of the firm is said to have lessened during the current year. Thus, based on

analysis of prior year, it can be hereby mentioned that net income or in other words net profit

of the firm has improved during the specified period of time, reflecting desirable financial

condition (Rakićević et al. 2016).

However, in terms of the competitor of the firm that is the Commonwealth Bank of Australia

(CBA), it can be said that during the same period of time, the net revenue of the firm was

registered to be $25089 million in 2017. This replicates the fact that net revenue of the

competitor firm Commonwealth Bank was comparatively higher in the year 2017 as

compared to the figure registered by the National Australia Bank (NAB).

Essentially, the profitability of the firm can also be analysed by application of certain key

profitability ratio (Omar et al. 2014)

Return on equity: As rightly indicated by Zainudin and Hashim (2016), the return on equity

refers to a profitability ratio that enumerates capability of a corporation to acquire profits

from particularly investments of the shareholders in the business concern. In essence, the

return on equity reflects the way profit of each dollar is generated from the equity of the

common shareholders of the firm (Alin-Eliodor 2014). The same is calculated by means of

dividing the net income of the company by the equity contribution of the firm’s shareholders.

Comparative analysis of NAB and its competitor’s profitability over the time period 2016 and

2017 is hereby presented below:

6

ACCOUNTING FOR BUSINESS

Return on Equity NAB CBA

2017 2016 2017 2016

Net Income 5288 357 9928 9227

Shareholder's Equity 51317 51315 63170 60206

10.30458 0.695703 15.71632 15.32572

Analysis of the return on equity (%) reveals capability of a firm to generate profits from

particularly the investments of the shareholders (Robinson et al. 2015). This ratio (%) has

increased sharply from 0.69 in 2016 to 10.30, reflecting a favourable financial condition for

the firm. Similarly, in case of CBA as well, the return on equity has increased over the

specified period of time although insignificantly. However, comparative analysis of the two

different firms reflects that the CBA has better financial position in terms of profitability

(return on equity on %) in the current period.

Profit Margin: As correctly mentioned by Abdullah (2016), profit margin indicates towards

what percentage of overall sales is carried out from the net sales of the firm. In essence, it

enumerates the total amount of profit that are generated at a certain stage.

The profit margin of NAB is seen to have increased significantly during the year 2017 in

comparison to the year 2016. The company attaining higher ratios reflects a desirable

financial condition for the corporation (Dalnial et al. 2014). Similarly, in case of CBA as

well, the profit margin has increased over the specified period of time although

insignificantly. However, comparative analysis of the two different firms reflects that the

NAB has better financial position in terms of profitability (Profit Margin) in the current

period.

ACCOUNTING FOR BUSINESS

Return on Equity NAB CBA

2017 2016 2017 2016

Net Income 5288 357 9928 9227

Shareholder's Equity 51317 51315 63170 60206

10.30458 0.695703 15.71632 15.32572

Analysis of the return on equity (%) reveals capability of a firm to generate profits from

particularly the investments of the shareholders (Robinson et al. 2015). This ratio (%) has

increased sharply from 0.69 in 2016 to 10.30, reflecting a favourable financial condition for

the firm. Similarly, in case of CBA as well, the return on equity has increased over the

specified period of time although insignificantly. However, comparative analysis of the two

different firms reflects that the CBA has better financial position in terms of profitability

(return on equity on %) in the current period.

Profit Margin: As correctly mentioned by Abdullah (2016), profit margin indicates towards

what percentage of overall sales is carried out from the net sales of the firm. In essence, it

enumerates the total amount of profit that are generated at a certain stage.

The profit margin of NAB is seen to have increased significantly during the year 2017 in

comparison to the year 2016. The company attaining higher ratios reflects a desirable

financial condition for the corporation (Dalnial et al. 2014). Similarly, in case of CBA as

well, the profit margin has increased over the specified period of time although

insignificantly. However, comparative analysis of the two different firms reflects that the

NAB has better financial position in terms of profitability (Profit Margin) in the current

period.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

ACCOUNTING FOR BUSINESS

NAB CBA

Profit Margin 2017 2016 2017 2016

Net Income 5288 357 9928 9227

Net Sales 8661 8978 25089 24225

0.610553 0.039764 0.395711 0.380888

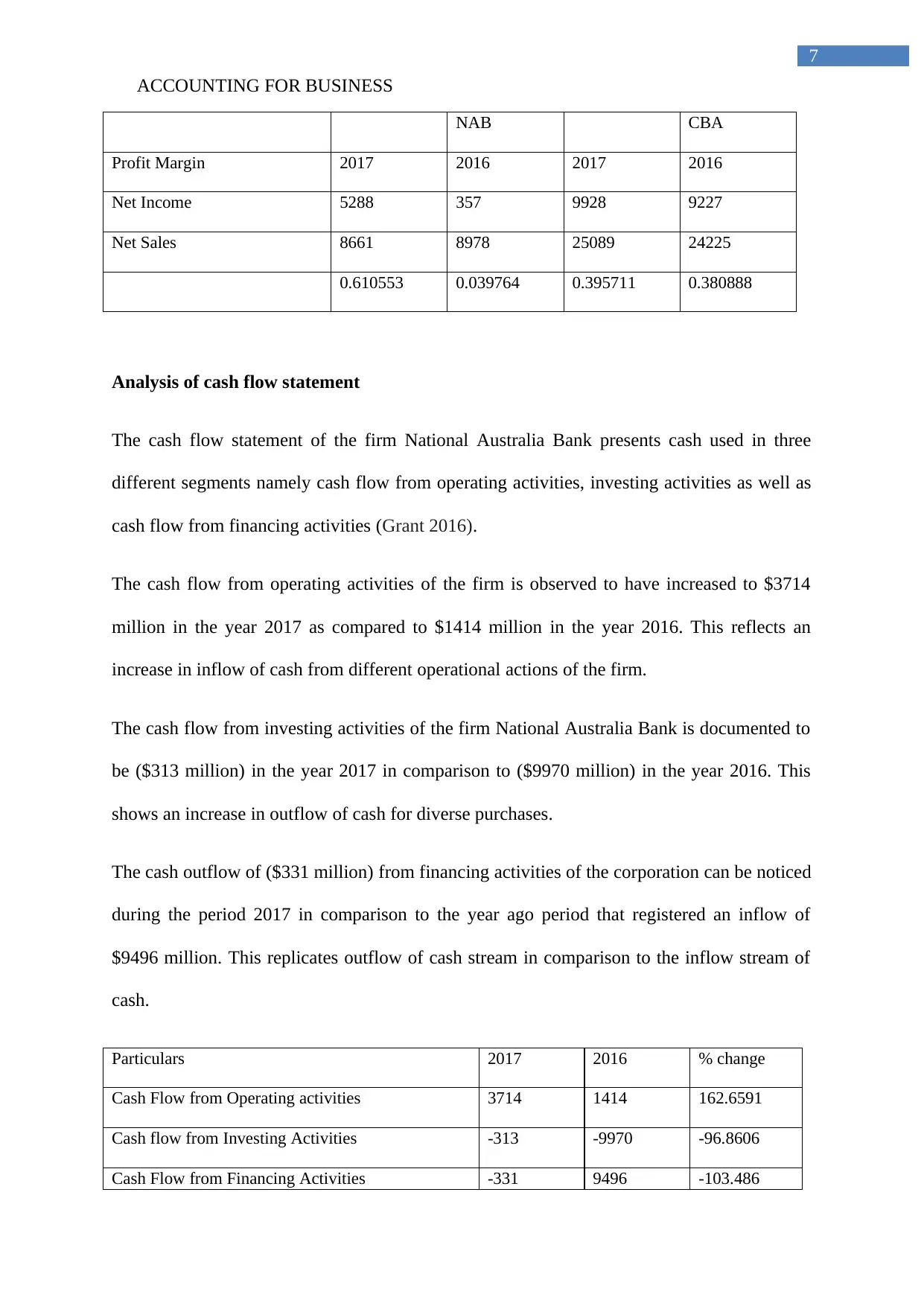

Analysis of cash flow statement

The cash flow statement of the firm National Australia Bank presents cash used in three

different segments namely cash flow from operating activities, investing activities as well as

cash flow from financing activities (Grant 2016).

The cash flow from operating activities of the firm is observed to have increased to $3714

million in the year 2017 as compared to $1414 million in the year 2016. This reflects an

increase in inflow of cash from different operational actions of the firm.

The cash flow from investing activities of the firm National Australia Bank is documented to

be ($313 million) in the year 2017 in comparison to ($9970 million) in the year 2016. This

shows an increase in outflow of cash for diverse purchases.

The cash outflow of ($331 million) from financing activities of the corporation can be noticed

during the period 2017 in comparison to the year ago period that registered an inflow of

$9496 million. This replicates outflow of cash stream in comparison to the inflow stream of

cash.

Particulars 2017 2016 % change

Cash Flow from Operating activities 3714 1414 162.6591

Cash flow from Investing Activities -313 -9970 -96.8606

Cash Flow from Financing Activities -331 9496 -103.486

ACCOUNTING FOR BUSINESS

NAB CBA

Profit Margin 2017 2016 2017 2016

Net Income 5288 357 9928 9227

Net Sales 8661 8978 25089 24225

0.610553 0.039764 0.395711 0.380888

Analysis of cash flow statement

The cash flow statement of the firm National Australia Bank presents cash used in three

different segments namely cash flow from operating activities, investing activities as well as

cash flow from financing activities (Grant 2016).

The cash flow from operating activities of the firm is observed to have increased to $3714

million in the year 2017 as compared to $1414 million in the year 2016. This reflects an

increase in inflow of cash from different operational actions of the firm.

The cash flow from investing activities of the firm National Australia Bank is documented to

be ($313 million) in the year 2017 in comparison to ($9970 million) in the year 2016. This

shows an increase in outflow of cash for diverse purchases.

The cash outflow of ($331 million) from financing activities of the corporation can be noticed

during the period 2017 in comparison to the year ago period that registered an inflow of

$9496 million. This replicates outflow of cash stream in comparison to the inflow stream of

cash.

Particulars 2017 2016 % change

Cash Flow from Operating activities 3714 1414 162.6591

Cash flow from Investing Activities -313 -9970 -96.8606

Cash Flow from Financing Activities -331 9496 -103.486

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

ACCOUNTING FOR BUSINESS

Cash Flow from Operating

activities Cash flow from Investing

Activities Cash Flow from Financing

Acitvities

-15000

-10000

-5000

0

5000

10000

15000

Cash Flow Analysis

2017

2016

Analysis of financial position of the company by analysing the balance sheet

Critical analysis of the balance sheet statement of the firm NAB reveals that total assets of

firm increased to $788325 million in the year 2017 in comparison to $776710 million

registered during the year 2016. The increase in total assets of the firm is mainly due to

relative increase in quick assets, loans as well as advances, goodwill along with different

intangible assets (Sridharan 2015). The increase in assets of the firm during the current period

in comparison to the year ago period cam be considered to be a desirable financial condition

of the corporation (Titman et al. 2017).

2017 2016 % change

Assets 788325 776710 1.49541

Liabilities 737008 725395 1.600921

Net Assets 51317 51315 0.003897

Cash and Liquid Assets 43826 30630 43.08195

Total Equity 51306 51292 0.027295

Current Ratio 1.069629 1.070741

Quick Ratio 0.059465 0.042225

ACCOUNTING FOR BUSINESS

Cash Flow from Operating

activities Cash flow from Investing

Activities Cash Flow from Financing

Acitvities

-15000

-10000

-5000

0

5000

10000

15000

Cash Flow Analysis

2017

2016

Analysis of financial position of the company by analysing the balance sheet

Critical analysis of the balance sheet statement of the firm NAB reveals that total assets of

firm increased to $788325 million in the year 2017 in comparison to $776710 million

registered during the year 2016. The increase in total assets of the firm is mainly due to

relative increase in quick assets, loans as well as advances, goodwill along with different

intangible assets (Sridharan 2015). The increase in assets of the firm during the current period

in comparison to the year ago period cam be considered to be a desirable financial condition

of the corporation (Titman et al. 2017).

2017 2016 % change

Assets 788325 776710 1.49541

Liabilities 737008 725395 1.600921

Net Assets 51317 51315 0.003897

Cash and Liquid Assets 43826 30630 43.08195

Total Equity 51306 51292 0.027295

Current Ratio 1.069629 1.070741

Quick Ratio 0.059465 0.042225

9

ACCOUNTING FOR BUSINESS

2017 2016

770000

772000

774000

776000

778000

780000

782000

784000

786000

788000

790000

National Australia Bank-Assets

Assets

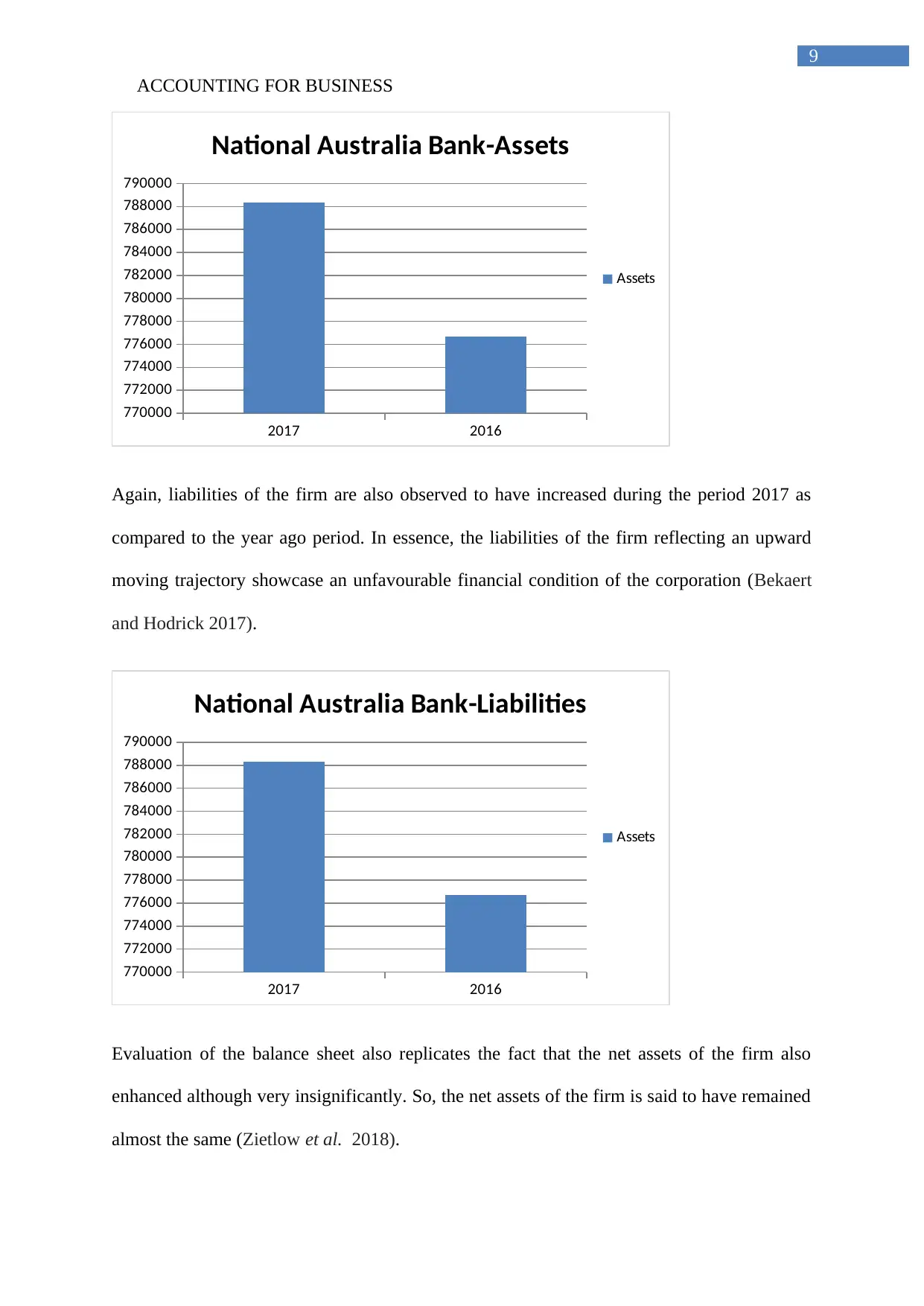

Again, liabilities of the firm are also observed to have increased during the period 2017 as

compared to the year ago period. In essence, the liabilities of the firm reflecting an upward

moving trajectory showcase an unfavourable financial condition of the corporation (Bekaert

and Hodrick 2017).

2017 2016

770000

772000

774000

776000

778000

780000

782000

784000

786000

788000

790000

National Australia Bank-Liabilities

Assets

Evaluation of the balance sheet also replicates the fact that the net assets of the firm also

enhanced although very insignificantly. So, the net assets of the firm is said to have remained

almost the same (Zietlow et al. 2018).

ACCOUNTING FOR BUSINESS

2017 2016

770000

772000

774000

776000

778000

780000

782000

784000

786000

788000

790000

National Australia Bank-Assets

Assets

Again, liabilities of the firm are also observed to have increased during the period 2017 as

compared to the year ago period. In essence, the liabilities of the firm reflecting an upward

moving trajectory showcase an unfavourable financial condition of the corporation (Bekaert

and Hodrick 2017).

2017 2016

770000

772000

774000

776000

778000

780000

782000

784000

786000

788000

790000

National Australia Bank-Liabilities

Assets

Evaluation of the balance sheet also replicates the fact that the net assets of the firm also

enhanced although very insignificantly. So, the net assets of the firm is said to have remained

almost the same (Zietlow et al. 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

ACCOUNTING FOR BUSINESS

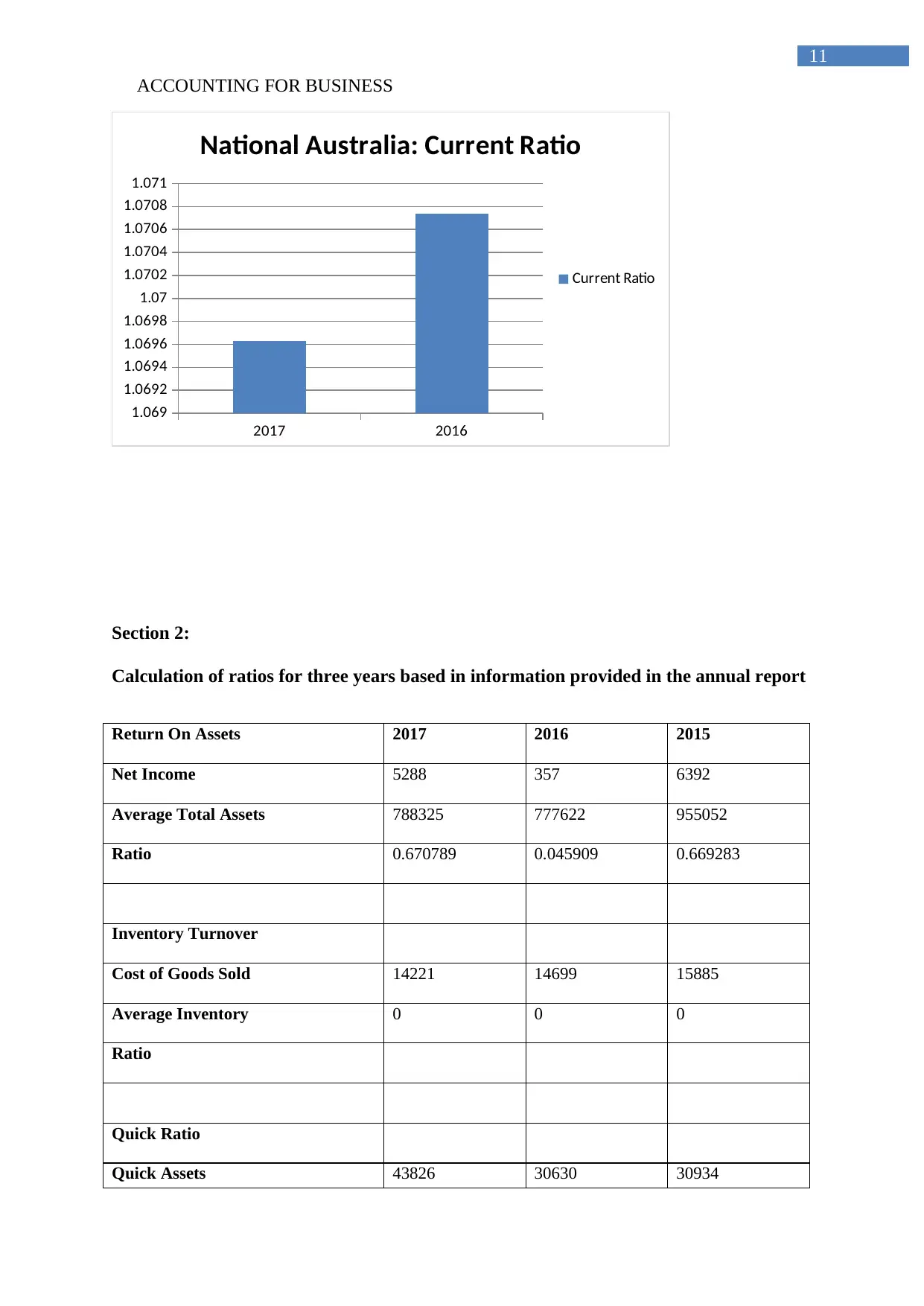

Current Ratio: Current ratio is a balance sheet ration that shows capability of the firm to pay

off the liabilities possessed by the firm in the short term period using the assets possessed by

the firm (Moutinho and Vargas-Sanchez 2018). Current ratio of the firm has decreased even

though insignificantly during the period 2017 in comparison to the period 2016. The decrease

in current ratio is said to be an undesirable financial condition as lower ratio indicates an

unfavourable condition. Also, the standard conventional current ratio is said to be 2:1 that

reflects assets of the firm is double to that of liabilities of the firm (Brigham et al. 2016).

Therefore, based on the industry standard it can be said that NAB has comparatively lower

current as well as quick ratio, reflecting undesirable financial condition.

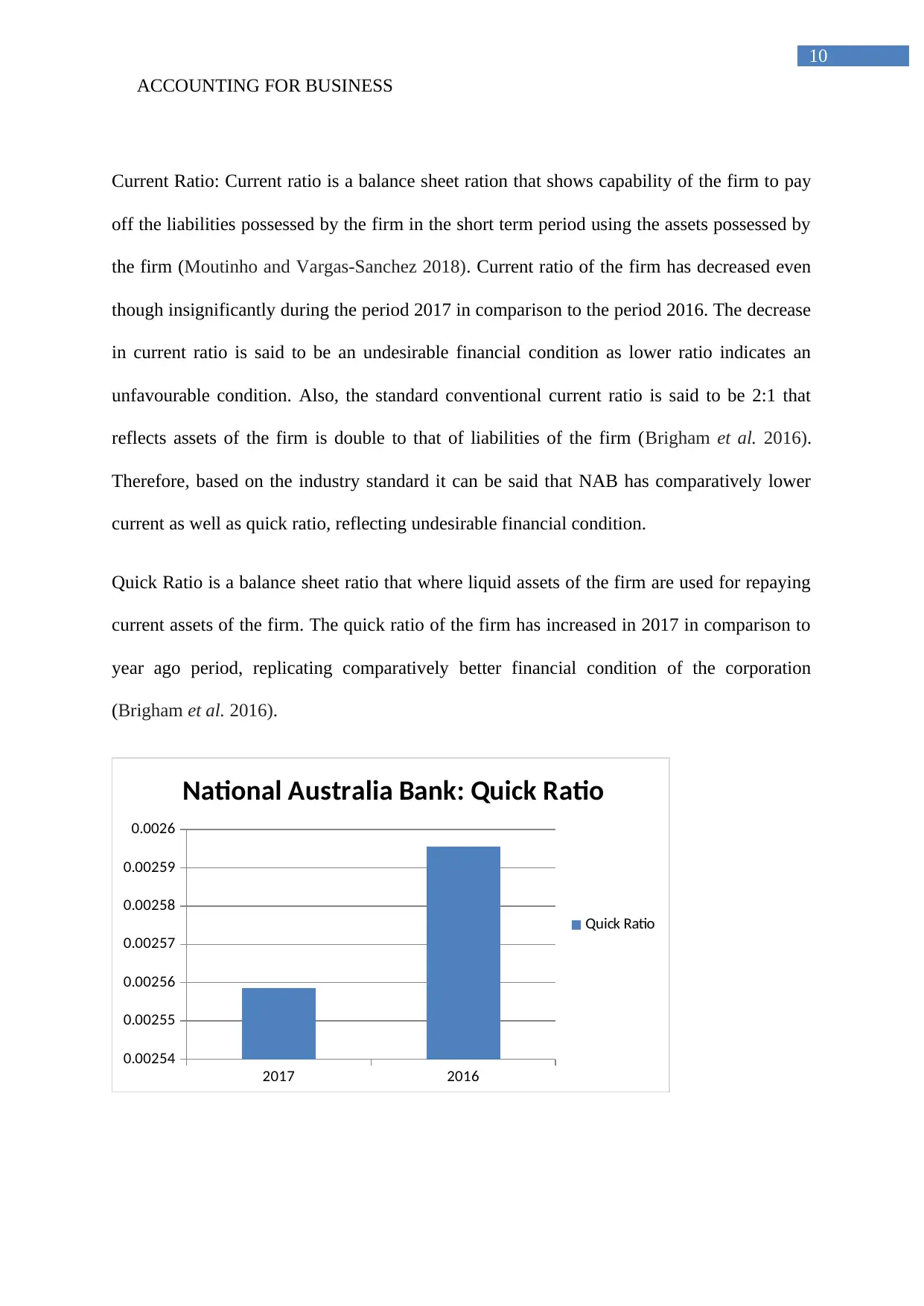

Quick Ratio is a balance sheet ratio that where liquid assets of the firm are used for repaying

current assets of the firm. The quick ratio of the firm has increased in 2017 in comparison to

year ago period, replicating comparatively better financial condition of the corporation

(Brigham et al. 2016).

2017 2016

0.00254

0.00255

0.00256

0.00257

0.00258

0.00259

0.0026

National Australia Bank: Quick Ratio

Quick Ratio

ACCOUNTING FOR BUSINESS

Current Ratio: Current ratio is a balance sheet ration that shows capability of the firm to pay

off the liabilities possessed by the firm in the short term period using the assets possessed by

the firm (Moutinho and Vargas-Sanchez 2018). Current ratio of the firm has decreased even

though insignificantly during the period 2017 in comparison to the period 2016. The decrease

in current ratio is said to be an undesirable financial condition as lower ratio indicates an

unfavourable condition. Also, the standard conventional current ratio is said to be 2:1 that

reflects assets of the firm is double to that of liabilities of the firm (Brigham et al. 2016).

Therefore, based on the industry standard it can be said that NAB has comparatively lower

current as well as quick ratio, reflecting undesirable financial condition.

Quick Ratio is a balance sheet ratio that where liquid assets of the firm are used for repaying

current assets of the firm. The quick ratio of the firm has increased in 2017 in comparison to

year ago period, replicating comparatively better financial condition of the corporation

(Brigham et al. 2016).

2017 2016

0.00254

0.00255

0.00256

0.00257

0.00258

0.00259

0.0026

National Australia Bank: Quick Ratio

Quick Ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

ACCOUNTING FOR BUSINESS

2017 2016

1.069

1.0692

1.0694

1.0696

1.0698

1.07

1.0702

1.0704

1.0706

1.0708

1.071

National Australia: Current Ratio

Current Ratio

Section 2:

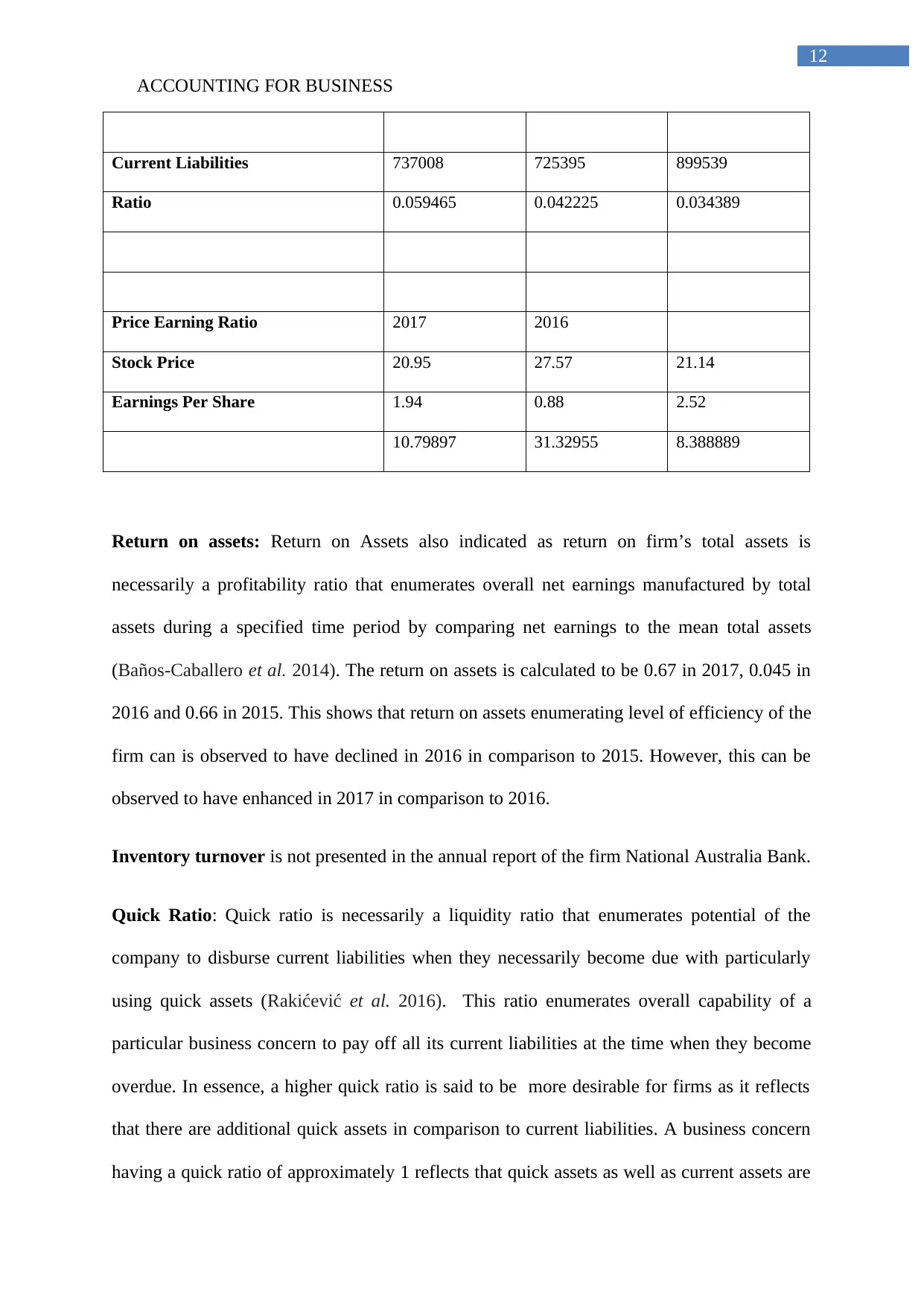

Calculation of ratios for three years based in information provided in the annual report

Return On Assets 2017 2016 2015

Net Income 5288 357 6392

Average Total Assets 788325 777622 955052

Ratio 0.670789 0.045909 0.669283

Inventory Turnover

Cost of Goods Sold 14221 14699 15885

Average Inventory 0 0 0

Ratio

Quick Ratio

Quick Assets 43826 30630 30934

ACCOUNTING FOR BUSINESS

2017 2016

1.069

1.0692

1.0694

1.0696

1.0698

1.07

1.0702

1.0704

1.0706

1.0708

1.071

National Australia: Current Ratio

Current Ratio

Section 2:

Calculation of ratios for three years based in information provided in the annual report

Return On Assets 2017 2016 2015

Net Income 5288 357 6392

Average Total Assets 788325 777622 955052

Ratio 0.670789 0.045909 0.669283

Inventory Turnover

Cost of Goods Sold 14221 14699 15885

Average Inventory 0 0 0

Ratio

Quick Ratio

Quick Assets 43826 30630 30934

12

ACCOUNTING FOR BUSINESS

Current Liabilities 737008 725395 899539

Ratio 0.059465 0.042225 0.034389

Price Earning Ratio 2017 2016

Stock Price 20.95 27.57 21.14

Earnings Per Share 1.94 0.88 2.52

10.79897 31.32955 8.388889

Return on assets: Return on Assets also indicated as return on firm’s total assets is

necessarily a profitability ratio that enumerates overall net earnings manufactured by total

assets during a specified time period by comparing net earnings to the mean total assets

(Baños-Caballero et al. 2014). The return on assets is calculated to be 0.67 in 2017, 0.045 in

2016 and 0.66 in 2015. This shows that return on assets enumerating level of efficiency of the

firm can is observed to have declined in 2016 in comparison to 2015. However, this can be

observed to have enhanced in 2017 in comparison to 2016.

Inventory turnover is not presented in the annual report of the firm National Australia Bank.

Quick Ratio: Quick ratio is necessarily a liquidity ratio that enumerates potential of the

company to disburse current liabilities when they necessarily become due with particularly

using quick assets (Rakićević et al. 2016). This ratio enumerates overall capability of a

particular business concern to pay off all its current liabilities at the time when they become

overdue. In essence, a higher quick ratio is said to be more desirable for firms as it reflects

that there are additional quick assets in comparison to current liabilities. A business concern

having a quick ratio of approximately 1 reflects that quick assets as well as current assets are

ACCOUNTING FOR BUSINESS

Current Liabilities 737008 725395 899539

Ratio 0.059465 0.042225 0.034389

Price Earning Ratio 2017 2016

Stock Price 20.95 27.57 21.14

Earnings Per Share 1.94 0.88 2.52

10.79897 31.32955 8.388889

Return on assets: Return on Assets also indicated as return on firm’s total assets is

necessarily a profitability ratio that enumerates overall net earnings manufactured by total

assets during a specified time period by comparing net earnings to the mean total assets

(Baños-Caballero et al. 2014). The return on assets is calculated to be 0.67 in 2017, 0.045 in

2016 and 0.66 in 2015. This shows that return on assets enumerating level of efficiency of the

firm can is observed to have declined in 2016 in comparison to 2015. However, this can be

observed to have enhanced in 2017 in comparison to 2016.

Inventory turnover is not presented in the annual report of the firm National Australia Bank.

Quick Ratio: Quick ratio is necessarily a liquidity ratio that enumerates potential of the

company to disburse current liabilities when they necessarily become due with particularly

using quick assets (Rakićević et al. 2016). This ratio enumerates overall capability of a

particular business concern to pay off all its current liabilities at the time when they become

overdue. In essence, a higher quick ratio is said to be more desirable for firms as it reflects

that there are additional quick assets in comparison to current liabilities. A business concern

having a quick ratio of approximately 1 reflects that quick assets as well as current assets are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.