Accounting for Managers: Cost Analysis and Overhead Allocation Report

VerifiedAdded on 2020/05/28

|12

|1693

|95

Report

AI Summary

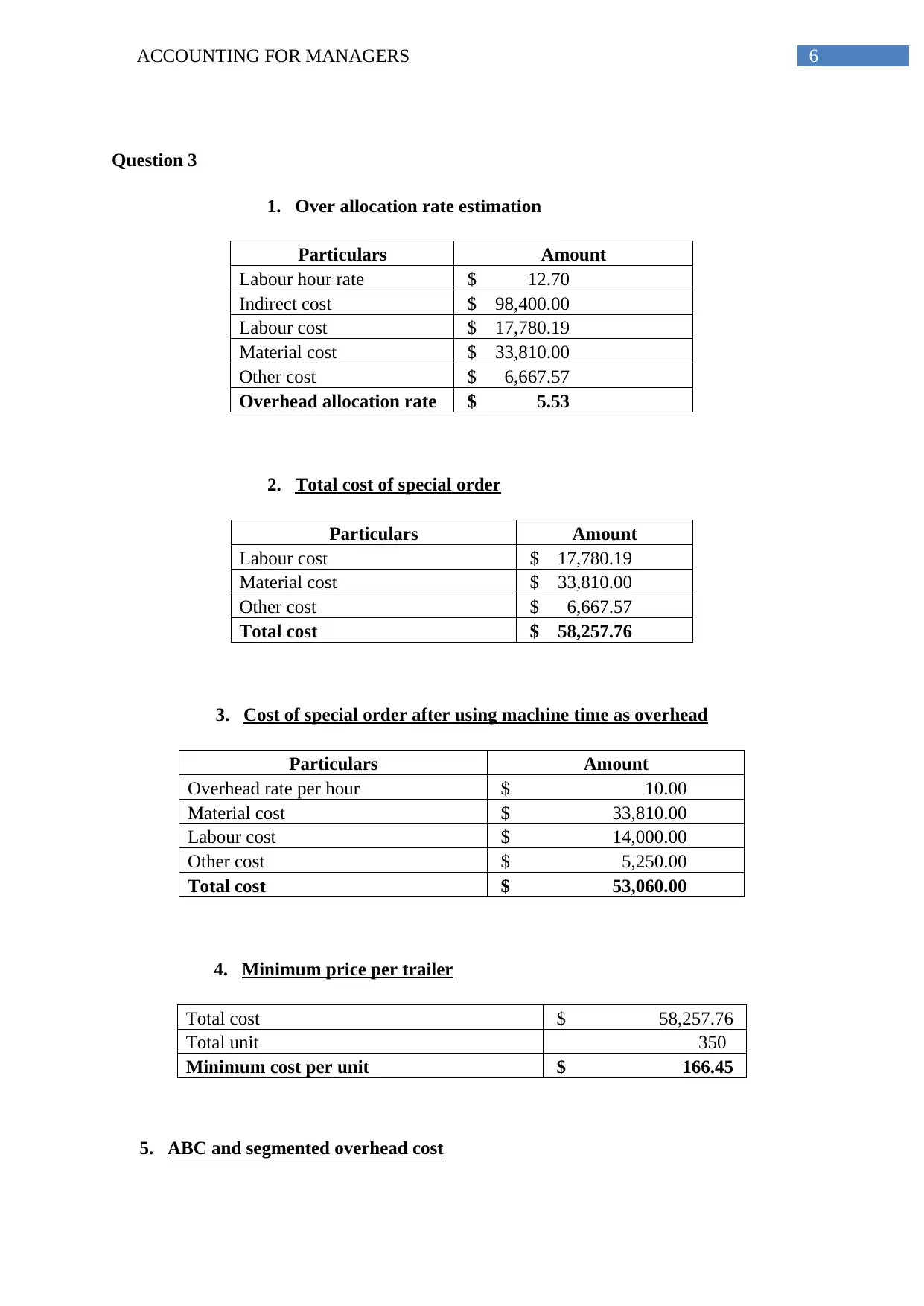

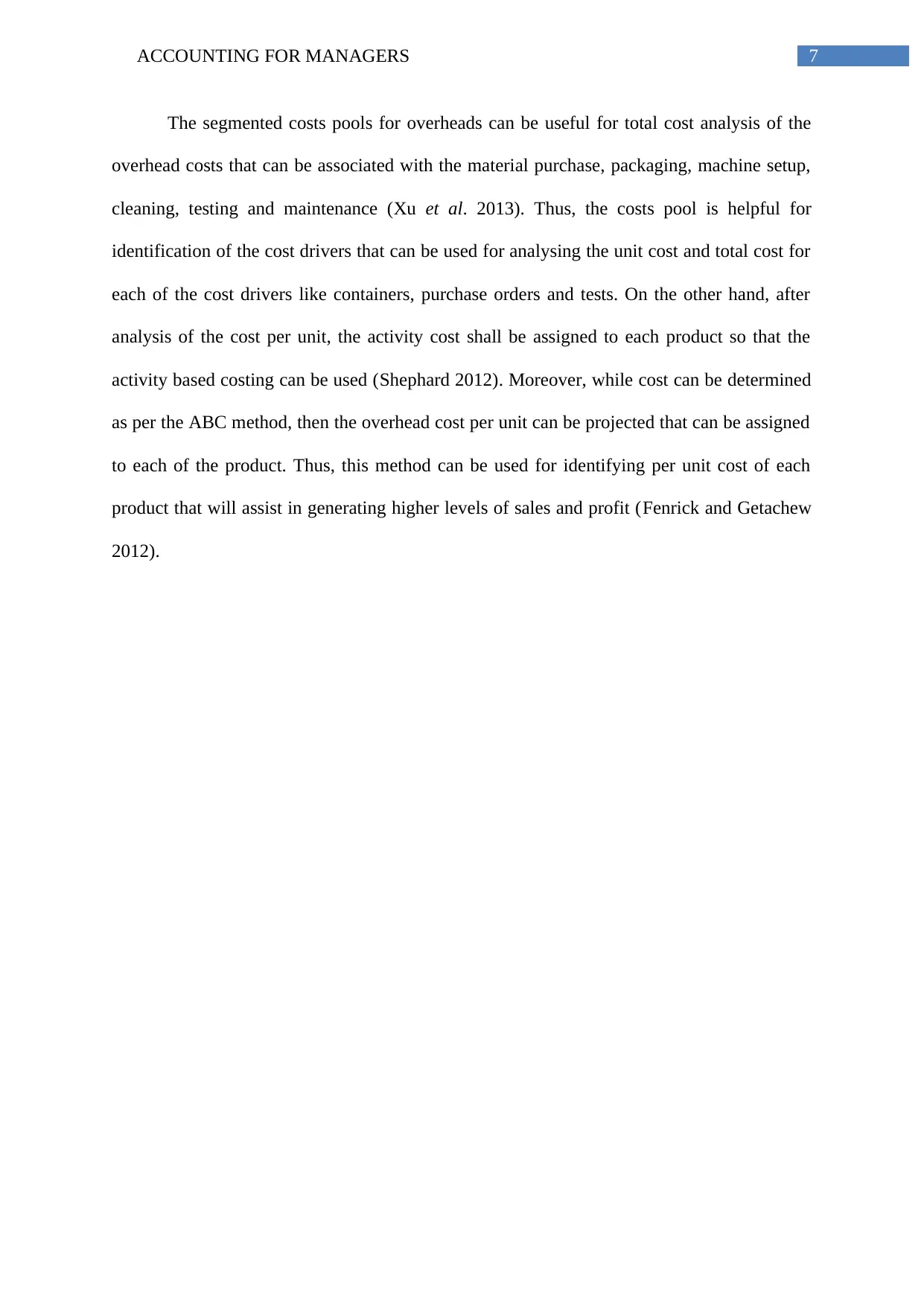

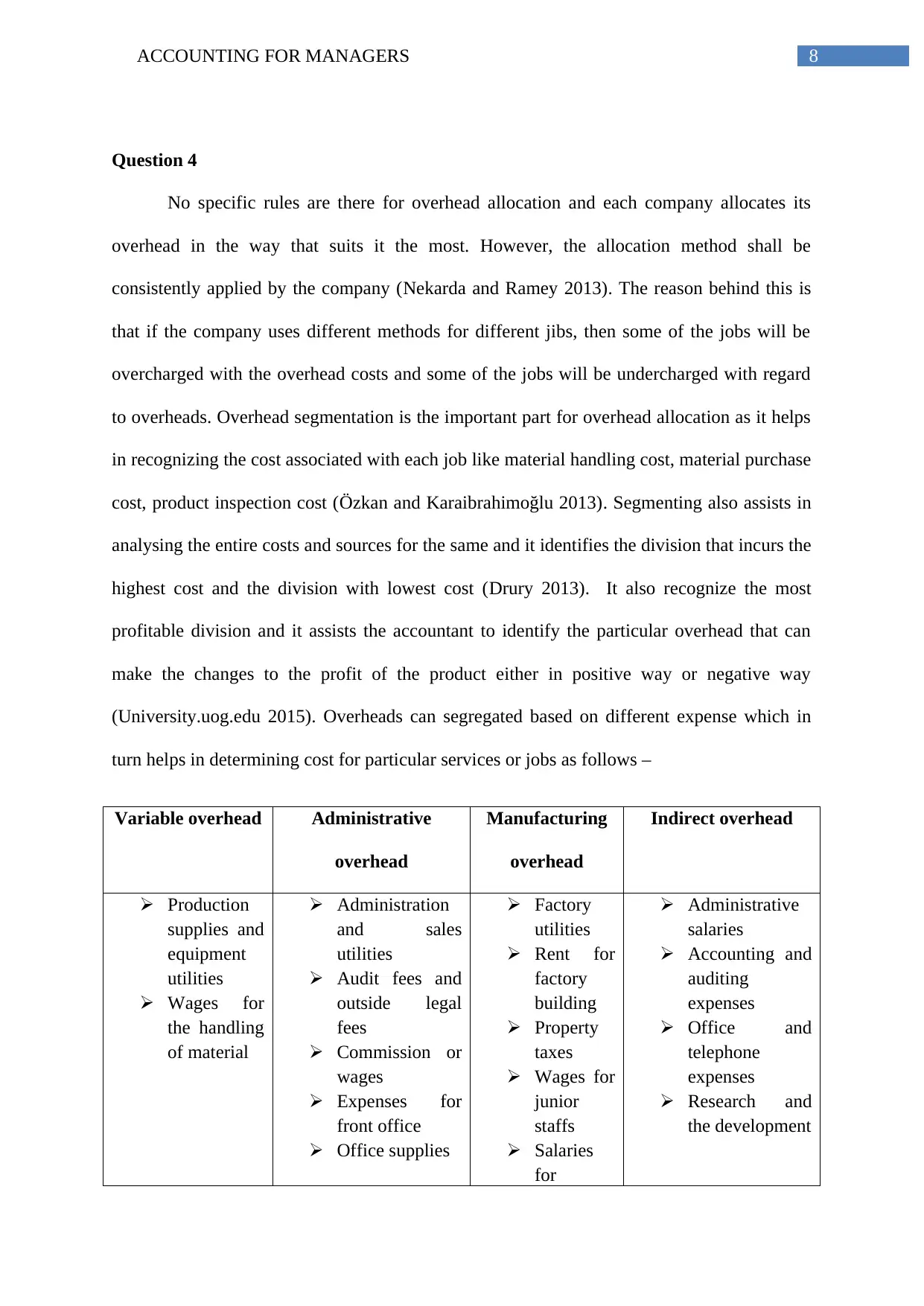

This report, titled "Accounting for Managers," analyzes the financial performance and cost structures of Bonza Handtools. It begins with an evaluation of three distinct proposals for increasing sales and profit, comparing their projected financial outcomes based on different strategies such as increased advertising, improved product quality, and promotional campaigns. The report then delves into a scenario-based analysis, assessing the impact of increased sales volume and reduced per-unit costs on overall profitability. Furthermore, the report examines overhead allocation methods, including the estimation of over-allocation rates and the application of Activity-Based Costing (ABC) for segmented overhead costs. Finally, the report explores the importance of overhead segmentation and allocation, emphasizing the use of consistent allocation methods and the identification of cost drivers to accurately reflect the costs associated with various services and jobs. The report uses examples to illustrate key concepts and provides references to support its findings.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.