Accounting Report: Financial Reporting and Gross Margin Analysis

VerifiedAdded on 2020/07/23

|7

|987

|46

Report

AI Summary

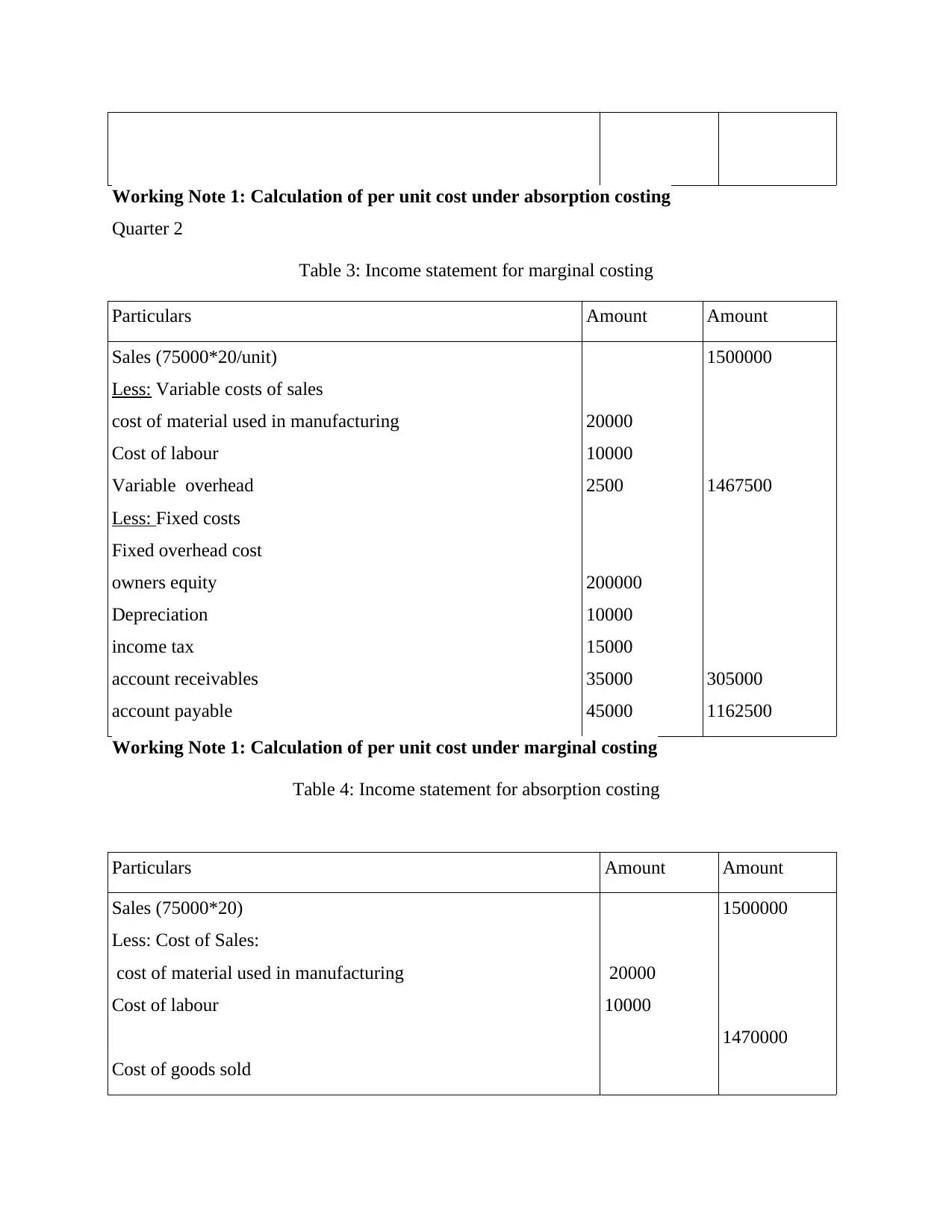

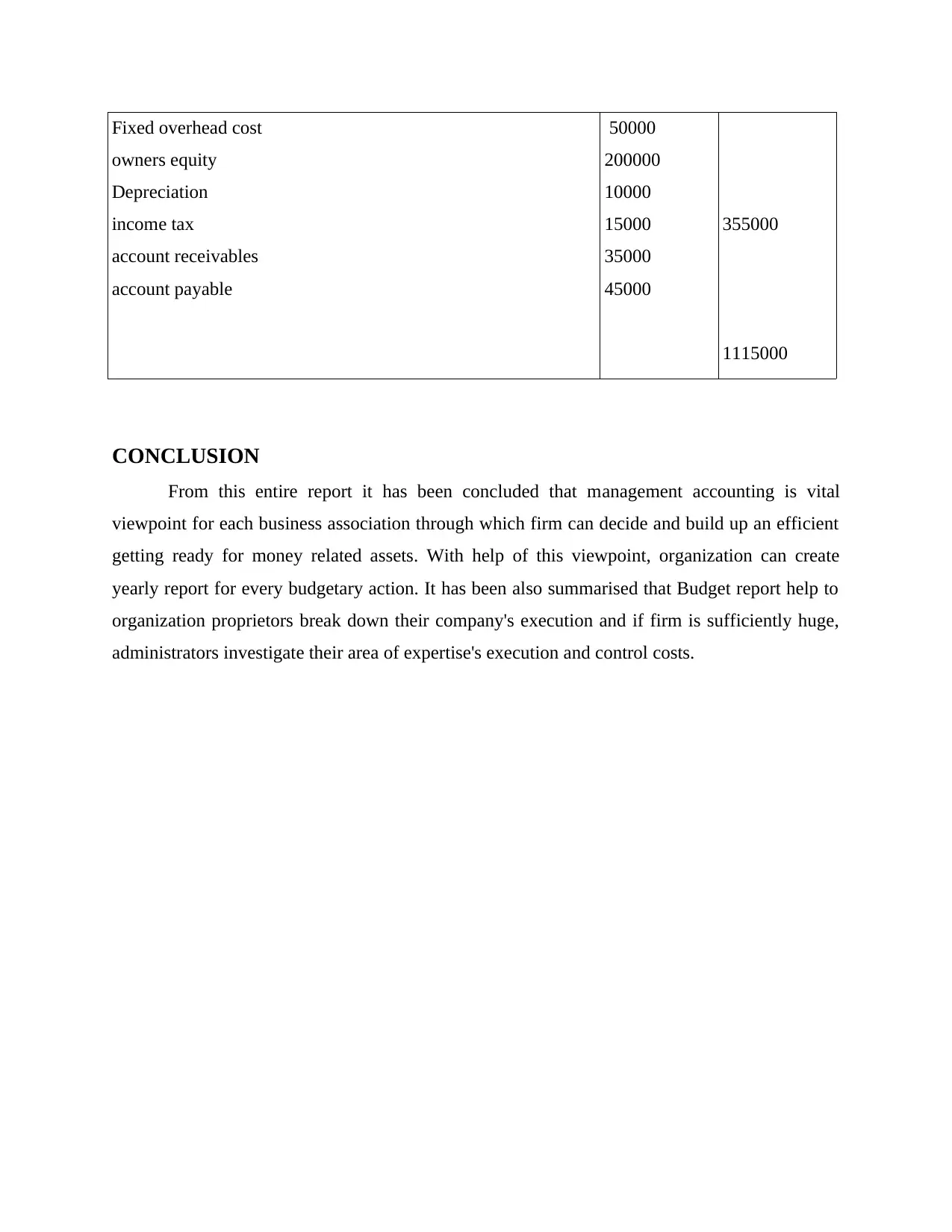

This report delves into the significance of management accounting within organizations, emphasizing its role in financial performance management. It explores the principles of management accounting and the responsibilities of accounting and financial managers. The report uses a scenario involving Para Sighting, a tourism company, to illustrate the importance of financial reporting for stakeholders, including investors and creditors, and its function in strategic planning and decision-making. Furthermore, the report includes income statements for both marginal and absorption costing methods for two quarters, enabling the calculation of gross margins. The conclusion highlights the importance of management accounting for effective financial resource planning and performance evaluation. The report is supported by relevant references to academic sources.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.