Comprehensive Management Accounting Report: Imda Ltd Analysis

VerifiedAdded on 2020/01/23

|18

|4742

|148

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles as applied to Imda Ltd, a producer of special chargers for mobile phones. The report explores the functions of management accounting, differentiating it from financial accounting and examining various management accounting systems, including financial, cost, inventory, and performance management systems. It then delves into the preparation of an income statement using both marginal and absorption costing methods to evaluate Imda Ltd's financial performance and aid in decision-making regarding product innovation. The report also covers different types of budgets, their advantages and drawbacks, and the budget preparation process. Furthermore, it addresses performance management strategies suitable for Imda Ltd. The analysis offers insights into Imda Ltd's financial position and provides recommendations for improving its monetary performance and business operations.

Management

Accounting

1

Accounting

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1) Functions of management accounting...................................................................................3

P2) Management accounting systems..........................................................................................5

TASK 2............................................................................................................................................6

P3) Income statement for Imda ltd...............................................................................................6

TASK 3 (p4)....................................................................................................................................9

a) Different types of budgets and their advantages and drawbacks.............................................9

b) Budget preparation process...................................................................................................11

c) Pricing strategies....................................................................................................................12

TASK 4 (p5)..................................................................................................................................13

Performance management for Imda ltd......................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCE.................................................................................................................................16

2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1) Functions of management accounting...................................................................................3

P2) Management accounting systems..........................................................................................5

TASK 2............................................................................................................................................6

P3) Income statement for Imda ltd...............................................................................................6

TASK 3 (p4)....................................................................................................................................9

a) Different types of budgets and their advantages and drawbacks.............................................9

b) Budget preparation process...................................................................................................11

c) Pricing strategies....................................................................................................................12

TASK 4 (p5)..................................................................................................................................13

Performance management for Imda ltd......................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCE.................................................................................................................................16

2

INTRODUCTION

Management accounting is a multidisciplinary approach that is useful for making

decisions and preparing planning for effective business operations. It decision making tool for

operating business activities and improving its efficiencies. The present report is based on

understanding different aspects of management accounting for Imda ltd. It is producer of special

charger for mobile telephone and its gadgets. In this regard, different functions of management

accounting and their systems can be described. However, income statement preparation through

marginal and absorption costing is to be presented for decision making to produce and

supplement goods through this assignment. Including this, several kinds of budgets including

critical evaluation on them is to be expressed through that leads to analyzing actual performance

of organization and improving efficiencies for further business operations. Moreover, different

ideas for maintaining performance and non-performance of Imda ltd can be understood. Thus,

learners are able to understand various management accounting aspects through this report for

effectiveness of mobile gadgets for proper management effectively.

TASK 1

P1) Functions of management accounting

Management accounting is essential for making decisions related to quality services of

organization. It includes analysis of actual organization's performance and generating different

ideas for management of overall business operations. In this regard, various tools and techniques

are used including costing, budgeting, preparing income statement, ratio analysis and so on.

However, on the basis of this analyzing company's performance, further decisions are made to

improving efficiencies of company efficiently (Bogt, Helden and Kolk, 2015). It is quite

different from financial accounting that is interrelated with economic performance and non -

monetary operations. Therefore, financial accounting is quite different from management

accounting that can be expressed as below:-

Financial accounting:- Under this accounting system, all transactions are recorded

related for exchanging goods and services. In accordance to this, incurred costs on expenditures

and gained revenue are recorded for implementing further business operations. However,

effective financial information are gained through this accounting system for creating balance

3

Management accounting is a multidisciplinary approach that is useful for making

decisions and preparing planning for effective business operations. It decision making tool for

operating business activities and improving its efficiencies. The present report is based on

understanding different aspects of management accounting for Imda ltd. It is producer of special

charger for mobile telephone and its gadgets. In this regard, different functions of management

accounting and their systems can be described. However, income statement preparation through

marginal and absorption costing is to be presented for decision making to produce and

supplement goods through this assignment. Including this, several kinds of budgets including

critical evaluation on them is to be expressed through that leads to analyzing actual performance

of organization and improving efficiencies for further business operations. Moreover, different

ideas for maintaining performance and non-performance of Imda ltd can be understood. Thus,

learners are able to understand various management accounting aspects through this report for

effectiveness of mobile gadgets for proper management effectively.

TASK 1

P1) Functions of management accounting

Management accounting is essential for making decisions related to quality services of

organization. It includes analysis of actual organization's performance and generating different

ideas for management of overall business operations. In this regard, various tools and techniques

are used including costing, budgeting, preparing income statement, ratio analysis and so on.

However, on the basis of this analyzing company's performance, further decisions are made to

improving efficiencies of company efficiently (Bogt, Helden and Kolk, 2015). It is quite

different from financial accounting that is interrelated with economic performance and non -

monetary operations. Therefore, financial accounting is quite different from management

accounting that can be expressed as below:-

Financial accounting:- Under this accounting system, all transactions are recorded

related for exchanging goods and services. In accordance to this, incurred costs on expenditures

and gained revenue are recorded for implementing further business operations. However,

effective financial information are gained through this accounting system for creating balance

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

between income and expenses effectively (Chan, Wang and Raffoni, 2014). Therefore, financial

accounting is essential for company's cash account increment and for transactions, creating debit

amount similar to credit amount.

Differences between financial and management accounting:- It is analyzed that

financial and management accounting systems are different from each other. Under which,

financial accounting is related to presenting economic performance of entity and on the basis of

this analysis strategies are prepared for financial development, relevance and reliability

(Chenhall and Moers, 2015). In addition to this, different financial statements are analyzed

including profit and loss account, balance sheet, cash flow-fund flow and so on.

While, on the other hand, management accounting involves all activities of business

organization including production and distribution of goods, performance management, income

statement as well preparing financial statements etc. However, it is wide in concept as well

remains useful for management of entire business activities. In addition to this, effectiveness of

business organization is gained through analyzing all tools and further making decisions to

implement action plans effectively (Costa and et.al., 2016). Thus, financial accounting is

different from management accounting for operating business operations and making decisions

regarding financial and non-monetary tools analysis. In this regard, comparison between

financial and management accounting can be expressed as below:-

Bases Financial accounting Management accounting

Purposes To disclose Imda ltd

financial performance

on a specific time.

To present end result as

profit and loss gained

by organization.

To help management

through financial

statement analysis.

To prepare strategies

and making decisions

for further

implementation and

effectiveness of firm.

Appropriate for users External users Mainly for internal users

Legal requirements It is needed according to law It is choice

4

accounting is essential for company's cash account increment and for transactions, creating debit

amount similar to credit amount.

Differences between financial and management accounting:- It is analyzed that

financial and management accounting systems are different from each other. Under which,

financial accounting is related to presenting economic performance of entity and on the basis of

this analysis strategies are prepared for financial development, relevance and reliability

(Chenhall and Moers, 2015). In addition to this, different financial statements are analyzed

including profit and loss account, balance sheet, cash flow-fund flow and so on.

While, on the other hand, management accounting involves all activities of business

organization including production and distribution of goods, performance management, income

statement as well preparing financial statements etc. However, it is wide in concept as well

remains useful for management of entire business activities. In addition to this, effectiveness of

business organization is gained through analyzing all tools and further making decisions to

implement action plans effectively (Costa and et.al., 2016). Thus, financial accounting is

different from management accounting for operating business operations and making decisions

regarding financial and non-monetary tools analysis. In this regard, comparison between

financial and management accounting can be expressed as below:-

Bases Financial accounting Management accounting

Purposes To disclose Imda ltd

financial performance

on a specific time.

To present end result as

profit and loss gained

by organization.

To help management

through financial

statement analysis.

To prepare strategies

and making decisions

for further

implementation and

effectiveness of firm.

Appropriate for users External users Mainly for internal users

Legal requirements It is needed according to law It is choice

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and tax

Time periodicity Generally year to year Prepared frequently in

accordance to choice

Accounting method Double entry systems Not based on double entry

system

P2) Management accounting systems

There are different kinds of management accounting systems are used for decision

making process regarding business operations. Under this system, management accountant of

Imda Ltd analyzes financial statements by which monetary position of organization is analyzed.

On the basis of analyzing these tools, further ideas are created for entity's effectiveness and

improving its efficiencies (De Waal, 2013). However, different management accounting systems

can be understood as below:- Financial accounting system:- This system involves several kinds of tools to present

economic performance of organization. In accordance to this, different statements are

analyzed including income statement, balance sheet, cash flow/ fund flow and so on.

Therefore, accounting for financial performance and its effectiveness is created for

improving monetary position effectively (Fullerton, Kennedy and Widener, 2014). Thus,

on the basis of analyzing these statements, further implementation and organization's

financial development can be achieved effectively. Cost accounting systems:- Through costing method, proper price determination that is a

process to set cost of products produced by organization. It is beneficial for cost

effectiveness and making appropriate decisions related to production and distribution of

goods provided by Imda Ltd. In this process, price is set for product according to incurred

cost on expenditures including material, labor and additional overhead. Thus, cost

accounting system, adequate cost of goods is decided that affects further production and

supplement of goods efficiently (Guffey, 2014). Inventory management system:- In this process, management of inventories is obtained

by which decision on putting goods safe and resource allocation is gained. However, for

5

Time periodicity Generally year to year Prepared frequently in

accordance to choice

Accounting method Double entry systems Not based on double entry

system

P2) Management accounting systems

There are different kinds of management accounting systems are used for decision

making process regarding business operations. Under this system, management accountant of

Imda Ltd analyzes financial statements by which monetary position of organization is analyzed.

On the basis of analyzing these tools, further ideas are created for entity's effectiveness and

improving its efficiencies (De Waal, 2013). However, different management accounting systems

can be understood as below:- Financial accounting system:- This system involves several kinds of tools to present

economic performance of organization. In accordance to this, different statements are

analyzed including income statement, balance sheet, cash flow/ fund flow and so on.

Therefore, accounting for financial performance and its effectiveness is created for

improving monetary position effectively (Fullerton, Kennedy and Widener, 2014). Thus,

on the basis of analyzing these statements, further implementation and organization's

financial development can be achieved effectively. Cost accounting systems:- Through costing method, proper price determination that is a

process to set cost of products produced by organization. It is beneficial for cost

effectiveness and making appropriate decisions related to production and distribution of

goods provided by Imda Ltd. In this process, price is set for product according to incurred

cost on expenditures including material, labor and additional overhead. Thus, cost

accounting system, adequate cost of goods is decided that affects further production and

supplement of goods efficiently (Guffey, 2014). Inventory management system:- In this process, management of inventories is obtained

by which decision on putting goods safe and resource allocation is gained. However, for

5

managing inventories, planning is implemented that affects resource management and

also helpful for reducing excess of production and materials. Thus, inventory

management system is related to putting goods safe and making decision regarding place

for providing goods and services of firm (Jiwani and et.al., 2014). In addition to this, it is

considered as management accounting segment for proper planning and decision to

operate further business activities.

Performance management system:- As management accounting is multi-disciplinary

approach that focuses on overall business operations. Therefore, management accountant

of Imda Ltd analyzes performance of employees and organization that proceed to make

decisions for enhancing working efficiencies (Kull and et.al., 2014). Including this,

performance management system is interrelated with entire planning procedure and

decision making process for better quality services and improving effectiveness at high

level.

TASK 2

P3) Income statement for Imda ltd

Income statement is a tool that presents financial performance of Imda tech. Through this

analysis, earned income and incurred expenditures. In this regard, cost of products is evaluated

that on the basis of which income prepared for improving efficiencies and financial development

of firm. It is done through different methods such as marginal, absorption, market demand and

competitive basis. Therefore, by using costing methods, price of goods and services is

determined for further production and distribution of goods (Lapsley and Rekers, 2016).

Including this, financial position of organization is gained through this process thereby effective

fund allocation and profitability can be enhanced properly. However, for preparing income

statement, at first gross and net profit is evaluated.

As per the given case scenario, it is analyze that Imda limited is planning for producing

special charger for mobile telephone and other equipment. Therefore, decisions are made for

further investment by using costing methods. Under this process system, cost incurred on

expenses are analyzed through last years' transactions. By which, cost is calculated for further

production and supplement of mobile charger (Najjar, Strickland and Kaplan, 2016). Costing

method including marginal and absorption can be understood as below:-

6

also helpful for reducing excess of production and materials. Thus, inventory

management system is related to putting goods safe and making decision regarding place

for providing goods and services of firm (Jiwani and et.al., 2014). In addition to this, it is

considered as management accounting segment for proper planning and decision to

operate further business activities.

Performance management system:- As management accounting is multi-disciplinary

approach that focuses on overall business operations. Therefore, management accountant

of Imda Ltd analyzes performance of employees and organization that proceed to make

decisions for enhancing working efficiencies (Kull and et.al., 2014). Including this,

performance management system is interrelated with entire planning procedure and

decision making process for better quality services and improving effectiveness at high

level.

TASK 2

P3) Income statement for Imda ltd

Income statement is a tool that presents financial performance of Imda tech. Through this

analysis, earned income and incurred expenditures. In this regard, cost of products is evaluated

that on the basis of which income prepared for improving efficiencies and financial development

of firm. It is done through different methods such as marginal, absorption, market demand and

competitive basis. Therefore, by using costing methods, price of goods and services is

determined for further production and distribution of goods (Lapsley and Rekers, 2016).

Including this, financial position of organization is gained through this process thereby effective

fund allocation and profitability can be enhanced properly. However, for preparing income

statement, at first gross and net profit is evaluated.

As per the given case scenario, it is analyze that Imda limited is planning for producing

special charger for mobile telephone and other equipment. Therefore, decisions are made for

further investment by using costing methods. Under this process system, cost incurred on

expenses are analyzed through last years' transactions. By which, cost is calculated for further

production and supplement of mobile charger (Najjar, Strickland and Kaplan, 2016). Costing

method including marginal and absorption can be understood as below:-

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

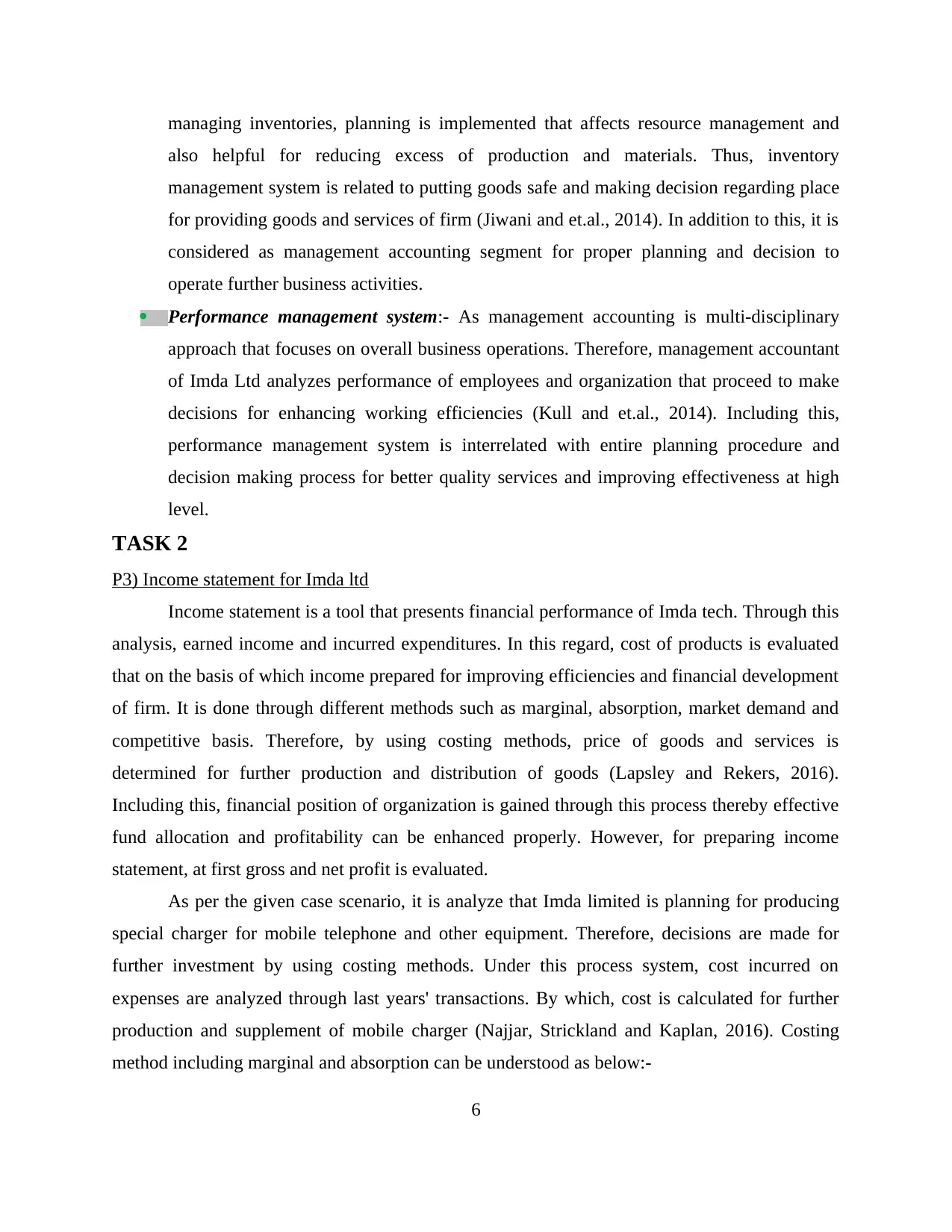

Marginal costing:- It is suitable for decision making for short term period. However, for

calculating net profit or loss, gross profit is deducted with cost incurred on variable production.

In this regard, through marginal costing, income statement is presented to achieve organization's

profit earning capacity. In addition to this, marginal costing is related to price determination

process for making decision regarding further production and distribution of goods and services

in future time (Nuhu, Baird and Bala, 2016). In accordance to this, net profit for organization can

be evaluated through following costing method:-

Interpretation:- By calculating marginal costing, it is evaluated that Imda ltd has gained

effective profit but so that company invest for innovations related to mobile gadgets. In this

regard, cost incurred on fixed assets is not included to calculate net profit. Therefore, gross profit

is evaluated as 22500 for which selling price of goods is 52500 which is deducted with

production for services is 30000. Further, gross profit is deducted with non-operating expenses

for administration and selling expenditures. However, net profit is measured as 4625. It can be

decided for organization to not invest for mobile gadgets.

Absorption costing:- Through this costing method, net profit is determined by deducting

gross profit with overall cost incurred on variable and fixed production. It is appropriate for long

term planning procedure and making decisions for high level of investment (Schaltegger,

7

calculating net profit or loss, gross profit is deducted with cost incurred on variable production.

In this regard, through marginal costing, income statement is presented to achieve organization's

profit earning capacity. In addition to this, marginal costing is related to price determination

process for making decision regarding further production and distribution of goods and services

in future time (Nuhu, Baird and Bala, 2016). In accordance to this, net profit for organization can

be evaluated through following costing method:-

Interpretation:- By calculating marginal costing, it is evaluated that Imda ltd has gained

effective profit but so that company invest for innovations related to mobile gadgets. In this

regard, cost incurred on fixed assets is not included to calculate net profit. Therefore, gross profit

is evaluated as 22500 for which selling price of goods is 52500 which is deducted with

production for services is 30000. Further, gross profit is deducted with non-operating expenses

for administration and selling expenditures. However, net profit is measured as 4625. It can be

decided for organization to not invest for mobile gadgets.

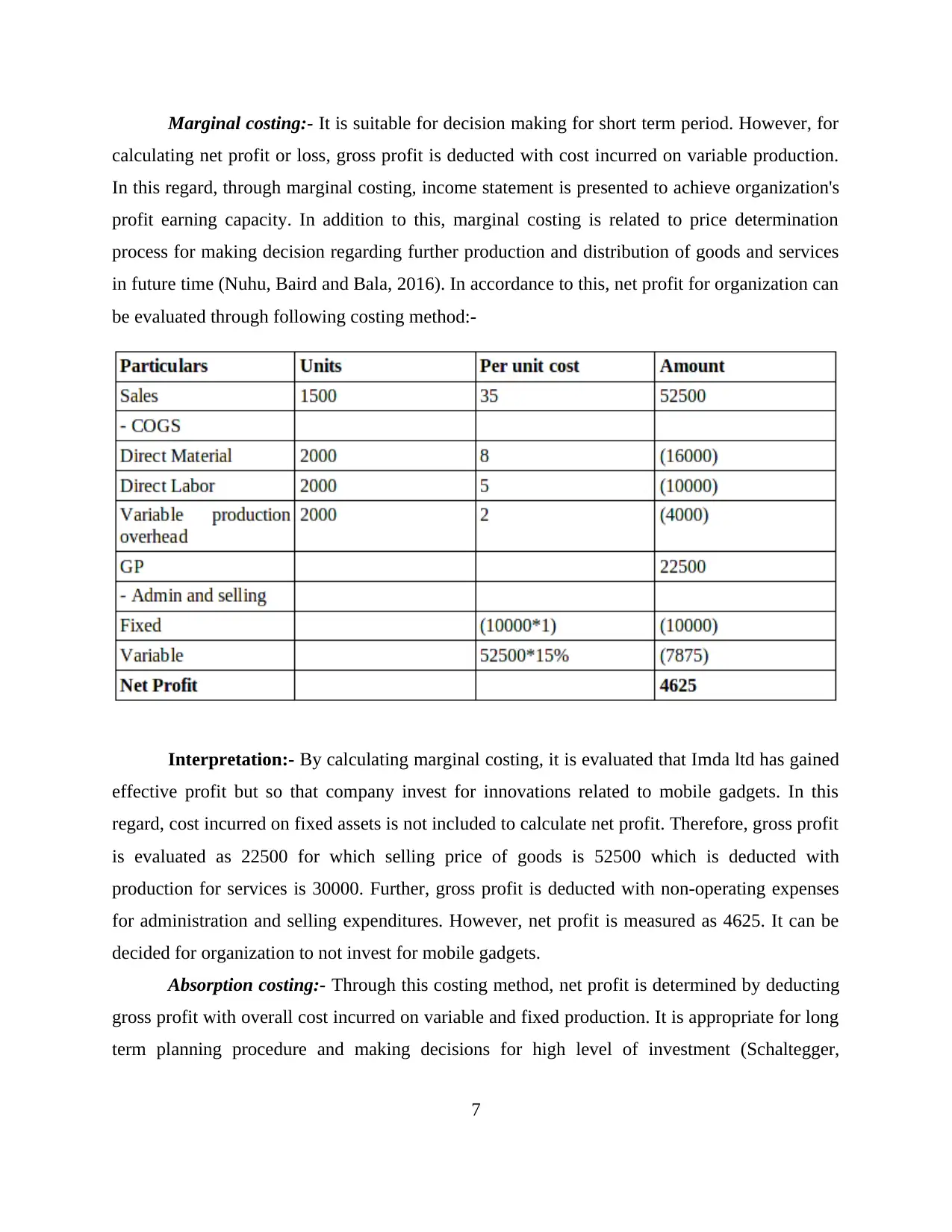

Absorption costing:- Through this costing method, net profit is determined by deducting

gross profit with overall cost incurred on variable and fixed production. It is appropriate for long

term planning procedure and making decisions for high level of investment (Schaltegger,

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Gibassier and Zvezdov, 2013). For this costing method, cost incurred on fixed assets is added to

variable costs therefore decisions are made regarding large scale of investment and operating

business activities for longs time periodicity. Thus, absorption costing method is useful for long

term decision making process and sustaining organization's value. In this process, Imda ltd

company's performance can be analyzed through following net profit or loss interpretation as:-

Interpretation:- It is interpreted that in September, Imda ltd has sold out 1500 units in

which per unit cost is 35. Therefore, amount evaluated as 52500. However, it is deducted with

cost of goods sold including price incurred on direct material, labor and overhead. Units

produced on all of three components was 2000 and per unit cost was 8, 5, 2 for variable

production and 5 for fixed production. However, expenses for material, labor and overhead is

analyzed as 16000, 10000, 4000 (variable production) and 10,000 for fixed production overhead.

Thus, gross profit is gained as 12500 which is moderate to present financial performance of Imda

ltd. For calculating net profit, gross profit is deducted with expenses incurred on admin and

selling of goods produced by organization. In this regard, company has got net loss as (-) 5375. It

is due to imbalanced production and distribution of mobile gadgets. Thus, according to this

8

variable costs therefore decisions are made regarding large scale of investment and operating

business activities for longs time periodicity. Thus, absorption costing method is useful for long

term decision making process and sustaining organization's value. In this process, Imda ltd

company's performance can be analyzed through following net profit or loss interpretation as:-

Interpretation:- It is interpreted that in September, Imda ltd has sold out 1500 units in

which per unit cost is 35. Therefore, amount evaluated as 52500. However, it is deducted with

cost of goods sold including price incurred on direct material, labor and overhead. Units

produced on all of three components was 2000 and per unit cost was 8, 5, 2 for variable

production and 5 for fixed production. However, expenses for material, labor and overhead is

analyzed as 16000, 10000, 4000 (variable production) and 10,000 for fixed production overhead.

Thus, gross profit is gained as 12500 which is moderate to present financial performance of Imda

ltd. For calculating net profit, gross profit is deducted with expenses incurred on admin and

selling of goods produced by organization. In this regard, company has got net loss as (-) 5375. It

is due to imbalanced production and distribution of mobile gadgets. Thus, according to this

8

interpretation, it is analyzed that company's financial position is not so efficient for further

investment to produce special kind of charger. Hence, there should not be investment for this

innovation.

Thus, it is recognized that financial position of Imda ltd is not so effective for investing

for mobile gadgets. In this regard, different strategies are required to be implemented for

economic stability and improving monetary performance effectively.

TASK 3 (P4)

a) Different types of budgets and their advantages and drawbacks

Budget is a management accounting technique by which current position of organization

is gained and also further different strategies are implemented. However, it is useful for best

allocation of resources and fund that affects productivity and profitability of organization

(Shields and et.al., 2015). There are five types of budget in management accounting, some of

them can be understood as follows:-

Master Budget

Operational Budget

Cash flow Budget

Financial Budget

Static Budget

Master Budget: A budget is a detailed projection of the manner in which management

needs to manage different aspects of its business during a particular year (Venkatnarayan and

et.al., 2014). Master budget is summarized form of estimated of cash budget, budgeted income

statement and budgeted balance sheet.

The advantages are:

It gives an overview of the whole budget that has been allotted to the different

departments.

It helps in determining the problems before hand and planning ahead.

The disadvantages are:

One cannot be specific since; the master budget is an overview of all the department’s

expenses and earnings.

9

investment to produce special kind of charger. Hence, there should not be investment for this

innovation.

Thus, it is recognized that financial position of Imda ltd is not so effective for investing

for mobile gadgets. In this regard, different strategies are required to be implemented for

economic stability and improving monetary performance effectively.

TASK 3 (P4)

a) Different types of budgets and their advantages and drawbacks

Budget is a management accounting technique by which current position of organization

is gained and also further different strategies are implemented. However, it is useful for best

allocation of resources and fund that affects productivity and profitability of organization

(Shields and et.al., 2015). There are five types of budget in management accounting, some of

them can be understood as follows:-

Master Budget

Operational Budget

Cash flow Budget

Financial Budget

Static Budget

Master Budget: A budget is a detailed projection of the manner in which management

needs to manage different aspects of its business during a particular year (Venkatnarayan and

et.al., 2014). Master budget is summarized form of estimated of cash budget, budgeted income

statement and budgeted balance sheet.

The advantages are:

It gives an overview of the whole budget that has been allotted to the different

departments.

It helps in determining the problems before hand and planning ahead.

The disadvantages are:

One cannot be specific since; the master budget is an overview of all the department’s

expenses and earnings.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Master budget can prove to be baseless at the time of uncertainty in any of the

department.

Operational Budget: It includes budgeted revenue and expenses of the company on day

to day basis. It helps to identify the fields where a company spends its money and in what areas

company is required to spend more (Bogt, Helden and Kolk, 2015).

The advantages are:

A small business can allocate budget for current quarters and upcoming quarters.

It keeps a check on the spending of the company and restricts unproductive expenses.

The disadvantages are:

Inaccuracy can lead to heavy losses.

Financial information keeps changing month to month. Therefore, it demands to make

assumptions in the budget accordingly.

Cash Flow Budget: It is an estimate of cash receipts and expenditure in a certain time

period. It predicts the company’s liquidity, whether the company have enough cash inflow to

meet out its expenses or is it falling short of cash.

The advantages are:

It predicts if there is enough cash inflow that can be utilized in various other productive

activities.

It identifies the cash that can be used to fulfill immediate short term obligations without

utilizing overdraft protection or line of credit.

The disadvantages are:

Relying on the estimates which has been prepared based in previous year’s cash flow

may not work every year.

At times, liquidity of a company doesn’t define the performance of the company.

Financial Budget: Financial budget those budgets in which the organization prepare all

the transaction of the year and plan how much money to be spent in which sector and shown in

company s balance sheet at the year end (Shields and et.al., 2015). It shows the effect of planned

operations and capital investments on assets and liabilities.

The advantages are:

10

department.

Operational Budget: It includes budgeted revenue and expenses of the company on day

to day basis. It helps to identify the fields where a company spends its money and in what areas

company is required to spend more (Bogt, Helden and Kolk, 2015).

The advantages are:

A small business can allocate budget for current quarters and upcoming quarters.

It keeps a check on the spending of the company and restricts unproductive expenses.

The disadvantages are:

Inaccuracy can lead to heavy losses.

Financial information keeps changing month to month. Therefore, it demands to make

assumptions in the budget accordingly.

Cash Flow Budget: It is an estimate of cash receipts and expenditure in a certain time

period. It predicts the company’s liquidity, whether the company have enough cash inflow to

meet out its expenses or is it falling short of cash.

The advantages are:

It predicts if there is enough cash inflow that can be utilized in various other productive

activities.

It identifies the cash that can be used to fulfill immediate short term obligations without

utilizing overdraft protection or line of credit.

The disadvantages are:

Relying on the estimates which has been prepared based in previous year’s cash flow

may not work every year.

At times, liquidity of a company doesn’t define the performance of the company.

Financial Budget: Financial budget those budgets in which the organization prepare all

the transaction of the year and plan how much money to be spent in which sector and shown in

company s balance sheet at the year end (Shields and et.al., 2015). It shows the effect of planned

operations and capital investments on assets and liabilities.

The advantages are:

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Having financial budget, a company can recognize and utilize the opportunities which

can help a company to expand

There can be a good control on credits of the company if it is aware about its financials

beforehand.

The disadvantages are:

Inaccuracy in the budget can lead to wrong financial decision making.

Due to the dynamic environment, department may not achieve the budgeted results.

Static Budget: It is a budget which remains same even when the volume changes. It is

fixed for the entire period. This kind of budget is used when the sales of a company is highly

predictable.

The advantages are:

It is east to implement and follow.

It allows a company to see its estimation of expenses and accordingly change the

strategy.

The disadvantages are:

Lack of flexibility.

It company find out that it is underperforming than it cannot allocate additional resources.

b) Budget preparation process

A budget procedure refers to process by which governance make and approve a budget

for a final presentation of budget at the end of financial year at 31st march (Stiepen, Gérard

and Soret, 2016).

The finance department prepare written record or legal document of all the transactions

of the year from 1'st April to 31'st march.

The top management calls a board meeting or managers meeting and they are present

and talk about plans for the next years as compare to previous year projected levels.

The managers or head of the division work with the fiscal services or work on self be

half for prepare an estimation for the next year budgets or projects.

The budgets is complete than the managers present the budget to there head of

department for assessment and approving the budget.

11

can help a company to expand

There can be a good control on credits of the company if it is aware about its financials

beforehand.

The disadvantages are:

Inaccuracy in the budget can lead to wrong financial decision making.

Due to the dynamic environment, department may not achieve the budgeted results.

Static Budget: It is a budget which remains same even when the volume changes. It is

fixed for the entire period. This kind of budget is used when the sales of a company is highly

predictable.

The advantages are:

It is east to implement and follow.

It allows a company to see its estimation of expenses and accordingly change the

strategy.

The disadvantages are:

Lack of flexibility.

It company find out that it is underperforming than it cannot allocate additional resources.

b) Budget preparation process

A budget procedure refers to process by which governance make and approve a budget

for a final presentation of budget at the end of financial year at 31st march (Stiepen, Gérard

and Soret, 2016).

The finance department prepare written record or legal document of all the transactions

of the year from 1'st April to 31'st march.

The top management calls a board meeting or managers meeting and they are present

and talk about plans for the next years as compare to previous year projected levels.

The managers or head of the division work with the fiscal services or work on self be

half for prepare an estimation for the next year budgets or projects.

The budgets is complete than the managers present the budget to there head of

department for assessment and approving the budget.

11

Consideration of the budget request for approval required in written document and with

the justification of the top management and finance adviser. In most of the time

managers talks with there top management or administrative body officer about the

budget programs requirements.

Budgeting is a process of expenditure or time consuming process of every organization or

organizations function (Van Dooren, Bouckaert and Halligan, 2015). It is estimation and portion

of capital used by company to achieve the budgeting designated targets of organization.

Steps for Budget preparation:-

Obtaining Estimates:- Obtaining estimates of the company in various fields like, sales,

production levels, electable costs and accessibility of resources from each department.

Coordinating estimation:- The organization and to estimation what resources are

available and can be reasonably assign among the diverse units of the organization.

Communicating Budget:- Communicating about the budget program to responsible

managers and the obsessed administrative division.

Implementing the budget plan:- the final budget is given to the manager concerned and

adopts as the design of procedure for the coming year budget period.

Reporting interim progress to words budgeted objectives:- As a feedback of the

budgeting report after the completion of budget report mangers present to top

management for feedback and correction.

c) Pricing strategies

A business or organization can usage a verify of price or pricing strategic than selling a

product or service. The price set by the company for maximizing profit for every unit of product

or service sale into market (Venkatnarayan and et.al., 2014). It can compete with existing market

player from new entrants for increasing customers' visibility and gaining market potential within

a market or to come in a new market.

Models of pricing:-

Absorption Pricing:- In this method of pricing owner recovered all costs of invest in

product manufacturing. Price Skimming:- Price skimming means charge high price from target market or target

customers and achieve high profit margin from customers.

12

the justification of the top management and finance adviser. In most of the time

managers talks with there top management or administrative body officer about the

budget programs requirements.

Budgeting is a process of expenditure or time consuming process of every organization or

organizations function (Van Dooren, Bouckaert and Halligan, 2015). It is estimation and portion

of capital used by company to achieve the budgeting designated targets of organization.

Steps for Budget preparation:-

Obtaining Estimates:- Obtaining estimates of the company in various fields like, sales,

production levels, electable costs and accessibility of resources from each department.

Coordinating estimation:- The organization and to estimation what resources are

available and can be reasonably assign among the diverse units of the organization.

Communicating Budget:- Communicating about the budget program to responsible

managers and the obsessed administrative division.

Implementing the budget plan:- the final budget is given to the manager concerned and

adopts as the design of procedure for the coming year budget period.

Reporting interim progress to words budgeted objectives:- As a feedback of the

budgeting report after the completion of budget report mangers present to top

management for feedback and correction.

c) Pricing strategies

A business or organization can usage a verify of price or pricing strategic than selling a

product or service. The price set by the company for maximizing profit for every unit of product

or service sale into market (Venkatnarayan and et.al., 2014). It can compete with existing market

player from new entrants for increasing customers' visibility and gaining market potential within

a market or to come in a new market.

Models of pricing:-

Absorption Pricing:- In this method of pricing owner recovered all costs of invest in

product manufacturing. Price Skimming:- Price skimming means charge high price from target market or target

customers and achieve high profit margin from customers.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.