UGB 163 Accounting and Finance Report: Performance Analysis

VerifiedAdded on 2023/01/18

|21

|3719

|23

Report

AI Summary

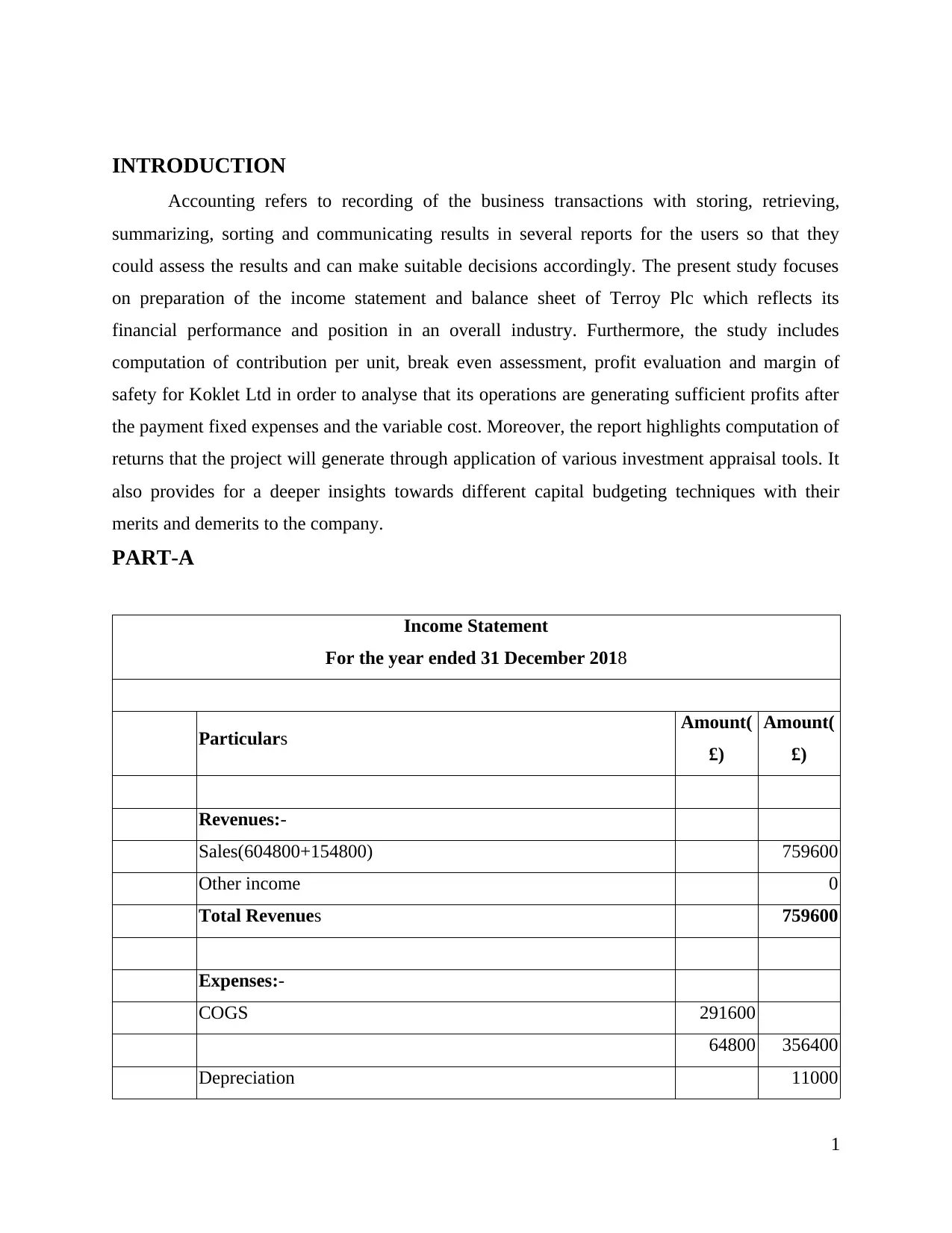

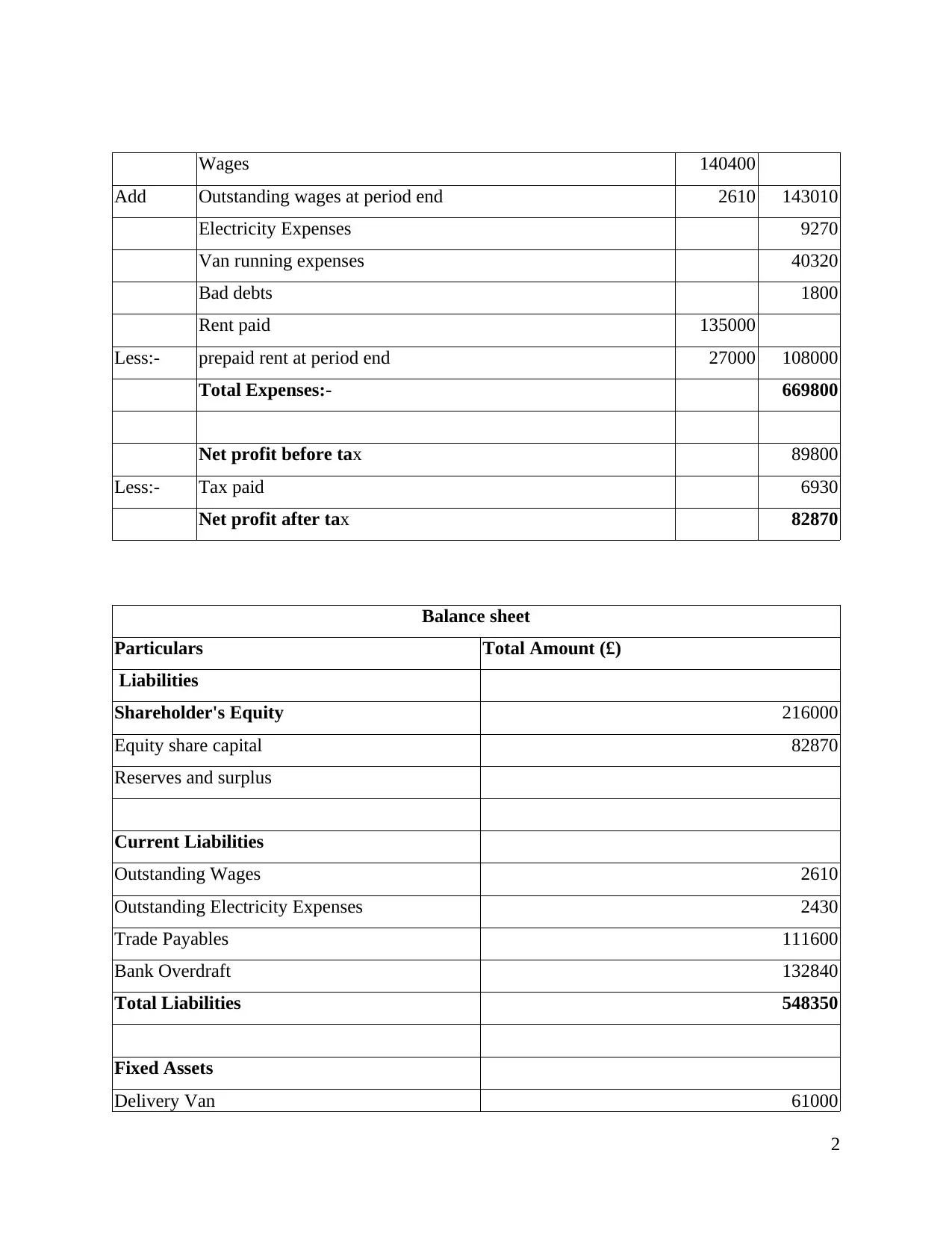

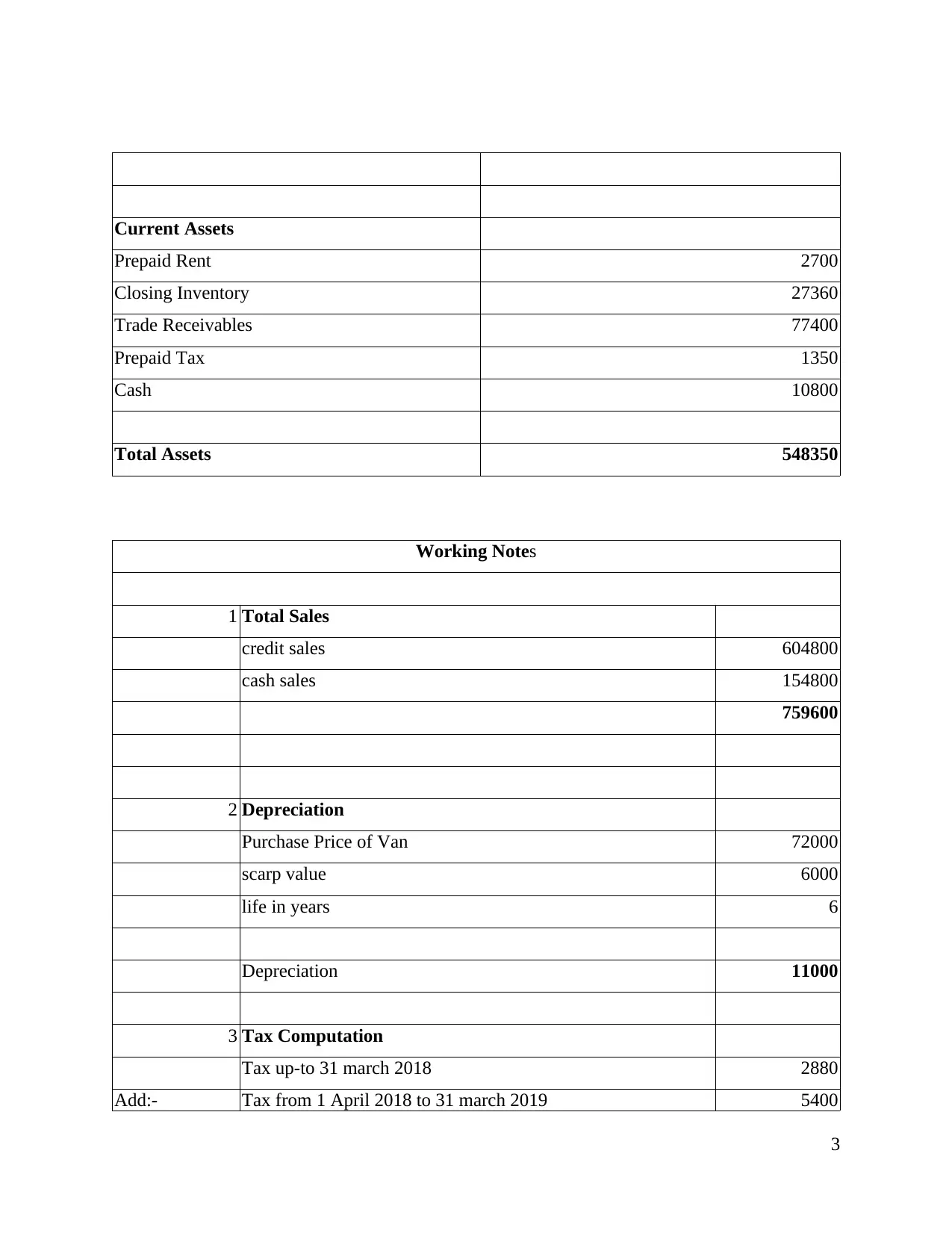

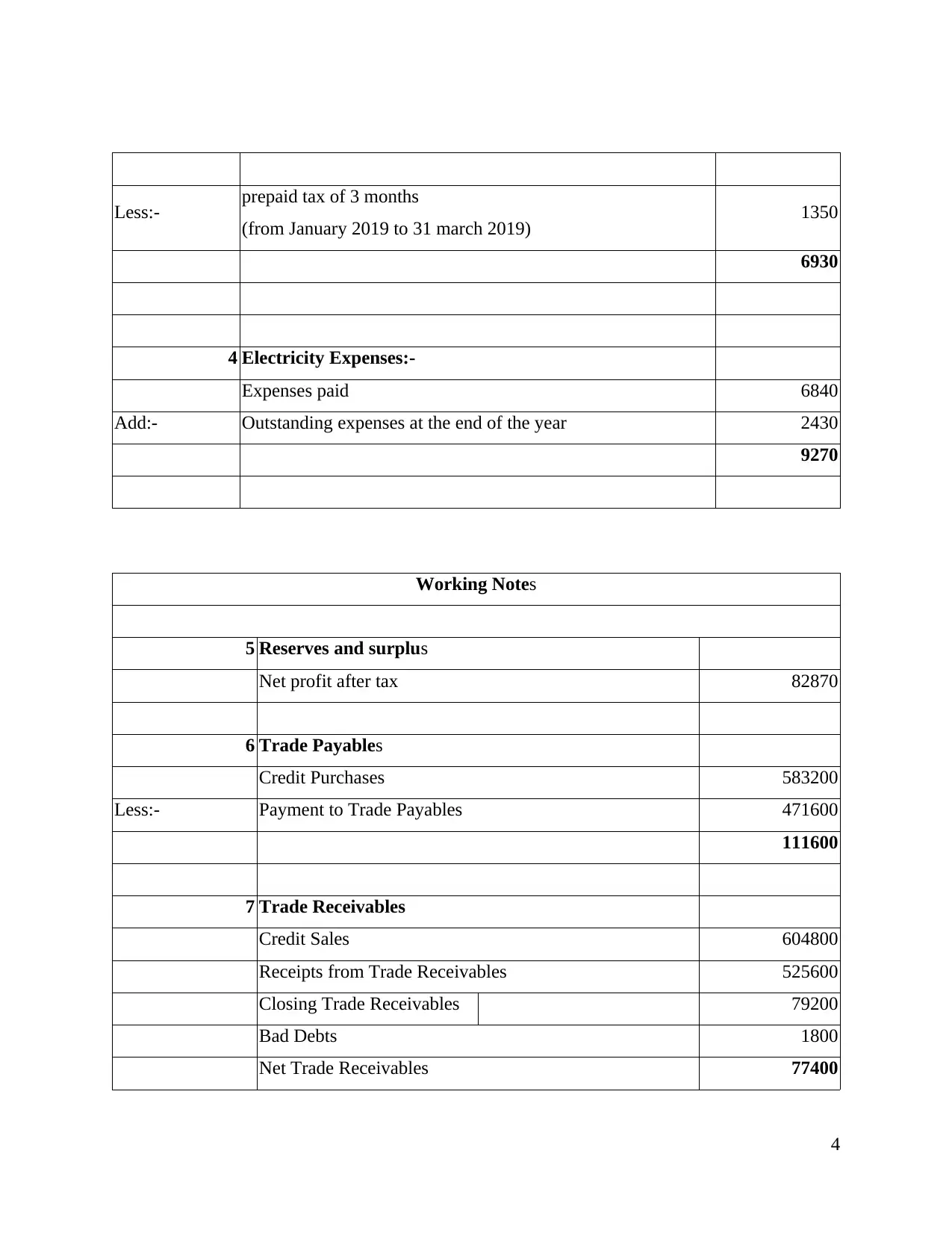

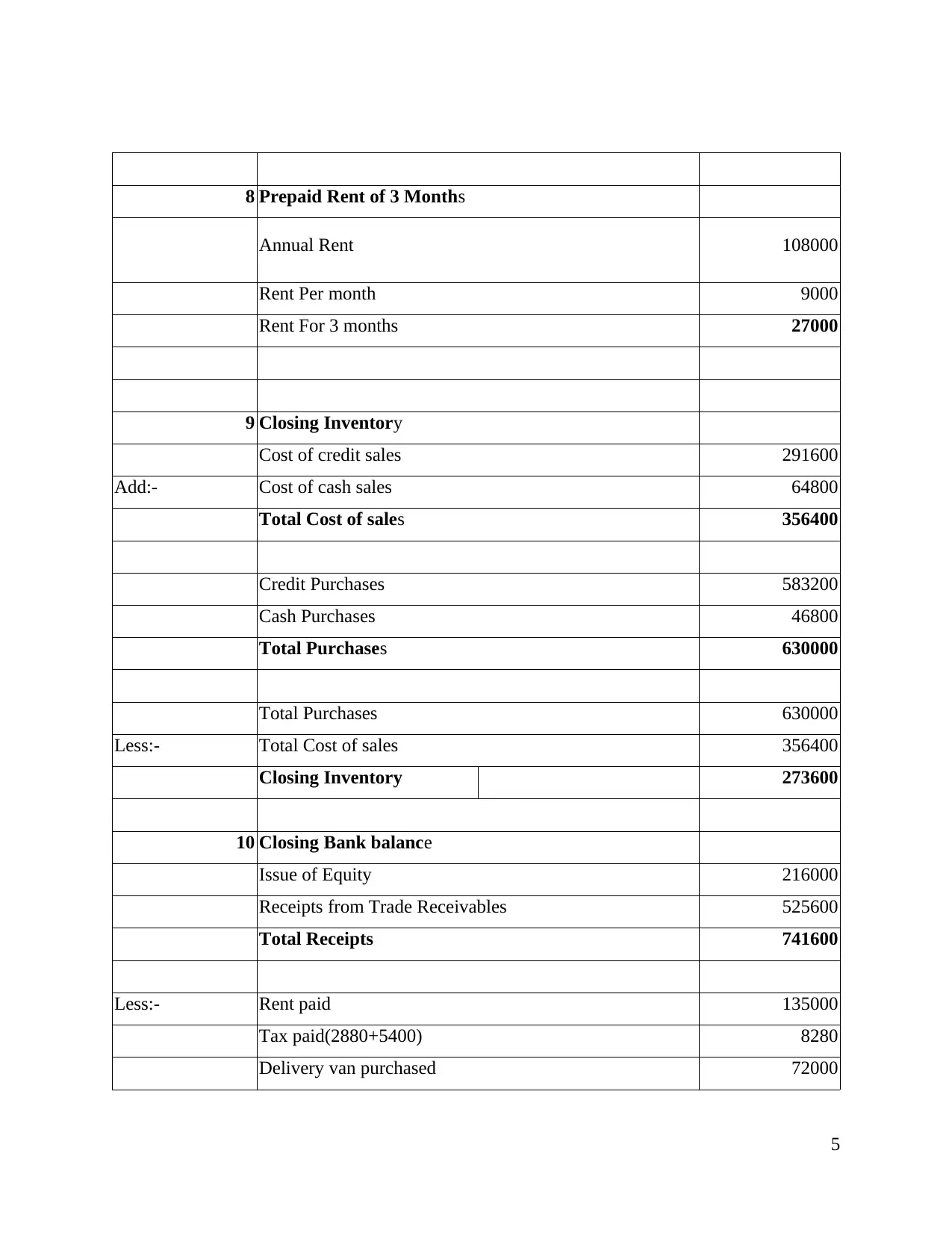

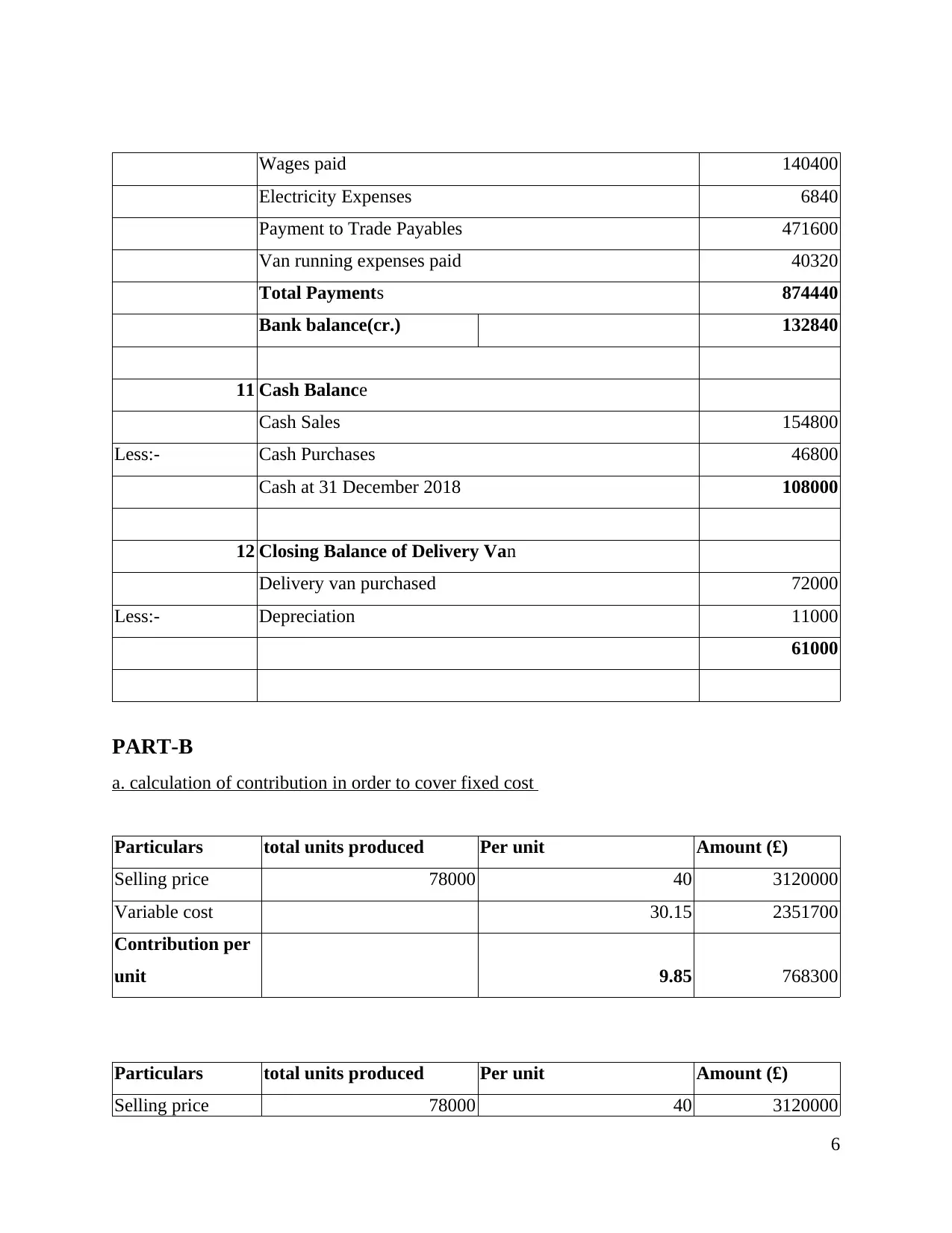

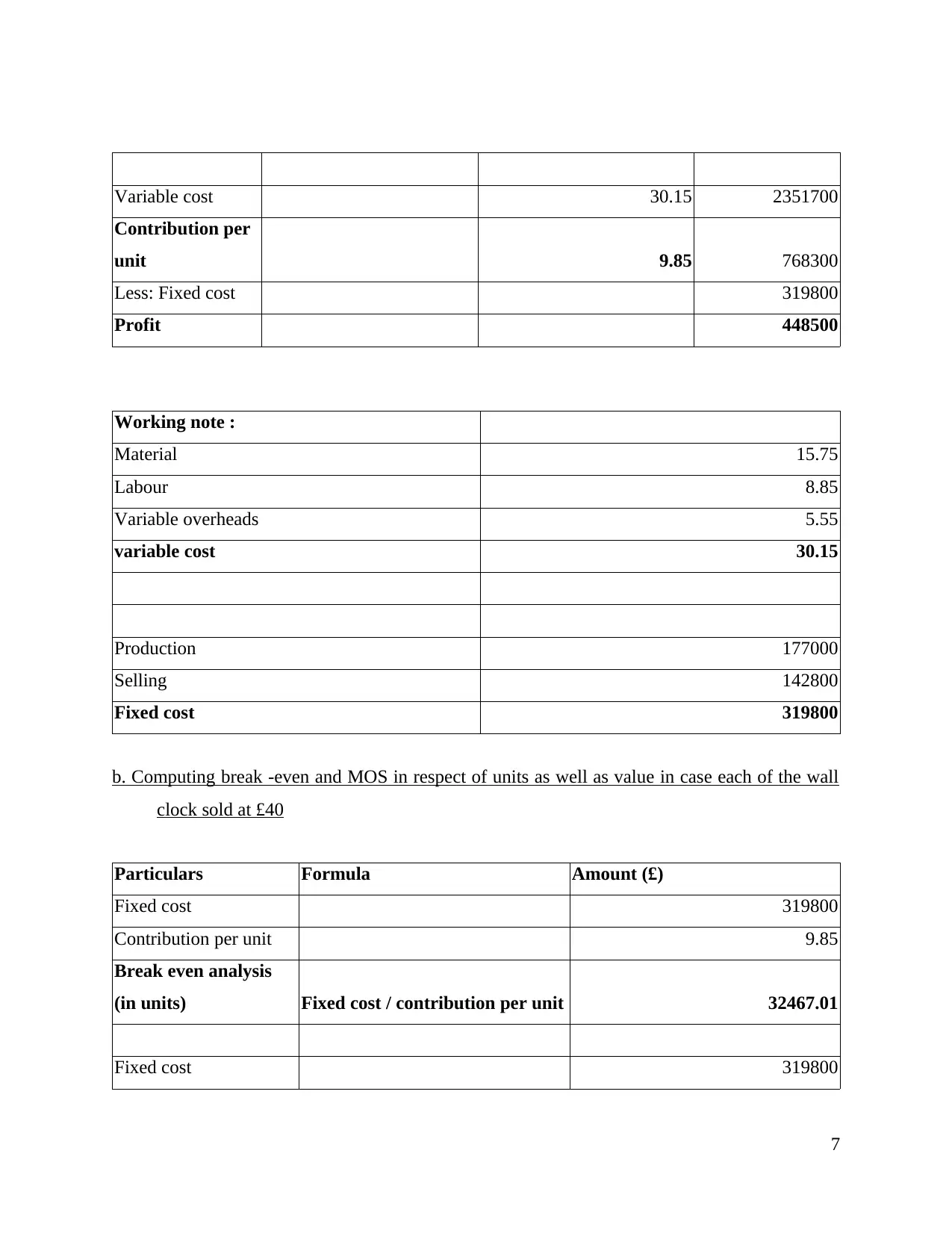

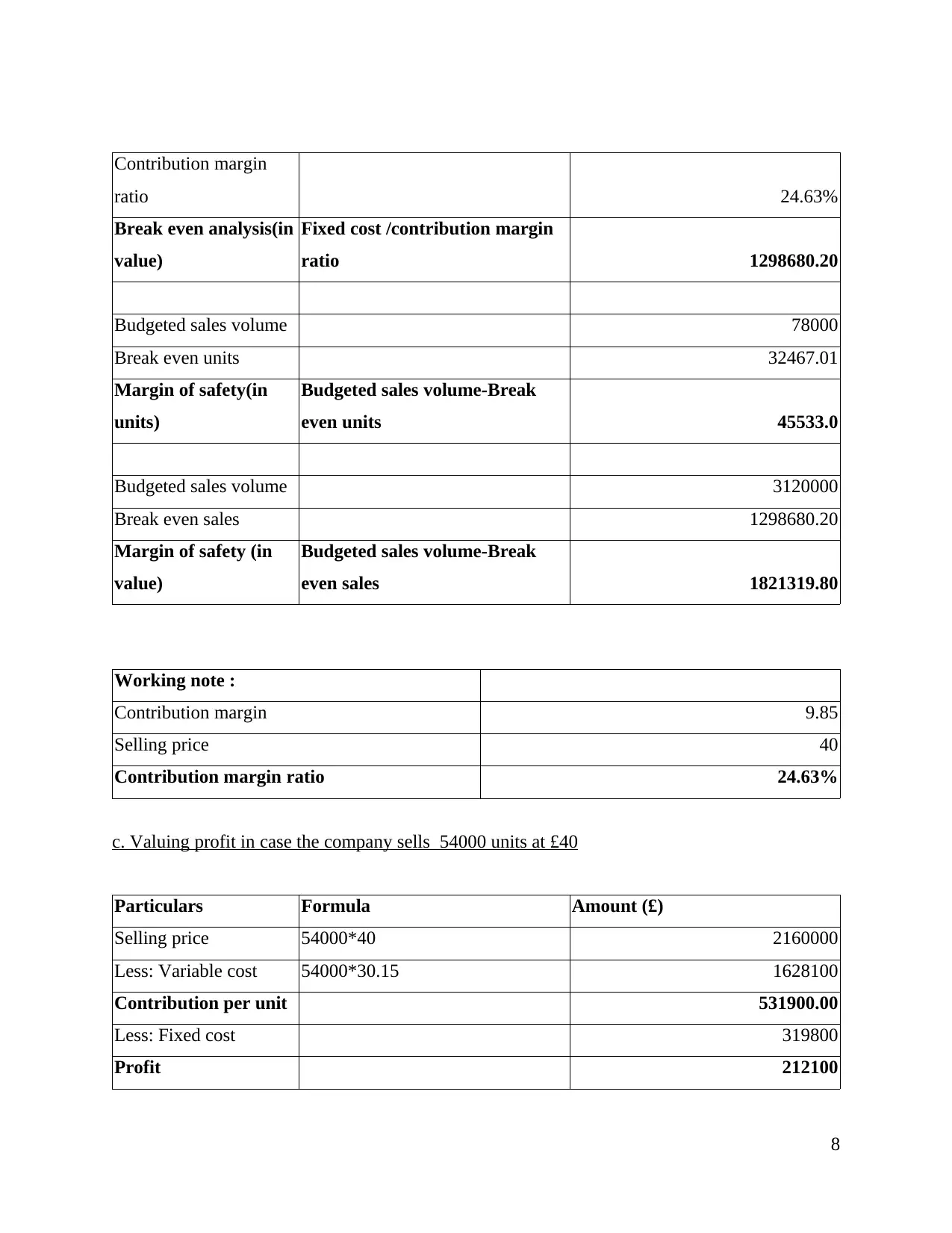

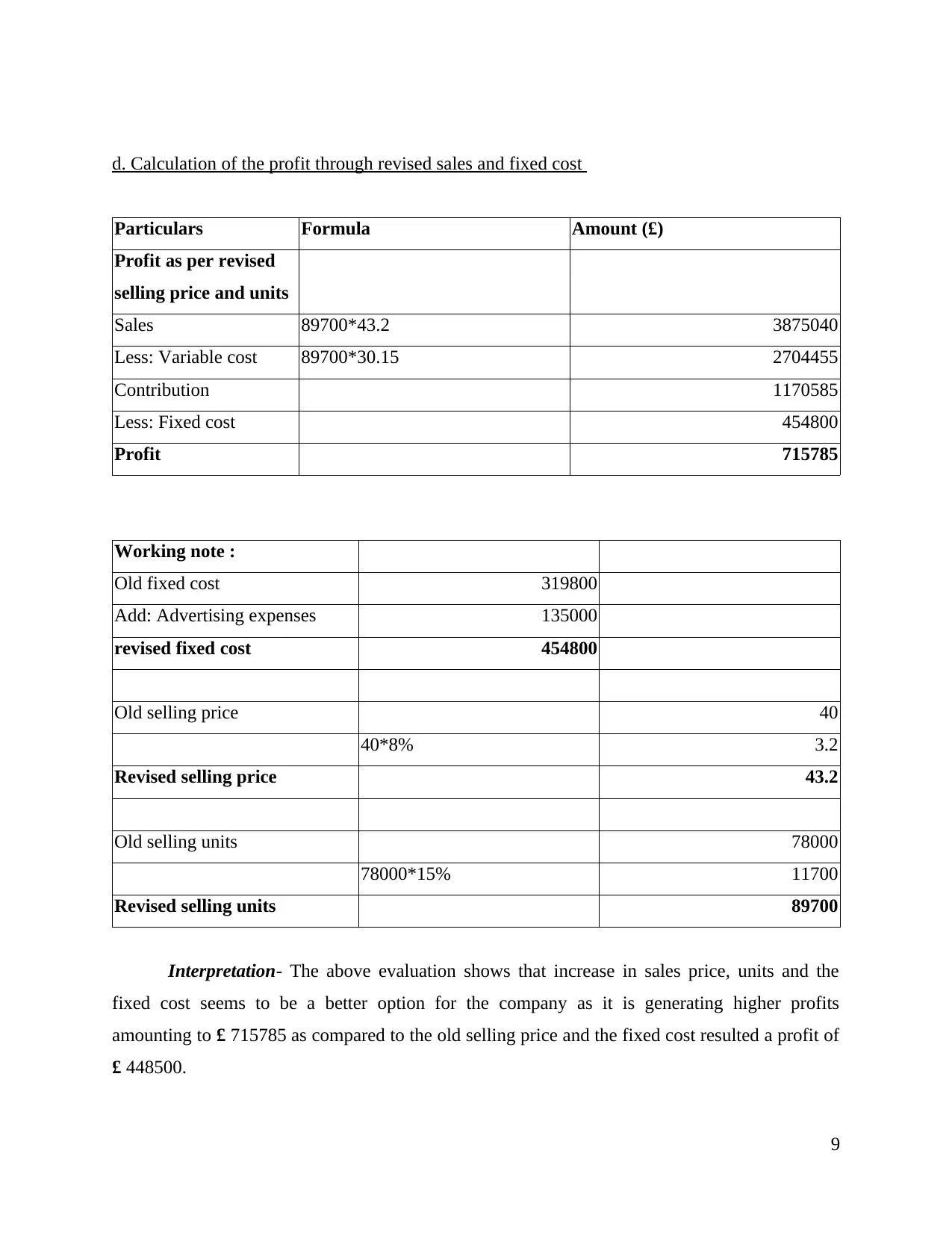

This report presents a comprehensive financial analysis, encompassing the preparation of income statements and balance sheets for Terroy Plc, reflecting its financial position. It delves into the computation of contribution per unit, break-even assessment, profit evaluation, and margin of safety for Koklet Ltd, assessing its profitability. Furthermore, the report explores investment appraisal tools, including payback period, Net Present Value (NPV), and Accounting Rate of Return (ARR), to evaluate project viability. It also examines capital budgeting techniques, including their merits and demerits, offering insights for informed decision-making. The report includes detailed calculations and interpretations of financial data, providing a robust understanding of financial performance and investment analysis.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.