Accounting for Business: Financial Ratios and Performance Analysis

VerifiedAdded on 2023/06/14

|12

|1857

|499

Report

AI Summary

This report provides a detailed financial analysis of a business, covering key aspects of accounting for business. It includes an income statement and balance sheet for the year ended 31st March 2020. The report also calculates the payback period, net present value (NPV), and internal rate of return (IRR) for an investment decision, justifying the advice based on these calculations and stating qualitative factors that should be considered. Furthermore, the report computes various financial ratios such as gross profit ratio, net profit ratio, current ratio, and quick ratio for two companies, A Ltd and B Ltd, commenting on their financial performance based on these ratios, and offering comparative insights.

Accounting for business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

SECTION A.....................................................................................................................................1

Question 1........................................................................................................................................1

a. Income Statement for the year ended 31st March 2020............................................................1

b) balance sheet............................................................................................................................2

SECTION B.....................................................................................................................................3

QUESTION 2..................................................................................................................................3

a) Calculating Payback period.....................................................................................................3

b) computing net present value....................................................................................................4

c) Justifying the basis of advice...................................................................................................4

d) stating 5 qualitative factor that should consider in decision making procedure.....................5

e) Computing IRR........................................................................................................................5

QUESTION 4..................................................................................................................................6

a) Calculating ratio......................................................................................................................6

b) Commenting on financial performance on the basis of computed ratios................................7

REFERENCES................................................................................................................................9

SECTION A.....................................................................................................................................1

Question 1........................................................................................................................................1

a. Income Statement for the year ended 31st March 2020............................................................1

b) balance sheet............................................................................................................................2

SECTION B.....................................................................................................................................3

QUESTION 2..................................................................................................................................3

a) Calculating Payback period.....................................................................................................3

b) computing net present value....................................................................................................4

c) Justifying the basis of advice...................................................................................................4

d) stating 5 qualitative factor that should consider in decision making procedure.....................5

e) Computing IRR........................................................................................................................5

QUESTION 4..................................................................................................................................6

a) Calculating ratio......................................................................................................................6

b) Commenting on financial performance on the basis of computed ratios................................7

REFERENCES................................................................................................................................9

SECTION A

Question 1

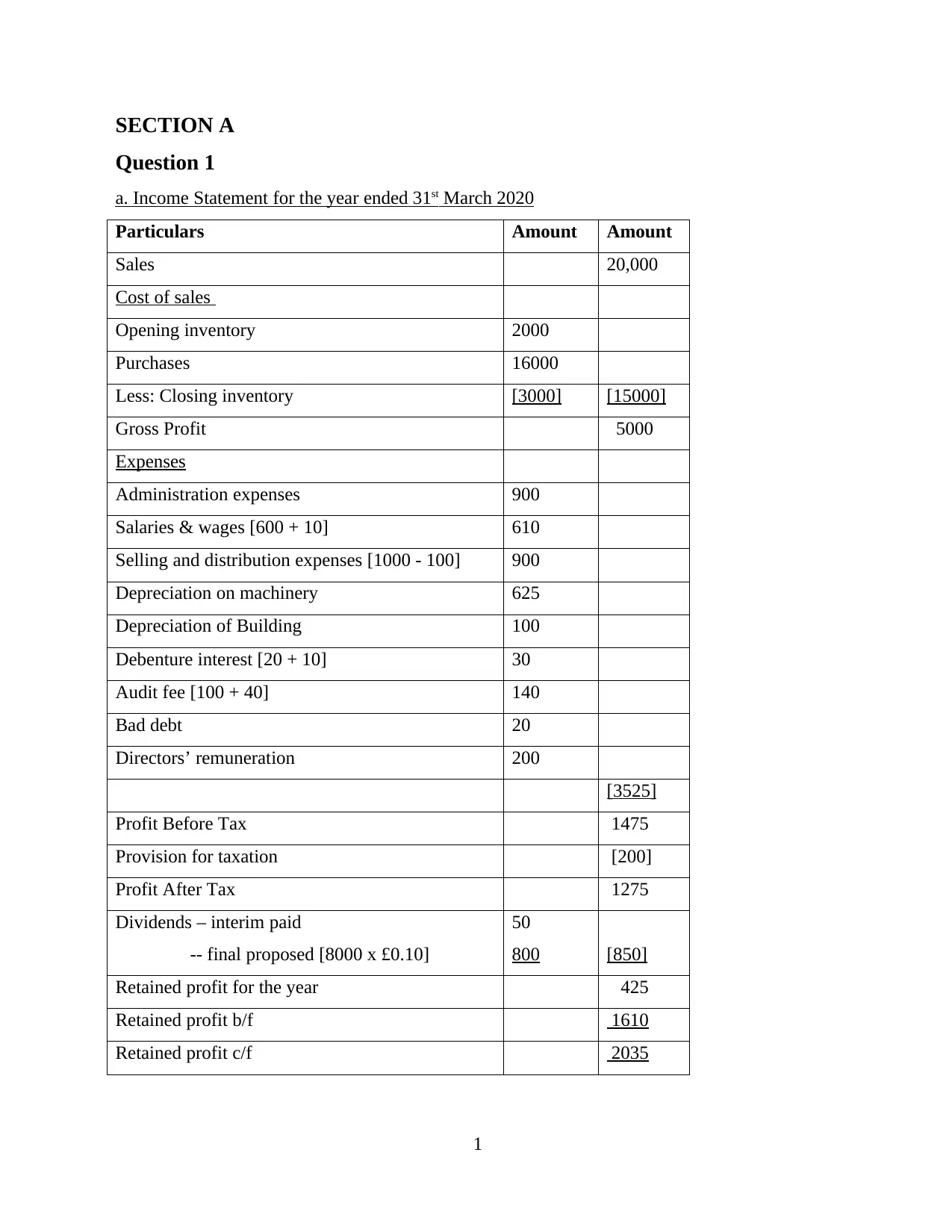

a. Income Statement for the year ended 31st March 2020

Particulars Amount Amount

Sales 20,000

Cost of sales

Opening inventory 2000

Purchases 16000

Less: Closing inventory [3000] [15000]

Gross Profit 5000

Expenses

Administration expenses 900

Salaries & wages [600 + 10] 610

Selling and distribution expenses [1000 - 100] 900

Depreciation on machinery 625

Depreciation of Building 100

Debenture interest [20 + 10] 30

Audit fee [100 + 40] 140

Bad debt 20

Directors’ remuneration 200

[3525]

Profit Before Tax 1475

Provision for taxation [200]

Profit After Tax 1275

Dividends – interim paid

-- final proposed [8000 x £0.10]

50

800 [850]

Retained profit for the year 425

Retained profit b/f 1610

Retained profit c/f 2035

1

Question 1

a. Income Statement for the year ended 31st March 2020

Particulars Amount Amount

Sales 20,000

Cost of sales

Opening inventory 2000

Purchases 16000

Less: Closing inventory [3000] [15000]

Gross Profit 5000

Expenses

Administration expenses 900

Salaries & wages [600 + 10] 610

Selling and distribution expenses [1000 - 100] 900

Depreciation on machinery 625

Depreciation of Building 100

Debenture interest [20 + 10] 30

Audit fee [100 + 40] 140

Bad debt 20

Directors’ remuneration 200

[3525]

Profit Before Tax 1475

Provision for taxation [200]

Profit After Tax 1275

Dividends – interim paid

-- final proposed [8000 x £0.10]

50

800 [850]

Retained profit for the year 425

Retained profit b/f 1610

Retained profit c/f 2035

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

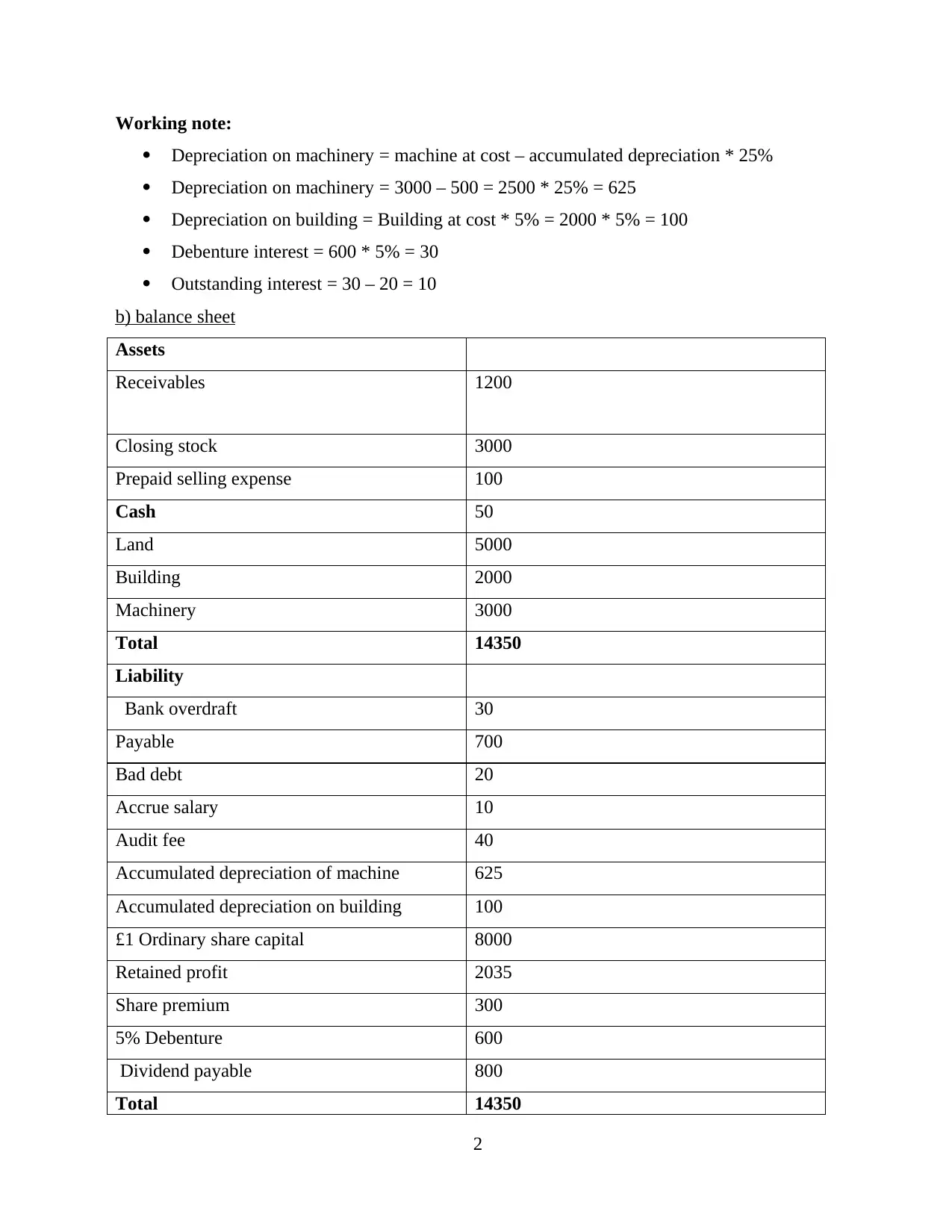

Working note:

Depreciation on machinery = machine at cost – accumulated depreciation * 25%

Depreciation on machinery = 3000 – 500 = 2500 * 25% = 625

Depreciation on building = Building at cost * 5% = 2000 * 5% = 100

Debenture interest = 600 * 5% = 30

Outstanding interest = 30 – 20 = 10

b) balance sheet

Assets

Receivables 1200

Closing stock 3000

Prepaid selling expense 100

Cash 50

Land 5000

Building 2000

Machinery 3000

Total 14350

Liability

Bank overdraft 30

Payable 700

Bad debt 20

Accrue salary 10

Audit fee 40

Accumulated depreciation of machine 625

Accumulated depreciation on building 100

£1 Ordinary share capital 8000

Retained profit 2035

Share premium 300

5% Debenture 600

Dividend payable 800

Total 14350

2

Depreciation on machinery = machine at cost – accumulated depreciation * 25%

Depreciation on machinery = 3000 – 500 = 2500 * 25% = 625

Depreciation on building = Building at cost * 5% = 2000 * 5% = 100

Debenture interest = 600 * 5% = 30

Outstanding interest = 30 – 20 = 10

b) balance sheet

Assets

Receivables 1200

Closing stock 3000

Prepaid selling expense 100

Cash 50

Land 5000

Building 2000

Machinery 3000

Total 14350

Liability

Bank overdraft 30

Payable 700

Bad debt 20

Accrue salary 10

Audit fee 40

Accumulated depreciation of machine 625

Accumulated depreciation on building 100

£1 Ordinary share capital 8000

Retained profit 2035

Share premium 300

5% Debenture 600

Dividend payable 800

Total 14350

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SECTION B

QUESTION 2

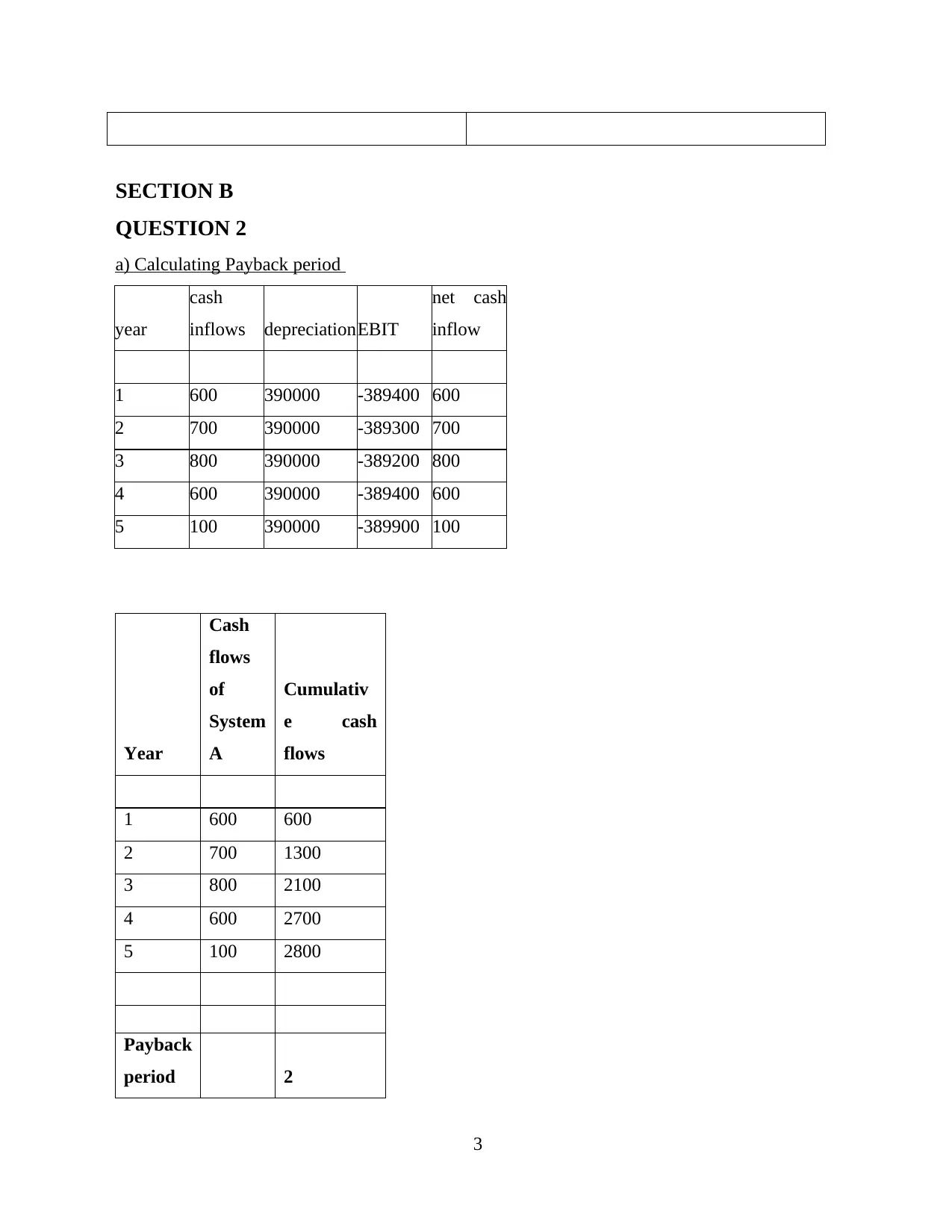

a) Calculating Payback period

year

cash

inflows depreciationEBIT

net cash

inflow

1 600 390000 -389400 600

2 700 390000 -389300 700

3 800 390000 -389200 800

4 600 390000 -389400 600

5 100 390000 -389900 100

Year

Cash

flows

of

System

A

Cumulativ

e cash

flows

1 600 600

2 700 1300

3 800 2100

4 600 2700

5 100 2800

Payback

period 2

3

QUESTION 2

a) Calculating Payback period

year

cash

inflows depreciationEBIT

net cash

inflow

1 600 390000 -389400 600

2 700 390000 -389300 700

3 800 390000 -389200 800

4 600 390000 -389400 600

5 100 390000 -389900 100

Year

Cash

flows

of

System

A

Cumulativ

e cash

flows

1 600 600

2 700 1300

3 800 2100

4 600 2700

5 100 2800

Payback

period 2

3

0.9

Payback

period

2 year and

9 months

From the above calculation it can be specified that NS Plc will become able to cover the

initial investment in 2.9 years

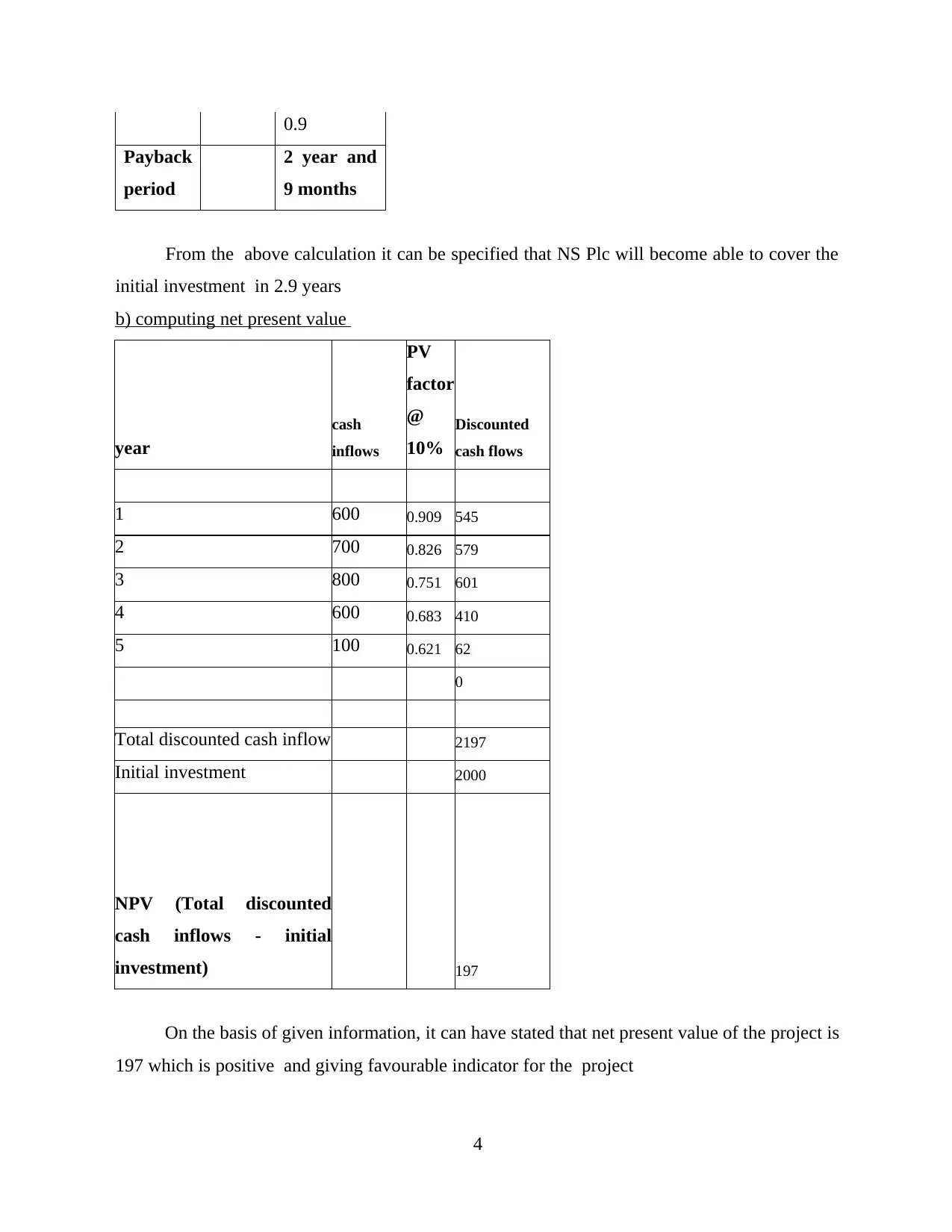

b) computing net present value

year

cash

inflows

PV

factor

@

10%

Discounted

cash flows

1 600 0.909 545

2 700 0.826 579

3 800 0.751 601

4 600 0.683 410

5 100 0.621 62

0

Total discounted cash inflow 2197

Initial investment 2000

NPV (Total discounted

cash inflows - initial

investment) 197

On the basis of given information, it can have stated that net present value of the project is

197 which is positive and giving favourable indicator for the project

4

Payback

period

2 year and

9 months

From the above calculation it can be specified that NS Plc will become able to cover the

initial investment in 2.9 years

b) computing net present value

year

cash

inflows

PV

factor

@

10%

Discounted

cash flows

1 600 0.909 545

2 700 0.826 579

3 800 0.751 601

4 600 0.683 410

5 100 0.621 62

0

Total discounted cash inflow 2197

Initial investment 2000

NPV (Total discounted

cash inflows - initial

investment) 197

On the basis of given information, it can have stated that net present value of the project is

197 which is positive and giving favourable indicator for the project

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

c) Justifying the basis of advice

On the basis of calculation via using payback period and net present value technique of

capital appraisal it can be identified that it will offer positive discounted cash flow. In addition to

this, it is good sign of the NPV tool that contribute in gaining appropriate decision. Payback

period is helpful to estimate how effectively the organization is making particular recovery of

initial invested capital. It will recover the investment with 2.9 year that is profitable. On the

basis of these factor it can be justified that specified firm should choose the option as it is

profitable & efficient.

d) stating 5 qualitative factor that should consider in decision making procedure

Following are the financial factors which are considered when making and investment,

Risk :

In an investment there are always risks involved which are considered to be the key

towards the consideration of the areas which help the organization to analyse whether they

should make investments regarding the areas of the financial investments (Gomes, 2020).

Liquidity :

The liquidity of the investment which the organization is making needs to be considered

before making the investment decision. This will help the organization understand how

effectively the business will be able to convert the investment into cash.

Fluctuations at investment market :

The investment market is one of the most fluctuating markets that needs to be considered

very heavily in order to understand the benefits of making an investment into any part of it

(Siziba and Hall, 2021).

Investment planning factors :

This is a factor which explains the opportunities which the investment has in its history

of being an investment which is considered to be the factor which helps in the minimization of

the risks.

Tax Implications :

Different tax implications are applicable on different kinds of investment which are made

by the organization. Studying these implications can help the company save some tax and also

be effective at the same time.

5

On the basis of calculation via using payback period and net present value technique of

capital appraisal it can be identified that it will offer positive discounted cash flow. In addition to

this, it is good sign of the NPV tool that contribute in gaining appropriate decision. Payback

period is helpful to estimate how effectively the organization is making particular recovery of

initial invested capital. It will recover the investment with 2.9 year that is profitable. On the

basis of these factor it can be justified that specified firm should choose the option as it is

profitable & efficient.

d) stating 5 qualitative factor that should consider in decision making procedure

Following are the financial factors which are considered when making and investment,

Risk :

In an investment there are always risks involved which are considered to be the key

towards the consideration of the areas which help the organization to analyse whether they

should make investments regarding the areas of the financial investments (Gomes, 2020).

Liquidity :

The liquidity of the investment which the organization is making needs to be considered

before making the investment decision. This will help the organization understand how

effectively the business will be able to convert the investment into cash.

Fluctuations at investment market :

The investment market is one of the most fluctuating markets that needs to be considered

very heavily in order to understand the benefits of making an investment into any part of it

(Siziba and Hall, 2021).

Investment planning factors :

This is a factor which explains the opportunities which the investment has in its history

of being an investment which is considered to be the factor which helps in the minimization of

the risks.

Tax Implications :

Different tax implications are applicable on different kinds of investment which are made

by the organization. Studying these implications can help the company save some tax and also

be effective at the same time.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

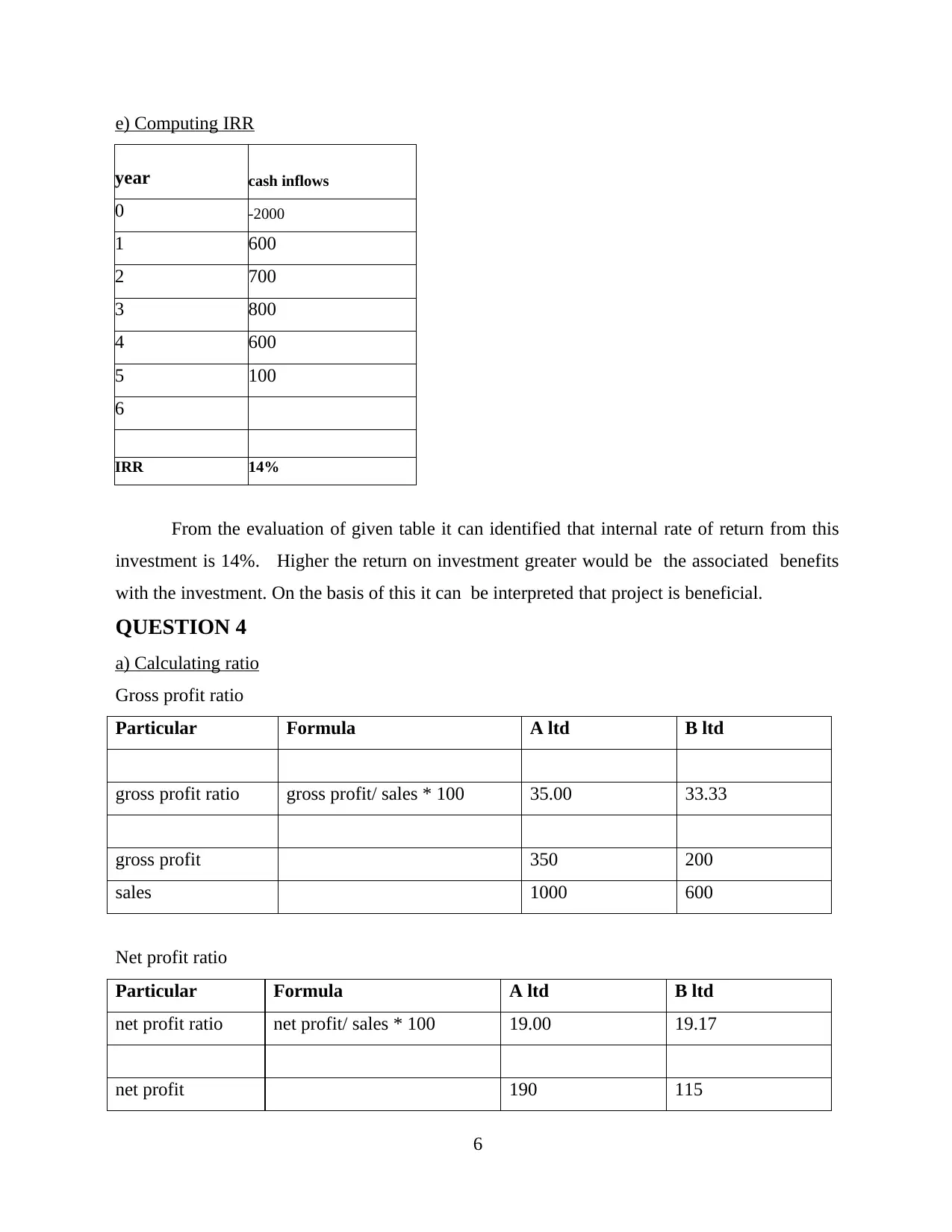

e) Computing IRR

year cash inflows

0 -2000

1 600

2 700

3 800

4 600

5 100

6

IRR 14%

From the evaluation of given table it can identified that internal rate of return from this

investment is 14%. Higher the return on investment greater would be the associated benefits

with the investment. On the basis of this it can be interpreted that project is beneficial.

QUESTION 4

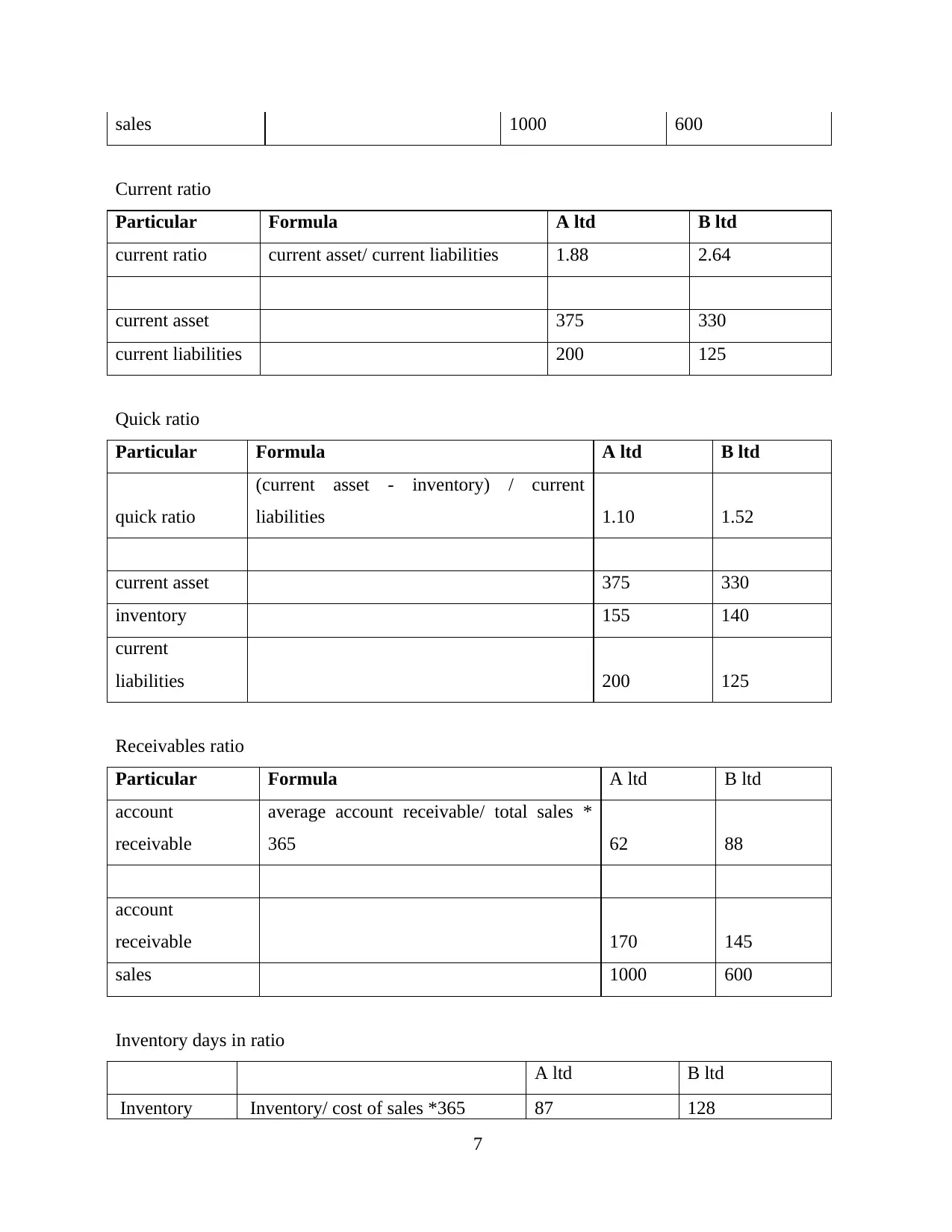

a) Calculating ratio

Gross profit ratio

Particular Formula A ltd B ltd

gross profit ratio gross profit/ sales * 100 35.00 33.33

gross profit 350 200

sales 1000 600

Net profit ratio

Particular Formula A ltd B ltd

net profit ratio net profit/ sales * 100 19.00 19.17

net profit 190 115

6

year cash inflows

0 -2000

1 600

2 700

3 800

4 600

5 100

6

IRR 14%

From the evaluation of given table it can identified that internal rate of return from this

investment is 14%. Higher the return on investment greater would be the associated benefits

with the investment. On the basis of this it can be interpreted that project is beneficial.

QUESTION 4

a) Calculating ratio

Gross profit ratio

Particular Formula A ltd B ltd

gross profit ratio gross profit/ sales * 100 35.00 33.33

gross profit 350 200

sales 1000 600

Net profit ratio

Particular Formula A ltd B ltd

net profit ratio net profit/ sales * 100 19.00 19.17

net profit 190 115

6

sales 1000 600

Current ratio

Particular Formula A ltd B ltd

current ratio current asset/ current liabilities 1.88 2.64

current asset 375 330

current liabilities 200 125

Quick ratio

Particular Formula A ltd B ltd

quick ratio

(current asset - inventory) / current

liabilities 1.10 1.52

current asset 375 330

inventory 155 140

current

liabilities 200 125

Receivables ratio

Particular Formula A ltd B ltd

account

receivable

average account receivable/ total sales *

365 62 88

account

receivable 170 145

sales 1000 600

Inventory days in ratio

A ltd B ltd

Inventory Inventory/ cost of sales *365 87 128

7

Current ratio

Particular Formula A ltd B ltd

current ratio current asset/ current liabilities 1.88 2.64

current asset 375 330

current liabilities 200 125

Quick ratio

Particular Formula A ltd B ltd

quick ratio

(current asset - inventory) / current

liabilities 1.10 1.52

current asset 375 330

inventory 155 140

current

liabilities 200 125

Receivables ratio

Particular Formula A ltd B ltd

account

receivable

average account receivable/ total sales *

365 62 88

account

receivable 170 145

sales 1000 600

Inventory days in ratio

A ltd B ltd

Inventory Inventory/ cost of sales *365 87 128

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

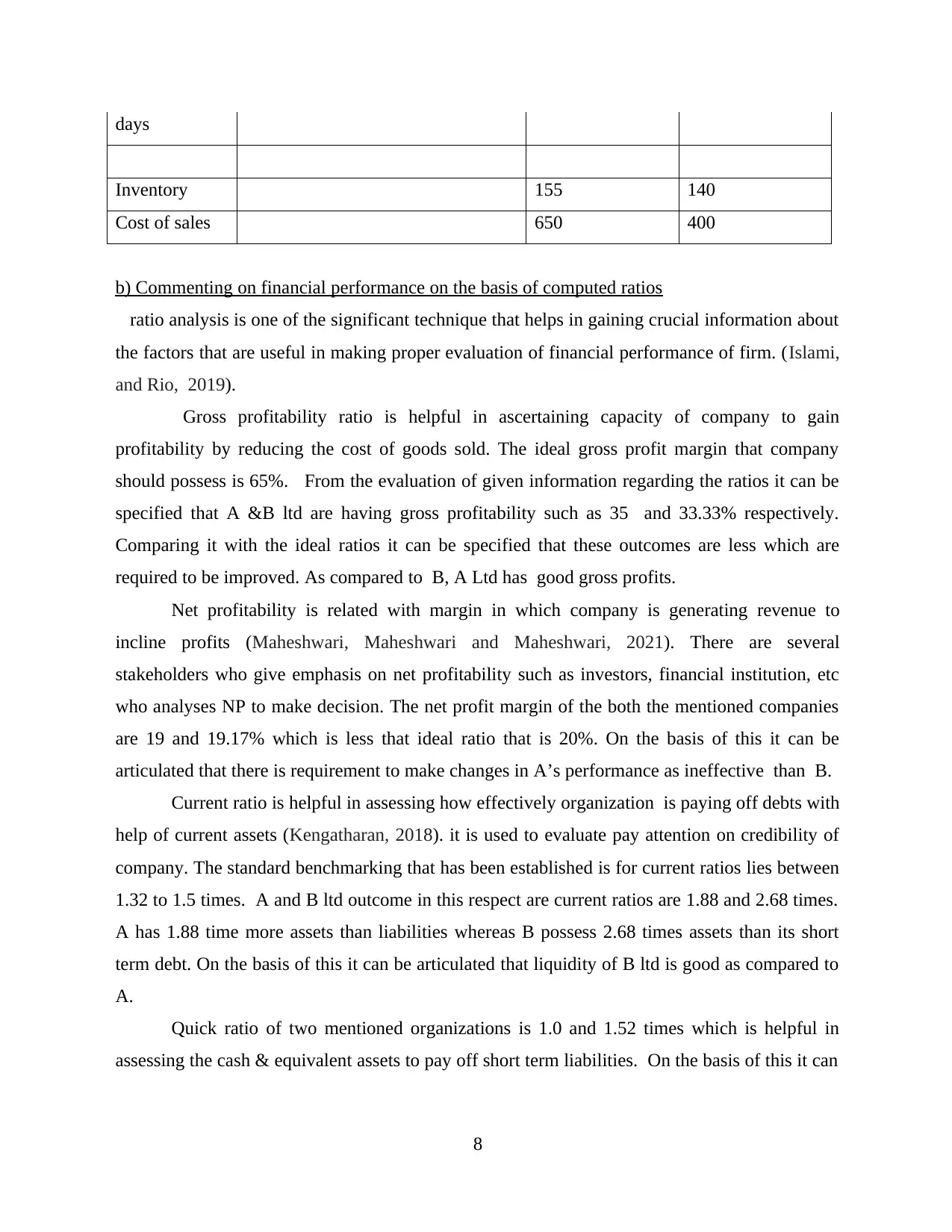

days

Inventory 155 140

Cost of sales 650 400

b) Commenting on financial performance on the basis of computed ratios

ratio analysis is one of the significant technique that helps in gaining crucial information about

the factors that are useful in making proper evaluation of financial performance of firm. (Islami,

and Rio, 2019).

Gross profitability ratio is helpful in ascertaining capacity of company to gain

profitability by reducing the cost of goods sold. The ideal gross profit margin that company

should possess is 65%. From the evaluation of given information regarding the ratios it can be

specified that A &B ltd are having gross profitability such as 35 and 33.33% respectively.

Comparing it with the ideal ratios it can be specified that these outcomes are less which are

required to be improved. As compared to B, A Ltd has good gross profits.

Net profitability is related with margin in which company is generating revenue to

incline profits (Maheshwari, Maheshwari and Maheshwari, 2021). There are several

stakeholders who give emphasis on net profitability such as investors, financial institution, etc

who analyses NP to make decision. The net profit margin of the both the mentioned companies

are 19 and 19.17% which is less that ideal ratio that is 20%. On the basis of this it can be

articulated that there is requirement to make changes in A’s performance as ineffective than B.

Current ratio is helpful in assessing how effectively organization is paying off debts with

help of current assets (Kengatharan, 2018). it is used to evaluate pay attention on credibility of

company. The standard benchmarking that has been established is for current ratios lies between

1.32 to 1.5 times. A and B ltd outcome in this respect are current ratios are 1.88 and 2.68 times.

A has 1.88 time more assets than liabilities whereas B possess 2.68 times assets than its short

term debt. On the basis of this it can be articulated that liquidity of B ltd is good as compared to

A.

Quick ratio of two mentioned organizations is 1.0 and 1.52 times which is helpful in

assessing the cash & equivalent assets to pay off short term liabilities. On the basis of this it can

8

Inventory 155 140

Cost of sales 650 400

b) Commenting on financial performance on the basis of computed ratios

ratio analysis is one of the significant technique that helps in gaining crucial information about

the factors that are useful in making proper evaluation of financial performance of firm. (Islami,

and Rio, 2019).

Gross profitability ratio is helpful in ascertaining capacity of company to gain

profitability by reducing the cost of goods sold. The ideal gross profit margin that company

should possess is 65%. From the evaluation of given information regarding the ratios it can be

specified that A &B ltd are having gross profitability such as 35 and 33.33% respectively.

Comparing it with the ideal ratios it can be specified that these outcomes are less which are

required to be improved. As compared to B, A Ltd has good gross profits.

Net profitability is related with margin in which company is generating revenue to

incline profits (Maheshwari, Maheshwari and Maheshwari, 2021). There are several

stakeholders who give emphasis on net profitability such as investors, financial institution, etc

who analyses NP to make decision. The net profit margin of the both the mentioned companies

are 19 and 19.17% which is less that ideal ratio that is 20%. On the basis of this it can be

articulated that there is requirement to make changes in A’s performance as ineffective than B.

Current ratio is helpful in assessing how effectively organization is paying off debts with

help of current assets (Kengatharan, 2018). it is used to evaluate pay attention on credibility of

company. The standard benchmarking that has been established is for current ratios lies between

1.32 to 1.5 times. A and B ltd outcome in this respect are current ratios are 1.88 and 2.68 times.

A has 1.88 time more assets than liabilities whereas B possess 2.68 times assets than its short

term debt. On the basis of this it can be articulated that liquidity of B ltd is good as compared to

A.

Quick ratio of two mentioned organizations is 1.0 and 1.52 times which is helpful in

assessing the cash & equivalent assets to pay off short term liabilities. On the basis of this it can

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

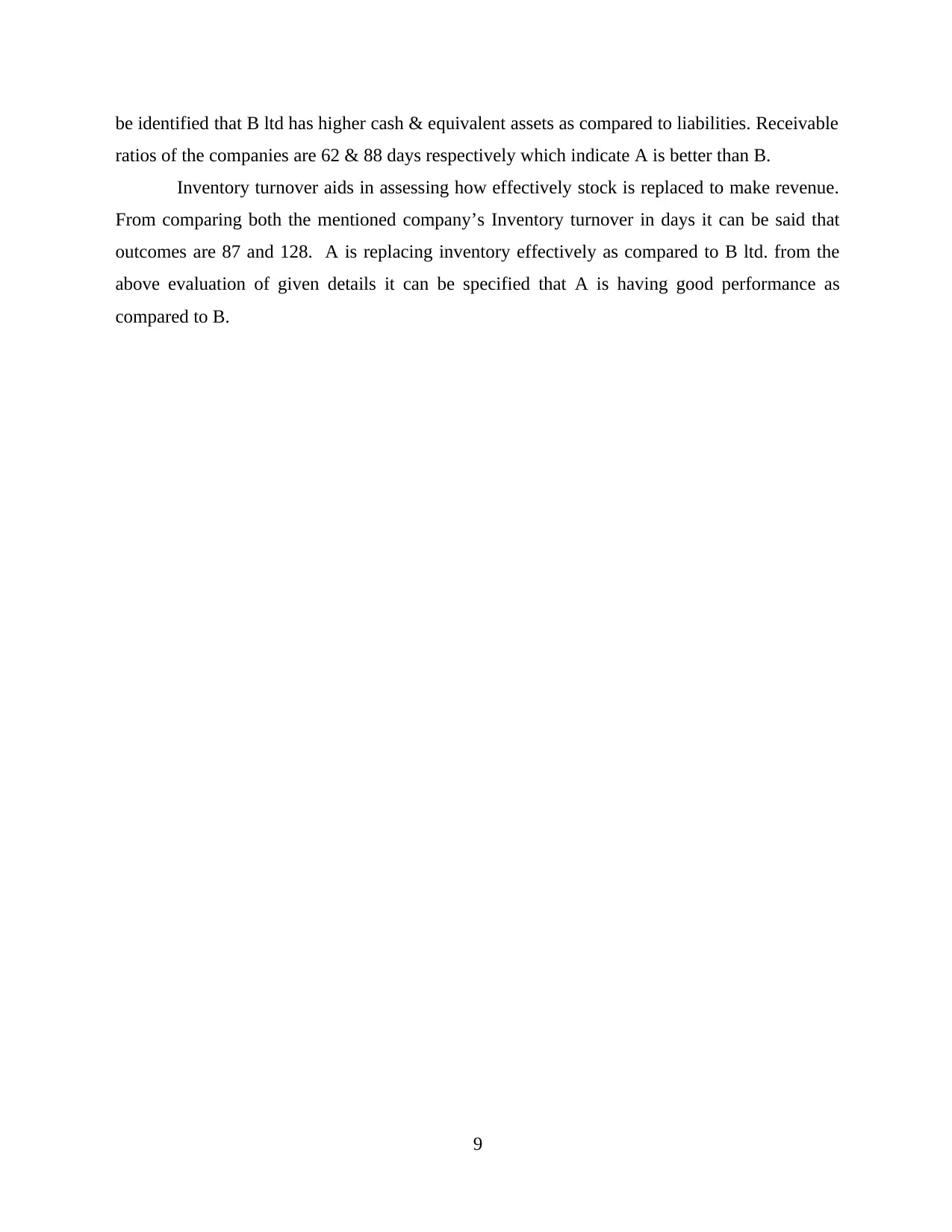

be identified that B ltd has higher cash & equivalent assets as compared to liabilities. Receivable

ratios of the companies are 62 & 88 days respectively which indicate A is better than B.

Inventory turnover aids in assessing how effectively stock is replaced to make revenue.

From comparing both the mentioned company’s Inventory turnover in days it can be said that

outcomes are 87 and 128. A is replacing inventory effectively as compared to B ltd. from the

above evaluation of given details it can be specified that A is having good performance as

compared to B.

9

ratios of the companies are 62 & 88 days respectively which indicate A is better than B.

Inventory turnover aids in assessing how effectively stock is replaced to make revenue.

From comparing both the mentioned company’s Inventory turnover in days it can be said that

outcomes are 87 and 128. A is replacing inventory effectively as compared to B ltd. from the

above evaluation of given details it can be specified that A is having good performance as

compared to B.

9

REFERENCES

Books and Journals

Gomes, P., 2021. Financial and non-financial responses to the Covid-19 pandemic: insights from

Portugal and lessons for future. Public Money & Management. pp.1-3.

Islami, I. N. and Rio, W., 2019. Financial ratio analysis to predict financial distress on property

and real estate company listed in indonesia stock exchange. JAAF (Journal of Applied

Accounting and Finance). 2(2). pp.125-137.

Kengatharan, L., 2018. Capital Budgeting Theory and Practice: A review and agenda for future

research. American Journal of economics and business management, 1(1), pp.20-53.

Maheshwari, S. N., Maheshwari, S. K. and Maheshwari, M. S. K., 2021. Principles of

Management Accounting. Sultan Chand & Sons.

Siziba, S. and Hall, J. H., 2021. The evolution of the application of capital budgeting techniques

in enterprises. Global Finance Journal. 47,. p.100504.

10

Books and Journals

Gomes, P., 2021. Financial and non-financial responses to the Covid-19 pandemic: insights from

Portugal and lessons for future. Public Money & Management. pp.1-3.

Islami, I. N. and Rio, W., 2019. Financial ratio analysis to predict financial distress on property

and real estate company listed in indonesia stock exchange. JAAF (Journal of Applied

Accounting and Finance). 2(2). pp.125-137.

Kengatharan, L., 2018. Capital Budgeting Theory and Practice: A review and agenda for future

research. American Journal of economics and business management, 1(1), pp.20-53.

Maheshwari, S. N., Maheshwari, S. K. and Maheshwari, M. S. K., 2021. Principles of

Management Accounting. Sultan Chand & Sons.

Siziba, S. and Hall, J. H., 2021. The evolution of the application of capital budgeting techniques

in enterprises. Global Finance Journal. 47,. p.100504.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.