Analysis and Comparison of Vodafone and BT Group Accounting Report

VerifiedAdded on 2020/02/05

|11

|3952

|154

Report

AI Summary

This report provides an introduction to accounting, focusing on the financial performance of two telecommunications companies: Vodafone and BT Group. It begins with a comparison of the companies, highlighting their market positions, revenue, operating income, and workforce size. The core of the report involves a detailed analysis of financial ratios, including profitability (operating profit, operating ratio, and net profit ratios), liquidity (current, quick, and cash ratios), and efficiency (total asset turnover, inventory turnover, and accounts receivable turnover ratios) for both companies over a three-year period (2013-2015). The analysis of these ratios allows for a deeper understanding of each company's financial health, operational efficiency, and overall market performance, with a conclusion that Vodafone's performance appears stronger. The report aims to provide a comprehensive overview of the companies' financial standings and offers valuable insights into their respective strengths and weaknesses.

Introduction to

Accounting

1

Accounting

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................3

ANALYSIS/ COMPARISON OF THE PERFORMANCE OF TWO COMPANIES....................3

CALCULATION OF RATIOS........................................................................................................4

CONCLUSION and RECOMMENDATION..................................................................................8

REFERENCES................................................................................................................................9

2

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................3

ANALYSIS/ COMPARISON OF THE PERFORMANCE OF TWO COMPANIES....................3

CALCULATION OF RATIOS........................................................................................................4

CONCLUSION and RECOMMENDATION..................................................................................8

REFERENCES................................................................................................................................9

2

INTRODUCTION

The term accounting is referred to as the systematic as well as comprehensive recording of the

data relating with financial transactions of the organization. On the other hand accounting can also be

defined as the process of summarizing, analyzing as well as reporting financial transactions (Li, 2015).

The role of accounting for every business whether large or small is significant. The major aim of

accounting is to offer means of recording, reporting, summarizing as well as interpreting economic data.

In this regard development of accounting system is being done. It is effective in serving the requirements

of the users of accounting information.

In the present report introduction to accounting has been discussed in context of two

organizations that are operating with Telecoms sector. This includes Vodafone and BT group. Vodafone

is British multinational telecommunication business that has headquarter in London. The company is

second largest telecommunications company measured in terms of both subscribers and revenues. On the

other hand BT group is world's leading communication service company that serves the requirement of

customers in UK. The study entails to make analysis of the performance of two firms. Further it includes

ratio calculation of both in order to assess their position in terms of financial health in the market.

ANALYSIS/ COMPARISON OF THE PERFORMANCE OF TWO

COMPANIES

This section of the report includes comparison of the performance of two companies which are

includes Vodafone and BT group. Vodafone group PLC is one of the British multinational

telecommunication firm that is headquartered in London and has a registered office in Newbury

Berkshire. The firm is world's largest mobile telecommunication organization if measured in terms of

both subscribers and revenues. The mission of Vodafone is to become communication leader in the

increasingly connected world (Taylor, Bogdan and DeVault, 2015). Further the organization is involved

in enhancing the value by the means of making delivery of affordable, reliable, customized

communication services that are easy to use, enjoyable as well as secure. As per data of 2014 Vodafone

had 434 million subscribers. The company owns and carries out its operations in 26 countries. Along with

this it possess partner networks in around 50 additional countries. Vodafone is the organization that has

primary listing on the London stock exchange and is the constituent of FTSE 100 index. The market

capitalization of the firm as per 2012 data is £89.1 billion which the third largest of any organization that

is being listed on London Stock Exchange (Heintz and Parry, 2016). Vodafone has secondary listing on

NASDAQ.

The company Vodafone is dealing in the products that includes fixed line and mobile telephony,

internet services and digital television. In accordance with 2015 data the revenue earned by company is

£42.22 billion. In addition to this the operating income of the business is £19.67 billion. Vodafone has

earned the profit of £5.761 billion (Vodafone Group PLC, 2016). The total asset with the particular

telecommunication organization is £122.5 billion. In contrast to this the total equity with Vodafone is

£66.1 billion. This presents that financial position of the firm is strong. Such implies that company is able

to attain pre-determined targets with effectiveness (Scott, 2016). The company possess the workforce of

101433 employees who are engaged in carry out the operations in the desired manner.

On the contrary BT Group is one of the British telecommunications service company that has

head office in London United Kingdom. The major purpose of BT group is to utilize the power of

communication for the development of better world. Along with this it make efforts towards bringing

together best networks and technology along with the expertise of people to create new possibilities as

well as make new networks. The company has operations in around 170 countries. In UK the firm is

leading communication service provider that is making sales of products and services to customers, small

and medium sized business as well as public sector. Further the company also makes sales of whole

3

The term accounting is referred to as the systematic as well as comprehensive recording of the

data relating with financial transactions of the organization. On the other hand accounting can also be

defined as the process of summarizing, analyzing as well as reporting financial transactions (Li, 2015).

The role of accounting for every business whether large or small is significant. The major aim of

accounting is to offer means of recording, reporting, summarizing as well as interpreting economic data.

In this regard development of accounting system is being done. It is effective in serving the requirements

of the users of accounting information.

In the present report introduction to accounting has been discussed in context of two

organizations that are operating with Telecoms sector. This includes Vodafone and BT group. Vodafone

is British multinational telecommunication business that has headquarter in London. The company is

second largest telecommunications company measured in terms of both subscribers and revenues. On the

other hand BT group is world's leading communication service company that serves the requirement of

customers in UK. The study entails to make analysis of the performance of two firms. Further it includes

ratio calculation of both in order to assess their position in terms of financial health in the market.

ANALYSIS/ COMPARISON OF THE PERFORMANCE OF TWO

COMPANIES

This section of the report includes comparison of the performance of two companies which are

includes Vodafone and BT group. Vodafone group PLC is one of the British multinational

telecommunication firm that is headquartered in London and has a registered office in Newbury

Berkshire. The firm is world's largest mobile telecommunication organization if measured in terms of

both subscribers and revenues. The mission of Vodafone is to become communication leader in the

increasingly connected world (Taylor, Bogdan and DeVault, 2015). Further the organization is involved

in enhancing the value by the means of making delivery of affordable, reliable, customized

communication services that are easy to use, enjoyable as well as secure. As per data of 2014 Vodafone

had 434 million subscribers. The company owns and carries out its operations in 26 countries. Along with

this it possess partner networks in around 50 additional countries. Vodafone is the organization that has

primary listing on the London stock exchange and is the constituent of FTSE 100 index. The market

capitalization of the firm as per 2012 data is £89.1 billion which the third largest of any organization that

is being listed on London Stock Exchange (Heintz and Parry, 2016). Vodafone has secondary listing on

NASDAQ.

The company Vodafone is dealing in the products that includes fixed line and mobile telephony,

internet services and digital television. In accordance with 2015 data the revenue earned by company is

£42.22 billion. In addition to this the operating income of the business is £19.67 billion. Vodafone has

earned the profit of £5.761 billion (Vodafone Group PLC, 2016). The total asset with the particular

telecommunication organization is £122.5 billion. In contrast to this the total equity with Vodafone is

£66.1 billion. This presents that financial position of the firm is strong. Such implies that company is able

to attain pre-determined targets with effectiveness (Scott, 2016). The company possess the workforce of

101433 employees who are engaged in carry out the operations in the desired manner.

On the contrary BT Group is one of the British telecommunications service company that has

head office in London United Kingdom. The major purpose of BT group is to utilize the power of

communication for the development of better world. Along with this it make efforts towards bringing

together best networks and technology along with the expertise of people to create new possibilities as

well as make new networks. The company has operations in around 170 countries. In UK the firm is

leading communication service provider that is making sales of products and services to customers, small

and medium sized business as well as public sector. Further the company also makes sales of whole

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

products and services to the communication providers within UK and across the globe (Groom, Rapti and

Pardina, 2016). BT is efficient is supplying managed networked IT services to the multinational

corporations, domestic businesses as well as national and local government business. BT is the firm that

has primary listing on the London stock exchange and is the constituent of FTSE 100 index. It has

secondary listing on New York Stock Exchange. The company BT group is dealing in the products that

includes fixed line telephony and mobile telephony, broadband internet, fiber- optic communication, IT

services and digital television. In accordance with 2015 data the revenue earned by company is £17.851

billion. Along with this the operating income of the business is £3.733 billion. BT group has earned the

profitability of £2135 billion (BT Group, 2016). The company possess the workforce of 88500 employees

who are engaged in carry out the operations in the desired manner. The major focus areas of BT group is

related with delivering greater experience to the customers. In addition to this emphasize over bringing

the benefits of connected society to every individual. The company also assist the communities by the

means of people as well as technology.

While making comparison of both the organization that is Vodafone and BT group it has been

assessed that the performance of Vodafone is sound in comparison to BT group. This can be said by

reviewing the figures of operating income and profitability of the organization. It demonstrate that the

organization is able to accomplish its targets within desired span of time. The operations of the firm is

much wider in comparison with BT group. Further the number of employees working in BT group is less

as compared to Vodafone.

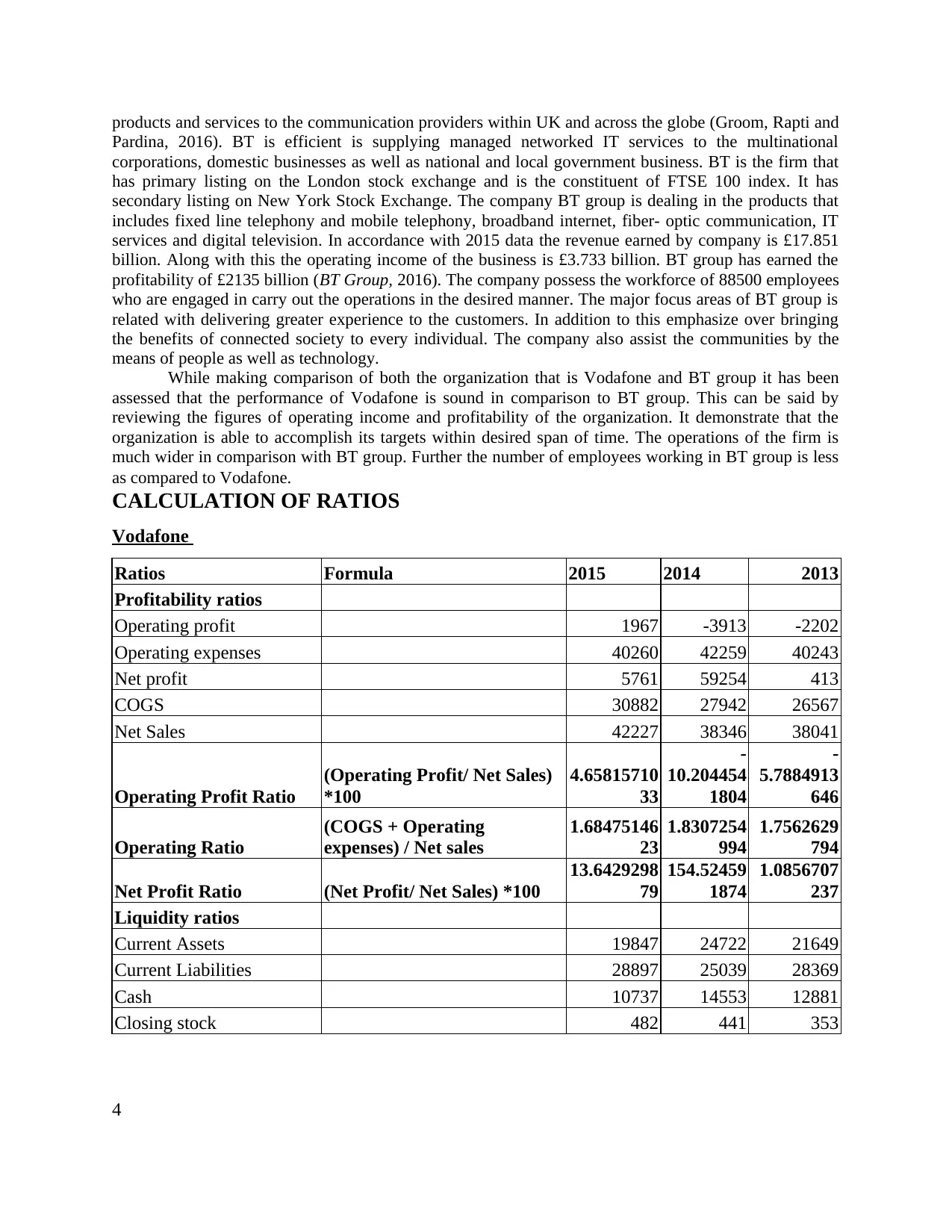

CALCULATION OF RATIOS

Vodafone

Ratios Formula 2015 2014 2013

Profitability ratios

Operating profit 1967 -3913 -2202

Operating expenses 40260 42259 40243

Net profit 5761 59254 413

COGS 30882 27942 26567

Net Sales 42227 38346 38041

Operating Profit Ratio

(Operating Profit/ Net Sales)

*100

4.65815710

33

-

10.204454

1804

-

5.7884913

646

Operating Ratio

(COGS + Operating

expenses) / Net sales

1.68475146

23

1.8307254

994

1.7562629

794

Net Profit Ratio (Net Profit/ Net Sales) *100

13.6429298

79

154.52459

1874

1.0856707

237

Liquidity ratios

Current Assets 19847 24722 21649

Current Liabilities 28897 25039 28369

Cash 10737 14553 12881

Closing stock 482 441 353

4

Pardina, 2016). BT is efficient is supplying managed networked IT services to the multinational

corporations, domestic businesses as well as national and local government business. BT is the firm that

has primary listing on the London stock exchange and is the constituent of FTSE 100 index. It has

secondary listing on New York Stock Exchange. The company BT group is dealing in the products that

includes fixed line telephony and mobile telephony, broadband internet, fiber- optic communication, IT

services and digital television. In accordance with 2015 data the revenue earned by company is £17.851

billion. Along with this the operating income of the business is £3.733 billion. BT group has earned the

profitability of £2135 billion (BT Group, 2016). The company possess the workforce of 88500 employees

who are engaged in carry out the operations in the desired manner. The major focus areas of BT group is

related with delivering greater experience to the customers. In addition to this emphasize over bringing

the benefits of connected society to every individual. The company also assist the communities by the

means of people as well as technology.

While making comparison of both the organization that is Vodafone and BT group it has been

assessed that the performance of Vodafone is sound in comparison to BT group. This can be said by

reviewing the figures of operating income and profitability of the organization. It demonstrate that the

organization is able to accomplish its targets within desired span of time. The operations of the firm is

much wider in comparison with BT group. Further the number of employees working in BT group is less

as compared to Vodafone.

CALCULATION OF RATIOS

Vodafone

Ratios Formula 2015 2014 2013

Profitability ratios

Operating profit 1967 -3913 -2202

Operating expenses 40260 42259 40243

Net profit 5761 59254 413

COGS 30882 27942 26567

Net Sales 42227 38346 38041

Operating Profit Ratio

(Operating Profit/ Net Sales)

*100

4.65815710

33

-

10.204454

1804

-

5.7884913

646

Operating Ratio

(COGS + Operating

expenses) / Net sales

1.68475146

23

1.8307254

994

1.7562629

794

Net Profit Ratio (Net Profit/ Net Sales) *100

13.6429298

79

154.52459

1874

1.0856707

237

Liquidity ratios

Current Assets 19847 24722 21649

Current Liabilities 28897 25039 28369

Cash 10737 14553 12881

Closing stock 482 441 353

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

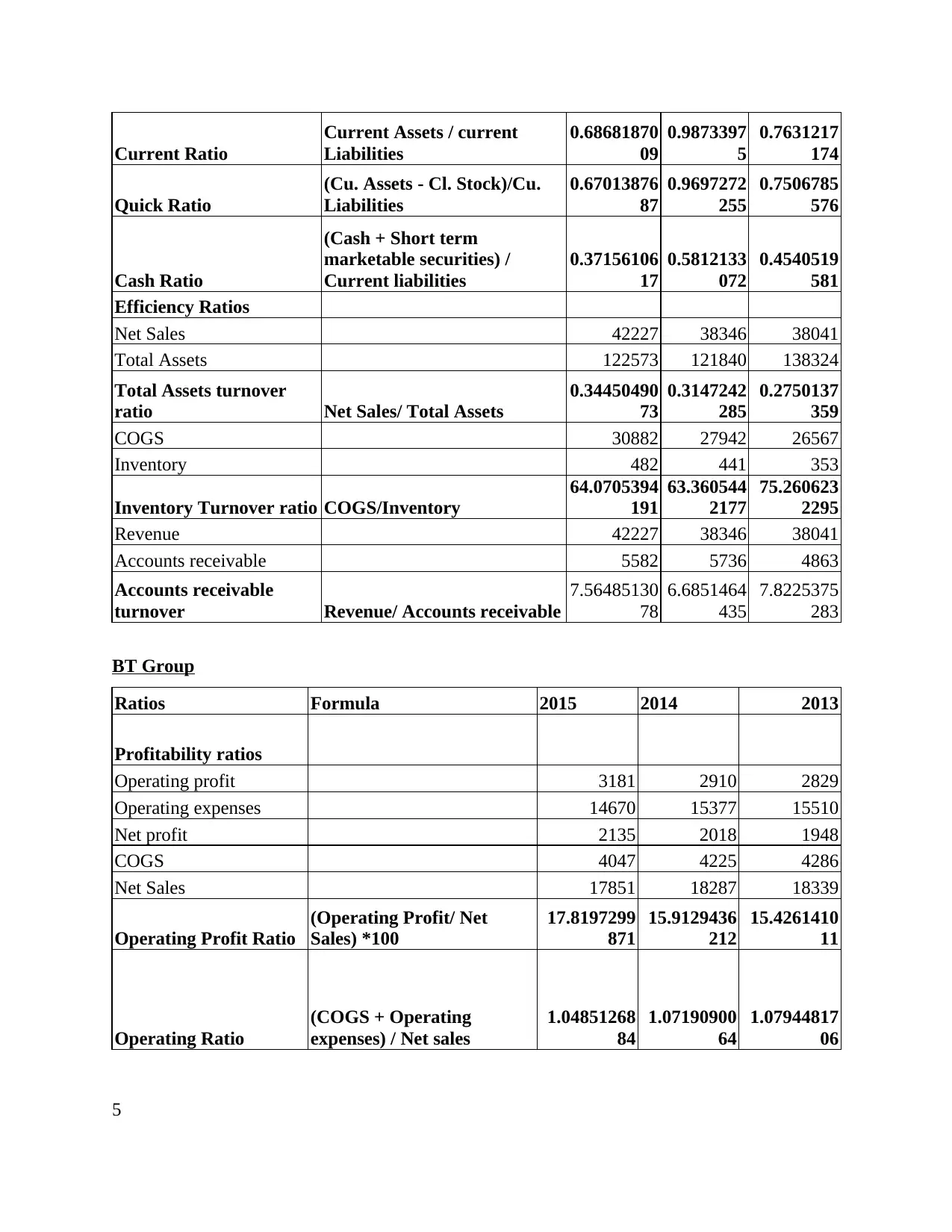

Current Ratio

Current Assets / current

Liabilities

0.68681870

09

0.9873397

5

0.7631217

174

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities

0.67013876

87

0.9697272

255

0.7506785

576

Cash Ratio

(Cash + Short term

marketable securities) /

Current liabilities

0.37156106

17

0.5812133

072

0.4540519

581

Efficiency Ratios

Net Sales 42227 38346 38041

Total Assets 122573 121840 138324

Total Assets turnover

ratio Net Sales/ Total Assets

0.34450490

73

0.3147242

285

0.2750137

359

COGS 30882 27942 26567

Inventory 482 441 353

Inventory Turnover ratio COGS/Inventory

64.0705394

191

63.360544

2177

75.260623

2295

Revenue 42227 38346 38041

Accounts receivable 5582 5736 4863

Accounts receivable

turnover Revenue/ Accounts receivable

7.56485130

78

6.6851464

435

7.8225375

283

BT Group

Ratios Formula 2015 2014 2013

Profitability ratios

Operating profit 3181 2910 2829

Operating expenses 14670 15377 15510

Net profit 2135 2018 1948

COGS 4047 4225 4286

Net Sales 17851 18287 18339

Operating Profit Ratio

(Operating Profit/ Net

Sales) *100

17.8197299

871

15.9129436

212

15.4261410

11

Operating Ratio

(COGS + Operating

expenses) / Net sales

1.04851268

84

1.07190900

64

1.07944817

06

5

Current Assets / current

Liabilities

0.68681870

09

0.9873397

5

0.7631217

174

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities

0.67013876

87

0.9697272

255

0.7506785

576

Cash Ratio

(Cash + Short term

marketable securities) /

Current liabilities

0.37156106

17

0.5812133

072

0.4540519

581

Efficiency Ratios

Net Sales 42227 38346 38041

Total Assets 122573 121840 138324

Total Assets turnover

ratio Net Sales/ Total Assets

0.34450490

73

0.3147242

285

0.2750137

359

COGS 30882 27942 26567

Inventory 482 441 353

Inventory Turnover ratio COGS/Inventory

64.0705394

191

63.360544

2177

75.260623

2295

Revenue 42227 38346 38041

Accounts receivable 5582 5736 4863

Accounts receivable

turnover Revenue/ Accounts receivable

7.56485130

78

6.6851464

435

7.8225375

283

BT Group

Ratios Formula 2015 2014 2013

Profitability ratios

Operating profit 3181 2910 2829

Operating expenses 14670 15377 15510

Net profit 2135 2018 1948

COGS 4047 4225 4286

Net Sales 17851 18287 18339

Operating Profit Ratio

(Operating Profit/ Net

Sales) *100

17.8197299

871

15.9129436

212

15.4261410

11

Operating Ratio

(COGS + Operating

expenses) / Net sales

1.04851268

84

1.07190900

64

1.07944817

06

5

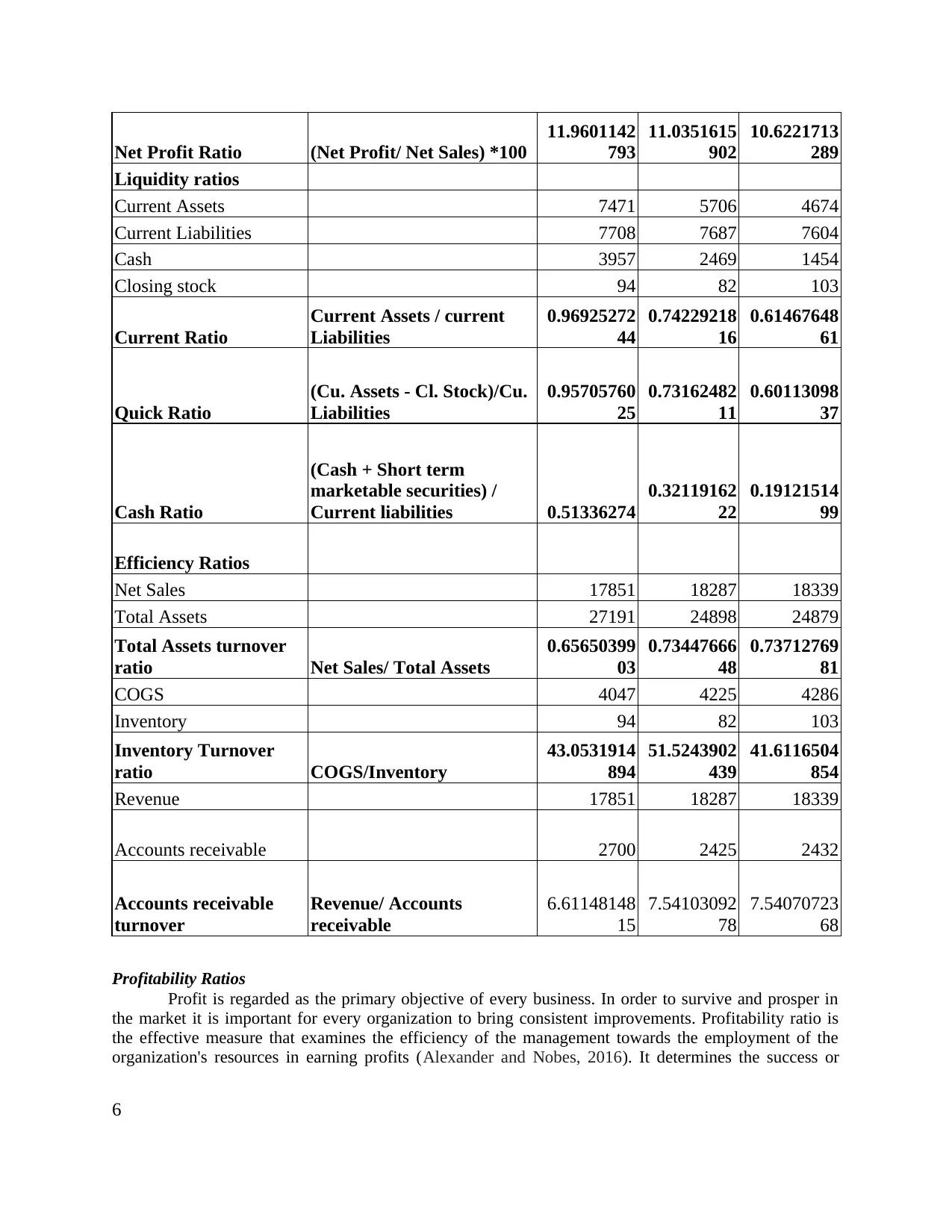

Net Profit Ratio (Net Profit/ Net Sales) *100

11.9601142

793

11.0351615

902

10.6221713

289

Liquidity ratios

Current Assets 7471 5706 4674

Current Liabilities 7708 7687 7604

Cash 3957 2469 1454

Closing stock 94 82 103

Current Ratio

Current Assets / current

Liabilities

0.96925272

44

0.74229218

16

0.61467648

61

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities

0.95705760

25

0.73162482

11

0.60113098

37

Cash Ratio

(Cash + Short term

marketable securities) /

Current liabilities 0.51336274

0.32119162

22

0.19121514

99

Efficiency Ratios

Net Sales 17851 18287 18339

Total Assets 27191 24898 24879

Total Assets turnover

ratio Net Sales/ Total Assets

0.65650399

03

0.73447666

48

0.73712769

81

COGS 4047 4225 4286

Inventory 94 82 103

Inventory Turnover

ratio COGS/Inventory

43.0531914

894

51.5243902

439

41.6116504

854

Revenue 17851 18287 18339

Accounts receivable 2700 2425 2432

Accounts receivable

turnover

Revenue/ Accounts

receivable

6.61148148

15

7.54103092

78

7.54070723

68

Profitability Ratios

Profit is regarded as the primary objective of every business. In order to survive and prosper in

the market it is important for every organization to bring consistent improvements. Profitability ratio is

the effective measure that examines the efficiency of the management towards the employment of the

organization's resources in earning profits (Alexander and Nobes, 2016). It determines the success or

6

11.9601142

793

11.0351615

902

10.6221713

289

Liquidity ratios

Current Assets 7471 5706 4674

Current Liabilities 7708 7687 7604

Cash 3957 2469 1454

Closing stock 94 82 103

Current Ratio

Current Assets / current

Liabilities

0.96925272

44

0.74229218

16

0.61467648

61

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities

0.95705760

25

0.73162482

11

0.60113098

37

Cash Ratio

(Cash + Short term

marketable securities) /

Current liabilities 0.51336274

0.32119162

22

0.19121514

99

Efficiency Ratios

Net Sales 17851 18287 18339

Total Assets 27191 24898 24879

Total Assets turnover

ratio Net Sales/ Total Assets

0.65650399

03

0.73447666

48

0.73712769

81

COGS 4047 4225 4286

Inventory 94 82 103

Inventory Turnover

ratio COGS/Inventory

43.0531914

894

51.5243902

439

41.6116504

854

Revenue 17851 18287 18339

Accounts receivable 2700 2425 2432

Accounts receivable

turnover

Revenue/ Accounts

receivable

6.61148148

15

7.54103092

78

7.54070723

68

Profitability Ratios

Profit is regarded as the primary objective of every business. In order to survive and prosper in

the market it is important for every organization to bring consistent improvements. Profitability ratio is

the effective measure that examines the efficiency of the management towards the employment of the

organization's resources in earning profits (Alexander and Nobes, 2016). It determines the success or

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

failure of concern for specific duration of time. The profitability ratio have been enumerated in the

manner stated as under:

Operating profit ratio: It is also referred to as operating margin ratio. It determines the percentage

of total revenue that is made up through operating income. In other words operating margin ratio

reflects the amount of revenue that are left after all the variables or operating could are being paid

off (Zhou, Ou and Li, 2016). On the other hand this ratio examines the proportion of revenue that

is available to cover the non-operating costs such as interest expense. The operating profit ratio is

the key indicator for creditors and investors to review the manner in which organization support

its operations. From the analysis of the above tables it can be examined that operating margin

ratio of Vodafone in the year 2015, 2014 and 2013 is 4.65, -10.20 as well as -5.78 respectively. In

contrast to this operating profit ratio of BT Group in 2015, 2014 and 2013 is 17.81, 15.91 as well

as 15.42 respectively. This presents that operating profit ratio of BT group is higher. Thus this

reflects the organization is making adequate money through its ongoing operations to make

payment towards its variable costs and fixed costs. However lower operating profit ratio of

Vodafone demonstrate that it does not making adequate amount of funds from its ongoing

operations.

Operating ratio: It is referred to as the financial term that defines the organization's operating

expenses as the percentage of revenue. Such kind of financial ratio is commonly used by the

industries who requires large percentage revenues for maintenance of operations ( Collier, 2015).

By carrying out analysis of the above tables it has been interpreted that operating ratio of

Vodafone in the year 2015, 2014 and 2013 is 1.68, 1.83 as well as 1.75 respectively. In contrast

to this operating ratio of BT Group in 2015, 2014 and 2013 is 1.04, 1.07 as well as 1.08

respectively. This presents that operating ratio of Vodafone is higher. This demonstrates that

company possess greater amount of revenue that can be used for the purpose of managing its

operations.

Net profit ratio: It is also known as return on sales ratio. It is effective in measuring the net

income earned by every dollar of the sales generated through comparison of net sales and net

income of the organization (Cahan, 2016). From the analysis of the above tables it has been

examined that net profit ratio of Vodafone in the year 2015, 2014 and 2013 is 13.64, 154.52 as

well as 1.08 respectively. In contrast to this net profit ratio of BT Group in 2015, 2014 and 2013

is 11.96, 11.03 as well as 10.62 respectively. This presents that net profit ratio of Vodafone is

higher. Thus this reflects the organization is able to manage its expenses in relation to net sales.

In contrast to this lower net profit ratio of BT group demonstrates that company is unable to

manage its expenses that relates with net sales.

Liquidity Ratios

It is the ratio that measures the adequacy of the current as well as liquid assets. Further it makes

evaluation of ability of firm to pay its short term debts.

Current ratio: It is the liquidity ratio that examines ability of the organization to make payment

against its short term liabilities (Macve, 2015). By carrying out analysis of the above tables it has

been interpreted that current ratio of Vodafone in the year 2015, 2014 and 2013 is 0.68, 0.98 as

well as 0.76 respectively. In contrast to this current ratio of BT Group in 2015, 2014 and 2013 is

0.96, 0.74 as well as 0.61 respectively. This presents that current ratio of BT group is higher in

2015. This presents that company is effectively making payment of current debts. On the other

hand Vodafone has lower current ratio that demonstrate that is unable to make payment against

its current debts. This might be due to decrease in organizational sales.

Quick ratio: This is liquidity ratio that measures the ability of the organization to make payment

against its current liabilities when they come due with only quick assets (Brown and Dillard,

2015). From the evaluation of the tables above it has been determined that quick ratio of BT

Group in the year 2015, 2014 and 2013 is 0.95, 0.73 as well as 0.60 respectively. In contrast to

7

manner stated as under:

Operating profit ratio: It is also referred to as operating margin ratio. It determines the percentage

of total revenue that is made up through operating income. In other words operating margin ratio

reflects the amount of revenue that are left after all the variables or operating could are being paid

off (Zhou, Ou and Li, 2016). On the other hand this ratio examines the proportion of revenue that

is available to cover the non-operating costs such as interest expense. The operating profit ratio is

the key indicator for creditors and investors to review the manner in which organization support

its operations. From the analysis of the above tables it can be examined that operating margin

ratio of Vodafone in the year 2015, 2014 and 2013 is 4.65, -10.20 as well as -5.78 respectively. In

contrast to this operating profit ratio of BT Group in 2015, 2014 and 2013 is 17.81, 15.91 as well

as 15.42 respectively. This presents that operating profit ratio of BT group is higher. Thus this

reflects the organization is making adequate money through its ongoing operations to make

payment towards its variable costs and fixed costs. However lower operating profit ratio of

Vodafone demonstrate that it does not making adequate amount of funds from its ongoing

operations.

Operating ratio: It is referred to as the financial term that defines the organization's operating

expenses as the percentage of revenue. Such kind of financial ratio is commonly used by the

industries who requires large percentage revenues for maintenance of operations ( Collier, 2015).

By carrying out analysis of the above tables it has been interpreted that operating ratio of

Vodafone in the year 2015, 2014 and 2013 is 1.68, 1.83 as well as 1.75 respectively. In contrast

to this operating ratio of BT Group in 2015, 2014 and 2013 is 1.04, 1.07 as well as 1.08

respectively. This presents that operating ratio of Vodafone is higher. This demonstrates that

company possess greater amount of revenue that can be used for the purpose of managing its

operations.

Net profit ratio: It is also known as return on sales ratio. It is effective in measuring the net

income earned by every dollar of the sales generated through comparison of net sales and net

income of the organization (Cahan, 2016). From the analysis of the above tables it has been

examined that net profit ratio of Vodafone in the year 2015, 2014 and 2013 is 13.64, 154.52 as

well as 1.08 respectively. In contrast to this net profit ratio of BT Group in 2015, 2014 and 2013

is 11.96, 11.03 as well as 10.62 respectively. This presents that net profit ratio of Vodafone is

higher. Thus this reflects the organization is able to manage its expenses in relation to net sales.

In contrast to this lower net profit ratio of BT group demonstrates that company is unable to

manage its expenses that relates with net sales.

Liquidity Ratios

It is the ratio that measures the adequacy of the current as well as liquid assets. Further it makes

evaluation of ability of firm to pay its short term debts.

Current ratio: It is the liquidity ratio that examines ability of the organization to make payment

against its short term liabilities (Macve, 2015). By carrying out analysis of the above tables it has

been interpreted that current ratio of Vodafone in the year 2015, 2014 and 2013 is 0.68, 0.98 as

well as 0.76 respectively. In contrast to this current ratio of BT Group in 2015, 2014 and 2013 is

0.96, 0.74 as well as 0.61 respectively. This presents that current ratio of BT group is higher in

2015. This presents that company is effectively making payment of current debts. On the other

hand Vodafone has lower current ratio that demonstrate that is unable to make payment against

its current debts. This might be due to decrease in organizational sales.

Quick ratio: This is liquidity ratio that measures the ability of the organization to make payment

against its current liabilities when they come due with only quick assets (Brown and Dillard,

2015). From the evaluation of the tables above it has been determined that quick ratio of BT

Group in the year 2015, 2014 and 2013 is 0.95, 0.73 as well as 0.60 respectively. In contrast to

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

this quick ratio of Vodafone in 2015, 2014 and 2013 is 0.67, 0.96 as well as 0.75 respectively.

This presents that quick ratio of BT group is higher as compared to Vodafone. Thus this reflects

the organization is able to make payment against its current liabilities without selling long term

assets. On the other hand lower quick ratio of Vodafone demonstrates that it makes payment for

its current liabilities by making sales of its long term assets. This is due to increasing in the

current liabilities of the firm.

Cash ratio: This ratio is also referred to as cash coverage ratio. It measures the ability of the

organization to pay off its current liabilities through only cash and cash equivalents (Grifell-Tatjé

and Lovell, 2015). By carrying out analysis of the above tables it has been interpreted that cash

ratio of Vodafone in the year 2015, 2014 and 2013 is 0.37, 0.58 as well as 0.45 respectively. In

contrast to this cash ratio of BT Group in 2015, 2014 and 2013 is 0.51, 0.32 as well as 0.19

respectively. This presents that cash ratio of Vodafone group is higher. This presents that

company is more liquid and can easily fund its debts. In contrast to this BT group possess lower

cash ratio which implies that it not much liquid and is unable to funds its debts in an effective

manner.

Efficiency Ratios

Efficiency ratio is the one that measure the extent to which the firm make effective utilization of

its assets and manages its liabilities (Farrow, 2015).

Total asset turnover ratio: It is an efficiency ratio that presents the extent to which the firm is

successful in using its assets towards generation of revenue (Sanchez-Matamoros, Gutiérrez-

Hidalgo and Macías, 2015). From the analysis of the above tables it has been examined that asset

turnover ratio of Vodafone in the year 2015, 2014 and 2013 is 0.34, 0.31 as well as 0.27

respectively. In contrast to this asset turnover ratio of BT Group in 2015, 2014 and 2013 is 0.65,

0.73 as well as 0.74 respectively. This presents that asset turnover ratio of BT Group is higher.

Hence it shows that Vodafone is not able to manage its assets in an optimum manner. On the

other hand lower ratio of Vodafone presents its ability to manage the asset with effectiveness.

Inventory turnover ratio: It is the ratio that presents the manner in which inventory is managed

through comparison of cost of goods sold with inventory for particular period (Wills and Napier-

Munn, 2015). By carrying out analysis of the above tables it has been interpreted that inventory

turnover ratio of Vodafone in the year 2015, 2014 and 2013 is 0.34, 0.31 as well as 0.27

respectively. In contrast to this operating profit ratio of BT Group in 2015, 2014 and 2013 is

43.05, 51.52 as well as 41.61 respectively. This presents that inventory turnover of BT group is

higher and it implies that firm does not over spends by purchasing too much inventory. Further it

does not wastes its resources through storage of non-saleable inventory. On the other hand

Vodafone makes storage of inventory which increases in turnover ratio. This increases the cost of

the firm to a greater level.

Account receivable turnover ratio: It is the efficiency ratio that determines the number of times

firm can turn its accounts receivables into cash during particular time span ( Efficiency ratios,

2016). From the analysis of the above tables it has been interpreted that account receivable

turnover of Vodafone in the year 2015, 2014 and 2013 is 7.56, 6.68 as well as 7.82 respectively.

On the contrary accounts receivable turnover ratio of BT Group in 2015, 2014 and 2013 is 6.61,

7.54 as well as 7.54 respectively. This presents that accounts receivable turnover ratio of

Vodafone is higher. Thus the company is able to collects its receivables more frequently

throughout the year. However BT group is not able to gather its receivable more frequently

within particular year.

CONCLUSION AND RECOMMENDATION

It can be concluded from the study that role of accounting can be greatly viewed towards

examining the financial position of the company. It has been inferred from the comparison of both the

8

This presents that quick ratio of BT group is higher as compared to Vodafone. Thus this reflects

the organization is able to make payment against its current liabilities without selling long term

assets. On the other hand lower quick ratio of Vodafone demonstrates that it makes payment for

its current liabilities by making sales of its long term assets. This is due to increasing in the

current liabilities of the firm.

Cash ratio: This ratio is also referred to as cash coverage ratio. It measures the ability of the

organization to pay off its current liabilities through only cash and cash equivalents (Grifell-Tatjé

and Lovell, 2015). By carrying out analysis of the above tables it has been interpreted that cash

ratio of Vodafone in the year 2015, 2014 and 2013 is 0.37, 0.58 as well as 0.45 respectively. In

contrast to this cash ratio of BT Group in 2015, 2014 and 2013 is 0.51, 0.32 as well as 0.19

respectively. This presents that cash ratio of Vodafone group is higher. This presents that

company is more liquid and can easily fund its debts. In contrast to this BT group possess lower

cash ratio which implies that it not much liquid and is unable to funds its debts in an effective

manner.

Efficiency Ratios

Efficiency ratio is the one that measure the extent to which the firm make effective utilization of

its assets and manages its liabilities (Farrow, 2015).

Total asset turnover ratio: It is an efficiency ratio that presents the extent to which the firm is

successful in using its assets towards generation of revenue (Sanchez-Matamoros, Gutiérrez-

Hidalgo and Macías, 2015). From the analysis of the above tables it has been examined that asset

turnover ratio of Vodafone in the year 2015, 2014 and 2013 is 0.34, 0.31 as well as 0.27

respectively. In contrast to this asset turnover ratio of BT Group in 2015, 2014 and 2013 is 0.65,

0.73 as well as 0.74 respectively. This presents that asset turnover ratio of BT Group is higher.

Hence it shows that Vodafone is not able to manage its assets in an optimum manner. On the

other hand lower ratio of Vodafone presents its ability to manage the asset with effectiveness.

Inventory turnover ratio: It is the ratio that presents the manner in which inventory is managed

through comparison of cost of goods sold with inventory for particular period (Wills and Napier-

Munn, 2015). By carrying out analysis of the above tables it has been interpreted that inventory

turnover ratio of Vodafone in the year 2015, 2014 and 2013 is 0.34, 0.31 as well as 0.27

respectively. In contrast to this operating profit ratio of BT Group in 2015, 2014 and 2013 is

43.05, 51.52 as well as 41.61 respectively. This presents that inventory turnover of BT group is

higher and it implies that firm does not over spends by purchasing too much inventory. Further it

does not wastes its resources through storage of non-saleable inventory. On the other hand

Vodafone makes storage of inventory which increases in turnover ratio. This increases the cost of

the firm to a greater level.

Account receivable turnover ratio: It is the efficiency ratio that determines the number of times

firm can turn its accounts receivables into cash during particular time span ( Efficiency ratios,

2016). From the analysis of the above tables it has been interpreted that account receivable

turnover of Vodafone in the year 2015, 2014 and 2013 is 7.56, 6.68 as well as 7.82 respectively.

On the contrary accounts receivable turnover ratio of BT Group in 2015, 2014 and 2013 is 6.61,

7.54 as well as 7.54 respectively. This presents that accounts receivable turnover ratio of

Vodafone is higher. Thus the company is able to collects its receivables more frequently

throughout the year. However BT group is not able to gather its receivable more frequently

within particular year.

CONCLUSION AND RECOMMENDATION

It can be concluded from the study that role of accounting can be greatly viewed towards

examining the financial position of the company. It has been inferred from the comparison of both the

8

telecommunication companies that position of Vodafone is much sound in comparison with BT group.

Along with this, ratio analysis provides that financial health of Vodafone is good. This presents that firm

has kept control over its expenses and is able to make payment against its debts in an effective manner. It

can also be concluded from the present report that liquidity position of BT group is more stable which

implies that firm is capable of to paying its short term obligations.

It is recommended to BT group to enhance its control over the expenses so that it can increase its

profitability to a greater extent. Along with this efficiency of the firm can be increased when it effectively

makes utilization of its assets for the purpose of attaining its pre-determined targets (Hilmola and Gupta,

2015).

9

Along with this, ratio analysis provides that financial health of Vodafone is good. This presents that firm

has kept control over its expenses and is able to make payment against its debts in an effective manner. It

can also be concluded from the present report that liquidity position of BT group is more stable which

implies that firm is capable of to paying its short term obligations.

It is recommended to BT group to enhance its control over the expenses so that it can increase its

profitability to a greater extent. Along with this efficiency of the firm can be increased when it effectively

makes utilization of its assets for the purpose of attaining its pre-determined targets (Hilmola and Gupta,

2015).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Journals and Books

Alexander, D. and Nobes, C., 2016. Financial Accounting 6th Edition. Pearson Higher Ed.

Brown, J. and Dillard, J., 2015. Opening Accounting to Critical Scrutiny: Towards Dialogic

Accounting for Policy Analysis and Democracy. Journal of Comparative Policy Analysis:

Research and Practice. 17(3). pp.247-268.

Cahan, S., 2016. Consequences of IFRS for capital markets, managers, auditors and standard‐

setters: an introduction. Accounting & Finance. 56(1). pp.5-8.

Collier, P. M., 2015. Accounting for managers: Interpreting accounting information for decision

making. John Wiley & Sons.

Farrow, S., 2015. Residual Risk Accounting: A Pilot Study. Review of Income and Wealth.

Grifell-Tatjé, E. and Lovell, C. K., 2015. Productivity Accounting. Cambridge University Press.

Groom, E., Rapti, R. S. and Pardina, M. R., 2016. Accounting for infrastructure regulation: an

introduction.

Heintz, J. and Parry, R., 2016. College Accounting Chapters 1-27. Cengage Learning.

Hilmola, O. P. and Gupta, M., 2015. Throughput accounting and performance of a

manufacturing company under stochastic demand and scrap rates.Expert Systems with

Applications. 42(22). pp.8423-8431.

Li, X., 2015. Accounting conservatism and the cost of capital: An international analysis. Journal

of Business Finance & Accounting. 42(5-6). pp.555-582.

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Sanchez-Matamoros, J. B., Gutiérrez-Hidalgo, F. and Macías, M., 2015. Innovation in

accounting thought and practice–an introduction. Accounting History. 20(3). pp.247-249.

Scott, P., 2016. Accounting for Business. Oxford University Press.

Taylor, S. J., Bogdan, R. and DeVault, M., 2015. Introduction to qualitative research methods:

A guidebook and resource. John Wiley & Sons.

Wills, B. A. and Napier-Munn, T., 2015. Wills' mineral processing technology: an introduction

to the practical aspects of ore treatment and mineral recovery. Butterworth-Heinemann.

10

Journals and Books

Alexander, D. and Nobes, C., 2016. Financial Accounting 6th Edition. Pearson Higher Ed.

Brown, J. and Dillard, J., 2015. Opening Accounting to Critical Scrutiny: Towards Dialogic

Accounting for Policy Analysis and Democracy. Journal of Comparative Policy Analysis:

Research and Practice. 17(3). pp.247-268.

Cahan, S., 2016. Consequences of IFRS for capital markets, managers, auditors and standard‐

setters: an introduction. Accounting & Finance. 56(1). pp.5-8.

Collier, P. M., 2015. Accounting for managers: Interpreting accounting information for decision

making. John Wiley & Sons.

Farrow, S., 2015. Residual Risk Accounting: A Pilot Study. Review of Income and Wealth.

Grifell-Tatjé, E. and Lovell, C. K., 2015. Productivity Accounting. Cambridge University Press.

Groom, E., Rapti, R. S. and Pardina, M. R., 2016. Accounting for infrastructure regulation: an

introduction.

Heintz, J. and Parry, R., 2016. College Accounting Chapters 1-27. Cengage Learning.

Hilmola, O. P. and Gupta, M., 2015. Throughput accounting and performance of a

manufacturing company under stochastic demand and scrap rates.Expert Systems with

Applications. 42(22). pp.8423-8431.

Li, X., 2015. Accounting conservatism and the cost of capital: An international analysis. Journal

of Business Finance & Accounting. 42(5-6). pp.555-582.

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Sanchez-Matamoros, J. B., Gutiérrez-Hidalgo, F. and Macías, M., 2015. Innovation in

accounting thought and practice–an introduction. Accounting History. 20(3). pp.247-249.

Scott, P., 2016. Accounting for Business. Oxford University Press.

Taylor, S. J., Bogdan, R. and DeVault, M., 2015. Introduction to qualitative research methods:

A guidebook and resource. John Wiley & Sons.

Wills, B. A. and Napier-Munn, T., 2015. Wills' mineral processing technology: an introduction

to the practical aspects of ore treatment and mineral recovery. Butterworth-Heinemann.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Zhou, Z., Ou, J. and Li, S., 2016. Ecological Accounting: A Research Review and Conceptual

Framework. Journal of Environmental Protection. 7(05). p.643.

Online

BT Group. 2016. [Online]. Available through:

<http://markets.ft.com/research/Markets/Tearsheets/Financials?

s=BT.A:LSE&subview=BalanceSheet>. [Accessed on 18th April 2016].

Efficiency ratios. 2016. [Online]. Available through:

<http://news.morningstar.com/classroom2/course.asp?docId=145093&page=3>. [Accessed on

18th April 2016].

Vodafone Group PLC. 2016. [Online]. Available through:

<http://markets.ft.com/research/Markets/Tearsheets/Financials?

s=VOD:LSE&subview=BalanceSheet>. [Accessed on 18th April 2016].

11

Framework. Journal of Environmental Protection. 7(05). p.643.

Online

BT Group. 2016. [Online]. Available through:

<http://markets.ft.com/research/Markets/Tearsheets/Financials?

s=BT.A:LSE&subview=BalanceSheet>. [Accessed on 18th April 2016].

Efficiency ratios. 2016. [Online]. Available through:

<http://news.morningstar.com/classroom2/course.asp?docId=145093&page=3>. [Accessed on

18th April 2016].

Vodafone Group PLC. 2016. [Online]. Available through:

<http://markets.ft.com/research/Markets/Tearsheets/Financials?

s=VOD:LSE&subview=BalanceSheet>. [Accessed on 18th April 2016].

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.