Financial Accounting Report: Weather and Sons & Company Performance

VerifiedAdded on 2019/12/04

|17

|4102

|162

Report

AI Summary

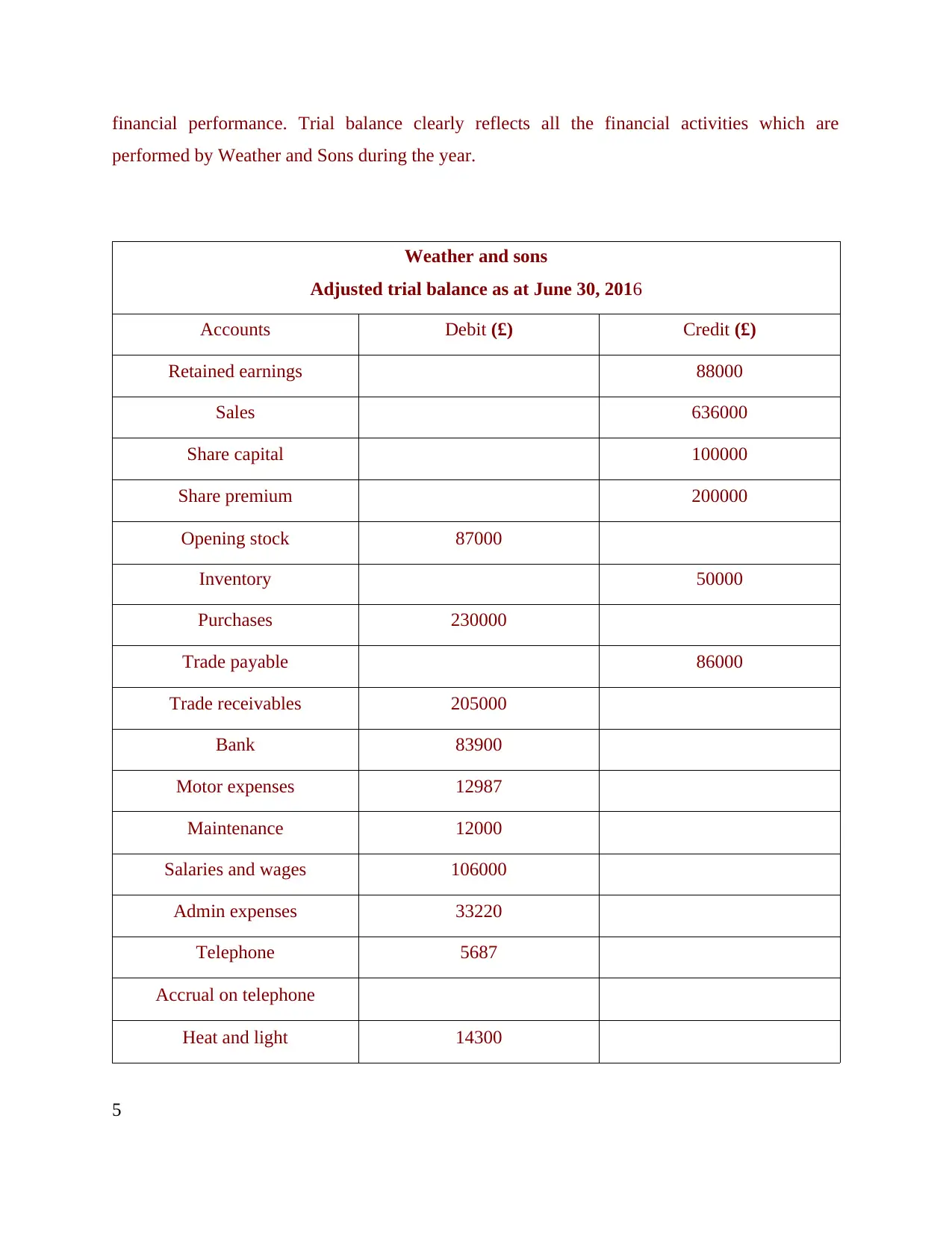

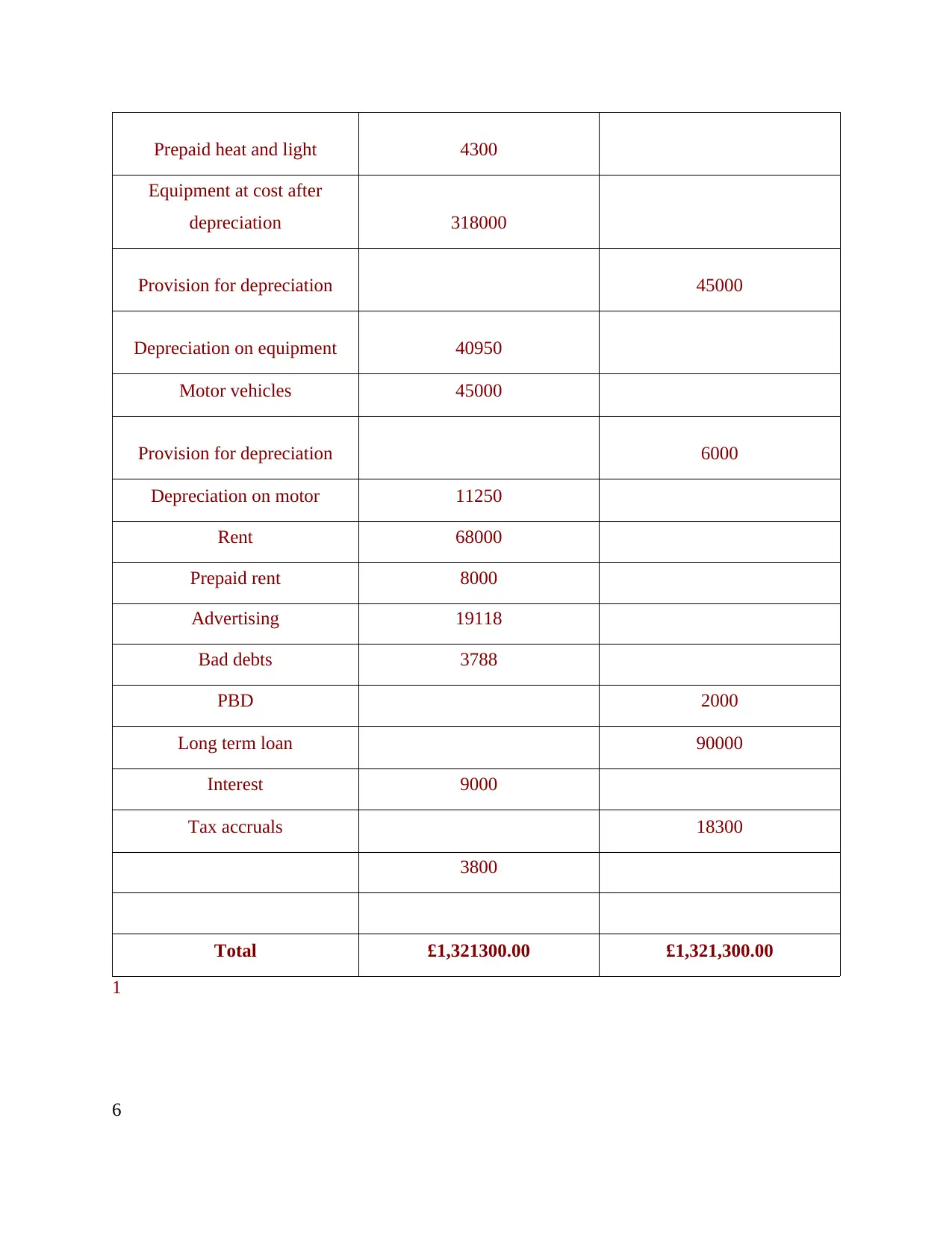

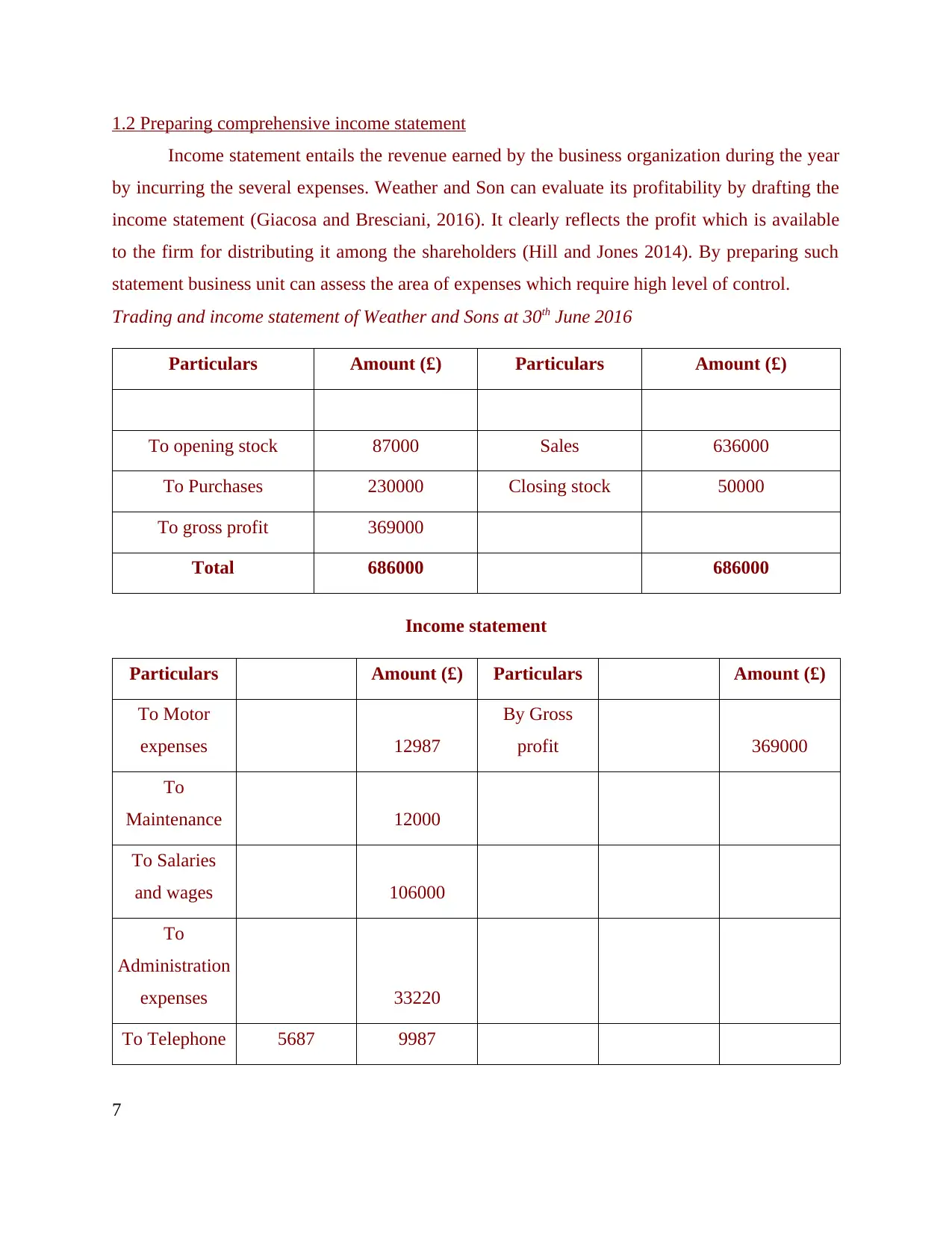

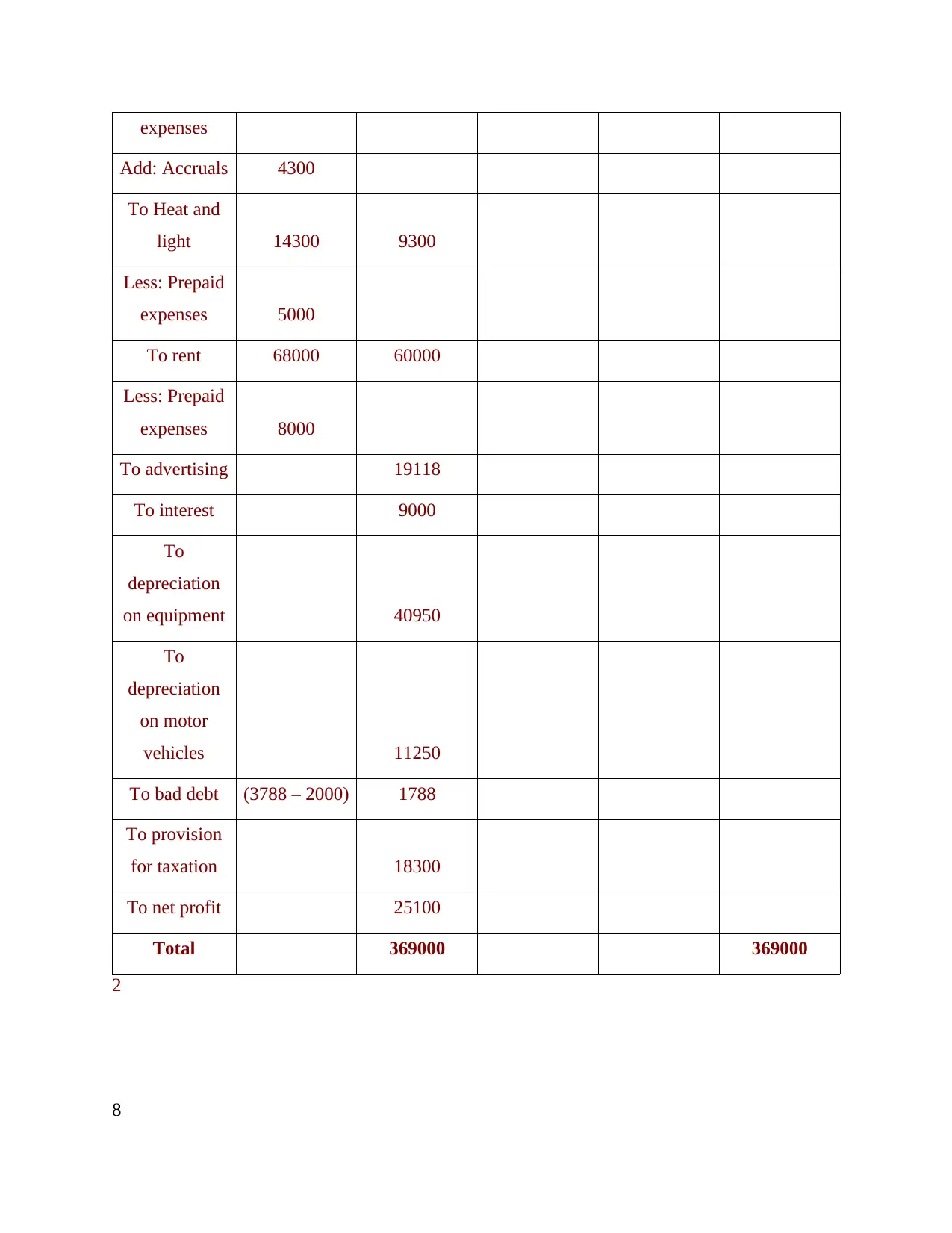

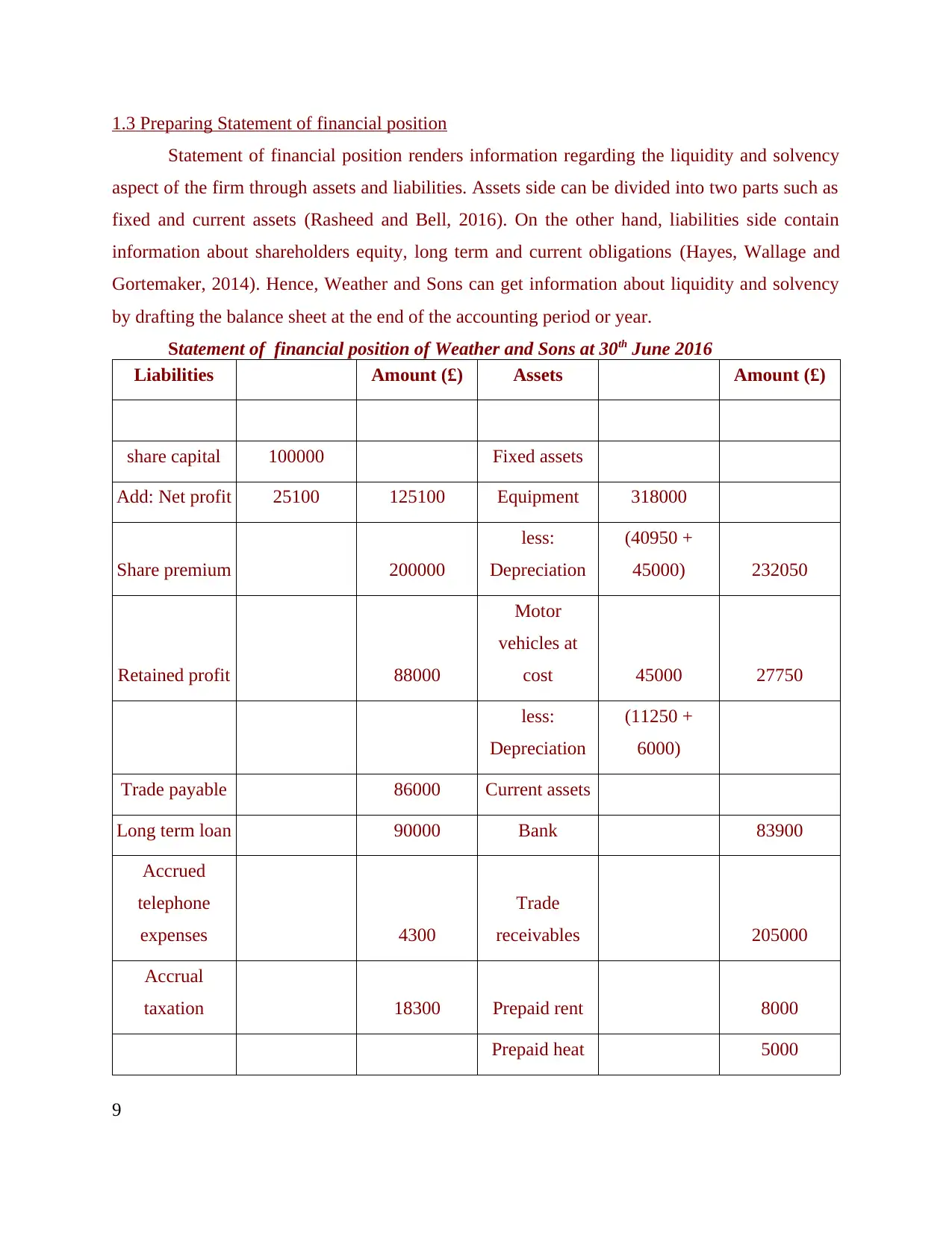

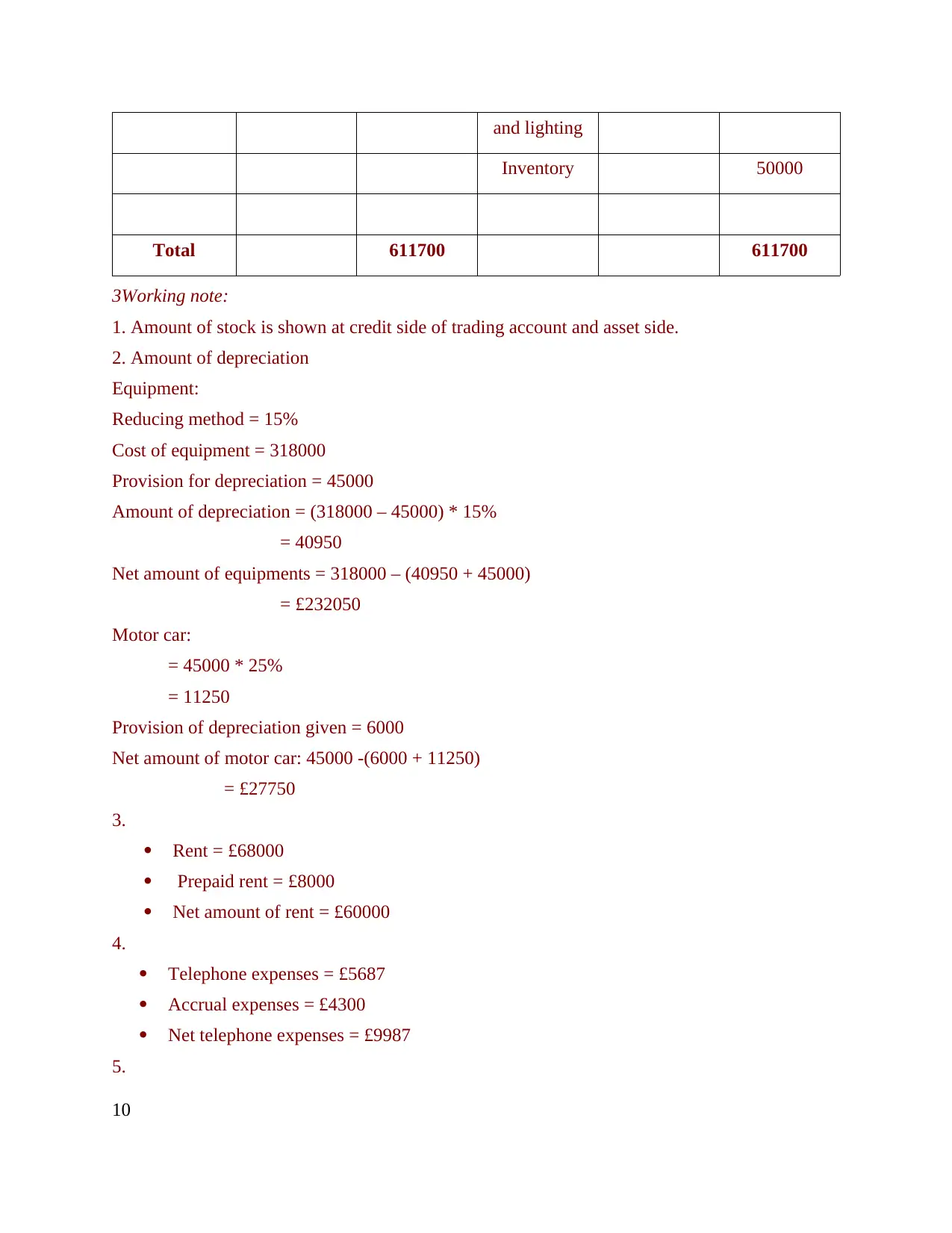

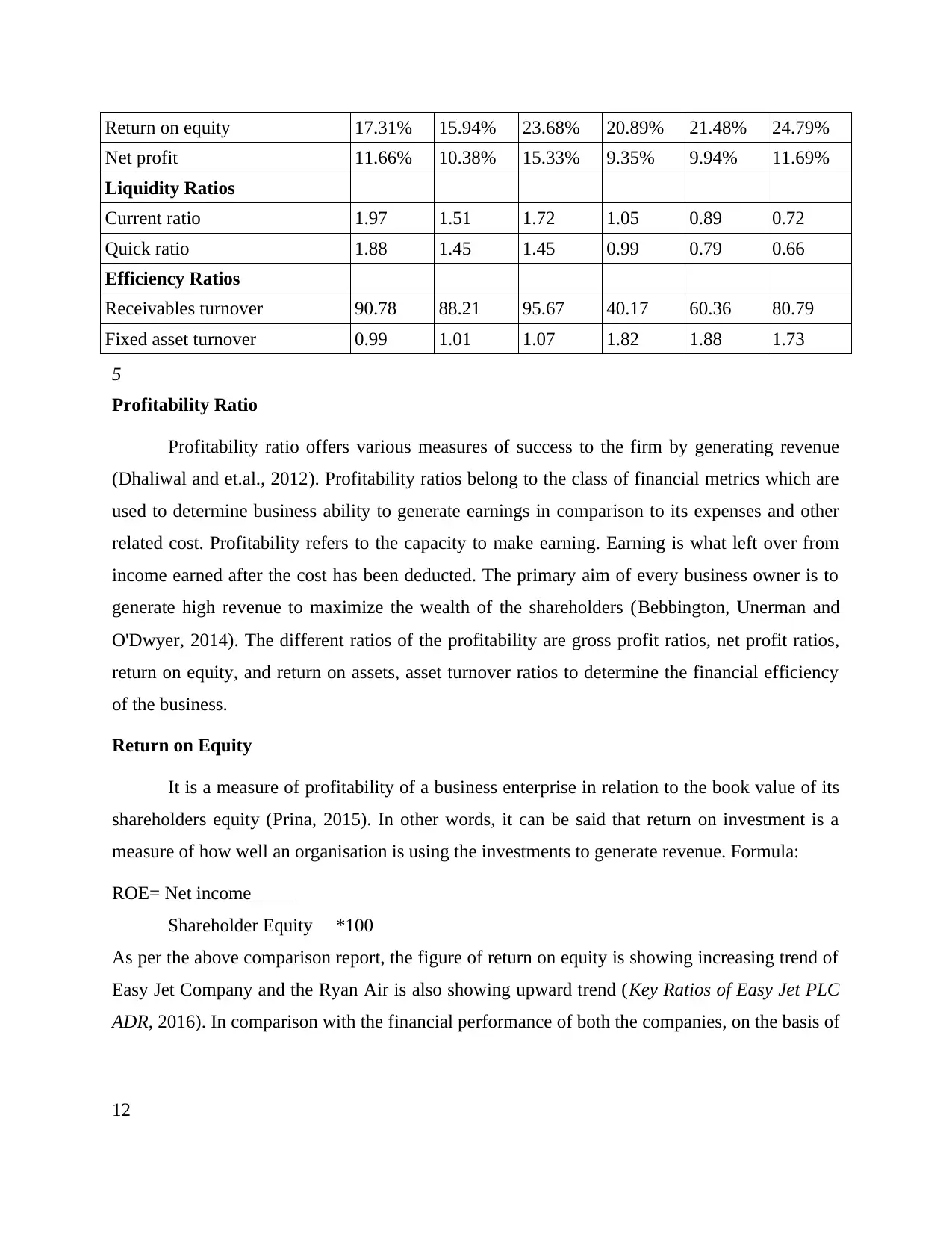

This report provides a comprehensive analysis of financial accounting principles and practices. It begins with an introduction to accounting, defining its role in maintaining financial records and communicating information to stakeholders. The report then delves into a practical application, focusing on Weather and Sons, where it prepares an adjusted trial balance, a comprehensive income statement, and a statement of financial position. These financial statements are crucial for understanding a company's financial health and performance. Furthermore, the report extends its analysis by comparing the financial performance of two organizations, utilizing financial ratios to assess their profitability and efficiency. The report uses tables to present the financial data, including adjusted trial balances, income statements, balance sheets, and comparison charts, offering a clear and organized presentation of the financial information and analysis. This report is a valuable resource for students studying accounting and finance, offering insights into real-world financial statement analysis and performance evaluation.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.