Accounting Policies and Estimates Used by BP Billiton Company Analysis

VerifiedAdded on 2020/04/07

|19

|4041

|41

Report

AI Summary

This report delves into the accounting policies and estimates employed by BP Billiton, a prominent Australian conglomerate in the oil and gas sector. It examines their adherence to International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP), focusing on depreciation methods, lease accounting (AASB16), impairment tests (IAS-136), and consolidation practices (AASB-5). The analysis includes a comparison of BP Billiton's accounting approaches with those of competitors like Morrison plc and Wesfarmers Plc, assessing accounting flexibility and potential red flags in their financial reporting. The report highlights the estimates used for income tax, inventory valuation, and other financial aspects. Furthermore, it suggests improvements for accounting policies and estimates and concludes with an overview of the reporting frameworks and stakeholders' requirements.

RUNNING HEAD: Accounting policies and estimates used by firm

1

Name of the Student-

Title- Accounting and reporting frameworks

University Name-

1

Name of the Student-

Title- Accounting and reporting frameworks

University Name-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting policies and estimates used by firm 2

Table of Contents

Introduction.................................................................................................................................................3

Accounting policies and GAAP rules followed by BP Billiton Company.......................................................4

Estimates used by BP Billiton Company...................................................................................................5

Estimates used by rivals...........................................................................................................................6

Comparison of accounting policies and estimates used by BP Billiton Company s and Morrison plc......6

Assesse accounting flexibility..................................................................................................................8

Evaluation of accounting strategies and policies.........................................................................................8

Changes in accounting estimates by the BP Billiton Company................................................................9

Suggestion for accounting policies and estimates prepared by BP Billiton Company............................10

Red flag in accounting report of BP Billiton Company...............................................................................10

Conclusion.................................................................................................................................................15

References.................................................................................................................................................16

Appendix...................................................................................................................................................19

Table of Contents

Introduction.................................................................................................................................................3

Accounting policies and GAAP rules followed by BP Billiton Company.......................................................4

Estimates used by BP Billiton Company...................................................................................................5

Estimates used by rivals...........................................................................................................................6

Comparison of accounting policies and estimates used by BP Billiton Company s and Morrison plc......6

Assesse accounting flexibility..................................................................................................................8

Evaluation of accounting strategies and policies.........................................................................................8

Changes in accounting estimates by the BP Billiton Company................................................................9

Suggestion for accounting policies and estimates prepared by BP Billiton Company............................10

Red flag in accounting report of BP Billiton Company...............................................................................10

Conclusion.................................................................................................................................................15

References.................................................................................................................................................16

Appendix...................................................................................................................................................19

Accounting policies and estimates used by firm 3

Introduction

This report reflects the debt understanding on normative and positive theories of financial

accounting. Each and every company needs to establish proper level of harmonization in

domestic and international accounting standards. There are several companies such as BP

Billiton Company, Wesfarmers plc and Morrison plc that have been running its business since

very long time in Australia. However, due to the different accounting sets and standards, these

companies have been facing several red flag while reporting its financial standardsIn this report,

it is given that reporting frameworks of organization are depends upon the accounting standards

and reporting framework of organization. It is observed that Accounting policies are the standard

and specific rules, procedure and accounting implication which are used by accountant to prepare

the accounts and financial reporting of organization. In this report study has been prepared how

BP Billiton Company has been following IFRS rules and possible red flags faced by company in

its reporting frameworks.

Present description of organization

In this report BP Billiton Company has been taken into consideration to identify the

estimates in accounting reporting and red flags in accounting and reporting of financial statement

of company. It is Australian Conglomerate Company which has been providing oil and gas

services on domestic and international level. This company has followed proper level of

international financial reporting standards and endeavor towards harmonization in GAAP rules

and regulation and application international accounting standard (Kieso, Weygandt and

Warfield, 2010)

Introduction

This report reflects the debt understanding on normative and positive theories of financial

accounting. Each and every company needs to establish proper level of harmonization in

domestic and international accounting standards. There are several companies such as BP

Billiton Company, Wesfarmers plc and Morrison plc that have been running its business since

very long time in Australia. However, due to the different accounting sets and standards, these

companies have been facing several red flag while reporting its financial standardsIn this report,

it is given that reporting frameworks of organization are depends upon the accounting standards

and reporting framework of organization. It is observed that Accounting policies are the standard

and specific rules, procedure and accounting implication which are used by accountant to prepare

the accounts and financial reporting of organization. In this report study has been prepared how

BP Billiton Company has been following IFRS rules and possible red flags faced by company in

its reporting frameworks.

Present description of organization

In this report BP Billiton Company has been taken into consideration to identify the

estimates in accounting reporting and red flags in accounting and reporting of financial statement

of company. It is Australian Conglomerate Company which has been providing oil and gas

services on domestic and international level. This company has followed proper level of

international financial reporting standards and endeavor towards harmonization in GAAP rules

and regulation and application international accounting standard (Kieso, Weygandt and

Warfield, 2010)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting policies and estimates used by firm 4

Accounting policies and GAAP rules followed by BP Billiton Company

There are several financial and accounting policies followed by BP Billiton Company while

accounting and reporting of financial statement (Irvine and Moerman, 2017).

BP Billiton Company has adopted straight line and written down method to charge

deprecation on its assets. With the help of these depreciation methods, company could

reflect the true and fair view to reflects the true value of its assets as per the IFRS rules

and standards (Hussey and Ong, 2017).

There is another implication which is related to AASB16 lease, BP Billiton Company has

made provision of right-of-use assets while reporting its underlying leased assets in the

business.

All the assets and consolidation of financial statement of company has been done as per

the AASB-5 IFRS rules and accounting standards (Cairns, et al. 2011).

With a view to showcase the true and fair view of assets of company, BP Billiton

Company has implemented impairment test in its business functioning. All the

impairment loss has been charged from the cash generating units of organization after

deducting the amount from the goodwill. (de Ricquebourg and Jonathan, 2013).

BP Billiton Company has prepared its financial statement after following AASB 101.

This level of reporting frameworks has allowed BP Billiton Company to increase the

transparency and effectiveness of financial statements in determined approach.

AASB-117 has also been followed by BP Billiton Company to strengthen its accounting

and reporting of its leased assets to its stakeholders in determined approach.

Accounting policies and GAAP rules followed by BP Billiton Company

There are several financial and accounting policies followed by BP Billiton Company while

accounting and reporting of financial statement (Irvine and Moerman, 2017).

BP Billiton Company has adopted straight line and written down method to charge

deprecation on its assets. With the help of these depreciation methods, company could

reflect the true and fair view to reflects the true value of its assets as per the IFRS rules

and standards (Hussey and Ong, 2017).

There is another implication which is related to AASB16 lease, BP Billiton Company has

made provision of right-of-use assets while reporting its underlying leased assets in the

business.

All the assets and consolidation of financial statement of company has been done as per

the AASB-5 IFRS rules and accounting standards (Cairns, et al. 2011).

With a view to showcase the true and fair view of assets of company, BP Billiton

Company has implemented impairment test in its business functioning. All the

impairment loss has been charged from the cash generating units of organization after

deducting the amount from the goodwill. (de Ricquebourg and Jonathan, 2013).

BP Billiton Company has prepared its financial statement after following AASB 101.

This level of reporting frameworks has allowed BP Billiton Company to increase the

transparency and effectiveness of financial statements in determined approach.

AASB-117 has also been followed by BP Billiton Company to strengthen its accounting

and reporting of its leased assets to its stakeholders in determined approach.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting policies and estimates used by firm 5

Estimates used by BP Billiton Company

BP Billiton Company has implemented proper rules and regulation while estimating its

future events such as income tax payment, valuation of inventories management, joint

venture transactions, commitment of company and identification of contingencies and other

details (Clinton, Pinello and Skaife, 2014). BP Billiton Company has relies on the data and

other details shown by its subsidiaries company while reporting its assets and liabilities in the

consolidation statement of company. In addition to this, company has implemented proper

level of international financial reporting standards while reporting its financial statement and

other required documents with the international reporting authorities (Nobes and Stadler,

2015). There will be following outcomes which would be observed in the BP Billiton

Company’s reporting frameworks.

International investors and stakeholders will make easy interpretation of financial

statement of company.

Consolidated financial statement of BP Billiton Company is prepared after following

AASB-5 and included all the estimates in its financial notes of accounts (Steman, 2016).

BP Billiton Company has adopted international financial reporting standards and

establish harmonization in its GAAP rules.

BP Billiton Company has implemented impairment test as per the IAS-136 provisions

and rules to report the value of its assets in its reporting framework’s.

It has set estimation for liabilities for wages and salary including non-monetary

transactions and explained that all the transaction should be set off within 12 months

from the reporting period.

Estimates used by BP Billiton Company

BP Billiton Company has implemented proper rules and regulation while estimating its

future events such as income tax payment, valuation of inventories management, joint

venture transactions, commitment of company and identification of contingencies and other

details (Clinton, Pinello and Skaife, 2014). BP Billiton Company has relies on the data and

other details shown by its subsidiaries company while reporting its assets and liabilities in the

consolidation statement of company. In addition to this, company has implemented proper

level of international financial reporting standards while reporting its financial statement and

other required documents with the international reporting authorities (Nobes and Stadler,

2015). There will be following outcomes which would be observed in the BP Billiton

Company’s reporting frameworks.

International investors and stakeholders will make easy interpretation of financial

statement of company.

Consolidated financial statement of BP Billiton Company is prepared after following

AASB-5 and included all the estimates in its financial notes of accounts (Steman, 2016).

BP Billiton Company has adopted international financial reporting standards and

establish harmonization in its GAAP rules.

BP Billiton Company has implemented impairment test as per the IAS-136 provisions

and rules to report the value of its assets in its reporting framework’s.

It has set estimation for liabilities for wages and salary including non-monetary

transactions and explained that all the transaction should be set off within 12 months

from the reporting period.

Accounting policies and estimates used by firm 6

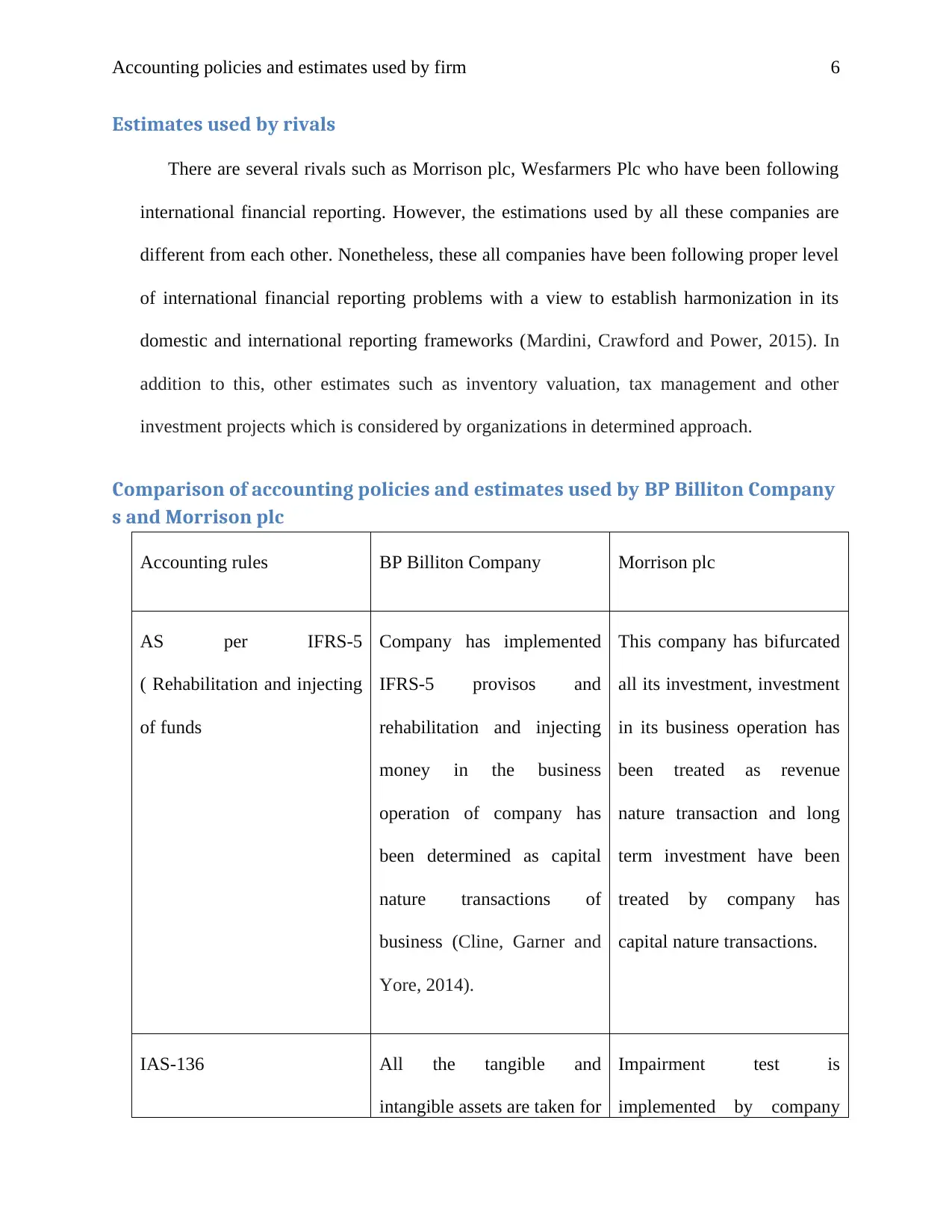

Estimates used by rivals

There are several rivals such as Morrison plc, Wesfarmers Plc who have been following

international financial reporting. However, the estimations used by all these companies are

different from each other. Nonetheless, these all companies have been following proper level

of international financial reporting problems with a view to establish harmonization in its

domestic and international reporting frameworks (Mardini, Crawford and Power, 2015). In

addition to this, other estimates such as inventory valuation, tax management and other

investment projects which is considered by organizations in determined approach.

Comparison of accounting policies and estimates used by BP Billiton Company

s and Morrison plc

Accounting rules BP Billiton Company Morrison plc

AS per IFRS-5

( Rehabilitation and injecting

of funds

Company has implemented

IFRS-5 provisos and

rehabilitation and injecting

money in the business

operation of company has

been determined as capital

nature transactions of

business (Cline, Garner and

Yore, 2014).

This company has bifurcated

all its investment, investment

in its business operation has

been treated as revenue

nature transaction and long

term investment have been

treated by company has

capital nature transactions.

IAS-136 All the tangible and

intangible assets are taken for

Impairment test is

implemented by company

Estimates used by rivals

There are several rivals such as Morrison plc, Wesfarmers Plc who have been following

international financial reporting. However, the estimations used by all these companies are

different from each other. Nonetheless, these all companies have been following proper level

of international financial reporting problems with a view to establish harmonization in its

domestic and international reporting frameworks (Mardini, Crawford and Power, 2015). In

addition to this, other estimates such as inventory valuation, tax management and other

investment projects which is considered by organizations in determined approach.

Comparison of accounting policies and estimates used by BP Billiton Company

s and Morrison plc

Accounting rules BP Billiton Company Morrison plc

AS per IFRS-5

( Rehabilitation and injecting

of funds

Company has implemented

IFRS-5 provisos and

rehabilitation and injecting

money in the business

operation of company has

been determined as capital

nature transactions of

business (Cline, Garner and

Yore, 2014).

This company has bifurcated

all its investment, investment

in its business operation has

been treated as revenue

nature transaction and long

term investment have been

treated by company has

capital nature transactions.

IAS-136 All the tangible and

intangible assets are taken for

Impairment test is

implemented by company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting policies and estimates used by firm 7

impairment test on annual

basis with view to showcase

the true and fair view of

assets. In addition to this,

goodwill and other cash

generating units will be used

for impairment test.

whenever needs arise for the

same.

ASSB- 5 It is evaluated that company

relies on the estimates and

values shared by subsidiaries

companies while reporting its

consolidated financial

statement.

All the financial statement

and consolidated financial

statement reporting is done

after following proper level

of IFRS rules and standard.

IFRS-23 (treatment of

income tax payment

Alt the tariff and traits paid

by company is charged from

the profit and loss. It is

observed that company has

charge all of its income tax

payment as revenue expenses

(Chen, Cumming, Hou, and

Lee, 2016).

Company has bifurcated all

of its income tax payment

and tariffs in two parts such

as revenue expenses and

capital expenditure. Current

tax payment will be charged

from the profit and loss

accounts and deferred tax

impairment test on annual

basis with view to showcase

the true and fair view of

assets. In addition to this,

goodwill and other cash

generating units will be used

for impairment test.

whenever needs arise for the

same.

ASSB- 5 It is evaluated that company

relies on the estimates and

values shared by subsidiaries

companies while reporting its

consolidated financial

statement.

All the financial statement

and consolidated financial

statement reporting is done

after following proper level

of IFRS rules and standard.

IFRS-23 (treatment of

income tax payment

Alt the tariff and traits paid

by company is charged from

the profit and loss. It is

observed that company has

charge all of its income tax

payment as revenue expenses

(Chen, Cumming, Hou, and

Lee, 2016).

Company has bifurcated all

of its income tax payment

and tariffs in two parts such

as revenue expenses and

capital expenditure. Current

tax payment will be charged

from the profit and loss

accounts and deferred tax

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting policies and estimates used by firm 8

payment will charged as

capital expenditure.

Assesse accounting flexibility

It is considered that accountants of BP Billiton Company has measured all of its assets at

estimated fair value (Christensen, et al. 2015). Interest payment and other provisions will be

deducted from the profit and loss accounts of company. However, changes in accounting

standard will also change the recording and classification of assets in determined approach. This

will not only strengthen the reporting of company but also keep all the financial statement

updated as per the newly introduced rules and regulation. In addition to this, it is also observed

that self- insured liabilities of the BP Billiton Company is based on the number of estimates and

management such as future inflation, return investment, application of accounting standard and

valuation of assets and liabilities (Ball, Li and Shivakumar, 2015).

Evaluation of accounting strategies and policies

There are several estimations which are adopted by the management debarment of BP

Billiton Company. These estimations used by company may result to distortion or damages

to the real value of organization. It is observed that if company does not use proper level of

estimation in its reporting frameworks then it may result to showing false views of assets and

liabilities of company. After evaluating the annual report of BP Billiton Company, it is

observed that management department with the collaboration of accountants have charged all

the hedge funds losses and other increased capital value from it profit and loss account which

payment will charged as

capital expenditure.

Assesse accounting flexibility

It is considered that accountants of BP Billiton Company has measured all of its assets at

estimated fair value (Christensen, et al. 2015). Interest payment and other provisions will be

deducted from the profit and loss accounts of company. However, changes in accounting

standard will also change the recording and classification of assets in determined approach. This

will not only strengthen the reporting of company but also keep all the financial statement

updated as per the newly introduced rules and regulation. In addition to this, it is also observed

that self- insured liabilities of the BP Billiton Company is based on the number of estimates and

management such as future inflation, return investment, application of accounting standard and

valuation of assets and liabilities (Ball, Li and Shivakumar, 2015).

Evaluation of accounting strategies and policies

There are several estimations which are adopted by the management debarment of BP

Billiton Company. These estimations used by company may result to distortion or damages

to the real value of organization. It is observed that if company does not use proper level of

estimation in its reporting frameworks then it may result to showing false views of assets and

liabilities of company. After evaluating the annual report of BP Billiton Company, it is

observed that management department with the collaboration of accountants have charged all

the hedge funds losses and other increased capital value from it profit and loss account which

Accounting policies and estimates used by firm 9

reduce the tax payment and profit of company as well. This level of accounting policies have

been adopted by organization to put cap on its overall cash flow. It is further observed that

inventory management and accounting policies adopted to manage the inventory may

provide proper reporting frameworks.

BP Billiton Company has followed both GAAP rules and standards and IFRS rules while

accounting and reporting of its financial data (Sytnik, 2014). For instance, plants and

machinery has been recorded in the books of account at their cost value after implementing

proper level of depreciation methods as per the IFRS rules and standard. Nonetheless, GAAP

rules provides that all the intangible assets should be recorded at the lowest of following

market value or cost value. This level of changes and amendment in the accounting standards

may result to destruction of reporting frameworks. Therefore, BP Billiton Company has

adopted both accounting GAAP and IFRS accounting standards while reporting it’s financial and

accounting information in its books of accounts. BP Billiton Company has been disclosing all of its

financial and non-financial information as per the AASB 101 (Brochet, Naranjo and Yu, 2016).

Changes in accounting estimates by the BP Billiton Company

There are several estimations which are adopted by the management debarment of BP

Billiton Company. These estimations and accounting implications used by company may

result to distortion or damages to the real value of organization. Company has changed its

estimation to hedge funds contracts and change in accounting estimates which will make

changes in its overall profit and loss of organization. In addition to this, estimation used by

company while deducting impairment loss may result to lower down the overall capital assets

of company and show casing true and faire views of its business assets (Bischof,

Brüggemann and Daske, 2014).

reduce the tax payment and profit of company as well. This level of accounting policies have

been adopted by organization to put cap on its overall cash flow. It is further observed that

inventory management and accounting policies adopted to manage the inventory may

provide proper reporting frameworks.

BP Billiton Company has followed both GAAP rules and standards and IFRS rules while

accounting and reporting of its financial data (Sytnik, 2014). For instance, plants and

machinery has been recorded in the books of account at their cost value after implementing

proper level of depreciation methods as per the IFRS rules and standard. Nonetheless, GAAP

rules provides that all the intangible assets should be recorded at the lowest of following

market value or cost value. This level of changes and amendment in the accounting standards

may result to destruction of reporting frameworks. Therefore, BP Billiton Company has

adopted both accounting GAAP and IFRS accounting standards while reporting it’s financial and

accounting information in its books of accounts. BP Billiton Company has been disclosing all of its

financial and non-financial information as per the AASB 101 (Brochet, Naranjo and Yu, 2016).

Changes in accounting estimates by the BP Billiton Company

There are several estimations which are adopted by the management debarment of BP

Billiton Company. These estimations and accounting implications used by company may

result to distortion or damages to the real value of organization. Company has changed its

estimation to hedge funds contracts and change in accounting estimates which will make

changes in its overall profit and loss of organization. In addition to this, estimation used by

company while deducting impairment loss may result to lower down the overall capital assets

of company and show casing true and faire views of its business assets (Bischof,

Brüggemann and Daske, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting policies and estimates used by firm 10

Suggestion for accounting policies and estimates prepared by BP Billiton

Company

There are several estimates and judgments used by BP Billiton Company such as

following FIFO method in management of inventories, deferred tax payment, impairment of

tangible and non-tangible assets (Barth, 2013). This has shown that payment of tax and

charging the same from profit and loss account of company is based on the estimation made

by company in its annual report. Moreover, it is observed that if company face problem in

complying with accounting and reporting frameworks after adopting GAAP rules and IFRS

rules and standard then IFRS rules and standard will override the compliance requirement of

organization. Nonetheless, all the estimates and provisional accounts created by BP Billiton

Company should be based on the actuaries’ method of calculation and the contingency plans

prepared (Aobdia, Lin and Petacchi, 2015). After evaluating the annual report of company,

and adjustment made in its annual report, it is observed that company had complied with all

the IFRS rules and estimations undertaken should be based on the reporting frameworks and

stakeholder’s requirement for company’s reporting. There are several red flags which could

be encountered by BP Billiton Company if it establish harmonization in its compliance and

reporting frameworks.

Red flag in accounting report of BP Billiton Company

There are several accounting issues and reporting problems which are faced by

organizations while complying with accounting and reporting frameworks. Red flags in

accounting report of BP Billiton Company could be defined as potential problems and threats

faced by BP Billiton Company in the accounting and reporting of financial statement. There

are several factors which could be identified by BP Billiton Company to evaluate the red flag

Suggestion for accounting policies and estimates prepared by BP Billiton

Company

There are several estimates and judgments used by BP Billiton Company such as

following FIFO method in management of inventories, deferred tax payment, impairment of

tangible and non-tangible assets (Barth, 2013). This has shown that payment of tax and

charging the same from profit and loss account of company is based on the estimation made

by company in its annual report. Moreover, it is observed that if company face problem in

complying with accounting and reporting frameworks after adopting GAAP rules and IFRS

rules and standard then IFRS rules and standard will override the compliance requirement of

organization. Nonetheless, all the estimates and provisional accounts created by BP Billiton

Company should be based on the actuaries’ method of calculation and the contingency plans

prepared (Aobdia, Lin and Petacchi, 2015). After evaluating the annual report of company,

and adjustment made in its annual report, it is observed that company had complied with all

the IFRS rules and estimations undertaken should be based on the reporting frameworks and

stakeholder’s requirement for company’s reporting. There are several red flags which could

be encountered by BP Billiton Company if it establish harmonization in its compliance and

reporting frameworks.

Red flag in accounting report of BP Billiton Company

There are several accounting issues and reporting problems which are faced by

organizations while complying with accounting and reporting frameworks. Red flags in

accounting report of BP Billiton Company could be defined as potential problems and threats

faced by BP Billiton Company in the accounting and reporting of financial statement. There

are several factors which could be identified by BP Billiton Company to evaluate the red flag

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting policies and estimates used by firm 11

in accounting report of BP Billiton Company (Atkins and Maroun, 2015). These red flags

arise when BP Billiton Company reports its financial statement to its reporting authorities. It is

observed that conflict or red flag arise when auditors of BP Billiton Company give remark on the

accounting policies followed by organization. If company has followed FIFO method and has

not disclosed proper level of information to its notes to accountant then it may destruct the

valuation methods in determined approach.

Monitor revenue and capital expenditure of company

The main problem or red flag in reporting frameworks of BP Billiton Company is related

to revenue and capital expenditure allocation in its profit and loss accounts. It is evaluated

that accountant of BP Billiton Company has charged all of its cost of capital from its profit

and loss accounts by considering revenue expenses. This level of treatment has reduced its

overall tax payment and reduced its overall profit. However, as per the IFRS rules and

standards, BP Billiton Company needs to make proper level of bifurcation in its all expenses.

Ideally expenses which provide benefits to company for more than one years should be treated as

capital expenditure. However, Income tax expenditure and deferred tax payment are the critical

terms and recording of these transactions is based on their nature. Deferred tax payment should be

treated as capital expenditure and annual income tax payment may be charged by BP Billiton

Company as revenue expenditure. This is one major Red Flag which BP Billiton Company

has been facing in its reporting frameworks.

Determination of depreciation amount to identify the true value of assets

It is considered that charging depreciation on the company’s assets is fully depends upon

the management’s discretion. BP Billiton Company has charged all of its assets through straight

in accounting report of BP Billiton Company (Atkins and Maroun, 2015). These red flags

arise when BP Billiton Company reports its financial statement to its reporting authorities. It is

observed that conflict or red flag arise when auditors of BP Billiton Company give remark on the

accounting policies followed by organization. If company has followed FIFO method and has

not disclosed proper level of information to its notes to accountant then it may destruct the

valuation methods in determined approach.

Monitor revenue and capital expenditure of company

The main problem or red flag in reporting frameworks of BP Billiton Company is related

to revenue and capital expenditure allocation in its profit and loss accounts. It is evaluated

that accountant of BP Billiton Company has charged all of its cost of capital from its profit

and loss accounts by considering revenue expenses. This level of treatment has reduced its

overall tax payment and reduced its overall profit. However, as per the IFRS rules and

standards, BP Billiton Company needs to make proper level of bifurcation in its all expenses.

Ideally expenses which provide benefits to company for more than one years should be treated as

capital expenditure. However, Income tax expenditure and deferred tax payment are the critical

terms and recording of these transactions is based on their nature. Deferred tax payment should be

treated as capital expenditure and annual income tax payment may be charged by BP Billiton

Company as revenue expenditure. This is one major Red Flag which BP Billiton Company

has been facing in its reporting frameworks.

Determination of depreciation amount to identify the true value of assets

It is considered that charging depreciation on the company’s assets is fully depends upon

the management’s discretion. BP Billiton Company has charged all of its assets through straight

Accounting policies and estimates used by firm 12

line method which may cause problem. It is observed that when company charges depreciation

through SLM method then it does not make full amount of depreciation from its assets. However,

depreciation amount charged is deducted from the profit and loss of company. In order to

showcase true and fair view of assets company needs to change its SML depreciation

charring method to written down value method. (Jaggi, et al. 2016).

Inventory valuation method

It is observe that as per the IAS-3 each and every listed company needs to follow FIFO

and LIFO method to manage its inventory in the business functioning. BP Billiton Company

has followed FIFO method to manage its inventory. It is considered that following FIFO method

will strengthen the inventory management of organization. BP Billiton Company use all the

inventories and management of business in FIFO and LIFO method to maintain inventories in its

reporting frameworks. With the help of LIFO method, BP Billiton Company has This FIFO

method has increase its overall turnover by 30% as compared to last five years. In addition to

this, this FIFO method will also change its overall profit and inventory which increase the

overall cost of productions to reduce the tax implication. Adoption of FIFO and LIFO

method depends upon the management discretion and inventory management techniques

followed by company.

Changes in net income, cash flow and related party transactions impact

As per the IAS24, BP Billiton Company should not enter into related party transactions to

which it has pecuniary and other materialistic relation. Nonetheless, transactions such as

offering remuneration, tax payment and other losses may be charged by company by passing

special resolution in the general meeting allowed payment to directors without passing

line method which may cause problem. It is observed that when company charges depreciation

through SLM method then it does not make full amount of depreciation from its assets. However,

depreciation amount charged is deducted from the profit and loss of company. In order to

showcase true and fair view of assets company needs to change its SML depreciation

charring method to written down value method. (Jaggi, et al. 2016).

Inventory valuation method

It is observe that as per the IAS-3 each and every listed company needs to follow FIFO

and LIFO method to manage its inventory in the business functioning. BP Billiton Company

has followed FIFO method to manage its inventory. It is considered that following FIFO method

will strengthen the inventory management of organization. BP Billiton Company use all the

inventories and management of business in FIFO and LIFO method to maintain inventories in its

reporting frameworks. With the help of LIFO method, BP Billiton Company has This FIFO

method has increase its overall turnover by 30% as compared to last five years. In addition to

this, this FIFO method will also change its overall profit and inventory which increase the

overall cost of productions to reduce the tax implication. Adoption of FIFO and LIFO

method depends upon the management discretion and inventory management techniques

followed by company.

Changes in net income, cash flow and related party transactions impact

As per the IAS24, BP Billiton Company should not enter into related party transactions to

which it has pecuniary and other materialistic relation. Nonetheless, transactions such as

offering remuneration, tax payment and other losses may be charged by company by passing

special resolution in the general meeting allowed payment to directors without passing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.