BA302 Accounting Theory: Comparing Accounting Policies of Telstra, TPG

VerifiedAdded on 2024/04/26

|13

|2082

|121

Report

AI Summary

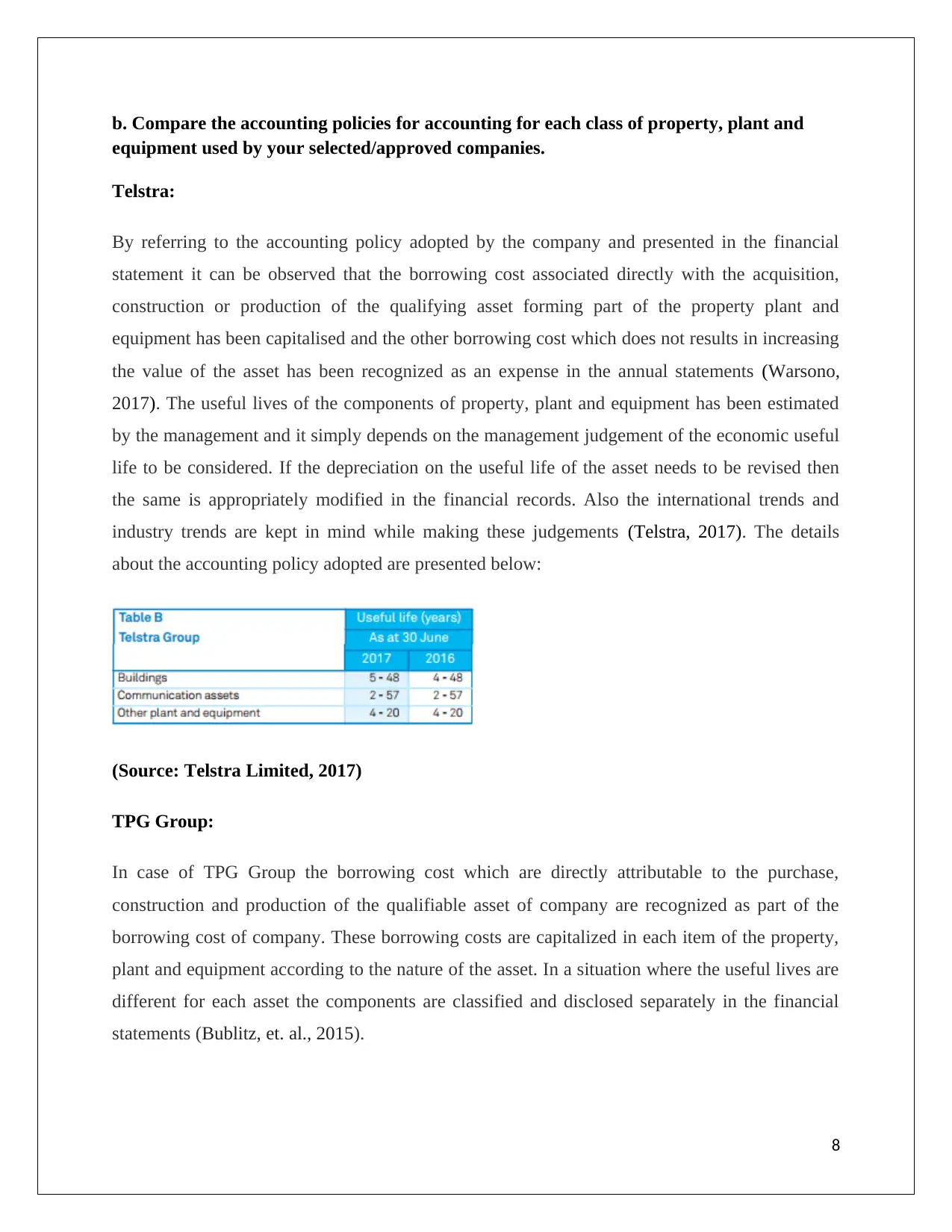

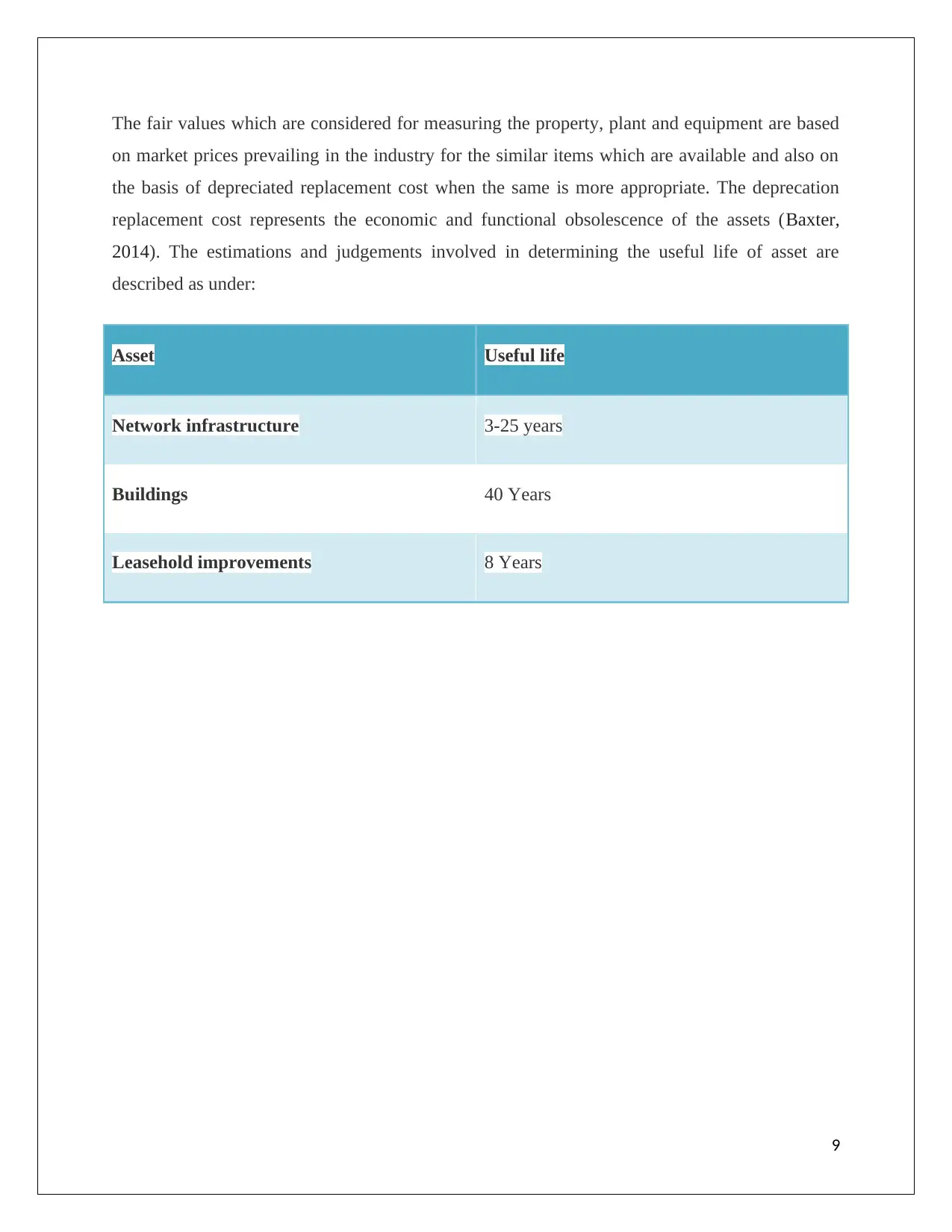

This report examines the accounting theory related to property, plant, and equipment (PPE), focusing on the accounting policies of Telstra and TPG Group, two companies in the Australian telecommunications sector. It describes the measurement and disclosure components of accounting policies for each class of PPE, comparing the policies used by Telstra and TPG. The report discusses whether all companies should be required to use identical accounting policies, highlighting the importance of harmonization in accounting standards for comparability and transparency in financial reporting. It concludes that while methods for measuring and recognizing assets may vary, identical accounting policies are desirable for enhancing the comparability and transparency of financial records, ultimately aiding investors and lenders in making informed economic decisions. Desklib offers a wealth of similar solved assignments and study resources for students.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.