Accounting Policies' Impact on TESCO PLC's Profit Disclosure

VerifiedAdded on 2020/10/22

|31

|7975

|283

Report

AI Summary

This report examines the impact of inappropriate accounting policies on the disclosure of profits and revenues at TESCO PLC. It begins with an introduction to corporate governance and the rationale for the research, focusing on the importance of accurate financial reporting for stakeholders. The report outlines the research aim, objectives, and questions, followed by a conceptual framework. A literature review explores the concept of accounting policies, the significance of profit and revenue disclosure, and the influence of inappropriate policies on TESCO PLC. The methodology includes both primary and secondary research, with results presented and discussed. The report concludes with recommendations and an action plan to help TESCO PLC overcome the negative impacts of inappropriate accounting policies, ensuring transparency and accurate financial representation to stakeholders. The analysis covers topics like going concern, consistency, accrual, prudence, and materiality, which are crucial for stakeholders' decision-making.

Corporate Strategy and

Governance

Governance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

TITLE:.............................................................................................................................................1

INTRODUCTION...........................................................................................................................1

Background of research..........................................................................................................1

Overview of organisation.......................................................................................................1

Rationale of research..............................................................................................................2

Research Aim.........................................................................................................................2

Research objectives................................................................................................................2

Research questions.................................................................................................................3

Conceptual framework...........................................................................................................3

LITERATURE REVIEW................................................................................................................5

The concept of accounting policies........................................................................................5

The importance of disclosure profit and revenue of association...........................................6

The influence of inappropriate accounting policies on revenues and profits of TESCO PLC7

The different ways through which TESCO PLC can easily overcome impact of inappropriate

accounting policies.................................................................................................................8

DISCUSSION OF PRIMARY AND SECONDARY RESEARCH................................................9

RESULTS OF SECONDARY AND PRIMARY RESEARCH....................................................13

Results of primary research..................................................................................................13

Results of Secondary research..............................................................................................21

RECOMMENDATIONS AND ACTION PLAN..........................................................................23

CONCLUSION..............................................................................................................................27

REFERENCES..............................................................................................................................28

TITLE:.............................................................................................................................................1

INTRODUCTION...........................................................................................................................1

Background of research..........................................................................................................1

Overview of organisation.......................................................................................................1

Rationale of research..............................................................................................................2

Research Aim.........................................................................................................................2

Research objectives................................................................................................................2

Research questions.................................................................................................................3

Conceptual framework...........................................................................................................3

LITERATURE REVIEW................................................................................................................5

The concept of accounting policies........................................................................................5

The importance of disclosure profit and revenue of association...........................................6

The influence of inappropriate accounting policies on revenues and profits of TESCO PLC7

The different ways through which TESCO PLC can easily overcome impact of inappropriate

accounting policies.................................................................................................................8

DISCUSSION OF PRIMARY AND SECONDARY RESEARCH................................................9

RESULTS OF SECONDARY AND PRIMARY RESEARCH....................................................13

Results of primary research..................................................................................................13

Results of Secondary research..............................................................................................21

RECOMMENDATIONS AND ACTION PLAN..........................................................................23

CONCLUSION..............................................................................................................................27

REFERENCES..............................................................................................................................28

TITLE:

“To identify the impact of inappropriate accounting policies on disclosure of profits

and revenues of association.” A case on TESCO.

INTRODUCTION

Background of research

Corporate governance refers to the process, mechanism, relations under which

organisation can be controlled, managed. This is the framework through which management

within an organisation can perform business activities in effective and reliable manner. Under

corporate governance, there are some strategies through which transparency, fairness,

accountability, etc. are the maintained (Albu, Lupu and Sandu, 2014). This helps to provide

complete and relevant information to stakeholders. Corporate governance framework has

following aspects-

Explicit and implicit contracts between organisation and stakeholders in order to

distribute roles, responsibilities and powers.

Reconciliation in case of conflict of interest of stakeholders in compilation to their duties,

roles, etc.

Procedure for supervision, manage flow of information, control, etc. within organisation.

With maintaining business operations according to these framework, it is easy to

maintain long term relations with stakeholders because true and fair representation of operations

and accounts provides satisfaction.

This research is based on TESCO is the organisation which is one of the leading

organisation in British this organisation has head quarter in Welwyn Garden City, Hertfordshire,

England, United Kingdom. In terms of revenue, this is the third largest organisation in world.

TESCO PLC deals in grocery, clothing, mobile, banking sector, etc.

Overview of organisation

TESCO PLC is the largest British retail store in UK. This organisation serves in different

parts of world such as Hungary, India, China, Europe, etc. These days there are some rules and

regulations which has to be followed by organisation. This helps to maintain safe and secure

environment and maintain loyalty with stakeholders (Aoyagi and Ganelli, 2014). Stakeholders

are the individuals or group of individuals or organisation who are concern about organisation's

1

“To identify the impact of inappropriate accounting policies on disclosure of profits

and revenues of association.” A case on TESCO.

INTRODUCTION

Background of research

Corporate governance refers to the process, mechanism, relations under which

organisation can be controlled, managed. This is the framework through which management

within an organisation can perform business activities in effective and reliable manner. Under

corporate governance, there are some strategies through which transparency, fairness,

accountability, etc. are the maintained (Albu, Lupu and Sandu, 2014). This helps to provide

complete and relevant information to stakeholders. Corporate governance framework has

following aspects-

Explicit and implicit contracts between organisation and stakeholders in order to

distribute roles, responsibilities and powers.

Reconciliation in case of conflict of interest of stakeholders in compilation to their duties,

roles, etc.

Procedure for supervision, manage flow of information, control, etc. within organisation.

With maintaining business operations according to these framework, it is easy to

maintain long term relations with stakeholders because true and fair representation of operations

and accounts provides satisfaction.

This research is based on TESCO is the organisation which is one of the leading

organisation in British this organisation has head quarter in Welwyn Garden City, Hertfordshire,

England, United Kingdom. In terms of revenue, this is the third largest organisation in world.

TESCO PLC deals in grocery, clothing, mobile, banking sector, etc.

Overview of organisation

TESCO PLC is the largest British retail store in UK. This organisation serves in different

parts of world such as Hungary, India, China, Europe, etc. These days there are some rules and

regulations which has to be followed by organisation. This helps to maintain safe and secure

environment and maintain loyalty with stakeholders (Aoyagi and Ganelli, 2014). Stakeholders

are the individuals or group of individuals or organisation who are concern about organisation's

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

actions and activities. It is important and relevant to analyse consumer demand which helps to

make long term relations with workers. These days, there is requirement of performing business

operations in authentic form. There are many stakeholders of TESCO PLC such as consumers,

suppliers, debtors, bank, competitors, employees, shareholders, etc. Hence it is important to

communicate them plans and policies of organisation. In this research, there is discussion about

accounting policies of TESCO PLC and its impact on disclosure of profits.

Rationale of research

In this research, there is discussion about corporate governance policies. Corporate

governance policies sets some framework which are relevant in current market because it

provides complete information about working style of organisation, change in plans and policies,

etc. Reason behind conducting this research is to analyse impact on inappropriate accounting

policies on disclosure of profits. There are issues in disclosing half yearly profits of TESCO PLC

which affects ran image of TESCO PLC. Stakeholders wants to analyse actual performance of

TESCO PLC because they have interest in operations of organisation. Hence with the help of this

research, it is easy to understand reason of inappropriate counting policies and its impact on

disclosing of profits (ArAs and et. al., 2016).

With the help of this research, it is easy to provide ways through which correct measures

can be provided to TESCO PLC. This also helps reader to provide knowledge about importance

of accounting policies in decision making of stakeholders. With the help of this research, it is

easy to recommend changes which has to be made by manager while changing their accounting

policies.

Research Aim

“To identify the impact of inappropriate accounting policies on disclosure of profits

and revenues of association.” A case on TESCO.

Research objectives

To understand the concept of accounting policies.

To evaluate the importance of disclosure profit and revenue of association.

To analyse the influence of inappropriate accounting policies on revenues and profits of

TESCO.

2

make long term relations with workers. These days, there is requirement of performing business

operations in authentic form. There are many stakeholders of TESCO PLC such as consumers,

suppliers, debtors, bank, competitors, employees, shareholders, etc. Hence it is important to

communicate them plans and policies of organisation. In this research, there is discussion about

accounting policies of TESCO PLC and its impact on disclosure of profits.

Rationale of research

In this research, there is discussion about corporate governance policies. Corporate

governance policies sets some framework which are relevant in current market because it

provides complete information about working style of organisation, change in plans and policies,

etc. Reason behind conducting this research is to analyse impact on inappropriate accounting

policies on disclosure of profits. There are issues in disclosing half yearly profits of TESCO PLC

which affects ran image of TESCO PLC. Stakeholders wants to analyse actual performance of

TESCO PLC because they have interest in operations of organisation. Hence with the help of this

research, it is easy to understand reason of inappropriate counting policies and its impact on

disclosing of profits (ArAs and et. al., 2016).

With the help of this research, it is easy to provide ways through which correct measures

can be provided to TESCO PLC. This also helps reader to provide knowledge about importance

of accounting policies in decision making of stakeholders. With the help of this research, it is

easy to recommend changes which has to be made by manager while changing their accounting

policies.

Research Aim

“To identify the impact of inappropriate accounting policies on disclosure of profits

and revenues of association.” A case on TESCO.

Research objectives

To understand the concept of accounting policies.

To evaluate the importance of disclosure profit and revenue of association.

To analyse the influence of inappropriate accounting policies on revenues and profits of

TESCO.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To recommend the different ways through which TESCO can easily overcome impact of

inappropriate accounting policies.

Research questions

Do you understand the concept of accounting policies?

What is the importance of disclosure profit and revenue of association?

What is the influence of inappropriate accounting policies on revenues and profits of

TESCO?

What are the different ways through which TESCO can easily overcome impact of

inappropriate accounting policies?

Conceptual framework

Conceptual framework is the way through which all the activities which are conducted

while conducting research is analysed. With the help of this framework, it is easy to understand

description which is taking place in various research activities. Research is process through

which in- depth analysis can be done on some specific topic. Hence research is conducted under

different chapters. Under conceptual framework it is easy to understand aspects which are

covered under various chapters of research.

Introduction is prime chapter which covers overview of research, background of

company, research aims and objectives, etc. With this section, it is easy to understand

about topic of research topic and organisation. Hence it is easy to make blue print related

to research in mind of reader with this section.

Second section is about literature review (Bain and Band, 2016). This is the concept

which talks about objectives discussed in introduction. In literature review, opinion is

authentic as per view of some specific author. This makes complete research authentic

and reliable.

Section third is about discussion about primary and secondary. This is the concept which

helps to collect information from respondents to give complete and relevant information.

Research is conducted with different activities such as introduction, literature review,

data collect and analysis, etc. which jointly known as research methodology.

Section four is about discussing results. With collecting data with the help of primary

and secondary method, then outcomes are discussed in this section. In this section,

3

inappropriate accounting policies.

Research questions

Do you understand the concept of accounting policies?

What is the importance of disclosure profit and revenue of association?

What is the influence of inappropriate accounting policies on revenues and profits of

TESCO?

What are the different ways through which TESCO can easily overcome impact of

inappropriate accounting policies?

Conceptual framework

Conceptual framework is the way through which all the activities which are conducted

while conducting research is analysed. With the help of this framework, it is easy to understand

description which is taking place in various research activities. Research is process through

which in- depth analysis can be done on some specific topic. Hence research is conducted under

different chapters. Under conceptual framework it is easy to understand aspects which are

covered under various chapters of research.

Introduction is prime chapter which covers overview of research, background of

company, research aims and objectives, etc. With this section, it is easy to understand

about topic of research topic and organisation. Hence it is easy to make blue print related

to research in mind of reader with this section.

Second section is about literature review (Bain and Band, 2016). This is the concept

which talks about objectives discussed in introduction. In literature review, opinion is

authentic as per view of some specific author. This makes complete research authentic

and reliable.

Section third is about discussion about primary and secondary. This is the concept which

helps to collect information from respondents to give complete and relevant information.

Research is conducted with different activities such as introduction, literature review,

data collect and analysis, etc. which jointly known as research methodology.

Section four is about discussing results. With collecting data with the help of primary

and secondary method, then outcomes are discussed in this section. In this section,

3

interpretation on the basis of primary data is discussed and gist is discussed of secondary

data collected discussed under literature review.

Last section is about recommendations and action plan. After discussing research

outcomes, there are recommendations through which issues faced by organisation can be

overcome. Action plan is the way through which actions can be taken by managers of

organisation to overcome issues (Bell, 2014).

4

data collected discussed under literature review.

Last section is about recommendations and action plan. After discussing research

outcomes, there are recommendations through which issues faced by organisation can be

overcome. Action plan is the way through which actions can be taken by managers of

organisation to overcome issues (Bell, 2014).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LITERATURE REVIEW

Literature review is the section in which objectives of research are discussed with some

authentic source. This is part of secondary data because information is collected from books,

online sources, journals, etc. In this research, there is discussion about impact of inappropriate

accounting policies on disclosing profits and revenue. Hence in this literature review, there is

discussion about author's view over the research objectives.

The concept of accounting policies

Accounting policies refers to the specific principles and methods which are implemented

while managing financial statement of organisation. These are the measurement system,

procedures for preparing books and accounts of TESCO PLC. According to Breitbarth and et. al.,

2015 accounting policies is different from accounting principles. Accounting principles are legal

laws and revelations which has to be considered while framing accounts for specific

organisation. TESCO PLC are legally bind towards these principles. For instance: depreciation

method, recognition of goodwill, research and development cost, valuation of stock, etc. are

accounting policies. While accounting principles are going concern principle, matching concept,

revenue recognition, etc. For instance: there is specific method through which stock within

organisation can be valued. There are different methods for valuation of stock such as LIFO,

FIFO, Weighted average, etc. There is specific method which is used by TESCO PLC for

showing their balance of stock. In order to make consistency in books of accounts and provide

complete and relevant information to stakeholders, specific method is used to year after year.

There is difference in accounting policies as per difference in organisation. But there are

some assumptions which has to be followed by managers of TESCO PLC which helps to get

appropriate and relevant outcome. In order to understand fundamental accounting policies, these

assumption are considered-

Going concern. As per this assumption, it is assumed that business will operate for longer

period of time in industry. Hence there is no assumptions related to closing down of

business after specific period of time.

Consistency. As per this assumption, it is assumed that accounting policies which are

used by managers of TESCO PLC is consistent in next year as well. This helps to

disclose profits and revenue appropriate and significant.

5

Literature review is the section in which objectives of research are discussed with some

authentic source. This is part of secondary data because information is collected from books,

online sources, journals, etc. In this research, there is discussion about impact of inappropriate

accounting policies on disclosing profits and revenue. Hence in this literature review, there is

discussion about author's view over the research objectives.

The concept of accounting policies

Accounting policies refers to the specific principles and methods which are implemented

while managing financial statement of organisation. These are the measurement system,

procedures for preparing books and accounts of TESCO PLC. According to Breitbarth and et. al.,

2015 accounting policies is different from accounting principles. Accounting principles are legal

laws and revelations which has to be considered while framing accounts for specific

organisation. TESCO PLC are legally bind towards these principles. For instance: depreciation

method, recognition of goodwill, research and development cost, valuation of stock, etc. are

accounting policies. While accounting principles are going concern principle, matching concept,

revenue recognition, etc. For instance: there is specific method through which stock within

organisation can be valued. There are different methods for valuation of stock such as LIFO,

FIFO, Weighted average, etc. There is specific method which is used by TESCO PLC for

showing their balance of stock. In order to make consistency in books of accounts and provide

complete and relevant information to stakeholders, specific method is used to year after year.

There is difference in accounting policies as per difference in organisation. But there are

some assumptions which has to be followed by managers of TESCO PLC which helps to get

appropriate and relevant outcome. In order to understand fundamental accounting policies, these

assumption are considered-

Going concern. As per this assumption, it is assumed that business will operate for longer

period of time in industry. Hence there is no assumptions related to closing down of

business after specific period of time.

Consistency. As per this assumption, it is assumed that accounting policies which are

used by managers of TESCO PLC is consistent in next year as well. This helps to

disclose profits and revenue appropriate and significant.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accural. Third assumption is that income or cost which are incurred whether received or

not, it must be recorded in period to which they are related. This helps to get actual

knowledge about expenses and incomes.

Hence accounting policies are different as per company. There is no specific policies with

which organisations are bind. There are some considerations which has to be followed by

TESCO PLC while farming financial statement. These are discussed as under-

Prudence. In organisation, future is uncertain, hence there are many activities which are

estimated for future. As per this accounting concept, in case of losses and expenses when

they are estimates are recorded (even if hey are not paid). While in case of profits and

revenues, it must be recorded only when it is received. Hence it is clear that in accounting

policies, risk is secured when it is identified, while in case of profits they are recorded on

received basis.

Substance over form. As per this principle, it is important to record financial data as per

governed principles (Chen and et. al., 2015).

Materiality. As per this principle, it is identified that only material things has to be

considered by managers of TESCO PLC. These are the factors which affects decisions of

stakeholders.

The importance of disclosure profit and revenue of association

There are many parties which deals with TESCO PLC in direct or indirect manner such

as consumers, suppliers, management, employees, etc. These are the people who have interest in

organisation's operations hence organisation has to disclose their books of accounts in

appropriate manner. It is important for TESCO PLC to disclose their profits and revenues

because stakeholders analyse performance and financial condition of company in appropriate and

relevant manner. There are many people whoo wants to analyse financial performance of

TESCO PLC due to different reasons. For instance: for shareholders books of accounts provides

complete and relevant information whether to invest or withdrawal. Hence books of accounts

plays crucial role in affecting decision making of individuals.

Financial position such as revenue, debt equity ration, pay back period, etc. are important

for suppliers as they give credit to TESCO PLC. Hence financial books of accounts are important

for analysing whether to give debt or not. According to Ciampi, 2015 in order to provide

complete and relevant information to stakeholders disclosure of profits and revenues is

6

not, it must be recorded in period to which they are related. This helps to get actual

knowledge about expenses and incomes.

Hence accounting policies are different as per company. There is no specific policies with

which organisations are bind. There are some considerations which has to be followed by

TESCO PLC while farming financial statement. These are discussed as under-

Prudence. In organisation, future is uncertain, hence there are many activities which are

estimated for future. As per this accounting concept, in case of losses and expenses when

they are estimates are recorded (even if hey are not paid). While in case of profits and

revenues, it must be recorded only when it is received. Hence it is clear that in accounting

policies, risk is secured when it is identified, while in case of profits they are recorded on

received basis.

Substance over form. As per this principle, it is important to record financial data as per

governed principles (Chen and et. al., 2015).

Materiality. As per this principle, it is identified that only material things has to be

considered by managers of TESCO PLC. These are the factors which affects decisions of

stakeholders.

The importance of disclosure profit and revenue of association

There are many parties which deals with TESCO PLC in direct or indirect manner such

as consumers, suppliers, management, employees, etc. These are the people who have interest in

organisation's operations hence organisation has to disclose their books of accounts in

appropriate manner. It is important for TESCO PLC to disclose their profits and revenues

because stakeholders analyse performance and financial condition of company in appropriate and

relevant manner. There are many people whoo wants to analyse financial performance of

TESCO PLC due to different reasons. For instance: for shareholders books of accounts provides

complete and relevant information whether to invest or withdrawal. Hence books of accounts

plays crucial role in affecting decision making of individuals.

Financial position such as revenue, debt equity ration, pay back period, etc. are important

for suppliers as they give credit to TESCO PLC. Hence financial books of accounts are important

for analysing whether to give debt or not. According to Ciampi, 2015 in order to provide

complete and relevant information to stakeholders disclosure of profits and revenues is

6

important. Employees must be aware about gains and profits because personal objectives of

employees can be achieved with progress of TESCO PLC. So in case of good profits, there must

be sharing to employees. This helps to maintain long term relations with workers and they give

their best. Accounting policies are used, so books of accounts give correct and authentic

information to external and internal parties of TESCO PLC.

As per case of TESCO PLC, there is inappropriate accounting policies. Hence in this

case, this gives wrong information to stakeholders because revenues and profits are not disclosed

correctly. There is issue in profits of half year after composition of composition of board of

directors and inappropriate accounting policies. With the help of constant accounting policies, it

is easy to give complete and relevant information to stakeholders. With providing complete

information regarding financial process of company, it is easy to get donations, sponsorship, etc.

because with sponsors wants to invest with big brands having good financial position for the

purpose of marketing.

The influence of inappropriate accounting policies on revenues and profits of TESCO PLC

There is direct impact of accounting policies on profits and revenues of company. When

accounts department of TESCO PLC is changing accounting policies frequently, then there is

effect on profits and revenues. Due to change in policies, there are possibilities that profits can be

under value or overvalued. Books of accounts does not give true and fair information. For

instance: manager of TESCO PLC is using FIFO method for valuation of stock. But in

subsequent year, they are using LIFO. As per FIFO method, while realising stock, old stock is

sold out first. While in case of LIFO, stock with collected later is realised first. According to

Clarke, 2015 there is difference in cost of stock, hence this affects overall profits and revenues of

both the year. Due to this difference, it is tough for stakeholders to analyse actual outcome for

analysis.

With change in accounting policies, actual position may gets misguide. In case of

TESCO PLC, they are using inappropriate accounting policies which affects results shown by

books of accounts. This issue arise because of change in board of directors. As per change in

accounting policies, financial position of TESCO PLC mislead which affects decisions of

stakeholders. There is issue in books of accounts but inappropriate accounting policies are

accepted by audit committee and profits are signed by board of directors. When books of

accounts does not have appropriate accounting policies of change in accounting technique, then

7

employees can be achieved with progress of TESCO PLC. So in case of good profits, there must

be sharing to employees. This helps to maintain long term relations with workers and they give

their best. Accounting policies are used, so books of accounts give correct and authentic

information to external and internal parties of TESCO PLC.

As per case of TESCO PLC, there is inappropriate accounting policies. Hence in this

case, this gives wrong information to stakeholders because revenues and profits are not disclosed

correctly. There is issue in profits of half year after composition of composition of board of

directors and inappropriate accounting policies. With the help of constant accounting policies, it

is easy to give complete and relevant information to stakeholders. With providing complete

information regarding financial process of company, it is easy to get donations, sponsorship, etc.

because with sponsors wants to invest with big brands having good financial position for the

purpose of marketing.

The influence of inappropriate accounting policies on revenues and profits of TESCO PLC

There is direct impact of accounting policies on profits and revenues of company. When

accounts department of TESCO PLC is changing accounting policies frequently, then there is

effect on profits and revenues. Due to change in policies, there are possibilities that profits can be

under value or overvalued. Books of accounts does not give true and fair information. For

instance: manager of TESCO PLC is using FIFO method for valuation of stock. But in

subsequent year, they are using LIFO. As per FIFO method, while realising stock, old stock is

sold out first. While in case of LIFO, stock with collected later is realised first. According to

Clarke, 2015 there is difference in cost of stock, hence this affects overall profits and revenues of

both the year. Due to this difference, it is tough for stakeholders to analyse actual outcome for

analysis.

With change in accounting policies, actual position may gets misguide. In case of

TESCO PLC, they are using inappropriate accounting policies which affects results shown by

books of accounts. This issue arise because of change in board of directors. As per change in

accounting policies, financial position of TESCO PLC mislead which affects decisions of

stakeholders. There is issue in books of accounts but inappropriate accounting policies are

accepted by audit committee and profits are signed by board of directors. When books of

accounts does not have appropriate accounting policies of change in accounting technique, then

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

it is responsibility of managers of TESCO PLC to disclose reason of changing accounting policy.

It is important to communicate with stakeholders regarding impact of change in accounting

policies. Hence with considering inappropriate accounting policies, profits and revenues gets

may be over or under valued.

The different ways through which TESCO PLC can easily overcome impact of inappropriate

accounting policies

In case of TESCO PLC, there is negative impact on brand image because books of

accounts does not give true and fair information. There is requirement of some changes in

disclosing accounting policies. There must be working notes which gives information to

stakeholders regarding impact of inappropriate accounting techniques. There are some basic

norms of accounting which has to be followed in order to make balance in asset, liability,

expenses and revenues. There must be complete information in books of accounts elated to any

assumption.

According to Coffee and Palia, 2015 there must be hiring of expertise personnel in

accounts department of TESCO PLC. There must be time to time audit which shows the

relevance of books of accounts. Board of Directors must frame policies which are free from

biasness. In case of any suspect, in- depth analysis of books of accounts must be done. In order

to overcome issues related to inappropriate accounting policies, difference in actual results and

outcome must be shown in working working with their impact.

8

It is important to communicate with stakeholders regarding impact of change in accounting

policies. Hence with considering inappropriate accounting policies, profits and revenues gets

may be over or under valued.

The different ways through which TESCO PLC can easily overcome impact of inappropriate

accounting policies

In case of TESCO PLC, there is negative impact on brand image because books of

accounts does not give true and fair information. There is requirement of some changes in

disclosing accounting policies. There must be working notes which gives information to

stakeholders regarding impact of inappropriate accounting techniques. There are some basic

norms of accounting which has to be followed in order to make balance in asset, liability,

expenses and revenues. There must be complete information in books of accounts elated to any

assumption.

According to Coffee and Palia, 2015 there must be hiring of expertise personnel in

accounts department of TESCO PLC. There must be time to time audit which shows the

relevance of books of accounts. Board of Directors must frame policies which are free from

biasness. In case of any suspect, in- depth analysis of books of accounts must be done. In order

to overcome issues related to inappropriate accounting policies, difference in actual results and

outcome must be shown in working working with their impact.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DISCUSSION OF PRIMARY AND SECONDARY RESEARCH

Research is the way through which investigation is done by individual on some specific

research topic. There are different techniques which has to be considered in order to get

appropriate outcome as recommendations and conclusions. These aspects are covered in research

methodology. Research methodology is the framework which covers different aspects of

research such as philosophy, approach, time, cost, method, sources, etc. There are two sources of

collecting data i.e. primary and secondary method. These methods are discussed as under-

PRIMARY RESEARCH

Primary research refers to the method in which individual collect data on their own

through different sources such as personal interview, questionnaire, etc. In this method, there is

personal interaction among researcher and respondents in case of personal interview. Hence in

this method, actual data is collected which is effective for giving recommendations and

conclusions. Data collection with the help of primary research is new and specific according to

research topic. Under this method, it is easy to get answer of issues, questions related to research

topic. While collecting data related to inappropriate accounting policies, it is easy to analyse

reactions of respondents over this issue (Cook and Glass, 2015). There are different methods

which are collecting primary data from respondents which is discussed as under-

Interview- Interview is the process in which some questions are asked with respondents

related to research topic. In this method, focus of researcher is on list of questions and this is

usually with some specific individuals. Interview can be conducted through face to face or

telephone media. In interview researcher has to record opinion to give some specific view. It is

ability of researcher to engage respondents to give clear and appropriate results.

Focus Group- Focus group refers to the method in which number of individuals are

observed when they re discussing about research topic. This helps to get knowledge about view

of majority of people on specific topic. Moderator analyse views of individuals and motivate

everyone to take part in discussion. Sometimes, there are possibilities that views are irrelevant

which affects decision of researcher (Crowther and Seifi, 2018).

Questionnaire- Questionnaire is also form of primary source which helps to collect

information about research topic. There are some set of questions framed by researcher related to

research issue. It is important for researcher to collect questionnaire from respondents. This is the

best method to collect primary sources from respondents because this method helps to get

9

Research is the way through which investigation is done by individual on some specific

research topic. There are different techniques which has to be considered in order to get

appropriate outcome as recommendations and conclusions. These aspects are covered in research

methodology. Research methodology is the framework which covers different aspects of

research such as philosophy, approach, time, cost, method, sources, etc. There are two sources of

collecting data i.e. primary and secondary method. These methods are discussed as under-

PRIMARY RESEARCH

Primary research refers to the method in which individual collect data on their own

through different sources such as personal interview, questionnaire, etc. In this method, there is

personal interaction among researcher and respondents in case of personal interview. Hence in

this method, actual data is collected which is effective for giving recommendations and

conclusions. Data collection with the help of primary research is new and specific according to

research topic. Under this method, it is easy to get answer of issues, questions related to research

topic. While collecting data related to inappropriate accounting policies, it is easy to analyse

reactions of respondents over this issue (Cook and Glass, 2015). There are different methods

which are collecting primary data from respondents which is discussed as under-

Interview- Interview is the process in which some questions are asked with respondents

related to research topic. In this method, focus of researcher is on list of questions and this is

usually with some specific individuals. Interview can be conducted through face to face or

telephone media. In interview researcher has to record opinion to give some specific view. It is

ability of researcher to engage respondents to give clear and appropriate results.

Focus Group- Focus group refers to the method in which number of individuals are

observed when they re discussing about research topic. This helps to get knowledge about view

of majority of people on specific topic. Moderator analyse views of individuals and motivate

everyone to take part in discussion. Sometimes, there are possibilities that views are irrelevant

which affects decision of researcher (Crowther and Seifi, 2018).

Questionnaire- Questionnaire is also form of primary source which helps to collect

information about research topic. There are some set of questions framed by researcher related to

research issue. It is important for researcher to collect questionnaire from respondents. This is the

best method to collect primary sources from respondents because this method helps to get

9

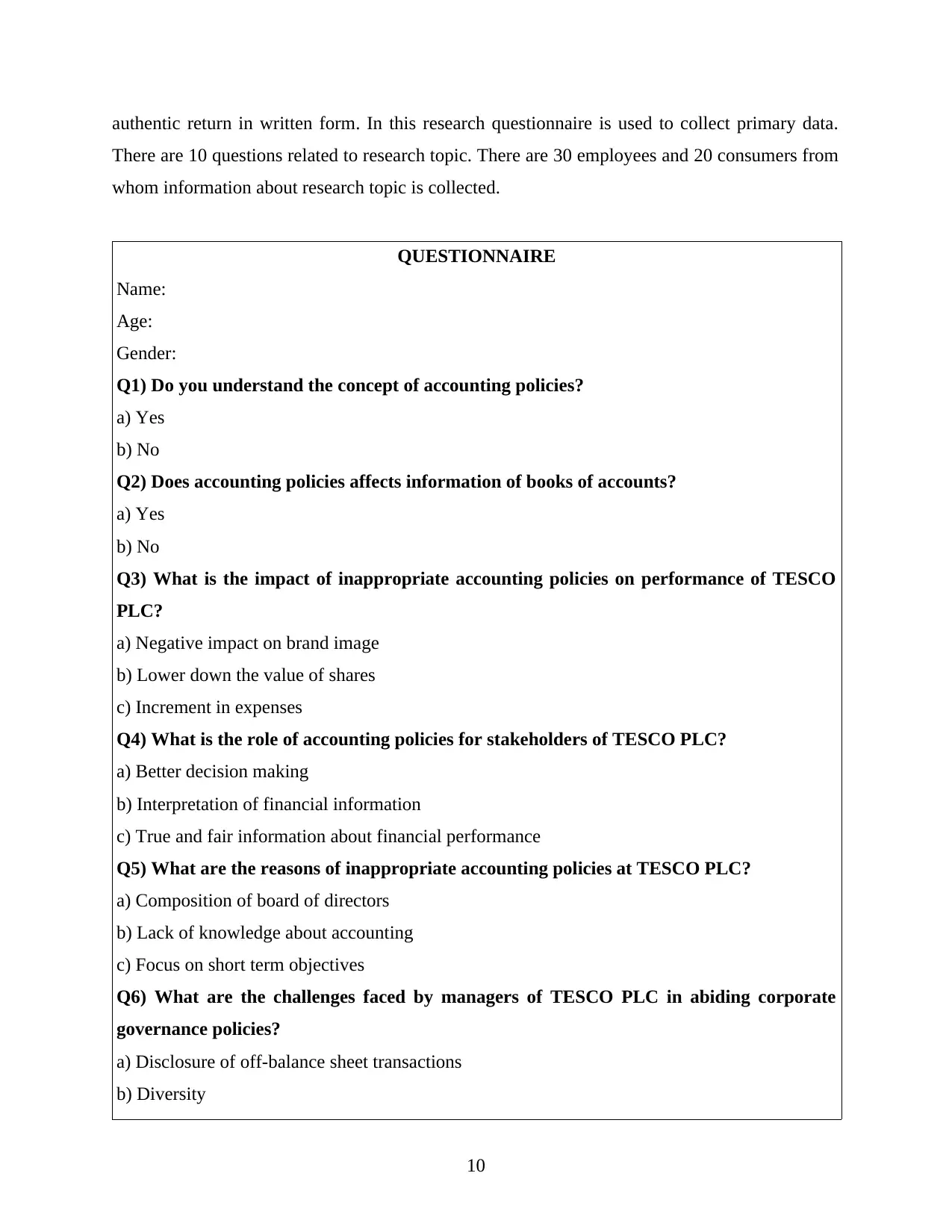

authentic return in written form. In this research questionnaire is used to collect primary data.

There are 10 questions related to research topic. There are 30 employees and 20 consumers from

whom information about research topic is collected.

QUESTIONNAIRE

Name:

Age:

Gender:

Q1) Do you understand the concept of accounting policies?

a) Yes

b) No

Q2) Does accounting policies affects information of books of accounts?

a) Yes

b) No

Q3) What is the impact of inappropriate accounting policies on performance of TESCO

PLC?

a) Negative impact on brand image

b) Lower down the value of shares

c) Increment in expenses

Q4) What is the role of accounting policies for stakeholders of TESCO PLC?

a) Better decision making

b) Interpretation of financial information

c) True and fair information about financial performance

Q5) What are the reasons of inappropriate accounting policies at TESCO PLC?

a) Composition of board of directors

b) Lack of knowledge about accounting

c) Focus on short term objectives

Q6) What are the challenges faced by managers of TESCO PLC in abiding corporate

governance policies?

a) Disclosure of off-balance sheet transactions

b) Diversity

10

There are 10 questions related to research topic. There are 30 employees and 20 consumers from

whom information about research topic is collected.

QUESTIONNAIRE

Name:

Age:

Gender:

Q1) Do you understand the concept of accounting policies?

a) Yes

b) No

Q2) Does accounting policies affects information of books of accounts?

a) Yes

b) No

Q3) What is the impact of inappropriate accounting policies on performance of TESCO

PLC?

a) Negative impact on brand image

b) Lower down the value of shares

c) Increment in expenses

Q4) What is the role of accounting policies for stakeholders of TESCO PLC?

a) Better decision making

b) Interpretation of financial information

c) True and fair information about financial performance

Q5) What are the reasons of inappropriate accounting policies at TESCO PLC?

a) Composition of board of directors

b) Lack of knowledge about accounting

c) Focus on short term objectives

Q6) What are the challenges faced by managers of TESCO PLC in abiding corporate

governance policies?

a) Disclosure of off-balance sheet transactions

b) Diversity

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 31

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.