Accounting Policy Changes, Warranty, Intangible Assets Solutions

VerifiedAdded on 2023/06/05

|7

|1568

|241

Homework Assignment

AI Summary

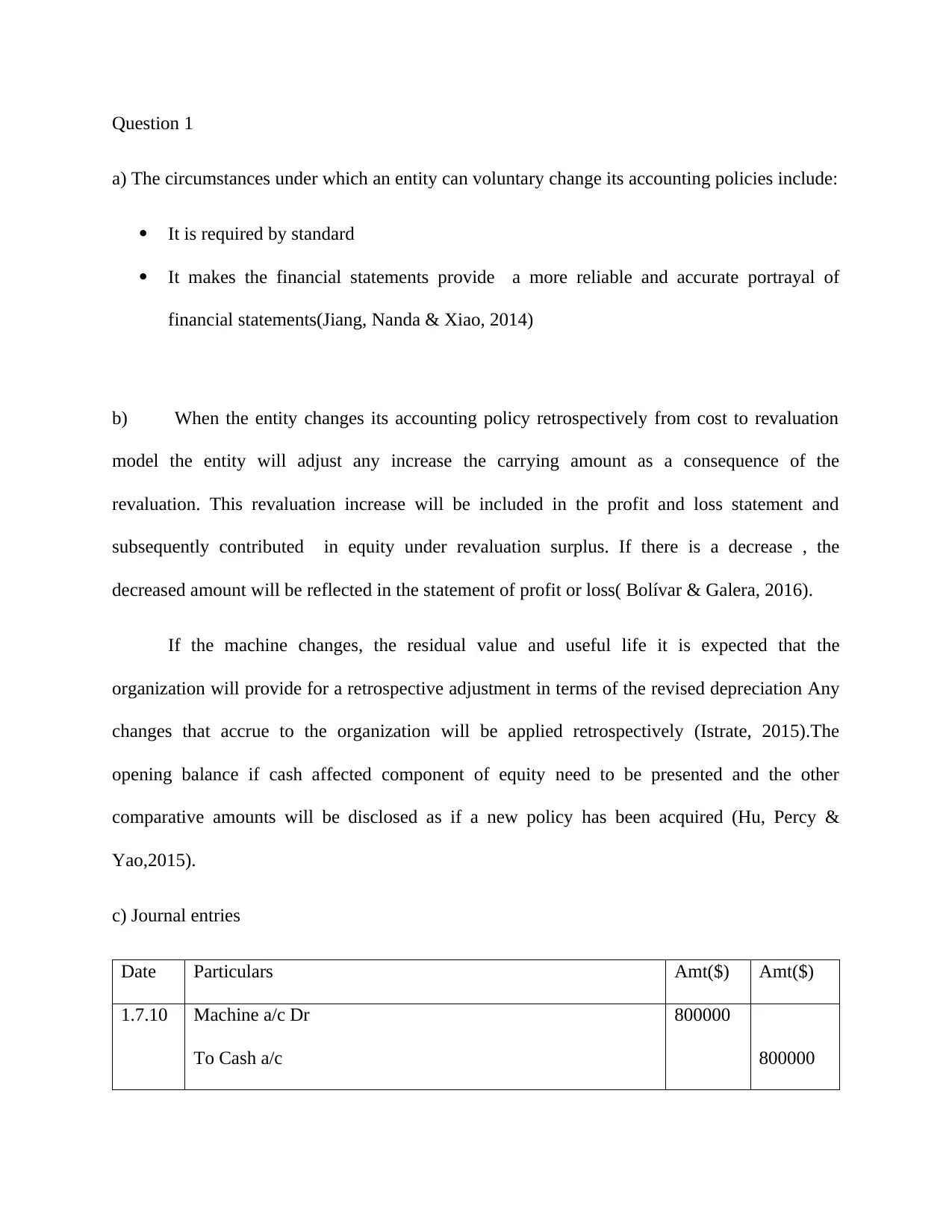

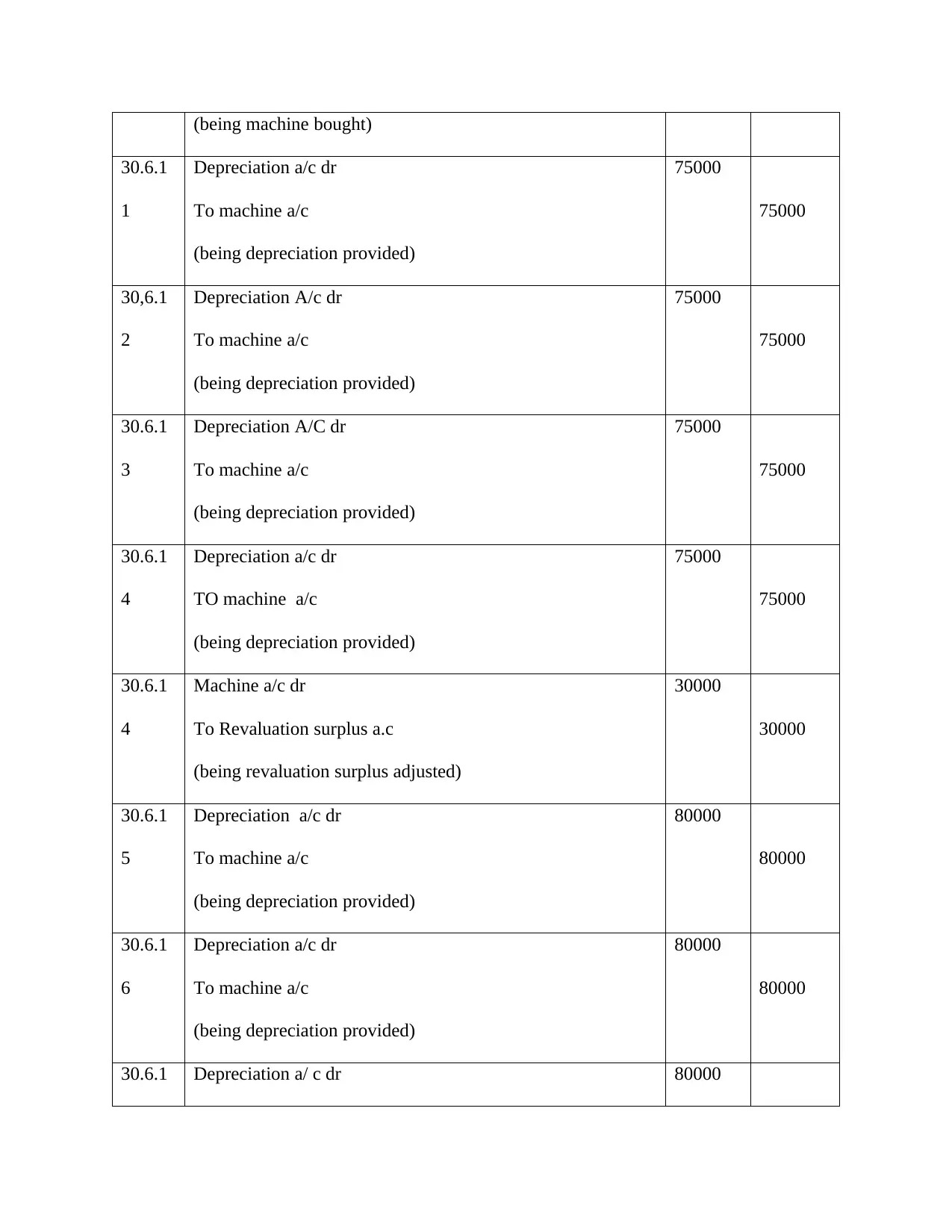

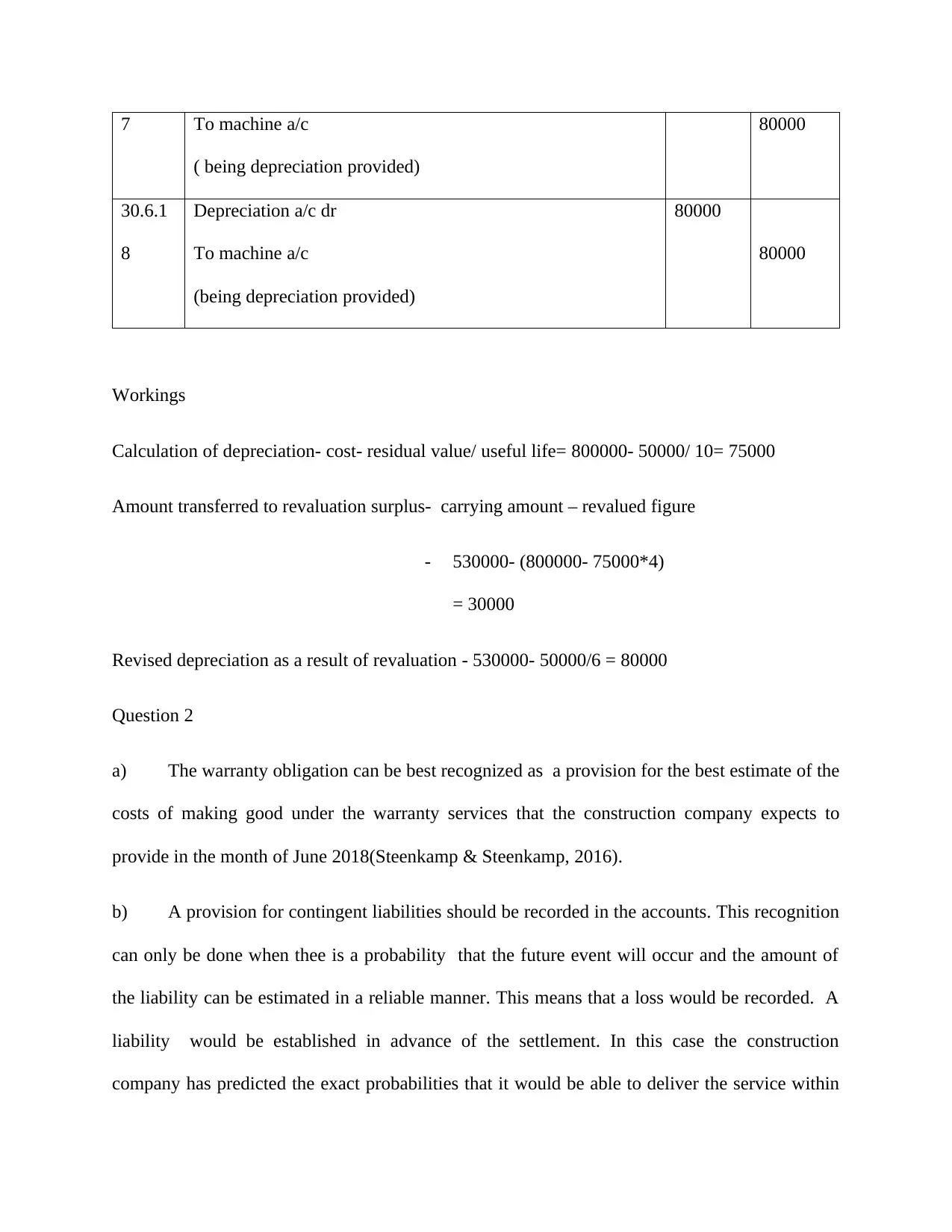

This assignment provides solutions to accounting problems related to changes in accounting policies, warranty obligations, and intangible assets. It covers the circumstances under which an entity can voluntarily change its accounting policies, including requirements by standards or to provide a more reliable portrayal of financial statements. The solution demonstrates the retrospective application of accounting policy changes, including journal entries for machine revaluation and depreciation. It also addresses the recognition of warranty obligations as provisions, contingent liabilities, and the criteria for recognizing intangible assets under AASB 138, differentiating between internally generated and acquired intangible assets. Desklib offers a wealth of similar solved assignments and study resources for students.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.