University Accounting Theory and Practice Workshop 8 Assignment

VerifiedAdded on 2023/04/23

|9

|1198

|461

Homework Assignment

AI Summary

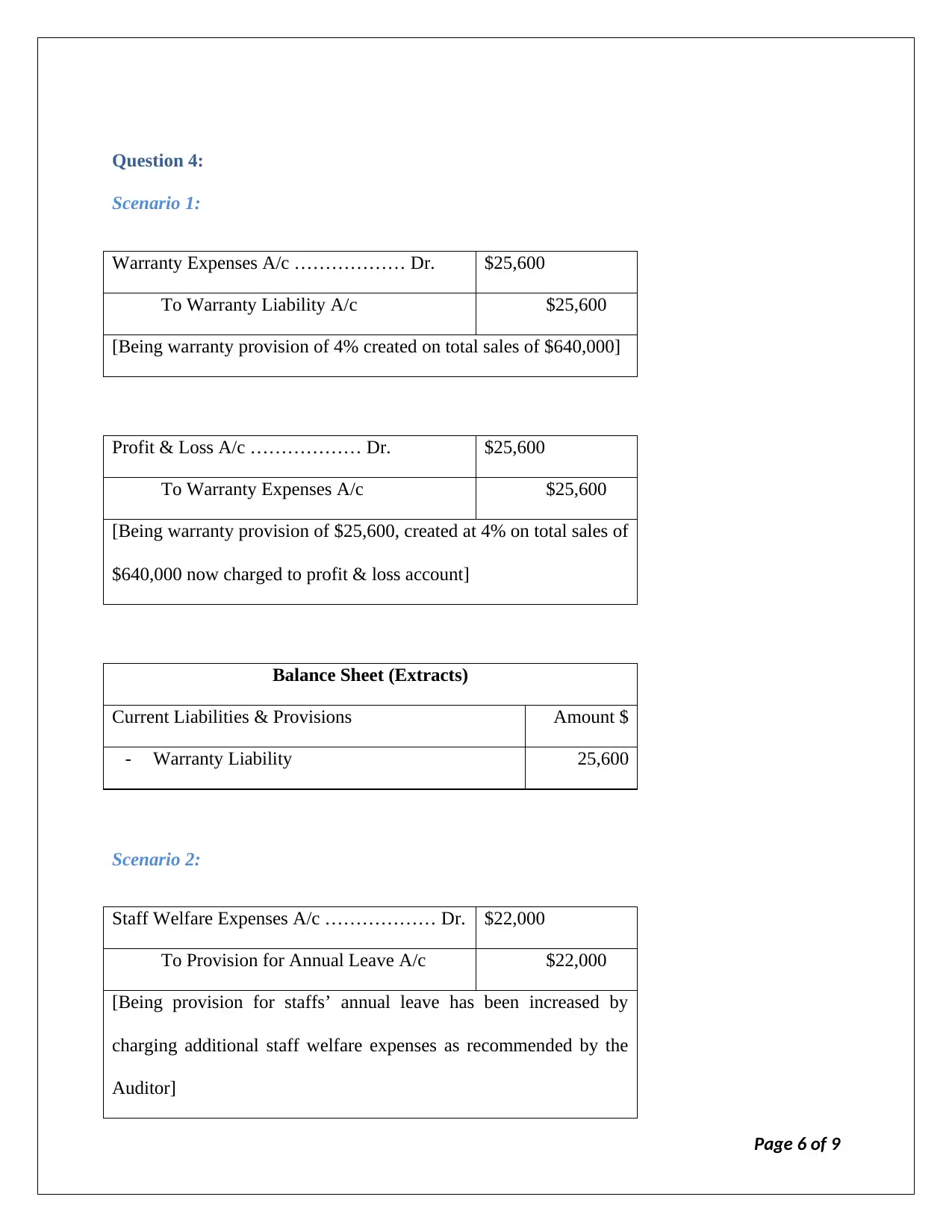

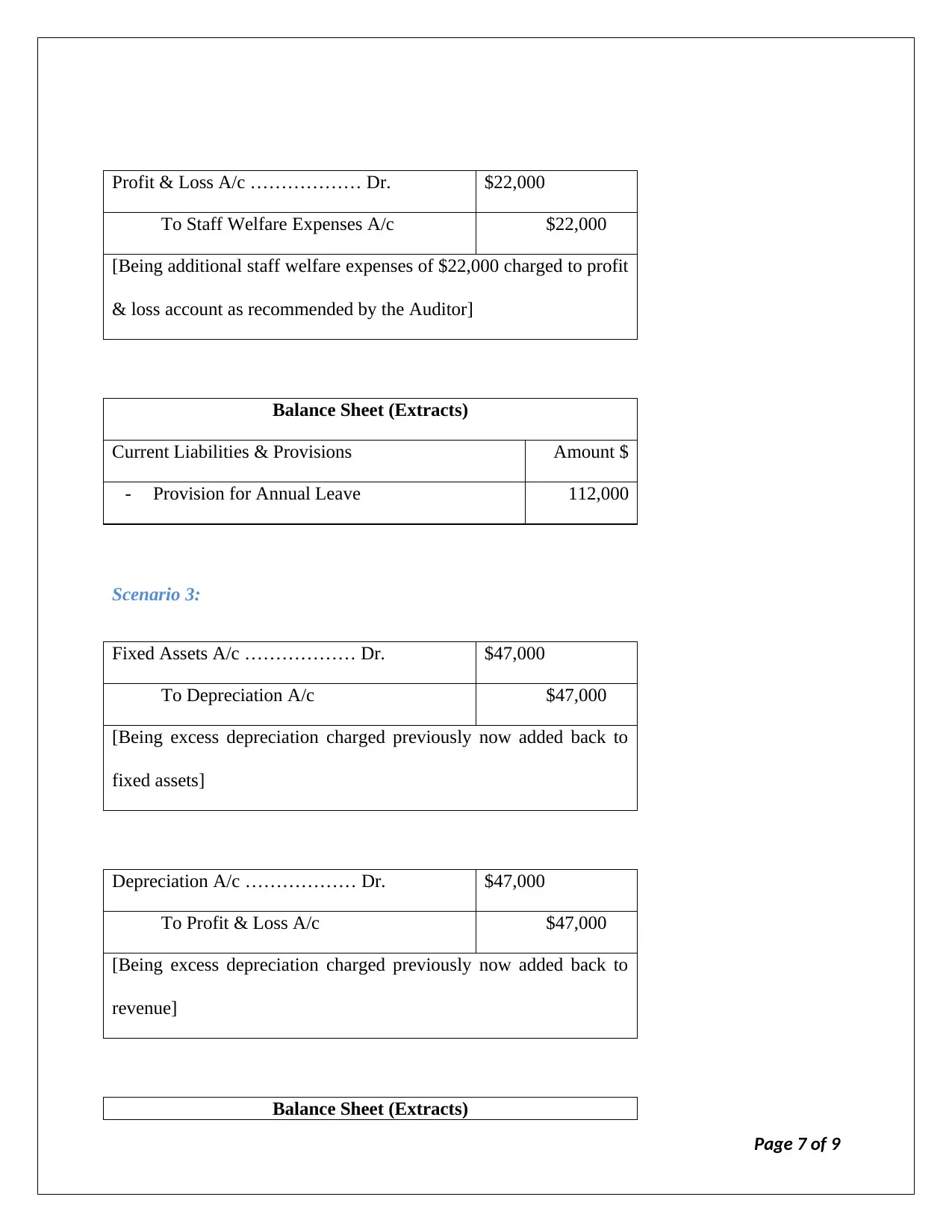

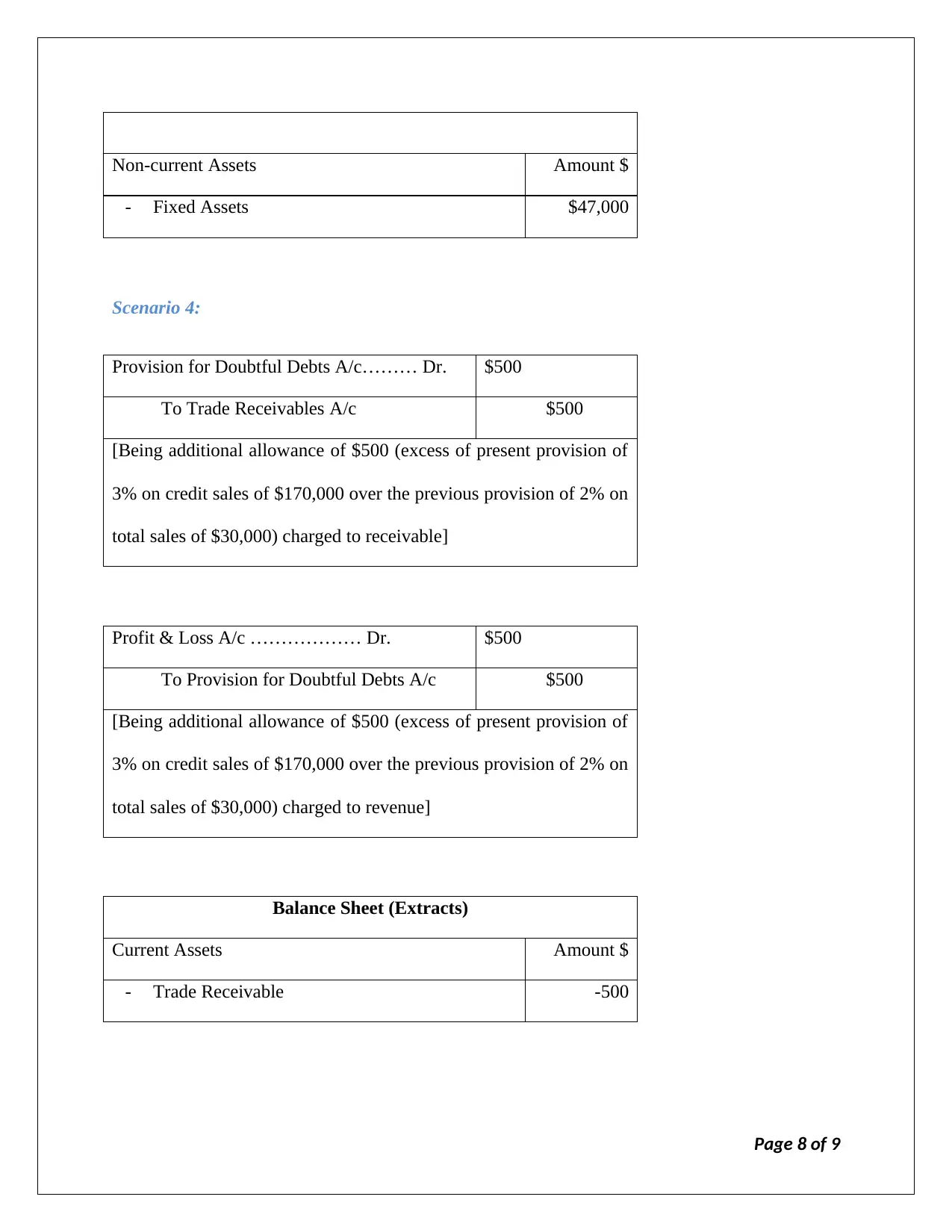

This assignment solution addresses key concepts in accounting theory and practice, focusing on changes in accounting policies and estimates. Question 1 differentiates between changes in accounting policy (e.g., revaluation method) and changes in accounting estimate (e.g., depreciation method), detailing their accounting treatments and impact on financial statements. Question 2 discusses the handling of prior period errors, emphasizing adjustments to opening equity based on the practicability of tracing the error. Question 3 examines a change in warranty provision and a prior period error. Question 4 provides journal entries and balance sheet extracts for various scenarios including warranty expenses, staff welfare expenses, excess depreciation, and doubtful debts, illustrating their impact on the profit and loss account and balance sheet. The solution incorporates references to relevant accounting standards and literature.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.