Analysis of Management Accounting Practices at Assael Architecture

VerifiedAdded on 2021/02/21

|20

|4305

|39

Report

AI Summary

This report delves into the realm of management accounting, focusing on its application within Assael Architecture Ltd. It commences with an introduction to management accounting, its core concepts, and the necessity of its diverse systems, emphasizing decision-making and financial planning. The report then scrutinizes various methods used for management accounting reporting, including trading and profit/loss accounts, income statements, and balance sheets. A significant portion is dedicated to cost analysis, exploring techniques like standard, normal, marginal, and absorption costing, with illustrative case studies. Furthermore, the report examines the advantages and disadvantages of planning tools used in budgetary control, and assesses how businesses adapt management accounting systems to address financial challenges. The analysis covers various types of accounting systems like cost accounting, inventory management, job costing and price optimization systems. The report concludes with a comprehensive overview of management accounting practices, offering valuable insights into financial management and strategic planning within the context of Assael Architecture Ltd.

MANAGEMENT AND

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Concept of Management Accounting and requirement of its different systems...................1

P2. Various Methods used for Management Accounting Reporting...........................................3

TASK 2............................................................................................................................................5

P3. Ascertainment of Costs using appropriate cost analysis techniques.....................................5

.........................................................................................................................................................8

TASK 3............................................................................................................................................8

P4. Advantages and Disadvantages of different planning tools used in Budgetary Control.......8

TASK 4..........................................................................................................................................13

P5. Assessing how businesses are adapting MAS to respond to financial problems................13

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Concept of Management Accounting and requirement of its different systems...................1

P2. Various Methods used for Management Accounting Reporting...........................................3

TASK 2............................................................................................................................................5

P3. Ascertainment of Costs using appropriate cost analysis techniques.....................................5

.........................................................................................................................................................8

TASK 3............................................................................................................................................8

P4. Advantages and Disadvantages of different planning tools used in Budgetary Control.......8

TASK 4..........................................................................................................................................13

P5. Assessing how businesses are adapting MAS to respond to financial problems................13

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Management Accounting helps in the analysis of accounting information in order to

communicate important results to both internal as well as external stakeholders of a business

(Bracci and Maran, 2012). For the successful completion of this report, Assael Architecture Ltd.

has been chosen in order to analyse the practices of management accounting in a critical manner.

Assael is a medium-sized manufacturing firm which was established by John Assael in 1994 and

is based out of Putney, UK. In addition to this, the given report also aims to provide a detailed

account of various types of management accounting systems as well as reports. It also

emphasizes on the various types of budgets, budgetary control as well as preparation of such

budgets using a wide variety of cases.

TASK 1

P1. Concept of Management Accounting and requirement of its different systems

Management accounting is a procedure of controlling , managing and evaluating the

organisational performance that helps to measure the internal control system of an organisation.

Assael Architecture Ltd uses management accounting process to betterment of the business

strategies related to decision making and financial planning .

Key functions of management accounting system:

Function of the management accounting system includes present the modified data to

evaluate the result through various techniques. It includes analysis and interpretation of relevant

data as ratio analysis or trend analysis to reckon the company growth and market valuation

(DRURY, 2013). Assael Architects Ltd is prepared the accounting statements such as fund flow

statements, cash flow statement, capital budgeting to facilitates the better control of the integral

parts of management. Modified and interpreted information are useful to management for taking

quality decision and strategic planning in management accounting. Assael company uses the

qualitative information for recognise the policy formulation, employees efficiency, detailed

business strategies.

Financial accounting system:

Financial accounting is a branch of accounting that records the business transaction over a

specific time period. It is the process of recording, summarizing of the business operations. This

system aims to prepare a financial report or financial statement such as an income statement or

1

Management Accounting helps in the analysis of accounting information in order to

communicate important results to both internal as well as external stakeholders of a business

(Bracci and Maran, 2012). For the successful completion of this report, Assael Architecture Ltd.

has been chosen in order to analyse the practices of management accounting in a critical manner.

Assael is a medium-sized manufacturing firm which was established by John Assael in 1994 and

is based out of Putney, UK. In addition to this, the given report also aims to provide a detailed

account of various types of management accounting systems as well as reports. It also

emphasizes on the various types of budgets, budgetary control as well as preparation of such

budgets using a wide variety of cases.

TASK 1

P1. Concept of Management Accounting and requirement of its different systems

Management accounting is a procedure of controlling , managing and evaluating the

organisational performance that helps to measure the internal control system of an organisation.

Assael Architecture Ltd uses management accounting process to betterment of the business

strategies related to decision making and financial planning .

Key functions of management accounting system:

Function of the management accounting system includes present the modified data to

evaluate the result through various techniques. It includes analysis and interpretation of relevant

data as ratio analysis or trend analysis to reckon the company growth and market valuation

(DRURY, 2013). Assael Architects Ltd is prepared the accounting statements such as fund flow

statements, cash flow statement, capital budgeting to facilitates the better control of the integral

parts of management. Modified and interpreted information are useful to management for taking

quality decision and strategic planning in management accounting. Assael company uses the

qualitative information for recognise the policy formulation, employees efficiency, detailed

business strategies.

Financial accounting system:

Financial accounting is a branch of accounting that records the business transaction over a

specific time period. It is the process of recording, summarizing of the business operations. This

system aims to prepare a financial report or financial statement such as an income statement or

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

balance sheet from the business operation. Accounting information system is a process of

retrieving,storing, collecting, reporting the financial data by accountant, consultant and business

analysts. These financial reports can be used by the internal management or external parties such

as investors, creditors, suppliers. For example investor uses the financial statement to know

profit of the company or its market valuation. Also, Internal control is a process in auditing to

affirm the operational effectiveness of the financial reporting. Internal control system of auditing

is scrutinization the relevant data checking whether it follow rules and regulation or compliance

the laws or not (Hilton and Platt, 2013). Auditing is a systematic or independent examination of

books of accounting and auditor conduct the official inspection of financial statement which are

made during the accounting period .Auditor examined the document and vouchers of the

business activities to determined that financial information are true or not.

Cost accounting system: It is the framework that helps in estimating cost of products for

evaluation of inventory, profitability analysis and cost control. The main requirement of

this system is to estimating accurate cost for make the business operations profitable.

Product-based costing is all about allocating direct and indirect expenses to individual

units of finished product. Productivity-based costing is a more complex system that

assigns costs to activity centres rather than the products 's cost. It assigns costs to

particular overhead activities then assigns costs to products. An activity-based costing

(ABC) system ascertains the relationship between overhead activities and manufactured

products. It specifies that allocating the cost through cost driver and add on value to its

product indirectly. For example – indirect expenses of a business , rent of the office is

allocating or distributing on the basis of the floor area space (Kaplan and Atkinson,

2015).

Management accounting system: Management accounting is a process that involves

decision making, business planning and performance management of the internal

stakeholders of an organisation. Decision support system is an information system that

supports to management in decision making activities. Profit management is business

activity that shows the income ahead of expenses and cost.

Tax accounting System: Tax accounting is a process of accounting methods that focused

on taxes. Tax accounting is governed by the Internal Revenue Code that represent the

specific rules of companies and individuals must follow when filing the tax returns. But

2

retrieving,storing, collecting, reporting the financial data by accountant, consultant and business

analysts. These financial reports can be used by the internal management or external parties such

as investors, creditors, suppliers. For example investor uses the financial statement to know

profit of the company or its market valuation. Also, Internal control is a process in auditing to

affirm the operational effectiveness of the financial reporting. Internal control system of auditing

is scrutinization the relevant data checking whether it follow rules and regulation or compliance

the laws or not (Hilton and Platt, 2013). Auditing is a systematic or independent examination of

books of accounting and auditor conduct the official inspection of financial statement which are

made during the accounting period .Auditor examined the document and vouchers of the

business activities to determined that financial information are true or not.

Cost accounting system: It is the framework that helps in estimating cost of products for

evaluation of inventory, profitability analysis and cost control. The main requirement of

this system is to estimating accurate cost for make the business operations profitable.

Product-based costing is all about allocating direct and indirect expenses to individual

units of finished product. Productivity-based costing is a more complex system that

assigns costs to activity centres rather than the products 's cost. It assigns costs to

particular overhead activities then assigns costs to products. An activity-based costing

(ABC) system ascertains the relationship between overhead activities and manufactured

products. It specifies that allocating the cost through cost driver and add on value to its

product indirectly. For example – indirect expenses of a business , rent of the office is

allocating or distributing on the basis of the floor area space (Kaplan and Atkinson,

2015).

Management accounting system: Management accounting is a process that involves

decision making, business planning and performance management of the internal

stakeholders of an organisation. Decision support system is an information system that

supports to management in decision making activities. Profit management is business

activity that shows the income ahead of expenses and cost.

Tax accounting System: Tax accounting is a process of accounting methods that focused

on taxes. Tax accounting is governed by the Internal Revenue Code that represent the

specific rules of companies and individuals must follow when filing the tax returns. But

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the corporate tax is charge on profit of the firms or registered company. GST accounting

is concludes all the records and accounts that maintain at the head of business as well as

all its branch (Lopez-Valeiras, Gomez-Conde and Naranjo-Gil, 2015).

P2. Various Methods used for Management Accounting Reporting

Different types of Managerial Accounting Reports:

Trading and Profit and Loss Account: Its main purpose is to ascertain the gross as well

as net profit that an organisation such as Assael Architecture Ltd. earns in a given year. It

is used to determine costs in a consolidated manner, in relation to total sales of a given

year. Net profit is calculated by reducing indirect expenses from the given the gross

profit.

Cost of Goods Sold: This is used to ascertain the cost of sales that is incurred by a

business in a particular year. The main use of this report is to check whether or not there

is substantial margin earned on every unit sold by a business.

Income Statement: It helps in calculating the net profit by analysing incomes against

expenditures for a definite time period. Its main use is to keep in check the administrative

overheads that may impact the overall profitability of a company.

Balance Sheet: One of the most important managerial reports that discloses the image as

well as the position of a business at a particular point of time. Its main purpose is to

present the assets and liabilities of the enterprise in a competent manner so as to

communicate worth of the business to different stakeholders.

Cash Flow Statement: Another important report, Cash Flow Statements' main purpose is

to facilitate the communication of the overall liquidity of cash by indicating sources of

funds and their application in a comprehensible manner (Nixon and Burns, 2012).

Types of Accounting Systems:

Cost accounting system:

It is a structure that is normally used by organisations to forecast their estimated total cost of

product in relation to profitability index, inventory valuation and cost control. This system also

performs cost analysis of product by taking into account different profit elements. It is suitable

for a company that aims to consider total cost of production at each step of production. Assael

Architecture Ltd. uses cost accounting system in order to calculate costs using appropriate

3

is concludes all the records and accounts that maintain at the head of business as well as

all its branch (Lopez-Valeiras, Gomez-Conde and Naranjo-Gil, 2015).

P2. Various Methods used for Management Accounting Reporting

Different types of Managerial Accounting Reports:

Trading and Profit and Loss Account: Its main purpose is to ascertain the gross as well

as net profit that an organisation such as Assael Architecture Ltd. earns in a given year. It

is used to determine costs in a consolidated manner, in relation to total sales of a given

year. Net profit is calculated by reducing indirect expenses from the given the gross

profit.

Cost of Goods Sold: This is used to ascertain the cost of sales that is incurred by a

business in a particular year. The main use of this report is to check whether or not there

is substantial margin earned on every unit sold by a business.

Income Statement: It helps in calculating the net profit by analysing incomes against

expenditures for a definite time period. Its main use is to keep in check the administrative

overheads that may impact the overall profitability of a company.

Balance Sheet: One of the most important managerial reports that discloses the image as

well as the position of a business at a particular point of time. Its main purpose is to

present the assets and liabilities of the enterprise in a competent manner so as to

communicate worth of the business to different stakeholders.

Cash Flow Statement: Another important report, Cash Flow Statements' main purpose is

to facilitate the communication of the overall liquidity of cash by indicating sources of

funds and their application in a comprehensible manner (Nixon and Burns, 2012).

Types of Accounting Systems:

Cost accounting system:

It is a structure that is normally used by organisations to forecast their estimated total cost of

product in relation to profitability index, inventory valuation and cost control. This system also

performs cost analysis of product by taking into account different profit elements. It is suitable

for a company that aims to consider total cost of production at each step of production. Assael

Architecture Ltd. uses cost accounting system in order to calculate costs using appropriate

3

techniques. Additionally, it also facilitates the verification of the operational cost and direct cost

on a regular basis.

Inventory management system :

This system includes techniques of stock management wherein an organisation is enabled to

track their inventory level, economic order quantity and Re-order level among others (Odar,

Kavčič and Jerman, 2012). In the context of given case scenario, Assael Architecture Ltd. makes

this inventory report on a monthly basis so as to know the closing balance of a particular

completed projected that needs to be handed over to a customer. It also facilitates in valuation of

the proposed projects or opportunities that may be undertaken by Assael in near future.

Job costing system:

It is a tracking system of cost wherein necessary information is accumulated regarding a specific

job whether the business deals is a manufacturing entity or a service provider. Job costing system

also includes the overhead cost like Depreciation or Rent. Through this system, a business is able

to prevent duplication of work. All these costs that are applicable to production or services are

mostly included in cost of good sold. Assael Architecture Ltd. is using the concepts for

reckoning the total cost on the job of a project that are labour cost, overhead expenses. As per

this system, Assael can track their cost of material, labour cost and overheads for an ongoing or

completed project.

Price optimisation system:

When an organisation wants to maximize their operating profits while minimizing their costs

simultaneously, a business may use a Price Optimisation system as it employs mathematical

analysis and helps an organisation in achieving complete optimisation of their prices for a given

product or service at various levels of costs. It is worthy to note that the product demand is

usually dependent on the product price as well as its quality. It is also helps in the determination

of that price level which will bring about excellent quality deliverance as well as maximum

number of sales for the company meeting customers' objective at the same time. Assael

Architecture Ltd. optimizes their pricing strategies at varying project costs by analysing different

pricing projects according to their targetted demand.

4

on a regular basis.

Inventory management system :

This system includes techniques of stock management wherein an organisation is enabled to

track their inventory level, economic order quantity and Re-order level among others (Odar,

Kavčič and Jerman, 2012). In the context of given case scenario, Assael Architecture Ltd. makes

this inventory report on a monthly basis so as to know the closing balance of a particular

completed projected that needs to be handed over to a customer. It also facilitates in valuation of

the proposed projects or opportunities that may be undertaken by Assael in near future.

Job costing system:

It is a tracking system of cost wherein necessary information is accumulated regarding a specific

job whether the business deals is a manufacturing entity or a service provider. Job costing system

also includes the overhead cost like Depreciation or Rent. Through this system, a business is able

to prevent duplication of work. All these costs that are applicable to production or services are

mostly included in cost of good sold. Assael Architecture Ltd. is using the concepts for

reckoning the total cost on the job of a project that are labour cost, overhead expenses. As per

this system, Assael can track their cost of material, labour cost and overheads for an ongoing or

completed project.

Price optimisation system:

When an organisation wants to maximize their operating profits while minimizing their costs

simultaneously, a business may use a Price Optimisation system as it employs mathematical

analysis and helps an organisation in achieving complete optimisation of their prices for a given

product or service at various levels of costs. It is worthy to note that the product demand is

usually dependent on the product price as well as its quality. It is also helps in the determination

of that price level which will bring about excellent quality deliverance as well as maximum

number of sales for the company meeting customers' objective at the same time. Assael

Architecture Ltd. optimizes their pricing strategies at varying project costs by analysing different

pricing projects according to their targetted demand.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

P3. Ascertainment of Costs using appropriate cost analysis techniques

The term 'cost' can be defined as the monetary value that is expended by a business while

engaging producing of goods and services. A cost may be analysed using different techniques

that have been enumerated as under:

Standard Costing:

It is a method in which a standards has been set for the production. These standard has been set

on the basis of estimates. Since Assael Architecture Ltd is a huge company and recording all

the actual cost is not practically possible, company uses standard costing. It plays a role of

budget for the company.

Normal Costing:

It is a method of costing which includes actual costs of production. It uses actual direct costs

which have been incurred during the production. Assael Architecture Ltd also prepare records

using normal accounting methods. Company derives its cost of production to show in the

financial statements.

Marginal Costing:

Marginal costing is a method of calculating the cost of making an extra unit of product in respect

of variable cost only. Marginal costing is also known as variable costing. In process of

calculating marginal cost, fixed cost is always written off against contribution. The management

of Assael Architecture Ltd is using marginal costing for better understanding of profit. A clear

bifurcation into fixed and variable costs helps the lower management to reduce and control

variable cost and upper management to balanced fixed cost.

Absorption Costing:

Absorption costing is a method of costing which assigned all the manufacturing cost to the units

produced weather it is fixed or variable (Otley and Emmanuel, 2013). Assael Architecture Ltd

uses absorption costing for reporting to the Internal Revenue Services (IRS). Company using this

costing method because it shows a clear picture of efficient use of valuable resources of the

organization. It also indicate under absorption or over absorption of the factory overheads.

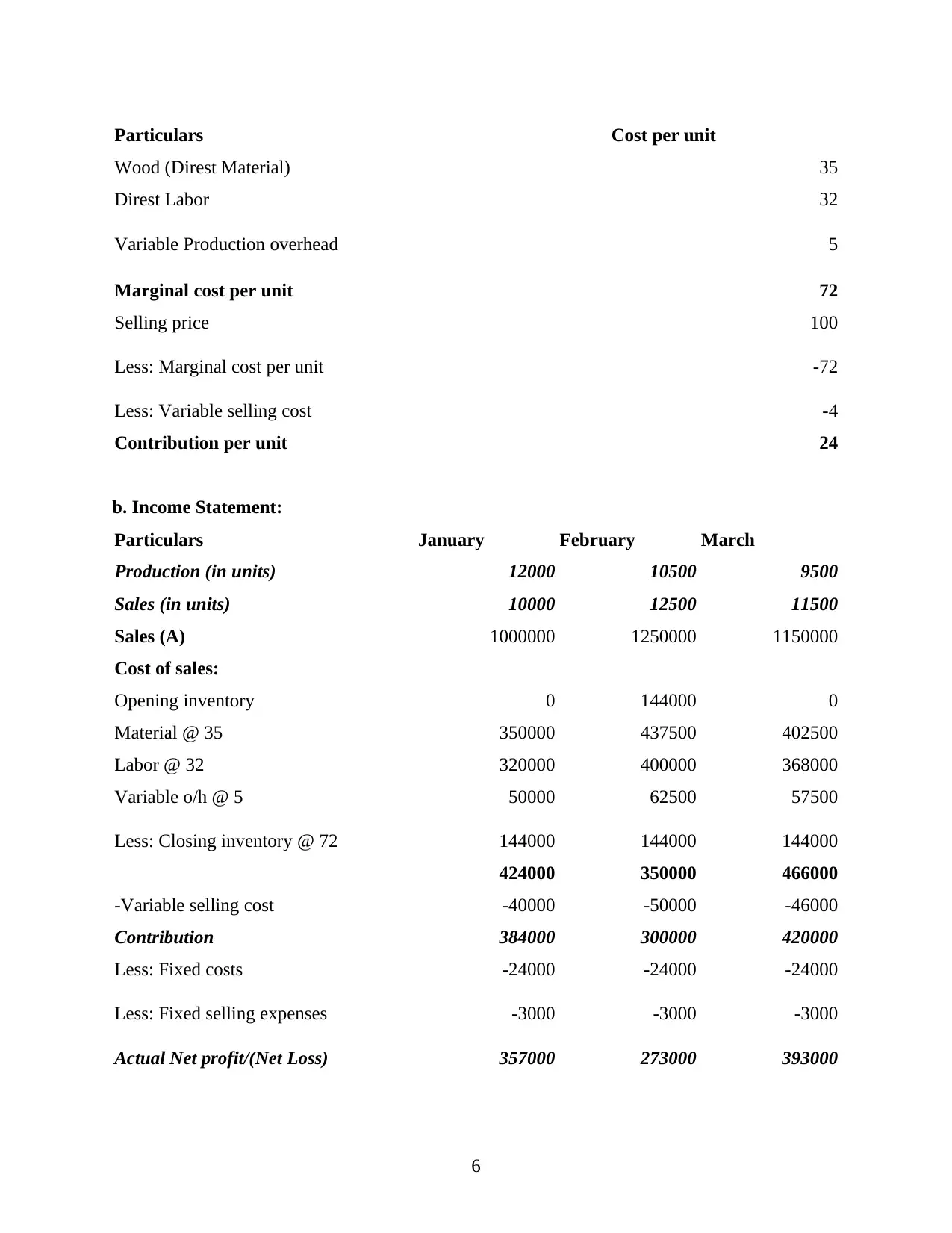

Case 1: Marginal Costing Technique

a. Cost Card:

Cost Card under Marginal Costing

5

P3. Ascertainment of Costs using appropriate cost analysis techniques

The term 'cost' can be defined as the monetary value that is expended by a business while

engaging producing of goods and services. A cost may be analysed using different techniques

that have been enumerated as under:

Standard Costing:

It is a method in which a standards has been set for the production. These standard has been set

on the basis of estimates. Since Assael Architecture Ltd is a huge company and recording all

the actual cost is not practically possible, company uses standard costing. It plays a role of

budget for the company.

Normal Costing:

It is a method of costing which includes actual costs of production. It uses actual direct costs

which have been incurred during the production. Assael Architecture Ltd also prepare records

using normal accounting methods. Company derives its cost of production to show in the

financial statements.

Marginal Costing:

Marginal costing is a method of calculating the cost of making an extra unit of product in respect

of variable cost only. Marginal costing is also known as variable costing. In process of

calculating marginal cost, fixed cost is always written off against contribution. The management

of Assael Architecture Ltd is using marginal costing for better understanding of profit. A clear

bifurcation into fixed and variable costs helps the lower management to reduce and control

variable cost and upper management to balanced fixed cost.

Absorption Costing:

Absorption costing is a method of costing which assigned all the manufacturing cost to the units

produced weather it is fixed or variable (Otley and Emmanuel, 2013). Assael Architecture Ltd

uses absorption costing for reporting to the Internal Revenue Services (IRS). Company using this

costing method because it shows a clear picture of efficient use of valuable resources of the

organization. It also indicate under absorption or over absorption of the factory overheads.

Case 1: Marginal Costing Technique

a. Cost Card:

Cost Card under Marginal Costing

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars Cost per unit

Wood (Direst Material) 35

Direst Labor 32

Variable Production overhead 5

Marginal cost per unit 72

Selling price 100

Less: Marginal cost per unit -72

Less: Variable selling cost -4

Contribution per unit 24

b. Income Statement:

Particulars January February March

Production (in units) 12000 10500 9500

Sales (in units) 10000 12500 11500

Sales (A) 1000000 1250000 1150000

Cost of sales:

Opening inventory 0 144000 0

Material @ 35 350000 437500 402500

Labor @ 32 320000 400000 368000

Variable o/h @ 5 50000 62500 57500

Less: Closing inventory @ 72 144000 144000 144000

424000 350000 466000

-Variable selling cost -40000 -50000 -46000

Contribution 384000 300000 420000

Less: Fixed costs -24000 -24000 -24000

Less: Fixed selling expenses -3000 -3000 -3000

Actual Net profit/(Net Loss) 357000 273000 393000

6

Wood (Direst Material) 35

Direst Labor 32

Variable Production overhead 5

Marginal cost per unit 72

Selling price 100

Less: Marginal cost per unit -72

Less: Variable selling cost -4

Contribution per unit 24

b. Income Statement:

Particulars January February March

Production (in units) 12000 10500 9500

Sales (in units) 10000 12500 11500

Sales (A) 1000000 1250000 1150000

Cost of sales:

Opening inventory 0 144000 0

Material @ 35 350000 437500 402500

Labor @ 32 320000 400000 368000

Variable o/h @ 5 50000 62500 57500

Less: Closing inventory @ 72 144000 144000 144000

424000 350000 466000

-Variable selling cost -40000 -50000 -46000

Contribution 384000 300000 420000

Less: Fixed costs -24000 -24000 -24000

Less: Fixed selling expenses -3000 -3000 -3000

Actual Net profit/(Net Loss) 357000 273000 393000

6

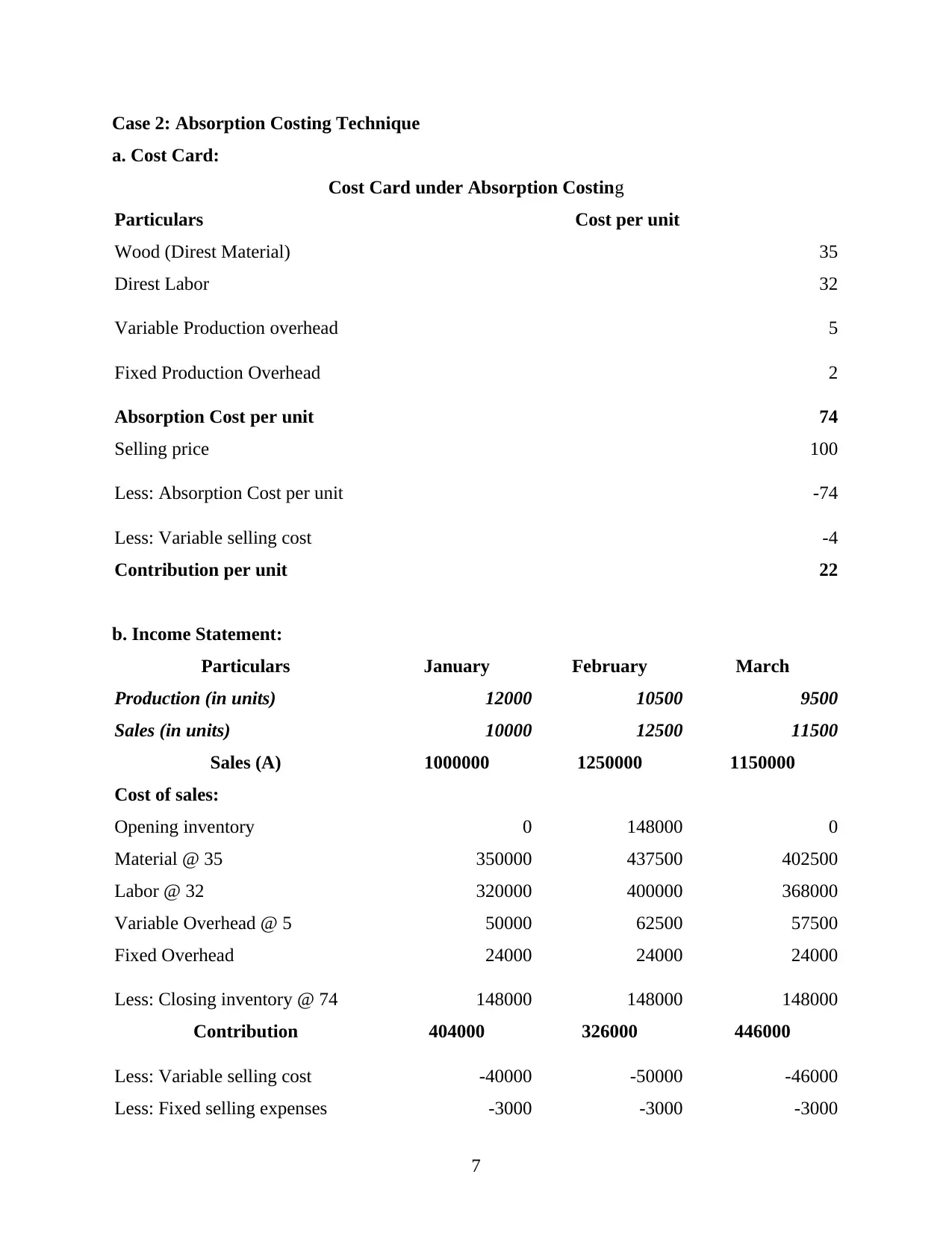

Case 2: Absorption Costing Technique

a. Cost Card:

Cost Card under Absorption Costing

Particulars Cost per unit

Wood (Direst Material) 35

Direst Labor 32

Variable Production overhead 5

Fixed Production Overhead 2

Absorption Cost per unit 74

Selling price 100

Less: Absorption Cost per unit -74

Less: Variable selling cost -4

Contribution per unit 22

b. Income Statement:

Particulars January February March

Production (in units) 12000 10500 9500

Sales (in units) 10000 12500 11500

Sales (A) 1000000 1250000 1150000

Cost of sales:

Opening inventory 0 148000 0

Material @ 35 350000 437500 402500

Labor @ 32 320000 400000 368000

Variable Overhead @ 5 50000 62500 57500

Fixed Overhead 24000 24000 24000

Less: Closing inventory @ 74 148000 148000 148000

Contribution 404000 326000 446000

Less: Variable selling cost -40000 -50000 -46000

Less: Fixed selling expenses -3000 -3000 -3000

7

a. Cost Card:

Cost Card under Absorption Costing

Particulars Cost per unit

Wood (Direst Material) 35

Direst Labor 32

Variable Production overhead 5

Fixed Production Overhead 2

Absorption Cost per unit 74

Selling price 100

Less: Absorption Cost per unit -74

Less: Variable selling cost -4

Contribution per unit 22

b. Income Statement:

Particulars January February March

Production (in units) 12000 10500 9500

Sales (in units) 10000 12500 11500

Sales (A) 1000000 1250000 1150000

Cost of sales:

Opening inventory 0 148000 0

Material @ 35 350000 437500 402500

Labor @ 32 320000 400000 368000

Variable Overhead @ 5 50000 62500 57500

Fixed Overhead 24000 24000 24000

Less: Closing inventory @ 74 148000 148000 148000

Contribution 404000 326000 446000

Less: Variable selling cost -40000 -50000 -46000

Less: Fixed selling expenses -3000 -3000 -3000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Actual Net profit/(Net Loss) 361000 273000 397000

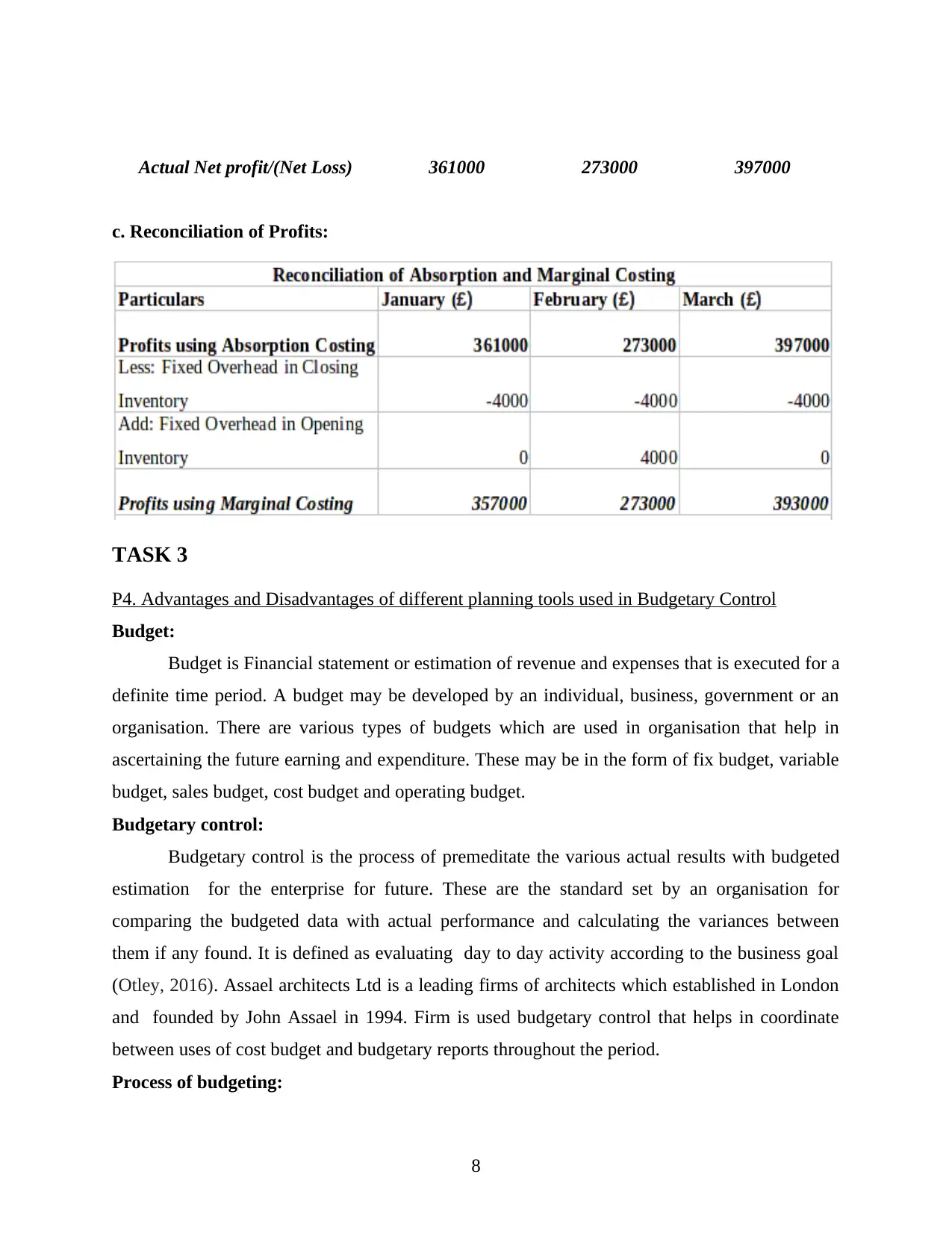

c. Reconciliation of Profits:

TASK 3

P4. Advantages and Disadvantages of different planning tools used in Budgetary Control

Budget:

Budget is Financial statement or estimation of revenue and expenses that is executed for a

definite time period. A budget may be developed by an individual, business, government or an

organisation. There are various types of budgets which are used in organisation that help in

ascertaining the future earning and expenditure. These may be in the form of fix budget, variable

budget, sales budget, cost budget and operating budget.

Budgetary control:

Budgetary control is the process of premeditate the various actual results with budgeted

estimation for the enterprise for future. These are the standard set by an organisation for

comparing the budgeted data with actual performance and calculating the variances between

them if any found. It is defined as evaluating day to day activity according to the business goal

(Otley, 2016). Assael architects Ltd is a leading firms of architects which established in London

and founded by John Assael in 1994. Firm is used budgetary control that helps in coordinate

between uses of cost budget and budgetary reports throughout the period.

Process of budgeting:

8

c. Reconciliation of Profits:

TASK 3

P4. Advantages and Disadvantages of different planning tools used in Budgetary Control

Budget:

Budget is Financial statement or estimation of revenue and expenses that is executed for a

definite time period. A budget may be developed by an individual, business, government or an

organisation. There are various types of budgets which are used in organisation that help in

ascertaining the future earning and expenditure. These may be in the form of fix budget, variable

budget, sales budget, cost budget and operating budget.

Budgetary control:

Budgetary control is the process of premeditate the various actual results with budgeted

estimation for the enterprise for future. These are the standard set by an organisation for

comparing the budgeted data with actual performance and calculating the variances between

them if any found. It is defined as evaluating day to day activity according to the business goal

(Otley, 2016). Assael architects Ltd is a leading firms of architects which established in London

and founded by John Assael in 1994. Firm is used budgetary control that helps in coordinate

between uses of cost budget and budgetary reports throughout the period.

Process of budgeting:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Every organisation needs a budget in order to carry out planning activities of its

operational activities. A formal budget process makes a strong foundation for business

management, growth and development. Budgeting process helps a business manager to identify

different business needs by obtaining necessary information regarding sales, production levels

and budgeted cost among others. A Budget committee assesses different plan of functional

department and determines the potentiality of plan and resource available to company. Once they

approve the budget, the budget committee communicates the same with all the department heads

in order to gain consensus. Also, each departmental head can check budget and implement

according to the requirement of their department. Once all the changes are incorporated, the head

of the department finalises the budget and presents the same to the top management level for

final approval. Different organisations use different budgets based on their needs and suitability.

In order to showcase this, the following budgets have been prepared and discussed:

Cash budget:

A Company such as Assael needs to estimate the required amount which can help in

meeting the short-term obligations of the business. If Assael is having excess cash then it can go

for credit sales. This can boost their profitability ratio. Hence, cash budget shows how an

organisation such as Assael can use their cash funds in an optimal manner. Advantage: It is used to determine whether or not the cash balance is sufficient for

carrying out day to day activities.

Disadvantage: Cash budget does not show the profit earned by an organisation. In

addition to this, the estimated cash balance using this budget does not depict a true

image.

Operating budget:

An operating budget is one which helps the organisation such as Assael in planning its

day to day activities. Through this budget the company is able to ascertain the manner in which

debt obligations can be met in an effective manner (Sánchez-Rodríguez and Spraakman, 2012). Advantage: This budget helps in evaluating the current actual as well as past expenses.

Thus, facilitating in the identification of any variation occurring in the expenditure.

Disadvantage: It is time consuming and may not be suitable for a small business

especially from taxation perspective.

Case 3

9

operational activities. A formal budget process makes a strong foundation for business

management, growth and development. Budgeting process helps a business manager to identify

different business needs by obtaining necessary information regarding sales, production levels

and budgeted cost among others. A Budget committee assesses different plan of functional

department and determines the potentiality of plan and resource available to company. Once they

approve the budget, the budget committee communicates the same with all the department heads

in order to gain consensus. Also, each departmental head can check budget and implement

according to the requirement of their department. Once all the changes are incorporated, the head

of the department finalises the budget and presents the same to the top management level for

final approval. Different organisations use different budgets based on their needs and suitability.

In order to showcase this, the following budgets have been prepared and discussed:

Cash budget:

A Company such as Assael needs to estimate the required amount which can help in

meeting the short-term obligations of the business. If Assael is having excess cash then it can go

for credit sales. This can boost their profitability ratio. Hence, cash budget shows how an

organisation such as Assael can use their cash funds in an optimal manner. Advantage: It is used to determine whether or not the cash balance is sufficient for

carrying out day to day activities.

Disadvantage: Cash budget does not show the profit earned by an organisation. In

addition to this, the estimated cash balance using this budget does not depict a true

image.

Operating budget:

An operating budget is one which helps the organisation such as Assael in planning its

day to day activities. Through this budget the company is able to ascertain the manner in which

debt obligations can be met in an effective manner (Sánchez-Rodríguez and Spraakman, 2012). Advantage: This budget helps in evaluating the current actual as well as past expenses.

Thus, facilitating in the identification of any variation occurring in the expenditure.

Disadvantage: It is time consuming and may not be suitable for a small business

especially from taxation perspective.

Case 3

9

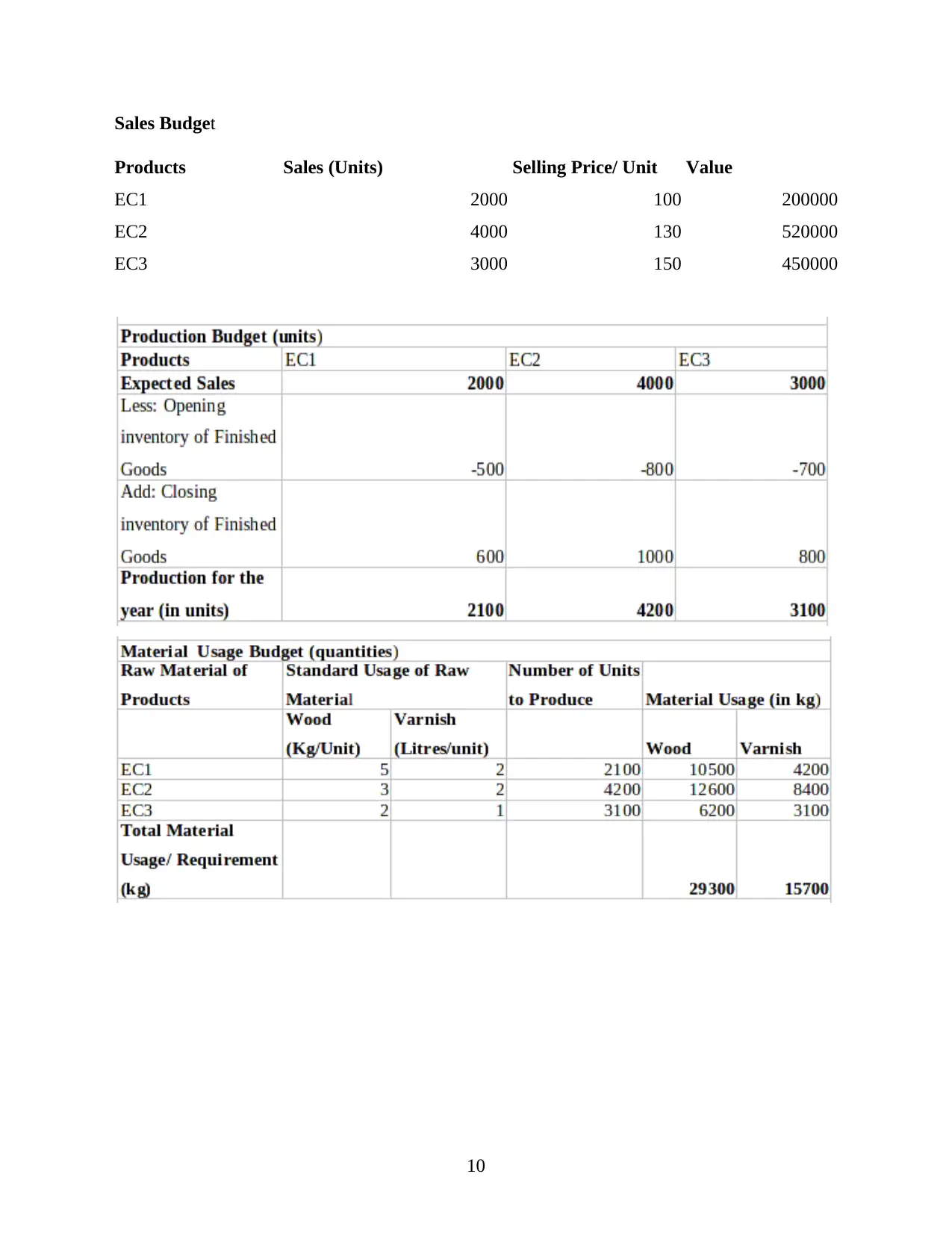

Sales Budget

Products Sales (Units) Selling Price/ Unit Value

EC1 2000 100 200000

EC2 4000 130 520000

EC3 3000 150 450000

10

Products Sales (Units) Selling Price/ Unit Value

EC1 2000 100 200000

EC2 4000 130 520000

EC3 3000 150 450000

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.