Financial Accounting Report: Zync Solutions and Practical Cases

VerifiedAdded on 2020/12/10

|29

|5360

|97

Report

AI Summary

This comprehensive financial accounting report provides a detailed overview of accounting principles and practices. It begins with an introduction to financial accounting and its purposes, followed by an exploration of accounting rules, including personal, nominal, and real accounts. The report delves into key accounting principles such as the dual aspect concept, cost principle, and matching principle. It also discusses the conventions and concepts relating to consistency and material disclosure. The report then presents practical scenarios involving various clients, including journal entries, ledger accounts, trial balances, and financial statements like profit and loss accounts and balance sheets. It covers topics such as bank reconciliation and suspense accounts, providing examples and explanations. The report concludes with a summary of the key findings and references.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCION..............................................................................................................................4

BUSINESS REPORT ....................................................................................................................4

1. Financial accounting and its purposes................................................................................4

3. Accounting rules and principles.........................................................................................6

4. The conventions and the concepts relating to consistency and the material disclosure.....7

CLIENT 1........................................................................................................................................7

(a) Journal Entry in the books of David Study......................................................................7

(b) Ledger Accounts.............................................................................................................11

(c) Trial Balance as at 31st January, 2018............................................................................18

CLIENT 2......................................................................................................................................19

(a) Statement of profit and loss for Peter Hampau for the year ended 31st July 2018 ........19

(b) Statement of financial position for Peter Hampau as at ended 31st July 2018 ..............20

CLIENT 3......................................................................................................................................21

(a) Profit and loss account of Bowling Limited for the year ended 31st July, 2018............21

(b) Balance Sheet of Bowling Limited as at 31st July, 2018...............................................22

(c) Accounts concepts such as consistency and prudency....................................................22

(d) Depreciation and its methods .........................................................................................23

CLIENT 4......................................................................................................................................23

(i) Bank reconciliation statement at 1st December, 2017.....................................................23

(ii) Durrell Ltd's updated cash book for December 2017.....................................................23

(iii) Bank Reconciliation Statement as at 31"t December 2017...........................................24

CLIENT 5......................................................................................................................................25

(a) Books of Henderson........................................................................................................25

(b) Control Account..............................................................................................................26

CLIENT 6......................................................................................................................................26

(a) Suspense Account...........................................................................................................26

(b) Drafting of Trial Balance:...............................................................................................27

(c) Trial balance have credit balance of £ 330 as suspense account....................................27

Suspense A/c.................................................28

(d) Difference between a Suspense A/c and Clearing A/c...................................................28

INTRODUCION..............................................................................................................................4

BUSINESS REPORT ....................................................................................................................4

1. Financial accounting and its purposes................................................................................4

3. Accounting rules and principles.........................................................................................6

4. The conventions and the concepts relating to consistency and the material disclosure.....7

CLIENT 1........................................................................................................................................7

(a) Journal Entry in the books of David Study......................................................................7

(b) Ledger Accounts.............................................................................................................11

(c) Trial Balance as at 31st January, 2018............................................................................18

CLIENT 2......................................................................................................................................19

(a) Statement of profit and loss for Peter Hampau for the year ended 31st July 2018 ........19

(b) Statement of financial position for Peter Hampau as at ended 31st July 2018 ..............20

CLIENT 3......................................................................................................................................21

(a) Profit and loss account of Bowling Limited for the year ended 31st July, 2018............21

(b) Balance Sheet of Bowling Limited as at 31st July, 2018...............................................22

(c) Accounts concepts such as consistency and prudency....................................................22

(d) Depreciation and its methods .........................................................................................23

CLIENT 4......................................................................................................................................23

(i) Bank reconciliation statement at 1st December, 2017.....................................................23

(ii) Durrell Ltd's updated cash book for December 2017.....................................................23

(iii) Bank Reconciliation Statement as at 31"t December 2017...........................................24

CLIENT 5......................................................................................................................................25

(a) Books of Henderson........................................................................................................25

(b) Control Account..............................................................................................................26

CLIENT 6......................................................................................................................................26

(a) Suspense Account...........................................................................................................26

(b) Drafting of Trial Balance:...............................................................................................27

(c) Trial balance have credit balance of £ 330 as suspense account....................................27

Suspense A/c.................................................28

(d) Difference between a Suspense A/c and Clearing A/c...................................................28

CONCLUSION..............................................................................................................................28

REFERENCES .............................................................................................................................30

REFERENCES .............................................................................................................................30

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCION

Financial Accounting is an accounting branch which contains the track of records for all

financial transaction of an entity. Financial transactions are recorded and presented as per

standardized guidelines in a financial report or statements like statement of income and financial

position. This report is divided in two parts such as business report for Zync Solutions limited

which is small accounting firm and the second part consider the practical scenarios based upon

accounting principles and concepts (Edwards, 2013). For a junior accountant, it is necessary to

prepare financial reports by applying the guidelines of accounting principles so that true and fair

view of financial statements can be presented. This report aims to follow rules and principles of

accountancy. This report covers regulations of financial accounting and purpose of it, book

keeping system, trial balance, profit and loss account and balance sheet of sole traders,

partnership firm and a company according to the relevant principles, convention and the

standards. This report also contains the bank reconciliation, its process of reconciliation and the

suspense account along with example containing the process of clearing the suspense account.

BUSINESS REPORT

1. Financial accounting and its purposes

Accounting means the way transactions are recorded, analysed and summarised in the

business. Financial accounting contains all financial information which is recoded in such a

manner that helps in preparation and presentation of financial information of the business by

presenting true and fair view of it (Agasisti and Catalano, 2013). Financial accounting is a way

of reporting business activities and financial information to investors, creditors, suppliers and

other persons outside the business organisation. The accountant of business is responsible to

follow all the rules and regulations and the policies relating to financial accounting so that

accurate information can be analysed.

Purposes of financial accounting: The main purpose of financial accounting is to

summarise

To provide true and fair view of financial transactions of organisation (Holthausen and

Watts, 2001).

To understand and analyse financial statement and fundamentals used in the preparation

of financial statements (Bushman and Smith, 2001).

Financial Accounting is an accounting branch which contains the track of records for all

financial transaction of an entity. Financial transactions are recorded and presented as per

standardized guidelines in a financial report or statements like statement of income and financial

position. This report is divided in two parts such as business report for Zync Solutions limited

which is small accounting firm and the second part consider the practical scenarios based upon

accounting principles and concepts (Edwards, 2013). For a junior accountant, it is necessary to

prepare financial reports by applying the guidelines of accounting principles so that true and fair

view of financial statements can be presented. This report aims to follow rules and principles of

accountancy. This report covers regulations of financial accounting and purpose of it, book

keeping system, trial balance, profit and loss account and balance sheet of sole traders,

partnership firm and a company according to the relevant principles, convention and the

standards. This report also contains the bank reconciliation, its process of reconciliation and the

suspense account along with example containing the process of clearing the suspense account.

BUSINESS REPORT

1. Financial accounting and its purposes

Accounting means the way transactions are recorded, analysed and summarised in the

business. Financial accounting contains all financial information which is recoded in such a

manner that helps in preparation and presentation of financial information of the business by

presenting true and fair view of it (Agasisti and Catalano, 2013). Financial accounting is a way

of reporting business activities and financial information to investors, creditors, suppliers and

other persons outside the business organisation. The accountant of business is responsible to

follow all the rules and regulations and the policies relating to financial accounting so that

accurate information can be analysed.

Purposes of financial accounting: The main purpose of financial accounting is to

summarise

To provide true and fair view of financial transactions of organisation (Holthausen and

Watts, 2001).

To understand and analyse financial statement and fundamentals used in the preparation

of financial statements (Bushman and Smith, 2001).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

With the help of financial accounting, management of organisation can know the profits

and losses of its business in current financial year and through this manager can make

future plans and strategies for future growth of organisation (Peterson, 2005).

The financial accounting can use in production of financial information in such a manner

that make it easy to interpret performance of company using ratio analysis (White, Sondh

and Fried, 2000).

The financial accounting contains various regulations that are needed to be follow by an

accountant of business organisation so that true and fair view of the financial statements can be

produced and analysed. As a result, company can know its financial growth and on the basis of it

investors and creditors can take their decisions. Regulations relating to financial accounting are

as follows:

In financial accounting, Generally Accepted Accounting Principle's rules, standards and

procedures of can be applied by an organisation so that financial statements of

organisation can be prepare correctly. There are various principles of GAAP which are to

be followed by the organisation in order to comply with regulations relating to financial

accounting such as: principle of consistency, precedence, regularity, periodicity etc

(Khan and Mayes, 2009)

The International Financial Reporting Standards framed regulations which is to be

followed by accountant of organisation because it focuses that how a particular type of

transactions or an events can be reported in financial statements of entity (Saunders,

Cornett and McGraw, 2006).

Regulations related to financial accounting such as debit and credit and their treatment in

accounts can be follow by the accountant of organisation so that relevant information and

data can be reported in financial statements of the organisation (Barth, 2015).

As per companies act, it is compulsory to put financial statements and other necessary

documents of company in front of general public so that they can know the financial

position of company for given reporting year (Libby, Bloomfield and Nelson, 2002).

3. Accounting rules and principles

Rules for accounting

Personal Account: The rule relating to personal account state that Debit the

receiver, credit the giver. This principle has been used in case of personal accounts.

and losses of its business in current financial year and through this manager can make

future plans and strategies for future growth of organisation (Peterson, 2005).

The financial accounting can use in production of financial information in such a manner

that make it easy to interpret performance of company using ratio analysis (White, Sondh

and Fried, 2000).

The financial accounting contains various regulations that are needed to be follow by an

accountant of business organisation so that true and fair view of the financial statements can be

produced and analysed. As a result, company can know its financial growth and on the basis of it

investors and creditors can take their decisions. Regulations relating to financial accounting are

as follows:

In financial accounting, Generally Accepted Accounting Principle's rules, standards and

procedures of can be applied by an organisation so that financial statements of

organisation can be prepare correctly. There are various principles of GAAP which are to

be followed by the organisation in order to comply with regulations relating to financial

accounting such as: principle of consistency, precedence, regularity, periodicity etc

(Khan and Mayes, 2009)

The International Financial Reporting Standards framed regulations which is to be

followed by accountant of organisation because it focuses that how a particular type of

transactions or an events can be reported in financial statements of entity (Saunders,

Cornett and McGraw, 2006).

Regulations related to financial accounting such as debit and credit and their treatment in

accounts can be follow by the accountant of organisation so that relevant information and

data can be reported in financial statements of the organisation (Barth, 2015).

As per companies act, it is compulsory to put financial statements and other necessary

documents of company in front of general public so that they can know the financial

position of company for given reporting year (Libby, Bloomfield and Nelson, 2002).

3. Accounting rules and principles

Rules for accounting

Personal Account: The rule relating to personal account state that Debit the

receiver, credit the giver. This principle has been used in case of personal accounts.

Examples of personal account are creditors, debtors, banks, capital account etc. As

well as if a person’s receive something from organisation than amount must be debit

on name of person in books of businesses

Nominal Account: The rule relating to nominal account state that Debit all expenses

and losses, credit all incomes and gains. In this account, capital account is considered

as liability for the business (DRURY, 2013). Thus it has a default credit balance.

Real Account: The rule relating to the nominal account state that Debit what comes

in, credit what goes out. The real account includes land and buildings, machineries,

plant and equipment etc. For example, if a person purchases furniture of $ 20000 in

cash, then the furniture account in business would be debit by $ 20000 and cash

account would be credit by $ 20000 in books of accounts of business.

Principles:

Dual aspect concept: Dual aspect concept refers that business entity are liable to record

all transaction on both debit and credit side of books of accounts. Whereas, single entry system

records only one aspect of business transaction which leads recording of some irrelevant

information also in books of accounts. Therefore, to avoid this problem, dual aspect principle is

introduced to assure that every business transaction needs to be recorded on both debit and credit

side of accounts (Edwards, 2013).

Cost principle: This principle assists that assets should be record in the books of accounts

at its acquiring cost. The business entity can't record the assets on revalued amount and therefore

they are obliged to record an asset on their balance sheet at cost only.

Matching principle: According to this principle, all expenses of business should be

matched with the revenues which are related to the same accounting period. The business entity

records the revenues that is, along with the expenses that brought them (Fourie and et. al., 2015).

4. The conventions and concepts relating to consistency and material disclosure

The guidelines of the accounting convention consist of practical applications of principles

of accounting. This is not a legally binding practices rather, it is a convention which is generally

accepted and based upon customs and it also provide help to accountant to resolve practical

issues which are arise in preparation and presentation of financial statements of the organisation.

Some of conventions of accounting are as follows:

well as if a person’s receive something from organisation than amount must be debit

on name of person in books of businesses

Nominal Account: The rule relating to nominal account state that Debit all expenses

and losses, credit all incomes and gains. In this account, capital account is considered

as liability for the business (DRURY, 2013). Thus it has a default credit balance.

Real Account: The rule relating to the nominal account state that Debit what comes

in, credit what goes out. The real account includes land and buildings, machineries,

plant and equipment etc. For example, if a person purchases furniture of $ 20000 in

cash, then the furniture account in business would be debit by $ 20000 and cash

account would be credit by $ 20000 in books of accounts of business.

Principles:

Dual aspect concept: Dual aspect concept refers that business entity are liable to record

all transaction on both debit and credit side of books of accounts. Whereas, single entry system

records only one aspect of business transaction which leads recording of some irrelevant

information also in books of accounts. Therefore, to avoid this problem, dual aspect principle is

introduced to assure that every business transaction needs to be recorded on both debit and credit

side of accounts (Edwards, 2013).

Cost principle: This principle assists that assets should be record in the books of accounts

at its acquiring cost. The business entity can't record the assets on revalued amount and therefore

they are obliged to record an asset on their balance sheet at cost only.

Matching principle: According to this principle, all expenses of business should be

matched with the revenues which are related to the same accounting period. The business entity

records the revenues that is, along with the expenses that brought them (Fourie and et. al., 2015).

4. The conventions and concepts relating to consistency and material disclosure

The guidelines of the accounting convention consist of practical applications of principles

of accounting. This is not a legally binding practices rather, it is a convention which is generally

accepted and based upon customs and it also provide help to accountant to resolve practical

issues which are arise in preparation and presentation of financial statements of the organisation.

Some of conventions of accounting are as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Convention of consistency: In accounts it is very important to compare results of different years

so that organisation can know growth of business in each year(s). Therefore, it is essential to

follow accounting principles and rules for similar transactions consistently and continuously. If

accounting policies are followed consistency then reliability of financial statements increased

and if accounting policies are continuously changes than reliability of financial statements can be

lost (Hale, Hale and Held, 2012). For example, if an organisation follows, cost or market price

method for valuation of stock and written down method for depreciation of fixed assets,

therefore it is necessary for company that it should follow these methods consistently and

continuously as per convention of consistency. As a result, comparison between financial

statement can be easy between different accounting years.

Convention of material disclosure: As per this convention, it is essential to disclose all

the significant financial information in the financial statements of the business entity, so that

accounts can prepare in such a manner that all material financial information has clearly disclose

to the reader. It is important for an organisation to provide all information in financial statements

so that investors, creditors and owners can know the true picture of the organisation and its

financial statements (Hall, 2012).

CLIENT 1

(a) Journal Entry in books of David Study

Date Particulars Debit Credit

01/01/

18

Premises A/c Dr. 440000

Motor Van A/c Dr. 45250

fixtures A/c Dr. 10100

Inventory A/c Dr. 40900

P Mole A/c Dr. 2200

F Lane A/c Dr. 2100

Bank A/c Dr. 42400

Cash A/c Dr. 10600

To S Hamid A/c 10150

so that organisation can know growth of business in each year(s). Therefore, it is essential to

follow accounting principles and rules for similar transactions consistently and continuously. If

accounting policies are followed consistency then reliability of financial statements increased

and if accounting policies are continuously changes than reliability of financial statements can be

lost (Hale, Hale and Held, 2012). For example, if an organisation follows, cost or market price

method for valuation of stock and written down method for depreciation of fixed assets,

therefore it is necessary for company that it should follow these methods consistently and

continuously as per convention of consistency. As a result, comparison between financial

statement can be easy between different accounting years.

Convention of material disclosure: As per this convention, it is essential to disclose all

the significant financial information in the financial statements of the business entity, so that

accounts can prepare in such a manner that all material financial information has clearly disclose

to the reader. It is important for an organisation to provide all information in financial statements

so that investors, creditors and owners can know the true picture of the organisation and its

financial statements (Hall, 2012).

CLIENT 1

(a) Journal Entry in books of David Study

Date Particulars Debit Credit

01/01/

18

Premises A/c Dr. 440000

Motor Van A/c Dr. 45250

fixtures A/c Dr. 10100

Inventory A/c Dr. 40900

P Mole A/c Dr. 2200

F Lane A/c Dr. 2100

Bank A/c Dr. 42400

Cash A/c Dr. 10600

To S Hamid A/c 10150

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To J. Brown A/c 9600

To Capital A/c (B/f) 573800

(Being Owner's Capital is calculated )

David Study's opening capital as at 1st January, 2018 is

£ 573800.

Date Particulars Debit Credit

01/01/

18

Storage cost A/c Dr. 800

To bank A/c 800

(Being storage cost is paid)

02/01/

18

Purchases A/c Dr. 7680

To S Hamid A/c 2450

To D Main A/c 2560

To W Tag A/c 1060

To R Foot A/c 1610

(Being goods purchases from various parties on credit)

03/01/

18

J Wilson A/c Dr. 2020

T Cole A/c Dr. 1840

F Seema A/c Dr. 2380

J Allen A/c Dr. 990

P White A/c Dr. 2820

F Lane A/c Dr. 1170

To Sales A/c 11220

To Capital A/c (B/f) 573800

(Being Owner's Capital is calculated )

David Study's opening capital as at 1st January, 2018 is

£ 573800.

Date Particulars Debit Credit

01/01/

18

Storage cost A/c Dr. 800

To bank A/c 800

(Being storage cost is paid)

02/01/

18

Purchases A/c Dr. 7680

To S Hamid A/c 2450

To D Main A/c 2560

To W Tag A/c 1060

To R Foot A/c 1610

(Being goods purchases from various parties on credit)

03/01/

18

J Wilson A/c Dr. 2020

T Cole A/c Dr. 1840

F Seema A/c Dr. 2380

J Allen A/c Dr. 990

P White A/c Dr. 2820

F Lane A/c Dr. 1170

To Sales A/c 11220

(Being goods sold to various parties on credit)

04/01/

18

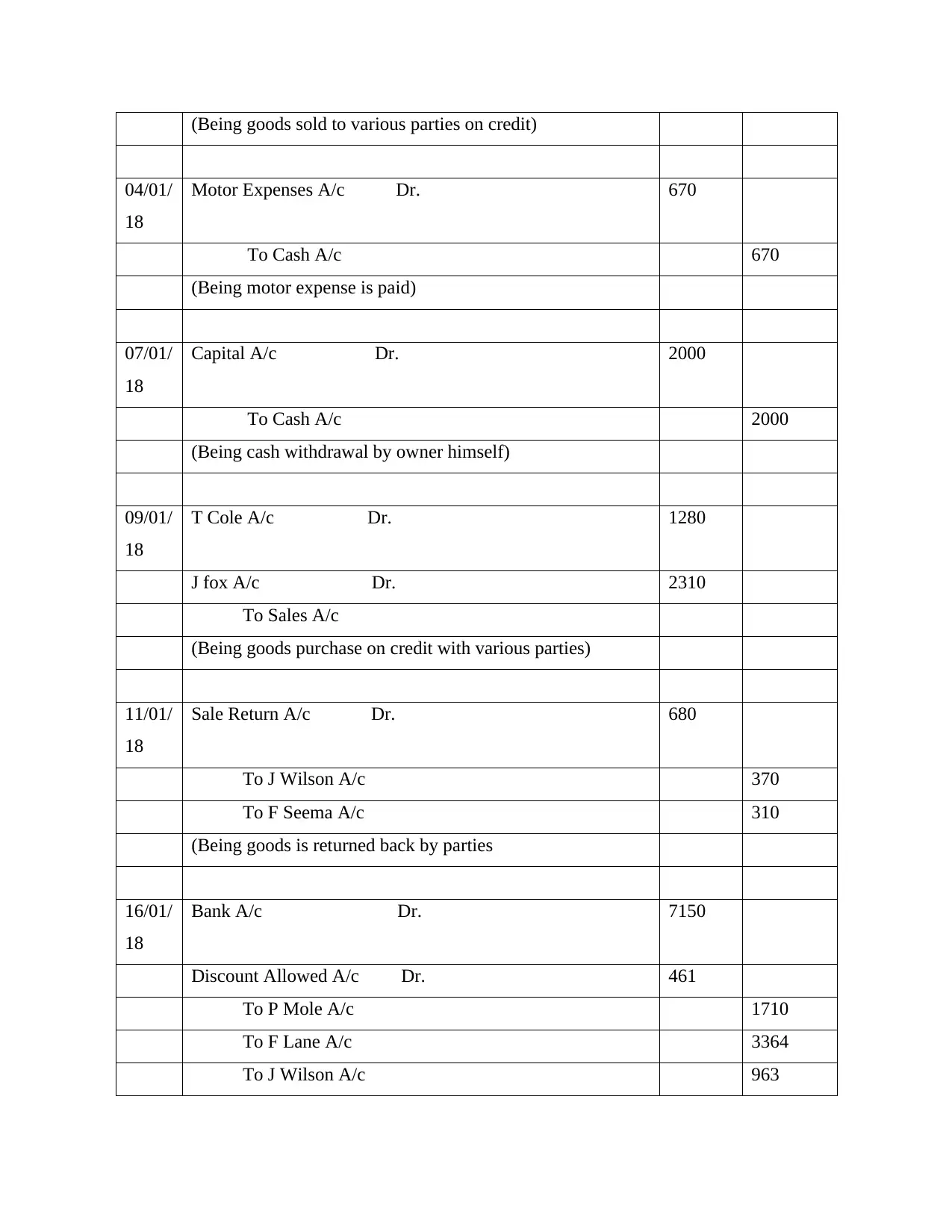

Motor Expenses A/c Dr. 670

To Cash A/c 670

(Being motor expense is paid)

07/01/

18

Capital A/c Dr. 2000

To Cash A/c 2000

(Being cash withdrawal by owner himself)

09/01/

18

T Cole A/c Dr. 1280

J fox A/c Dr. 2310

To Sales A/c

(Being goods purchase on credit with various parties)

11/01/

18

Sale Return A/c Dr. 680

To J Wilson A/c 370

To F Seema A/c 310

(Being goods is returned back by parties

16/01/

18

Bank A/c Dr. 7150

Discount Allowed A/c Dr. 461

To P Mole A/c 1710

To F Lane A/c 3364

To J Wilson A/c 963

04/01/

18

Motor Expenses A/c Dr. 670

To Cash A/c 670

(Being motor expense is paid)

07/01/

18

Capital A/c Dr. 2000

To Cash A/c 2000

(Being cash withdrawal by owner himself)

09/01/

18

T Cole A/c Dr. 1280

J fox A/c Dr. 2310

To Sales A/c

(Being goods purchase on credit with various parties)

11/01/

18

Sale Return A/c Dr. 680

To J Wilson A/c 370

To F Seema A/c 310

(Being goods is returned back by parties

16/01/

18

Bank A/c Dr. 7150

Discount Allowed A/c Dr. 461

To P Mole A/c 1710

To F Lane A/c 3364

To J Wilson A/c 963

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

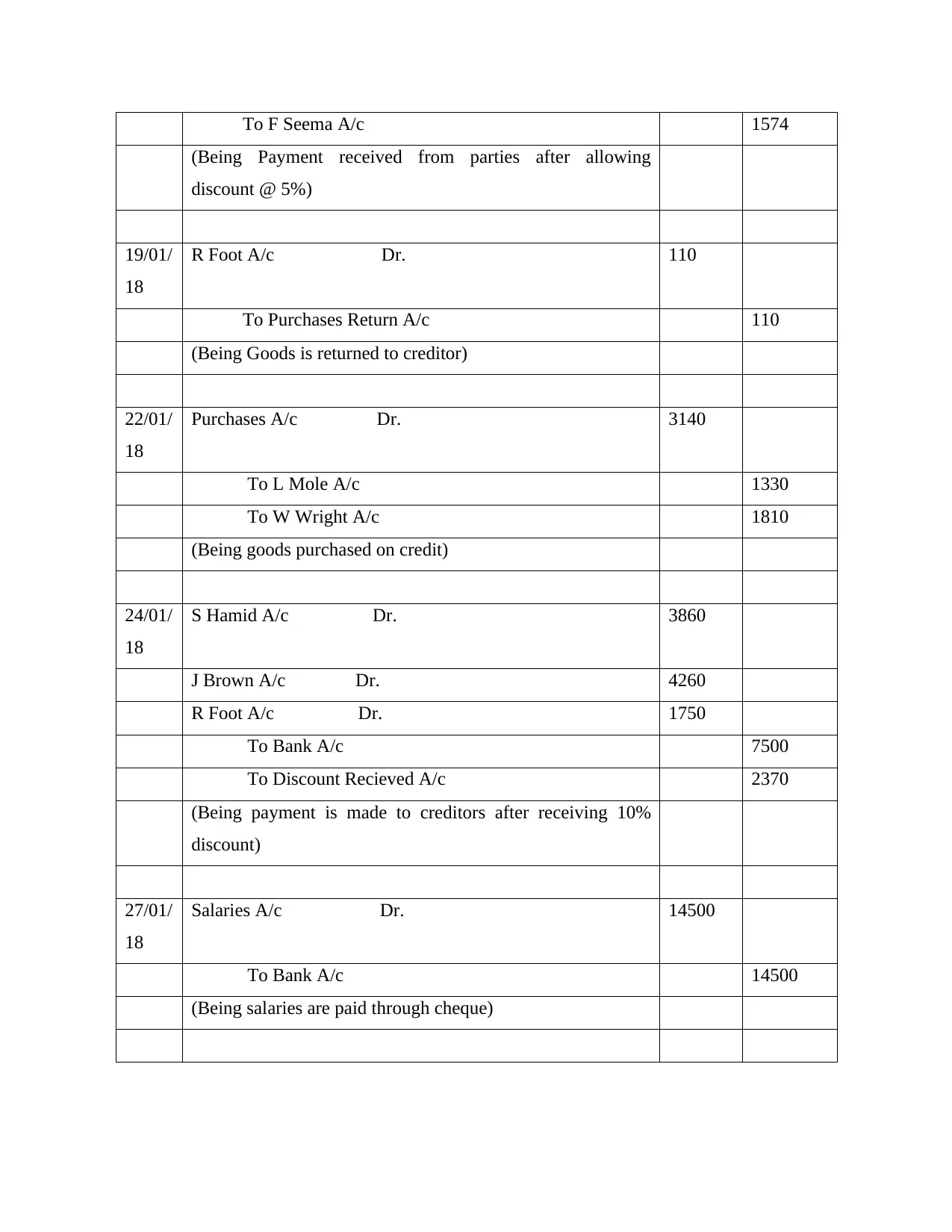

To F Seema A/c 1574

(Being Payment received from parties after allowing

discount @ 5%)

19/01/

18

R Foot A/c Dr. 110

To Purchases Return A/c 110

(Being Goods is returned to creditor)

22/01/

18

Purchases A/c Dr. 3140

To L Mole A/c 1330

To W Wright A/c 1810

(Being goods purchased on credit)

24/01/

18

S Hamid A/c Dr. 3860

J Brown A/c Dr. 4260

R Foot A/c Dr. 1750

To Bank A/c 7500

To Discount Recieved A/c 2370

(Being payment is made to creditors after receiving 10%

discount)

27/01/

18

Salaries A/c Dr. 14500

To Bank A/c 14500

(Being salaries are paid through cheque)

(Being Payment received from parties after allowing

discount @ 5%)

19/01/

18

R Foot A/c Dr. 110

To Purchases Return A/c 110

(Being Goods is returned to creditor)

22/01/

18

Purchases A/c Dr. 3140

To L Mole A/c 1330

To W Wright A/c 1810

(Being goods purchased on credit)

24/01/

18

S Hamid A/c Dr. 3860

J Brown A/c Dr. 4260

R Foot A/c Dr. 1750

To Bank A/c 7500

To Discount Recieved A/c 2370

(Being payment is made to creditors after receiving 10%

discount)

27/01/

18

Salaries A/c Dr. 14500

To Bank A/c 14500

(Being salaries are paid through cheque)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

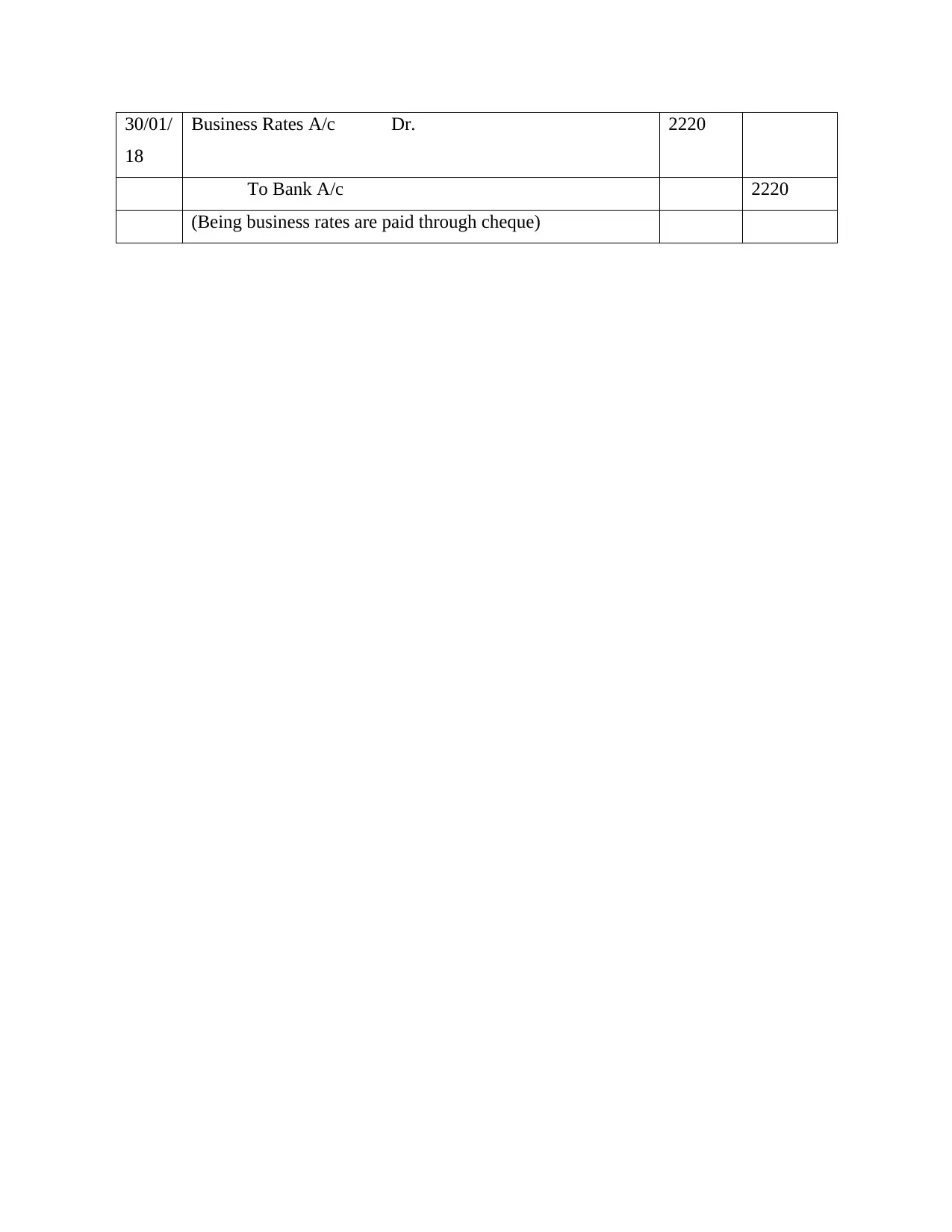

30/01/

18

Business Rates A/c Dr. 2220

To Bank A/c 2220

(Being business rates are paid through cheque)

18

Business Rates A/c Dr. 2220

To Bank A/c 2220

(Being business rates are paid through cheque)

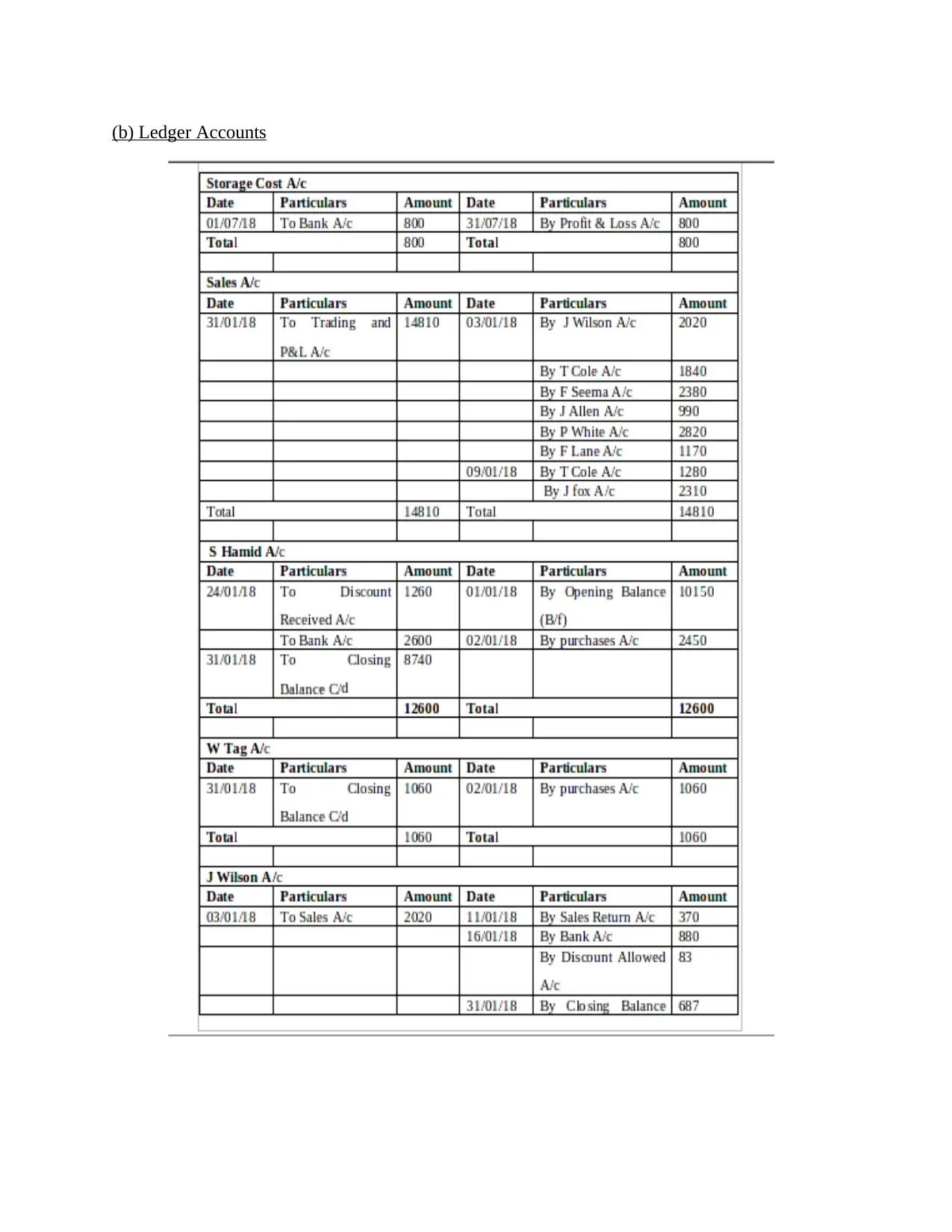

(b) Ledger Accounts

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.