Accounting Fundamentals Assignment: Income Statement and Balance Sheet

VerifiedAdded on 2023/06/08

|10

|2749

|169

Homework Assignment

AI Summary

This assignment delves into the core principles of accounting, focusing on the preparation of financial statements. It begins with the creation of an income statement and balance sheet based on provided trial balance data. The assignment then transitions to a detailed discussion of crucial accounting principles, such as the business entity concept, money measurement concept, dual aspect concept, going concern, cost concept, matching concept, realization concept, accrual concept, revenue recognition principle, economic entity principle, monetary unit principle and reliability principle. Furthermore, it covers the four main accounting conventions: conservatism, consistency, materiality, and full disclosure. The aim is to provide a comprehensive understanding of how these principles and conventions shape the recording, interpretation, and communication of financial information, ultimately aiding in informed decision-making.

Accounting

Fundamentals

Fundamentals

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

1.a) Prepare income statement.....................................................................................................3

1.b) Prepare Balance sheet...........................................................................................................3

2. Discuss the accounting principles and their usage in the financial statements........................4

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

1.a) Prepare income statement.....................................................................................................3

1.b) Prepare Balance sheet...........................................................................................................3

2. Discuss the accounting principles and their usage in the financial statements........................4

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Accounting principles provides framework for maintaining books of accounts for

business entity. It facilitates decision making process and helps in analysis and interpretation of

records. Whenever the books of accounts are prepared theses are to be considered mandatorily

(Churyk Reinstein and Smith, 2018). In this report, Angela 's a business entity's trial balance is

given based on which income statement and balance sheet for the organisation have to be

prepared. The relevance of accounting standards and concepts such as going concern, dual

aspect, business entity etc. will be defined to have a better understanding of how accounting is

done.

MAIN BODY

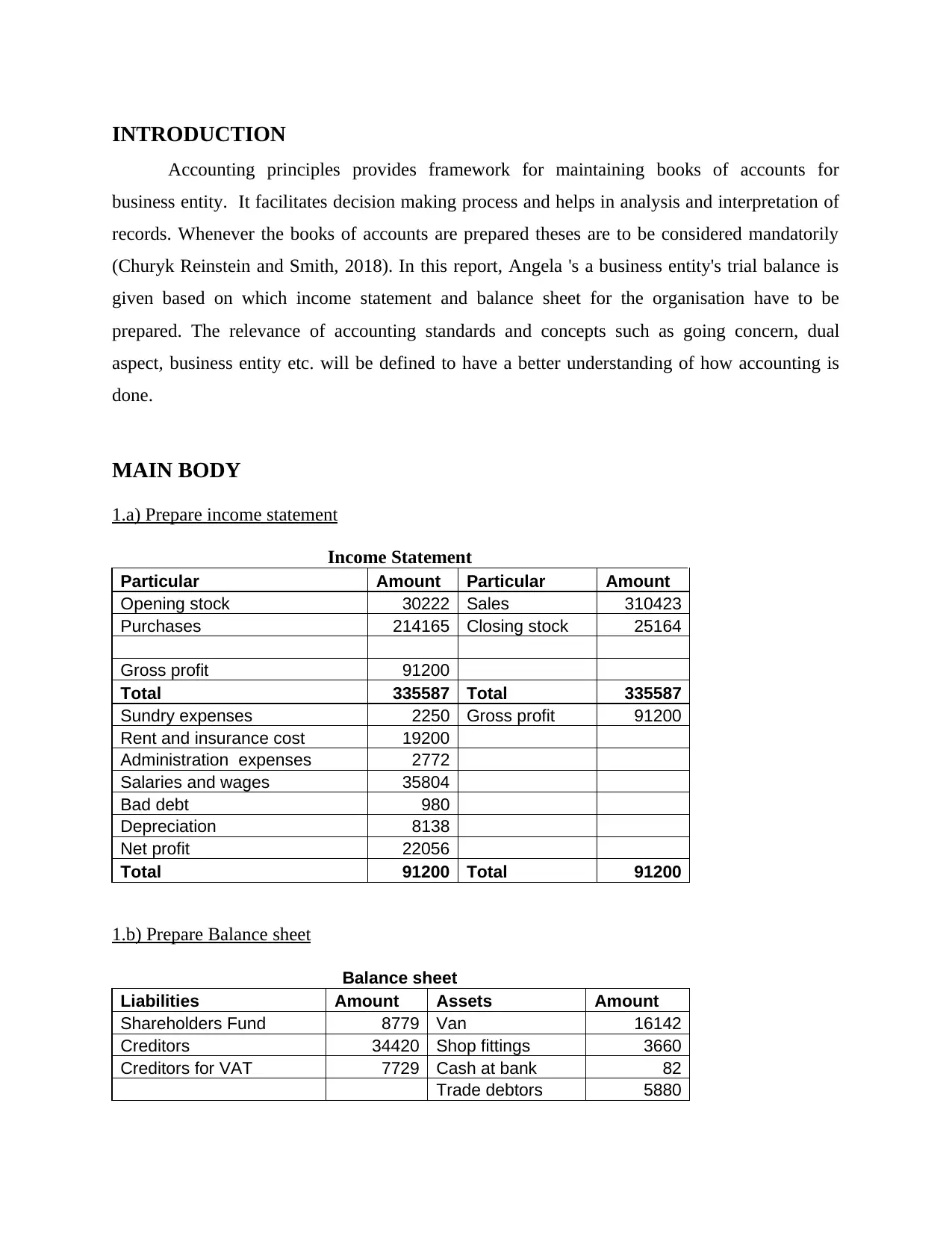

1.a) Prepare income statement

Income Statement

Particular Amount Particular Amount

Opening stock 30222 Sales 310423

Purchases 214165 Closing stock 25164

Gross profit 91200

Total 335587 Total 335587

Sundry expenses 2250 Gross profit 91200

Rent and insurance cost 19200

Administration expenses 2772

Salaries and wages 35804

Bad debt 980

Depreciation 8138

Net profit 22056

Total 91200 Total 91200

1.b) Prepare Balance sheet

Balance sheet

Liabilities Amount Assets Amount

Shareholders Fund 8779 Van 16142

Creditors 34420 Shop fittings 3660

Creditors for VAT 7729 Cash at bank 82

Trade debtors 5880

Accounting principles provides framework for maintaining books of accounts for

business entity. It facilitates decision making process and helps in analysis and interpretation of

records. Whenever the books of accounts are prepared theses are to be considered mandatorily

(Churyk Reinstein and Smith, 2018). In this report, Angela 's a business entity's trial balance is

given based on which income statement and balance sheet for the organisation have to be

prepared. The relevance of accounting standards and concepts such as going concern, dual

aspect, business entity etc. will be defined to have a better understanding of how accounting is

done.

MAIN BODY

1.a) Prepare income statement

Income Statement

Particular Amount Particular Amount

Opening stock 30222 Sales 310423

Purchases 214165 Closing stock 25164

Gross profit 91200

Total 335587 Total 335587

Sundry expenses 2250 Gross profit 91200

Rent and insurance cost 19200

Administration expenses 2772

Salaries and wages 35804

Bad debt 980

Depreciation 8138

Net profit 22056

Total 91200 Total 91200

1.b) Prepare Balance sheet

Balance sheet

Liabilities Amount Assets Amount

Shareholders Fund 8779 Van 16142

Creditors 34420 Shop fittings 3660

Creditors for VAT 7729 Cash at bank 82

Trade debtors 5880

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

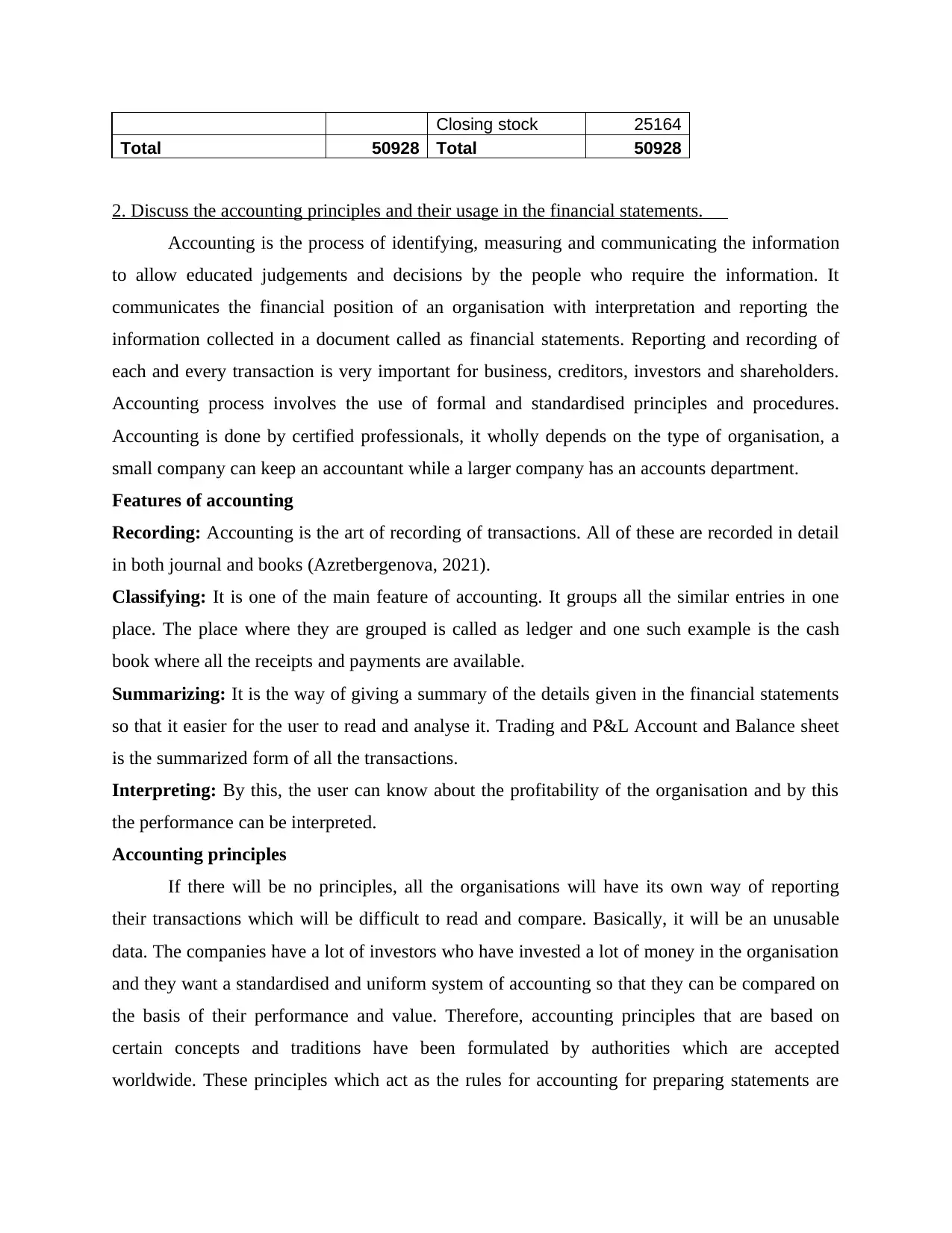

Closing stock 25164

Total 50928 Total 50928

2. Discuss the accounting principles and their usage in the financial statements.

Accounting is the process of identifying, measuring and communicating the information

to allow educated judgements and decisions by the people who require the information. It

communicates the financial position of an organisation with interpretation and reporting the

information collected in a document called as financial statements. Reporting and recording of

each and every transaction is very important for business, creditors, investors and shareholders.

Accounting process involves the use of formal and standardised principles and procedures.

Accounting is done by certified professionals, it wholly depends on the type of organisation, a

small company can keep an accountant while a larger company has an accounts department.

Features of accounting

Recording: Accounting is the art of recording of transactions. All of these are recorded in detail

in both journal and books (Azretbergenova, 2021).

Classifying: It is one of the main feature of accounting. It groups all the similar entries in one

place. The place where they are grouped is called as ledger and one such example is the cash

book where all the receipts and payments are available.

Summarizing: It is the way of giving a summary of the details given in the financial statements

so that it easier for the user to read and analyse it. Trading and P&L Account and Balance sheet

is the summarized form of all the transactions.

Interpreting: By this, the user can know about the profitability of the organisation and by this

the performance can be interpreted.

Accounting principles

If there will be no principles, all the organisations will have its own way of reporting

their transactions which will be difficult to read and compare. Basically, it will be an unusable

data. The companies have a lot of investors who have invested a lot of money in the organisation

and they want a standardised and uniform system of accounting so that they can be compared on

the basis of their performance and value. Therefore, accounting principles that are based on

certain concepts and traditions have been formulated by authorities which are accepted

worldwide. These principles which act as the rules for accounting for preparing statements are

Total 50928 Total 50928

2. Discuss the accounting principles and their usage in the financial statements.

Accounting is the process of identifying, measuring and communicating the information

to allow educated judgements and decisions by the people who require the information. It

communicates the financial position of an organisation with interpretation and reporting the

information collected in a document called as financial statements. Reporting and recording of

each and every transaction is very important for business, creditors, investors and shareholders.

Accounting process involves the use of formal and standardised principles and procedures.

Accounting is done by certified professionals, it wholly depends on the type of organisation, a

small company can keep an accountant while a larger company has an accounts department.

Features of accounting

Recording: Accounting is the art of recording of transactions. All of these are recorded in detail

in both journal and books (Azretbergenova, 2021).

Classifying: It is one of the main feature of accounting. It groups all the similar entries in one

place. The place where they are grouped is called as ledger and one such example is the cash

book where all the receipts and payments are available.

Summarizing: It is the way of giving a summary of the details given in the financial statements

so that it easier for the user to read and analyse it. Trading and P&L Account and Balance sheet

is the summarized form of all the transactions.

Interpreting: By this, the user can know about the profitability of the organisation and by this

the performance can be interpreted.

Accounting principles

If there will be no principles, all the organisations will have its own way of reporting

their transactions which will be difficult to read and compare. Basically, it will be an unusable

data. The companies have a lot of investors who have invested a lot of money in the organisation

and they want a standardised and uniform system of accounting so that they can be compared on

the basis of their performance and value. Therefore, accounting principles that are based on

certain concepts and traditions have been formulated by authorities which are accepted

worldwide. These principles which act as the rules for accounting for preparing statements are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

known as “Generally Accepted Accounting Principles” or GAAP. The usage of these makes the

statements more reliable (Aldeia, 2021).

Accounting concepts

Business entity concept: A business and its owner are two different entities and their

financial transactions are also different. By doing this, separate accounts for business

excluding assets and liabilities of any other entity or the owner. Without this concept,

records of a number of entities will get mixed which will make it difficult to find taxable

results of a business. There are a lot of reasons to validate this concept like tracking taxes

separately, financial performance and the position of the business. If an organisation gets

liquidated, this concept will help in the calculation of payout to various owners. The most

important reason being, it will not be possible to audit if the accounts are mixed with

other entities.

Money measurement concept: Only the transactions that can be expressed in money

terms has to be recorded in accounting, although the other transactions can be provided

separately outside the statements. This means that only quantitative transactions can be

recorded. Examples of items that cannot be recorded include, skill level of employees,

product durability, the efficiency of administration, etc. since these transactions cannot be

quantified, hence they will not be recorded. The biggest flaw is that a lot of factors can

cause long term changes in the financial results or financial position of a business but this

concept does not allow it to be stated in financial statements (Edwards, 2019).

Dual concept: For every entry, the transaction is recorded twice, once on the debit side

and once on the credit side without this the transaction is incomplete. The concept is

derived from the accounting equation is as follows

Assets = Liabilities + Equity

Going concern: According to accounting, a business is supposed to go on for a long

time, this means that the business will not be forced to shut and liquidate its assets at

cheaper prices. If the accountant feels that the business will no longer be able to sustain

which raises the issue of whether the assets or obsolete for which the liquidation value

will have to be calculated. The auditor looks at negative trends in results, default of loan

or legal proceedings to determine the going concern of the company. In these cases, it

statements more reliable (Aldeia, 2021).

Accounting concepts

Business entity concept: A business and its owner are two different entities and their

financial transactions are also different. By doing this, separate accounts for business

excluding assets and liabilities of any other entity or the owner. Without this concept,

records of a number of entities will get mixed which will make it difficult to find taxable

results of a business. There are a lot of reasons to validate this concept like tracking taxes

separately, financial performance and the position of the business. If an organisation gets

liquidated, this concept will help in the calculation of payout to various owners. The most

important reason being, it will not be possible to audit if the accounts are mixed with

other entities.

Money measurement concept: Only the transactions that can be expressed in money

terms has to be recorded in accounting, although the other transactions can be provided

separately outside the statements. This means that only quantitative transactions can be

recorded. Examples of items that cannot be recorded include, skill level of employees,

product durability, the efficiency of administration, etc. since these transactions cannot be

quantified, hence they will not be recorded. The biggest flaw is that a lot of factors can

cause long term changes in the financial results or financial position of a business but this

concept does not allow it to be stated in financial statements (Edwards, 2019).

Dual concept: For every entry, the transaction is recorded twice, once on the debit side

and once on the credit side without this the transaction is incomplete. The concept is

derived from the accounting equation is as follows

Assets = Liabilities + Equity

Going concern: According to accounting, a business is supposed to go on for a long

time, this means that the business will not be forced to shut and liquidate its assets at

cheaper prices. If the accountant feels that the business will no longer be able to sustain

which raises the issue of whether the assets or obsolete for which the liquidation value

will have to be calculated. The auditor looks at negative trends in results, default of loan

or legal proceedings to determine the going concern of the company. In these cases, it

will be evaluated for a period of one year following the date of preparation of financial

statements.

Cost concept: The fixed assets are to be recorded on the cost they were bought in the

first year of accounting. After which they are recorded on the price less depreciation.

Market price is not considered. This applies to fixed assets only. Although this concept is

becoming less valid because accounting standards are moving towards adjusting assets on

their fair value. If a cost has not yet been consumed, it will be recorded in the balance

sheet. If it has been consumed, it will be recorded in income statement. This cost is

usually recorded through the payables system or through journal entries (Karwowski,

2018).

Accounting year concept: Each and every organisation has to choose a business cycle

for example, monthly, quarterly or yearly as per a fiscal or calendar year. One exception

to it can be when a business has just been started so the accounting period can maybe a

few days. For a public company the accounting period is 3 months.

Matching concept: It states that whenever an expense is recorded an equal amount of

revenue should also be recorded in the accounting process to correctly calculate profit or

loss. It is one of the most crucial concept in accrual basis of accounting since it makes it

compulsory to record transactions in the same period. This will ensure that the profits are

not overvalued.

Realisation concept: Profit is recognised only when it is earned. An advance will not be

considered as a profit until the goods or services have successfully been delivered. The

realisation concept is sometimes misused to accelerate revenue (Richard and Rambaud,

2021).

Accrual concept: It is the concept of recording revenues when they are earned and

expenses when they are incurred. It impacts the balance sheet when receivables and

payables are recorded without cash receipt or payment. The accrual basis is accepted by

both GAAP and IFRS. These frameworks provide help in guiding how to record

transactions without receipt. The major problem with this concept is that it can show

profits even when the cash flows have not happened. The company might be profitable in

books but doesn't have cash which can cause bankruptcy. Special attention should be

statements.

Cost concept: The fixed assets are to be recorded on the cost they were bought in the

first year of accounting. After which they are recorded on the price less depreciation.

Market price is not considered. This applies to fixed assets only. Although this concept is

becoming less valid because accounting standards are moving towards adjusting assets on

their fair value. If a cost has not yet been consumed, it will be recorded in the balance

sheet. If it has been consumed, it will be recorded in income statement. This cost is

usually recorded through the payables system or through journal entries (Karwowski,

2018).

Accounting year concept: Each and every organisation has to choose a business cycle

for example, monthly, quarterly or yearly as per a fiscal or calendar year. One exception

to it can be when a business has just been started so the accounting period can maybe a

few days. For a public company the accounting period is 3 months.

Matching concept: It states that whenever an expense is recorded an equal amount of

revenue should also be recorded in the accounting process to correctly calculate profit or

loss. It is one of the most crucial concept in accrual basis of accounting since it makes it

compulsory to record transactions in the same period. This will ensure that the profits are

not overvalued.

Realisation concept: Profit is recognised only when it is earned. An advance will not be

considered as a profit until the goods or services have successfully been delivered. The

realisation concept is sometimes misused to accelerate revenue (Richard and Rambaud,

2021).

Accrual concept: It is the concept of recording revenues when they are earned and

expenses when they are incurred. It impacts the balance sheet when receivables and

payables are recorded without cash receipt or payment. The accrual basis is accepted by

both GAAP and IFRS. These frameworks provide help in guiding how to record

transactions without receipt. The major problem with this concept is that it can show

profits even when the cash flows have not happened. The company might be profitable in

books but doesn't have cash which can cause bankruptcy. Special attention should be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

given to the cash flows to determine the flows of cash in and out of business (Maffei,

Casciello and Meucci, 2021).

Revenue recognition principle: It states that the revenue should be recorded when it has

been earned and not when it is collected. Realizable means that goods and services have

been received but payment will be done later. According to the accrual concept, if a

payment is received in advance, then it is recorded as a liability.

Economic entity principle: This principal suggests that business and the owner have to

treated as separate legal entity. The owners, partners or any related business finance are

to kept different from the organisation's transaction. This should be taken into

consideration for all the organisations irrespective of their structure and type. This

principal helps in ensuring that stakeholders interest is not comprised. Since there might

chances when owners try to fulfil his personal liabilities through company's assets.

Monetary unit principle: This accounting concepts tools, defines that transaction that

are to be recorded in the books of accounts should be monetary. The currency unit of the

transaction is the only way by which the transactions can be entered in financial records.

This applies to each and every organisation existing in the economy. An organisation

cannot journalize the qualitative skills of employees like motivation provided and

appreciation given to anyone inside the organisation's. This concept also takes into

account that the worth of the unit of currency which used to record the transaction

remains stable for a given period of time (Oncioiu, 2021).

Reliability principle: In this concept it is said that only transaction against which

existence proof is provided is to be recorded. These are basically receipts and bills which

acknowledges that a transaction took place. This is very important principal when

transparency and fairness of the books of the accounts are questioned. It also helps in

auditing process and justify the actions took place. It is a bit of problematic when

transactions like reserves, allowance, contingent events and doubtful are to be accounted.

Accounting conventions

The four main conventions used in accounting are as follows:

1. Conservatism is the convention that states that when a transaction has two values the

lower value is considered and recorded. The profit should never be overestimated and a

provision for losses should be made. The expenses and liabilities should be recorded as

Casciello and Meucci, 2021).

Revenue recognition principle: It states that the revenue should be recorded when it has

been earned and not when it is collected. Realizable means that goods and services have

been received but payment will be done later. According to the accrual concept, if a

payment is received in advance, then it is recorded as a liability.

Economic entity principle: This principal suggests that business and the owner have to

treated as separate legal entity. The owners, partners or any related business finance are

to kept different from the organisation's transaction. This should be taken into

consideration for all the organisations irrespective of their structure and type. This

principal helps in ensuring that stakeholders interest is not comprised. Since there might

chances when owners try to fulfil his personal liabilities through company's assets.

Monetary unit principle: This accounting concepts tools, defines that transaction that

are to be recorded in the books of accounts should be monetary. The currency unit of the

transaction is the only way by which the transactions can be entered in financial records.

This applies to each and every organisation existing in the economy. An organisation

cannot journalize the qualitative skills of employees like motivation provided and

appreciation given to anyone inside the organisation's. This concept also takes into

account that the worth of the unit of currency which used to record the transaction

remains stable for a given period of time (Oncioiu, 2021).

Reliability principle: In this concept it is said that only transaction against which

existence proof is provided is to be recorded. These are basically receipts and bills which

acknowledges that a transaction took place. This is very important principal when

transparency and fairness of the books of the accounts are questioned. It also helps in

auditing process and justify the actions took place. It is a bit of problematic when

transactions like reserves, allowance, contingent events and doubtful are to be accounted.

Accounting conventions

The four main conventions used in accounting are as follows:

1. Conservatism is the convention that states that when a transaction has two values the

lower value is considered and recorded. The profit should never be overestimated and a

provision for losses should be made. The expenses and liabilities should be recorded as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and when they arise while the revenues and assets should be recorded only when the

business is sure that it will occur. If there is uncertainty with incurring of loss, always

record the loss and if there is uncertainty about gains, do not record it (Oulasvirta, 2019).

2. Consistency states that the same accounting principles should be followed from one

period to another so that the profit can be compared with the same standards being used.

Not following this will mean that the business is going to switch between different

accounting treatments which will make analysing its long term financial position very

difficult. Auditors are usually concerned with this principle, to have comparable results.

This is often ignored when the management is trying to show more of revenue.

3. Materiality means, all the material facts should be recorded in accounting. Accountants

should record all the relevant information and ignore the irrelevant data. If any data that

can influence the decision of stakeholders is said to be material. This concept allows the

company to ignore some standards in order to improve efficiency (Partalidou, 2020).

4. Full disclosure, as the name suggests revealing all the information both the favourable as

well as unfavourable which can be of use for the stakeholders. The interpretation of this

principle is highly subjective as the amount of information is huge. So only disclose those

items that can have a material impact on the company's position. Lawsuit or dispute of

tax, these cannot be quantified but still they are disclosed. This also include reporting

existing policies as well as any change in those policies.

CONCLUSION

For the above stated report, Angela's final statements were prepared i.e. income

statements and balance sheet were made from the trial balance given in the case. Moreover, the

accounting concepts, assumptions and rules help in understanding the book of accounts of the

organisation. The concepts are to be mandatorily followed while preparing the records. The

process of recording, posting and analysis are based on the concepts. For fair, transparent and

preparation of accounts of the company accounting principles are to be considered.

business is sure that it will occur. If there is uncertainty with incurring of loss, always

record the loss and if there is uncertainty about gains, do not record it (Oulasvirta, 2019).

2. Consistency states that the same accounting principles should be followed from one

period to another so that the profit can be compared with the same standards being used.

Not following this will mean that the business is going to switch between different

accounting treatments which will make analysing its long term financial position very

difficult. Auditors are usually concerned with this principle, to have comparable results.

This is often ignored when the management is trying to show more of revenue.

3. Materiality means, all the material facts should be recorded in accounting. Accountants

should record all the relevant information and ignore the irrelevant data. If any data that

can influence the decision of stakeholders is said to be material. This concept allows the

company to ignore some standards in order to improve efficiency (Partalidou, 2020).

4. Full disclosure, as the name suggests revealing all the information both the favourable as

well as unfavourable which can be of use for the stakeholders. The interpretation of this

principle is highly subjective as the amount of information is huge. So only disclose those

items that can have a material impact on the company's position. Lawsuit or dispute of

tax, these cannot be quantified but still they are disclosed. This also include reporting

existing policies as well as any change in those policies.

CONCLUSION

For the above stated report, Angela's final statements were prepared i.e. income

statements and balance sheet were made from the trial balance given in the case. Moreover, the

accounting concepts, assumptions and rules help in understanding the book of accounts of the

organisation. The concepts are to be mandatorily followed while preparing the records. The

process of recording, posting and analysis are based on the concepts. For fair, transparent and

preparation of accounts of the company accounting principles are to be considered.

REFERENCES

Books and Journals

Aldeia, S., 2021. THE ACCOUNTING PROFIT'S RELEVANCE IN COLLECTING TAX

REVENUE OF SPAIN. Journal of Legal, Ethical and Regulatory Issues. 24, pp.1-7.

Azretbergenova, E.E.G., 2021. COST ACCOUNTING IN SMALL AND MEDIUM

MANUFACTURING ENTERPRISES. Journal of science. Lyon. (18) .pp.3-5.

Churyk, N.T., Reinstein, A. and Smith, L., 2018. Jones Enterprises Real Estate Investment Trust:

Comparing US and Canadian Acquisition Accounting, Balance Sheet and Security

Commission Reporting, and Initial Public Offering Location. Issues in Accounting

Education. 33(2).pp.35-42.

Edwards, J.R., 2019. Accounting for the erosion of fixed assets 1863–1900. A case

study. Accounting History Review. 29(2).pp.287-304.

Karwowski, M., 2018, May. Materiality in Financial Accounting—Theory and Practice.

In Annual Conference on Finance and Accounting (pp. 199-209). Springer, Cham.

Maffei, M., Casciello, R. and Meucci, F., 2021. Blockchain technology: uninvestigated issues

emerging from an integrated view within accounting and auditing practices. Journal of

Organizational Change Management.

Oncioiu, I., 2021. The Potential Role of Intellectual Capital in the Process of Accounting

Convergence. In Encyclopedia of Organizational Knowledge, Administration, and

Technology (pp. 12-23). IGI Global.

Oulasvirta, L., 2019. Theoretical approaches to financial accounting purposes and principles.

Partalidou, X., 2020. Financial accounting, auditing and environmental behavior of socially

responsible companies (Doctoral dissertation, Δημοκρίτειο Πανεπιστήμιο Θράκης

(ΔΠΘ). Σχολή Επιστημών Γεωπονίας και Δασολογίας. Τμήμα Αγροτικής Ανάπτυξης.

Τομέας Αγροτικής Οικονομίας και Διοίκησης Αγροτικών Επιχειρήσεων).

Richard, J. and Rambaud, A., 2021. Capital in the History of Accounting and Economic

Thought: Capitalism, Ecology, and Democracy. Routledge.

Sava, R., 2018, May. Innovative teaching strategies in accounting. In International Economic

Conference of Sibiu (pp. 323-329). Springer, Cham.

Books and Journals

Aldeia, S., 2021. THE ACCOUNTING PROFIT'S RELEVANCE IN COLLECTING TAX

REVENUE OF SPAIN. Journal of Legal, Ethical and Regulatory Issues. 24, pp.1-7.

Azretbergenova, E.E.G., 2021. COST ACCOUNTING IN SMALL AND MEDIUM

MANUFACTURING ENTERPRISES. Journal of science. Lyon. (18) .pp.3-5.

Churyk, N.T., Reinstein, A. and Smith, L., 2018. Jones Enterprises Real Estate Investment Trust:

Comparing US and Canadian Acquisition Accounting, Balance Sheet and Security

Commission Reporting, and Initial Public Offering Location. Issues in Accounting

Education. 33(2).pp.35-42.

Edwards, J.R., 2019. Accounting for the erosion of fixed assets 1863–1900. A case

study. Accounting History Review. 29(2).pp.287-304.

Karwowski, M., 2018, May. Materiality in Financial Accounting—Theory and Practice.

In Annual Conference on Finance and Accounting (pp. 199-209). Springer, Cham.

Maffei, M., Casciello, R. and Meucci, F., 2021. Blockchain technology: uninvestigated issues

emerging from an integrated view within accounting and auditing practices. Journal of

Organizational Change Management.

Oncioiu, I., 2021. The Potential Role of Intellectual Capital in the Process of Accounting

Convergence. In Encyclopedia of Organizational Knowledge, Administration, and

Technology (pp. 12-23). IGI Global.

Oulasvirta, L., 2019. Theoretical approaches to financial accounting purposes and principles.

Partalidou, X., 2020. Financial accounting, auditing and environmental behavior of socially

responsible companies (Doctoral dissertation, Δημοκρίτειο Πανεπιστήμιο Θράκης

(ΔΠΘ). Σχολή Επιστημών Γεωπονίας και Δασολογίας. Τμήμα Αγροτικής Ανάπτυξης.

Τομέας Αγροτικής Οικονομίας και Διοίκησης Αγροτικών Επιχειρήσεων).

Richard, J. and Rambaud, A., 2021. Capital in the History of Accounting and Economic

Thought: Capitalism, Ecology, and Democracy. Routledge.

Sava, R., 2018, May. Innovative teaching strategies in accounting. In International Economic

Conference of Sibiu (pp. 323-329). Springer, Cham.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tohirovich, Q.N., 2021. International financial accounting standards in

Uzbekistan. ACADEMICIA: An International Multidisciplinary Research

Journal. 11(4).pp.328-333.

Uzbekistan. ACADEMICIA: An International Multidisciplinary Research

Journal. 11(4).pp.328-333.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.