Accounting Principles: Budgetary Control, Ethics and Ratio Analysis

VerifiedAdded on 2023/06/07

|23

|4996

|489

Report

AI Summary

This report delves into the crucial role of accounting principles within organizations, emphasizing their importance in tracking income, expenditures, costs, and revenue generation. It highlights the purpose and scope of accounting functions in complex operating environments, including maintaining financial records, observing financial transactions, maintaining digital records, making financial projections, and ensuring legal compliance. The report evaluates the accounting function's role in informing decision-making and meeting stakeholder expectations, discussing the main branches of accounting such as financial, cost, managerial, and tax accounting, along with necessary job skills and competencies. It also addresses the impact of technology on modern accounting systems, ethical and regulatory issues, and the evaluation of budgets and budgetary control. Furthermore, the report includes the calculation and critical evaluation of key performance ratios to assess business performance, concluding with the benefits of contemporary accounting software in preparing financial statements. The document is available on Desklib, a platform offering a wide range of study resources for students.

Accounting Principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

SECTION 1......................................................................................................................................3

The purpose and scope of accounting in complex operating environments................................3

Evaluate the accounting function in informing decision making and meeting stakeholder and societal needs and expectations.

......................................................................................................................................................4

The main branches of accounting and job skill sets and competencies.......................................5

Accounting systems and the role of technology in modern-day accounting...............................5

Issues of ethics, regulation and compliance and the extent to which they are constraints or threats to the organisation. 5

Evaluate role of budgets and budgetary control and their advantages and disadvantages and how can they assist to identify problems

at business....................................................................................................................................6

Calculation of comparative key performance ratios such as profitably, liquidity, asset usage and investment ratios. 8

Critical evaluation of the performance to the business year on year ........................................10

The benefits of contemporary accounting software packages and how they are used preparing financial statements. 12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

SECTION 1......................................................................................................................................3

The purpose and scope of accounting in complex operating environments................................3

Evaluate the accounting function in informing decision making and meeting stakeholder and societal needs and expectations.

......................................................................................................................................................4

The main branches of accounting and job skill sets and competencies.......................................5

Accounting systems and the role of technology in modern-day accounting...............................5

Issues of ethics, regulation and compliance and the extent to which they are constraints or threats to the organisation. 5

Evaluate role of budgets and budgetary control and their advantages and disadvantages and how can they assist to identify problems

at business....................................................................................................................................6

Calculation of comparative key performance ratios such as profitably, liquidity, asset usage and investment ratios. 8

Critical evaluation of the performance to the business year on year ........................................10

The benefits of contemporary accounting software packages and how they are used preparing financial statements. 12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Accounting as a subject plays a very crucial role in the workings of an organisation as it assists the businesses in tracking upon

the incomes, expenditures, costs and the revenues being generated in the organisation. It helps to prepare and manage the accounting

information’s with the assistance of various accounting functions provided by the business (Yang and et.al., 2021). In this report, the

importance and purpose of accounting functions is explained while also giving an overview of the accounting functions that exists in

an organisation. The report consists of the preparation of various necessary financial accounts of the business such as cash budgets,

financial accounting ratios and the analysis of those financial ratios to provide an overview of the financial situation of the

organisation. The report also consists of preparation of cash budgets while providing an overview of financial situation of business

with these financials. It also consists explanation of budgets and budgetary control while also giving an overview of their advantages

and disadvantage for an organisation.

SECTION 1

The purpose and scope of accounting in complex operating environments.

Accounting is an essential skill for the management and analysis of the financial and monetary resources in the establishment.

The functions of accounting involve a systematic tracking, sorting, analysis, maintenance of records and summarise the financial

statements of a business enterprise. The primary purpose of accounting functions lies in the assistance provided by it to management

and authoritative bodies of organisation when taking up crucial decisions. It also aids authorities in determining areas which are of less

importance or areas which need special attention. With assistance of functions of accounting and fiscal history maintained through, the

company can utilise same data in preparation of quantitative reports, creation of budget, reduction in costs and maximisation of profits

(Anderson, 2020).

The functions of accounting which assist an organisation are:

Accounting as a subject plays a very crucial role in the workings of an organisation as it assists the businesses in tracking upon

the incomes, expenditures, costs and the revenues being generated in the organisation. It helps to prepare and manage the accounting

information’s with the assistance of various accounting functions provided by the business (Yang and et.al., 2021). In this report, the

importance and purpose of accounting functions is explained while also giving an overview of the accounting functions that exists in

an organisation. The report consists of the preparation of various necessary financial accounts of the business such as cash budgets,

financial accounting ratios and the analysis of those financial ratios to provide an overview of the financial situation of the

organisation. The report also consists of preparation of cash budgets while providing an overview of financial situation of business

with these financials. It also consists explanation of budgets and budgetary control while also giving an overview of their advantages

and disadvantage for an organisation.

SECTION 1

The purpose and scope of accounting in complex operating environments.

Accounting is an essential skill for the management and analysis of the financial and monetary resources in the establishment.

The functions of accounting involve a systematic tracking, sorting, analysis, maintenance of records and summarise the financial

statements of a business enterprise. The primary purpose of accounting functions lies in the assistance provided by it to management

and authoritative bodies of organisation when taking up crucial decisions. It also aids authorities in determining areas which are of less

importance or areas which need special attention. With assistance of functions of accounting and fiscal history maintained through, the

company can utilise same data in preparation of quantitative reports, creation of budget, reduction in costs and maximisation of profits

(Anderson, 2020).

The functions of accounting which assist an organisation are:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Maintaining financial records: Accounting assists organisations in preparation and maintenance of financial records for daily

transactions which takes place in the business. The transactions may include purchase receipts,sales invoices, supply purchases

and documents relating to payments made. Observation of financial transactions: The accountants in an organisation have responsibility of tracking on many multiple

financial transactions of business to make sure that organisation revenue and expenses are all correctly computed. The

accounting function also aims to maintain that business continues to generate profits by regularly checking upon necessary

resources (Arata, Shimogawa and Inohara, 2022). Maintaining digital records: Accountants in business organisation as in form of their accounting functions are responsible for

the purpose of creating, maintaining and updating digital records of business transactions for storing financial data of company

in an effective manner. The maintenance of such digital records benefits organisation by providing them with the credit of

authenticity for maintaining these records and also assisting accounting department of business in easily finding data and

information when needed. Making financial projections: Accounting involves the analysis of the financial data of the businesses for purpose of making

analysis of the company's financial resources and expected incomes so that future business revenues, growth and expansion

opportunities can be predicted (Belesis, Sorros and Karagiorgos, 2020).

Complying with legal requirements: Accounting functions have a basic purpose of complying with all legal requirements of

company required by law and governing rules and regulations. It should be made sure that company aligns with various rules,

regulations relating to government policies, financial reporting, employee wages.

Hence purpose of accounting functions primarily lies upon above mentioned areas which include: maintenance of financial

records, observation of financial transactions, compliance with legal requirements, maintenance of digital records and making future

business projections (Ehoff and Bouillon, 2019). The purpose of such various accounting functions then lies upon improving the

transactions which takes place in the business. The transactions may include purchase receipts,sales invoices, supply purchases

and documents relating to payments made. Observation of financial transactions: The accountants in an organisation have responsibility of tracking on many multiple

financial transactions of business to make sure that organisation revenue and expenses are all correctly computed. The

accounting function also aims to maintain that business continues to generate profits by regularly checking upon necessary

resources (Arata, Shimogawa and Inohara, 2022). Maintaining digital records: Accountants in business organisation as in form of their accounting functions are responsible for

the purpose of creating, maintaining and updating digital records of business transactions for storing financial data of company

in an effective manner. The maintenance of such digital records benefits organisation by providing them with the credit of

authenticity for maintaining these records and also assisting accounting department of business in easily finding data and

information when needed. Making financial projections: Accounting involves the analysis of the financial data of the businesses for purpose of making

analysis of the company's financial resources and expected incomes so that future business revenues, growth and expansion

opportunities can be predicted (Belesis, Sorros and Karagiorgos, 2020).

Complying with legal requirements: Accounting functions have a basic purpose of complying with all legal requirements of

company required by law and governing rules and regulations. It should be made sure that company aligns with various rules,

regulations relating to government policies, financial reporting, employee wages.

Hence purpose of accounting functions primarily lies upon above mentioned areas which include: maintenance of financial

records, observation of financial transactions, compliance with legal requirements, maintenance of digital records and making future

business projections (Ehoff and Bouillon, 2019). The purpose of such various accounting functions then lies upon improving the

financial positions and strength of business. Taking necessary actions guided by accounting functions so that business is able to

achieve desired revenues and profits while making an efficient employment and usage of resources of business.

Evaluate the accounting function in informing decision making and meeting stakeholder and societal needs and expectations.

Accountancy supports the process of decision making and taking informed decisions. The primary objective of business

organisation is to accelerate higher profits of the organisation and this is done when the transactions are recorded by the accounting

departments in an accurate manner. After the preparation of financials of company, the organisation receives suggestions regarding the

products that are beneficial for company and services which should be cut down as they are not generating enough incomes for

business (Vedpuriswar, 2021). It assist to provide idea of how the budgets in business should be forecasted and what tasks are

necessary to perform organisational tasks effectively. The shareholders and investors normally utilise the financials to assess the

financial position of business and the profits earned by it. The investors go upon investing in the business only when the financials

show an impressive business positions upon observation. Accounting functions are essential as they are the only way in which

organisation's costs and expenditures along with profits could be measured effectively.

The main branches of accounting and job skill sets and competencies.

The four primary branches of accounting are:1. Financial accounting: It involves recording and categorizing of the business transactions that take place. The data taken into

account is mainly the past data and on the basis of this business data the financials of the concern are prepared.2. Cost accounting: It is primarily used in the manufacturing industry as it involves the maximum cost and resource involvement.

It is concerned with recording and analysing the manufacturing costs for business.3. Managerial accounting: This accounting branch assist to provide the data relating to an organisation's operations to the

management of the business. It involves budgeting, cost analysis and forecasting of data.

4. Tax accounting: This is concerned with the planning of tax returns, their preparations and tax filings. This enables the business

to be compliant of the regulations which are set by the IRS (Radin, 2018).

achieve desired revenues and profits while making an efficient employment and usage of resources of business.

Evaluate the accounting function in informing decision making and meeting stakeholder and societal needs and expectations.

Accountancy supports the process of decision making and taking informed decisions. The primary objective of business

organisation is to accelerate higher profits of the organisation and this is done when the transactions are recorded by the accounting

departments in an accurate manner. After the preparation of financials of company, the organisation receives suggestions regarding the

products that are beneficial for company and services which should be cut down as they are not generating enough incomes for

business (Vedpuriswar, 2021). It assist to provide idea of how the budgets in business should be forecasted and what tasks are

necessary to perform organisational tasks effectively. The shareholders and investors normally utilise the financials to assess the

financial position of business and the profits earned by it. The investors go upon investing in the business only when the financials

show an impressive business positions upon observation. Accounting functions are essential as they are the only way in which

organisation's costs and expenditures along with profits could be measured effectively.

The main branches of accounting and job skill sets and competencies.

The four primary branches of accounting are:1. Financial accounting: It involves recording and categorizing of the business transactions that take place. The data taken into

account is mainly the past data and on the basis of this business data the financials of the concern are prepared.2. Cost accounting: It is primarily used in the manufacturing industry as it involves the maximum cost and resource involvement.

It is concerned with recording and analysing the manufacturing costs for business.3. Managerial accounting: This accounting branch assist to provide the data relating to an organisation's operations to the

management of the business. It involves budgeting, cost analysis and forecasting of data.

4. Tax accounting: This is concerned with the planning of tax returns, their preparations and tax filings. This enables the business

to be compliant of the regulations which are set by the IRS (Radin, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The job skill sets and competencies that are required in accounting as a subject field are:

Knowledge of Accounting Practices: The accountant should have enough knowledge regarding all the various accounting

principles that are present and to be followed and implemented.

Proficiency in Accounting Software: The accountant is supposed to be proficient in the use of various accounting software

that are utilised in the business and its operations. This assist the accountant to record, interpret and analyse the data

effectively.

Ability to Prepare Financial Statements: The accountant should be very proficient in the preparation and analysis of the

financial statements that are necessary for analysing business performances.

Knowledge of General Business Practices: All the general business practices which are present in accounting are necessary

to be in knowledge of the accountant as this will help to better understand the issues and financial needs of the customers.

Accounting systems and the role of technology in modern-day accounting.

An accounting systems are a set of accounting processes along with various combined procedures and controls. They are

responsible for recording the business transactions, combining and summarizing them and generate reports which can be utilised by

the decision makers to monitor the performances of the business and improve the results with the help of that analysis (Wallington,

Marques and Maroun, 2021). The accounting systems assist in tracking upon incomes, expenditures, ensuring statutory compliances

and providing investors, management and governing authorities with the necessary and quantitative informations.

Technology plays an essential role in present day accounting methods as it assist to solve various problems which were

previously creating issues for organisations. Technology has transformed the accounting sector with the use of various new and

advanced software's that enable accuracy and reduction in the errors committed while preparing financials. It has also made it very

easy to maintain organisation of the huge block of transactions and details regarding the accounts effectively.

Knowledge of Accounting Practices: The accountant should have enough knowledge regarding all the various accounting

principles that are present and to be followed and implemented.

Proficiency in Accounting Software: The accountant is supposed to be proficient in the use of various accounting software

that are utilised in the business and its operations. This assist the accountant to record, interpret and analyse the data

effectively.

Ability to Prepare Financial Statements: The accountant should be very proficient in the preparation and analysis of the

financial statements that are necessary for analysing business performances.

Knowledge of General Business Practices: All the general business practices which are present in accounting are necessary

to be in knowledge of the accountant as this will help to better understand the issues and financial needs of the customers.

Accounting systems and the role of technology in modern-day accounting.

An accounting systems are a set of accounting processes along with various combined procedures and controls. They are

responsible for recording the business transactions, combining and summarizing them and generate reports which can be utilised by

the decision makers to monitor the performances of the business and improve the results with the help of that analysis (Wallington,

Marques and Maroun, 2021). The accounting systems assist in tracking upon incomes, expenditures, ensuring statutory compliances

and providing investors, management and governing authorities with the necessary and quantitative informations.

Technology plays an essential role in present day accounting methods as it assist to solve various problems which were

previously creating issues for organisations. Technology has transformed the accounting sector with the use of various new and

advanced software's that enable accuracy and reduction in the errors committed while preparing financials. It has also made it very

easy to maintain organisation of the huge block of transactions and details regarding the accounts effectively.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Issues of ethics, regulation and compliance and the extent to which they are constraints or threats to the organisation.

Ethics in accounting are primarily concerned with moral choices with which decisions are made in the area of accounting,

while preparation of accounting statements, disclosure of financial informations and many more. It consists of the specific rules and

regulations that are established to prevent any misuse of financial data or of the management position in the organisation (Mercl and

et.al., 2019).

Regulations in accounting are the various rules, regulations, standards and the laws established and communicated by the

various governing bodies for the purpose of maintained transparency, reliability, consistency and comparability in the financial

statements of various organisations.

The ethical and regulatory issues in accounting which act as the constraints are a follows: Fraudulent reporting of financials: The major ethical issue in accounting is of fraudulent reporting of financial statements of

a business enterprise which is misstatement of financials of company by the management (Hajimoradkhani and Zare Ahan

Panjeh, 2021). This is done to mislead investors and maintain high share prices of company's shares. Although these fraudulent

activities can boost prices of company's shares, they create severe effects on company and its financial health in long term. Violation of data disclosure: As fraudulent activities, the failure in proper disclosure of company's data and information is

also an ethical constraint in accounting. The failure in disclosing such data to investors and key stakeholders of the company

who may use this data for making some crucial decisions, is termed as unethical practise in accounting. Lack of transparency in accounting decisions: It is a regulatory issue in accounting which involves failure in proper

disclosure and transparency in the financial informations of company. As lack in the revelation of financial informations and

accounting data of business results in misappropriation of financials from the company's key stakeholders and investors.

Tax Evasion: Performance of tax evasion is an illegal activity which is against rules and regulations of governing authorities

of a country. It is a regulatory constraint which affects goodwill of an organisation and is done through a misrepresentation of

Ethics in accounting are primarily concerned with moral choices with which decisions are made in the area of accounting,

while preparation of accounting statements, disclosure of financial informations and many more. It consists of the specific rules and

regulations that are established to prevent any misuse of financial data or of the management position in the organisation (Mercl and

et.al., 2019).

Regulations in accounting are the various rules, regulations, standards and the laws established and communicated by the

various governing bodies for the purpose of maintained transparency, reliability, consistency and comparability in the financial

statements of various organisations.

The ethical and regulatory issues in accounting which act as the constraints are a follows: Fraudulent reporting of financials: The major ethical issue in accounting is of fraudulent reporting of financial statements of

a business enterprise which is misstatement of financials of company by the management (Hajimoradkhani and Zare Ahan

Panjeh, 2021). This is done to mislead investors and maintain high share prices of company's shares. Although these fraudulent

activities can boost prices of company's shares, they create severe effects on company and its financial health in long term. Violation of data disclosure: As fraudulent activities, the failure in proper disclosure of company's data and information is

also an ethical constraint in accounting. The failure in disclosing such data to investors and key stakeholders of the company

who may use this data for making some crucial decisions, is termed as unethical practise in accounting. Lack of transparency in accounting decisions: It is a regulatory issue in accounting which involves failure in proper

disclosure and transparency in the financial informations of company. As lack in the revelation of financial informations and

accounting data of business results in misappropriation of financials from the company's key stakeholders and investors.

Tax Evasion: Performance of tax evasion is an illegal activity which is against rules and regulations of governing authorities

of a country. It is a regulatory constraint which affects goodwill of an organisation and is done through a misrepresentation of

company financials (McEnroe and Sullivan, 2018). It is done to deliberately avoid tax liability of company and to save the

money by using this fraudulent activity.

Evaluate role of budgets and budgetary control and their advantages and disadvantages and how can they assist to identify problems at

business.

Budget: A budget is a financial plan for an organisation which is made for a particular future period. It provides for

informations relating to income and expenditures for a certain time period. Budgets are prepared to cover for all functional and

effective areas of business which are responsible for generating revenues and incur expenditures in future (Mohamed and Farhan,

2020). It is a system which is responsible for planning and control in the organisation. A budget is primarily concerned with framing

of necessary policies for business which will be utilised for comparing actual results with standard results that were set by organisation

in future. If actual numbers of business vary with budgeted figures, the budgets needs to be revised appropriately on that basis.

Budgetary control: It involves comparison of estimated expenses of business with actual expenses that were incurred in

businesses working. Also, budgetary control involves placement of responsibilities for failures which occurred in prepared budgets

and actual results. The periodic checking up of income, expenses and business costs related to budget administration is termed as

budgetary control. It is system of management control in which different operations of business are forecasted and planned upon in

advance for the purpose of revising current and future policies of budgets. It provides with outer lines on the basis of which actual

results of company are compared with budgeted results.

Advantages of budgets, budgetary planning and controlling:1. Definite planning: Budgets are developed based on well defined and researched planning. They enable organisations in

knowing what is expected to be done and to be achieved in the future time periods. They guide the business organisations in

prior on the amount that they will spend in future on its activities and the amount that the business may expect to earn in the

future (Mukhtaruddin, and Fuadah, 2022).

money by using this fraudulent activity.

Evaluate role of budgets and budgetary control and their advantages and disadvantages and how can they assist to identify problems at

business.

Budget: A budget is a financial plan for an organisation which is made for a particular future period. It provides for

informations relating to income and expenditures for a certain time period. Budgets are prepared to cover for all functional and

effective areas of business which are responsible for generating revenues and incur expenditures in future (Mohamed and Farhan,

2020). It is a system which is responsible for planning and control in the organisation. A budget is primarily concerned with framing

of necessary policies for business which will be utilised for comparing actual results with standard results that were set by organisation

in future. If actual numbers of business vary with budgeted figures, the budgets needs to be revised appropriately on that basis.

Budgetary control: It involves comparison of estimated expenses of business with actual expenses that were incurred in

businesses working. Also, budgetary control involves placement of responsibilities for failures which occurred in prepared budgets

and actual results. The periodic checking up of income, expenses and business costs related to budget administration is termed as

budgetary control. It is system of management control in which different operations of business are forecasted and planned upon in

advance for the purpose of revising current and future policies of budgets. It provides with outer lines on the basis of which actual

results of company are compared with budgeted results.

Advantages of budgets, budgetary planning and controlling:1. Definite planning: Budgets are developed based on well defined and researched planning. They enable organisations in

knowing what is expected to be done and to be achieved in the future time periods. They guide the business organisations in

prior on the amount that they will spend in future on its activities and the amount that the business may expect to earn in the

future (Mukhtaruddin, and Fuadah, 2022).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Efficient and proper communication: Budgets are prepared keeping in mind the feedbacks and the useful informations which

is provided by the subordinates and business employees at lower levels of the organisation. As the individuals at that level

come with direct contact of all the activities and functions performed by the business and hence create an environment of

proper and transparent communications among the management resulting in efficient and fruitful decision making. As each

and every department in the organisation generates their individual budgets hence the flow of communication is very efficient

in between the budget framing staff and the departmental staff.3. Delegation of authority: Budgeting and budgetary control assists and encourages the delegation of authority in an

organisation. It provides the maximum limits in which delegated authority can be utilised (Wen and Wang, 2022). The

subordinates and executives of organisation can produce for initiatives and judgements within the limits of budgetary control.4. Motivation: Budget and the budgetary control acts as an essential and a strong motivator as an incentive to the employees in

the business organisation by motivating them in fixing their business performances to attain the targets that are set by the

management of the business.5. Uniform Policy: The preparation of budgets and budgetary control equally in business divisions and departments assists in

making a uniform policy for all departments of business without generating any disadvantage to any of the departments like an

authoritarian type of business organisation.

Disadvantages of budgets, budgetary planning and controlling:

1. Future uncertainty: Since budgets are prepared keeping in mind the future predictions for the business hence it can sometimes

fail to predict for a future situation. As sometimes a change in the future situations may create a difference in predicted budget

and actual budget hence reduces utility of the budgetary control system.

2. Constant revisions necessary: Since the budgets are prepared keeping in mind some future predictions and assumptions, any

variation in the predictions necessitate the situation for revising the budgets of the company (Saleh, Al-Shaghdari and Ali

Hakami, 2023). The frequent revisions then reduce the importance and effectiveness of budgets.

is provided by the subordinates and business employees at lower levels of the organisation. As the individuals at that level

come with direct contact of all the activities and functions performed by the business and hence create an environment of

proper and transparent communications among the management resulting in efficient and fruitful decision making. As each

and every department in the organisation generates their individual budgets hence the flow of communication is very efficient

in between the budget framing staff and the departmental staff.3. Delegation of authority: Budgeting and budgetary control assists and encourages the delegation of authority in an

organisation. It provides the maximum limits in which delegated authority can be utilised (Wen and Wang, 2022). The

subordinates and executives of organisation can produce for initiatives and judgements within the limits of budgetary control.4. Motivation: Budget and the budgetary control acts as an essential and a strong motivator as an incentive to the employees in

the business organisation by motivating them in fixing their business performances to attain the targets that are set by the

management of the business.5. Uniform Policy: The preparation of budgets and budgetary control equally in business divisions and departments assists in

making a uniform policy for all departments of business without generating any disadvantage to any of the departments like an

authoritarian type of business organisation.

Disadvantages of budgets, budgetary planning and controlling:

1. Future uncertainty: Since budgets are prepared keeping in mind the future predictions for the business hence it can sometimes

fail to predict for a future situation. As sometimes a change in the future situations may create a difference in predicted budget

and actual budget hence reduces utility of the budgetary control system.

2. Constant revisions necessary: Since the budgets are prepared keeping in mind some future predictions and assumptions, any

variation in the predictions necessitate the situation for revising the budgets of the company (Saleh, Al-Shaghdari and Ali

Hakami, 2023). The frequent revisions then reduce the importance and effectiveness of budgets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Problem of Co-ordination: The success of the budgetary control entirely depends on the coordination among the various

departments of the business. As the performance and results achieved in one department affects performance of another. Hence

budgets needs to coordinate among various departments in an effective manner so that best outcome could be achieved with

the utilisation of those budgets.

4. Conflicts among departments: Preparation of budgetary control may induce conflicts among the various departments of the

organisation. As every departmental head tries upon to benefit their own department by allocation of maximum resources in

their departments which results in conflict in between the departments and sometime loose upon effectiveness of budgetary

control.

5. Support of top management: The budgetary control and the preparation of budgets requires the support from the top

management of the company. As efforts initiated by the top management assess quality and effectiveness of budgets prepared

for the company (Rao, 2021). In situations if business lacks support from top level management, entire system for preparation

of budgets collapses.

departments of the business. As the performance and results achieved in one department affects performance of another. Hence

budgets needs to coordinate among various departments in an effective manner so that best outcome could be achieved with

the utilisation of those budgets.

4. Conflicts among departments: Preparation of budgetary control may induce conflicts among the various departments of the

organisation. As every departmental head tries upon to benefit their own department by allocation of maximum resources in

their departments which results in conflict in between the departments and sometime loose upon effectiveness of budgetary

control.

5. Support of top management: The budgetary control and the preparation of budgets requires the support from the top

management of the company. As efforts initiated by the top management assess quality and effectiveness of budgets prepared

for the company (Rao, 2021). In situations if business lacks support from top level management, entire system for preparation

of budgets collapses.

SECTION 2

Calculation of comparative key performance ratios such as profitably, liquidity, asset usage and investment ratios.

Financial ratios- Ratio is a mathematical expression which establishes relationship between any two individual accounting

figures. It is utilized by business managers, investors and creditors of an enterprise . Ratio aids to ascertain fair prices of the shares of

an organisation. By using ratios, financial analysts discover the strength and weakness of a business. The various types of ratios are:

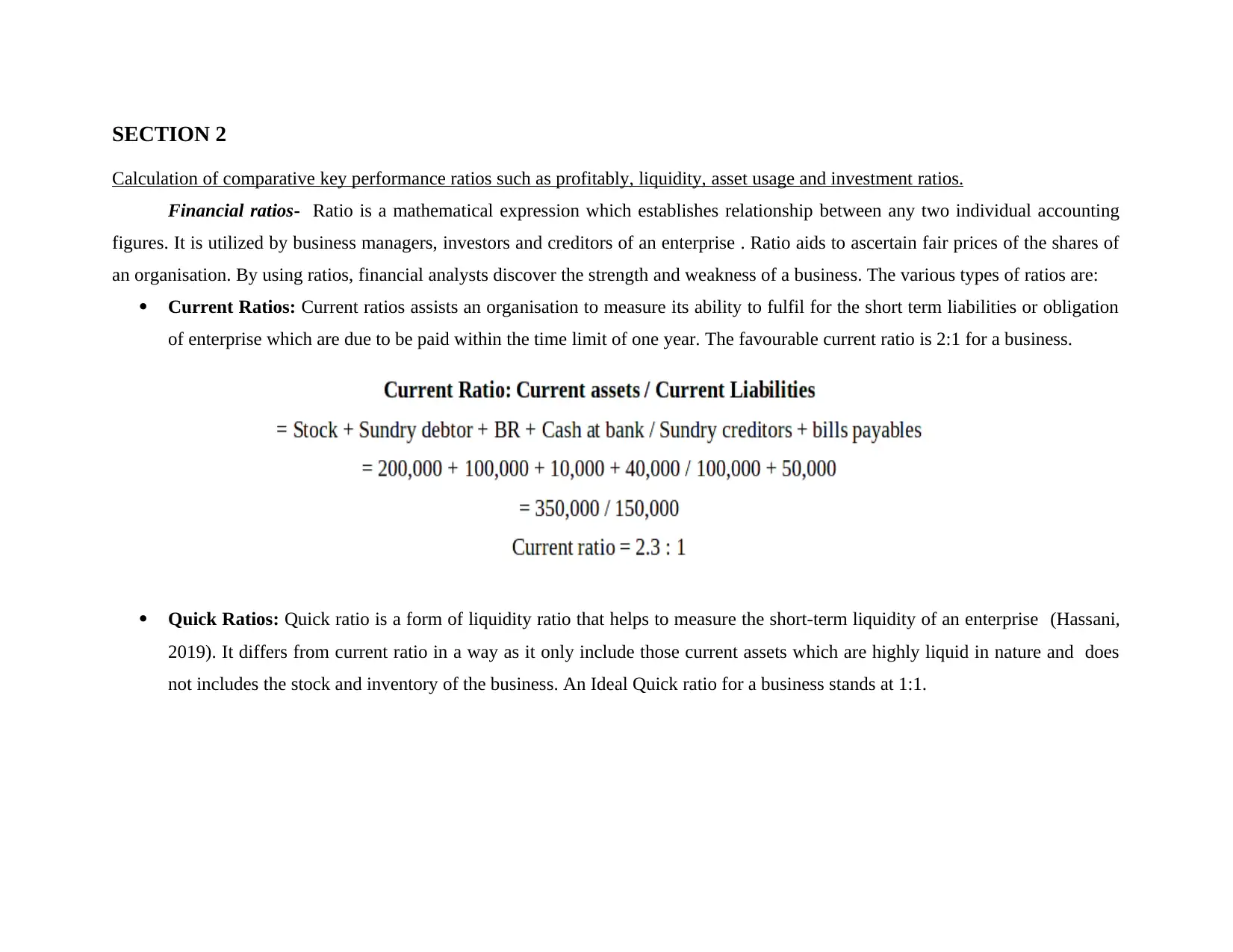

Current Ratios: Current ratios assists an organisation to measure its ability to fulfil for the short term liabilities or obligation

of enterprise which are due to be paid within the time limit of one year. The favourable current ratio is 2:1 for a business.

Quick Ratios: Quick ratio is a form of liquidity ratio that helps to measure the short-term liquidity of an enterprise (Hassani,

2019). It differs from current ratio in a way as it only include those current assets which are highly liquid in nature and does

not includes the stock and inventory of the business. An Ideal Quick ratio for a business stands at 1:1.

Calculation of comparative key performance ratios such as profitably, liquidity, asset usage and investment ratios.

Financial ratios- Ratio is a mathematical expression which establishes relationship between any two individual accounting

figures. It is utilized by business managers, investors and creditors of an enterprise . Ratio aids to ascertain fair prices of the shares of

an organisation. By using ratios, financial analysts discover the strength and weakness of a business. The various types of ratios are:

Current Ratios: Current ratios assists an organisation to measure its ability to fulfil for the short term liabilities or obligation

of enterprise which are due to be paid within the time limit of one year. The favourable current ratio is 2:1 for a business.

Quick Ratios: Quick ratio is a form of liquidity ratio that helps to measure the short-term liquidity of an enterprise (Hassani,

2019). It differs from current ratio in a way as it only include those current assets which are highly liquid in nature and does

not includes the stock and inventory of the business. An Ideal Quick ratio for a business stands at 1:1.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.