Accounting Principles: Accounting in Context and Budgetary Control

VerifiedAdded on 2023/02/07

|9

|2361

|33

Report

AI Summary

This report provides a comprehensive overview of accounting principles and budgetary control within an organizational context. It explores the purpose of the accounting function, encompassing financial reporting, ethical constraints, and regulatory compliance, including GAAP and IFRS. The report examines how accounting meets organizational, stakeholder, and societal needs, emphasizing its role in informing decision-making within complex operating environments. It includes a discussion on preparing a cash budget and analyzes the benefits, limitations, and corrective actions related to budgetary planning and control. The study uses ARAMCO as a case study and provides insight on how budgetary control solutions impact resource deployment and organizational decision-making. The report highlights the importance of ethical considerations, the role of accounting in providing accurate information for prudent business choices, and the significance of budgetary control in achieving financial goals. Finally, it emphasizes the role of accounting in maintaining a company's financial health and reporting on it.

Unit 5: Accounting Principles

Accounting in Context and Budgetary Control

Part-1 (LO1&4)

Accounting in Context and Budgetary Control

Part-1 (LO1&4)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

The purpose of the accounting function within an organisation......................................................3

The accounting function within the organisation in the context of regulatory and ethical

constraints........................................................................................................................................4

The accounting function meets organizational, stakeholder, and societal needs.............................5

The role of accounting in informing decision making to meet organisational, stakeholder and

societal needs within complex operating environments..................................................................5

Preparing a cash budget from given data for an organization using a spreadsheet.........................6

The benefits and limitations of budgets and budgetary planning, and control for an organization.7

The corrective actions to problems revealed by budgetary planning and control for effective

organisational decision making.......................................................................................................7

The budgetary control solutions and their impact on organisational decision making to ensure

efficient and effective deployment of resources..............................................................................7

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

Introduction......................................................................................................................................3

The purpose of the accounting function within an organisation......................................................3

The accounting function within the organisation in the context of regulatory and ethical

constraints........................................................................................................................................4

The accounting function meets organizational, stakeholder, and societal needs.............................5

The role of accounting in informing decision making to meet organisational, stakeholder and

societal needs within complex operating environments..................................................................5

Preparing a cash budget from given data for an organization using a spreadsheet.........................6

The benefits and limitations of budgets and budgetary planning, and control for an organization.7

The corrective actions to problems revealed by budgetary planning and control for effective

organisational decision making.......................................................................................................7

The budgetary control solutions and their impact on organisational decision making to ensure

efficient and effective deployment of resources..............................................................................7

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

Introduction

Because the future is fluid and hard to anticipate, it is essential to plan ahead and to do it in a

manner that will have a significant and long-lasting impact on the value of the business in the

long run. The planning aspect of accounting comes into play at this point. An exhaustive study

was conducted on ARAMCO, which is really the current topic of an analysis that encompasses a

variety of topics including accounting tasks, ethical constraints, and cash budgeting. This study

was conducted because ARAMCO continues to operate on a massive scale and has thus gained a

significant market share.

The purpose of the accounting function within an organisation.

In a nutshell, the practice of accounting involves gathering, analyzing, and disclosing data on the

flow of financial resources. A business manager has a variety of purposes for running his or her

company, all of which contribute to the accounting process. The accounting function serves a

variety of purposes within an organization, some of which are listed below:

When a transaction (cost) is registered, it is essential that all monetary inputs and outputs

be tracked. There is a risk that important information may be overlooked if these items

are left off the list. Financial reporting and tax payments are likely to become

problematic, which might lead to legal issues for the company.

On a routine basis, monitor the news to ensure that your financial reports are updated.

The proprietors and managers of the organization were able to keep track of everyone and

everything that entered and exited the premises by using this technology. In addition to

that, the graph illustrates whether or not the activity level is growing or decreasing. If you

want to ensure that all of your payments are paid in full and on time, you should check

the balances of your accounts every day.

An organization's managers are responsible for ensuring that the company's resources are

properly allocated and managed in order to function smoothly. A manager's

responsibilities include the effective administration of a company's finances, participation

in decision making, and the resolution of operational issues.

It's all going to work out perfectly as long as the transactions are recorded and kept track

of. It is possible to exercise more command over the company's current financial

Because the future is fluid and hard to anticipate, it is essential to plan ahead and to do it in a

manner that will have a significant and long-lasting impact on the value of the business in the

long run. The planning aspect of accounting comes into play at this point. An exhaustive study

was conducted on ARAMCO, which is really the current topic of an analysis that encompasses a

variety of topics including accounting tasks, ethical constraints, and cash budgeting. This study

was conducted because ARAMCO continues to operate on a massive scale and has thus gained a

significant market share.

The purpose of the accounting function within an organisation.

In a nutshell, the practice of accounting involves gathering, analyzing, and disclosing data on the

flow of financial resources. A business manager has a variety of purposes for running his or her

company, all of which contribute to the accounting process. The accounting function serves a

variety of purposes within an organization, some of which are listed below:

When a transaction (cost) is registered, it is essential that all monetary inputs and outputs

be tracked. There is a risk that important information may be overlooked if these items

are left off the list. Financial reporting and tax payments are likely to become

problematic, which might lead to legal issues for the company.

On a routine basis, monitor the news to ensure that your financial reports are updated.

The proprietors and managers of the organization were able to keep track of everyone and

everything that entered and exited the premises by using this technology. In addition to

that, the graph illustrates whether or not the activity level is growing or decreasing. If you

want to ensure that all of your payments are paid in full and on time, you should check

the balances of your accounts every day.

An organization's managers are responsible for ensuring that the company's resources are

properly allocated and managed in order to function smoothly. A manager's

responsibilities include the effective administration of a company's finances, participation

in decision making, and the resolution of operational issues.

It's all going to work out perfectly as long as the transactions are recorded and kept track

of. It is possible to exercise more command over the company's current financial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

situation. This makes it possible for the organization to maintain tabs on the amount of

money that enters and leaves the company at any one time.

ARAMCO is one example of this. The accounting department works with a wide range of other

functions. It's possible that these and other interactions might happen like follows: For example,

upper staff may obtain information from the accounting department via various sorts of

information; from the employees or HR departments concerning employee wages; from the

procurement department related to payment authorizations for suppliers and payment

requirements; from the sales representatives related to payment receipts and bad loans; and from

the retail chains departments concerning the mobility of inventory.

The accounting function within the organisation in the context of regulatory

and ethical constraints.

The GAAP and the International Financial Reporting Standards (IFRS) are examples of

accounting rules that have been created. Because of this, organizations can now be analyzed

more easily.

Every nation has its own set of accounting rules. IFRS (the majority standard) or GAAP are used

in almost every nation (fewer countries use this). Generally Accepted Accounting Principles are

used in the United Kingdom. If your firm is audited and you don't employ these standards or

follow the guidelines provided by them, you will fail the audit. If your firm is publicly listed, this

might have devastating implications. Let's just say that if a company's financial statements can't

be verified by a public accounting firm, they're in danger of losing their license to operate. If the

firm is privately held, it may still have shareholders who utilize the financial statements to make

informed decisions. As a result, it's best to "follow the rules." Since most mom-and-pop

businesses don't need financial disclosures from their bookkeepers, the IRS is your only major

concern when it comes to easy accounting and bookkeeping for a small company (Cardoza,

2020).

To maintain a thriving economy, the proper regulations must be in play. Ethics have a role in the

effectiveness of regulation as well. To maintain high standards and consistency, legislation based

on ethical principles is essential. Accountants are often confronted with moral quandaries in the

line of duty. Most significant partners in a business might be deceived if consumers tell their

money that enters and leaves the company at any one time.

ARAMCO is one example of this. The accounting department works with a wide range of other

functions. It's possible that these and other interactions might happen like follows: For example,

upper staff may obtain information from the accounting department via various sorts of

information; from the employees or HR departments concerning employee wages; from the

procurement department related to payment authorizations for suppliers and payment

requirements; from the sales representatives related to payment receipts and bad loans; and from

the retail chains departments concerning the mobility of inventory.

The accounting function within the organisation in the context of regulatory

and ethical constraints.

The GAAP and the International Financial Reporting Standards (IFRS) are examples of

accounting rules that have been created. Because of this, organizations can now be analyzed

more easily.

Every nation has its own set of accounting rules. IFRS (the majority standard) or GAAP are used

in almost every nation (fewer countries use this). Generally Accepted Accounting Principles are

used in the United Kingdom. If your firm is audited and you don't employ these standards or

follow the guidelines provided by them, you will fail the audit. If your firm is publicly listed, this

might have devastating implications. Let's just say that if a company's financial statements can't

be verified by a public accounting firm, they're in danger of losing their license to operate. If the

firm is privately held, it may still have shareholders who utilize the financial statements to make

informed decisions. As a result, it's best to "follow the rules." Since most mom-and-pop

businesses don't need financial disclosures from their bookkeepers, the IRS is your only major

concern when it comes to easy accounting and bookkeeping for a small company (Cardoza,

2020).

To maintain a thriving economy, the proper regulations must be in play. Ethics have a role in the

effectiveness of regulation as well. To maintain high standards and consistency, legislation based

on ethical principles is essential. Accountants are often confronted with moral quandaries in the

line of duty. Most significant partners in a business might be deceived if consumers tell their

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accountants not to provide truthful financial statement data. They have to choose between

satisfying their clients and preserving the interests of the majority. Codes of ethics for accounting

associations like the AICPA have been written by members to serve as a guidance for making

smart sound decisions. Since their work and the obligations that are included in them are so

complex and difficult to understand, people who are familiar with the five most critical

principles (i.e. duty, public interest and integrity; integrity; objectivity; and carefulness. will be

better able to make ethical or practical judgments. A company's reputation and the economy as a

whole may be improved if accountants abide by certain ethical standards. Their influence may

even extend to their own domains as a result of this (Maclay, 2022).

The accounting function meets organizational, stakeholder, and societal needs.

There are many organizations that use accounting. It is the ultimate purpose to maintain track of

and report on the financial well-being of an organization. Having this information will allow you

to make the best choices for the company's management or investment. If a firm wants to

develop, it must identify which components of the organization are lucrative and which require

improvement.

Successful organizations may be anticipated by looking at how effectively they accomplish their

objectives and satisfy their stakeholders. As a result, they'll be better able to deal with their

encounters with an organization. As part of this design and development process, stakeholders

are identified, studied, and actions to meet and engage with them are planned and executed

(Azim & Jesmin, 2015).

To match social expectations and norms, accounting may also be used in this manner.

Maintaining a company's overall financial health and reporting on it are two of the primary

functions of this kind of accountancy. Having this information will allow you to make the best

choices for the company's management or investment. This study will be beneficial to

individuals as well as to society as a whole. Should they make the decision to invest in the

company, they will find this knowledge to be helpful (Hall, 2015).

satisfying their clients and preserving the interests of the majority. Codes of ethics for accounting

associations like the AICPA have been written by members to serve as a guidance for making

smart sound decisions. Since their work and the obligations that are included in them are so

complex and difficult to understand, people who are familiar with the five most critical

principles (i.e. duty, public interest and integrity; integrity; objectivity; and carefulness. will be

better able to make ethical or practical judgments. A company's reputation and the economy as a

whole may be improved if accountants abide by certain ethical standards. Their influence may

even extend to their own domains as a result of this (Maclay, 2022).

The accounting function meets organizational, stakeholder, and societal needs.

There are many organizations that use accounting. It is the ultimate purpose to maintain track of

and report on the financial well-being of an organization. Having this information will allow you

to make the best choices for the company's management or investment. If a firm wants to

develop, it must identify which components of the organization are lucrative and which require

improvement.

Successful organizations may be anticipated by looking at how effectively they accomplish their

objectives and satisfy their stakeholders. As a result, they'll be better able to deal with their

encounters with an organization. As part of this design and development process, stakeholders

are identified, studied, and actions to meet and engage with them are planned and executed

(Azim & Jesmin, 2015).

To match social expectations and norms, accounting may also be used in this manner.

Maintaining a company's overall financial health and reporting on it are two of the primary

functions of this kind of accountancy. Having this information will allow you to make the best

choices for the company's management or investment. This study will be beneficial to

individuals as well as to society as a whole. Should they make the decision to invest in the

company, they will find this knowledge to be helpful (Hall, 2015).

The role of accounting in informing decision making to meet organisational,

stakeholder and societal needs within complex operating environments.

Accountancy can provide the exact information required to aid in prudent company choices by

providing a thorough comprehension of the relevant data. Management accounting requires the

use of a wide variety of effects in order to build a bookkeeping environment that allows useful

and timely information. Since the financial reporting adheres to recognized accounting rules and

expectations, it is free of errors. Accounting management relies on three essential concepts to

keep its records accurate, timely, and up to date. Financial performance increase when decision-

makers use reliable data to guide their actions. There's no need to worry about the accuracy of

the data provided by this source. The financial accounts and budgets of a firm are subject to both

internal and external audits by this organization. Finally, it contributes in making a sound

business choice for the organization.

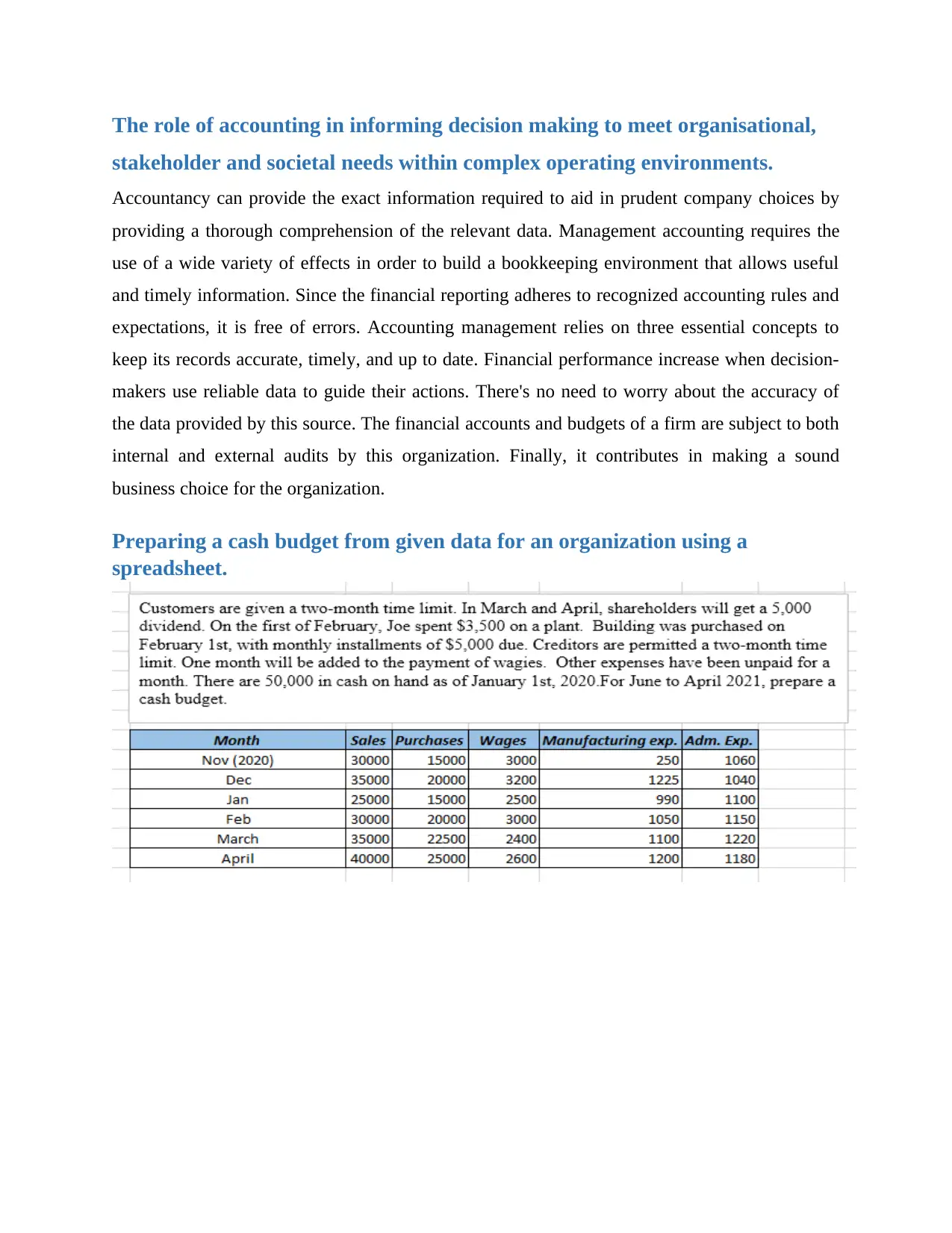

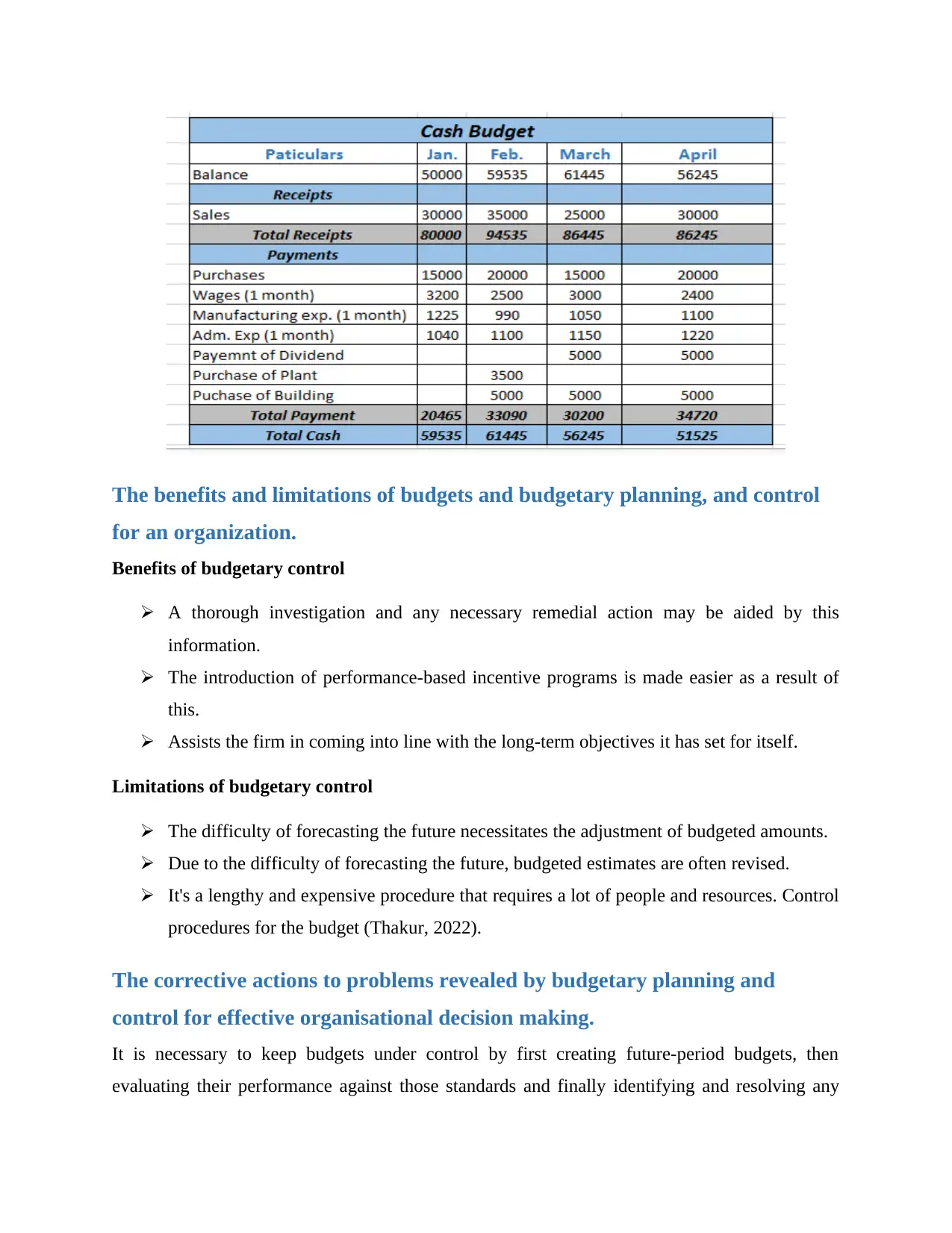

Preparing a cash budget from given data for an organization using a

spreadsheet.

stakeholder and societal needs within complex operating environments.

Accountancy can provide the exact information required to aid in prudent company choices by

providing a thorough comprehension of the relevant data. Management accounting requires the

use of a wide variety of effects in order to build a bookkeeping environment that allows useful

and timely information. Since the financial reporting adheres to recognized accounting rules and

expectations, it is free of errors. Accounting management relies on three essential concepts to

keep its records accurate, timely, and up to date. Financial performance increase when decision-

makers use reliable data to guide their actions. There's no need to worry about the accuracy of

the data provided by this source. The financial accounts and budgets of a firm are subject to both

internal and external audits by this organization. Finally, it contributes in making a sound

business choice for the organization.

Preparing a cash budget from given data for an organization using a

spreadsheet.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The benefits and limitations of budgets and budgetary planning, and control

for an organization.

Benefits of budgetary control

A thorough investigation and any necessary remedial action may be aided by this

information.

The introduction of performance-based incentive programs is made easier as a result of

this.

Assists the firm in coming into line with the long-term objectives it has set for itself.

Limitations of budgetary control

The difficulty of forecasting the future necessitates the adjustment of budgeted amounts.

Due to the difficulty of forecasting the future, budgeted estimates are often revised.

It's a lengthy and expensive procedure that requires a lot of people and resources. Control

procedures for the budget (Thakur, 2022).

The corrective actions to problems revealed by budgetary planning and

control for effective organisational decision making.

It is necessary to keep budgets under control by first creating future-period budgets, then

evaluating their performance against those standards and finally identifying and resolving any

for an organization.

Benefits of budgetary control

A thorough investigation and any necessary remedial action may be aided by this

information.

The introduction of performance-based incentive programs is made easier as a result of

this.

Assists the firm in coming into line with the long-term objectives it has set for itself.

Limitations of budgetary control

The difficulty of forecasting the future necessitates the adjustment of budgeted amounts.

Due to the difficulty of forecasting the future, budgeted estimates are often revised.

It's a lengthy and expensive procedure that requires a lot of people and resources. Control

procedures for the budget (Thakur, 2022).

The corrective actions to problems revealed by budgetary planning and

control for effective organisational decision making.

It is necessary to keep budgets under control by first creating future-period budgets, then

evaluating their performance against those standards and finally identifying and resolving any

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

discrepancies. To make a wise decision for the company, the budgeting officer may go through a

variety of techniques. Initially, a budgetary controller attempts to place up a budget that

describes the business' future goals. To determine whether there are any differences, the

budgeting office should evaluate the completed budget with the actual outcomes. If this budget

has to be fixed, he or she will suggest that figures from the agencies that created it be altered

(Song, Martens & Vanhoucke, 2020).

The budgetary control solutions and their impact on organisational decision

making to ensure efficient and effective deployment of resources.

As a main means of internal control, most companies rely significantly on their capacity to

monitor their budgets. This ensures that their capabilities are dispersed in an even more efficient

way feasible. Keep a record of your current expenditure and compare it to your budget to make

sure you're in complete command of your money. To establish a budget and achieve other

financial goals, this method is crucial. By implementing budgetary control into projecting

activities, companies may enhance long-term planning and budgeting. Normally, the accounting

and management departments’ work together to accurately forecast the company's costs and

revenues. A company's need to anticipate and plan for future threats and possibilities may be

addressed by effectively implementing monitoring system. This issue may be solved with a well-

managed budget (Zimmerman, 2011).

Conclusion

The purpose of accounting is to keep track of a company's financial situation in a consistent

fashion. Establishing a record-keeping system, monitoring activities within a certain system, and

preparing financial statements based on the data generated are the three steps of the recording

process. Budget and budgetary plan are critical procedures for the finance industry of the

organization. This has to be handled correctly in order to reduce problems. The majority of your

attention for this project will be directed into the many facets of accounting and budgeting. As

the owner of the firm, it is your responsibility to monitor the ways in which the money is being

used by the business.

variety of techniques. Initially, a budgetary controller attempts to place up a budget that

describes the business' future goals. To determine whether there are any differences, the

budgeting office should evaluate the completed budget with the actual outcomes. If this budget

has to be fixed, he or she will suggest that figures from the agencies that created it be altered

(Song, Martens & Vanhoucke, 2020).

The budgetary control solutions and their impact on organisational decision

making to ensure efficient and effective deployment of resources.

As a main means of internal control, most companies rely significantly on their capacity to

monitor their budgets. This ensures that their capabilities are dispersed in an even more efficient

way feasible. Keep a record of your current expenditure and compare it to your budget to make

sure you're in complete command of your money. To establish a budget and achieve other

financial goals, this method is crucial. By implementing budgetary control into projecting

activities, companies may enhance long-term planning and budgeting. Normally, the accounting

and management departments’ work together to accurately forecast the company's costs and

revenues. A company's need to anticipate and plan for future threats and possibilities may be

addressed by effectively implementing monitoring system. This issue may be solved with a well-

managed budget (Zimmerman, 2011).

Conclusion

The purpose of accounting is to keep track of a company's financial situation in a consistent

fashion. Establishing a record-keeping system, monitoring activities within a certain system, and

preparing financial statements based on the data generated are the three steps of the recording

process. Budget and budgetary plan are critical procedures for the finance industry of the

organization. This has to be handled correctly in order to reduce problems. The majority of your

attention for this project will be directed into the many facets of accounting and budgeting. As

the owner of the firm, it is your responsibility to monitor the ways in which the money is being

used by the business.

References

Abraham Cardoza, Jr. (2020), what are the rules of accounting? [Online] Available at:

https://www.quora.com/What-are-the-rules-of-accounting?q=what%20is%20accounting

%20rules%20and%20regualtions%20and%20ethics, [Accessed on: 8 June 2022].

Kyle Maclay, (2022), accounting regulation and ethics, [online] Available at:

https://www.personalfinancelab.com/finance-knowledge/accounting/accounting-regulation-and-

ethics/, [Accessed on: 8 June 2022].

Hall, J.A., 2015. Accounting information systems. Cengage Learning.

Azim, Md & Ara, Jesmin. (2015). Accountability of Accounting Stakeholders. Global Journal of

Management and Business Research. 15. 5-10.

Madhuri Thakur, (2022), budgetary control, [Online] Available at:

https://www.wallstreetmojo.com/budgetary-control/#h-advantages-and-disadvantages-of-

budgetary-control, [Accessed on: 9 June 2022].

Song, J., Martens, A. and Vanhoucke, M., 2020. The impact of a limited budget on the corrective

action taking process. European Journal of Operational Research, 286(3), pp.1070-1086.

L Zimmerman, J., 2011. Accounting for decision making and control. McGraw-Hill/Irwin.

Abraham Cardoza, Jr. (2020), what are the rules of accounting? [Online] Available at:

https://www.quora.com/What-are-the-rules-of-accounting?q=what%20is%20accounting

%20rules%20and%20regualtions%20and%20ethics, [Accessed on: 8 June 2022].

Kyle Maclay, (2022), accounting regulation and ethics, [online] Available at:

https://www.personalfinancelab.com/finance-knowledge/accounting/accounting-regulation-and-

ethics/, [Accessed on: 8 June 2022].

Hall, J.A., 2015. Accounting information systems. Cengage Learning.

Azim, Md & Ara, Jesmin. (2015). Accountability of Accounting Stakeholders. Global Journal of

Management and Business Research. 15. 5-10.

Madhuri Thakur, (2022), budgetary control, [Online] Available at:

https://www.wallstreetmojo.com/budgetary-control/#h-advantages-and-disadvantages-of-

budgetary-control, [Accessed on: 9 June 2022].

Song, J., Martens, A. and Vanhoucke, M., 2020. The impact of a limited budget on the corrective

action taking process. European Journal of Operational Research, 286(3), pp.1070-1086.

L Zimmerman, J., 2011. Accounting for decision making and control. McGraw-Hill/Irwin.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.