Accounting Techniques in Financial Statement Analysis for Carrefour

VerifiedAdded on 2022/03/15

|31

|6808

|254

Report

AI Summary

This report provides a detailed analysis of the application of financial and management accounting techniques within Carrefour Supermarket. It explores the purposes of the accounting function, including budgeting, planning, decision-making, compliance with laws, reporting, and fraud prevention. The report delves into ethical and regulatory constraints, examining issues such as manipulation of figures, greed, confidentiality, and misappropriation of assets. It also covers the nature of accounting, generally accepted accounting principles (GAAP), and the context and purpose of the accounting function, differentiating between financial, managerial, and cost accounting. Appendices provide additional context on sole proprietorships, partnerships, ratios, and non-profit organizations. Furthermore, it discusses the benefits and limitations of budgets and budgetary planning for an organization, offering a comprehensive overview of accounting principles in a real-world business context.

1 | P a g e

ACCOUNTING PRINCIPLE

ASSIGNMENT TITLE: APPLICATION OF FINANCIAL AND

MANAGEMENT ACCOUNTING TECHNIQUES IN THE

PREPARATION AND ANALYSIS OF FINANCIAL

STATEMENTS IN AN ORGANISATION.

DATE: 11/15/2021

ACCOUNTING PRINCIPLE

ASSIGNMENT TITLE: APPLICATION OF FINANCIAL AND

MANAGEMENT ACCOUNTING TECHNIQUES IN THE

PREPARATION AND ANALYSIS OF FINANCIAL

STATEMENTS IN AN ORGANISATION.

DATE: 11/15/2021

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2 | P a g e

Contents

Purposes of accounting function within Carrefour Supermarket..................................................20

Budgeting and planning.............................................................................................................20

Decision making........................................................................................................................20

Compliance of the law...............................................................................................................20

Reporting and financial statements............................................................................................21

Avoiding fraud...........................................................................................................................21

Accounting function within Carrefour in the context of regulatory and ethical constraints.........21

Ethical constraints in accounting...............................................................................................21

Manipulation of figures.........................................................................................................22

Effects of greed......................................................................................................................22

Confidentiality.......................................................................................................................22

Misappropriation of assets.....................................................................................................22

Regulatory constraints in accounting.............................................................................................23

Nature of accounting..................................................................................................................23

Generally accepted accounting principles (Gaap).....................................................................23

Context and purpose of the accounting function clearly showing the role of accounting in

informing decision.........................................................................................................................24

Financial accounting..................................................................................................................25

Managerial accounting...............................................................................................................25

Cost accounting.....................................................................................................................25

Appendix 1.....................................................................................................................................28

Sole proprietorship.....................................................................................................................28

Appendix 2.....................................................................................................................................30

Partnership.................................................................................................................................30

Appendix 3.....................................................................................................................................32

Ratios.........................................................................................................................................32

Liquidity ratios.......................................................................................................................32

Turnover ratios.......................................................................................................................33

Profitability ratios..................................................................................................................34

Contents

Purposes of accounting function within Carrefour Supermarket..................................................20

Budgeting and planning.............................................................................................................20

Decision making........................................................................................................................20

Compliance of the law...............................................................................................................20

Reporting and financial statements............................................................................................21

Avoiding fraud...........................................................................................................................21

Accounting function within Carrefour in the context of regulatory and ethical constraints.........21

Ethical constraints in accounting...............................................................................................21

Manipulation of figures.........................................................................................................22

Effects of greed......................................................................................................................22

Confidentiality.......................................................................................................................22

Misappropriation of assets.....................................................................................................22

Regulatory constraints in accounting.............................................................................................23

Nature of accounting..................................................................................................................23

Generally accepted accounting principles (Gaap).....................................................................23

Context and purpose of the accounting function clearly showing the role of accounting in

informing decision.........................................................................................................................24

Financial accounting..................................................................................................................25

Managerial accounting...............................................................................................................25

Cost accounting.....................................................................................................................25

Appendix 1.....................................................................................................................................28

Sole proprietorship.....................................................................................................................28

Appendix 2.....................................................................................................................................30

Partnership.................................................................................................................................30

Appendix 3.....................................................................................................................................32

Ratios.........................................................................................................................................32

Liquidity ratios.......................................................................................................................32

Turnover ratios.......................................................................................................................33

Profitability ratios..................................................................................................................34

3 | P a g e

Gearing ratios.........................................................................................................................35

Appendix 4.....................................................................................................................................37

Non-profit organizations............................................................................................................37

Appendix 5.....................................................................................................................................40

Cash budget...............................................................................................................................40

Benefits and limitations of budgets and budgetary planning, and control for an organization. 41

Benefits..................................................................................................................................41

Limitations.............................................................................................................................42

References......................................................................................................................................44

Gearing ratios.........................................................................................................................35

Appendix 4.....................................................................................................................................37

Non-profit organizations............................................................................................................37

Appendix 5.....................................................................................................................................40

Cash budget...............................................................................................................................40

Benefits and limitations of budgets and budgetary planning, and control for an organization. 41

Benefits..................................................................................................................................41

Limitations.............................................................................................................................42

References......................................................................................................................................44

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4 | P a g e

Purposes of accounting function within Carrefour Supermarket

Accounting is referred to as the practice of analyzing, summarizing and recording financial

transactions and activities. There are various types of accounting such as forensic, management

and government accounting. Accounting is mostly essential to business owners, investors and

stakeholders. Regarding Carrefour, the accounting department should be able to produce critical

information such as profit and loss that is needed to analyze the financial status of an

organization (Freshbooks, 2020).

The different purposes of accounting within Carrefour include;

Budgeting and planning

Accountants are responsible for developing the organization’s budget. Accountants create annual

budgets using historical financial data and future revenue projections. Accountants also create

different budgets for individual departments within the business (Indeed, 2021). For instance,

Carrefour must plan on how they will use resources such as machinery, labor and so on.

Decision making

Accounting aids the business in a variety of decision making procedures and also aids business

owners in creating policies to optimize the efficiency of business operations. Carrefour will have

to make accounting based choices that include, resources required to manufacture products and

services, creating price points for their items as well as financing business opportunities

(Freshbooks, 2020).

Compliance of the law

An organization must follow its governments laws and standards such as those imposed by the

Kenyan Revenue Authority (KRA). Counties also impose monetary regulations on businesses.

Accounting will help to make sure that Carrefour’s financials are complying with their states

laws and regulations (Indeed, 2021).

Purposes of accounting function within Carrefour Supermarket

Accounting is referred to as the practice of analyzing, summarizing and recording financial

transactions and activities. There are various types of accounting such as forensic, management

and government accounting. Accounting is mostly essential to business owners, investors and

stakeholders. Regarding Carrefour, the accounting department should be able to produce critical

information such as profit and loss that is needed to analyze the financial status of an

organization (Freshbooks, 2020).

The different purposes of accounting within Carrefour include;

Budgeting and planning

Accountants are responsible for developing the organization’s budget. Accountants create annual

budgets using historical financial data and future revenue projections. Accountants also create

different budgets for individual departments within the business (Indeed, 2021). For instance,

Carrefour must plan on how they will use resources such as machinery, labor and so on.

Decision making

Accounting aids the business in a variety of decision making procedures and also aids business

owners in creating policies to optimize the efficiency of business operations. Carrefour will have

to make accounting based choices that include, resources required to manufacture products and

services, creating price points for their items as well as financing business opportunities

(Freshbooks, 2020).

Compliance of the law

An organization must follow its governments laws and standards such as those imposed by the

Kenyan Revenue Authority (KRA). Counties also impose monetary regulations on businesses.

Accounting will help to make sure that Carrefour’s financials are complying with their states

laws and regulations (Indeed, 2021).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5 | P a g e

Reporting and financial statements

The provision of financial statements is yet another responsibility of accountants within a

business. The business’s accountants compile financial data primarily to create accurate and

truthful reports and financial statements such as income statements and balance sheets and

internal communications (Luenendonk, 2021).

Accountants are also in charge of preparing financial statements at the end of every year.

Carrefour can use these reports in order to engage with investors and stakeholders and to also

generate leads (Luenendonk, 2021).

Avoiding fraud

An accountant will ensure that capital is neither mishandled or wasted inside a business.

Accountants are aiming to safeguard the business’s assets from internal or an eternal fraud

attack, nowadays this is usually done via cybersecurity. Carrefour should monitor its financial

data to ensure that funds are not being mishandled or misappropriated by the employees for their

own benefit (Indeed, 2021).

Accounting function within Carrefour in the context of

regulatory and ethical constraints

Ethical constraints in accounting

Ethical constraints are implications that one must operate within the socially recognized norms

and standards in order to avoid committing any type of offence (Mattwattsmedia, 2012).

Managing ethical concerns within a business is generally quite difficult for most business

owners. It is Carrefour’s management’s responsibility to bring accountability to employees who

are unethical (Holton, 2020).

The following are some of the ethical issues that the Carrefour accounting department

should look to avoid;

Reporting and financial statements

The provision of financial statements is yet another responsibility of accountants within a

business. The business’s accountants compile financial data primarily to create accurate and

truthful reports and financial statements such as income statements and balance sheets and

internal communications (Luenendonk, 2021).

Accountants are also in charge of preparing financial statements at the end of every year.

Carrefour can use these reports in order to engage with investors and stakeholders and to also

generate leads (Luenendonk, 2021).

Avoiding fraud

An accountant will ensure that capital is neither mishandled or wasted inside a business.

Accountants are aiming to safeguard the business’s assets from internal or an eternal fraud

attack, nowadays this is usually done via cybersecurity. Carrefour should monitor its financial

data to ensure that funds are not being mishandled or misappropriated by the employees for their

own benefit (Indeed, 2021).

Accounting function within Carrefour in the context of

regulatory and ethical constraints

Ethical constraints in accounting

Ethical constraints are implications that one must operate within the socially recognized norms

and standards in order to avoid committing any type of offence (Mattwattsmedia, 2012).

Managing ethical concerns within a business is generally quite difficult for most business

owners. It is Carrefour’s management’s responsibility to bring accountability to employees who

are unethical (Holton, 2020).

The following are some of the ethical issues that the Carrefour accounting department

should look to avoid;

6 | P a g e

Manipulation of figures

Operating a business might be very pressuring for some business owners. The business owners

of Carrefour may have the urge to get their accounting department to manipulate financial data.

This is not an ideal situation for accountants, as they have a legal and ethical duty to correctly

present Carrefour’s financial status, and the failure to do exactly just this can lead to criminal or

civil consequences (Decker, 2019).

Effects of greed

Businesses face a lot of cases where their accountants will break ethical boundaries in the sake of

generating more money. An accountant who works in the Carrefour shouldn’t let their financial

desires skew their ethical behavior, he or she must adhere to the business’s ethical financial

reporting guidelines (Content, 2017).

Confidentiality

Professional accountants are expected to protect the privacy and confidentiality of sensitive

information that could be obtained via business and professional relations. This sensitive

information should never be revealed to any third parties without getting permission or it’s a

legal matter and they are forced to disclose the information. Accountants working for Carrefour

should know that it is unethical for them to break this code of conduct (Nordmeyer, 2018).

Misappropriation of assets

Carrefour may also face misappropriation of assets from their accountants. The use of business

assets for purposes that are not in line with company interests is referred to as asset

misappropriation. A top executive, for example could bill a family lunch on to Carrefour as a

business cost (Freedman, 2019).

Manipulation of figures

Operating a business might be very pressuring for some business owners. The business owners

of Carrefour may have the urge to get their accounting department to manipulate financial data.

This is not an ideal situation for accountants, as they have a legal and ethical duty to correctly

present Carrefour’s financial status, and the failure to do exactly just this can lead to criminal or

civil consequences (Decker, 2019).

Effects of greed

Businesses face a lot of cases where their accountants will break ethical boundaries in the sake of

generating more money. An accountant who works in the Carrefour shouldn’t let their financial

desires skew their ethical behavior, he or she must adhere to the business’s ethical financial

reporting guidelines (Content, 2017).

Confidentiality

Professional accountants are expected to protect the privacy and confidentiality of sensitive

information that could be obtained via business and professional relations. This sensitive

information should never be revealed to any third parties without getting permission or it’s a

legal matter and they are forced to disclose the information. Accountants working for Carrefour

should know that it is unethical for them to break this code of conduct (Nordmeyer, 2018).

Misappropriation of assets

Carrefour may also face misappropriation of assets from their accountants. The use of business

assets for purposes that are not in line with company interests is referred to as asset

misappropriation. A top executive, for example could bill a family lunch on to Carrefour as a

business cost (Freedman, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7 | P a g e

Regulatory constraints in accounting

Nature of accounting

The nature of accounting can be broken down to qualitative attributes and quantitative attributes.

Qualitative characteristics simplify and expand on financial data to make sure that outcomes are

easily understood and comparable. These attributes include, reliability, relevance,

understandability, comparability and faithful presentation (Commerceiets, 2019).

Quantitative attributes of accounting are simply preparing financial statements in a measurable

form and assigning them to relevant users. Some of these attributes include recording of financial

transactions only, classifying the transactions and summarizing the transactions (EP, 2020).

In order to preserve the quantitative and qualitative attributes of accounting, the regulatory body

GAAP has created various principles that a business’s accounting function must use whilst

creating financial statements. While widely recognized accounting standards seek to eliminate

erroneous financial reporting and help businesses in generating accurate and valid financial

information, they do have limitations that have constrained Carrefour’s accounting function

(Indeed, 2021).

Generally accepted accounting principles (Gaap)

The following are some of the principles that Carrefour’s accounting function is constrained to

regarding GAAP;

Reliability principle: This principle requires for Carrefour to only document transactions

which can be verified using objective proof. Forms of objective proof can include, bank

statements, checks, receipts and so on (Bragg, 2021).

Relevance principle: The relevance principle states that the information obtained from

an accounting system should be able to aid the end-users in making key decisions.

Carrefour’s external and internal stakeholders can be considered end users. Carrefour’s

employees are examples of internal stakeholders while external stakeholders include

lenders, investors and so on. For the information to be deemed relevant it must be clear,

Regulatory constraints in accounting

Nature of accounting

The nature of accounting can be broken down to qualitative attributes and quantitative attributes.

Qualitative characteristics simplify and expand on financial data to make sure that outcomes are

easily understood and comparable. These attributes include, reliability, relevance,

understandability, comparability and faithful presentation (Commerceiets, 2019).

Quantitative attributes of accounting are simply preparing financial statements in a measurable

form and assigning them to relevant users. Some of these attributes include recording of financial

transactions only, classifying the transactions and summarizing the transactions (EP, 2020).

In order to preserve the quantitative and qualitative attributes of accounting, the regulatory body

GAAP has created various principles that a business’s accounting function must use whilst

creating financial statements. While widely recognized accounting standards seek to eliminate

erroneous financial reporting and help businesses in generating accurate and valid financial

information, they do have limitations that have constrained Carrefour’s accounting function

(Indeed, 2021).

Generally accepted accounting principles (Gaap)

The following are some of the principles that Carrefour’s accounting function is constrained to

regarding GAAP;

Reliability principle: This principle requires for Carrefour to only document transactions

which can be verified using objective proof. Forms of objective proof can include, bank

statements, checks, receipts and so on (Bragg, 2021).

Relevance principle: The relevance principle states that the information obtained from

an accounting system should be able to aid the end-users in making key decisions.

Carrefour’s external and internal stakeholders can be considered end users. Carrefour’s

employees are examples of internal stakeholders while external stakeholders include

lenders, investors and so on. For the information to be deemed relevant it must be clear,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8 | P a g e

timely and useful to aid end-users such as investors to make key decisions (Banerjee,

2021).

Understandability principle: Understandability refers to the idea that financial data

must be given in such a way that a user such as an investor can readily comprehend it.

This notion implies the user has a basic understanding in accounting. Adhering to a fair

degree of understandability can preclude Carrefour from purposefully obscuring financial

data to deceive users of the financial statements. In order for accounting information to

be understandable, it must be clear, concise, complete and organized (Bragg, 2021).

Comparability principle: The comparability principle helps users such as investors to

compare financial performance and situations over time and also with other businesses.

Comparability increases the value of Carrefour’s financial statements as it allows the

users to carry out analysis such as cross-sectional, common-size and trend analysis.

Carrefour may use cross-sectional analysis to make a performance comparison with that

of its competitors (Jan, 2020).

Faithful presentation: The notion of faithful representation requires for Carrefour to

produce its financial statements correctly reflecting the its current situation. For instance,

if Carrefour recorded on its balance sheet fifty thousand in October then it should be so.

For accounting data to be faithfully represented then it should be unbiased, error free and

complete (Bragg, 2021).

Context and purpose of the accounting function clearly showing

the role of accounting in informing decision

Accounting plays a vital role when it comes to decision making and decision making is done

mainly through two forms of accounting, this being, financial accounting and cost accounting

within managerial accounting. The main distinction between managerial and financial

accounting would be that financial accounting information is more provided to external parties

such as investors whilst managerial accounting information is intended more to assist the

businesses management in making decisions for the business (Kenton, 2020).

timely and useful to aid end-users such as investors to make key decisions (Banerjee,

2021).

Understandability principle: Understandability refers to the idea that financial data

must be given in such a way that a user such as an investor can readily comprehend it.

This notion implies the user has a basic understanding in accounting. Adhering to a fair

degree of understandability can preclude Carrefour from purposefully obscuring financial

data to deceive users of the financial statements. In order for accounting information to

be understandable, it must be clear, concise, complete and organized (Bragg, 2021).

Comparability principle: The comparability principle helps users such as investors to

compare financial performance and situations over time and also with other businesses.

Comparability increases the value of Carrefour’s financial statements as it allows the

users to carry out analysis such as cross-sectional, common-size and trend analysis.

Carrefour may use cross-sectional analysis to make a performance comparison with that

of its competitors (Jan, 2020).

Faithful presentation: The notion of faithful representation requires for Carrefour to

produce its financial statements correctly reflecting the its current situation. For instance,

if Carrefour recorded on its balance sheet fifty thousand in October then it should be so.

For accounting data to be faithfully represented then it should be unbiased, error free and

complete (Bragg, 2021).

Context and purpose of the accounting function clearly showing

the role of accounting in informing decision

Accounting plays a vital role when it comes to decision making and decision making is done

mainly through two forms of accounting, this being, financial accounting and cost accounting

within managerial accounting. The main distinction between managerial and financial

accounting would be that financial accounting information is more provided to external parties

such as investors whilst managerial accounting information is intended more to assist the

businesses management in making decisions for the business (Kenton, 2020).

9 | P a g e

Financial accounting

Through financial accounting Carrefour can collect and report the financial information that

flows in and out of their business, allowing the management as well as external analysts and

investors to evaluate the business’s financial health therefore making educated decisions (Drury,

2021).

The following are the major ways in which financial accounting aids in making decisions;

Financial accounting gives investors a starting point for analyzing and comparing the

financial health of businesses issuing securities to know whether it is well values or not,

if it is they can decide to invest into Carrefour by buying into shares of the business

(Drury, 2021).

Financial accounting aids creditors in determining Carrefour’s solvency and credibility.

When the business has generated the appropriate financial statements detailing all its

assets and debt, lenders attain a better understanding of the company’s credibility and

they can make a decision such as lending Carrefour capital to buy more equipment for

manufacturing (Drury, 2021). An example of this financial statement can be a balance

sheet that shows investors all the assets and liabilities that Carrefour owns.

Financial accounting enables outside stakeholders to assess a company's profitability and

worth. An investor can determine whether Carrefour has regularly outperformed, paid

dividends, and look to have favorable margins. A lender can examine financial data such

as fixed charge coverage ratio to determine liquidity, cash flow, leverage, and overall

solvency to figure out whether the business has substantial cash flow available to be able

to reimburse debt, therefore helping an investor make decisions such as funding a new

product idea from Carrefour (Drury, 2021).

Managerial accounting

Cost accounting

A business’s management uses cost accounting to determine all variables and fixed costs

involved with the manufacturing. Input expenses are compared with output results to help assess

financial success and make decisions in the long term (Tuovila, 2021).

Financial accounting

Through financial accounting Carrefour can collect and report the financial information that

flows in and out of their business, allowing the management as well as external analysts and

investors to evaluate the business’s financial health therefore making educated decisions (Drury,

2021).

The following are the major ways in which financial accounting aids in making decisions;

Financial accounting gives investors a starting point for analyzing and comparing the

financial health of businesses issuing securities to know whether it is well values or not,

if it is they can decide to invest into Carrefour by buying into shares of the business

(Drury, 2021).

Financial accounting aids creditors in determining Carrefour’s solvency and credibility.

When the business has generated the appropriate financial statements detailing all its

assets and debt, lenders attain a better understanding of the company’s credibility and

they can make a decision such as lending Carrefour capital to buy more equipment for

manufacturing (Drury, 2021). An example of this financial statement can be a balance

sheet that shows investors all the assets and liabilities that Carrefour owns.

Financial accounting enables outside stakeholders to assess a company's profitability and

worth. An investor can determine whether Carrefour has regularly outperformed, paid

dividends, and look to have favorable margins. A lender can examine financial data such

as fixed charge coverage ratio to determine liquidity, cash flow, leverage, and overall

solvency to figure out whether the business has substantial cash flow available to be able

to reimburse debt, therefore helping an investor make decisions such as funding a new

product idea from Carrefour (Drury, 2021).

Managerial accounting

Cost accounting

A business’s management uses cost accounting to determine all variables and fixed costs

involved with the manufacturing. Input expenses are compared with output results to help assess

financial success and make decisions in the long term (Tuovila, 2021).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10 | P a g e

The following are the various types of costs in cost accounting;

Fixed costs: These are the types of costs which do not fluctuate with the volume of

production. Often these costs are things such as leases and mortgage payments on a

structure or an equipment which is depreciated at a month-to-month rate. Those costs

would not change at all whether output levels increased or decreased (Tuovila, 2021).

Variable costs: These are that costs that are directly affected by the business’s volume of

production. For example, if Carrefour is to increase production specifically for the

Christmas holidays, it’s inventory may suffer greater expenses when it acquires a large

amount of items from suppliers (Tuovila, 2021).

Operating costs: These are the type of costs that are connected to the business’s daily

activities. Based on circumstances, these expenses can be variable ore fixed. For

example, if Carrefour has a payroll where it’s employees get paid a certain amount of

salary based on their level of work output then the cost is variable, but if they get paid the

same salary no matter the circumstance, then the cost is fixed (Tuovila, 2021).

Carrefour’s managerial accountants help them examine the progressive advantage of increasing

output, which is known as margin analysis. This leads towards breakeven analysis, that entails

computing the contribution margin of sales mix in order to then find the volume of units that

Carrefour’s gross sales match the total expenses. This material is to be used by the managerial

accountants to establish the pricing point range for items (Freshbooks, 2021).

Carrefour’s managerial accountants use financial information to aid Carrefour in determining

where, when and the amount of capital to spend. Utilizing basic budgetary performance

measures like internal rate of return and net present value to assist decision making on whether

or not they should undertake purchases or costly projects. The process entails examining

propositions, determining whether there is or isn’t a demand for certain products, and

determining the best methods to finance for the purchases. This even specifies repayment

periods, allowing management to forecast future benefits and costs (Freshbooks, 2021).

The bottom line is that, accounting allows companies to monitor their activities while also

providing an overview of their financial condition. By Carrefour giving their lenders and

investors and themselves an overview of its financial information through various financial

The following are the various types of costs in cost accounting;

Fixed costs: These are the types of costs which do not fluctuate with the volume of

production. Often these costs are things such as leases and mortgage payments on a

structure or an equipment which is depreciated at a month-to-month rate. Those costs

would not change at all whether output levels increased or decreased (Tuovila, 2021).

Variable costs: These are that costs that are directly affected by the business’s volume of

production. For example, if Carrefour is to increase production specifically for the

Christmas holidays, it’s inventory may suffer greater expenses when it acquires a large

amount of items from suppliers (Tuovila, 2021).

Operating costs: These are the type of costs that are connected to the business’s daily

activities. Based on circumstances, these expenses can be variable ore fixed. For

example, if Carrefour has a payroll where it’s employees get paid a certain amount of

salary based on their level of work output then the cost is variable, but if they get paid the

same salary no matter the circumstance, then the cost is fixed (Tuovila, 2021).

Carrefour’s managerial accountants help them examine the progressive advantage of increasing

output, which is known as margin analysis. This leads towards breakeven analysis, that entails

computing the contribution margin of sales mix in order to then find the volume of units that

Carrefour’s gross sales match the total expenses. This material is to be used by the managerial

accountants to establish the pricing point range for items (Freshbooks, 2021).

Carrefour’s managerial accountants use financial information to aid Carrefour in determining

where, when and the amount of capital to spend. Utilizing basic budgetary performance

measures like internal rate of return and net present value to assist decision making on whether

or not they should undertake purchases or costly projects. The process entails examining

propositions, determining whether there is or isn’t a demand for certain products, and

determining the best methods to finance for the purchases. This even specifies repayment

periods, allowing management to forecast future benefits and costs (Freshbooks, 2021).

The bottom line is that, accounting allows companies to monitor their activities while also

providing an overview of their financial condition. By Carrefour giving their lenders and

investors and themselves an overview of its financial information through various financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11 | P a g e

statements such as income statements, it gives them more confirmation when it comes to

decision making (Drury, 2021).

The following are the different users that use accounting information to make decisions;

Investors: People who want to invest in Carrefour will want to know about its performance and

financial status. As a result, they obtain this information from the company's accounting records

(Accountingsimplified, 2021).

Lenders: Banks and as well as other lending institutions need to know that their money will be

reimbursed before the deadlines. Furthermore, financial data assists lenders in assessing such a

stance. As a result, banks as well as other lending institutions will use financial statements to

determine the acceptance for an application for Carrefour’s loan (Accountingsimplified, 2021).

Managers: Successful budget preparation and monitoring need accurate accounting data

pertaining to Carrefour’s numerous operations, goods, divisions and departments. Managers also

use accounting to monitor the organizations performance in comparison to historical results and

deciding whether or not to adjust business strategies depending on the results

(Accountingsimplified, 2021).

Owners: Accounting information assists Carrefour’s owners in determining the amount of

stability with in business over time as well as the magnitude to which change in the economic

conditions have influenced the financial performance of the business (Accountingsimplified,

2021).

statements such as income statements, it gives them more confirmation when it comes to

decision making (Drury, 2021).

The following are the different users that use accounting information to make decisions;

Investors: People who want to invest in Carrefour will want to know about its performance and

financial status. As a result, they obtain this information from the company's accounting records

(Accountingsimplified, 2021).

Lenders: Banks and as well as other lending institutions need to know that their money will be

reimbursed before the deadlines. Furthermore, financial data assists lenders in assessing such a

stance. As a result, banks as well as other lending institutions will use financial statements to

determine the acceptance for an application for Carrefour’s loan (Accountingsimplified, 2021).

Managers: Successful budget preparation and monitoring need accurate accounting data

pertaining to Carrefour’s numerous operations, goods, divisions and departments. Managers also

use accounting to monitor the organizations performance in comparison to historical results and

deciding whether or not to adjust business strategies depending on the results

(Accountingsimplified, 2021).

Owners: Accounting information assists Carrefour’s owners in determining the amount of

stability with in business over time as well as the magnitude to which change in the economic

conditions have influenced the financial performance of the business (Accountingsimplified,

2021).

12 | P a g e

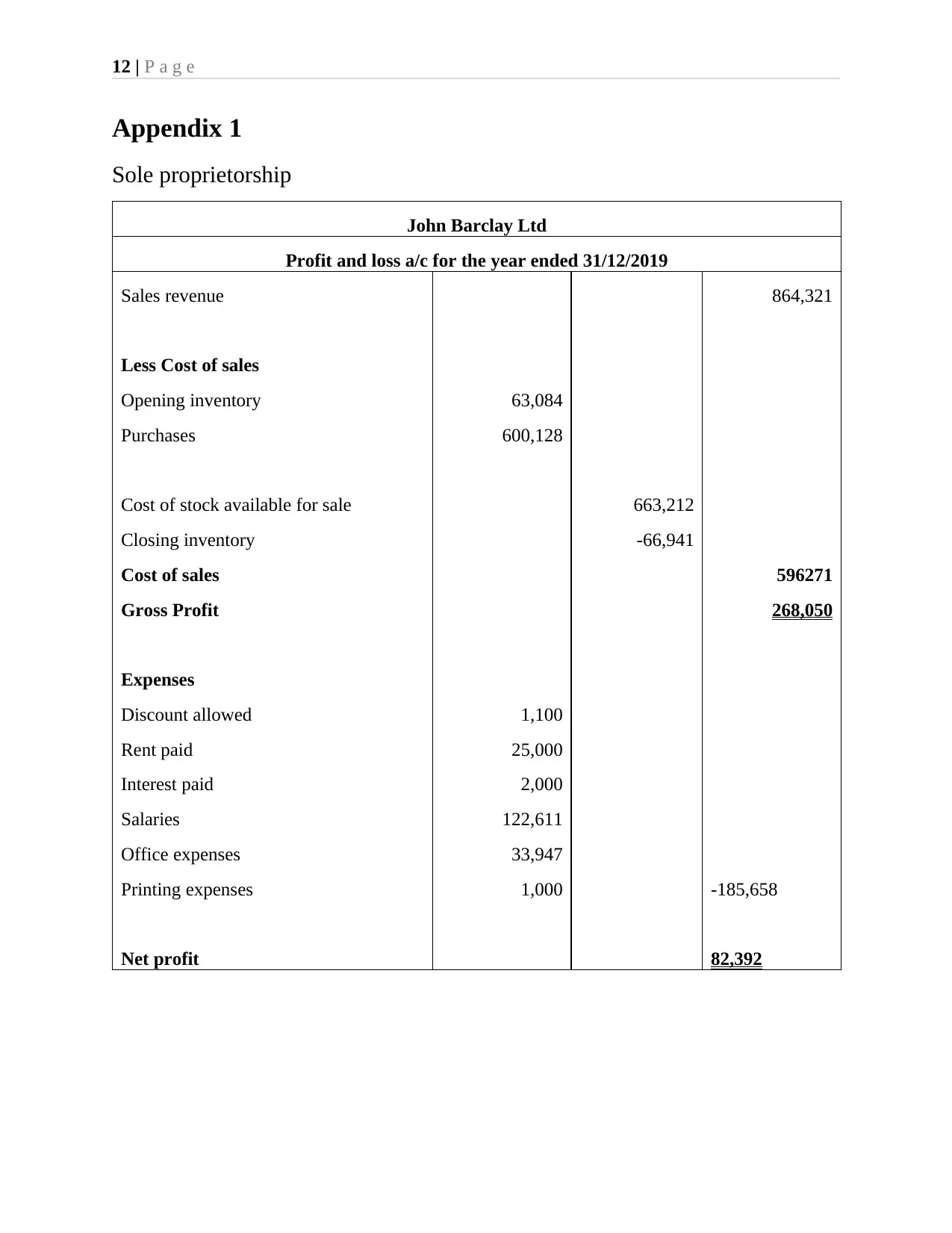

Appendix 1

Sole proprietorship

John Barclay Ltd

Profit and loss a/c for the year ended 31/12/2019

Sales revenue 864,321

Less Cost of sales

Opening inventory 63,084

Purchases 600,128

Cost of stock available for sale 663,212

Closing inventory -66,941

Cost of sales 596271

Gross Profit 268,050

Expenses

Discount allowed 1,100

Rent paid 25,000

Interest paid 2,000

Salaries 122,611

Office expenses 33,947

Printing expenses 1,000 -185,658

Net profit 82,392

Appendix 1

Sole proprietorship

John Barclay Ltd

Profit and loss a/c for the year ended 31/12/2019

Sales revenue 864,321

Less Cost of sales

Opening inventory 63,084

Purchases 600,128

Cost of stock available for sale 663,212

Closing inventory -66,941

Cost of sales 596271

Gross Profit 268,050

Expenses

Discount allowed 1,100

Rent paid 25,000

Interest paid 2,000

Salaries 122,611

Office expenses 33,947

Printing expenses 1,000 -185,658

Net profit 82,392

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 31

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.