Financial Accounting Report: Principles, Statements, and Analysis

VerifiedAdded on 2020/12/09

|24

|4016

|112

Report

AI Summary

This report provides a comprehensive overview of financial accounting principles and their practical application. It begins with an introduction to financial accounting, outlining its objectives and regulations, including the International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP). The report then delves into key accounting concepts such as materiality, consistency, and disclosure, explaining their significance in financial reporting. The report also includes practical examples, such as journal entries, ledger accounts, trial balances, and financial statements (profit and loss, balance sheet). Case studies are presented to illustrate accounting concepts like bank reconciliation, control accounts, and suspense accounts. Finally, the report concludes with a discussion of accounting concepts like prudence and consistency, and the role of depreciation in accounting, offering a well-rounded understanding of financial accounting principles and their real-world applications.

FINANCIAL

ACCOUNTING

PRINCIPLES

ACCOUNTING

PRINCIPLES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................4

Report about financial accounting along with its regulations.....................................................4

1. Financial Accounting with its objectives................................................................................4

Representing regulations of financial accounting.......................................................................5

Principles and function of Accounting for preparing financial statements................................6

Justifying different concepts of accounting such as materiality, consistency and disclosure.....7

CLIENT 1........................................................................................................................................8

1. Presenting Journal entries.......................................................................................................8

2. Presenting ledger account with context of double entry recording.........................................9

3. Determining the level of accuracy of trial balance.................................................................9

CLIENT 2......................................................................................................................................10

(a) Presenting statement of profit and loss for Sierra Laurent for year 2018 (July).................10

(b) Presenting statement of financial position for Sierra Laurent for year 2018 (July)............12

CLIENT 3......................................................................................................................................13

(a) Preparing statement of Profit and loss statement of LMS Ltd for 31st July 2018...............13

(b) Presenting statement of financial position for LMS Ltd for year 31st July 2018...............14

(c) Explaining the accounting concept of prudence and consistence........................................14

(d) Objective of depreciation for accounting along with its both method................................15

CLIENT 4......................................................................................................................................15

A) Objective of framing Bank Reconciliation Statement.........................................................15

(B) Listing areas which might create variances from bank statements.....................................16

C. Kendal's cash book along with its bank reconciliation statement........................................16

CLIENT 5......................................................................................................................................19

(a) Preparing Sales and Purchase ledger account .....................................................................19

(b) Define Control Account .....................................................................................................20

CLIENT 6......................................................................................................................................20

(a) Describing Suspense account along with its features..........................................................20

(b and c) Preparing trial balance...............................................................................................21

(d) Compare Clearing account and Suspense account.............................................................21

INTRODUCTION...........................................................................................................................4

Report about financial accounting along with its regulations.....................................................4

1. Financial Accounting with its objectives................................................................................4

Representing regulations of financial accounting.......................................................................5

Principles and function of Accounting for preparing financial statements................................6

Justifying different concepts of accounting such as materiality, consistency and disclosure.....7

CLIENT 1........................................................................................................................................8

1. Presenting Journal entries.......................................................................................................8

2. Presenting ledger account with context of double entry recording.........................................9

3. Determining the level of accuracy of trial balance.................................................................9

CLIENT 2......................................................................................................................................10

(a) Presenting statement of profit and loss for Sierra Laurent for year 2018 (July).................10

(b) Presenting statement of financial position for Sierra Laurent for year 2018 (July)............12

CLIENT 3......................................................................................................................................13

(a) Preparing statement of Profit and loss statement of LMS Ltd for 31st July 2018...............13

(b) Presenting statement of financial position for LMS Ltd for year 31st July 2018...............14

(c) Explaining the accounting concept of prudence and consistence........................................14

(d) Objective of depreciation for accounting along with its both method................................15

CLIENT 4......................................................................................................................................15

A) Objective of framing Bank Reconciliation Statement.........................................................15

(B) Listing areas which might create variances from bank statements.....................................16

C. Kendal's cash book along with its bank reconciliation statement........................................16

CLIENT 5......................................................................................................................................19

(a) Preparing Sales and Purchase ledger account .....................................................................19

(b) Define Control Account .....................................................................................................20

CLIENT 6......................................................................................................................................20

(a) Describing Suspense account along with its features..........................................................20

(b and c) Preparing trial balance...............................................................................................21

(d) Compare Clearing account and Suspense account.............................................................21

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................24

REFERENCES..............................................................................................................................24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting principles plays very important role in every organization as it

creates ease for determining future expenses and for purpose of controlling its cost on specific

operation which are performed in premises. The present report is giving brief discussion about

different accounting regulations, rules along with its principles. It had reflected their major

importance for accomplishing profitably and growth as it is followed by every industry. Further

it had shown various financial statements such as profit and loss, balance sheet and trial balance.

It is also articulating about different control account with its features and in same series it had

shown difference in suspense and clearing account.

Report about financial accounting along with its regulations

1. Financial Accounting with its objectives

Financial accounting is referred as specific branch of accounting, which directly traces

the financial statements of company in systematic manner. The transactions of any business

entity is measured, reported, collected and recorded on basis of shareholders and investors with

context of financial accounting. It is considered as a significant source for observing financial

stability and performance of any business entity, as it reflects report in fair and consistent

aspects. The statement should be framed by considering various financial standards such as

International Financial Reporting Standards (IFRS) and Generally Accepted Accounting

Principles (GAAP).

The main objectives of financial accounting are stated below:

Comparability

Relevance

Consistency

Reliability

Comparability: The financial statement would be easily compared from any other

organization's statements or with statement of previous year. There is presence of system which

had been established for reporting and recording financial statements which are prepared. It

would be creating too much ease for investors with reference to date which could be compared

Financial accounting principles plays very important role in every organization as it

creates ease for determining future expenses and for purpose of controlling its cost on specific

operation which are performed in premises. The present report is giving brief discussion about

different accounting regulations, rules along with its principles. It had reflected their major

importance for accomplishing profitably and growth as it is followed by every industry. Further

it had shown various financial statements such as profit and loss, balance sheet and trial balance.

It is also articulating about different control account with its features and in same series it had

shown difference in suspense and clearing account.

Report about financial accounting along with its regulations

1. Financial Accounting with its objectives

Financial accounting is referred as specific branch of accounting, which directly traces

the financial statements of company in systematic manner. The transactions of any business

entity is measured, reported, collected and recorded on basis of shareholders and investors with

context of financial accounting. It is considered as a significant source for observing financial

stability and performance of any business entity, as it reflects report in fair and consistent

aspects. The statement should be framed by considering various financial standards such as

International Financial Reporting Standards (IFRS) and Generally Accepted Accounting

Principles (GAAP).

The main objectives of financial accounting are stated below:

Comparability

Relevance

Consistency

Reliability

Comparability: The financial statement would be easily compared from any other

organization's statements or with statement of previous year. There is presence of system which

had been established for reporting and recording financial statements which are prepared. It

would be creating too much ease for investors with reference to date which could be compared

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and to be adjusted with process of decision making about its investments (Concepts of

Accounting Principles, 2018).

Relevance: The financial statement provides financial information that should be

relevant and applicable for its end user. All the financial statements must create ease for the

purpose of understanding and decision making with respect to financial performance of business

entity. The recent information is considered as relevant and it would be providing outcome on

quarterly and annual aspects.

Consistency: There is presence of various alterations in standards so this would be

creating deficiency for preparing statement with appropriate consistency. It became a reason for

standards so the end users of financial statement reflected data which is consistent and for

process of decision-making it created ease for comparing.

Reliability: The financial information that had been provided through financial

statements should be reliable. If in this context, investors would be not capable for attaining

reliable information as it creates difficulty for the process of decision-making. In the same series,

all reliable information should not mislead others as it should be free from biases so it would be

verified with much ease (McLaren, 2018).

Representing regulations of financial accounting

The financial information should be unbiased, fair, comparable, understandable and fair.

According to this, board has set regulations for developing, presenting and preparing financial

statements. The companies, which are listed under FTSE in United Kingdom, had to follow the

standards of GAAP. The organizations had to prepare financial statements with respect to

principles, which are abolished through GAAP. With reference to expansion of business entities

of global market international accounting, board have to follow these regulations such as IASB

and IFRS.

The various accounting regulations are stated below:

International accounting standard board (IASB): The specific objective of IASB is to

give appropriate disclosure of information with context of professionals. It provides significant

guidelines for particular objectives for framing database and reports with respect to financial

statements. It is also applicable for giving appropriate revaluation of accounts. The stakeholders

would accept a specific legal structure for identifying financial information and it would

influence number of investors with context of different countries.

Accounting Principles, 2018).

Relevance: The financial statement provides financial information that should be

relevant and applicable for its end user. All the financial statements must create ease for the

purpose of understanding and decision making with respect to financial performance of business

entity. The recent information is considered as relevant and it would be providing outcome on

quarterly and annual aspects.

Consistency: There is presence of various alterations in standards so this would be

creating deficiency for preparing statement with appropriate consistency. It became a reason for

standards so the end users of financial statement reflected data which is consistent and for

process of decision-making it created ease for comparing.

Reliability: The financial information that had been provided through financial

statements should be reliable. If in this context, investors would be not capable for attaining

reliable information as it creates difficulty for the process of decision-making. In the same series,

all reliable information should not mislead others as it should be free from biases so it would be

verified with much ease (McLaren, 2018).

Representing regulations of financial accounting

The financial information should be unbiased, fair, comparable, understandable and fair.

According to this, board has set regulations for developing, presenting and preparing financial

statements. The companies, which are listed under FTSE in United Kingdom, had to follow the

standards of GAAP. The organizations had to prepare financial statements with respect to

principles, which are abolished through GAAP. With reference to expansion of business entities

of global market international accounting, board have to follow these regulations such as IASB

and IFRS.

The various accounting regulations are stated below:

International accounting standard board (IASB): The specific objective of IASB is to

give appropriate disclosure of information with context of professionals. It provides significant

guidelines for particular objectives for framing database and reports with respect to financial

statements. It is also applicable for giving appropriate revaluation of accounts. The stakeholders

would accept a specific legal structure for identifying financial information and it would

influence number of investors with context of different countries.

International Financial reporting standards (IFRS): It had directly constituted as

contribution of Financial Reporting from 2005 in United Kingdom. It had been framed for

setting various global standards for preparing and disclosing financial statements. If single

accounting standard had been adopted for various countries as it gives financial information that

is consistent and could be comparable especially for investors. It gives guidance for purpose of

financial reporting instead of setting its regulations.

Principles and function of Accounting for preparing financial statements

There is presence of various concepts, principles and rules, which helps in governing

various uses of accounting.

The specific concepts and rules are stated below:

Historical Cost: The specific value of asset had to be stated in financial statement with

context of its original value but not on the present market value.

Business Entity: The financial statements would not consider any personal transactions

of owner and in this, same series business is known as separate entity from specific

owner.

Monetary unit: All the specific information should be recorded on monetary prospective

and if it is vice versa then it would not be recorded in statements. Monetary unit could be

describes as INR, $ etc.

Matching: In this principle, all expenses and revenue which are stated should be similar

within specific accounting period for getting actual earnings (Pawlowski, Nalbantis and

Coates, 2018).

Going concern: It would be considering an assumption that there will be continuity by

specific organization for performing in time period which is indefinite. On this particular

aspect, value of asset would be traced in financial statements.

Consistency: It is referred as accounting process which is applicable for business

perspective as it must be consistent, similar and alteration is necessity.

Accounting period: There is presence of accounting process within specific time

duration such as half yearly, fiscal year and quarterly.

contribution of Financial Reporting from 2005 in United Kingdom. It had been framed for

setting various global standards for preparing and disclosing financial statements. If single

accounting standard had been adopted for various countries as it gives financial information that

is consistent and could be comparable especially for investors. It gives guidance for purpose of

financial reporting instead of setting its regulations.

Principles and function of Accounting for preparing financial statements

There is presence of various concepts, principles and rules, which helps in governing

various uses of accounting.

The specific concepts and rules are stated below:

Historical Cost: The specific value of asset had to be stated in financial statement with

context of its original value but not on the present market value.

Business Entity: The financial statements would not consider any personal transactions

of owner and in this, same series business is known as separate entity from specific

owner.

Monetary unit: All the specific information should be recorded on monetary prospective

and if it is vice versa then it would not be recorded in statements. Monetary unit could be

describes as INR, $ etc.

Matching: In this principle, all expenses and revenue which are stated should be similar

within specific accounting period for getting actual earnings (Pawlowski, Nalbantis and

Coates, 2018).

Going concern: It would be considering an assumption that there will be continuity by

specific organization for performing in time period which is indefinite. On this particular

aspect, value of asset would be traced in financial statements.

Consistency: It is referred as accounting process which is applicable for business

perspective as it must be consistent, similar and alteration is necessity.

Accounting period: There is presence of accounting process within specific time

duration such as half yearly, fiscal year and quarterly.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Objectivity: The amount which had been recorded with respect to financial statements

must have presence of supporting evidence which is impartial.

Conservatism: There is presence of two specific amounts of option with context of

transaction of business, so in this series lower amount had been considered in financial

statements.

Materiality: it is referred as mistake in process of accounting which would be providing

impact to user's decision and it gained importance and there is requirement of reporting it

appropriately.

Justifying different concepts of accounting such as materiality, consistency and disclosure

Materiality This accounting concept is stating that organization must disclose each and

everything which is considered as very important for its users. There is

presence of various items which had created its importance to any other

organisation, as it could be ignored because it is not giving any major impact

on the context of financial entity of business. It is known as very important

accounting concepts which is creating help for auditors and accountant for

taking decision about classification of amount which is material or immaterial.

Consistency This specific method is implied on process of accounting should be consistent

from any particular financial period to other. If there is presence of any

alteration in accounting techniques to its disclosure and it had performed true

explanation on the context of financial statements. It is known as very

important measure for comparability which helps in enabling investors along

with its users of financial statements for comparison it from previous year's

statements. The accounting policies could be altered along with its techniques

if there is presence of more than one reasonable ground which would directly

reflect in financial performance and stability of organization (Trucco, 2015).

Full Disclosure This concept is directly linked to materiality as it had huge requirement for

disclosing each financial detail such as accounting policies with respect to

financial statements. The creditors and investors had gained huge knowledge

of all information which is relevant in context of operation of organization on

particular basis of accounting. This specific principle is elaborating alterations

must have presence of supporting evidence which is impartial.

Conservatism: There is presence of two specific amounts of option with context of

transaction of business, so in this series lower amount had been considered in financial

statements.

Materiality: it is referred as mistake in process of accounting which would be providing

impact to user's decision and it gained importance and there is requirement of reporting it

appropriately.

Justifying different concepts of accounting such as materiality, consistency and disclosure

Materiality This accounting concept is stating that organization must disclose each and

everything which is considered as very important for its users. There is

presence of various items which had created its importance to any other

organisation, as it could be ignored because it is not giving any major impact

on the context of financial entity of business. It is known as very important

accounting concepts which is creating help for auditors and accountant for

taking decision about classification of amount which is material or immaterial.

Consistency This specific method is implied on process of accounting should be consistent

from any particular financial period to other. If there is presence of any

alteration in accounting techniques to its disclosure and it had performed true

explanation on the context of financial statements. It is known as very

important measure for comparability which helps in enabling investors along

with its users of financial statements for comparison it from previous year's

statements. The accounting policies could be altered along with its techniques

if there is presence of more than one reasonable ground which would directly

reflect in financial performance and stability of organization (Trucco, 2015).

Full Disclosure This concept is directly linked to materiality as it had huge requirement for

disclosing each financial detail such as accounting policies with respect to

financial statements. The creditors and investors had gained huge knowledge

of all information which is relevant in context of operation of organization on

particular basis of accounting. This specific principle is elaborating alterations

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

for decisions of external user with reference to specific organization as it

should give appropriate financial statements along with disclosure. The users

get ensured that there is not any lack of information and along with this it is

not misleading any financial statements.

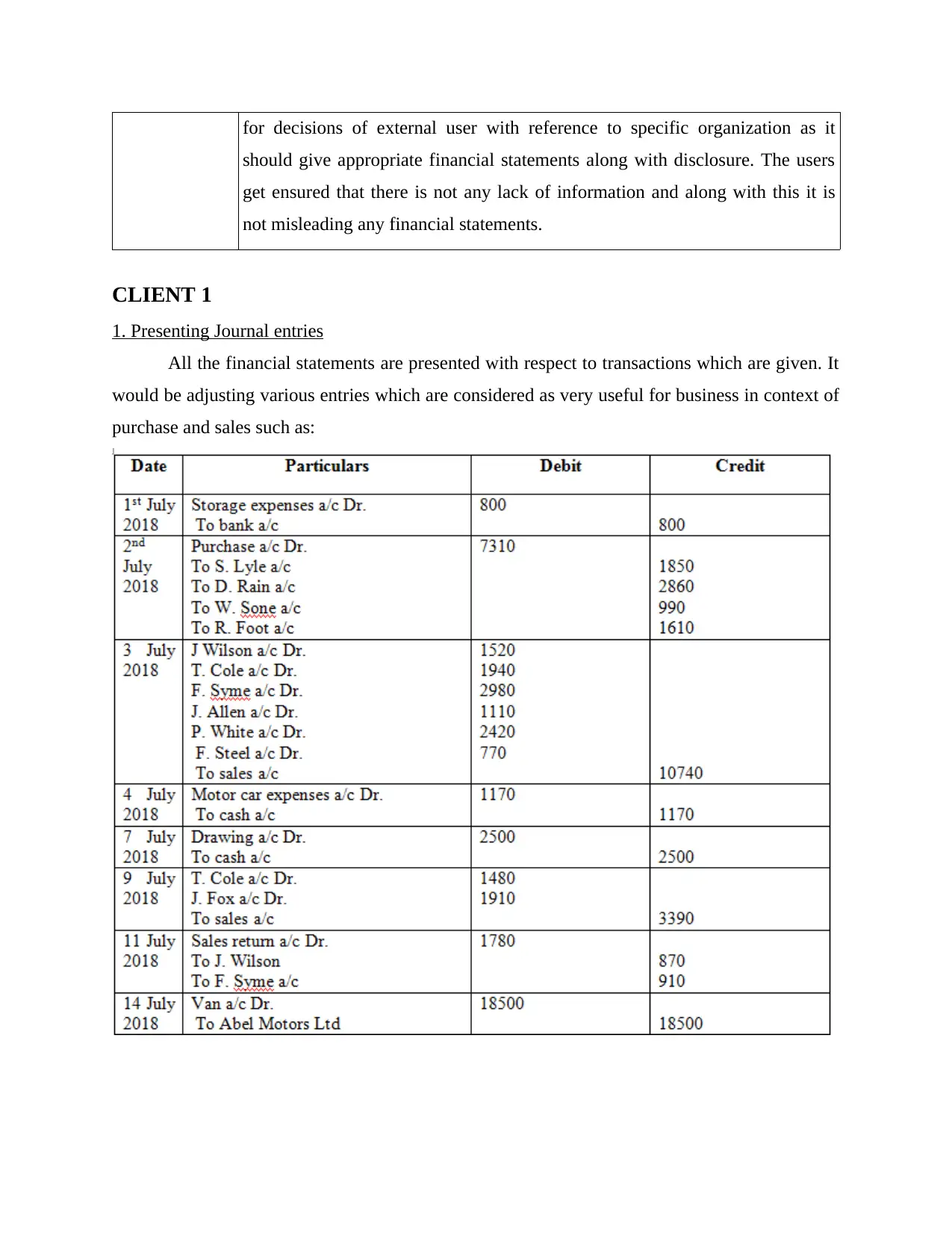

CLIENT 1

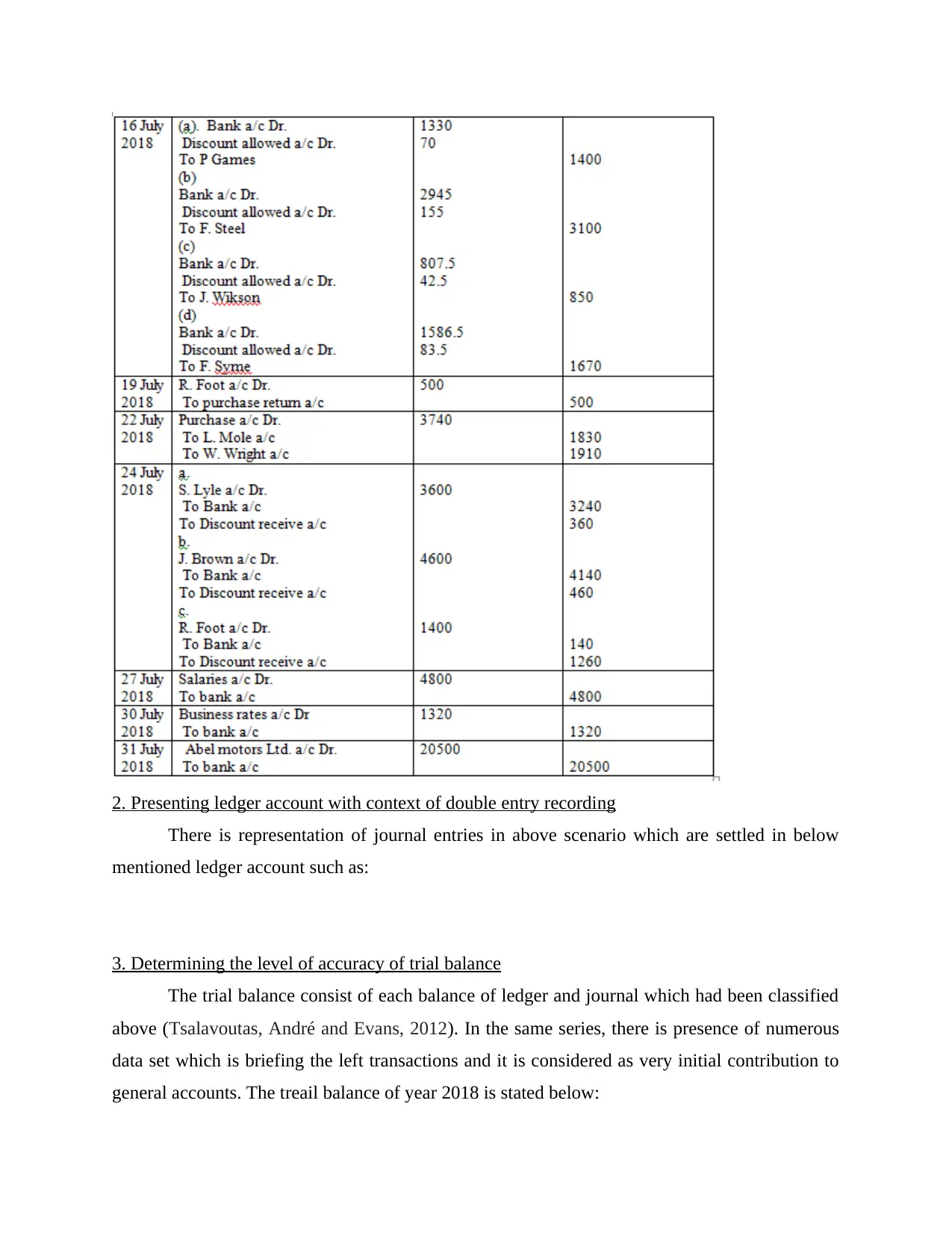

1. Presenting Journal entries

All the financial statements are presented with respect to transactions which are given. It

would be adjusting various entries which are considered as very useful for business in context of

purchase and sales such as:

should give appropriate financial statements along with disclosure. The users

get ensured that there is not any lack of information and along with this it is

not misleading any financial statements.

CLIENT 1

1. Presenting Journal entries

All the financial statements are presented with respect to transactions which are given. It

would be adjusting various entries which are considered as very useful for business in context of

purchase and sales such as:

2. Presenting ledger account with context of double entry recording

There is representation of journal entries in above scenario which are settled in below

mentioned ledger account such as:

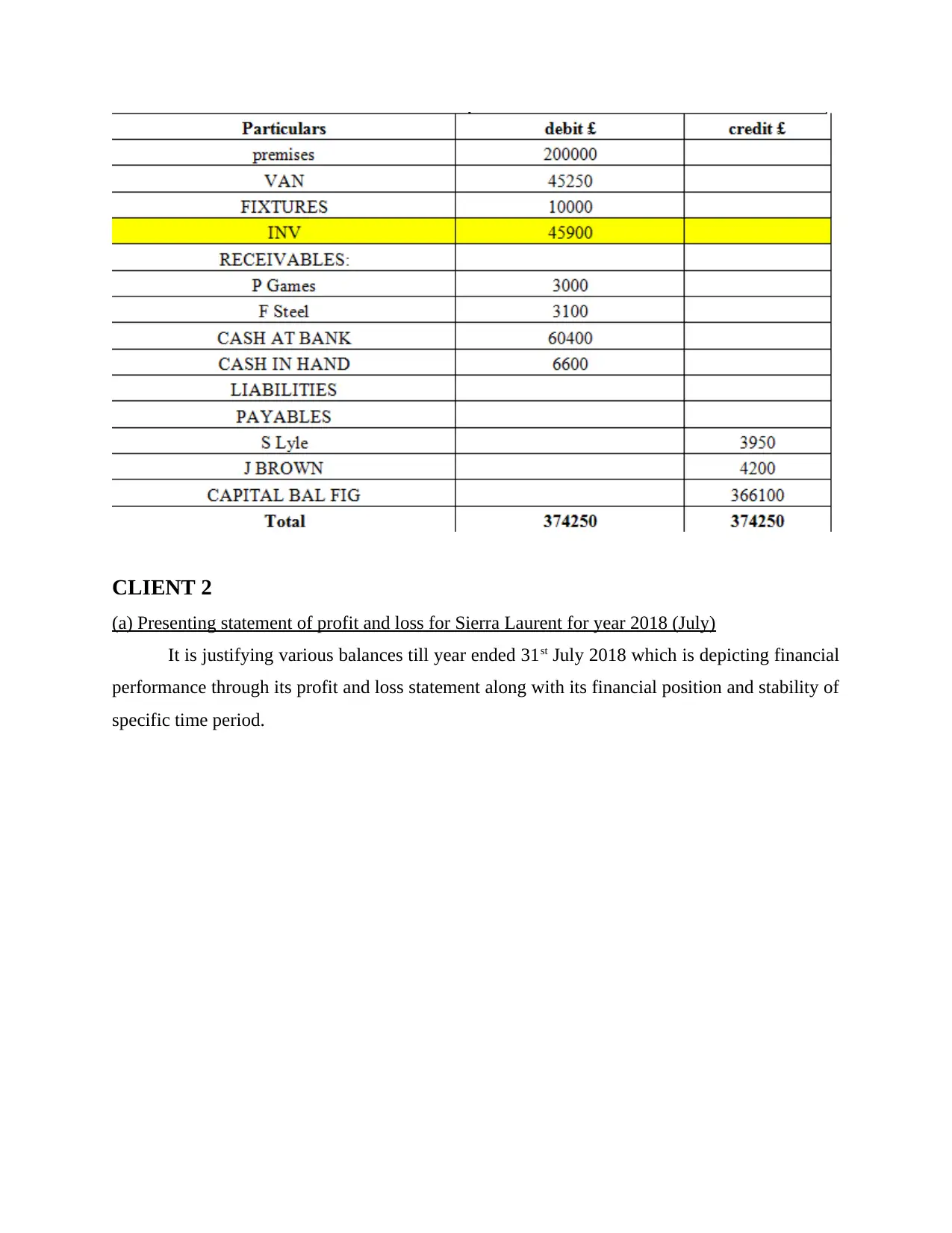

3. Determining the level of accuracy of trial balance

The trial balance consist of each balance of ledger and journal which had been classified

above (Tsalavoutas, André and Evans, 2012). In the same series, there is presence of numerous

data set which is briefing the left transactions and it is considered as very initial contribution to

general accounts. The treail balance of year 2018 is stated below:

There is representation of journal entries in above scenario which are settled in below

mentioned ledger account such as:

3. Determining the level of accuracy of trial balance

The trial balance consist of each balance of ledger and journal which had been classified

above (Tsalavoutas, André and Evans, 2012). In the same series, there is presence of numerous

data set which is briefing the left transactions and it is considered as very initial contribution to

general accounts. The treail balance of year 2018 is stated below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CLIENT 2

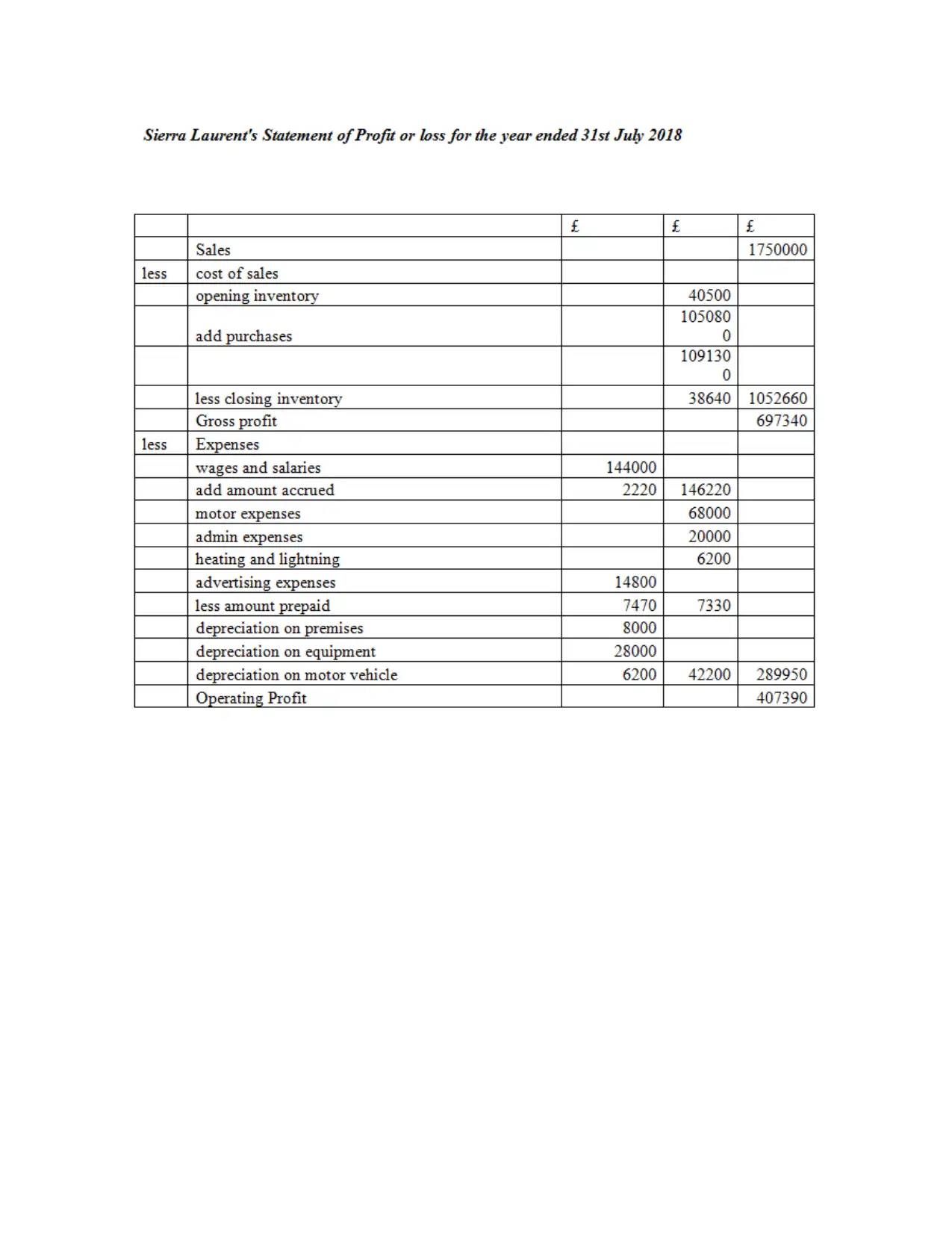

(a) Presenting statement of profit and loss for Sierra Laurent for year 2018 (July)

It is justifying various balances till year ended 31st July 2018 which is depicting financial

performance through its profit and loss statement along with its financial position and stability of

specific time period.

(a) Presenting statement of profit and loss for Sierra Laurent for year 2018 (July)

It is justifying various balances till year ended 31st July 2018 which is depicting financial

performance through its profit and loss statement along with its financial position and stability of

specific time period.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

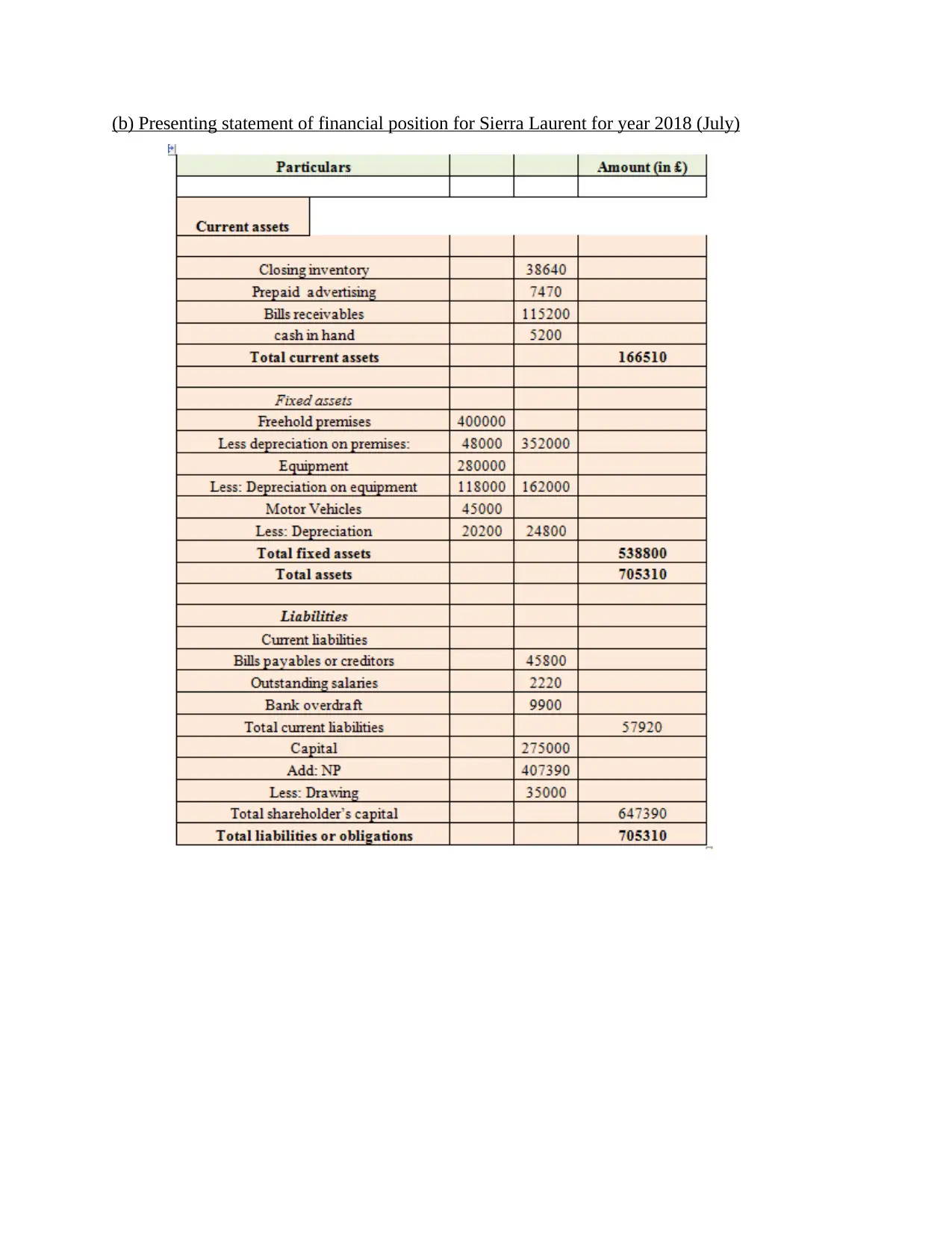

(b) Presenting statement of financial position for Sierra Laurent for year 2018 (July)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.