Accounting Principles: Context, Budgeting, Statements & Interpretation

VerifiedAdded on 2023/06/09

|17

|5188

|484

Report

AI Summary

This report provides a detailed analysis of accounting principles, starting with the role and scope of accounting in complex environments and its importance in decision-making. It covers key areas such as financial reporting, management reporting, and the advantages and disadvantages of accounting practices. The report delves into the primary branches of accounting, including management, taxation, and auditing, highlighting essential skills for accountants. It explains core accounting concepts like separate entity, ongoing concern, and matching principles, alongside discussions on regulation, compliance, and ethics. Furthermore, the report includes practical exercises such as preparing schedules for expected cash collections and disbursements, creating cash budgets, and constructing flexible budgets. The second part focuses on preparing an income statement and balance sheet, computing liquidity, profitability, and investment ratios, and providing an assessment of the organization's financial position with recommendations for improvement. The report concludes with key findings and suggestions based on the business's performance.

Accounting Principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

Look at the reason and extent of bookkeeping in complex working conditions.........................1

Accounting capability in illuminating navigation and meeting partner and cultural necessities.

......................................................................................................................................................3

Primary branches of bookkeeping and occupation ranges of abilities and skills sets.................3

Define initial concepts of Accounting.........................................................................................4

Issue of regulation, compliance and ethics and area to which threats to the business

enterprises....................................................................................................................................5

Prepare a schedule of expected cash collections for the quarter..................................................6

Prepare a schedule of expected cash disbursements for merchandise inventory purchases for

the quarter....................................................................................................................................6

Prepare a cash budget for July, August, September and Q1 (first quarter). Indicate in the

financing section any borrowing that will be needed in any month............................................7

Merits and demerits of budgetary control, budgets and budgeting..............................................7

Construct a Flexible Budget.......................................................................................................10

PART 2..........................................................................................................................................10

Prepare income statement and balance sheet.............................................................................10

Compute the liquidity, profitability and investment ratios........................................................11

Comment on the liquidity position of the organisation considering that whether the company is

capable of taking overdraft or not..............................................................................................12

Give Conclusions and recommendations as per the performance of the business....................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Accounting has been suitably called the language of business. It is called so in light of the

fact that it is a viable strategy for conveying business data to different clients who may be keen

on looking for point by point data about the activities of business and its monetary status. The

consistently changing business climate have enlarged the extent of bookkeeping from the

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

Look at the reason and extent of bookkeeping in complex working conditions.........................1

Accounting capability in illuminating navigation and meeting partner and cultural necessities.

......................................................................................................................................................3

Primary branches of bookkeeping and occupation ranges of abilities and skills sets.................3

Define initial concepts of Accounting.........................................................................................4

Issue of regulation, compliance and ethics and area to which threats to the business

enterprises....................................................................................................................................5

Prepare a schedule of expected cash collections for the quarter..................................................6

Prepare a schedule of expected cash disbursements for merchandise inventory purchases for

the quarter....................................................................................................................................6

Prepare a cash budget for July, August, September and Q1 (first quarter). Indicate in the

financing section any borrowing that will be needed in any month............................................7

Merits and demerits of budgetary control, budgets and budgeting..............................................7

Construct a Flexible Budget.......................................................................................................10

PART 2..........................................................................................................................................10

Prepare income statement and balance sheet.............................................................................10

Compute the liquidity, profitability and investment ratios........................................................11

Comment on the liquidity position of the organisation considering that whether the company is

capable of taking overdraft or not..............................................................................................12

Give Conclusions and recommendations as per the performance of the business....................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Accounting has been suitably called the language of business. It is called so in light of the

fact that it is a viable strategy for conveying business data to different clients who may be keen

on looking for point by point data about the activities of business and its monetary status. The

consistently changing business climate have enlarged the extent of bookkeeping from the

previous simple record - holding component to an energetic subject now in order to address the

issues of different vested parties (Ahmed and et.al., 2018). Bookkeeping carries out the

indispensable roles of keeping efficient records of the exchanges that occur over the span of

maintaining the business. It safeguards the business properties and furthermore helps the

administration in the undertaking of arranging, control and co-appointment of the business

exercises. In this following report, objective of accounting in dynamic working circumstances,

critically appraisal of accounting role, branches of accounting and matters of ethics, policy and

compliance are analysed and define. The below report also contain, preparation of expected cash

collection and disbursement, preparation of flexible budget, preparation of cash budget of first

financial year quarter as well as meaning, advantages and disadvantages of budgets, budgeting

and budgetary control. Moreover, it includes income statement and balance sheet of the year

ending and some financial ratio investment, profitability and liquidity along with decision

making, conclusion and recommendation.

PART 1

Look at the reason and extent of bookkeeping in complex working conditions.

Accounting is the most important tool for any of the organization because it helps them to

trace cash inflows and outflows, assure statutory compliance, recording of transactions,

reporting, analysis, gives shareholders, administration and legislative along with numerical

financial data which can be used in future forecasting and appropriate decision making (Hu,

Wang and Wang., 2021).

Accounting has three types of key financial statements which are as follows:

The first key financial statement is income statement that provides information about

gains or losses.

Balance sheet is the most important financial statement that provides clear view of

organization monetary place at the end of the financial year.

Cash flow of financial statement creates a relationship between balance sheet and income

statement and reports the money produced and spent during a particular timeframe.

It is important to record a day to day accurate transaction for running the business smoothly

without facing any disturbance. Business uses several steps to keep a clear record of accounting,

few are listed below:

issues of different vested parties (Ahmed and et.al., 2018). Bookkeeping carries out the

indispensable roles of keeping efficient records of the exchanges that occur over the span of

maintaining the business. It safeguards the business properties and furthermore helps the

administration in the undertaking of arranging, control and co-appointment of the business

exercises. In this following report, objective of accounting in dynamic working circumstances,

critically appraisal of accounting role, branches of accounting and matters of ethics, policy and

compliance are analysed and define. The below report also contain, preparation of expected cash

collection and disbursement, preparation of flexible budget, preparation of cash budget of first

financial year quarter as well as meaning, advantages and disadvantages of budgets, budgeting

and budgetary control. Moreover, it includes income statement and balance sheet of the year

ending and some financial ratio investment, profitability and liquidity along with decision

making, conclusion and recommendation.

PART 1

Look at the reason and extent of bookkeeping in complex working conditions.

Accounting is the most important tool for any of the organization because it helps them to

trace cash inflows and outflows, assure statutory compliance, recording of transactions,

reporting, analysis, gives shareholders, administration and legislative along with numerical

financial data which can be used in future forecasting and appropriate decision making (Hu,

Wang and Wang., 2021).

Accounting has three types of key financial statements which are as follows:

The first key financial statement is income statement that provides information about

gains or losses.

Balance sheet is the most important financial statement that provides clear view of

organization monetary place at the end of the financial year.

Cash flow of financial statement creates a relationship between balance sheet and income

statement and reports the money produced and spent during a particular timeframe.

It is important to record a day to day accurate transaction for running the business smoothly

without facing any disturbance. Business uses several steps to keep a clear record of accounting,

few are listed below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Recording: It is most initial stage of accounting which is also recognized by the name of

bookkeeping. At this stage, all the data of monetary transaction are writing down in an

organized and arranged manner in the books or accounts. Bookkeeping recorders are the

reports and books engaged with getting ready fiscal summaries(Buallay and et.al., 2020).

Bookkeeping recorders incorporate records of resources, liabilities, records, journal and

other supporting archives like solicitations and checks.

Classifying: In this stage of accounting contain ordering and assembling alike substances

under the account, category and appointed name. This stage involves efficient

examination of kept information in which all exchanges are assembled in one spot. For

instance, "travel costs" may be a classification that bookkeepers use to group costs

connecting with organization travel. The expression "record" alludes to the book wherein

orders are recorded

Reporting: The summing up period of bookkeeping includes summing up the

information after each bookkeeping period, like a month, quarter or year(Ernstberger and

et.al., 2020). The information should be introduced in a way which is straightforward and

use by both outer and inside clients of the bookkeeping proclamations. Diagrams and

other visual components are many times used to supplement the text information.

Analyzing: The analysing period of the bookkeeping system is anxious with observing

monetary information, and is a basic device for future forecasting or decision making.

This last stage interprets the kept information in a way which permits end-clients to make

significant decisions with respect to the monetary states of a business or individual

record, as well as the benefit of business tasks. This information is then used to get ready

likely arrangements and casing strategies to execute monetary plans.

Accounting capability in illuminating navigation and meeting partner and cultural necessities.

Accounting is useful for the business to analyze the financial position, company goodwill and

working of operation during a given period. It is done through financial statement such as

balance sheet and profit & loss account, a business firm can provide lender or shareholders a

specific types of power in business decision making. There are many types of accounting

function that helps the business in meeting shareholder or investors and societal expectations and

needs as well as informing decision making. Two types of accounting function are described

below:

bookkeeping. At this stage, all the data of monetary transaction are writing down in an

organized and arranged manner in the books or accounts. Bookkeeping recorders are the

reports and books engaged with getting ready fiscal summaries(Buallay and et.al., 2020).

Bookkeeping recorders incorporate records of resources, liabilities, records, journal and

other supporting archives like solicitations and checks.

Classifying: In this stage of accounting contain ordering and assembling alike substances

under the account, category and appointed name. This stage involves efficient

examination of kept information in which all exchanges are assembled in one spot. For

instance, "travel costs" may be a classification that bookkeepers use to group costs

connecting with organization travel. The expression "record" alludes to the book wherein

orders are recorded

Reporting: The summing up period of bookkeeping includes summing up the

information after each bookkeeping period, like a month, quarter or year(Ernstberger and

et.al., 2020). The information should be introduced in a way which is straightforward and

use by both outer and inside clients of the bookkeeping proclamations. Diagrams and

other visual components are many times used to supplement the text information.

Analyzing: The analysing period of the bookkeeping system is anxious with observing

monetary information, and is a basic device for future forecasting or decision making.

This last stage interprets the kept information in a way which permits end-clients to make

significant decisions with respect to the monetary states of a business or individual

record, as well as the benefit of business tasks. This information is then used to get ready

likely arrangements and casing strategies to execute monetary plans.

Accounting capability in illuminating navigation and meeting partner and cultural necessities.

Accounting is useful for the business to analyze the financial position, company goodwill and

working of operation during a given period. It is done through financial statement such as

balance sheet and profit & loss account, a business firm can provide lender or shareholders a

specific types of power in business decision making. There are many types of accounting

function that helps the business in meeting shareholder or investors and societal expectations and

needs as well as informing decision making. Two types of accounting function are described

below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Reporting: Standard systems for furnishing partners with an exact image of an

organization's funds, including their incomes, costs, benefits, capital, and income, as well

as true keeps that proposal inside and out bits of knowledge into monetary data are

alluded to as monetary revealing (Musallam., 2018).

Management Reporting: The objective of the executive’s reports is to illuminate

administrators regarding different business factors so they might pursue more educated

choices. They accumulate data from the organization's various offices that track key

execution pointers and obviously show it.

Advantages of Accounting Disadvantages of Accounting

Accounting portrays a business' or an

assortment of undertakings' monetary

circumstance.

Accounting does not show accurate financial

statement all the time.

An account provides the management with

the crucial information they need to make

decisions in the form of a balance sheet and a

profit-and-loss account.

It only considers the qualitative element does

not consider any type of relation, pubic

relation and emotions.

It exchanges should be appropriately kept to

supplant the need to review exchanges.

It is very costly for the small organization

because it contains chartered account and

audit practice for the firm.

Primary branches of bookkeeping and occupation ranges of abilities and skills sets

Following are some primary branches of accounting:

Management Accounting: Maximizing benefit and limiting misfortunes is the

fundamental objective of administrative bookkeeping (Argento and et.al., 2019). It

assembles, evaluates, inspects, interprets, and transfers monetary information to the

executives. This information helps direction by organization proprietors and the

executives.

Taxation Accounting: Tax Accounting focuses on taxes instead of public fiscal

statement (Keasey and Watson., 2019). It focuses around exchanges that influence a

business' taxation rate, and how those things connect with legitimate duty estimation and

organization's funds, including their incomes, costs, benefits, capital, and income, as well

as true keeps that proposal inside and out bits of knowledge into monetary data are

alluded to as monetary revealing (Musallam., 2018).

Management Reporting: The objective of the executive’s reports is to illuminate

administrators regarding different business factors so they might pursue more educated

choices. They accumulate data from the organization's various offices that track key

execution pointers and obviously show it.

Advantages of Accounting Disadvantages of Accounting

Accounting portrays a business' or an

assortment of undertakings' monetary

circumstance.

Accounting does not show accurate financial

statement all the time.

An account provides the management with

the crucial information they need to make

decisions in the form of a balance sheet and a

profit-and-loss account.

It only considers the qualitative element does

not consider any type of relation, pubic

relation and emotions.

It exchanges should be appropriately kept to

supplant the need to review exchanges.

It is very costly for the small organization

because it contains chartered account and

audit practice for the firm.

Primary branches of bookkeeping and occupation ranges of abilities and skills sets

Following are some primary branches of accounting:

Management Accounting: Maximizing benefit and limiting misfortunes is the

fundamental objective of administrative bookkeeping (Argento and et.al., 2019). It

assembles, evaluates, inspects, interprets, and transfers monetary information to the

executives. This information helps direction by organization proprietors and the

executives.

Taxation Accounting: Tax Accounting focuses on taxes instead of public fiscal

statement (Keasey and Watson., 2019). It focuses around exchanges that influence a

business' taxation rate, and how those things connect with legitimate duty estimation and

readiness of expense reports. It is administered by the Internal Revenue Code, which

should be completely followed when people and organizations set up their assessment

forms

Auditing Accounting: It is the objective inner or outer survey and evaluation of an

organization's fiscal summaries by an administration organization, for example, the

Internal Revenue Service. Audit generally are three types; IRS, internal or external.

Competencies for accountants: Accountant capacities show to managers that a

bookkeeper has the information and capacities to keep exact monetary records and break

down that information accurately to offer sound counsel. Bookkeepers with explicit

center abilities can help entrepreneurs in settling on urgent monetary choices. Fruitful

bookkeepers can likewise foresee patterns in view of verifiable information for a firm to

assist with coordinating the future course of their business' funds.

Define initial concepts of Accounting

There are several types of accounting concepts and some of the accounting concepts are as

follows:

Separate Entity: The Accounting rule that all substances associated with a firm ought to be

represented independently is known as a different business element (Rustam, Wang and Zameer.,

2019). The financial substance supposition that is a hypothesis that fights that all organizations,

organizations that are attached to them and entrepreneurs ought to be treated as independent

elements for the purpose of bookkeeping.

Ongoing Concern: According to this concern, a corporate association will keep on working for

an unending measure of time. It essentially implies that each corporate element has a proceeding

with presence. Therefore, it won't break up at any point in the near future. This is a vital

bookkeeping assumption since it gives the reason for showing the worth of resources on the

monetary record.

Matching Concept: The matching concept is a bookkeeping practice by which firms perceive

incomes and their connected costs in a similar bookkeeping period. Firms report "incomes," that

is, alongside the "costs" that brought them. The motivation behind the matching idea is to try not

to misquote profit for a period.

should be completely followed when people and organizations set up their assessment

forms

Auditing Accounting: It is the objective inner or outer survey and evaluation of an

organization's fiscal summaries by an administration organization, for example, the

Internal Revenue Service. Audit generally are three types; IRS, internal or external.

Competencies for accountants: Accountant capacities show to managers that a

bookkeeper has the information and capacities to keep exact monetary records and break

down that information accurately to offer sound counsel. Bookkeepers with explicit

center abilities can help entrepreneurs in settling on urgent monetary choices. Fruitful

bookkeepers can likewise foresee patterns in view of verifiable information for a firm to

assist with coordinating the future course of their business' funds.

Define initial concepts of Accounting

There are several types of accounting concepts and some of the accounting concepts are as

follows:

Separate Entity: The Accounting rule that all substances associated with a firm ought to be

represented independently is known as a different business element (Rustam, Wang and Zameer.,

2019). The financial substance supposition that is a hypothesis that fights that all organizations,

organizations that are attached to them and entrepreneurs ought to be treated as independent

elements for the purpose of bookkeeping.

Ongoing Concern: According to this concern, a corporate association will keep on working for

an unending measure of time. It essentially implies that each corporate element has a proceeding

with presence. Therefore, it won't break up at any point in the near future. This is a vital

bookkeeping assumption since it gives the reason for showing the worth of resources on the

monetary record.

Matching Concept: The matching concept is a bookkeeping practice by which firms perceive

incomes and their connected costs in a similar bookkeeping period. Firms report "incomes," that

is, alongside the "costs" that brought them. The motivation behind the matching idea is to try not

to misquote profit for a period.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Issue of regulation, compliance and ethics and area to which threats to the business enterprises.

Business morals cover a wide scope of subjects that fall inside an association's moral

rules. Advancing conduct in light of genuineness and trust are crucial moral difficulties in

business, yet more confounded issues incorporate embracing variety, pursuing choices with

compassion, and sticking to consistence and administration that is in accordance with the

association's fundamental standards (Chakrabarti and Chakrabarti., 2019). The recognition of

regulations, rules, orders, and details appropriate to an association's business processes is alluded

to as administrative consistence. Administrative consistence infringement much of the times

bring about legitimate authorizations, including government punishments. Consistence with

guidelines alludes to an organization's adherence to rules, strategies, rules, and prerequisites that

are relevant to its business tasks. Legitimate punishments, like government fines, are regularly

forced for administrative consistence infringement.

ROLE OF IRFS: Organizations should keep up with and unveil their records as per IFRS rules.

The target of the worldwide monetary revealing guidelines, which were created to lay out a

typical bookkeeping language, is to offer monetary expressions sound and steady across different

ventures and countries. An unambiguous and unfit assertion of consistence with IFRS should be

remembered for IFRS budget reports. Fiscal reports should allude to IFRS as embraced by the

EU, per the Companies Act (Deswanto and Siregar., 2018). As indicated by moral norms,

bookkeepers should maintain the guidelines and regulations that control their areas of training

and ward. Business partners and others ought to sensibly anticipate that you should avoid taking

any exercises that would harm your calling's standing.

ROLE OF IAS: The standards of lead expected of people working in the public area are

illustrated in a lawfully restricting set of principles. The Civil Service code depicts the key rules

that guide the Civil Service as well as the lead that all government workers are supposed to show

in regarding these standards. Orchestrating the monetary data given by guarantors of protections

in the European Union is the objective of the International Accounting Standards (IAS)

Regulation (EU). Universally tantamount bookkeeping principles empower receptiveness,

obligation, and adequacy in every monetary market. This advances capital portion and empowers

financial backers and other market members to settle on all around informed monetary

conclusions about venture valuable open doors and risks (Nujoom, Wang and Mohammed.,

2018).

Business morals cover a wide scope of subjects that fall inside an association's moral

rules. Advancing conduct in light of genuineness and trust are crucial moral difficulties in

business, yet more confounded issues incorporate embracing variety, pursuing choices with

compassion, and sticking to consistence and administration that is in accordance with the

association's fundamental standards (Chakrabarti and Chakrabarti., 2019). The recognition of

regulations, rules, orders, and details appropriate to an association's business processes is alluded

to as administrative consistence. Administrative consistence infringement much of the times

bring about legitimate authorizations, including government punishments. Consistence with

guidelines alludes to an organization's adherence to rules, strategies, rules, and prerequisites that

are relevant to its business tasks. Legitimate punishments, like government fines, are regularly

forced for administrative consistence infringement.

ROLE OF IRFS: Organizations should keep up with and unveil their records as per IFRS rules.

The target of the worldwide monetary revealing guidelines, which were created to lay out a

typical bookkeeping language, is to offer monetary expressions sound and steady across different

ventures and countries. An unambiguous and unfit assertion of consistence with IFRS should be

remembered for IFRS budget reports. Fiscal reports should allude to IFRS as embraced by the

EU, per the Companies Act (Deswanto and Siregar., 2018). As indicated by moral norms,

bookkeepers should maintain the guidelines and regulations that control their areas of training

and ward. Business partners and others ought to sensibly anticipate that you should avoid taking

any exercises that would harm your calling's standing.

ROLE OF IAS: The standards of lead expected of people working in the public area are

illustrated in a lawfully restricting set of principles. The Civil Service code depicts the key rules

that guide the Civil Service as well as the lead that all government workers are supposed to show

in regarding these standards. Orchestrating the monetary data given by guarantors of protections

in the European Union is the objective of the International Accounting Standards (IAS)

Regulation (EU). Universally tantamount bookkeeping principles empower receptiveness,

obligation, and adequacy in every monetary market. This advances capital portion and empowers

financial backers and other market members to settle on all around informed monetary

conclusions about venture valuable open doors and risks (Nujoom, Wang and Mohammed.,

2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

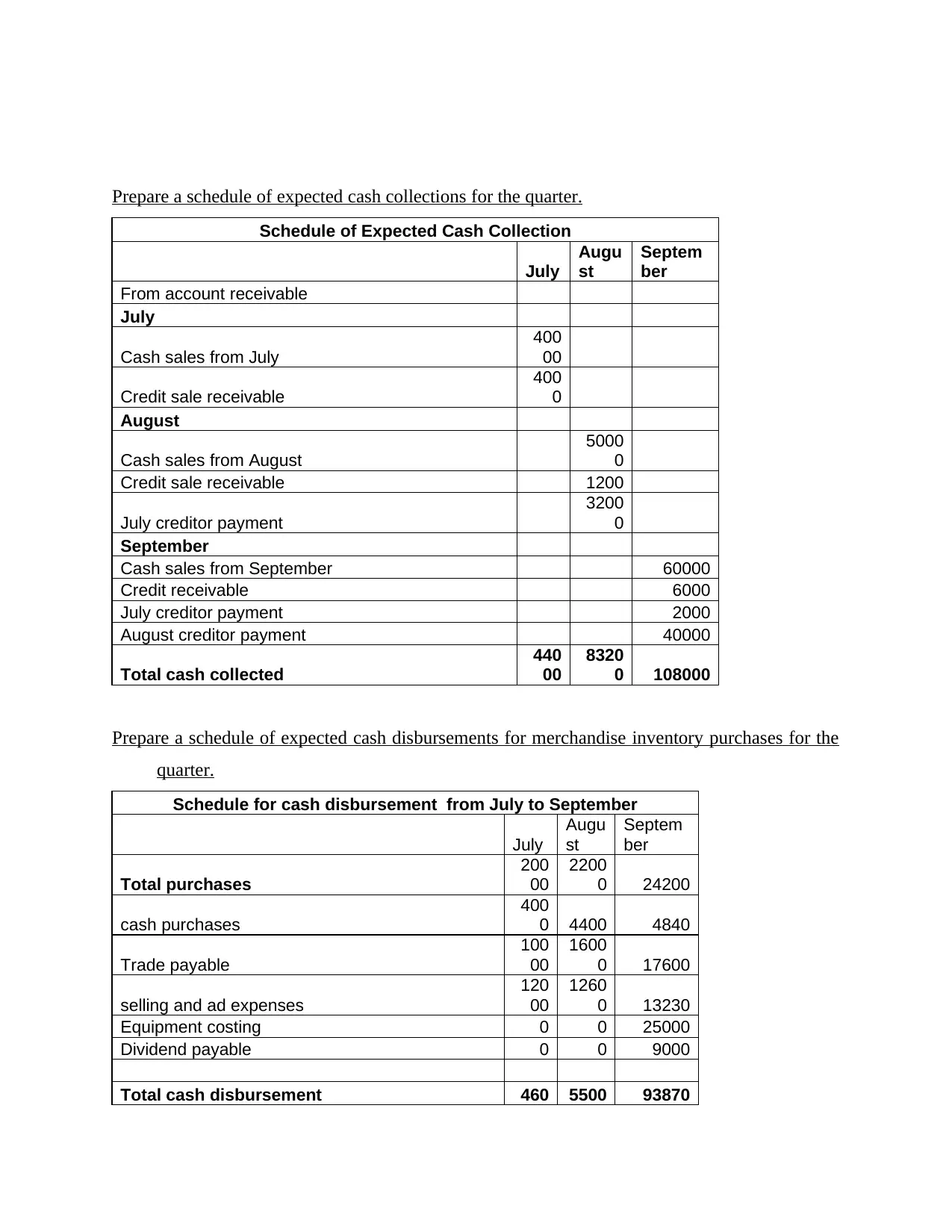

Prepare a schedule of expected cash collections for the quarter.

Schedule of Expected Cash Collection

July

Augu

st

Septem

ber

From account receivable

July

Cash sales from July

400

00

Credit sale receivable

400

0

August

Cash sales from August

5000

0

Credit sale receivable 1200

July creditor payment

3200

0

September

Cash sales from September 60000

Credit receivable 6000

July creditor payment 2000

August creditor payment 40000

Total cash collected

440

00

8320

0 108000

Prepare a schedule of expected cash disbursements for merchandise inventory purchases for the

quarter.

Schedule for cash disbursement from July to September

July

Augu

st

Septem

ber

Total purchases

200

00

2200

0 24200

cash purchases

400

0 4400 4840

Trade payable

100

00

1600

0 17600

selling and ad expenses

120

00

1260

0 13230

Equipment costing 0 0 25000

Dividend payable 0 0 9000

Total cash disbursement 460 5500 93870

Schedule of Expected Cash Collection

July

Augu

st

Septem

ber

From account receivable

July

Cash sales from July

400

00

Credit sale receivable

400

0

August

Cash sales from August

5000

0

Credit sale receivable 1200

July creditor payment

3200

0

September

Cash sales from September 60000

Credit receivable 6000

July creditor payment 2000

August creditor payment 40000

Total cash collected

440

00

8320

0 108000

Prepare a schedule of expected cash disbursements for merchandise inventory purchases for the

quarter.

Schedule for cash disbursement from July to September

July

Augu

st

Septem

ber

Total purchases

200

00

2200

0 24200

cash purchases

400

0 4400 4840

Trade payable

100

00

1600

0 17600

selling and ad expenses

120

00

1260

0 13230

Equipment costing 0 0 25000

Dividend payable 0 0 9000

Total cash disbursement 460 5500 93870

00 0

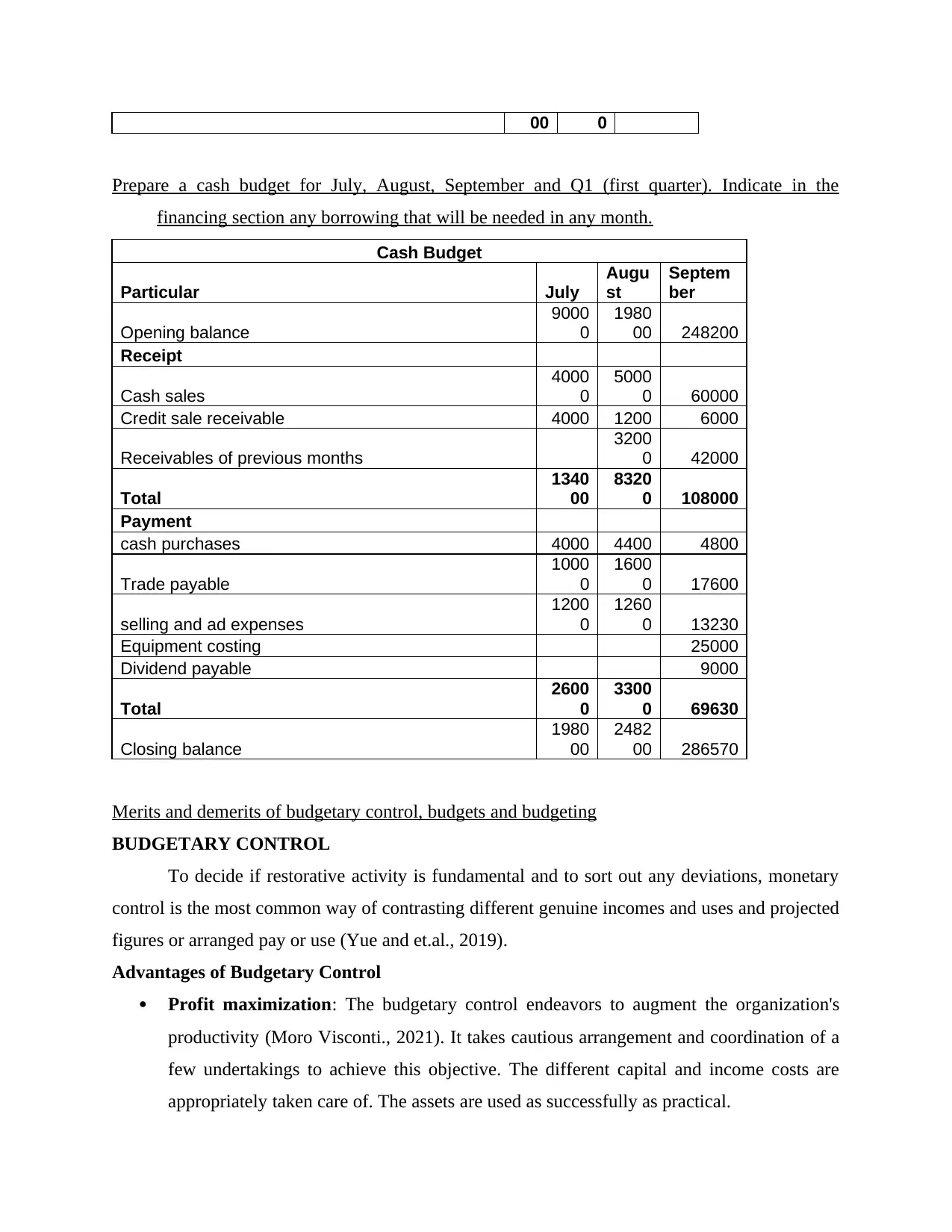

Prepare a cash budget for July, August, September and Q1 (first quarter). Indicate in the

financing section any borrowing that will be needed in any month.

Cash Budget

Particular July

Augu

st

Septem

ber

Opening balance

9000

0

1980

00 248200

Receipt

Cash sales

4000

0

5000

0 60000

Credit sale receivable 4000 1200 6000

Receivables of previous months

3200

0 42000

Total

1340

00

8320

0 108000

Payment

cash purchases 4000 4400 4800

Trade payable

1000

0

1600

0 17600

selling and ad expenses

1200

0

1260

0 13230

Equipment costing 25000

Dividend payable 9000

Total

2600

0

3300

0 69630

Closing balance

1980

00

2482

00 286570

Merits and demerits of budgetary control, budgets and budgeting

BUDGETARY CONTROL

To decide if restorative activity is fundamental and to sort out any deviations, monetary

control is the most common way of contrasting different genuine incomes and uses and projected

figures or arranged pay or use (Yue and et.al., 2019).

Advantages of Budgetary Control

Profit maximization: The budgetary control endeavors to augment the organization's

productivity (Moro Visconti., 2021). It takes cautious arrangement and coordination of a

few undertakings to achieve this objective. The different capital and income costs are

appropriately taken care of. The assets are used as successfully as practical.

Prepare a cash budget for July, August, September and Q1 (first quarter). Indicate in the

financing section any borrowing that will be needed in any month.

Cash Budget

Particular July

Augu

st

Septem

ber

Opening balance

9000

0

1980

00 248200

Receipt

Cash sales

4000

0

5000

0 60000

Credit sale receivable 4000 1200 6000

Receivables of previous months

3200

0 42000

Total

1340

00

8320

0 108000

Payment

cash purchases 4000 4400 4800

Trade payable

1000

0

1600

0 17600

selling and ad expenses

1200

0

1260

0 13230

Equipment costing 25000

Dividend payable 9000

Total

2600

0

3300

0 69630

Closing balance

1980

00

2482

00 286570

Merits and demerits of budgetary control, budgets and budgeting

BUDGETARY CONTROL

To decide if restorative activity is fundamental and to sort out any deviations, monetary

control is the most common way of contrasting different genuine incomes and uses and projected

figures or arranged pay or use (Yue and et.al., 2019).

Advantages of Budgetary Control

Profit maximization: The budgetary control endeavors to augment the organization's

productivity (Moro Visconti., 2021). It takes cautious arrangement and coordination of a

few undertakings to achieve this objective. The different capital and income costs are

appropriately taken care of. The assets are used as successfully as practical.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Togetherness: Various offices and areas work in a very much planned way. The financial

plans of numerous divisions impact each other. Accomplishing planned objectives

requires the coordination of various chiefs and subordinates.

Precise aim: Top administration settles on choices in regards to the plans, strategies, and

goals. To accomplish the association's common goal, all endeavours are consolidated.

Each division has an objective that should be met (Tsang, Yang and Zheng., 2022). The

endeavours are centred on getting a couple of specific goals. The endeavours will be

wasted seeking after a few objectives on the off chance that there is no reasonable

objective.

Performance Measuring Tool: The monetary control offers a technique for assessing

administrative execution by laying out objectives for different divisions. Genuine results

are appeared differently in relation to the planned focuses to distinguish differences. The

upper administration is educated regarding every division's presentation. The execution

of the executives by special case is made conceivable by this methodology.

Advantages of Budgetary Control

Future Uncertainty: The financial plans are made for the impending time span. Indeed,

even the most dependable projections for the future may not generally happen. Future

occasions are never ensured, thus the situation that is expected to exist might modify. The

financial plans that should be made in view of explicit presumptions are upset by the

adjustment of future conditions. A monetary control framework is less valuable because

of the obscure future.

Budget Revision Is Necessary: Financial plans are made under the assumption that

specific conditions will turn out as expected. Expected conditions probably won't emerge

because of future vulnerability, provoking a difference in monetary objectives. Spending

plans will lose esteem on the off chance that objectives are every now and again

overhauled, and changes additionally bring about tremendous expenses.

Dissuade Effective People: Each representative in the association is given the objectives

under the monetary control framework. Individuals often have the impulse to zero in just

on accomplishing their objectives (Sun and An., 2018). However, a few useful people

might surpass the objectives, they will in any case feel fulfilled on the off chance that the

objectives are met. Thusly, the board drives might be obliged by spending plans.

plans of numerous divisions impact each other. Accomplishing planned objectives

requires the coordination of various chiefs and subordinates.

Precise aim: Top administration settles on choices in regards to the plans, strategies, and

goals. To accomplish the association's common goal, all endeavours are consolidated.

Each division has an objective that should be met (Tsang, Yang and Zheng., 2022). The

endeavours are centred on getting a couple of specific goals. The endeavours will be

wasted seeking after a few objectives on the off chance that there is no reasonable

objective.

Performance Measuring Tool: The monetary control offers a technique for assessing

administrative execution by laying out objectives for different divisions. Genuine results

are appeared differently in relation to the planned focuses to distinguish differences. The

upper administration is educated regarding every division's presentation. The execution

of the executives by special case is made conceivable by this methodology.

Advantages of Budgetary Control

Future Uncertainty: The financial plans are made for the impending time span. Indeed,

even the most dependable projections for the future may not generally happen. Future

occasions are never ensured, thus the situation that is expected to exist might modify. The

financial plans that should be made in view of explicit presumptions are upset by the

adjustment of future conditions. A monetary control framework is less valuable because

of the obscure future.

Budget Revision Is Necessary: Financial plans are made under the assumption that

specific conditions will turn out as expected. Expected conditions probably won't emerge

because of future vulnerability, provoking a difference in monetary objectives. Spending

plans will lose esteem on the off chance that objectives are every now and again

overhauled, and changes additionally bring about tremendous expenses.

Dissuade Effective People: Each representative in the association is given the objectives

under the monetary control framework. Individuals often have the impulse to zero in just

on accomplishing their objectives (Sun and An., 2018). However, a few useful people

might surpass the objectives, they will in any case feel fulfilled on the off chance that the

objectives are met. Thusly, the board drives might be obliged by spending plans.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Coordinating Issue: The collaboration between numerous divisions is fundamental for

the accomplishment of monetary control. Results from different offices are influenced by

one division's presentation. The issue of coordination should be tackled, and a monetary

official is required. Few out of every odd association can stand to enlist a monetary

official. Horrible showing is the result of incapable departmental collaboration.

BUDGETS

A spending plan is an arrangement or assessment of one's monetary expenses throughout

a foreordained time span. This system can integrate incomes, receipts, commitments, scale

volume expected, and different costs. It depends on profit and different costs.

Advantages of Budget

Control and the executives: A financial plan offers a strategic game plan. It imparts a

feeling of reasonability with respect to the costs that either an establishment or an

individual can manage (Abu-Rayash and Dincer., 2021). Thusly, assessing choices and

base decisions on their viability is useful.

Strategy assessment: A financial plan empowers a survey of the targets and decides that

have been laid out to act as an aide for future spending choices.

Capital expansion: With a sound spending plan, a business or individual can use its

capital and assets to the furthest reaches conceivable, bringing about expanded efficiency

and benefit.

Disadvantages of Budget

Inaccurate and unrealistic: A financial plan is based on suppositions and decisions,

which makes it incorrect and ridiculous. The whole gauge across the spending

arrangement will be influenced by any progressions to the field-tested strategy or

execution. Subsequently, the results of a monetary arrangement are rarely sure and at

times questionable.

Unbending: A spending plan is made in view of explicit institutional strategies or

individual objectives that impact navigation (Yeh., 2018). The spending plan,

notwithstanding, can't be changed in the event that there is a need to survey what is

happening considering market vacillations.

the accomplishment of monetary control. Results from different offices are influenced by

one division's presentation. The issue of coordination should be tackled, and a monetary

official is required. Few out of every odd association can stand to enlist a monetary

official. Horrible showing is the result of incapable departmental collaboration.

BUDGETS

A spending plan is an arrangement or assessment of one's monetary expenses throughout

a foreordained time span. This system can integrate incomes, receipts, commitments, scale

volume expected, and different costs. It depends on profit and different costs.

Advantages of Budget

Control and the executives: A financial plan offers a strategic game plan. It imparts a

feeling of reasonability with respect to the costs that either an establishment or an

individual can manage (Abu-Rayash and Dincer., 2021). Thusly, assessing choices and

base decisions on their viability is useful.

Strategy assessment: A financial plan empowers a survey of the targets and decides that

have been laid out to act as an aide for future spending choices.

Capital expansion: With a sound spending plan, a business or individual can use its

capital and assets to the furthest reaches conceivable, bringing about expanded efficiency

and benefit.

Disadvantages of Budget

Inaccurate and unrealistic: A financial plan is based on suppositions and decisions,

which makes it incorrect and ridiculous. The whole gauge across the spending

arrangement will be influenced by any progressions to the field-tested strategy or

execution. Subsequently, the results of a monetary arrangement are rarely sure and at

times questionable.

Unbending: A spending plan is made in view of explicit institutional strategies or

individual objectives that impact navigation (Yeh., 2018). The spending plan,

notwithstanding, can't be changed in the event that there is a need to survey what is

happening considering market vacillations.

Finance-centred: The financial plan doesn't consider the requirements and interests of

the general population. While the prerequisites of individuals are more subjective in

nature, it is more benefit situated, which is more quantitative.

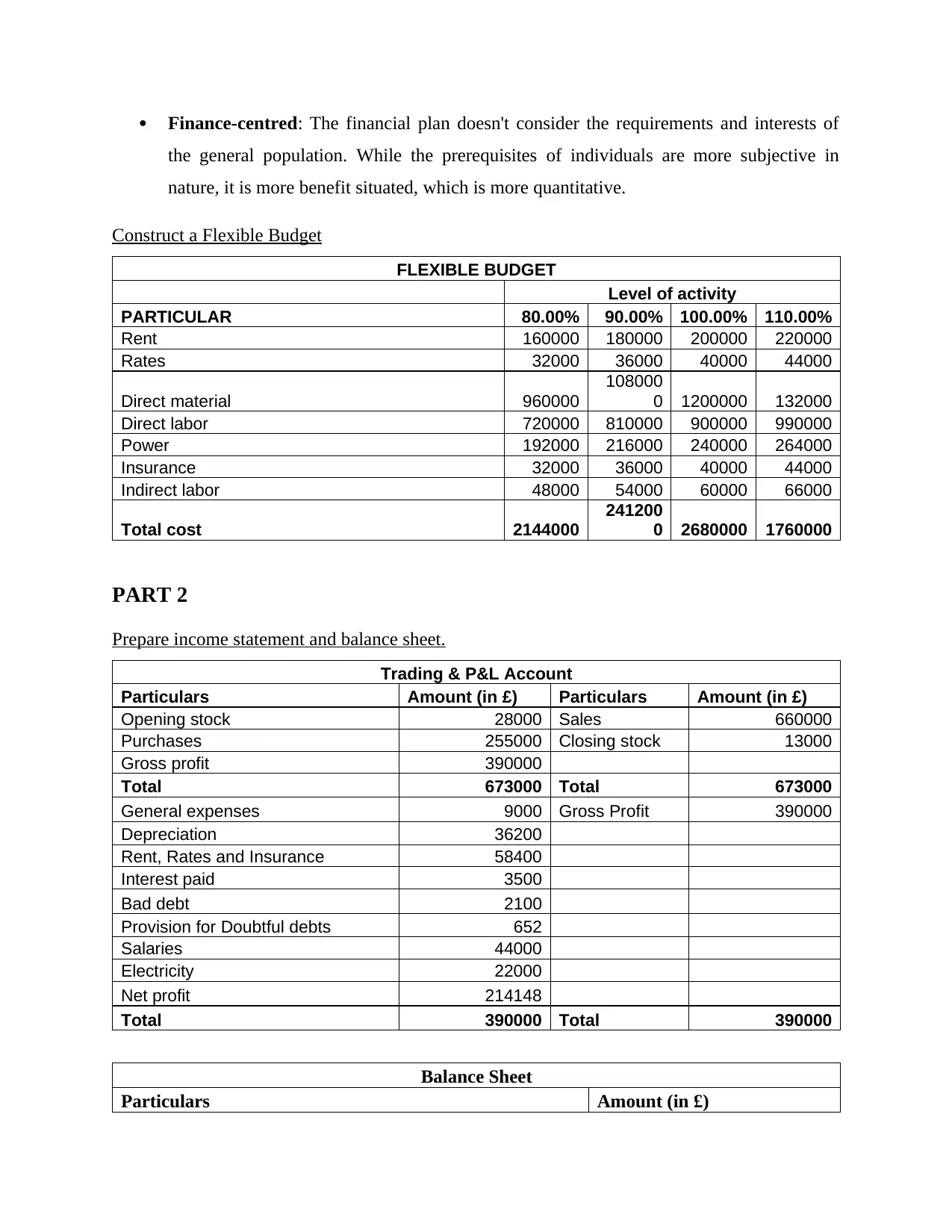

Construct a Flexible Budget

FLEXIBLE BUDGET

Level of activity

PARTICULAR 80.00% 90.00% 100.00% 110.00%

Rent 160000 180000 200000 220000

Rates 32000 36000 40000 44000

Direct material 960000

108000

0 1200000 132000

Direct labor 720000 810000 900000 990000

Power 192000 216000 240000 264000

Insurance 32000 36000 40000 44000

Indirect labor 48000 54000 60000 66000

Total cost 2144000

241200

0 2680000 1760000

PART 2

Prepare income statement and balance sheet.

Trading & P&L Account

Particulars Amount (in £) Particulars Amount (in £)

Opening stock 28000 Sales 660000

Purchases 255000 Closing stock 13000

Gross profit 390000

Total 673000 Total 673000

General expenses 9000 Gross Profit 390000

Depreciation 36200

Rent, Rates and Insurance 58400

Interest paid 3500

Bad debt 2100

Provision for Doubtful debts 652

Salaries 44000

Electricity 22000

Net profit 214148

Total 390000 Total 390000

Balance Sheet

Particulars Amount (in £)

the general population. While the prerequisites of individuals are more subjective in

nature, it is more benefit situated, which is more quantitative.

Construct a Flexible Budget

FLEXIBLE BUDGET

Level of activity

PARTICULAR 80.00% 90.00% 100.00% 110.00%

Rent 160000 180000 200000 220000

Rates 32000 36000 40000 44000

Direct material 960000

108000

0 1200000 132000

Direct labor 720000 810000 900000 990000

Power 192000 216000 240000 264000

Insurance 32000 36000 40000 44000

Indirect labor 48000 54000 60000 66000

Total cost 2144000

241200

0 2680000 1760000

PART 2

Prepare income statement and balance sheet.

Trading & P&L Account

Particulars Amount (in £) Particulars Amount (in £)

Opening stock 28000 Sales 660000

Purchases 255000 Closing stock 13000

Gross profit 390000

Total 673000 Total 673000

General expenses 9000 Gross Profit 390000

Depreciation 36200

Rent, Rates and Insurance 58400

Interest paid 3500

Bad debt 2100

Provision for Doubtful debts 652

Salaries 44000

Electricity 22000

Net profit 214148

Total 390000 Total 390000

Balance Sheet

Particulars Amount (in £)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.