Comprehensive Financial Accounting Report: Brooks City Case Study

VerifiedAdded on 2021/02/20

|30

|6425

|19

Report

AI Summary

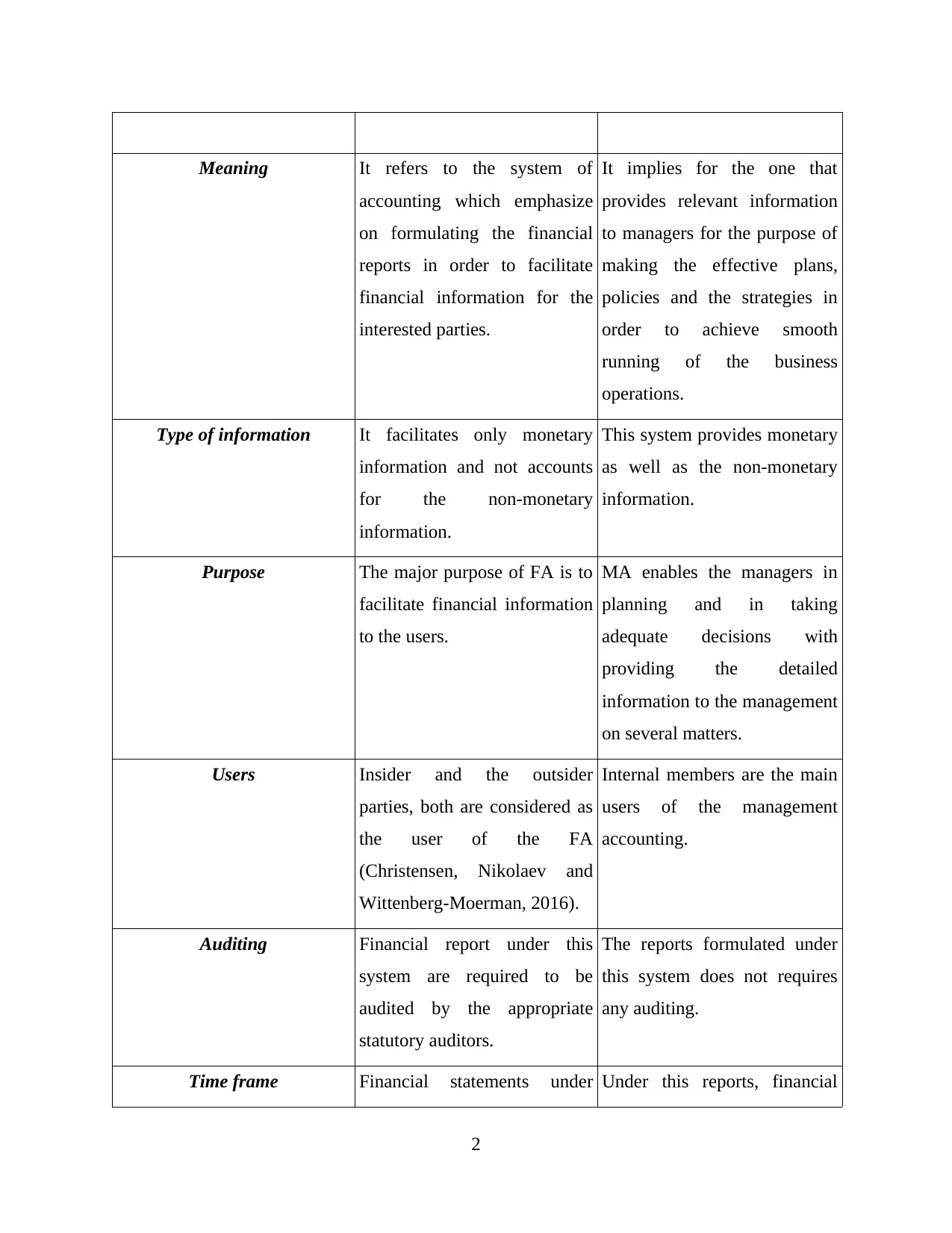

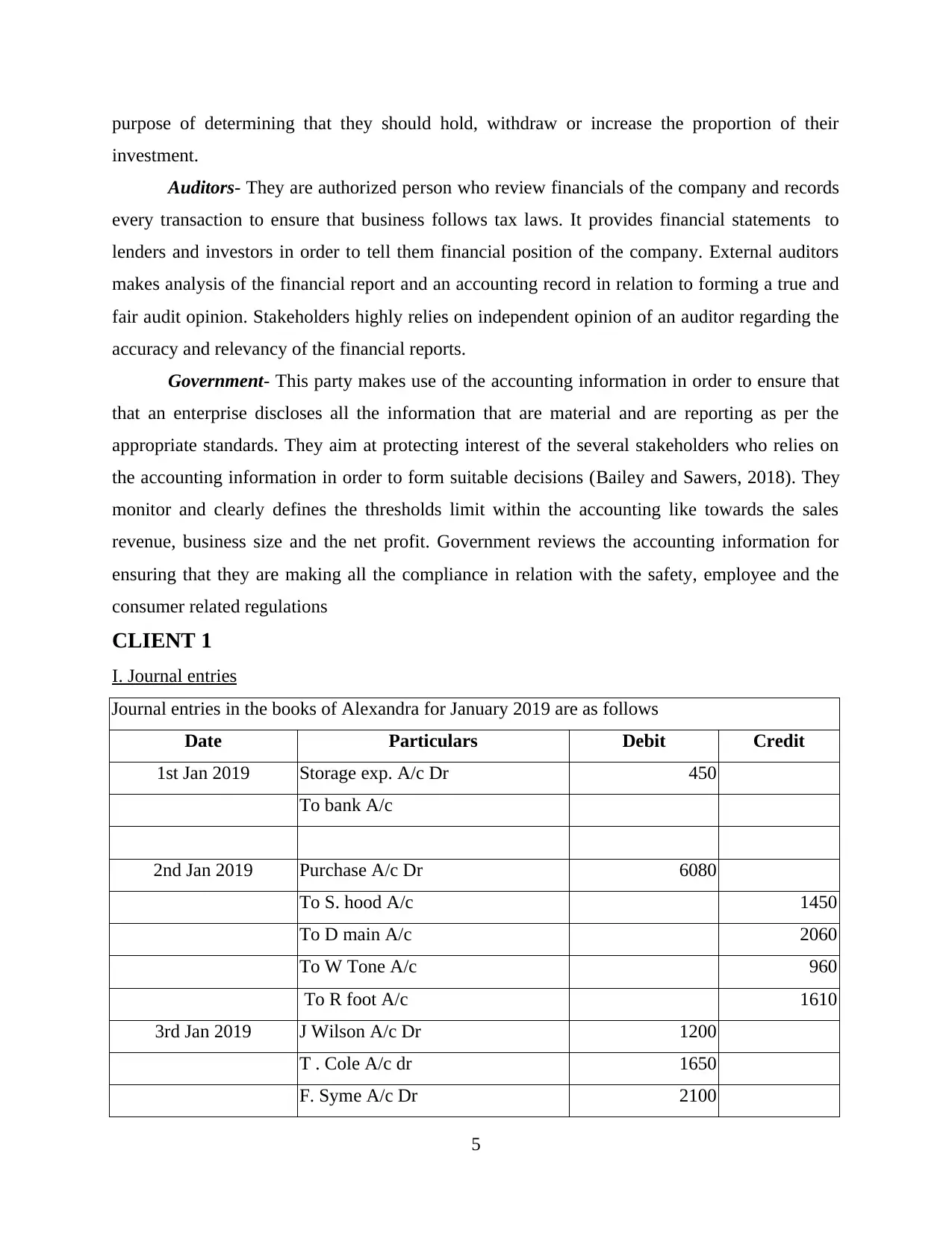

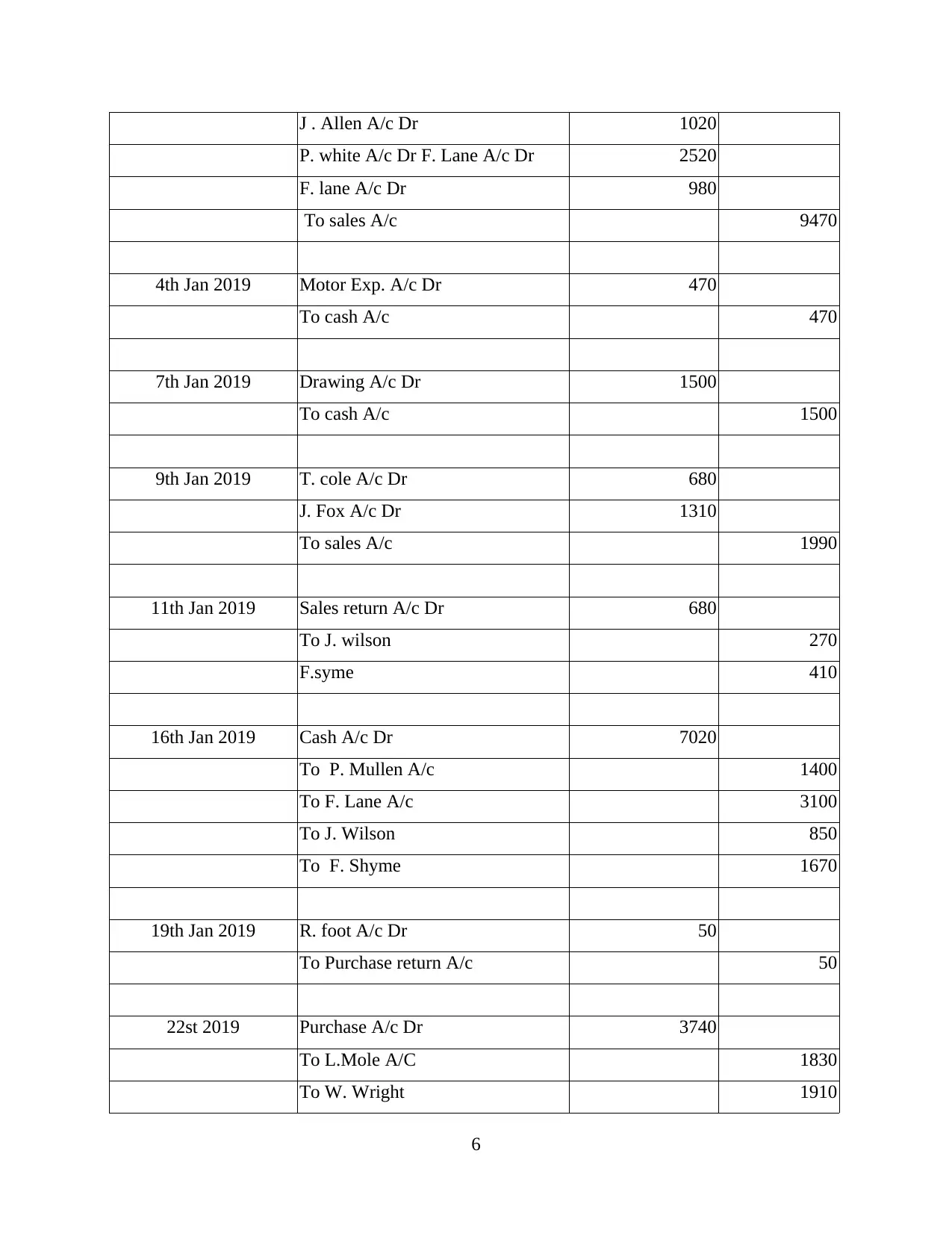

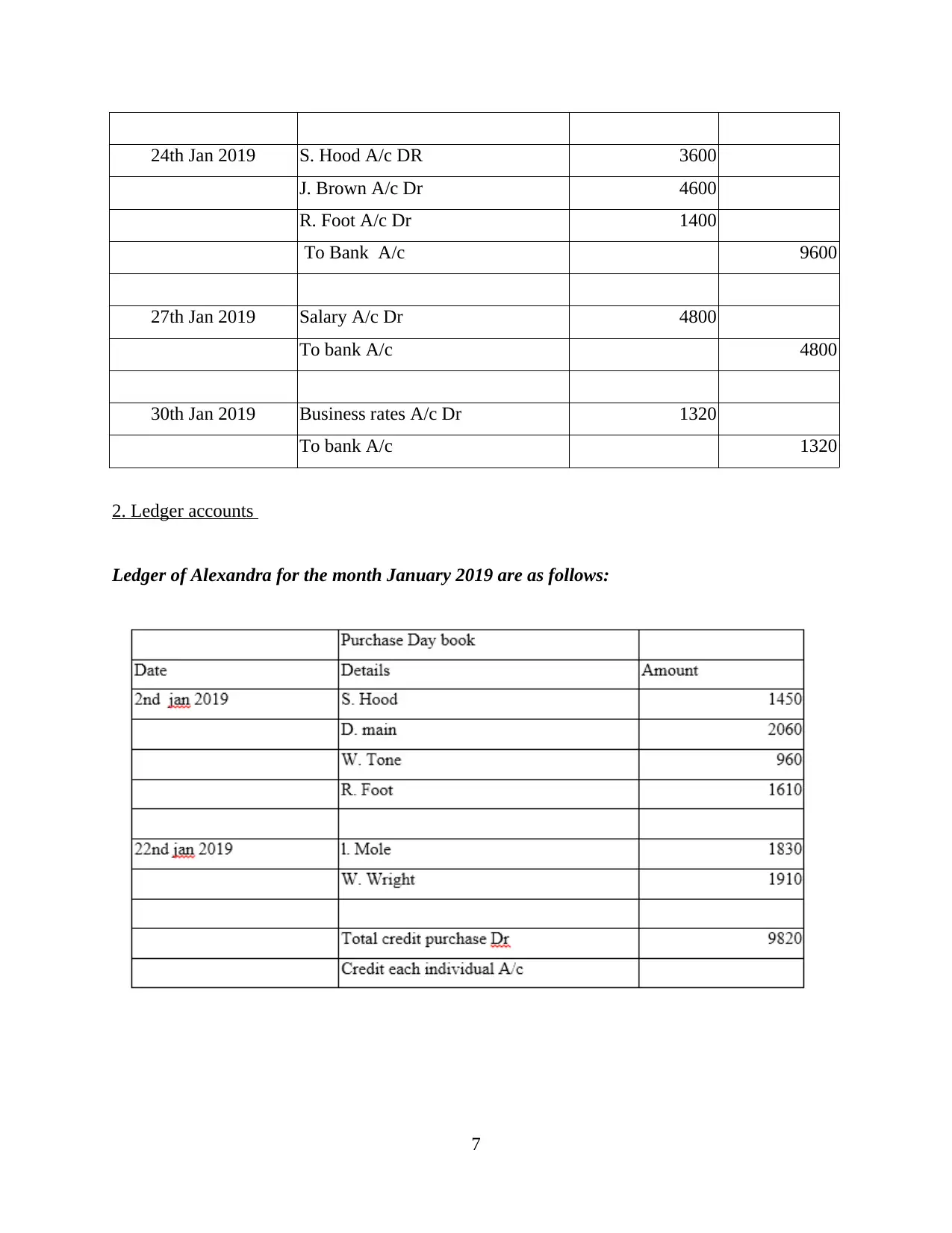

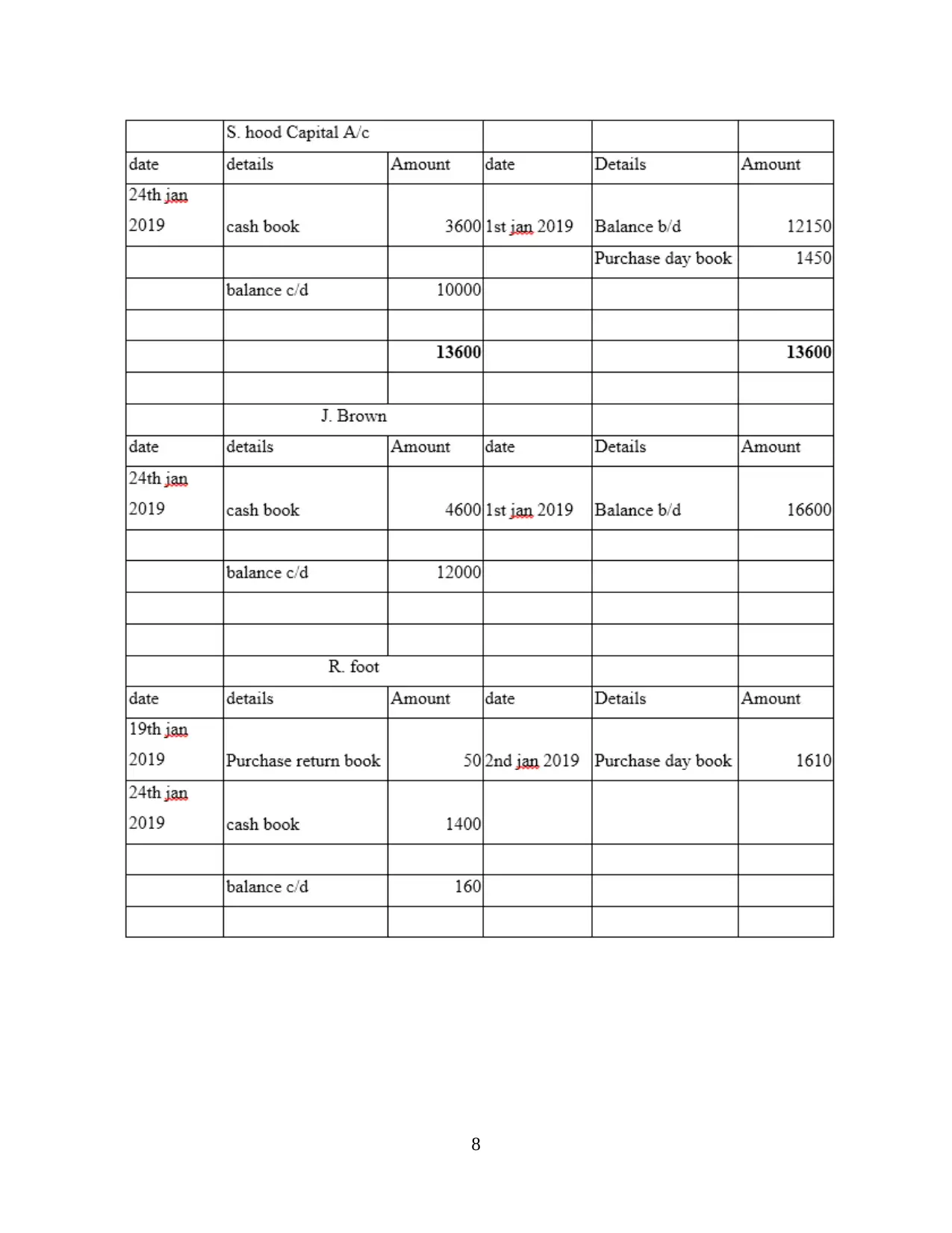

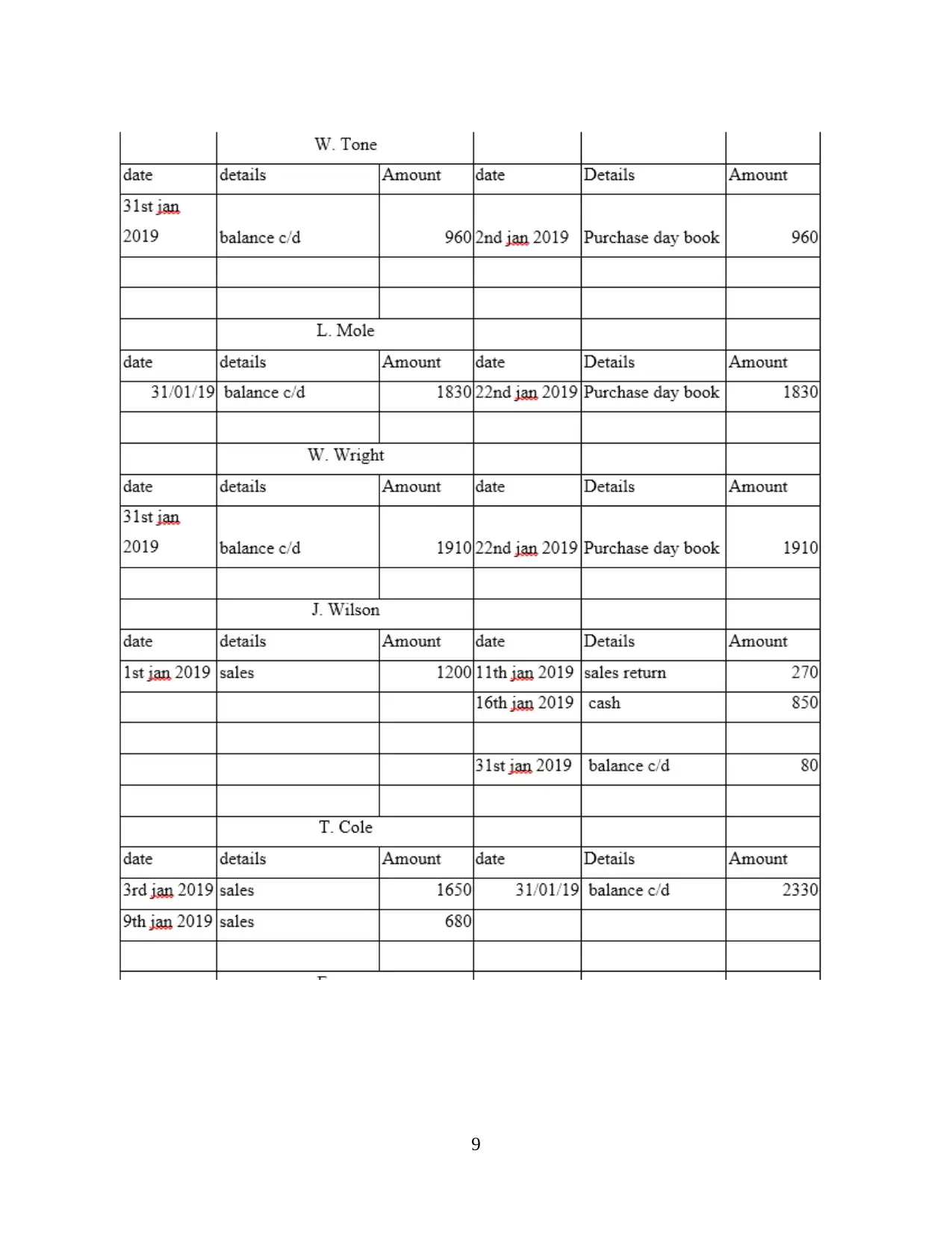

This report delves into financial accounting principles, examining their significance and purpose within the context of Brooks City, a small business accountancy firm. It covers the definition of financial accounting, its major purposes, and the preparation of financial statements. The report identifies and describes both internal (managers and owners) and external stakeholders (lenders, investors, auditors, and government), highlighting their respective interests in financial reporting. It includes detailed journal entries for January 2019, illustrating transaction recording. Furthermore, the report provides insights into accounting concepts like depreciation, suspense, and control accounts, as well as Bank Reconciliation Statements (BRS) and the causes of deviations in comparison to cash flow statements, offering a comprehensive overview of financial accounting practices.

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.