Management Accounting Principles: Costing, Planning, and Reporting

VerifiedAdded on 2024/06/11

|23

|4598

|395

Report

AI Summary

This report provides a detailed explanation of management accounting principles and their application in business organizations. It explores the essential requirements of different management accounting systems and various methods for management accounting reporting. The report evaluates the benefits of these systems and their integration within organizational processes. It includes cost calculations using marginal and absorption costing techniques to prepare income statements and applies a range of management accounting techniques to produce financial reporting documents. The analysis extends to the advantages and disadvantages of different planning tools and their use in preparing and forecasting budgets, along with how management accounting systems can respond to financial problems and contribute to sustainable success. Desklib offers this assignment solution and many more resources for students.

Management Accounting Principles and

Effective Planning Tools for Managing

Accounts

1

Effective Planning Tools for Managing

Accounts

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction....................................................................................................................................3

Task 1..............................................................................................................................................4

Introduction....................................................................................................................................4

P1 Explain management accounting and give the essential requirements of different types

of management accounting systems.............................................................................................4

P2 Explain different methods used for management accounting reporting............................6

M1 Evaluate the benefits of management accounting systems and their application within

an organizational context..............................................................................................................7

D1 Critically evaluated how management accounting systems and management accounting

reporting is integrated within organizational processes............................................................7

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs..........................................................................8

M2 Accurately apply a range of management accounting techniques and produce

appropriate financial reporting documents..............................................................................10

D2 Produce financial reports that accurately can be apply and interpret data for complex

business activities.........................................................................................................................12

Task 2............................................................................................................................................13

P4 Advantages and disadvantages of different types of planning tools..................................14

M3. Use of planning tools and its application for preparing and forecasting budgets.........16

P5. Management accounting systems to respond to financial problems................................17

M4 How responding to financial problems can lead an organization to sustainable success.

.......................................................................................................................................................18

D3 How planning tools respond to financial problems can lead an organization to

sustainable success.......................................................................................................................19

Conclusion....................................................................................................................................20

Conclusion....................................................................................................................................21

Bibliography.................................................................................................................................22

2

Introduction....................................................................................................................................3

Task 1..............................................................................................................................................4

Introduction....................................................................................................................................4

P1 Explain management accounting and give the essential requirements of different types

of management accounting systems.............................................................................................4

P2 Explain different methods used for management accounting reporting............................6

M1 Evaluate the benefits of management accounting systems and their application within

an organizational context..............................................................................................................7

D1 Critically evaluated how management accounting systems and management accounting

reporting is integrated within organizational processes............................................................7

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs..........................................................................8

M2 Accurately apply a range of management accounting techniques and produce

appropriate financial reporting documents..............................................................................10

D2 Produce financial reports that accurately can be apply and interpret data for complex

business activities.........................................................................................................................12

Task 2............................................................................................................................................13

P4 Advantages and disadvantages of different types of planning tools..................................14

M3. Use of planning tools and its application for preparing and forecasting budgets.........16

P5. Management accounting systems to respond to financial problems................................17

M4 How responding to financial problems can lead an organization to sustainable success.

.......................................................................................................................................................18

D3 How planning tools respond to financial problems can lead an organization to

sustainable success.......................................................................................................................19

Conclusion....................................................................................................................................20

Conclusion....................................................................................................................................21

Bibliography.................................................................................................................................22

2

Introduction

The given report has been prepared with the aim of explaining the concept of management

accounting in detail. This will help every business organization and especially the top level or

strategic level of any business enterprise so as to achieve a strategic competitive advantage over

its rival firms which is crucial and imperative in the dynamic environment. For the purpose of

explaining the concept of management accounting, the report has been divided into two parts.

Each part deals with different aspects of management accounting and serves different fields of

management accounting. Consideration and detailed study of both the parts will help to

understand the limitations along with the significance and importance of management

accounting. The first part deals with the concept of management accounting along with the

computation of income as per marginal and absorption costing approach. In the same manner, the

second part deals with the planning tools and its relevance in solving financial problems in a

systematic manner.

3

The given report has been prepared with the aim of explaining the concept of management

accounting in detail. This will help every business organization and especially the top level or

strategic level of any business enterprise so as to achieve a strategic competitive advantage over

its rival firms which is crucial and imperative in the dynamic environment. For the purpose of

explaining the concept of management accounting, the report has been divided into two parts.

Each part deals with different aspects of management accounting and serves different fields of

management accounting. Consideration and detailed study of both the parts will help to

understand the limitations along with the significance and importance of management

accounting. The first part deals with the concept of management accounting along with the

computation of income as per marginal and absorption costing approach. In the same manner, the

second part deals with the planning tools and its relevance in solving financial problems in a

systematic manner.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 1

Introduction

The given report has been divided into two parts covering the both theoretical and practical part.

As such, the theoretical part covers the explanation of management accounting along with the

difference between the management accounting system and management accounting reporting.

This will help to understand in a more lucid manner or way.

P1 Explain management accounting and give the essential requirements of different types

of management accounting systems.

Management accounting is concerned with the collecting, analyzing and interpreting the

information obtained from or data gathered from the financial accounting and another field of

accounting (Allison, 2014). Although management accounting has been introduced with the

alignment of financial accounting, due to the requirement and need of the top level management,

the scope and ambit of management accounting have been expanded with the increase in scope.

This has widened the boundaries of management accounting.

As of now, management accounting covers both quantitative and qualitative aspects of

management accounting (Yalcin, 2012). The main and sole purpose of management accounting

is to supply information so that the top level or strategic level can take correct and financially

viable decisions.

Image 1: Scope and ambit of management accounting

Source: By Author, 2018

It can be observed from the above image that management accounting covers both quantitative

and qualitative aspects.

The different or varied requirements of management accounting are described below. This will

help to understand the concept of management accounting in a lucid manner and can be applied

to the organizational structure of any business enterprise (Van der Stede, 2017).

4

Quantitative

information Qualitative

information

Introduction

The given report has been divided into two parts covering the both theoretical and practical part.

As such, the theoretical part covers the explanation of management accounting along with the

difference between the management accounting system and management accounting reporting.

This will help to understand in a more lucid manner or way.

P1 Explain management accounting and give the essential requirements of different types

of management accounting systems.

Management accounting is concerned with the collecting, analyzing and interpreting the

information obtained from or data gathered from the financial accounting and another field of

accounting (Allison, 2014). Although management accounting has been introduced with the

alignment of financial accounting, due to the requirement and need of the top level management,

the scope and ambit of management accounting have been expanded with the increase in scope.

This has widened the boundaries of management accounting.

As of now, management accounting covers both quantitative and qualitative aspects of

management accounting (Yalcin, 2012). The main and sole purpose of management accounting

is to supply information so that the top level or strategic level can take correct and financially

viable decisions.

Image 1: Scope and ambit of management accounting

Source: By Author, 2018

It can be observed from the above image that management accounting covers both quantitative

and qualitative aspects.

The different or varied requirements of management accounting are described below. This will

help to understand the concept of management accounting in a lucid manner and can be applied

to the organizational structure of any business enterprise (Van der Stede, 2017).

4

Quantitative

information Qualitative

information

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Image 2: Distinct functions of management accounting

Source: By Author, 2018

It can be observed from the above figure that there are different features through which

management accounting can be explained in an easy manner. Also, the above three features are

prominent and are widely used to explain the complex nature of management accounting.

Besides, these above three features, there can be other features and characteristics as well. Thus,

the figure explaining the management accounting is an exhaustive representation and there can

be others unique features as well.

5

Break even analysis

Inventory analysis

Capital budgeting analysis

Source: By Author, 2018

It can be observed from the above figure that there are different features through which

management accounting can be explained in an easy manner. Also, the above three features are

prominent and are widely used to explain the complex nature of management accounting.

Besides, these above three features, there can be other features and characteristics as well. Thus,

the figure explaining the management accounting is an exhaustive representation and there can

be others unique features as well.

5

Break even analysis

Inventory analysis

Capital budgeting analysis

P2 Explain different methods used for management accounting reporting.

There are various tools and techniques which are used or are intended for reporting of

management accounting. These tools are important since the only application of management

accounting is not important. But drawing and obtaining valid outputs from such management

accounting is equally important. This will help the reader or user of the report to understand the

data derived from the application of management accounting tools and techniques accurately and

correctly.

Selection of management accounting reporting depends on the concerned management

accounting tools and techniques applied. For instance, if cost accounting has been applied, then

cost report or product report will be relevant and appropriate management accounting reporting.

Likewise, profitability statements will be the appropriate and relevant format for the application

of financial management, another branch or field of management accounting.

Generally, there are different methods that can be employed for management accounting

reporting. Also, it is important to understand that management accounting reporting is different

from that of financial reporting. As such, financial reporting is intended for outside stakeholders.

On the other hand, management accounting is for the purpose of internal stakeholders. Thus,

information generated from the management accounting reporting can be used only by the

management and generally will not be displayed to an outsider.

Traditionally, the management accounting is also known as cost accounting. This is because

normally, the executives or senior level managers at the top level are more concerned with the

information pertaining to the cost of different products or services dealt with by the concerned

business enterprise.

However, with the passage of time, the meaning and types of the report included in management

accounting have changed and widened. Thus, all the documents derived from the application of

management accounting constitute the management accounting reporting. Thus, budget reports,

execution reports along with cost reports along with other different types of reports form part of

management accounting.

These different types of reports have been discussed in detail one by one:

Budgets: Budgets are the basic and widely used method of management accounting reporting. It

consists of benchmarks and standards that need to be achieved or fulfilled within a specified time

frame. As such, it establishes the criteria accomplishing which will help to gain a competitive

advantage over its rival firms thereby retaining the market share in the relevant industry to which

the concerned business enterprise or organization belongs. Different types of budgets that are

prepared within a business enterprise are cash budget, purchase budget, sales budget, master

budget and so on. For the betterment of result, departmental heads can be held responsible for the

preparation of different types of budgets.

Cost reports: A Cost report explains the cost structure of all the brands and products range in

which any business organisations deals. It also helps to identify the costs that can be eliminated

6

There are various tools and techniques which are used or are intended for reporting of

management accounting. These tools are important since the only application of management

accounting is not important. But drawing and obtaining valid outputs from such management

accounting is equally important. This will help the reader or user of the report to understand the

data derived from the application of management accounting tools and techniques accurately and

correctly.

Selection of management accounting reporting depends on the concerned management

accounting tools and techniques applied. For instance, if cost accounting has been applied, then

cost report or product report will be relevant and appropriate management accounting reporting.

Likewise, profitability statements will be the appropriate and relevant format for the application

of financial management, another branch or field of management accounting.

Generally, there are different methods that can be employed for management accounting

reporting. Also, it is important to understand that management accounting reporting is different

from that of financial reporting. As such, financial reporting is intended for outside stakeholders.

On the other hand, management accounting is for the purpose of internal stakeholders. Thus,

information generated from the management accounting reporting can be used only by the

management and generally will not be displayed to an outsider.

Traditionally, the management accounting is also known as cost accounting. This is because

normally, the executives or senior level managers at the top level are more concerned with the

information pertaining to the cost of different products or services dealt with by the concerned

business enterprise.

However, with the passage of time, the meaning and types of the report included in management

accounting have changed and widened. Thus, all the documents derived from the application of

management accounting constitute the management accounting reporting. Thus, budget reports,

execution reports along with cost reports along with other different types of reports form part of

management accounting.

These different types of reports have been discussed in detail one by one:

Budgets: Budgets are the basic and widely used method of management accounting reporting. It

consists of benchmarks and standards that need to be achieved or fulfilled within a specified time

frame. As such, it establishes the criteria accomplishing which will help to gain a competitive

advantage over its rival firms thereby retaining the market share in the relevant industry to which

the concerned business enterprise or organization belongs. Different types of budgets that are

prepared within a business enterprise are cash budget, purchase budget, sales budget, master

budget and so on. For the betterment of result, departmental heads can be held responsible for the

preparation of different types of budgets.

Cost reports: A Cost report explains the cost structure of all the brands and products range in

which any business organisations deals. It also helps to identify the costs that can be eliminated

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of proper care and reasonable steps can be taken. This will help to place a proper control on the

costs and more amounts of profit can be earned.

7

costs and more amounts of profit can be earned.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M1 Evaluate the benefits of management accounting systems and their application within

an organizational context.

Before understanding the concept of management accounting, it is primitive to understand that

management accounting system is different from that of management accounting. Management

accounting is the application of various qualitative and quantitative tools and techniques. On the

other hand, management accounting system is the formulation and implementation of output and

result derived from management accounting to draw a meaningful and informative statement

which can be applied in decision making.

D1 Critically evaluated how management accounting systems and management accounting

reporting is integrated within organizational processes.

Management accounting reporting and management accounting systems can be integrated so as

to achieve the desired or expected result. Only then the concerned business enterprise will be

able to survive in the industry in the long run. It becomes more important when there exists

perfect competition in the market. Thus, it will be advisable to apply equally both the

management accounting systems and management accounting reporting. Both these concepts can

be applied with the proper coordination and cooperation of all the departments and segments

operating within the business enterprise. Besides, there must be an appropriate regulatory

authority supervising and overseeing the operations and outcome of these two concepts.

For instance, the cost accounting and cost report should come under the charge of cost

accountant. In the case of organizations dealing with the

8

an organizational context.

Before understanding the concept of management accounting, it is primitive to understand that

management accounting system is different from that of management accounting. Management

accounting is the application of various qualitative and quantitative tools and techniques. On the

other hand, management accounting system is the formulation and implementation of output and

result derived from management accounting to draw a meaningful and informative statement

which can be applied in decision making.

D1 Critically evaluated how management accounting systems and management accounting

reporting is integrated within organizational processes.

Management accounting reporting and management accounting systems can be integrated so as

to achieve the desired or expected result. Only then the concerned business enterprise will be

able to survive in the industry in the long run. It becomes more important when there exists

perfect competition in the market. Thus, it will be advisable to apply equally both the

management accounting systems and management accounting reporting. Both these concepts can

be applied with the proper coordination and cooperation of all the departments and segments

operating within the business enterprise. Besides, there must be an appropriate regulatory

authority supervising and overseeing the operations and outcome of these two concepts.

For instance, the cost accounting and cost report should come under the charge of cost

accountant. In the case of organizations dealing with the

8

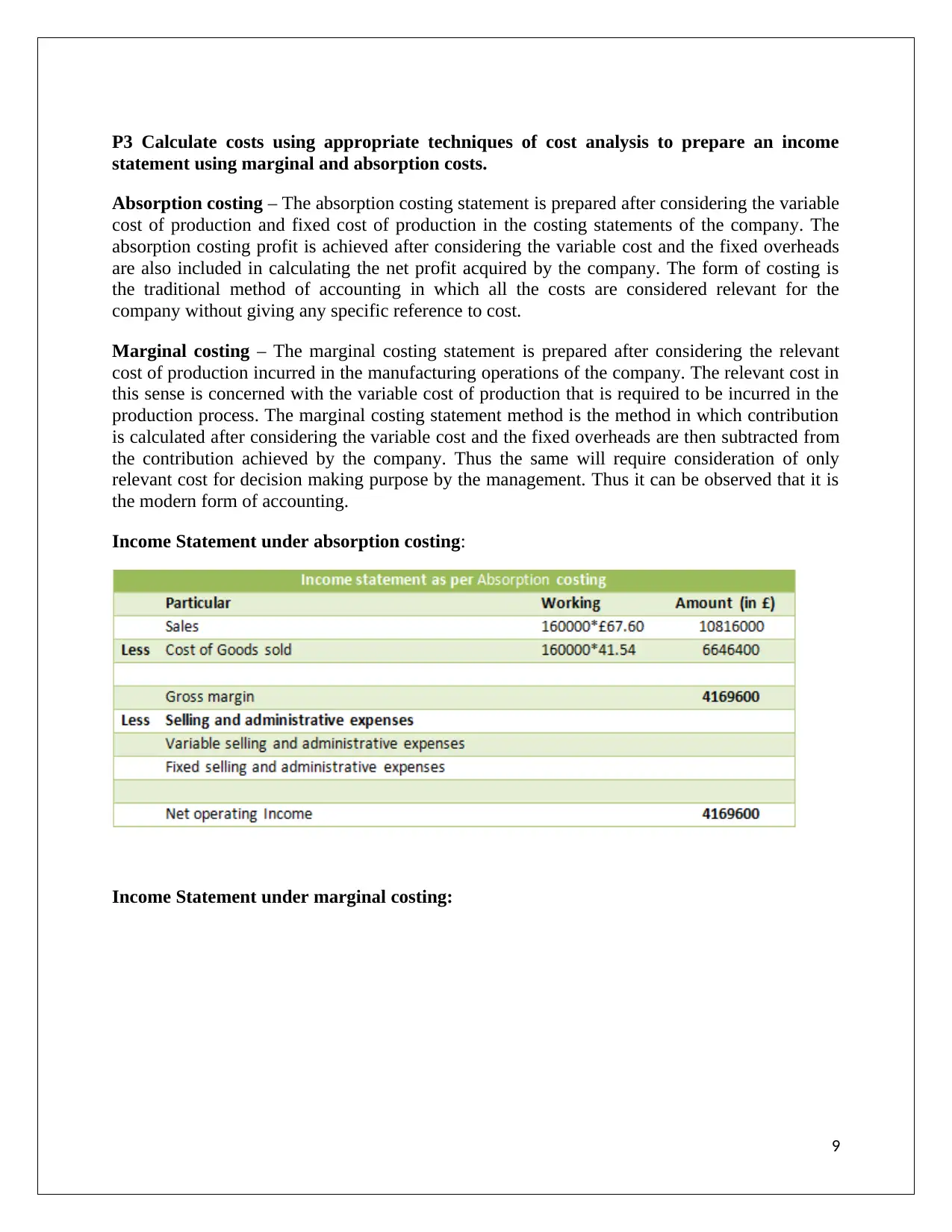

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs.

Absorption costing – The absorption costing statement is prepared after considering the variable

cost of production and fixed cost of production in the costing statements of the company. The

absorption costing profit is achieved after considering the variable cost and the fixed overheads

are also included in calculating the net profit acquired by the company. The form of costing is

the traditional method of accounting in which all the costs are considered relevant for the

company without giving any specific reference to cost.

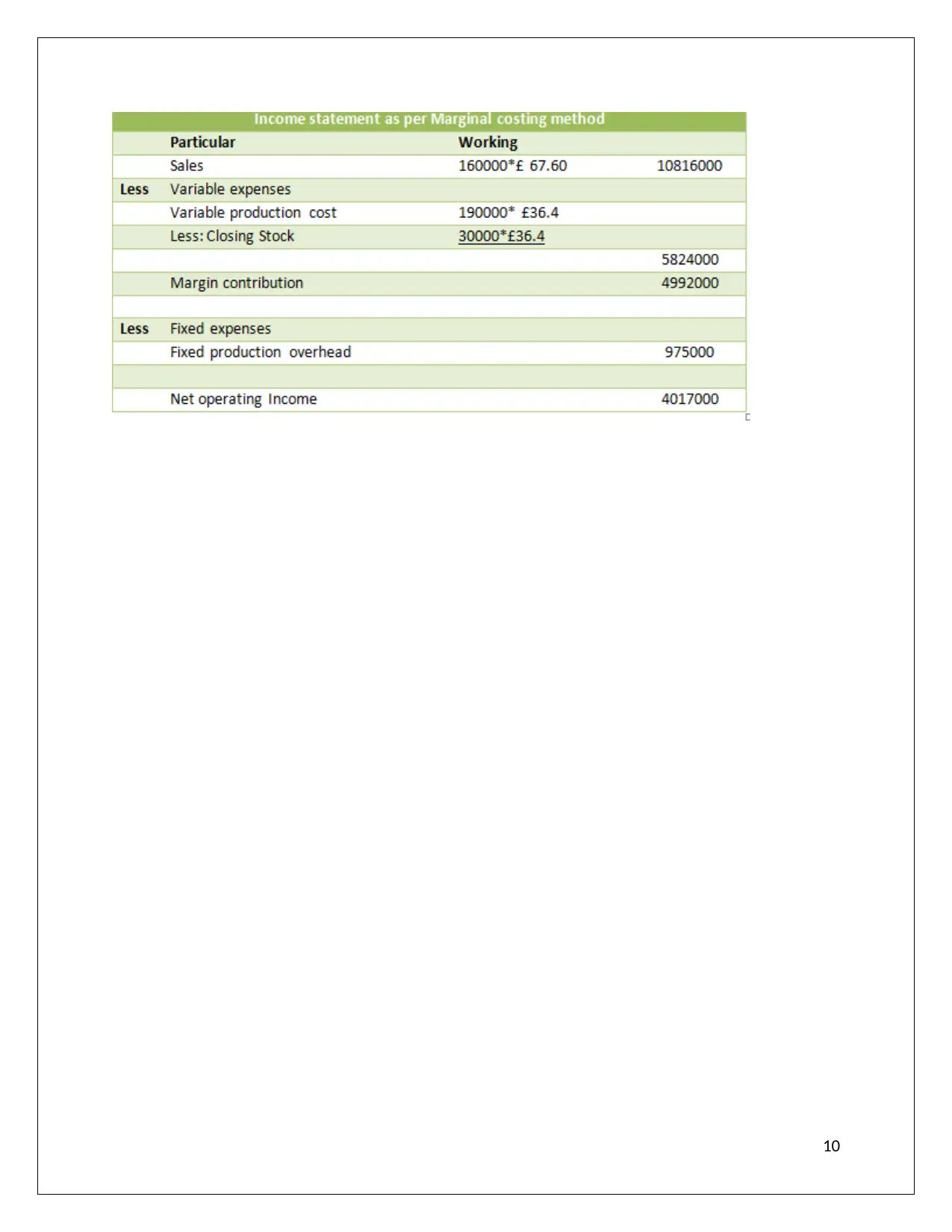

Marginal costing – The marginal costing statement is prepared after considering the relevant

cost of production incurred in the manufacturing operations of the company. The relevant cost in

this sense is concerned with the variable cost of production that is required to be incurred in the

production process. The marginal costing statement method is the method in which contribution

is calculated after considering the variable cost and the fixed overheads are then subtracted from

the contribution achieved by the company. Thus the same will require consideration of only

relevant cost for decision making purpose by the management. Thus it can be observed that it is

the modern form of accounting.

Income Statement under absorption costing:

Income Statement under marginal costing:

9

statement using marginal and absorption costs.

Absorption costing – The absorption costing statement is prepared after considering the variable

cost of production and fixed cost of production in the costing statements of the company. The

absorption costing profit is achieved after considering the variable cost and the fixed overheads

are also included in calculating the net profit acquired by the company. The form of costing is

the traditional method of accounting in which all the costs are considered relevant for the

company without giving any specific reference to cost.

Marginal costing – The marginal costing statement is prepared after considering the relevant

cost of production incurred in the manufacturing operations of the company. The relevant cost in

this sense is concerned with the variable cost of production that is required to be incurred in the

production process. The marginal costing statement method is the method in which contribution

is calculated after considering the variable cost and the fixed overheads are then subtracted from

the contribution achieved by the company. Thus the same will require consideration of only

relevant cost for decision making purpose by the management. Thus it can be observed that it is

the modern form of accounting.

Income Statement under absorption costing:

Income Statement under marginal costing:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M2 Accurately apply a range of management accounting techniques and produce

appropriate financial reporting documents.

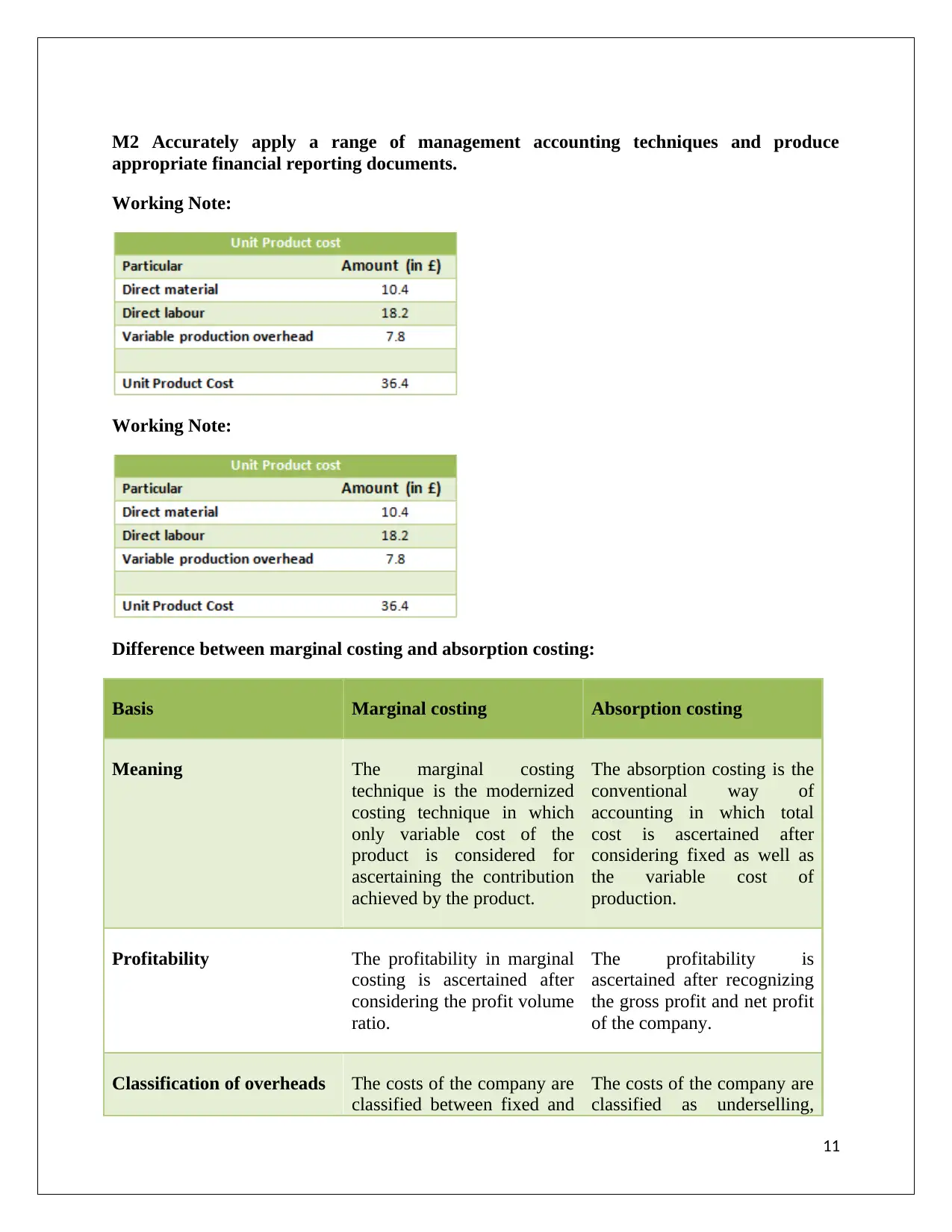

Working Note:

Working Note:

Difference between marginal costing and absorption costing:

Basis Marginal costing Absorption costing

Meaning The marginal costing

technique is the modernized

costing technique in which

only variable cost of the

product is considered for

ascertaining the contribution

achieved by the product.

The absorption costing is the

conventional way of

accounting in which total

cost is ascertained after

considering fixed as well as

the variable cost of

production.

Profitability The profitability in marginal

costing is ascertained after

considering the profit volume

ratio.

The profitability is

ascertained after recognizing

the gross profit and net profit

of the company.

Classification of overheads The costs of the company are

classified between fixed and

The costs of the company are

classified as underselling,

11

appropriate financial reporting documents.

Working Note:

Working Note:

Difference between marginal costing and absorption costing:

Basis Marginal costing Absorption costing

Meaning The marginal costing

technique is the modernized

costing technique in which

only variable cost of the

product is considered for

ascertaining the contribution

achieved by the product.

The absorption costing is the

conventional way of

accounting in which total

cost is ascertained after

considering fixed as well as

the variable cost of

production.

Profitability The profitability in marginal

costing is ascertained after

considering the profit volume

ratio.

The profitability is

ascertained after recognizing

the gross profit and net profit

of the company.

Classification of overheads The costs of the company are

classified between fixed and

The costs of the company are

classified as underselling,

11

variable cost. administration and

distribution overheads.

Absorption rate There is no requirement to

calculate the absorption rate

for the company.

The absorption rate is

calculated after considering

the variable cost of the

company and appropriate

cost center.

12

distribution overheads.

Absorption rate There is no requirement to

calculate the absorption rate

for the company.

The absorption rate is

calculated after considering

the variable cost of the

company and appropriate

cost center.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.