Accounting Principles TMA 02: VAT, Depreciation, and Ledgers

VerifiedAdded on 2020/01/07

|13

|2254

|450

Homework Assignment

AI Summary

This accounting assignment solution covers several key areas of accounting principles. It begins with a VAT account preparation, detailing transactions and obligations. The solution then assesses an extended trial balance, including accrual adjustments and prepaid expenses. Further, it explains the treatment of wages in business accounts, emphasizing the separate entity principle. The assignment also addresses depreciation calculations for various assets (buildings, plant & equipment, lorries), profit/loss on disposal, and allowance for irrecoverable receivables. It also covers non-current assets balance, figures of receivables, inventory accounting systems (AVCO and FIFO), and the profitability equation. The solution includes receivable and payment ledgers, trial balance preparation, and explanations for recording business transactions, purchase day books, and VAT registration. Finally, it provides a bank reconciliation statement, detailing adjustments and balances.

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

TMA 02...........................................................................................................................................4

QUESTION 1..................................................................................................................................4

a. Preparation of Vat account.......................................................................................................4

b. Assessing amount for extended trial balance..........................................................................5

C. Explanation for the treatment of wages in business accounts.................................................6

QUESTION 2..................................................................................................................................6

A. Calculation of depreciation, loss/profit on disposal an allowance for irrecoverable

receivables...................................................................................................................................6

B. Non-current assets balance on 30th June 2016........................................................................9

C. Figures of receivables on balance sheet................................................................................10

D. Inventory accounting system, AVCO and FIFO..................................................................11

E. Explaining profitability equation..........................................................................................11

QUESTION 3................................................................................................................................11

a. Setting out receivable and payment ledgers account.............................................................11

b. Balance off general, receivable and payment ledger account................................................12

c. Presenting a trial balance.......................................................................................................12

QUESTION 4................................................................................................................................13

a. Explaining the reasons due to which Peter needs to record all the business transactions.....13

b. Assessing the importance of purchase day book in record keeping......................................13

c. Giving advice in relation to registering VAT immediately...................................................14

d. Preparing a bank reconciliation statement.............................................................................14

TMA 02...........................................................................................................................................4

QUESTION 1..................................................................................................................................4

a. Preparation of Vat account.......................................................................................................4

b. Assessing amount for extended trial balance..........................................................................5

C. Explanation for the treatment of wages in business accounts.................................................6

QUESTION 2..................................................................................................................................6

A. Calculation of depreciation, loss/profit on disposal an allowance for irrecoverable

receivables...................................................................................................................................6

B. Non-current assets balance on 30th June 2016........................................................................9

C. Figures of receivables on balance sheet................................................................................10

D. Inventory accounting system, AVCO and FIFO..................................................................11

E. Explaining profitability equation..........................................................................................11

QUESTION 3................................................................................................................................11

a. Setting out receivable and payment ledgers account.............................................................11

b. Balance off general, receivable and payment ledger account................................................12

c. Presenting a trial balance.......................................................................................................12

QUESTION 4................................................................................................................................13

a. Explaining the reasons due to which Peter needs to record all the business transactions.....13

b. Assessing the importance of purchase day book in record keeping......................................13

c. Giving advice in relation to registering VAT immediately...................................................14

d. Preparing a bank reconciliation statement.............................................................................14

TMA 02

QUESTION 1

On the basis of cited case situation Carol owns and operates night club and it is registered

for Vat. Hence, in this, Carol wants to know his obligations in relation to Vat. Thus, Vat account

of Carol for the month ended at 30th November 2016 is as follows:

a. Preparation of Vat account

VAT account

Date

Particular

s

Debit

(in £) Date Particulars

Credit

(in £)

7-Nov-

2016 To bank 2400 1st November 2016

By balance

b/d 11200

8-Nov-

2016 to bank 11200 14-November-2016 By creditors 384

17-

Nov-

2016 To debtors 1920 15-November-2016 By bank a/c 450

30-November-2016

By balance

c/d 3486

15520 15520

The above mentioned table clearly presents that Vat obligations of Carol are related to the

amount of £3486. Moreover, Carol received £15520 from customers through the means of sales.

On the other side, individual paid £12034 for making purchase. Hence, by taking into

consideration such aspects it can be said that Carol has liability to pay £3486 to the government.

Date Transaction Assumptions

2 November Bars and restaurant takings Entry is no needed because vat

is not charged or calculated on

services.

4 November Payment of wages Wages are not the subject of

vat.

QUESTION 1

On the basis of cited case situation Carol owns and operates night club and it is registered

for Vat. Hence, in this, Carol wants to know his obligations in relation to Vat. Thus, Vat account

of Carol for the month ended at 30th November 2016 is as follows:

a. Preparation of Vat account

VAT account

Date

Particular

s

Debit

(in £) Date Particulars

Credit

(in £)

7-Nov-

2016 To bank 2400 1st November 2016

By balance

b/d 11200

8-Nov-

2016 to bank 11200 14-November-2016 By creditors 384

17-

Nov-

2016 To debtors 1920 15-November-2016 By bank a/c 450

30-November-2016

By balance

c/d 3486

15520 15520

The above mentioned table clearly presents that Vat obligations of Carol are related to the

amount of £3486. Moreover, Carol received £15520 from customers through the means of sales.

On the other side, individual paid £12034 for making purchase. Hence, by taking into

consideration such aspects it can be said that Carol has liability to pay £3486 to the government.

Date Transaction Assumptions

2 November Bars and restaurant takings Entry is no needed because vat

is not charged or calculated on

services.

4 November Payment of wages Wages are not the subject of

vat.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7 November Receiving invoice Sales of £12000 have been

made for bottled drinks.

8 November Payment of vat Vat of October has been paid.

14 November Purchase of computer Vat is charged by the seller on

computer worth of £1920.

15 November Making payment for painting Vat worth of £450 has been

paid by carol for money

invested in painting.

16 November Payment of license fees License fees are not the part of

vat.

17 November Bank receipts for sales done

through credit card

Vat is charged from customers

for the services offered by

carol.

21 November Payment for servicing the

music equipment

Services charges do not come

under the category of vat.

22 November Drawing Money withdrawal for

personal use is not the subject

of Vat payment.

24 November Cash refund from customer No vat obligations

26 November Money received from

subscription

No vat obligations

29 November Making payment for

advertising leaflets

No vat obligations

b. Assessing amount for extended trial balance

In accordance with the scenario, following accrual adjustments should be made for the

next quarter ending on 31st December, 2016, mentioned below:

1. Accrual Adjustment

Telephone expenditures a/c Dr. £1,500

made for bottled drinks.

8 November Payment of vat Vat of October has been paid.

14 November Purchase of computer Vat is charged by the seller on

computer worth of £1920.

15 November Making payment for painting Vat worth of £450 has been

paid by carol for money

invested in painting.

16 November Payment of license fees License fees are not the part of

vat.

17 November Bank receipts for sales done

through credit card

Vat is charged from customers

for the services offered by

carol.

21 November Payment for servicing the

music equipment

Services charges do not come

under the category of vat.

22 November Drawing Money withdrawal for

personal use is not the subject

of Vat payment.

24 November Cash refund from customer No vat obligations

26 November Money received from

subscription

No vat obligations

29 November Making payment for

advertising leaflets

No vat obligations

b. Assessing amount for extended trial balance

In accordance with the scenario, following accrual adjustments should be made for the

next quarter ending on 31st December, 2016, mentioned below:

1. Accrual Adjustment

Telephone expenditures a/c Dr. £1,500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

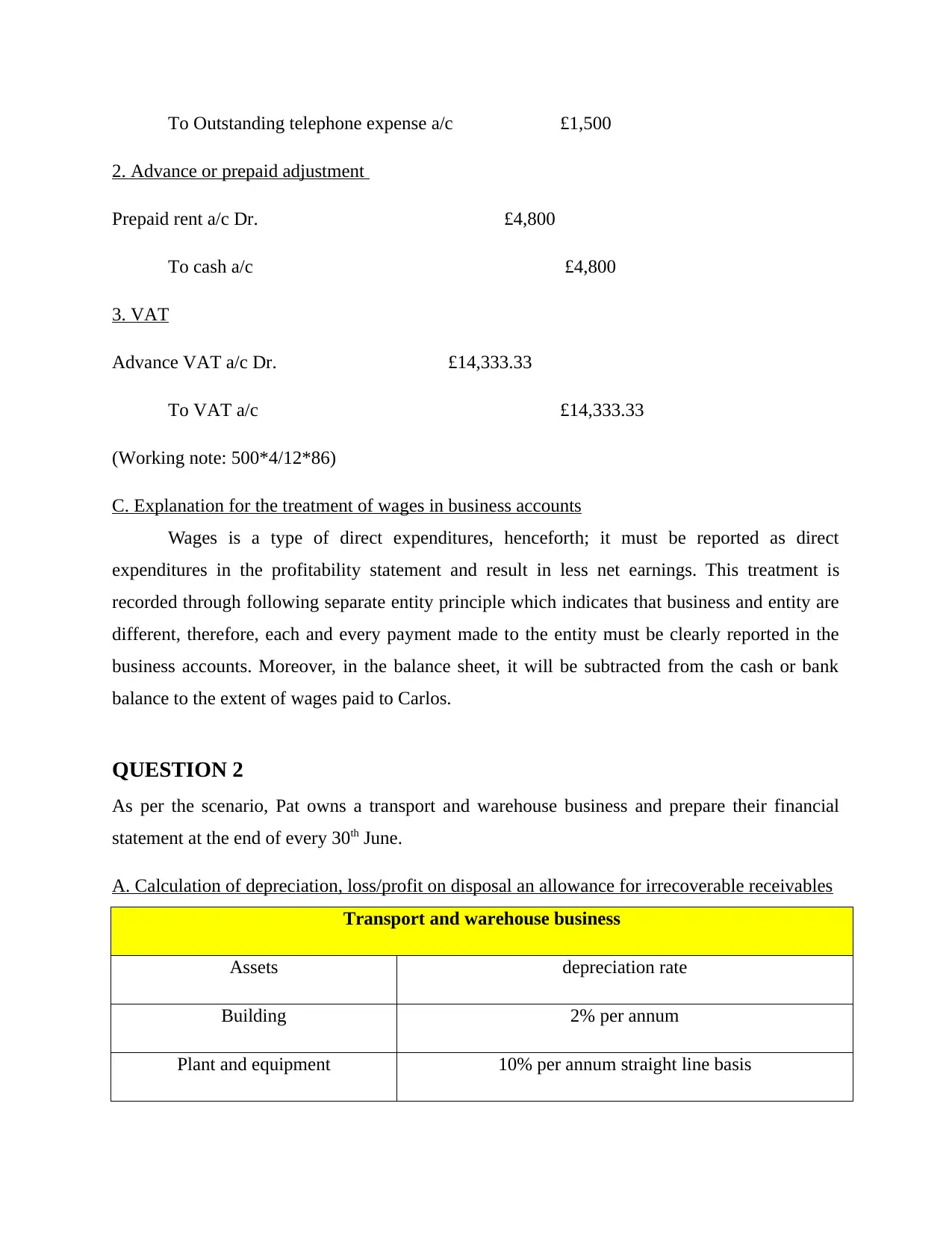

To Outstanding telephone expense a/c £1,500

2. Advance or prepaid adjustment

Prepaid rent a/c Dr. £4,800

To cash a/c £4,800

3. VAT

Advance VAT a/c Dr. £14,333.33

To VAT a/c £14,333.33

(Working note: 500*4/12*86)

C. Explanation for the treatment of wages in business accounts

Wages is a type of direct expenditures, henceforth; it must be reported as direct

expenditures in the profitability statement and result in less net earnings. This treatment is

recorded through following separate entity principle which indicates that business and entity are

different, therefore, each and every payment made to the entity must be clearly reported in the

business accounts. Moreover, in the balance sheet, it will be subtracted from the cash or bank

balance to the extent of wages paid to Carlos.

QUESTION 2

As per the scenario, Pat owns a transport and warehouse business and prepare their financial

statement at the end of every 30th June.

A. Calculation of depreciation, loss/profit on disposal an allowance for irrecoverable receivables

Transport and warehouse business

Assets depreciation rate

Building 2% per annum

Plant and equipment 10% per annum straight line basis

2. Advance or prepaid adjustment

Prepaid rent a/c Dr. £4,800

To cash a/c £4,800

3. VAT

Advance VAT a/c Dr. £14,333.33

To VAT a/c £14,333.33

(Working note: 500*4/12*86)

C. Explanation for the treatment of wages in business accounts

Wages is a type of direct expenditures, henceforth; it must be reported as direct

expenditures in the profitability statement and result in less net earnings. This treatment is

recorded through following separate entity principle which indicates that business and entity are

different, therefore, each and every payment made to the entity must be clearly reported in the

business accounts. Moreover, in the balance sheet, it will be subtracted from the cash or bank

balance to the extent of wages paid to Carlos.

QUESTION 2

As per the scenario, Pat owns a transport and warehouse business and prepare their financial

statement at the end of every 30th June.

A. Calculation of depreciation, loss/profit on disposal an allowance for irrecoverable receivables

Transport and warehouse business

Assets depreciation rate

Building 2% per annum

Plant and equipment 10% per annum straight line basis

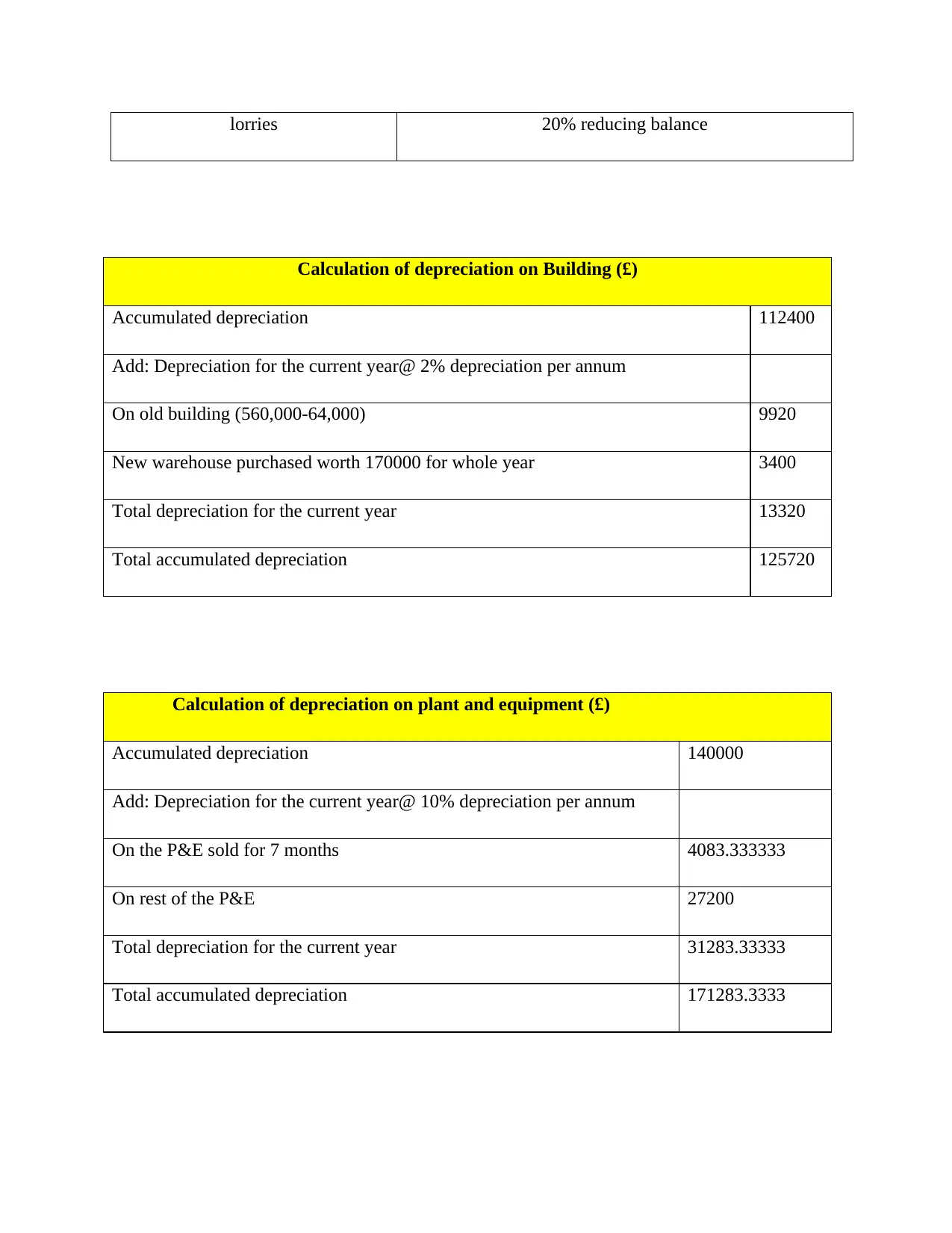

lorries 20% reducing balance

Calculation of depreciation on Building (£)

Accumulated depreciation 112400

Add: Depreciation for the current year@ 2% depreciation per annum

On old building (560,000-64,000) 9920

New warehouse purchased worth 170000 for whole year 3400

Total depreciation for the current year 13320

Total accumulated depreciation 125720

Calculation of depreciation on plant and equipment (£)

Accumulated depreciation 140000

Add: Depreciation for the current year@ 10% depreciation per annum

On the P&E sold for 7 months 4083.333333

On rest of the P&E 27200

Total depreciation for the current year 31283.33333

Total accumulated depreciation 171283.3333

Calculation of depreciation on Building (£)

Accumulated depreciation 112400

Add: Depreciation for the current year@ 2% depreciation per annum

On old building (560,000-64,000) 9920

New warehouse purchased worth 170000 for whole year 3400

Total depreciation for the current year 13320

Total accumulated depreciation 125720

Calculation of depreciation on plant and equipment (£)

Accumulated depreciation 140000

Add: Depreciation for the current year@ 10% depreciation per annum

On the P&E sold for 7 months 4083.333333

On rest of the P&E 27200

Total depreciation for the current year 31283.33333

Total accumulated depreciation 171283.3333

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

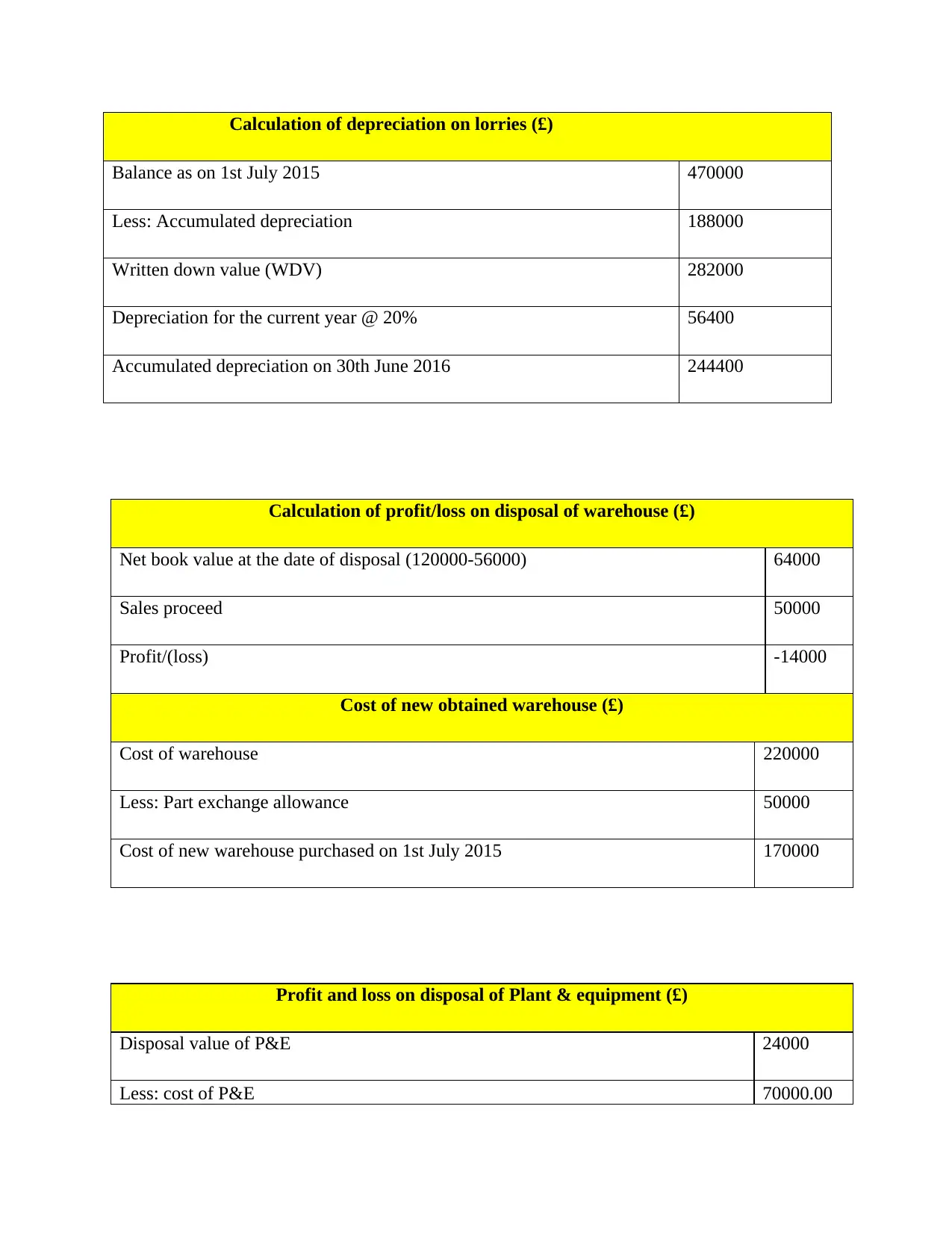

Calculation of depreciation on lorries (£)

Balance as on 1st July 2015 470000

Less: Accumulated depreciation 188000

Written down value (WDV) 282000

Depreciation for the current year @ 20% 56400

Accumulated depreciation on 30th June 2016 244400

Calculation of profit/loss on disposal of warehouse (£)

Net book value at the date of disposal (120000-56000) 64000

Sales proceed 50000

Profit/(loss) -14000

Cost of new obtained warehouse (£)

Cost of warehouse 220000

Less: Part exchange allowance 50000

Cost of new warehouse purchased on 1st July 2015 170000

Profit and loss on disposal of Plant & equipment (£)

Disposal value of P&E 24000

Less: cost of P&E 70000.00

Balance as on 1st July 2015 470000

Less: Accumulated depreciation 188000

Written down value (WDV) 282000

Depreciation for the current year @ 20% 56400

Accumulated depreciation on 30th June 2016 244400

Calculation of profit/loss on disposal of warehouse (£)

Net book value at the date of disposal (120000-56000) 64000

Sales proceed 50000

Profit/(loss) -14000

Cost of new obtained warehouse (£)

Cost of warehouse 220000

Less: Part exchange allowance 50000

Cost of new warehouse purchased on 1st July 2015 170000

Profit and loss on disposal of Plant & equipment (£)

Disposal value of P&E 24000

Less: cost of P&E 70000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

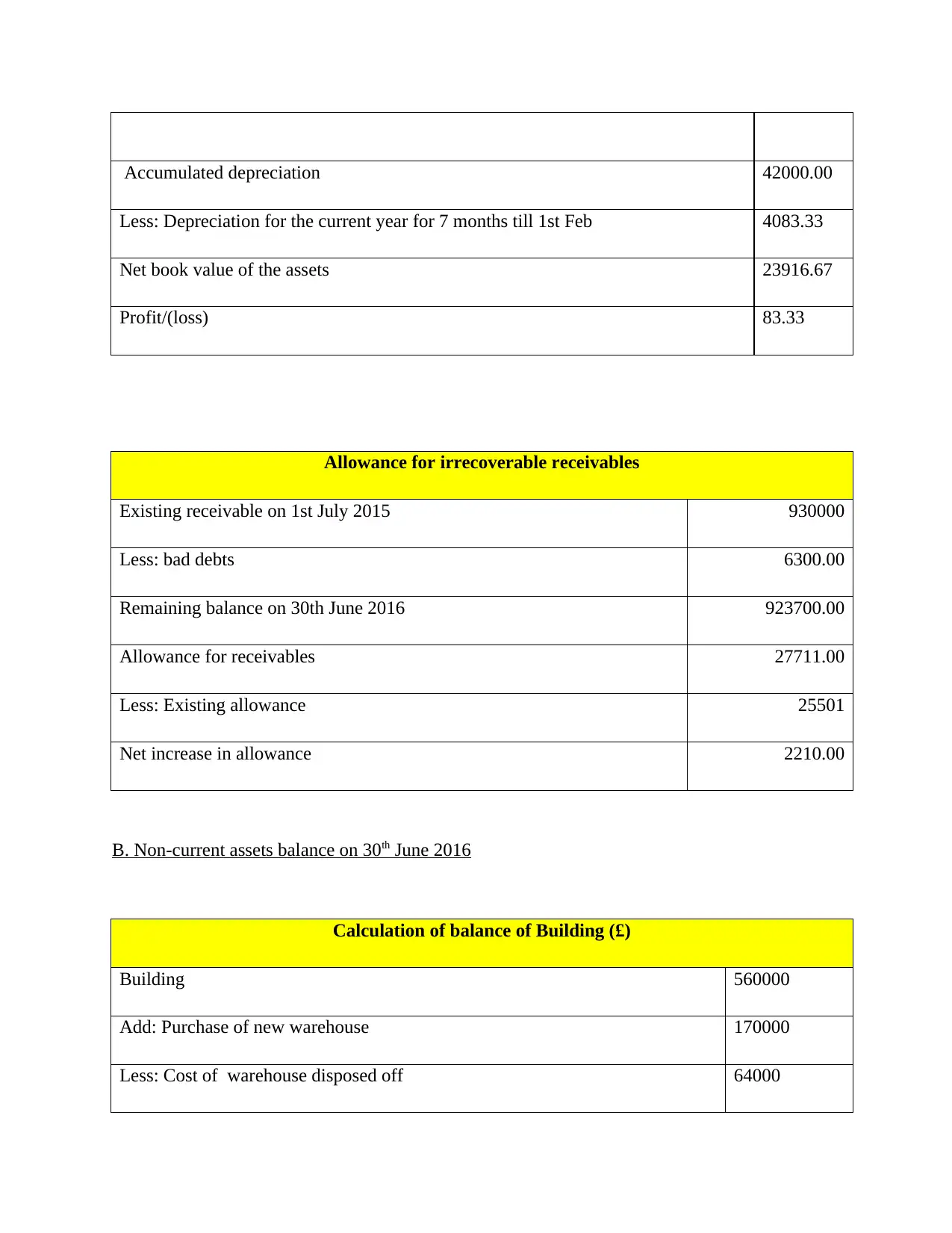

Accumulated depreciation 42000.00

Less: Depreciation for the current year for 7 months till 1st Feb 4083.33

Net book value of the assets 23916.67

Profit/(loss) 83.33

Allowance for irrecoverable receivables

Existing receivable on 1st July 2015 930000

Less: bad debts 6300.00

Remaining balance on 30th June 2016 923700.00

Allowance for receivables 27711.00

Less: Existing allowance 25501

Net increase in allowance 2210.00

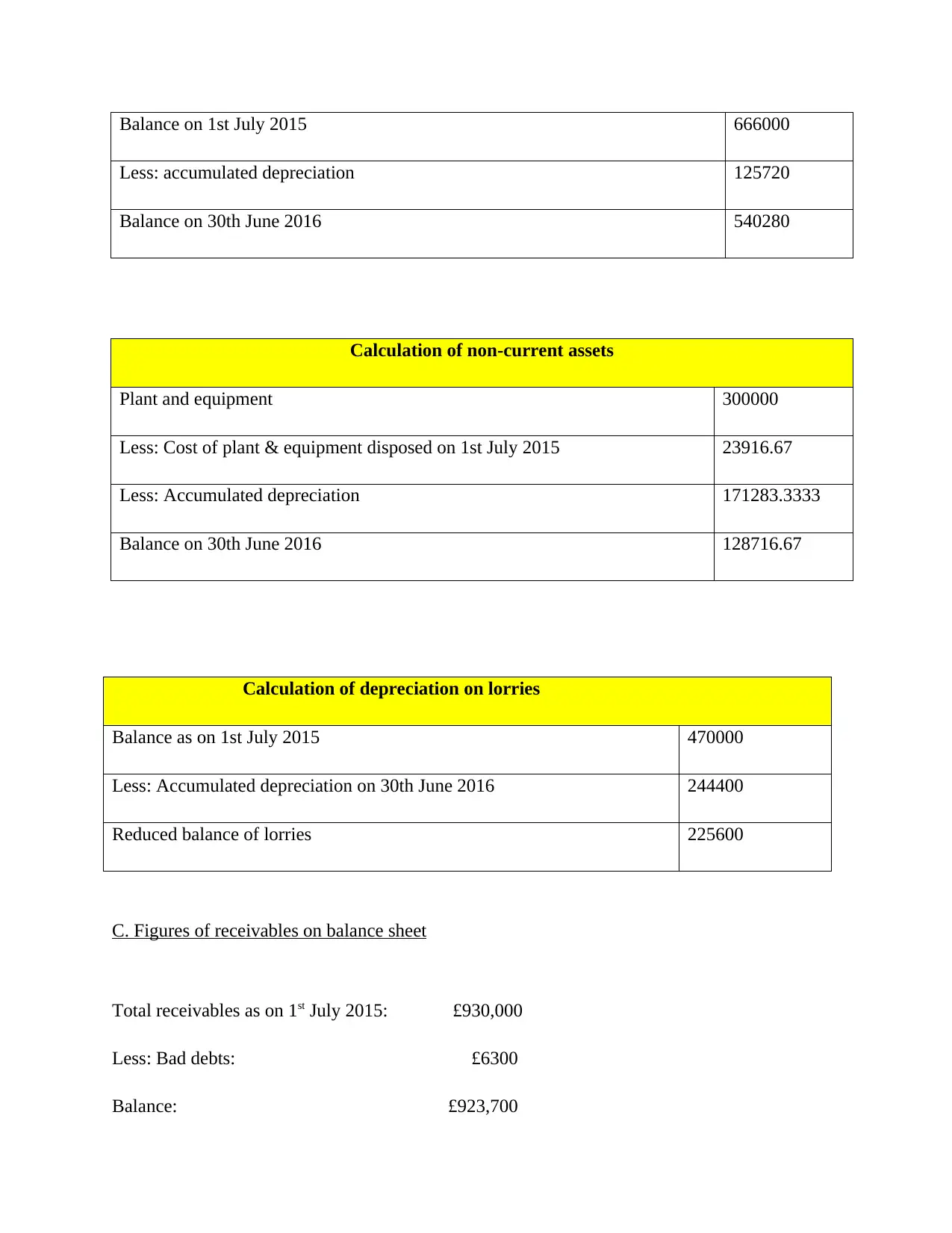

B. Non-current assets balance on 30th June 2016

Calculation of balance of Building (£)

Building 560000

Add: Purchase of new warehouse 170000

Less: Cost of warehouse disposed off 64000

Less: Depreciation for the current year for 7 months till 1st Feb 4083.33

Net book value of the assets 23916.67

Profit/(loss) 83.33

Allowance for irrecoverable receivables

Existing receivable on 1st July 2015 930000

Less: bad debts 6300.00

Remaining balance on 30th June 2016 923700.00

Allowance for receivables 27711.00

Less: Existing allowance 25501

Net increase in allowance 2210.00

B. Non-current assets balance on 30th June 2016

Calculation of balance of Building (£)

Building 560000

Add: Purchase of new warehouse 170000

Less: Cost of warehouse disposed off 64000

Balance on 1st July 2015 666000

Less: accumulated depreciation 125720

Balance on 30th June 2016 540280

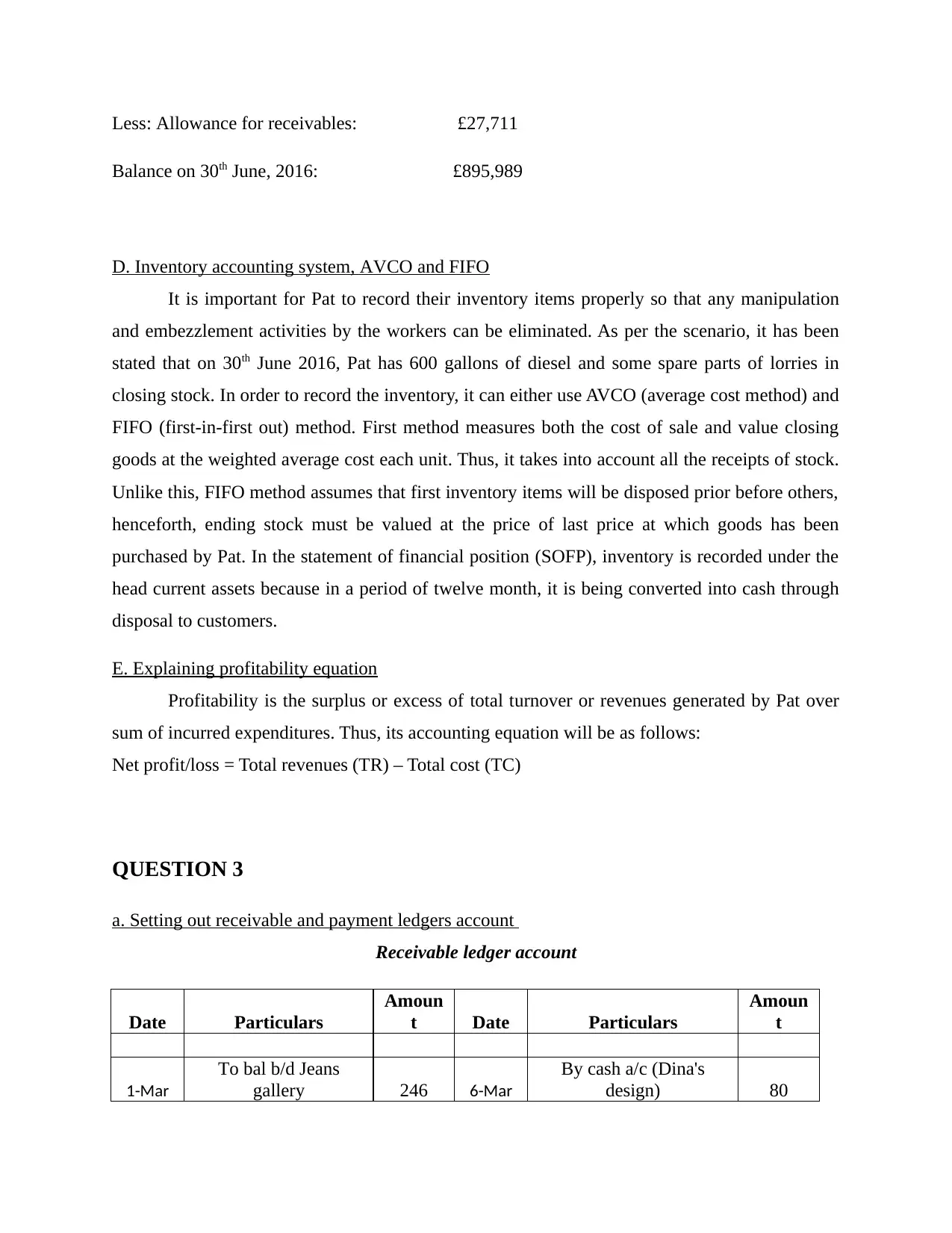

Calculation of non-current assets

Plant and equipment 300000

Less: Cost of plant & equipment disposed on 1st July 2015 23916.67

Less: Accumulated depreciation 171283.3333

Balance on 30th June 2016 128716.67

Calculation of depreciation on lorries

Balance as on 1st July 2015 470000

Less: Accumulated depreciation on 30th June 2016 244400

Reduced balance of lorries 225600

C. Figures of receivables on balance sheet

Total receivables as on 1st July 2015: £930,000

Less: Bad debts: £6300

Balance: £923,700

Less: accumulated depreciation 125720

Balance on 30th June 2016 540280

Calculation of non-current assets

Plant and equipment 300000

Less: Cost of plant & equipment disposed on 1st July 2015 23916.67

Less: Accumulated depreciation 171283.3333

Balance on 30th June 2016 128716.67

Calculation of depreciation on lorries

Balance as on 1st July 2015 470000

Less: Accumulated depreciation on 30th June 2016 244400

Reduced balance of lorries 225600

C. Figures of receivables on balance sheet

Total receivables as on 1st July 2015: £930,000

Less: Bad debts: £6300

Balance: £923,700

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less: Allowance for receivables: £27,711

Balance on 30th June, 2016: £895,989

D. Inventory accounting system, AVCO and FIFO

It is important for Pat to record their inventory items properly so that any manipulation

and embezzlement activities by the workers can be eliminated. As per the scenario, it has been

stated that on 30th June 2016, Pat has 600 gallons of diesel and some spare parts of lorries in

closing stock. In order to record the inventory, it can either use AVCO (average cost method) and

FIFO (first-in-first out) method. First method measures both the cost of sale and value closing

goods at the weighted average cost each unit. Thus, it takes into account all the receipts of stock.

Unlike this, FIFO method assumes that first inventory items will be disposed prior before others,

henceforth, ending stock must be valued at the price of last price at which goods has been

purchased by Pat. In the statement of financial position (SOFP), inventory is recorded under the

head current assets because in a period of twelve month, it is being converted into cash through

disposal to customers.

E. Explaining profitability equation

Profitability is the surplus or excess of total turnover or revenues generated by Pat over

sum of incurred expenditures. Thus, its accounting equation will be as follows:

Net profit/loss = Total revenues (TR) – Total cost (TC)

QUESTION 3

a. Setting out receivable and payment ledgers account

Receivable ledger account

Date Particulars

Amoun

t Date Particulars

Amoun

t

1-Mar

To bal b/d Jeans

gallery 246 6-Mar

By cash a/c (Dina's

design) 80

Balance on 30th June, 2016: £895,989

D. Inventory accounting system, AVCO and FIFO

It is important for Pat to record their inventory items properly so that any manipulation

and embezzlement activities by the workers can be eliminated. As per the scenario, it has been

stated that on 30th June 2016, Pat has 600 gallons of diesel and some spare parts of lorries in

closing stock. In order to record the inventory, it can either use AVCO (average cost method) and

FIFO (first-in-first out) method. First method measures both the cost of sale and value closing

goods at the weighted average cost each unit. Thus, it takes into account all the receipts of stock.

Unlike this, FIFO method assumes that first inventory items will be disposed prior before others,

henceforth, ending stock must be valued at the price of last price at which goods has been

purchased by Pat. In the statement of financial position (SOFP), inventory is recorded under the

head current assets because in a period of twelve month, it is being converted into cash through

disposal to customers.

E. Explaining profitability equation

Profitability is the surplus or excess of total turnover or revenues generated by Pat over

sum of incurred expenditures. Thus, its accounting equation will be as follows:

Net profit/loss = Total revenues (TR) – Total cost (TC)

QUESTION 3

a. Setting out receivable and payment ledgers account

Receivable ledger account

Date Particulars

Amoun

t Date Particulars

Amoun

t

1-Mar

To bal b/d Jeans

gallery 246 6-Mar

By cash a/c (Dina's

design) 80

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1-Mar

To bal b/d Dina's

design 80 12-Mar

By cash a/c (Juliette

Lebelle) 514

1-Mar

To bal b/d Shraddha

Ltd 175 14-Mar

By cash a/c (Jeans

gallery) 220

1-Mar

To bal b/d Juliette

Lebelle 1147 20-Mar

By cash a/c (Shraddha

ltd) 175

22-Mar To sales a/c 90 31-Mar By bal c/d 785

24-Mar To sales a/c 36

1774 1774

Payable Ledger account

Date Particulars

Amoun

t Date Particulars

Amoun

t

8-

Mar

To cash a/c (Payment made to

Armin supplies) 36

1-

Mar

By bal b/d Armin

supplies 36

28-

Mar

To cash a/c (Payment made to

Seamus o. Byrne) 600

1-

Mar By bal b/d Jayden Ltd 144

31-

Mar By bal c/d 312

1-

Mar

By bal b/d Seamus o'

Byrne 600

21-

Mar

By purchase a/c

(Armin supplies) 168

948 948

b. Balance off general, receivable and payment ledger account

By preparing receivable and payable ledger peter can assess the actual balance of

debtors and creditors. On the basis of this aspect balance of receivable ledger account is £785.

On the other side, balance of payable ledger account is £312. Hence, by considering such aspect

business unit can prepare suitable trial balance.

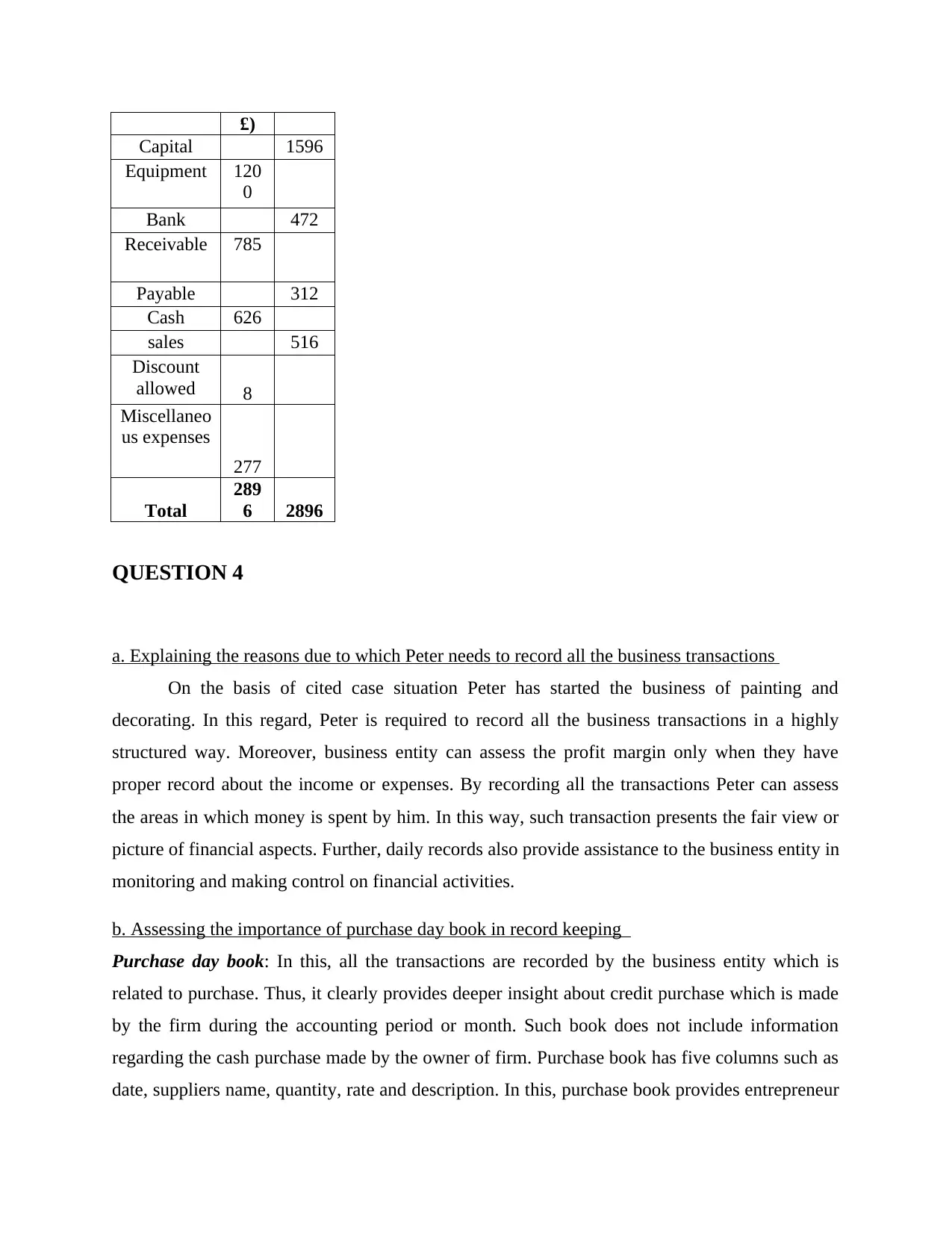

c. Presenting a trial balance

Trial balance at 1st April

Particulars Deb

it

(in

Cred

it (in

£)

To bal b/d Dina's

design 80 12-Mar

By cash a/c (Juliette

Lebelle) 514

1-Mar

To bal b/d Shraddha

Ltd 175 14-Mar

By cash a/c (Jeans

gallery) 220

1-Mar

To bal b/d Juliette

Lebelle 1147 20-Mar

By cash a/c (Shraddha

ltd) 175

22-Mar To sales a/c 90 31-Mar By bal c/d 785

24-Mar To sales a/c 36

1774 1774

Payable Ledger account

Date Particulars

Amoun

t Date Particulars

Amoun

t

8-

Mar

To cash a/c (Payment made to

Armin supplies) 36

1-

Mar

By bal b/d Armin

supplies 36

28-

Mar

To cash a/c (Payment made to

Seamus o. Byrne) 600

1-

Mar By bal b/d Jayden Ltd 144

31-

Mar By bal c/d 312

1-

Mar

By bal b/d Seamus o'

Byrne 600

21-

Mar

By purchase a/c

(Armin supplies) 168

948 948

b. Balance off general, receivable and payment ledger account

By preparing receivable and payable ledger peter can assess the actual balance of

debtors and creditors. On the basis of this aspect balance of receivable ledger account is £785.

On the other side, balance of payable ledger account is £312. Hence, by considering such aspect

business unit can prepare suitable trial balance.

c. Presenting a trial balance

Trial balance at 1st April

Particulars Deb

it

(in

Cred

it (in

£)

£)

Capital 1596

Equipment 120

0

Bank 472

Receivable 785

Payable 312

Cash 626

sales 516

Discount

allowed 8

Miscellaneo

us expenses

277

Total

289

6 2896

QUESTION 4

a. Explaining the reasons due to which Peter needs to record all the business transactions

On the basis of cited case situation Peter has started the business of painting and

decorating. In this regard, Peter is required to record all the business transactions in a highly

structured way. Moreover, business entity can assess the profit margin only when they have

proper record about the income or expenses. By recording all the transactions Peter can assess

the areas in which money is spent by him. In this way, such transaction presents the fair view or

picture of financial aspects. Further, daily records also provide assistance to the business entity in

monitoring and making control on financial activities.

b. Assessing the importance of purchase day book in record keeping

Purchase day book: In this, all the transactions are recorded by the business entity which is

related to purchase. Thus, it clearly provides deeper insight about credit purchase which is made

by the firm during the accounting period or month. Such book does not include information

regarding the cash purchase made by the owner of firm. Purchase book has five columns such as

date, suppliers name, quantity, rate and description. In this, purchase book provides entrepreneur

Capital 1596

Equipment 120

0

Bank 472

Receivable 785

Payable 312

Cash 626

sales 516

Discount

allowed 8

Miscellaneo

us expenses

277

Total

289

6 2896

QUESTION 4

a. Explaining the reasons due to which Peter needs to record all the business transactions

On the basis of cited case situation Peter has started the business of painting and

decorating. In this regard, Peter is required to record all the business transactions in a highly

structured way. Moreover, business entity can assess the profit margin only when they have

proper record about the income or expenses. By recording all the transactions Peter can assess

the areas in which money is spent by him. In this way, such transaction presents the fair view or

picture of financial aspects. Further, daily records also provide assistance to the business entity in

monitoring and making control on financial activities.

b. Assessing the importance of purchase day book in record keeping

Purchase day book: In this, all the transactions are recorded by the business entity which is

related to purchase. Thus, it clearly provides deeper insight about credit purchase which is made

by the firm during the accounting period or month. Such book does not include information

regarding the cash purchase made by the owner of firm. Purchase book has five columns such as

date, suppliers name, quantity, rate and description. In this, purchase book provides entrepreneur

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.