HA1020 Accounting Principles and Practices Tutorial Questions 2020

VerifiedAdded on 2023/01/10

|6

|571

|29

Homework Assignment

AI Summary

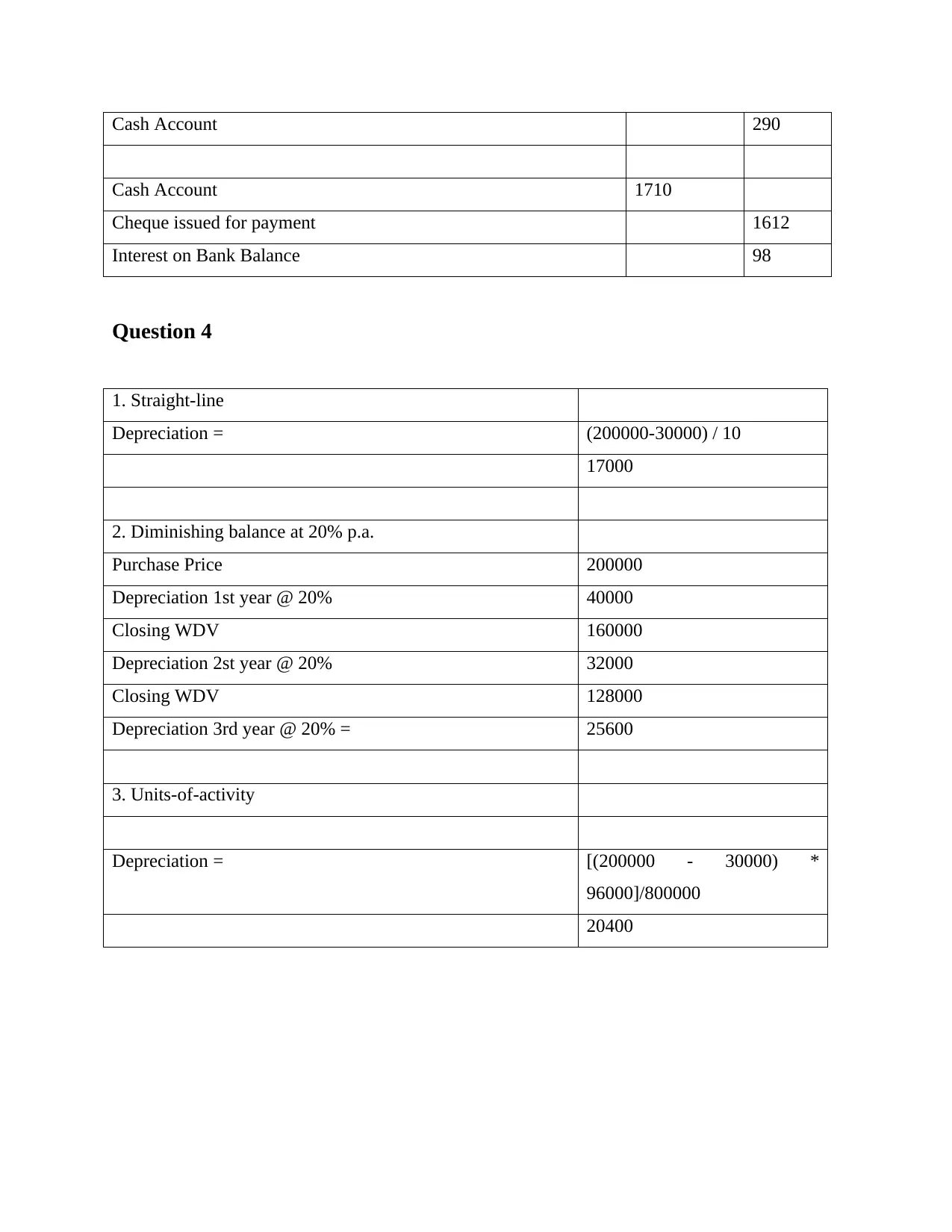

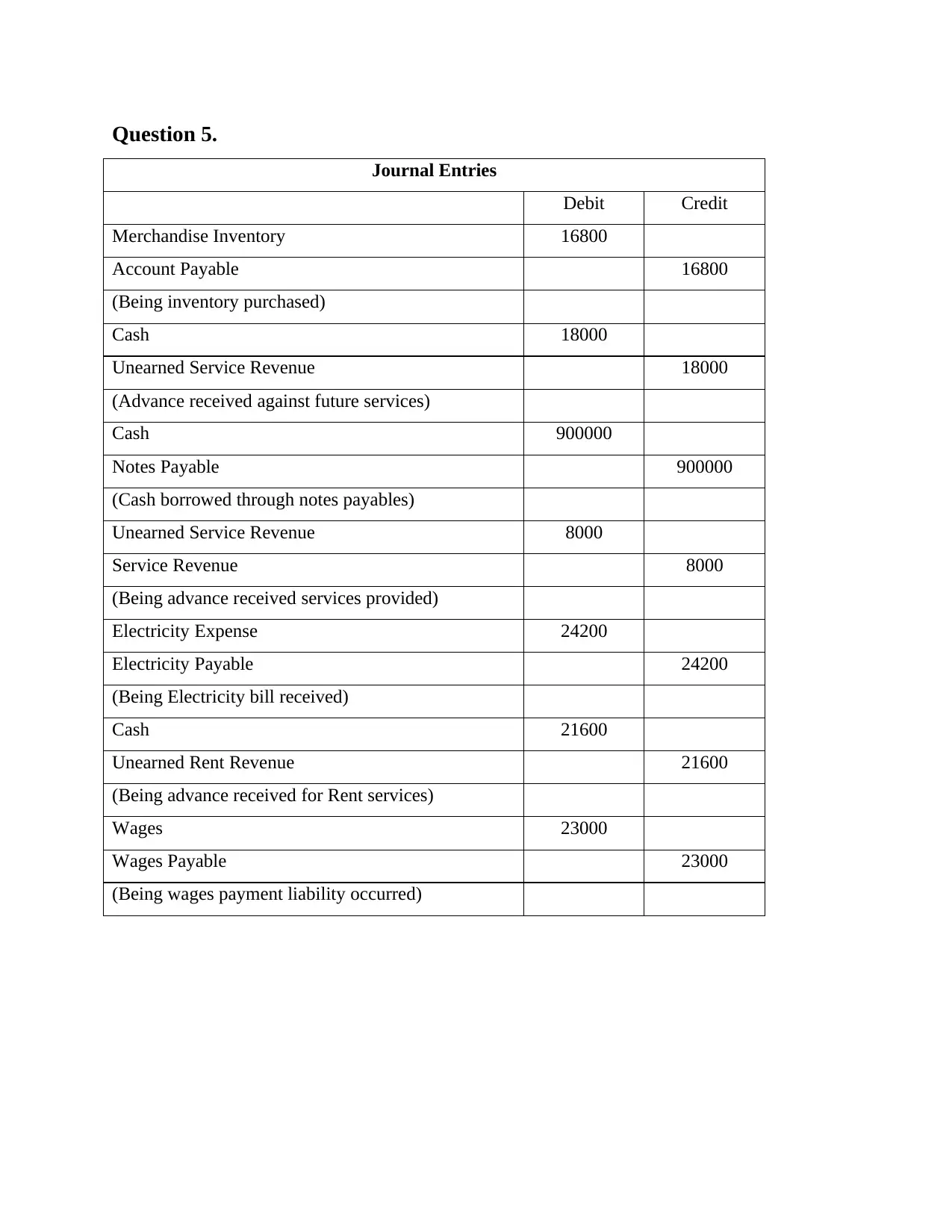

This document contains solutions to tutorial questions from an accounting principles and practices course (HA1020). The solutions cover key accounting concepts, including bad debts, the allowance for doubtful accounts, inventory systems (periodic and perpetual), bank reconciliation, and depreciation methods (straight-line, diminishing balance, and units-of-activity). The assignment also provides journal entries for various transactions, such as inventory purchases, unearned revenue, notes payable, and expense accruals. This resource is designed to help students understand and apply accounting principles to solve practical problems and prepare for assessments.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.