Solutions to Problems: Advance Financial Accounting - Inventory Ratios

VerifiedAdded on 2023/04/23

|9

|1958

|415

Homework Assignment

AI Summary

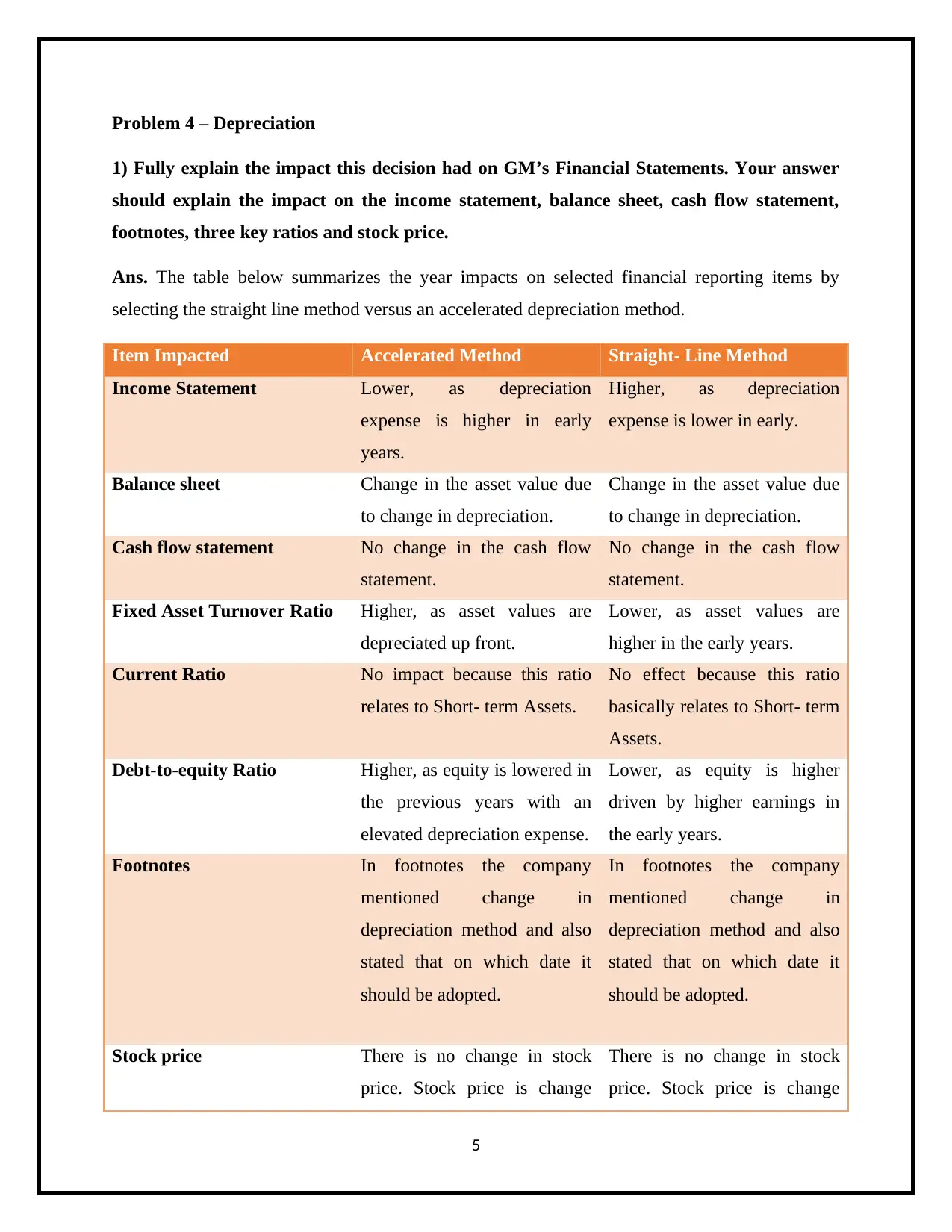

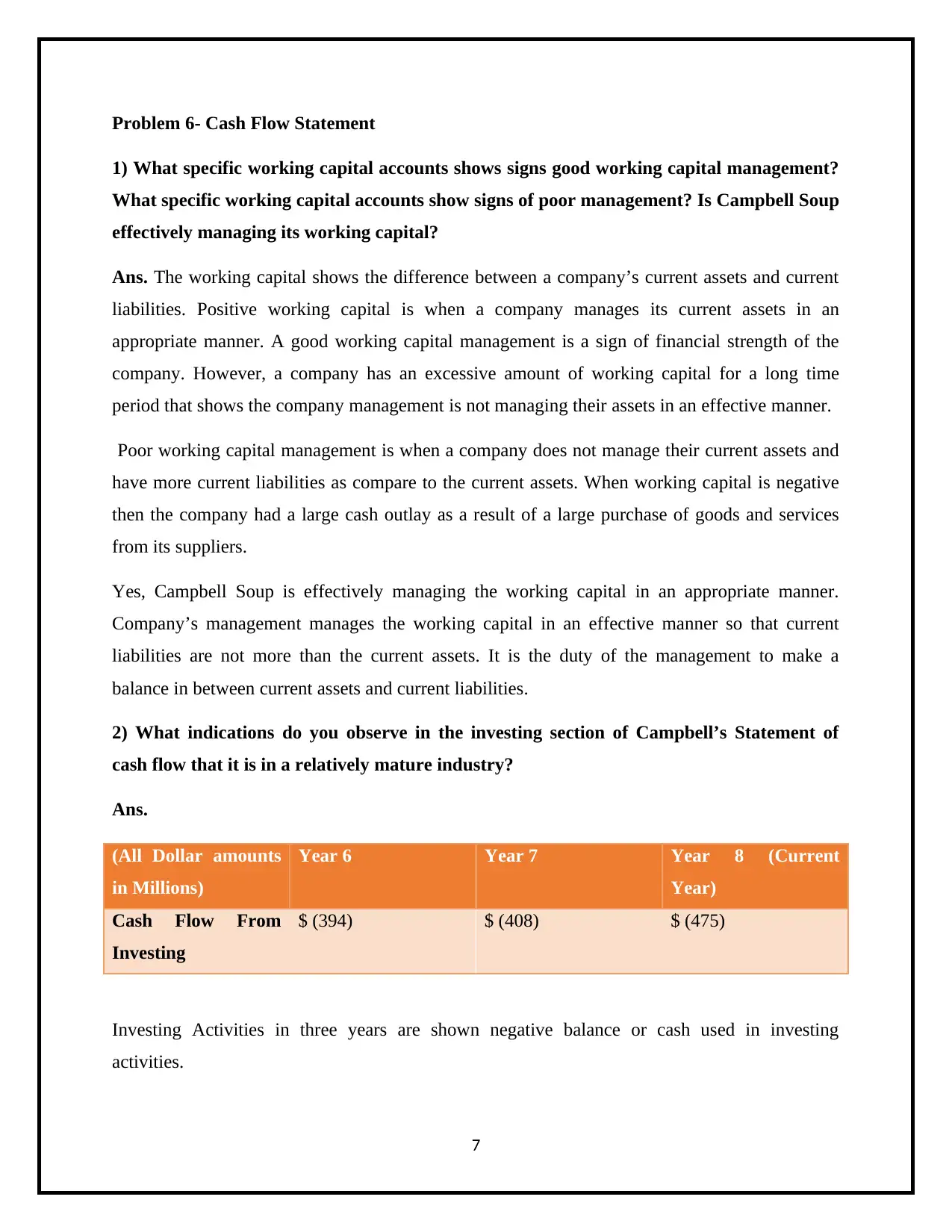

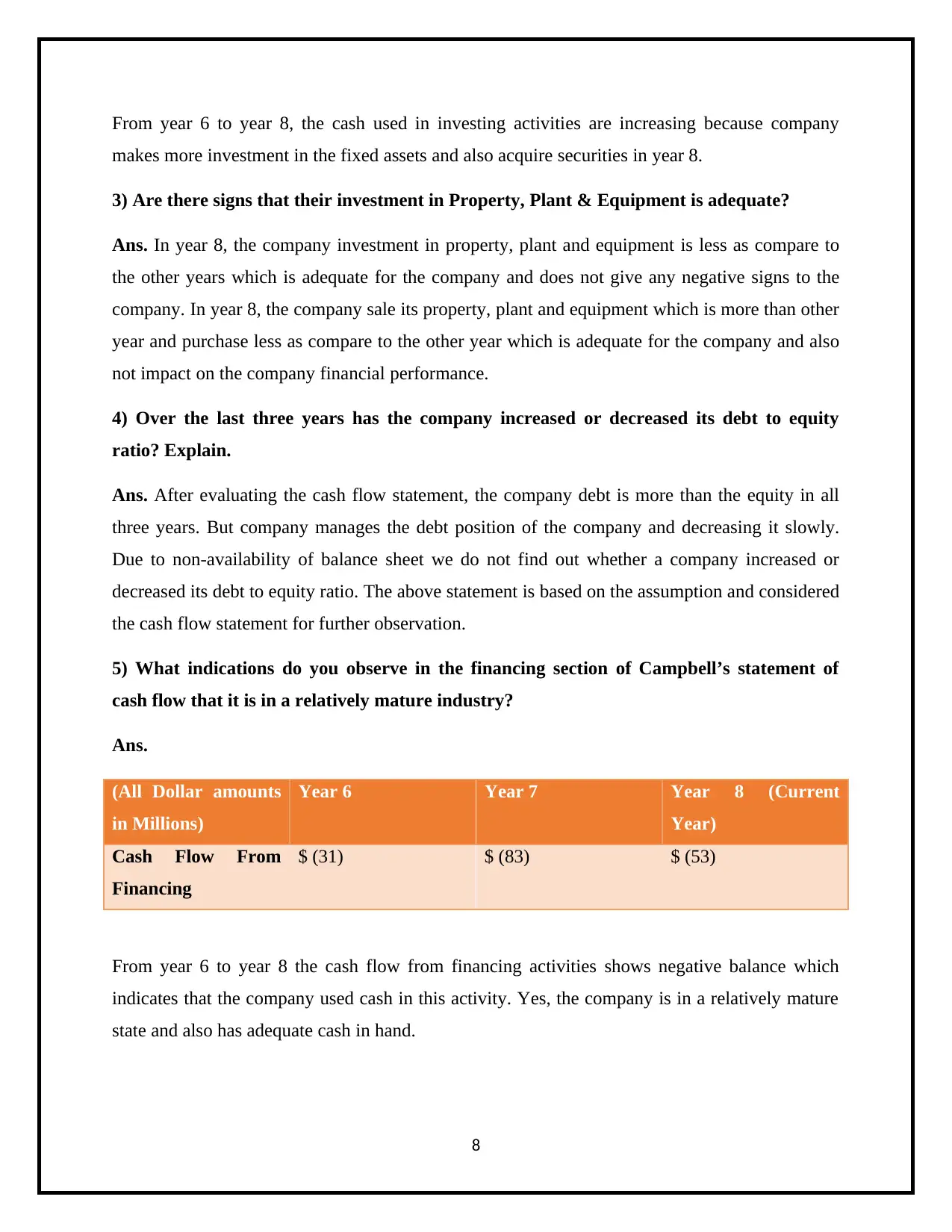

This assignment provides solutions to several problems in advanced financial accounting. The first problem compares the impact of LIFO and FIFO inventory costing methods on key financial ratios. The second problem analyzes HP's accounts receivable, including the allowance for doubtful accounts and bad debt expense, across multiple years. The fourth problem discusses the impact of changing depreciation methods on GM's financial statements and the justifications for such a change. Finally, the sixth problem examines Campbell Soup's cash flow statement, focusing on working capital management, investment activities, and financing activities, to assess the company's financial health and maturity. Desklib is a platform where students can find similar solved assignments and past papers.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.