Assignment Solution: Accounting Processes and Systems Analysis

VerifiedAdded on 2023/01/16

|19

|4063

|99

Homework Assignment

AI Summary

This document presents a comprehensive solution to an accounting assignment focused on accounting processes and systems. The solution begins with detailed journal entries for various transactions, followed by the creation of ledger accounts to track the impact of these transactions. An unadjusted trial balance is then constructed, and adjusting journal entries are provided to ensure accuracy. The document culminates in the preparation of an income statement and a balance sheet, offering a complete overview of the company's financial performance and position. The assignment also includes explanations of key concepts like double-entry bookkeeping and its importance. The solution covers a range of accounting topics, from initial investment and loans to depreciation, revenue recognition, and expense allocation, demonstrating a thorough understanding of accounting principles. Additionally, the assignment explores the implications of loan repayment on the company's financial health and ratios.

Running head: ACCOUNTING PROCESSES AND SYSTEMS

1

ACCOUNTING PROCESSES AND SYSTEMS

1

ACCOUNTING PROCESSES AND SYSTEMS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING PROCESSES AND SYSTEMS 2

Table of Contents

Question 1...................................................................................................................................................3

1...............................................................................................................................................................3

2...............................................................................................................................................................5

3...............................................................................................................................................................8

4...............................................................................................................................................................9

5.............................................................................................................................................................10

6.............................................................................................................................................................10

7.............................................................................................................................................................11

Question 2.................................................................................................................................................11

Importance of Double Entry Bookkeeping.............................................................................................12

Question 3.................................................................................................................................................14

1.............................................................................................................................................................14

Accounting issues..................................................................................................................................15

Related party Transactions....................................................................................................................15

Opaque Operations................................................................................................................................15

Poor strategic planning and expansion...................................................................................................16

2.............................................................................................................................................................16

Ethical issues.........................................................................................................................................16

References.................................................................................................................................................18

Table of Contents

Question 1...................................................................................................................................................3

1...............................................................................................................................................................3

2...............................................................................................................................................................5

3...............................................................................................................................................................8

4...............................................................................................................................................................9

5.............................................................................................................................................................10

6.............................................................................................................................................................10

7.............................................................................................................................................................11

Question 2.................................................................................................................................................11

Importance of Double Entry Bookkeeping.............................................................................................12

Question 3.................................................................................................................................................14

1.............................................................................................................................................................14

Accounting issues..................................................................................................................................15

Related party Transactions....................................................................................................................15

Opaque Operations................................................................................................................................15

Poor strategic planning and expansion...................................................................................................16

2.............................................................................................................................................................16

Ethical issues.........................................................................................................................................16

References.................................................................................................................................................18

ACCOUNTING PROCESSES AND SYSTEMS 3

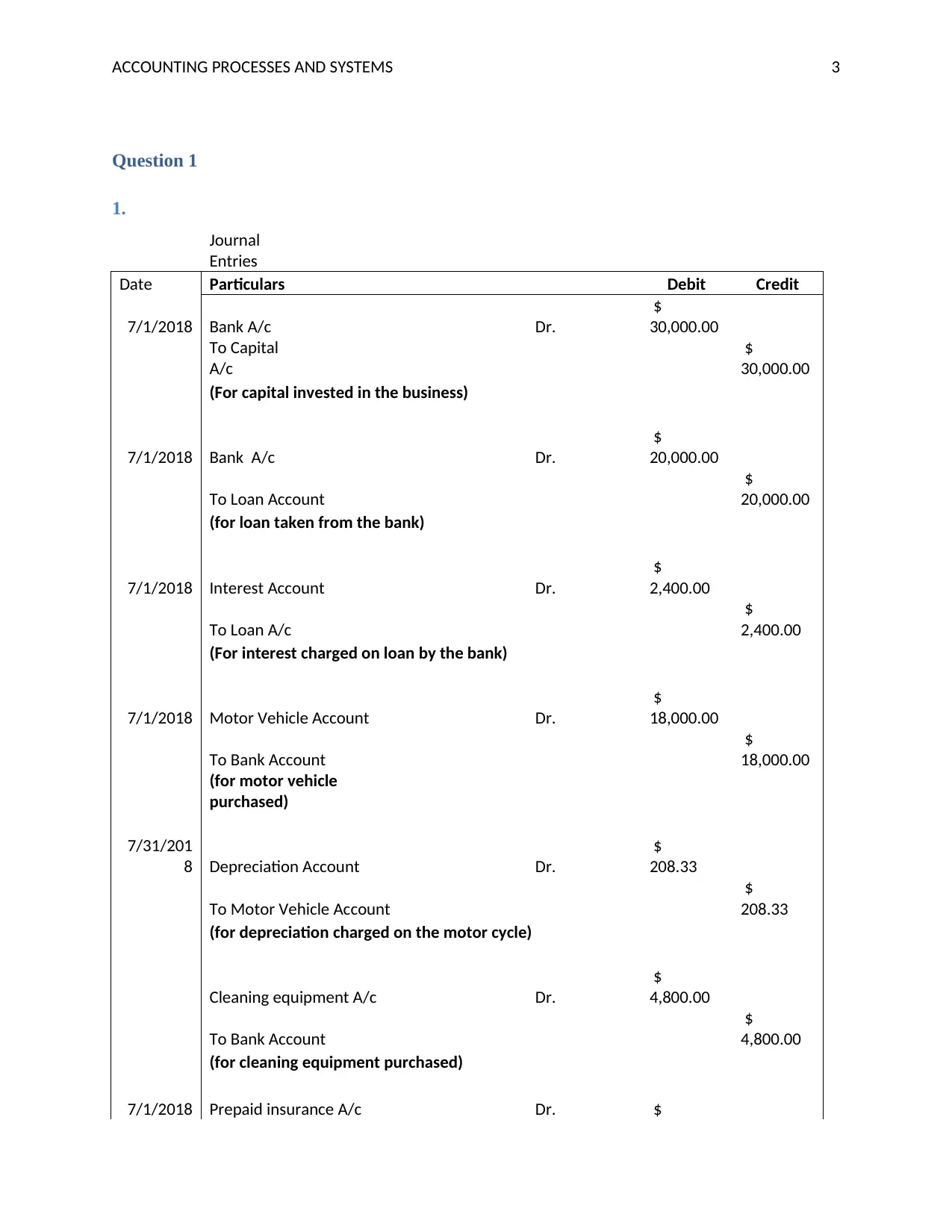

Question 1

1.

Journal

Entries

Date Particulars Debit Credit

7/1/2018 Bank A/c Dr.

$

30,000.00

To Capital

A/c

$

30,000.00

(For capital invested in the business)

7/1/2018 Bank A/c Dr.

$

20,000.00

To Loan Account

$

20,000.00

(for loan taken from the bank)

7/1/2018 Interest Account Dr.

$

2,400.00

To Loan A/c

$

2,400.00

(For interest charged on loan by the bank)

7/1/2018 Motor Vehicle Account Dr.

$

18,000.00

To Bank Account

$

18,000.00

(for motor vehicle

purchased)

7/31/201

8 Depreciation Account Dr.

$

208.33

To Motor Vehicle Account

$

208.33

(for depreciation charged on the motor cycle)

Cleaning equipment A/c Dr.

$

4,800.00

To Bank Account

$

4,800.00

(for cleaning equipment purchased)

7/1/2018 Prepaid insurance A/c Dr. $

Question 1

1.

Journal

Entries

Date Particulars Debit Credit

7/1/2018 Bank A/c Dr.

$

30,000.00

To Capital

A/c

$

30,000.00

(For capital invested in the business)

7/1/2018 Bank A/c Dr.

$

20,000.00

To Loan Account

$

20,000.00

(for loan taken from the bank)

7/1/2018 Interest Account Dr.

$

2,400.00

To Loan A/c

$

2,400.00

(For interest charged on loan by the bank)

7/1/2018 Motor Vehicle Account Dr.

$

18,000.00

To Bank Account

$

18,000.00

(for motor vehicle

purchased)

7/31/201

8 Depreciation Account Dr.

$

208.33

To Motor Vehicle Account

$

208.33

(for depreciation charged on the motor cycle)

Cleaning equipment A/c Dr.

$

4,800.00

To Bank Account

$

4,800.00

(for cleaning equipment purchased)

7/1/2018 Prepaid insurance A/c Dr. $

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

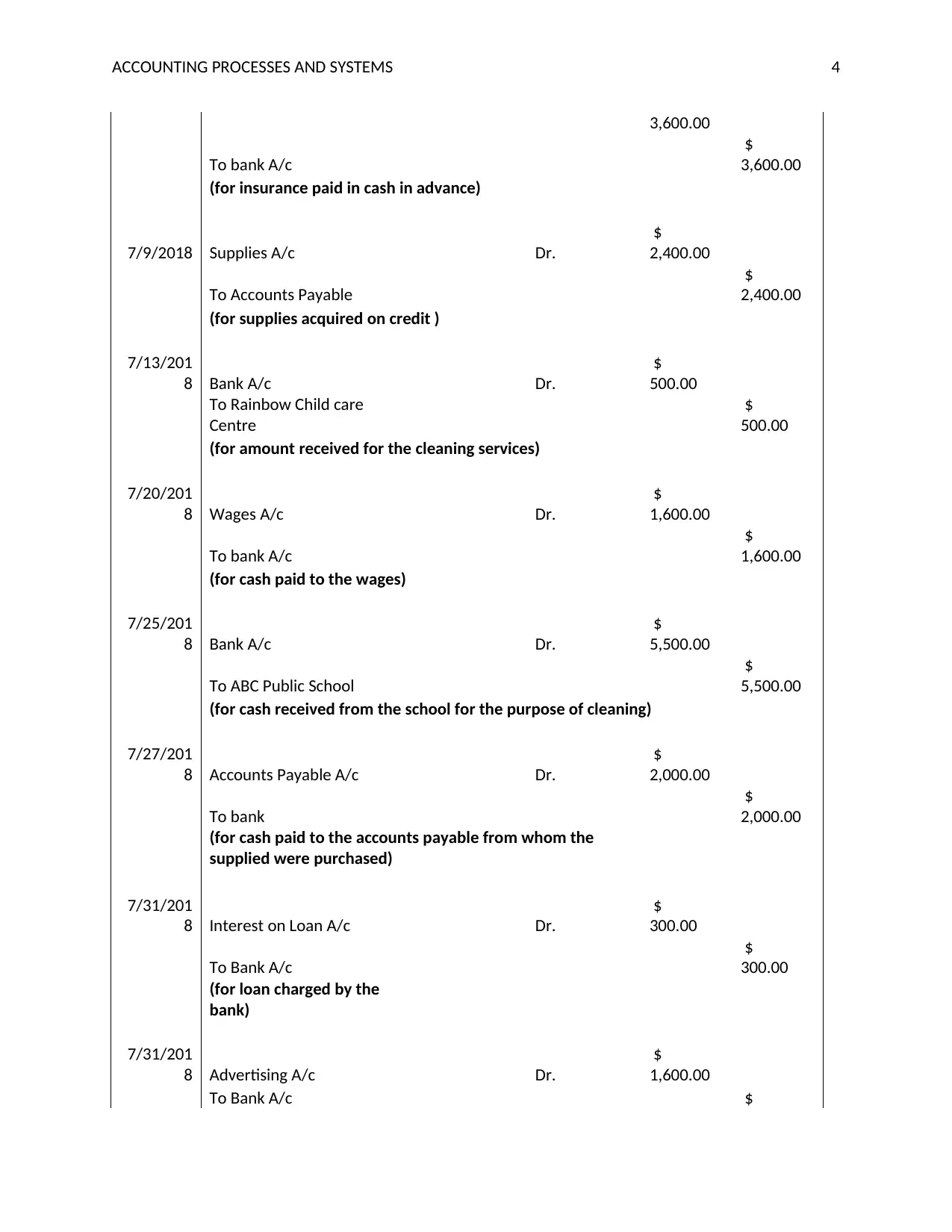

ACCOUNTING PROCESSES AND SYSTEMS 4

3,600.00

To bank A/c

$

3,600.00

(for insurance paid in cash in advance)

7/9/2018 Supplies A/c Dr.

$

2,400.00

To Accounts Payable

$

2,400.00

(for supplies acquired on credit )

7/13/201

8 Bank A/c Dr.

$

500.00

To Rainbow Child care

Centre

$

500.00

(for amount received for the cleaning services)

7/20/201

8 Wages A/c Dr.

$

1,600.00

To bank A/c

$

1,600.00

(for cash paid to the wages)

7/25/201

8 Bank A/c Dr.

$

5,500.00

To ABC Public School

$

5,500.00

(for cash received from the school for the purpose of cleaning)

7/27/201

8 Accounts Payable A/c Dr.

$

2,000.00

To bank

$

2,000.00

(for cash paid to the accounts payable from whom the

supplied were purchased)

7/31/201

8 Interest on Loan A/c Dr.

$

300.00

To Bank A/c

$

300.00

(for loan charged by the

bank)

7/31/201

8 Advertising A/c Dr.

$

1,600.00

To Bank A/c $

3,600.00

To bank A/c

$

3,600.00

(for insurance paid in cash in advance)

7/9/2018 Supplies A/c Dr.

$

2,400.00

To Accounts Payable

$

2,400.00

(for supplies acquired on credit )

7/13/201

8 Bank A/c Dr.

$

500.00

To Rainbow Child care

Centre

$

500.00

(for amount received for the cleaning services)

7/20/201

8 Wages A/c Dr.

$

1,600.00

To bank A/c

$

1,600.00

(for cash paid to the wages)

7/25/201

8 Bank A/c Dr.

$

5,500.00

To ABC Public School

$

5,500.00

(for cash received from the school for the purpose of cleaning)

7/27/201

8 Accounts Payable A/c Dr.

$

2,000.00

To bank

$

2,000.00

(for cash paid to the accounts payable from whom the

supplied were purchased)

7/31/201

8 Interest on Loan A/c Dr.

$

300.00

To Bank A/c

$

300.00

(for loan charged by the

bank)

7/31/201

8 Advertising A/c Dr.

$

1,600.00

To Bank A/c $

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING PROCESSES AND SYSTEMS 5

1,600.00

(for advertising charges paid thorugh bank account)

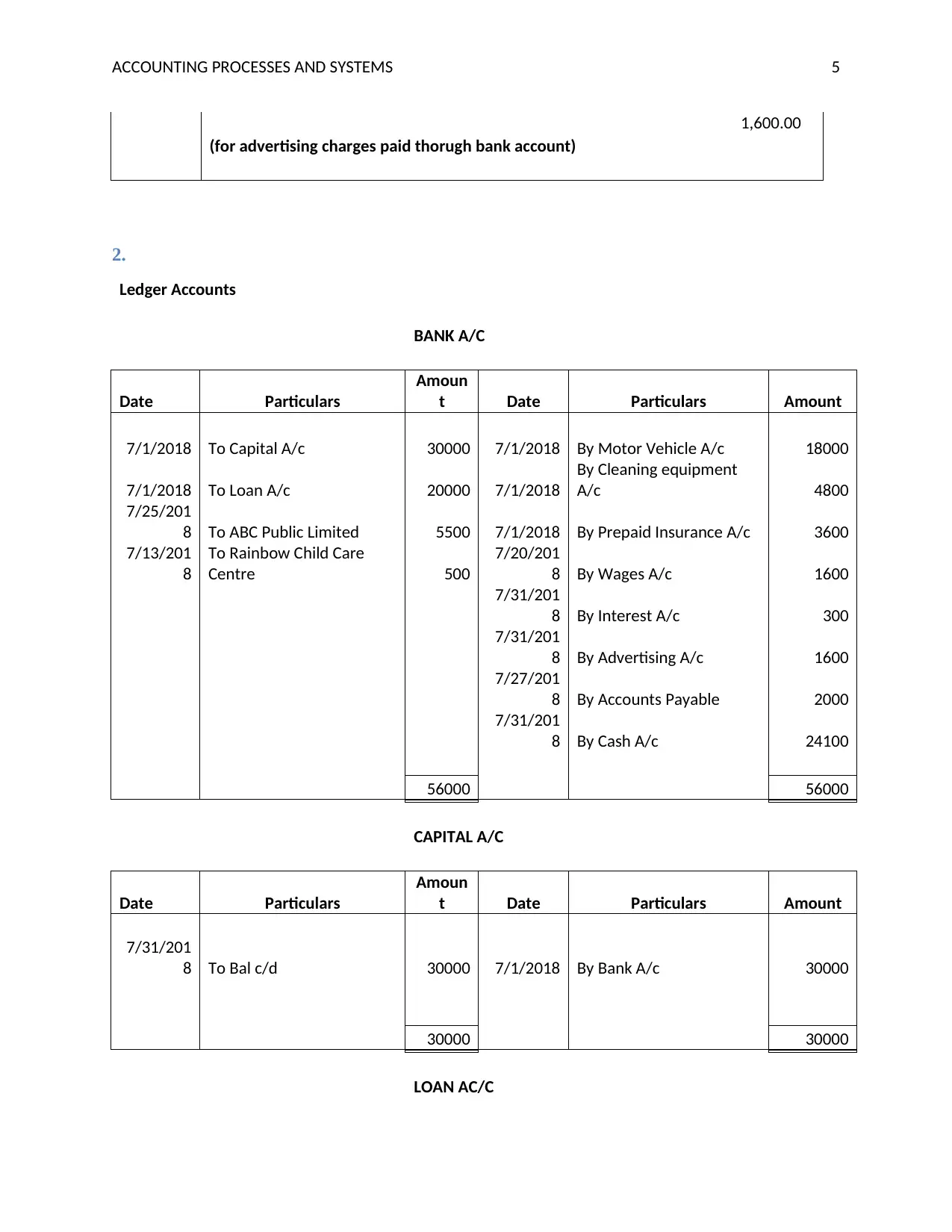

2.

Ledger Accounts

BANK A/C

Date Particulars

Amoun

t Date Particulars Amount

7/1/2018 To Capital A/c 30000 7/1/2018 By Motor Vehicle A/c 18000

7/1/2018 To Loan A/c 20000 7/1/2018

By Cleaning equipment

A/c 4800

7/25/201

8 To ABC Public Limited 5500 7/1/2018 By Prepaid Insurance A/c 3600

7/13/201

8

To Rainbow Child Care

Centre 500

7/20/201

8 By Wages A/c 1600

7/31/201

8 By Interest A/c 300

7/31/201

8 By Advertising A/c 1600

7/27/201

8 By Accounts Payable 2000

7/31/201

8 By Cash A/c 24100

56000 56000

CAPITAL A/C

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bal c/d 30000 7/1/2018 By Bank A/c 30000

30000 30000

LOAN AC/C

1,600.00

(for advertising charges paid thorugh bank account)

2.

Ledger Accounts

BANK A/C

Date Particulars

Amoun

t Date Particulars Amount

7/1/2018 To Capital A/c 30000 7/1/2018 By Motor Vehicle A/c 18000

7/1/2018 To Loan A/c 20000 7/1/2018

By Cleaning equipment

A/c 4800

7/25/201

8 To ABC Public Limited 5500 7/1/2018 By Prepaid Insurance A/c 3600

7/13/201

8

To Rainbow Child Care

Centre 500

7/20/201

8 By Wages A/c 1600

7/31/201

8 By Interest A/c 300

7/31/201

8 By Advertising A/c 1600

7/27/201

8 By Accounts Payable 2000

7/31/201

8 By Cash A/c 24100

56000 56000

CAPITAL A/C

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bal c/d 30000 7/1/2018 By Bank A/c 30000

30000 30000

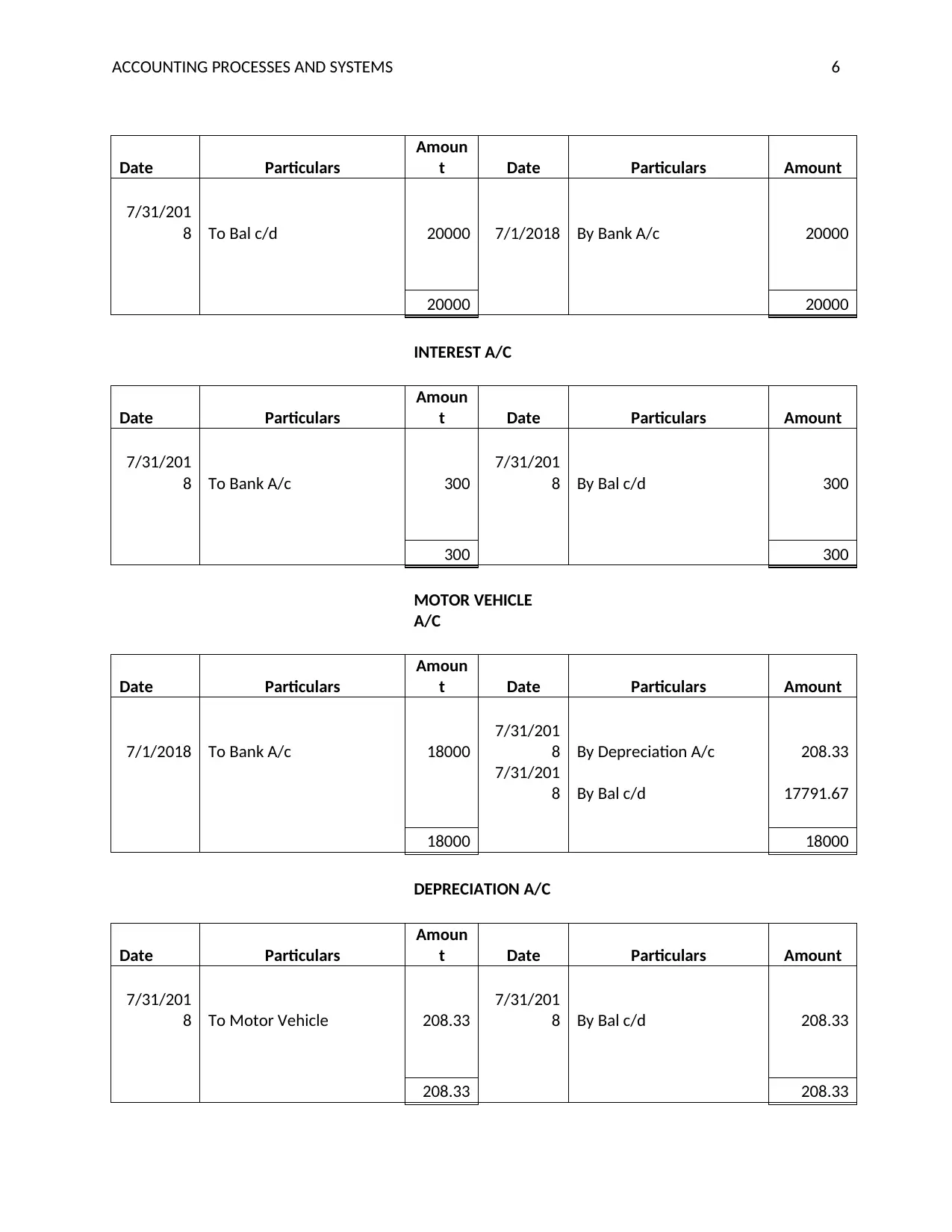

LOAN AC/C

ACCOUNTING PROCESSES AND SYSTEMS 6

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bal c/d 20000 7/1/2018 By Bank A/c 20000

20000 20000

INTEREST A/C

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bank A/c 300

7/31/201

8 By Bal c/d 300

300 300

MOTOR VEHICLE

A/C

Date Particulars

Amoun

t Date Particulars Amount

7/1/2018 To Bank A/c 18000

7/31/201

8 By Depreciation A/c 208.33

7/31/201

8 By Bal c/d 17791.67

18000 18000

DEPRECIATION A/C

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Motor Vehicle 208.33

7/31/201

8 By Bal c/d 208.33

208.33 208.33

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bal c/d 20000 7/1/2018 By Bank A/c 20000

20000 20000

INTEREST A/C

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bank A/c 300

7/31/201

8 By Bal c/d 300

300 300

MOTOR VEHICLE

A/C

Date Particulars

Amoun

t Date Particulars Amount

7/1/2018 To Bank A/c 18000

7/31/201

8 By Depreciation A/c 208.33

7/31/201

8 By Bal c/d 17791.67

18000 18000

DEPRECIATION A/C

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Motor Vehicle 208.33

7/31/201

8 By Bal c/d 208.33

208.33 208.33

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

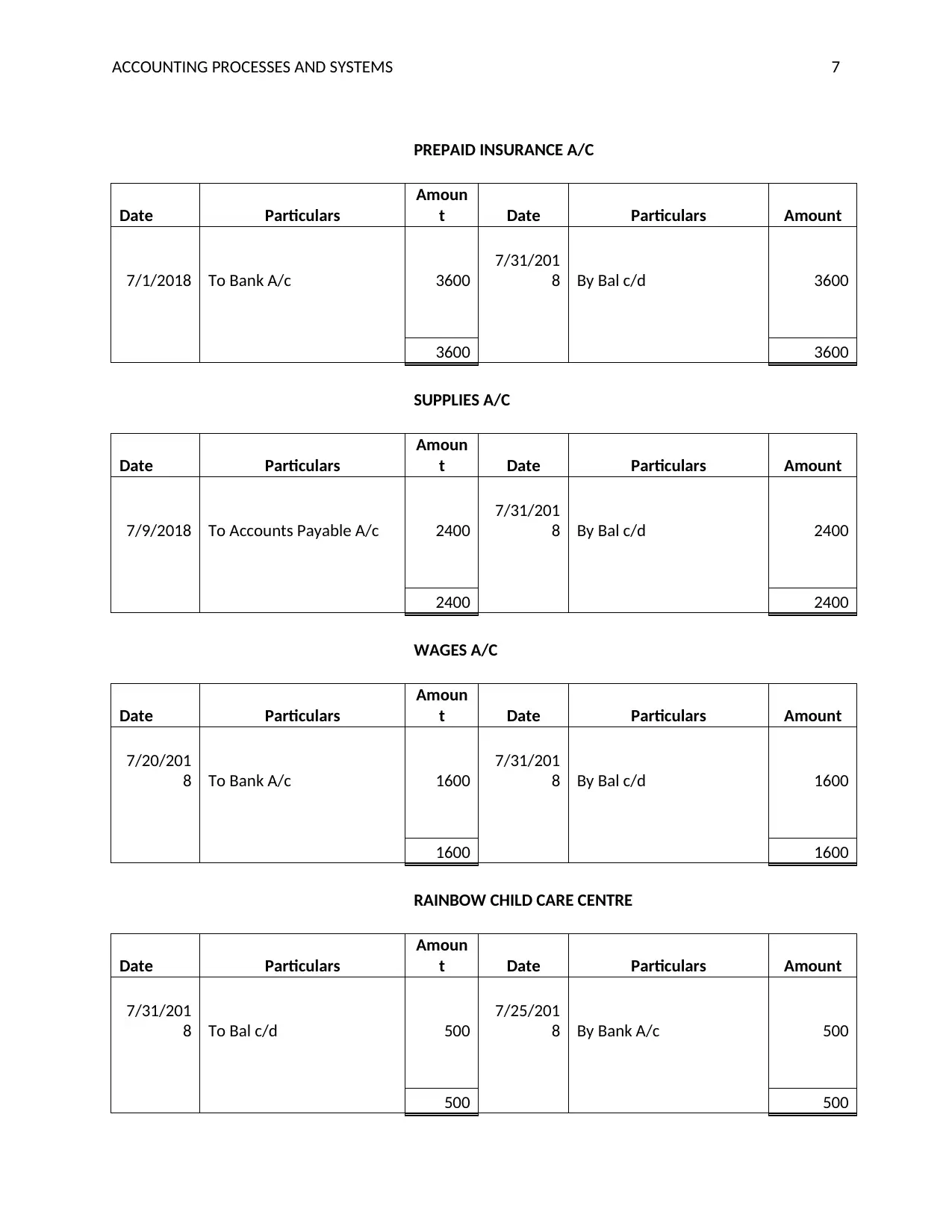

ACCOUNTING PROCESSES AND SYSTEMS 7

PREPAID INSURANCE A/C

Date Particulars

Amoun

t Date Particulars Amount

7/1/2018 To Bank A/c 3600

7/31/201

8 By Bal c/d 3600

3600 3600

SUPPLIES A/C

Date Particulars

Amoun

t Date Particulars Amount

7/9/2018 To Accounts Payable A/c 2400

7/31/201

8 By Bal c/d 2400

2400 2400

WAGES A/C

Date Particulars

Amoun

t Date Particulars Amount

7/20/201

8 To Bank A/c 1600

7/31/201

8 By Bal c/d 1600

1600 1600

RAINBOW CHILD CARE CENTRE

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bal c/d 500

7/25/201

8 By Bank A/c 500

500 500

PREPAID INSURANCE A/C

Date Particulars

Amoun

t Date Particulars Amount

7/1/2018 To Bank A/c 3600

7/31/201

8 By Bal c/d 3600

3600 3600

SUPPLIES A/C

Date Particulars

Amoun

t Date Particulars Amount

7/9/2018 To Accounts Payable A/c 2400

7/31/201

8 By Bal c/d 2400

2400 2400

WAGES A/C

Date Particulars

Amoun

t Date Particulars Amount

7/20/201

8 To Bank A/c 1600

7/31/201

8 By Bal c/d 1600

1600 1600

RAINBOW CHILD CARE CENTRE

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bal c/d 500

7/25/201

8 By Bank A/c 500

500 500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING PROCESSES AND SYSTEMS 8

ABC PUBLIC LIMITED

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bal c/d 5500

7/25/201

8 By Bank A/c 5500

5500 5500

ACCOUNTS PAYABLE A/C

Date Particulars

Amoun

t Date Particulars Amount

7/27/201

8 To Bank A/c 2000 7/9/2018 By Supplies A/c 2400

To Bal C/d 400

2400 2400

INTEREST ON LOAN A/C

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bank A/c 300

7/31/201

8 By interest on Loan A/c 2400

7/31/201

8 To Bal c/d 2100

2400 2400

ADVERTISING A/C

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bank A/c 1600 By Bal c/d 1600

1600 1600

ABC PUBLIC LIMITED

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bal c/d 5500

7/25/201

8 By Bank A/c 5500

5500 5500

ACCOUNTS PAYABLE A/C

Date Particulars

Amoun

t Date Particulars Amount

7/27/201

8 To Bank A/c 2000 7/9/2018 By Supplies A/c 2400

To Bal C/d 400

2400 2400

INTEREST ON LOAN A/C

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bank A/c 300

7/31/201

8 By interest on Loan A/c 2400

7/31/201

8 To Bal c/d 2100

2400 2400

ADVERTISING A/C

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bank A/c 1600 By Bal c/d 1600

1600 1600

ACCOUNTING PROCESSES AND SYSTEMS 9

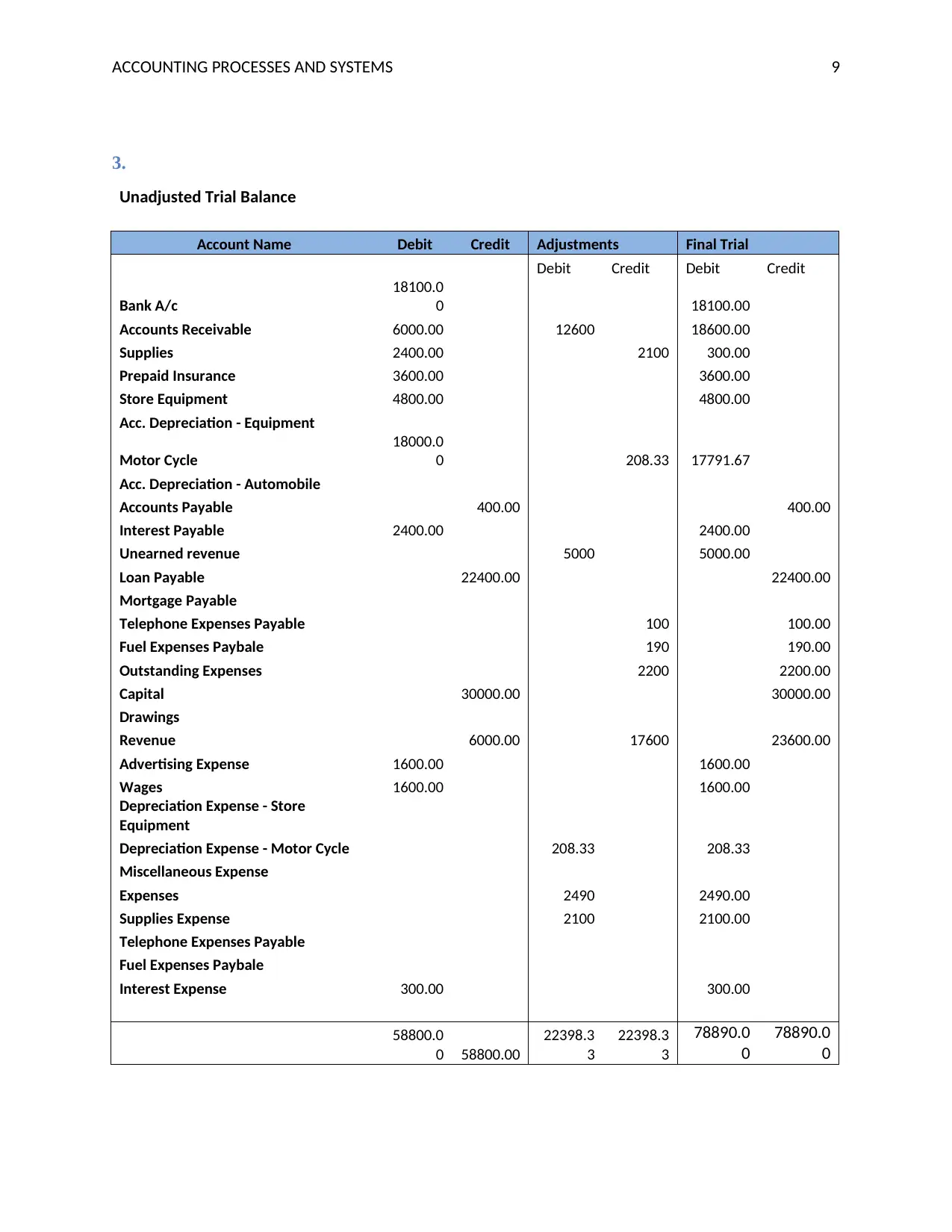

3.

Unadjusted Trial Balance

Account Name Debit Credit Adjustments Final Trial

Debit Credit Debit Credit

Bank A/c

18100.0

0 18100.00

Accounts Receivable 6000.00 12600 18600.00

Supplies 2400.00 2100 300.00

Prepaid Insurance 3600.00 3600.00

Store Equipment 4800.00 4800.00

Acc. Depreciation - Equipment

Motor Cycle

18000.0

0 208.33 17791.67

Acc. Depreciation - Automobile

Accounts Payable 400.00 400.00

Interest Payable 2400.00 2400.00

Unearned revenue 5000 5000.00

Loan Payable 22400.00 22400.00

Mortgage Payable

Telephone Expenses Payable 100 100.00

Fuel Expenses Paybale 190 190.00

Outstanding Expenses 2200 2200.00

Capital 30000.00 30000.00

Drawings

Revenue 6000.00 17600 23600.00

Advertising Expense 1600.00 1600.00

Wages 1600.00 1600.00

Depreciation Expense - Store

Equipment

Depreciation Expense - Motor Cycle 208.33 208.33

Miscellaneous Expense

Expenses 2490 2490.00

Supplies Expense 2100 2100.00

Telephone Expenses Payable

Fuel Expenses Paybale

Interest Expense 300.00 300.00

58800.0

0 58800.00

22398.3

3

22398.3

3

78890.0

0

78890.0

0

3.

Unadjusted Trial Balance

Account Name Debit Credit Adjustments Final Trial

Debit Credit Debit Credit

Bank A/c

18100.0

0 18100.00

Accounts Receivable 6000.00 12600 18600.00

Supplies 2400.00 2100 300.00

Prepaid Insurance 3600.00 3600.00

Store Equipment 4800.00 4800.00

Acc. Depreciation - Equipment

Motor Cycle

18000.0

0 208.33 17791.67

Acc. Depreciation - Automobile

Accounts Payable 400.00 400.00

Interest Payable 2400.00 2400.00

Unearned revenue 5000 5000.00

Loan Payable 22400.00 22400.00

Mortgage Payable

Telephone Expenses Payable 100 100.00

Fuel Expenses Paybale 190 190.00

Outstanding Expenses 2200 2200.00

Capital 30000.00 30000.00

Drawings

Revenue 6000.00 17600 23600.00

Advertising Expense 1600.00 1600.00

Wages 1600.00 1600.00

Depreciation Expense - Store

Equipment

Depreciation Expense - Motor Cycle 208.33 208.33

Miscellaneous Expense

Expenses 2490 2490.00

Supplies Expense 2100 2100.00

Telephone Expenses Payable

Fuel Expenses Paybale

Interest Expense 300.00 300.00

58800.0

0 58800.00

22398.3

3

22398.3

3

78890.0

0

78890.0

0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING PROCESSES AND SYSTEMS 10

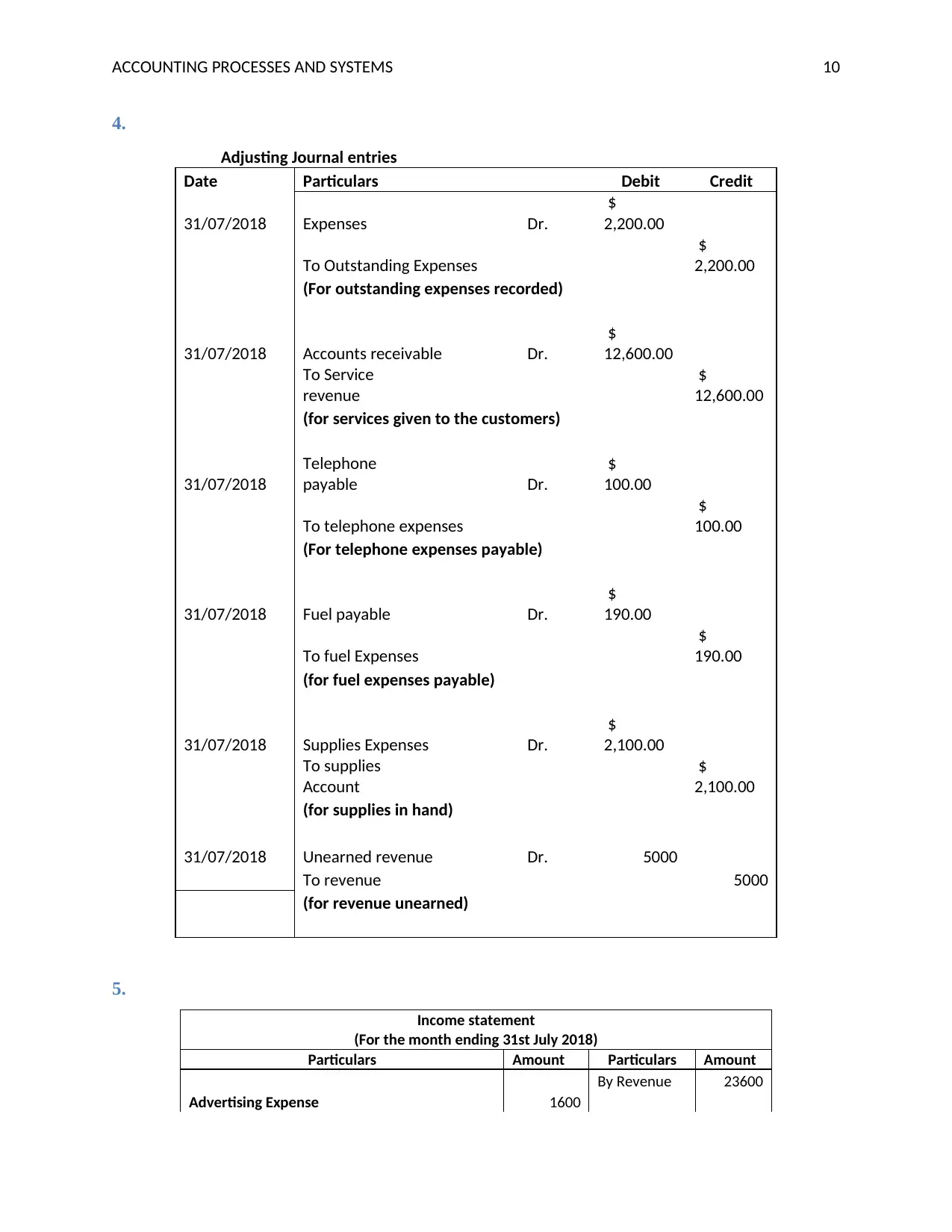

4.

Adjusting Journal entries

Date Particulars Debit Credit

31/07/2018 Expenses Dr.

$

2,200.00

To Outstanding Expenses

$

2,200.00

(For outstanding expenses recorded)

31/07/2018 Accounts receivable Dr.

$

12,600.00

To Service

revenue

$

12,600.00

(for services given to the customers)

31/07/2018

Telephone

payable Dr.

$

100.00

To telephone expenses

$

100.00

(For telephone expenses payable)

31/07/2018 Fuel payable Dr.

$

190.00

To fuel Expenses

$

190.00

(for fuel expenses payable)

31/07/2018 Supplies Expenses Dr.

$

2,100.00

To supplies

Account

$

2,100.00

(for supplies in hand)

31/07/2018 Unearned revenue Dr. 5000

To revenue 5000

(for revenue unearned)

5.

Income statement

(For the month ending 31st July 2018)

Particulars Amount Particulars Amount

By Revenue 23600

Advertising Expense 1600

4.

Adjusting Journal entries

Date Particulars Debit Credit

31/07/2018 Expenses Dr.

$

2,200.00

To Outstanding Expenses

$

2,200.00

(For outstanding expenses recorded)

31/07/2018 Accounts receivable Dr.

$

12,600.00

To Service

revenue

$

12,600.00

(for services given to the customers)

31/07/2018

Telephone

payable Dr.

$

100.00

To telephone expenses

$

100.00

(For telephone expenses payable)

31/07/2018 Fuel payable Dr.

$

190.00

To fuel Expenses

$

190.00

(for fuel expenses payable)

31/07/2018 Supplies Expenses Dr.

$

2,100.00

To supplies

Account

$

2,100.00

(for supplies in hand)

31/07/2018 Unearned revenue Dr. 5000

To revenue 5000

(for revenue unearned)

5.

Income statement

(For the month ending 31st July 2018)

Particulars Amount Particulars Amount

By Revenue 23600

Advertising Expense 1600

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING PROCESSES AND SYSTEMS 11

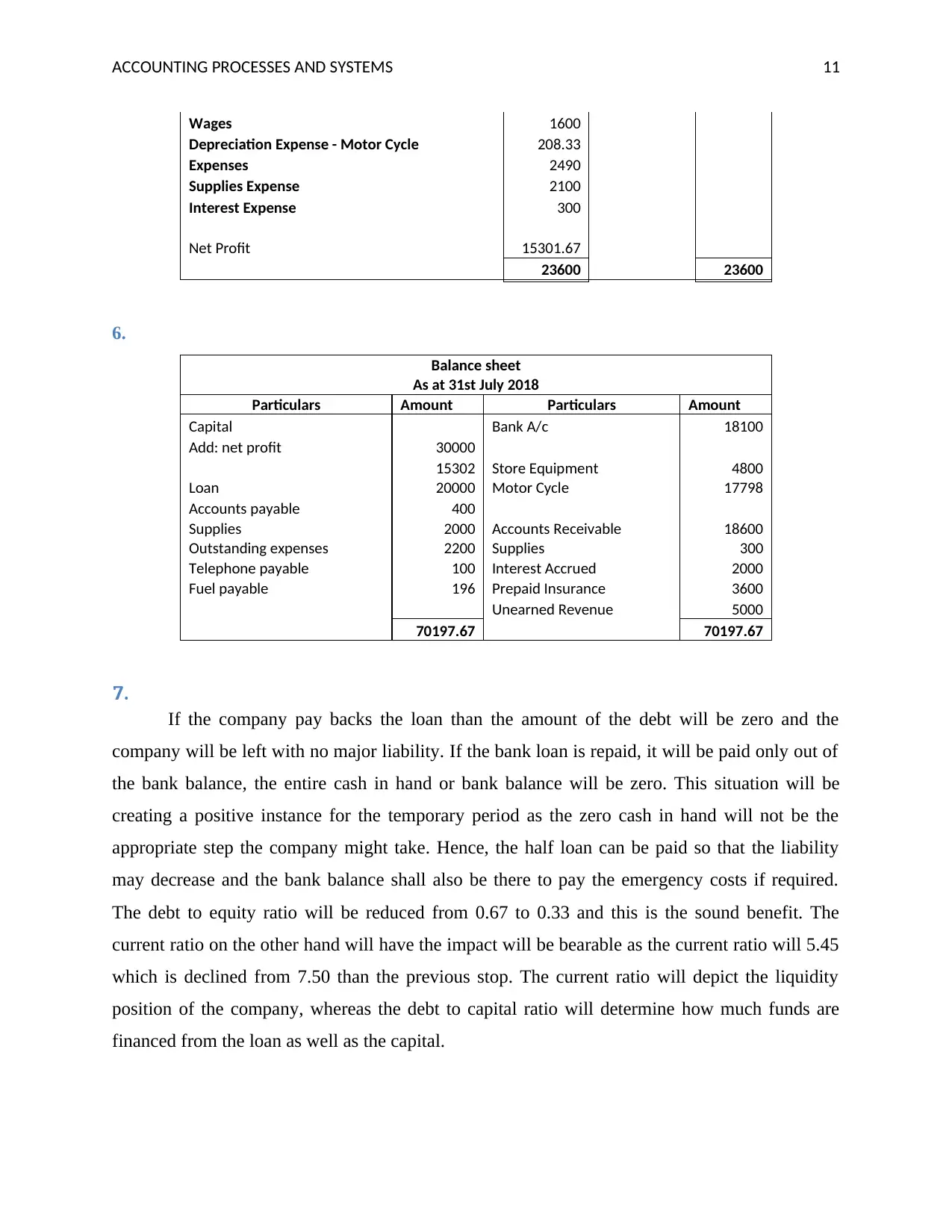

Wages 1600

Depreciation Expense - Motor Cycle 208.33

Expenses 2490

Supplies Expense 2100

Interest Expense 300

Net Profit 15301.67

23600 23600

6.

Balance sheet

As at 31st July 2018

Particulars Amount Particulars Amount

Capital Bank A/c 18100

Add: net profit 30000

15302 Store Equipment 4800

Loan 20000 Motor Cycle 17798

Accounts payable 400

Supplies 2000 Accounts Receivable 18600

Outstanding expenses 2200 Supplies 300

Telephone payable 100 Interest Accrued 2000

Fuel payable 196 Prepaid Insurance 3600

Unearned Revenue 5000

70197.67 70197.67

7.

If the company pay backs the loan than the amount of the debt will be zero and the

company will be left with no major liability. If the bank loan is repaid, it will be paid only out of

the bank balance, the entire cash in hand or bank balance will be zero. This situation will be

creating a positive instance for the temporary period as the zero cash in hand will not be the

appropriate step the company might take. Hence, the half loan can be paid so that the liability

may decrease and the bank balance shall also be there to pay the emergency costs if required.

The debt to equity ratio will be reduced from 0.67 to 0.33 and this is the sound benefit. The

current ratio on the other hand will have the impact will be bearable as the current ratio will 5.45

which is declined from 7.50 than the previous stop. The current ratio will depict the liquidity

position of the company, whereas the debt to capital ratio will determine how much funds are

financed from the loan as well as the capital.

Wages 1600

Depreciation Expense - Motor Cycle 208.33

Expenses 2490

Supplies Expense 2100

Interest Expense 300

Net Profit 15301.67

23600 23600

6.

Balance sheet

As at 31st July 2018

Particulars Amount Particulars Amount

Capital Bank A/c 18100

Add: net profit 30000

15302 Store Equipment 4800

Loan 20000 Motor Cycle 17798

Accounts payable 400

Supplies 2000 Accounts Receivable 18600

Outstanding expenses 2200 Supplies 300

Telephone payable 100 Interest Accrued 2000

Fuel payable 196 Prepaid Insurance 3600

Unearned Revenue 5000

70197.67 70197.67

7.

If the company pay backs the loan than the amount of the debt will be zero and the

company will be left with no major liability. If the bank loan is repaid, it will be paid only out of

the bank balance, the entire cash in hand or bank balance will be zero. This situation will be

creating a positive instance for the temporary period as the zero cash in hand will not be the

appropriate step the company might take. Hence, the half loan can be paid so that the liability

may decrease and the bank balance shall also be there to pay the emergency costs if required.

The debt to equity ratio will be reduced from 0.67 to 0.33 and this is the sound benefit. The

current ratio on the other hand will have the impact will be bearable as the current ratio will 5.45

which is declined from 7.50 than the previous stop. The current ratio will depict the liquidity

position of the company, whereas the debt to capital ratio will determine how much funds are

financed from the loan as well as the capital.

ACCOUNTING PROCESSES AND SYSTEMS 12

Question 2

Double entry bookkeeping is said to be a concept that is applicable and followed in all the

transactions in the account. According to this concept, all the accounting transactions have two

effects on the financial aspects of the business. The general ledger is used to record the two sides

of every transaction takes in an organization. It a business vends its services or products, the

revenue of the company increases and cash also increased by the same amount. The time a

business borrows some funds from its creditor, the cash balance of the company increased

however the debt balance of the business also increases with the same amount (Walshaw, 2018).

The system of double-entry results in creating a balance sheet comprised of equity,

liabilities, and assets. The sheet is said to be balanced since the assets of the company always

remain equal to liabilities plus equity. Assets of the company are comprised of a list of items

such as machinery, inventory, cash and intangible assets like patents. Liabilities of the company

highlights all the items that business owns to someone else, like long-term notes payable and

short term accounts payable. Equity highlights the stake of the owner in the business. Equity can

also be the owner's contribution to the business, plus profits or minus losses of the company.

Every entry possesses a credit side and a debit side that is recorded by the accountant of the

company in the general ledger (Bragg, 2011).

The double entry system book was first presented by Fra Luca Pacioli and Leonardo da

Vinci the Italian mathematicians. The book was published in the year 1994, with the title

“Summa de arithmetical, geometric, proportion et proportionality”. da Vinci and Pacioli do not

call themselves the inventors of this system but have discovered the way concepts can be utilized

in an effective and planned manner.

Da Vinci is responsible for drawing the practical examples and Pacioli is responsible for

writing text in order to assist in understanding the book. The book was separated into the diverse

segment and the part that illustrates double entry system was titled with the name “Particularis de

computis et scripturis”. The book was further separated into different small sections or chapters

that recite about trial balance, income statement, double entry, balance sheet, journals, and

different techniques and tools successively accepted by a number of traders and accountants.

Question 2

Double entry bookkeeping is said to be a concept that is applicable and followed in all the

transactions in the account. According to this concept, all the accounting transactions have two

effects on the financial aspects of the business. The general ledger is used to record the two sides

of every transaction takes in an organization. It a business vends its services or products, the

revenue of the company increases and cash also increased by the same amount. The time a

business borrows some funds from its creditor, the cash balance of the company increased

however the debt balance of the business also increases with the same amount (Walshaw, 2018).

The system of double-entry results in creating a balance sheet comprised of equity,

liabilities, and assets. The sheet is said to be balanced since the assets of the company always

remain equal to liabilities plus equity. Assets of the company are comprised of a list of items

such as machinery, inventory, cash and intangible assets like patents. Liabilities of the company

highlights all the items that business owns to someone else, like long-term notes payable and

short term accounts payable. Equity highlights the stake of the owner in the business. Equity can

also be the owner's contribution to the business, plus profits or minus losses of the company.

Every entry possesses a credit side and a debit side that is recorded by the accountant of the

company in the general ledger (Bragg, 2011).

The double entry system book was first presented by Fra Luca Pacioli and Leonardo da

Vinci the Italian mathematicians. The book was published in the year 1994, with the title

“Summa de arithmetical, geometric, proportion et proportionality”. da Vinci and Pacioli do not

call themselves the inventors of this system but have discovered the way concepts can be utilized

in an effective and planned manner.

Da Vinci is responsible for drawing the practical examples and Pacioli is responsible for

writing text in order to assist in understanding the book. The book was separated into the diverse

segment and the part that illustrates double entry system was titled with the name “Particularis de

computis et scripturis”. The book was further separated into different small sections or chapters

that recite about trial balance, income statement, double entry, balance sheet, journals, and

different techniques and tools successively accepted by a number of traders and accountants.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.