ACC00724 Accounting for Managers Assignment Solution: Profit Analysis

VerifiedAdded on 2023/04/23

|12

|1503

|386

Homework Assignment

AI Summary

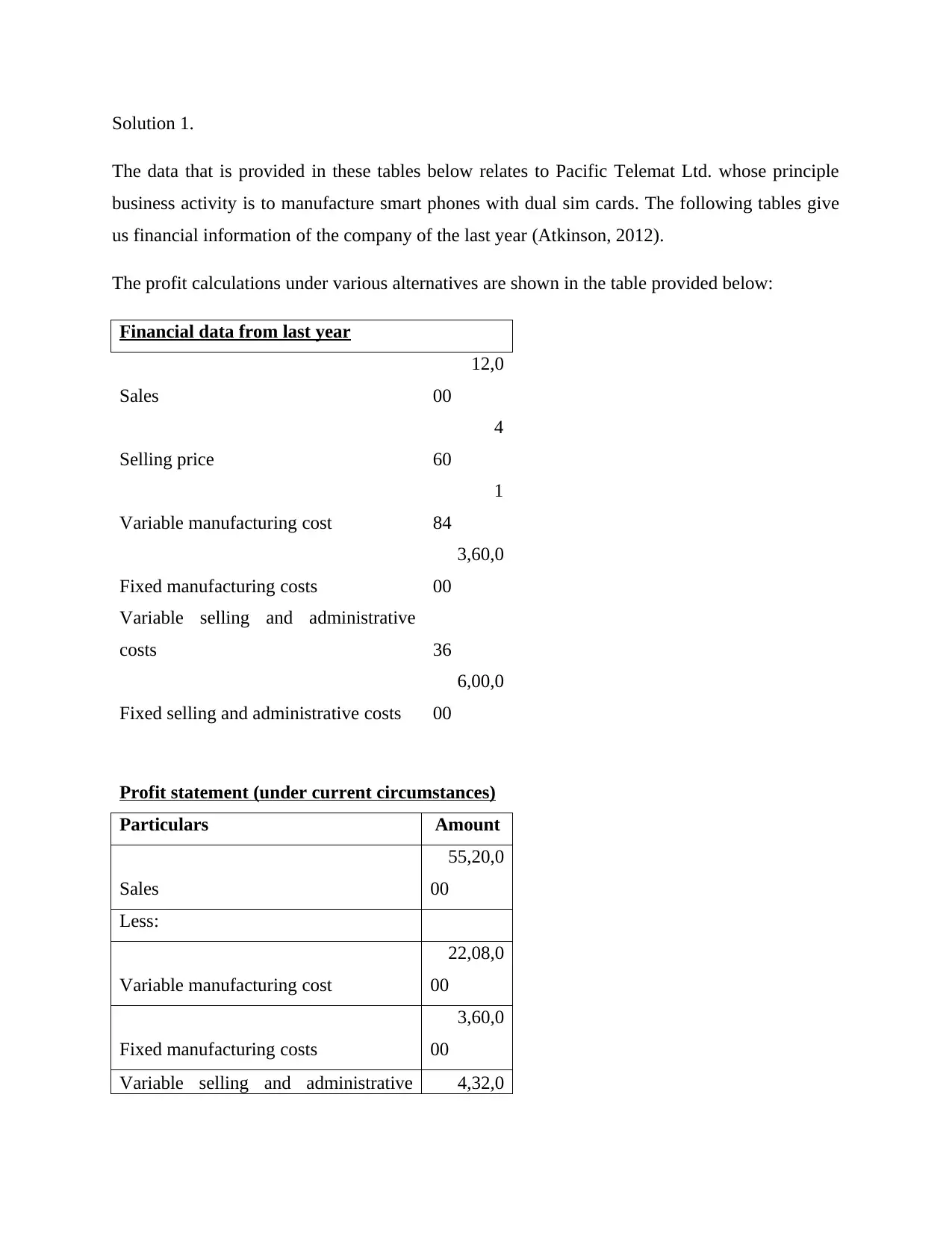

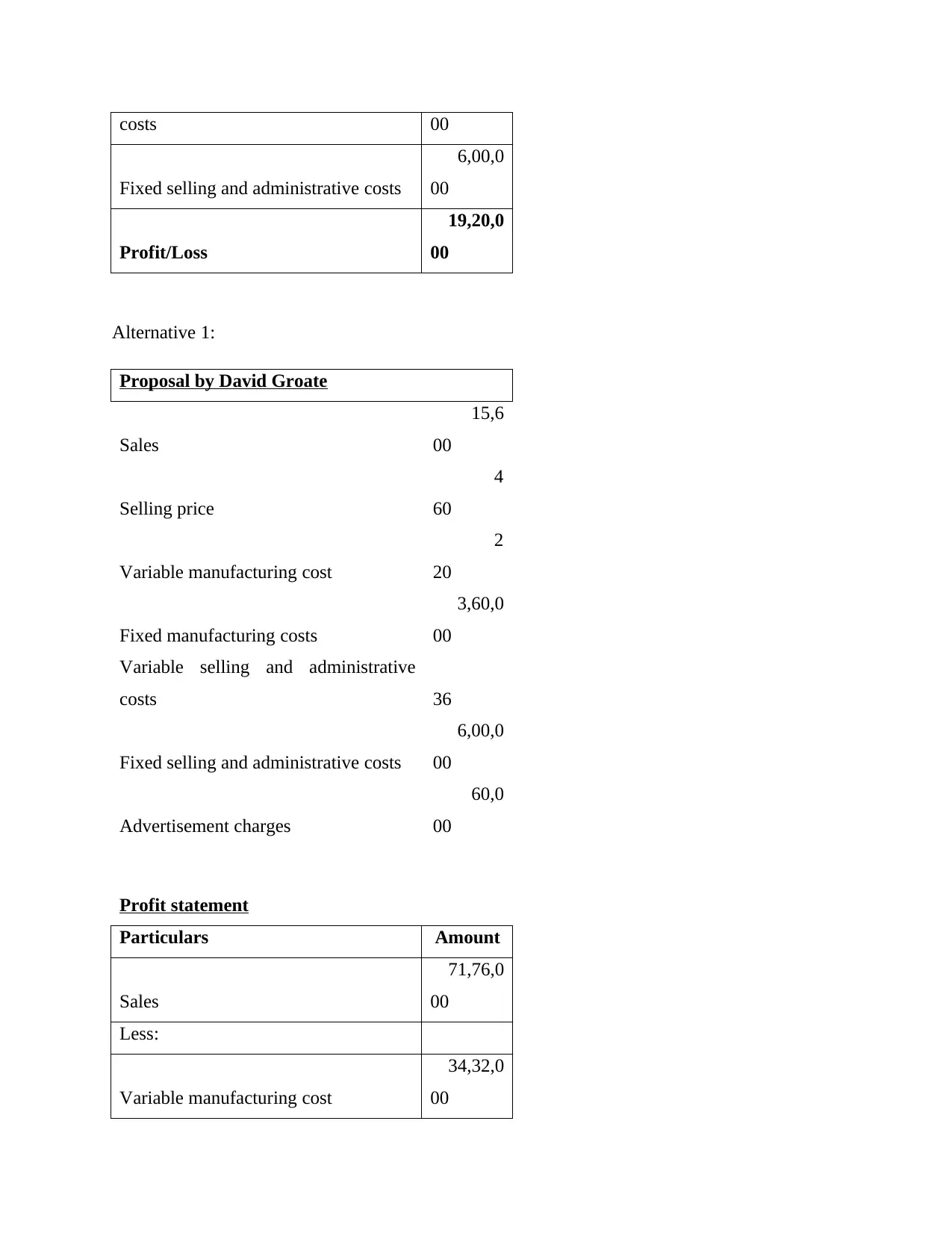

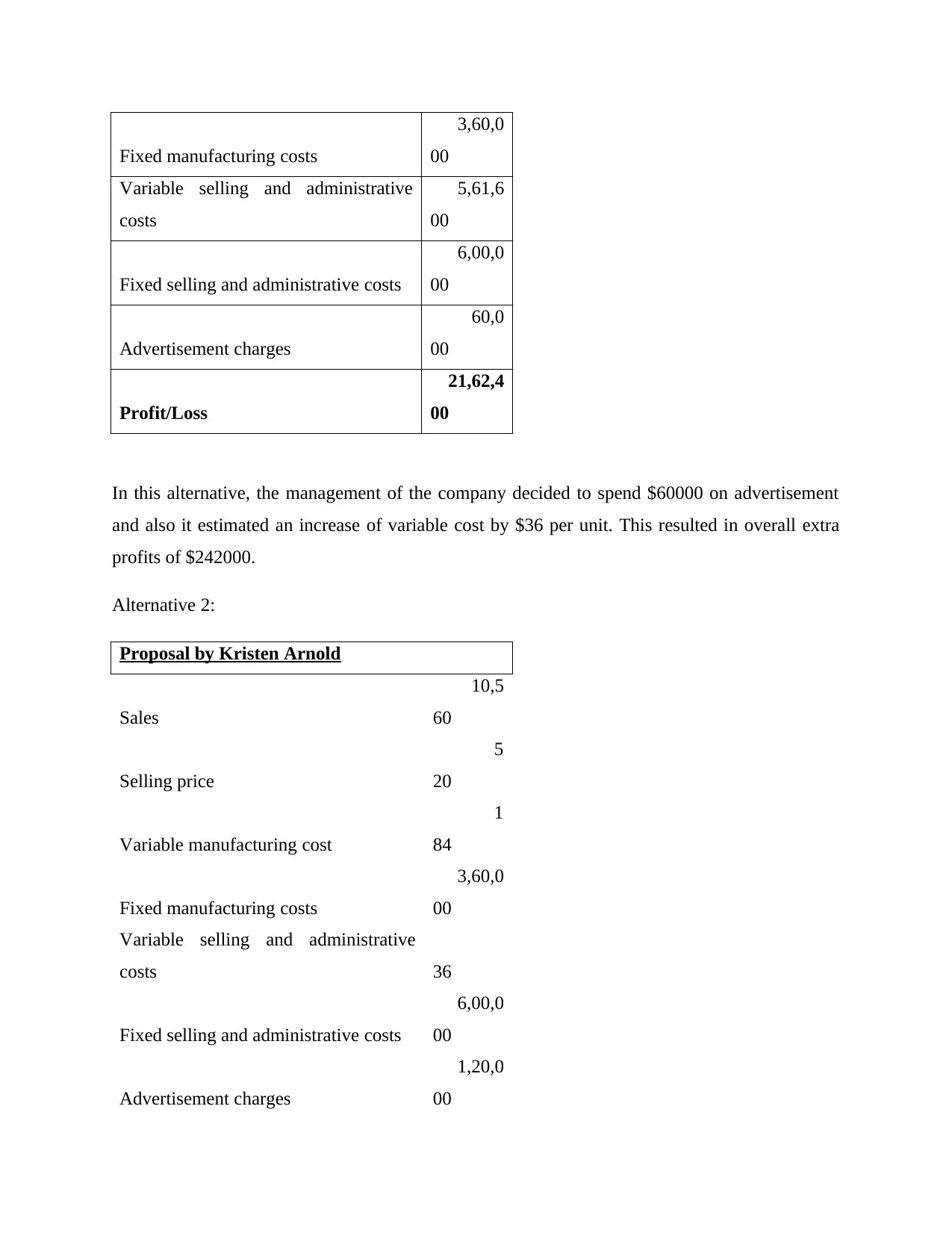

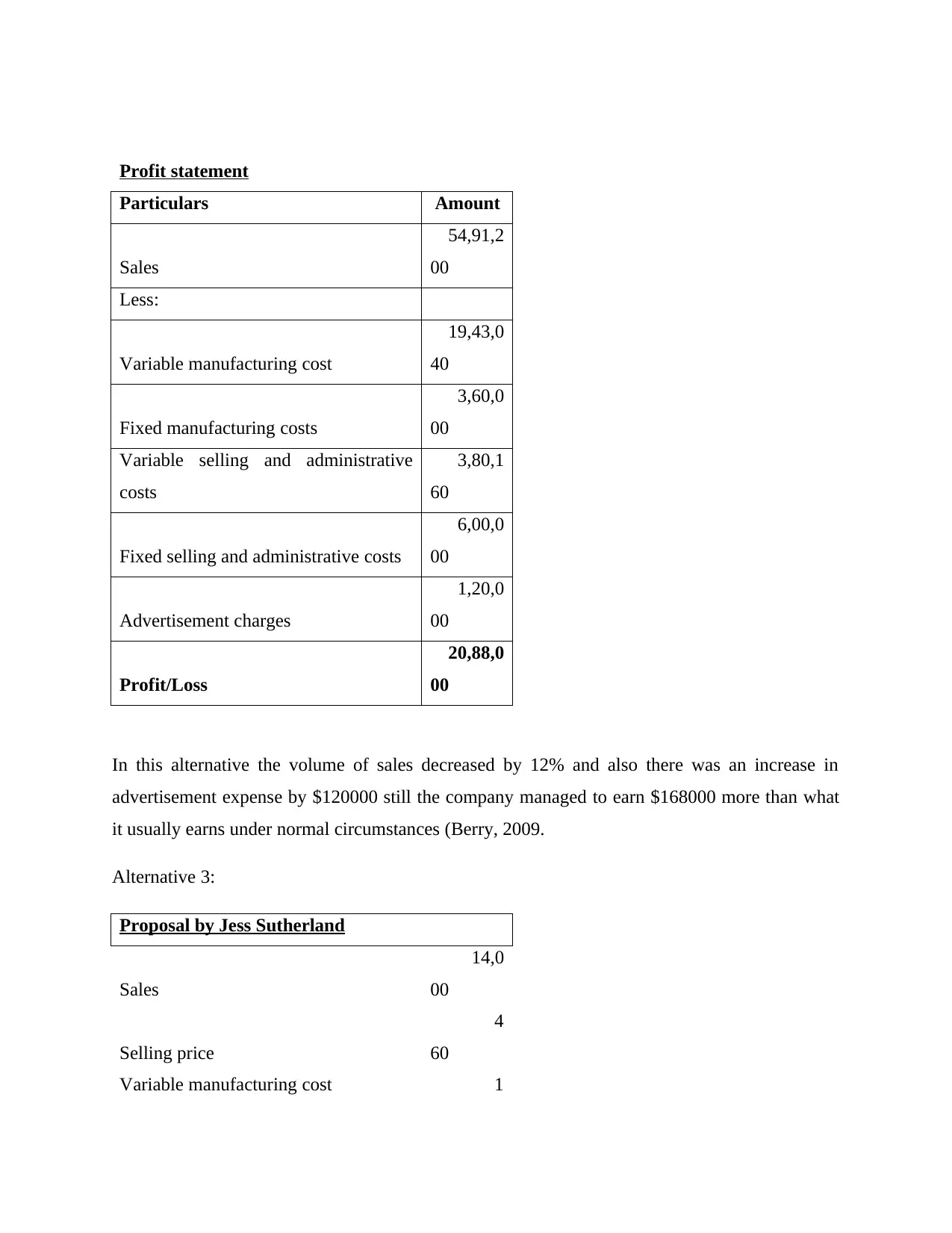

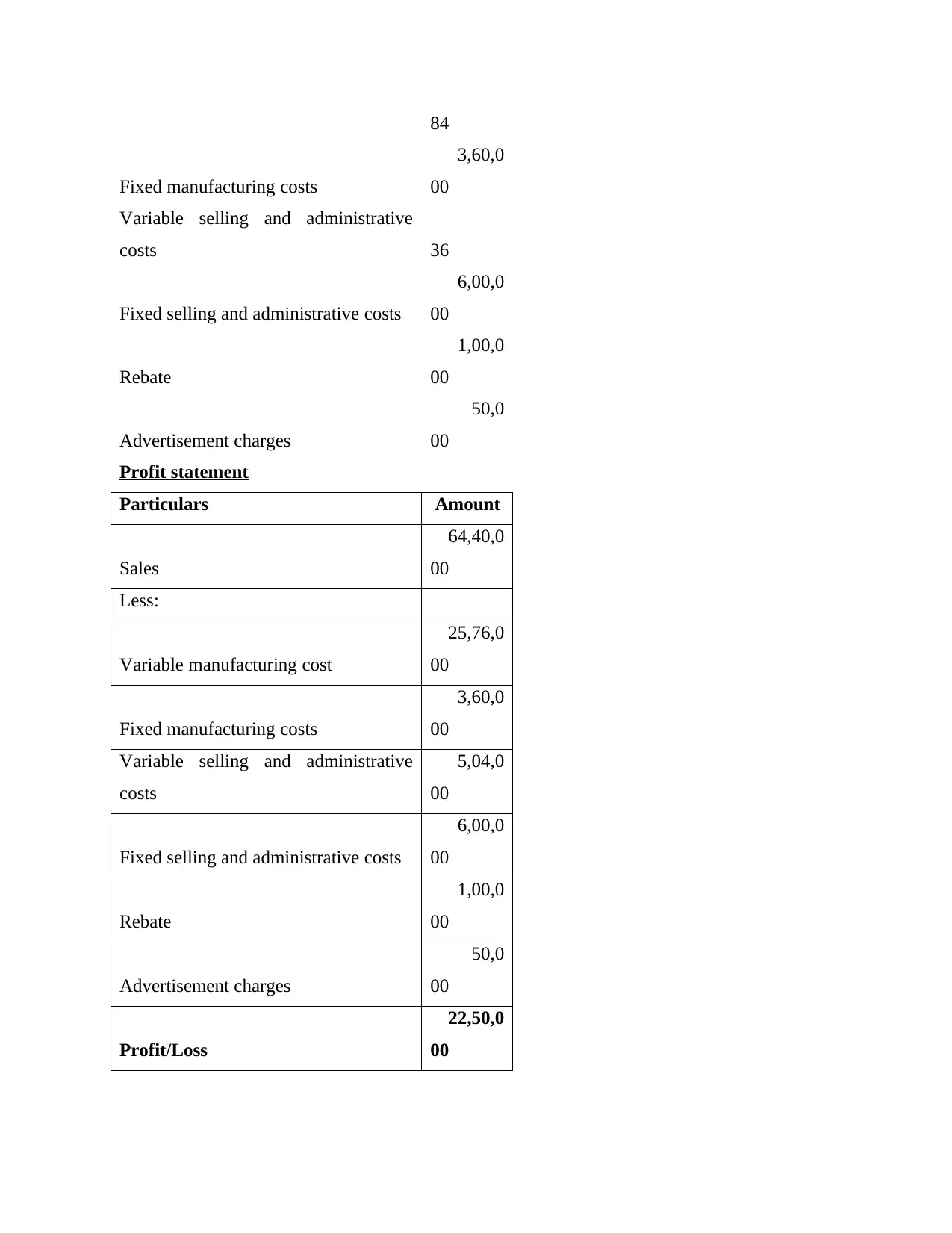

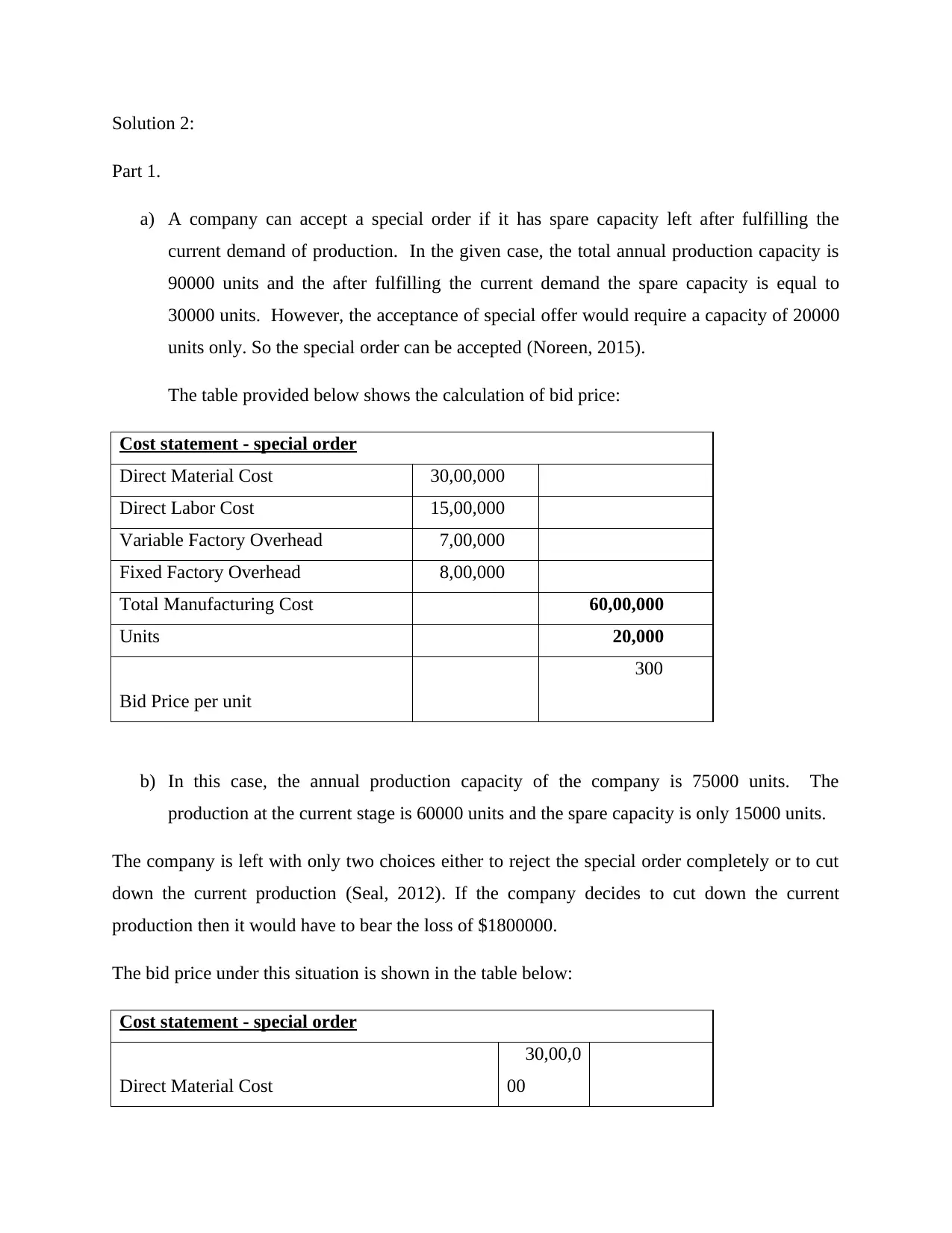

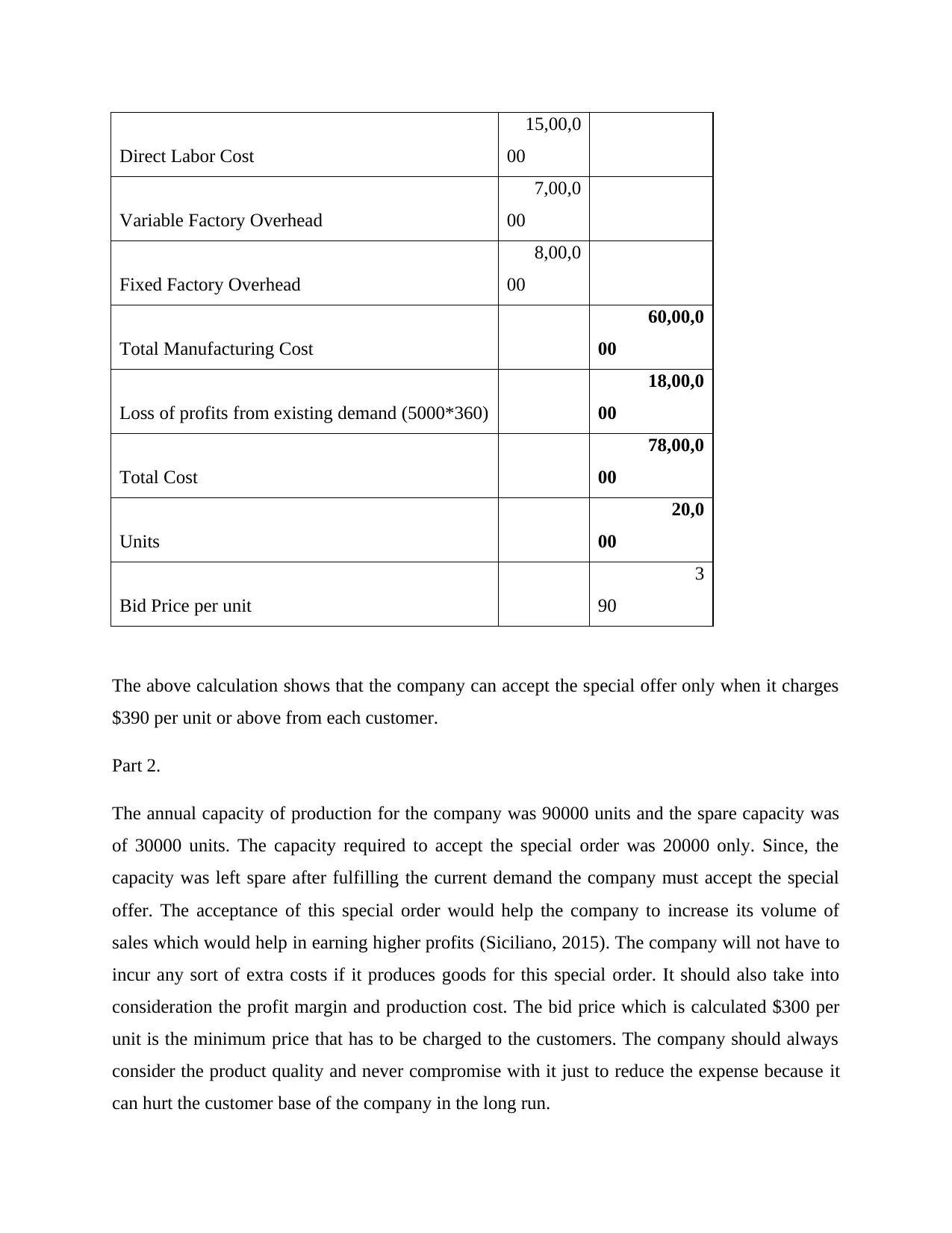

This assignment solution analyzes the financial data of Pacific Telemat Ltd., a company manufacturing smartphones. It presents profit calculations under various scenarios proposed by different managers, including advertising campaigns, increased variable costs, and rebates. The solution explores the implications of these alternatives on profitability, considering both quantitative and qualitative factors. It also includes an analysis of a special order, determining bid prices based on spare capacity and potential losses. Furthermore, the solution reflects on the importance of management accounting in decision-making and the impact of financial choices on a company's success. The document is completed with Harvard referencing style.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.