Accounting Report: A Comprehensive Analysis of Profitability Options

VerifiedAdded on 2023/06/15

|8

|1125

|409

Report

AI Summary

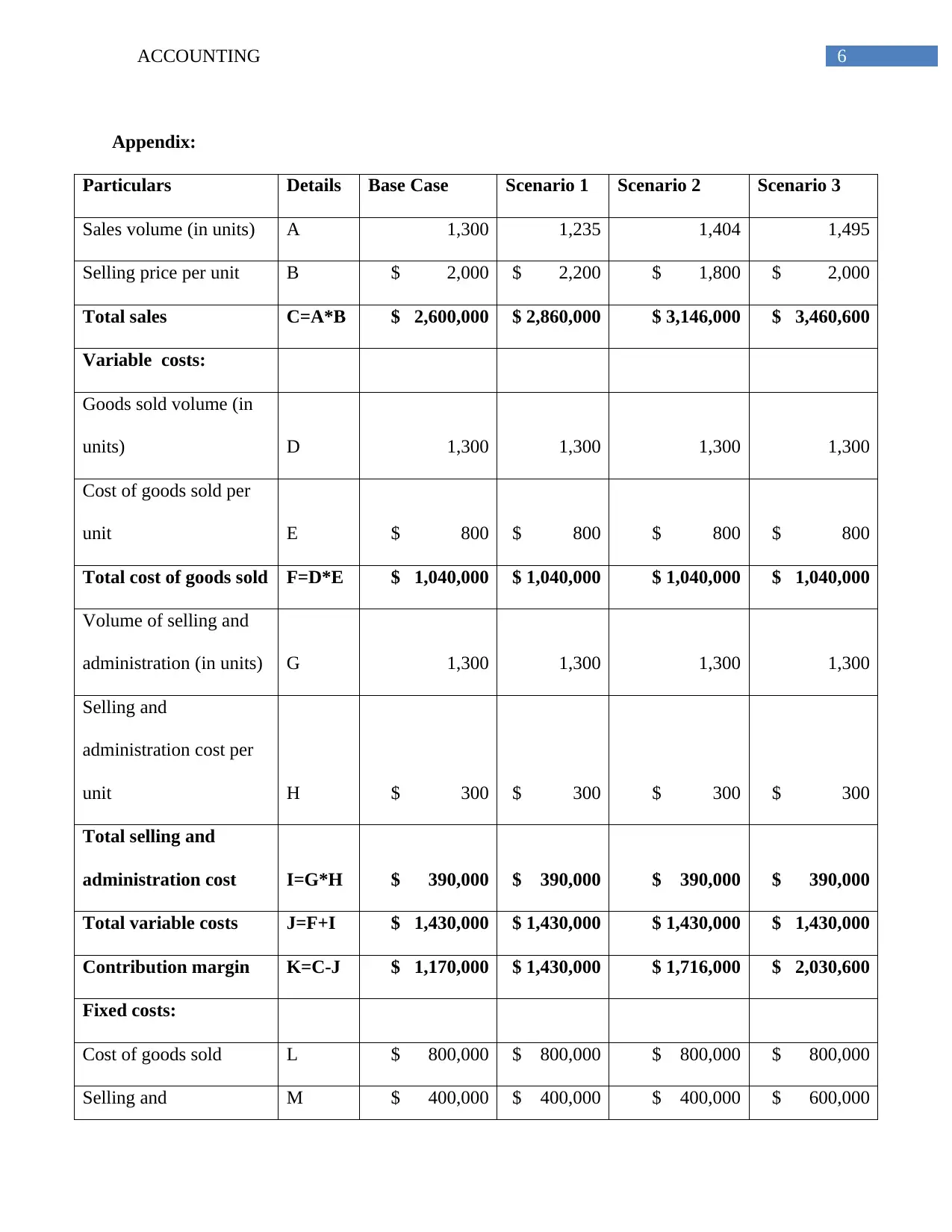

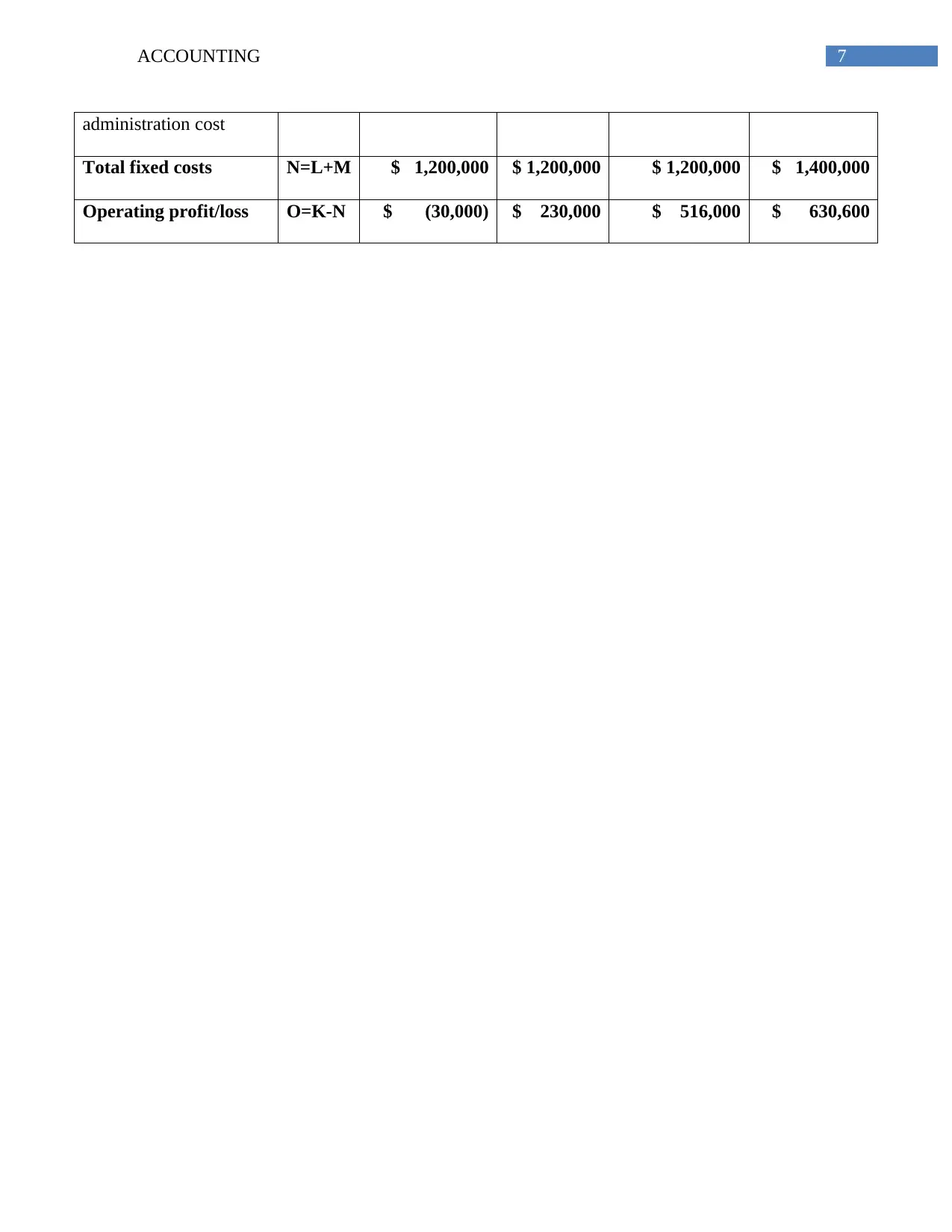

This accounting report evaluates three options for Performance Sports to improve its profitability. Option 1 involves increasing the selling price by 10%, which would minimize the sales volume by 5%, resulting in an operating income of $230,000. Option 2 suggests reducing the selling price by 10%, expecting an 8% rise in sales volume, leading to an operating income of $516,000. Option 3 proposes increasing advertising costs by $200,000, anticipating a 15% increase in sales volume and an operating income of $630,600. The report discusses the advantages and disadvantages of each option, ultimately suggesting that option 2 is the most feasible investment despite option 3's potential for higher operating income. It also includes a detailed table presenting the projected operating profit/loss for each option, with option 3 being accepted due to its potential to significantly improve business operations through increased profit levels.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.