University Corporate Accounting Project Report Analysis

VerifiedAdded on 2023/06/10

|7

|830

|124

Project

AI Summary

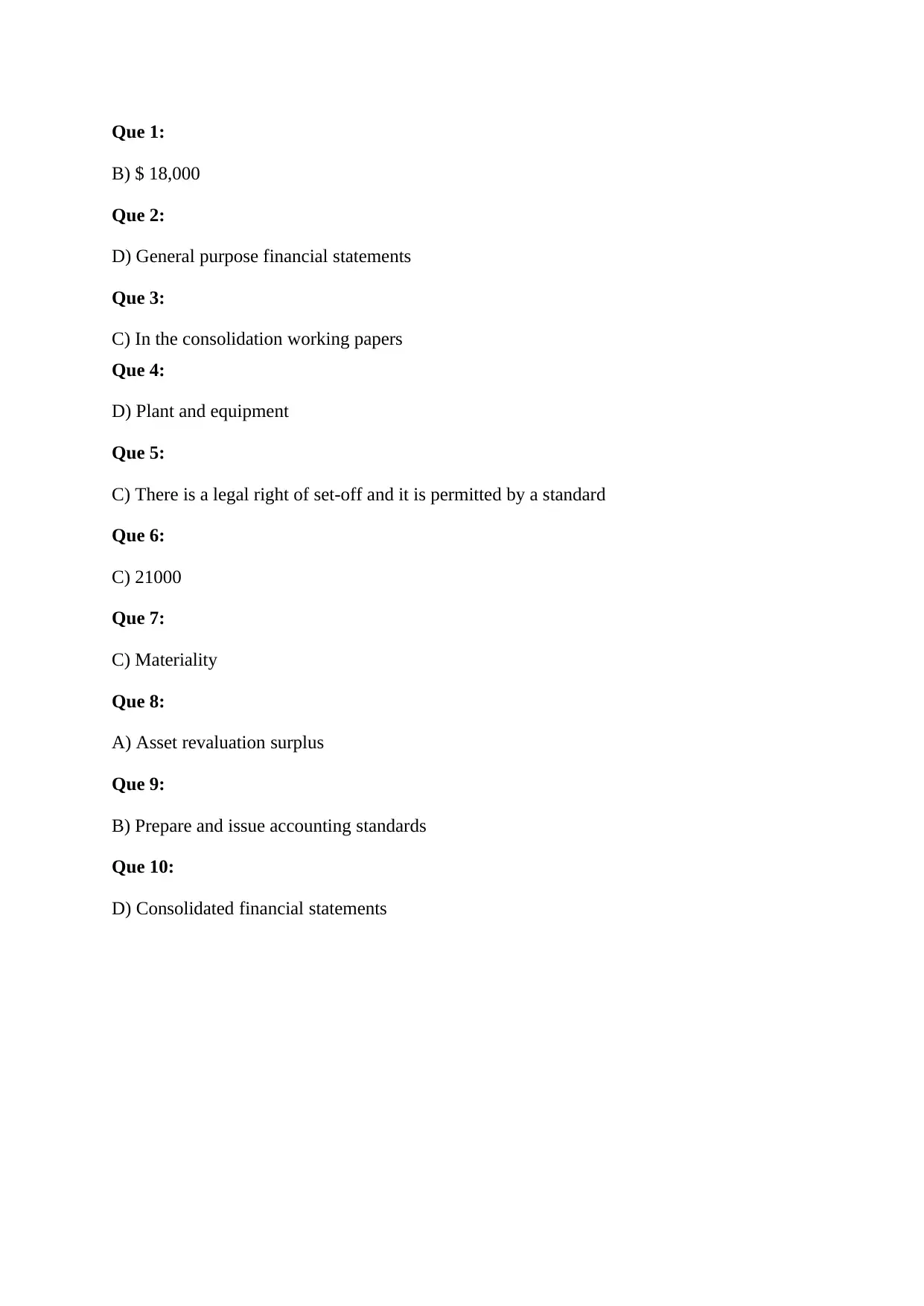

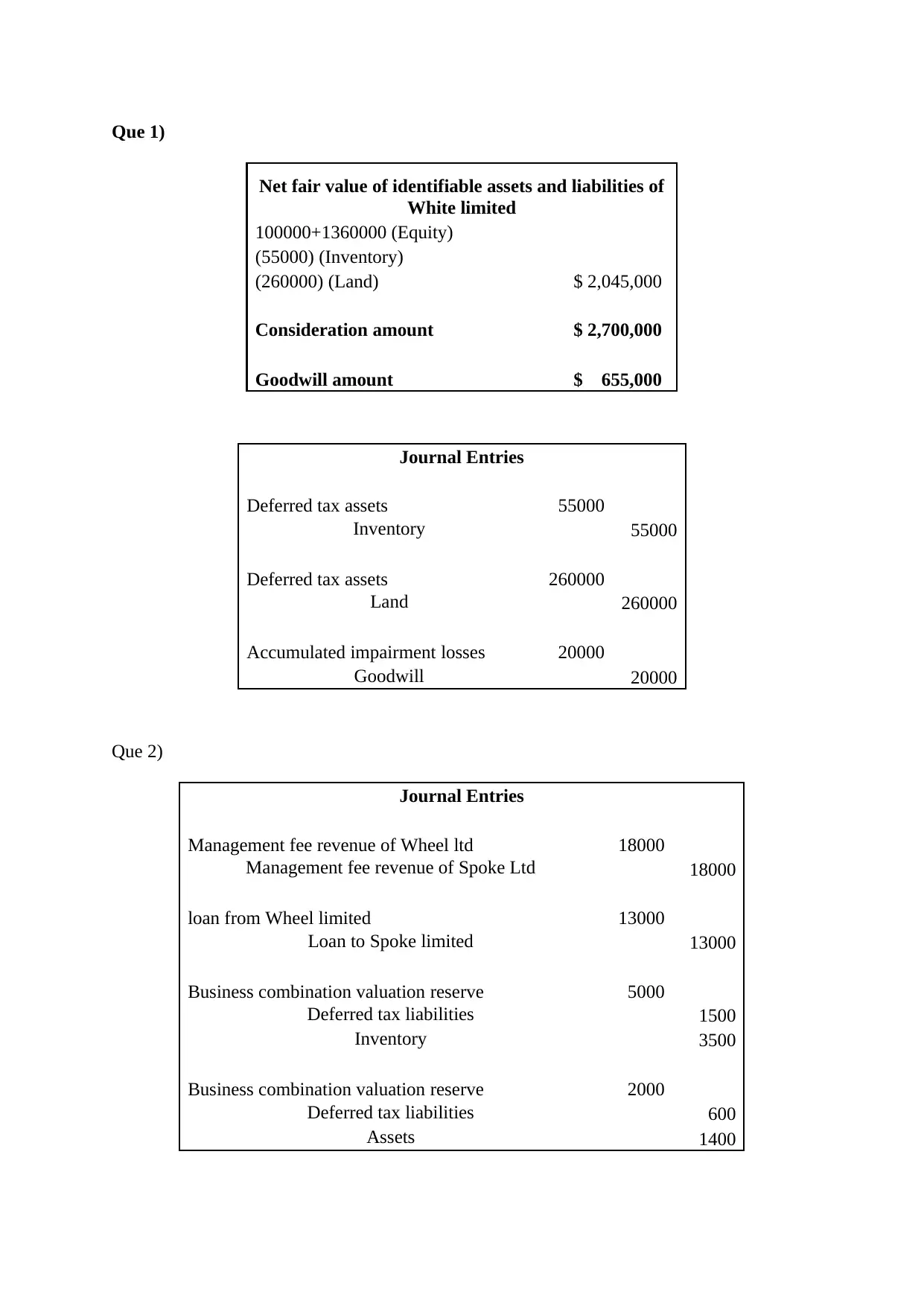

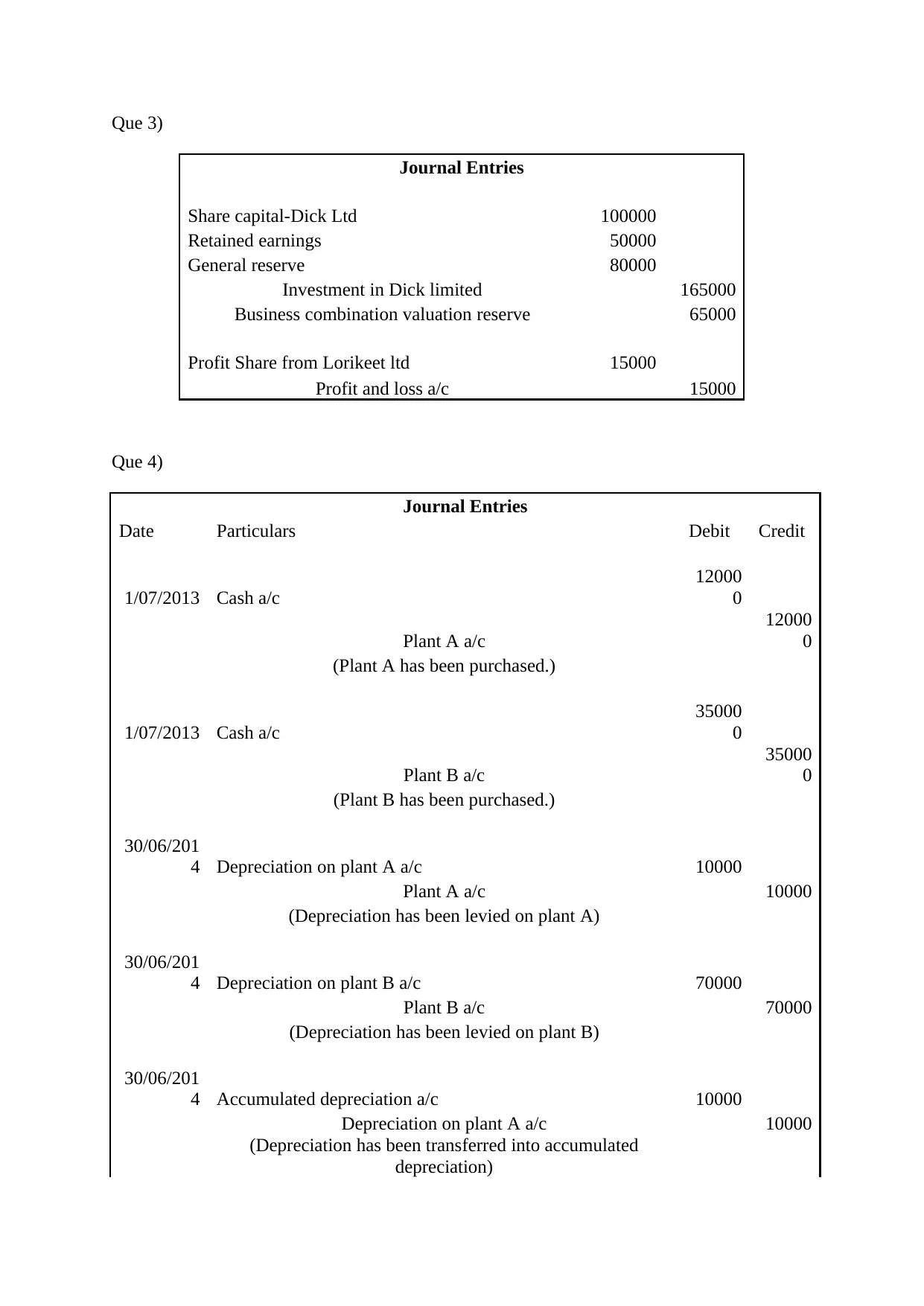

This project report provides solutions to a corporate accounting assignment, covering multiple-choice questions and in-depth problem-solving. The assignment addresses topics such as investment valuation using the equity method, the preparation of general-purpose financial statements, and the recording of consolidation worksheet entries. It also includes detailed journal entries for business combinations, asset purchases, and depreciation calculations. Furthermore, the report explores different types of liquidation, unrealized profits, and residual value, providing definitions and explanations with relevant references. The solutions demonstrate a comprehensive understanding of corporate accounting principles and their practical application.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.