Detailed Analysis of Accounting for Property, Plant & Equipment

VerifiedAdded on 2021/04/16

|15

|732

|78

Report

AI Summary

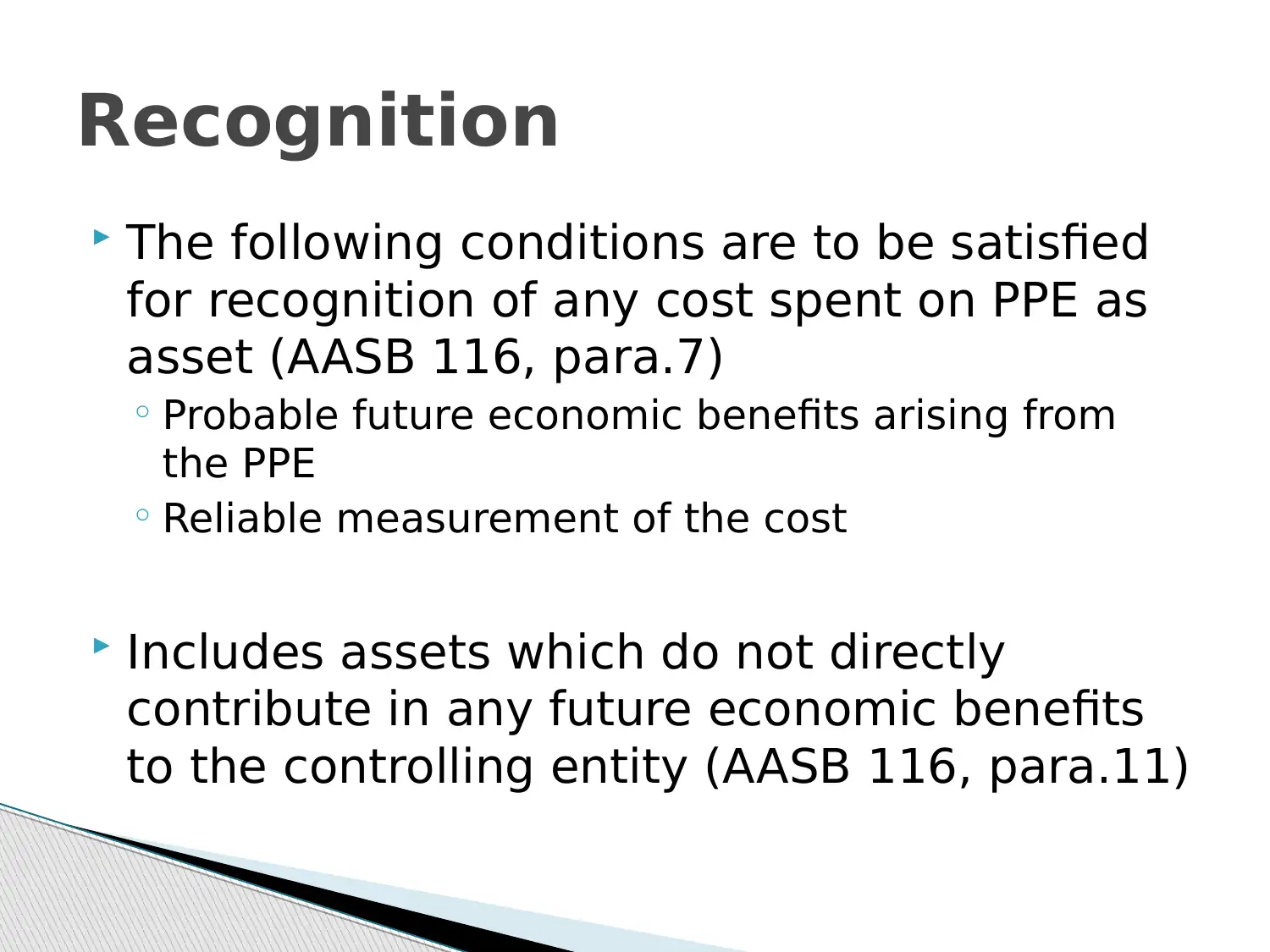

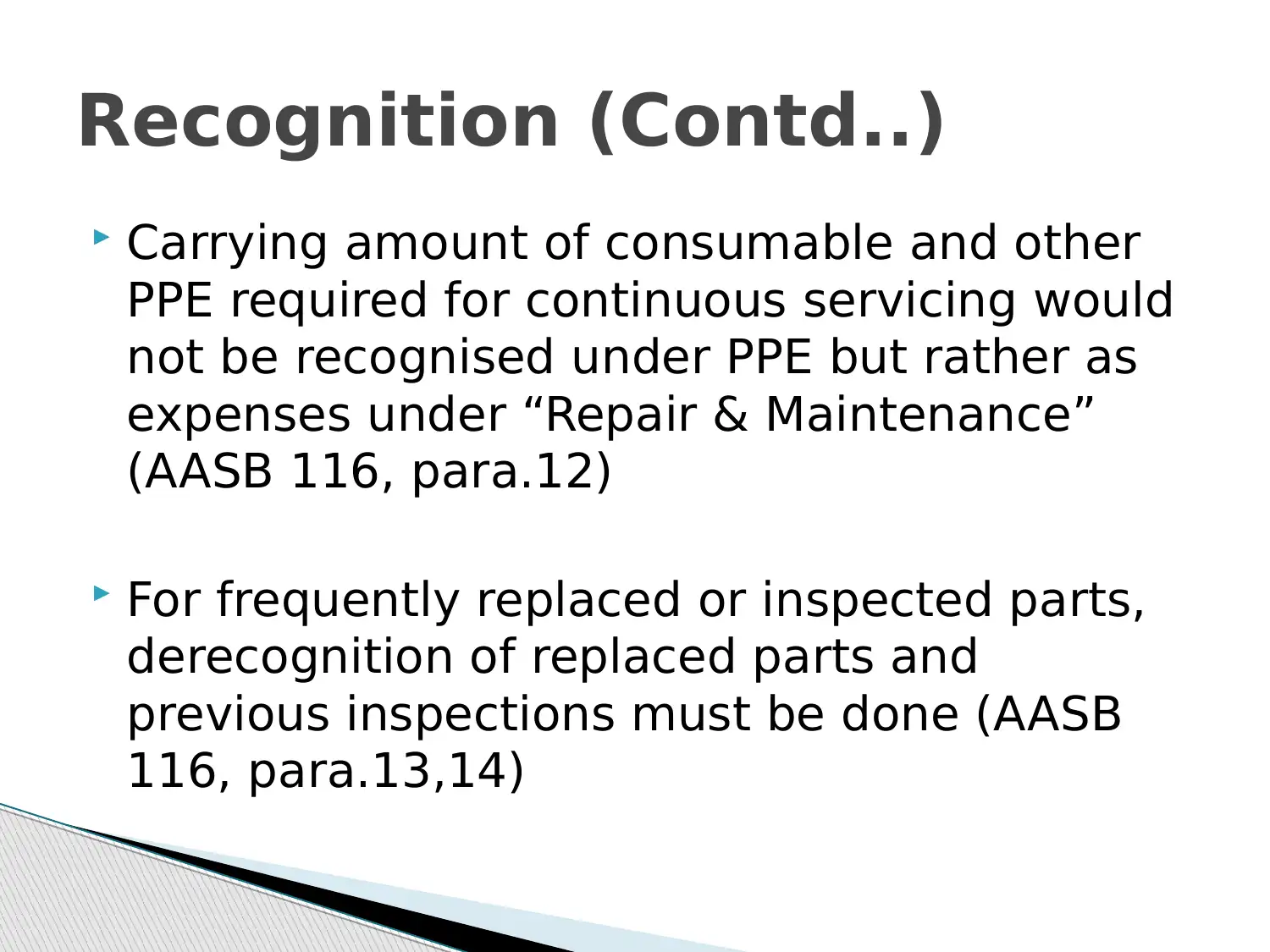

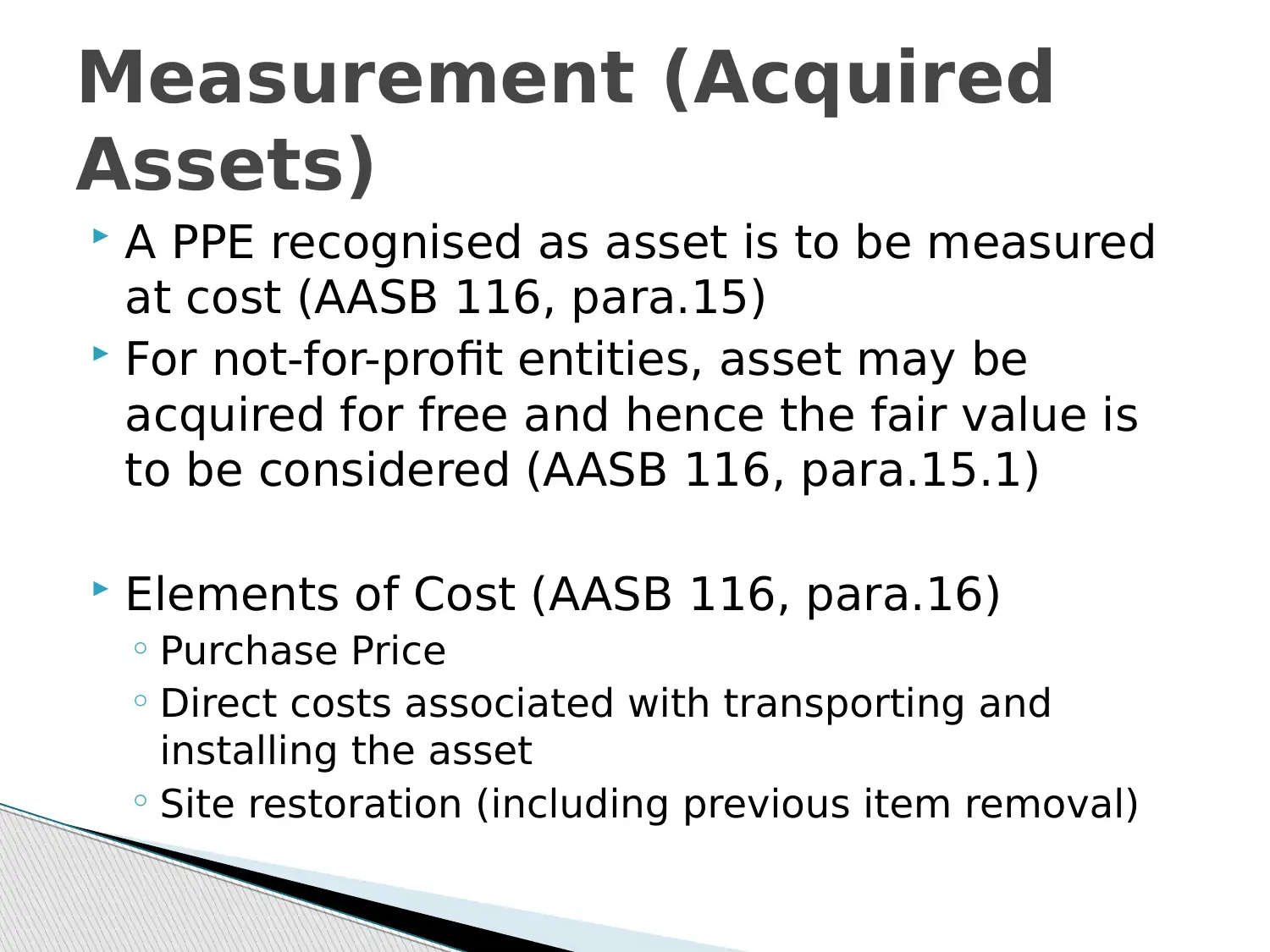

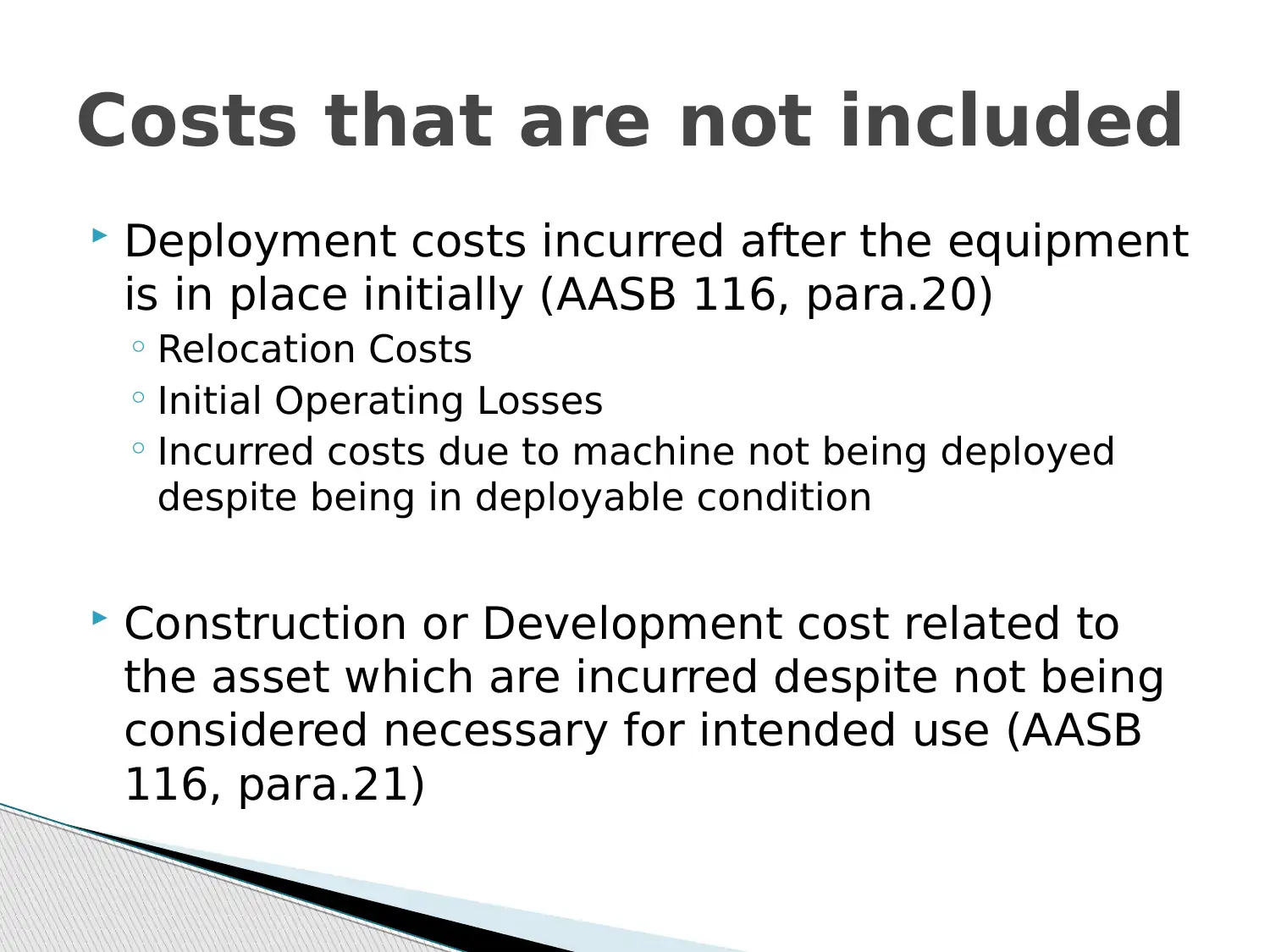

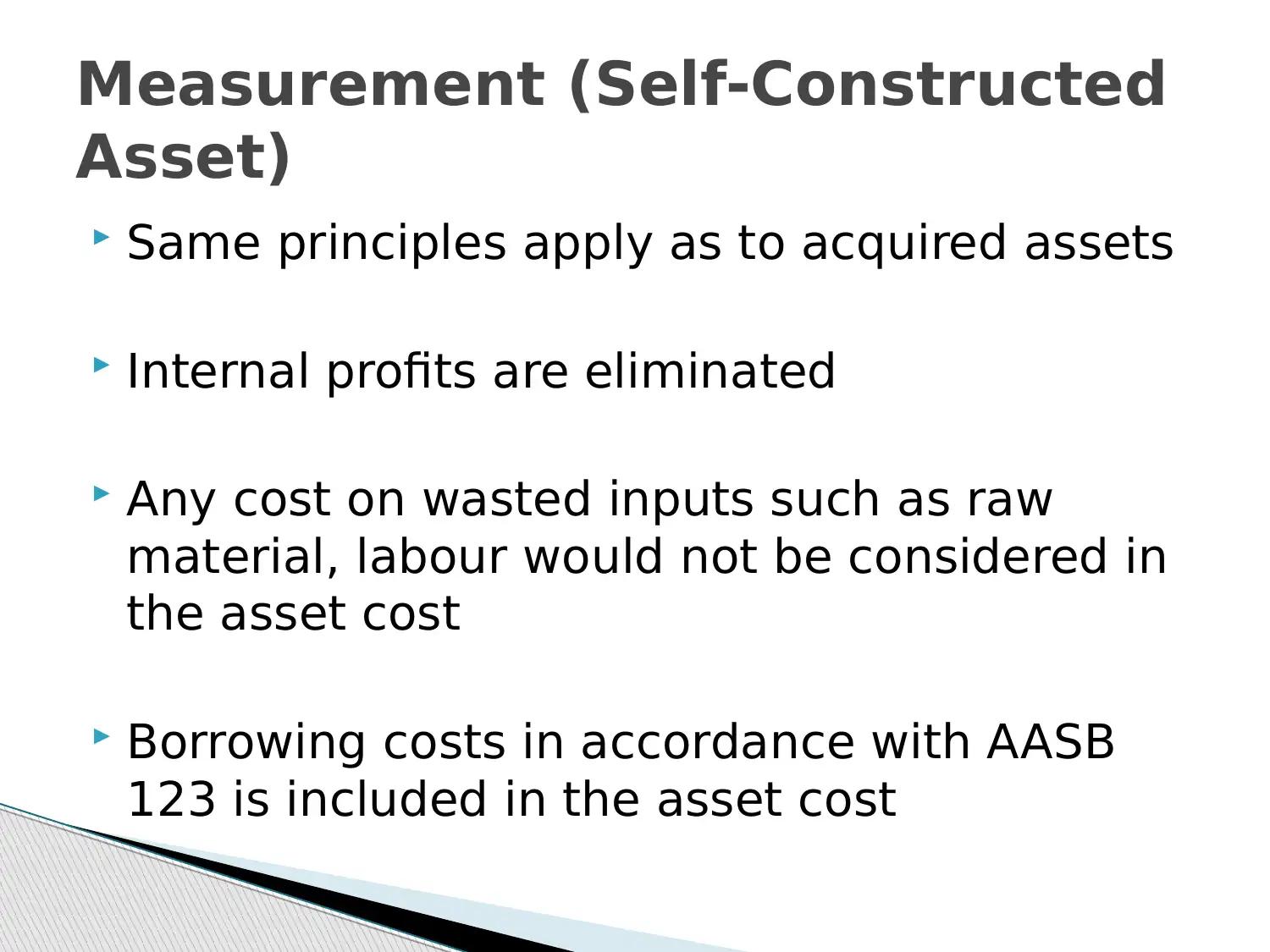

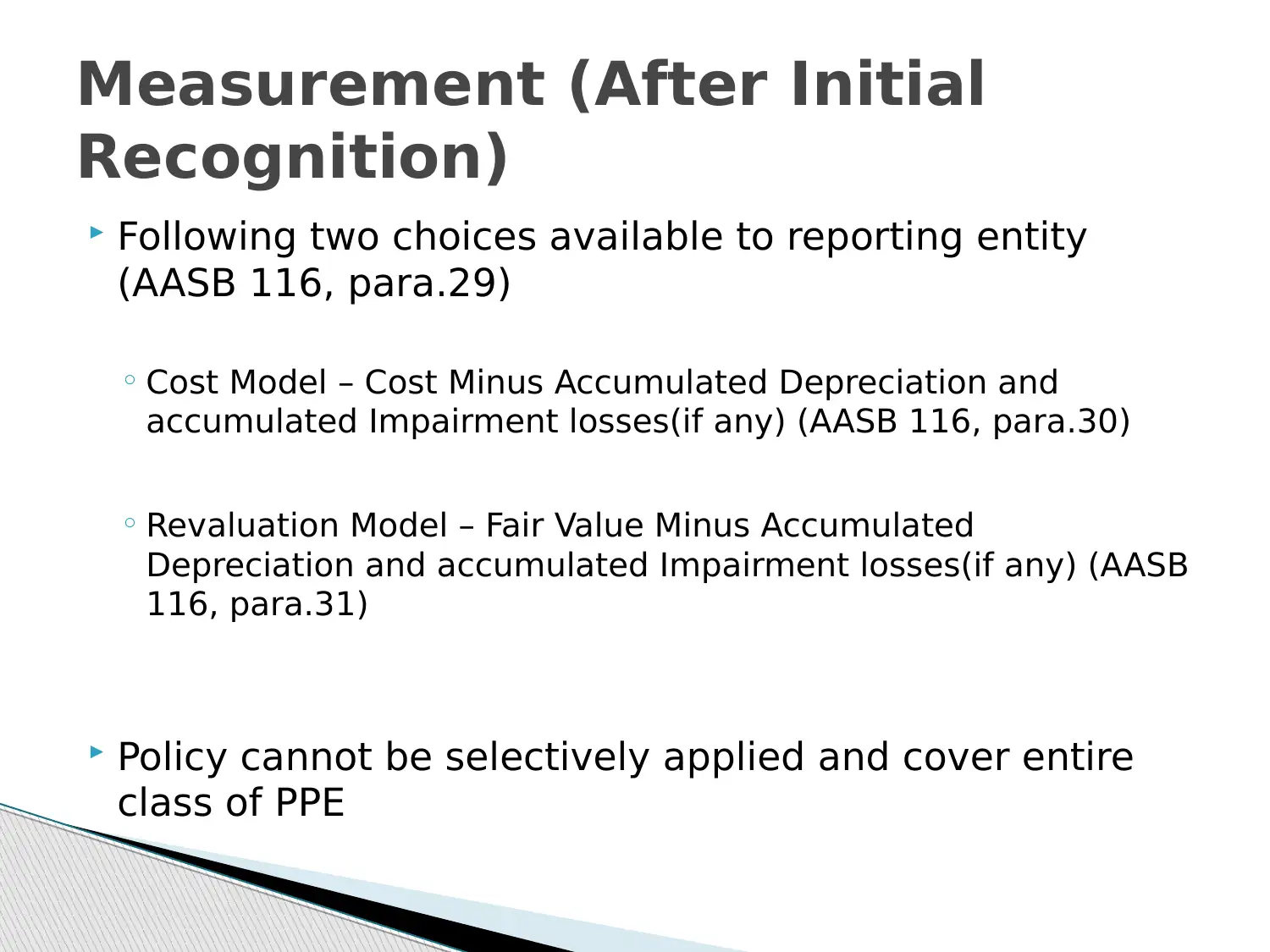

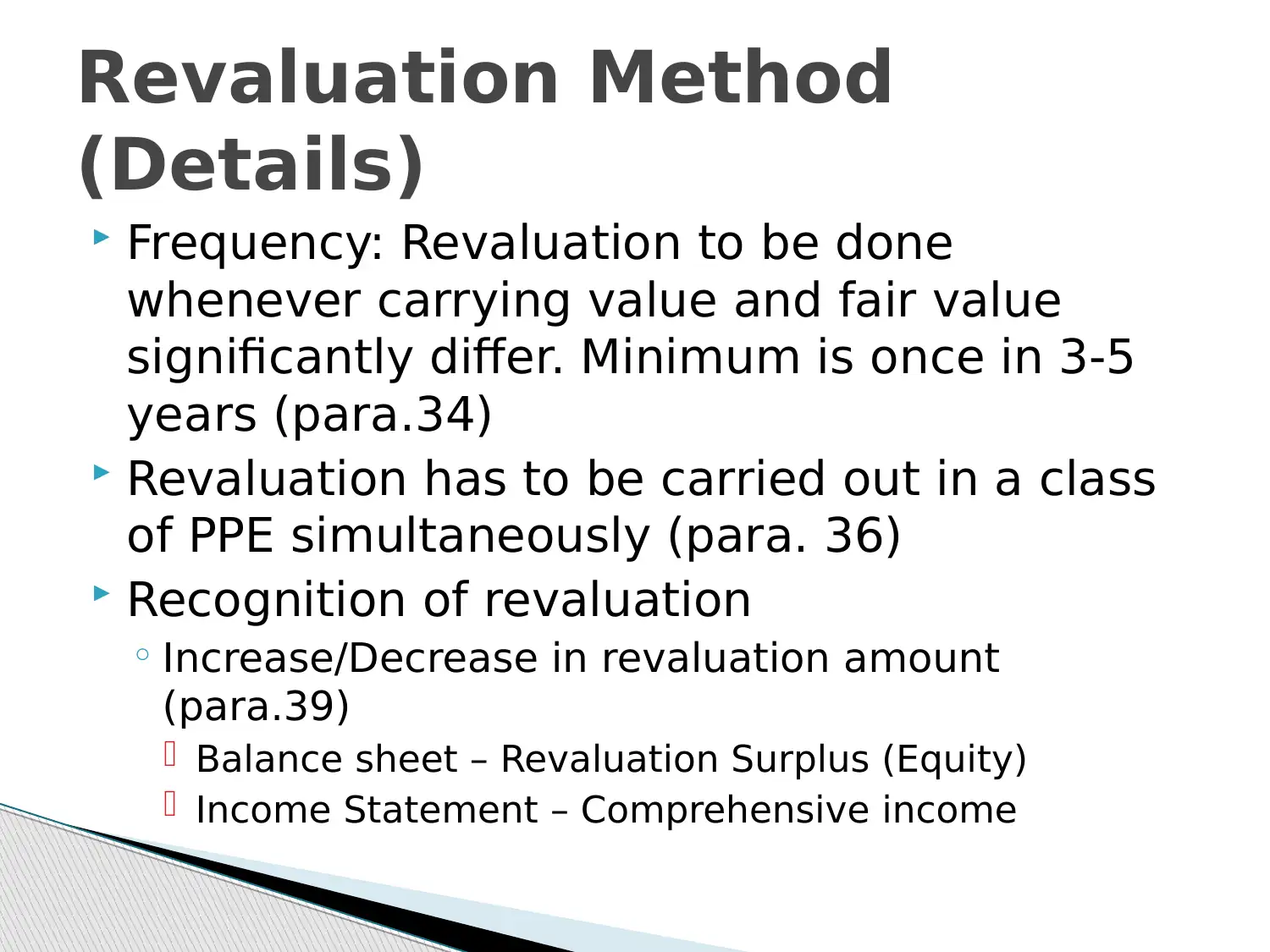

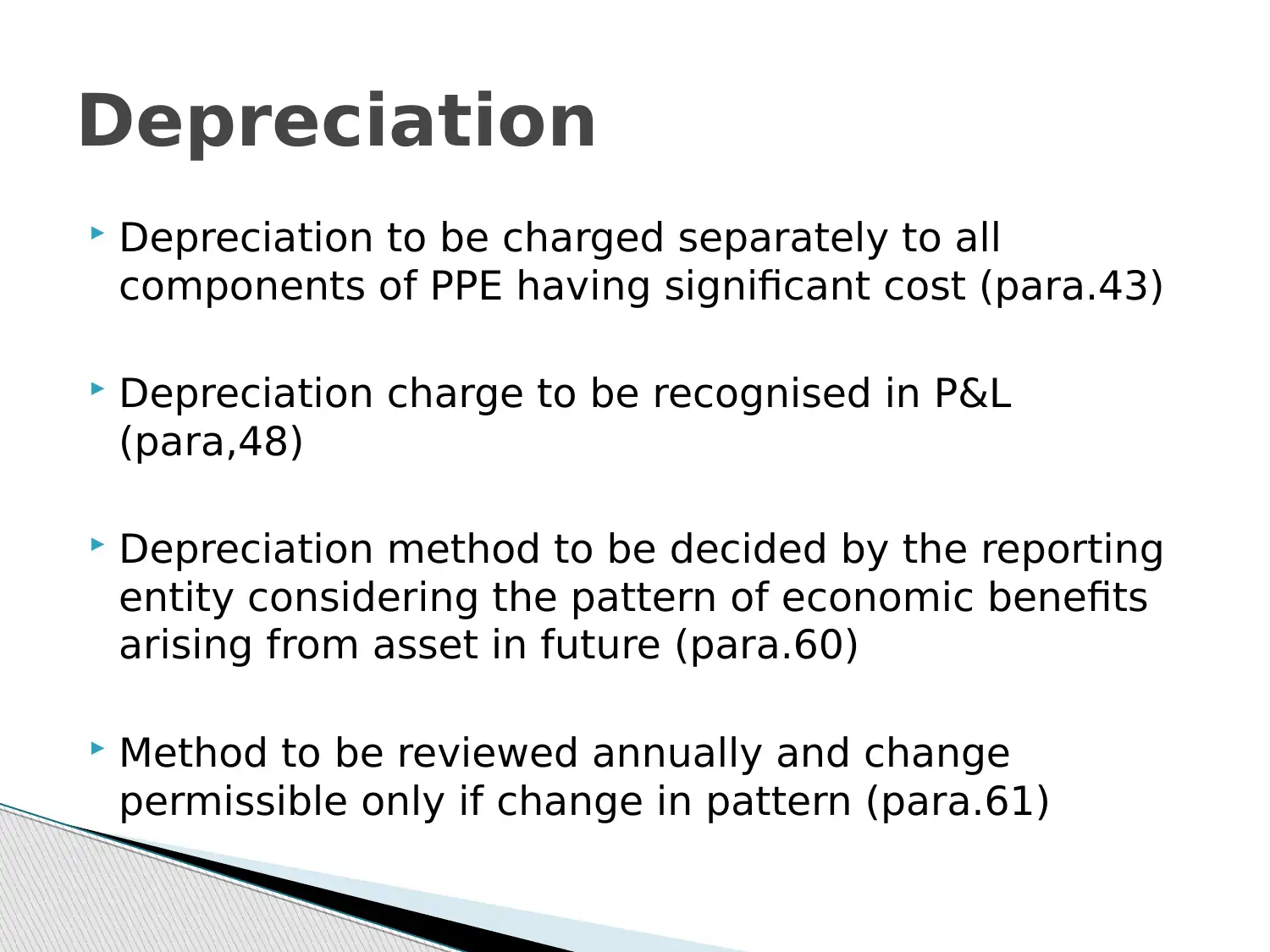

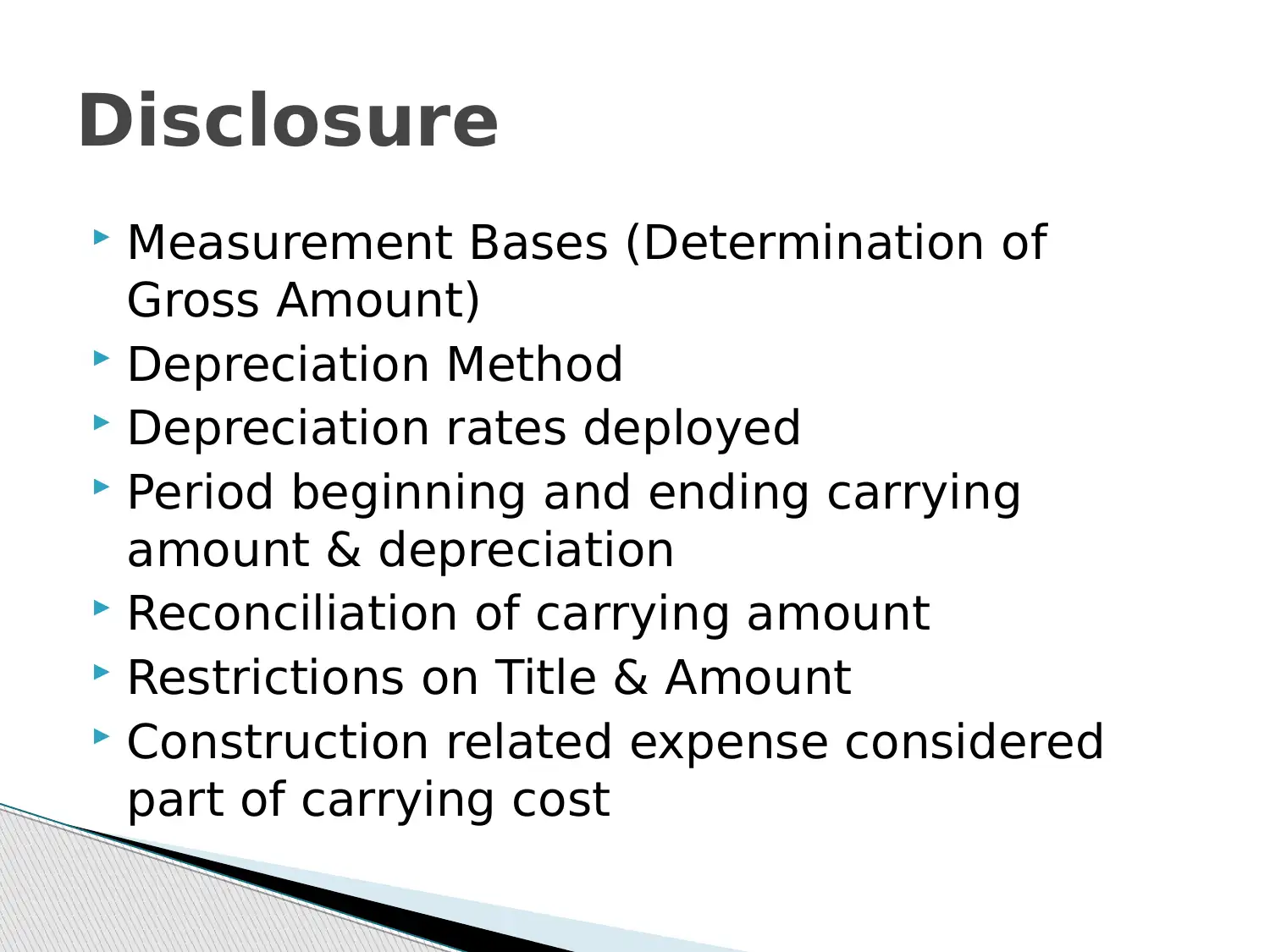

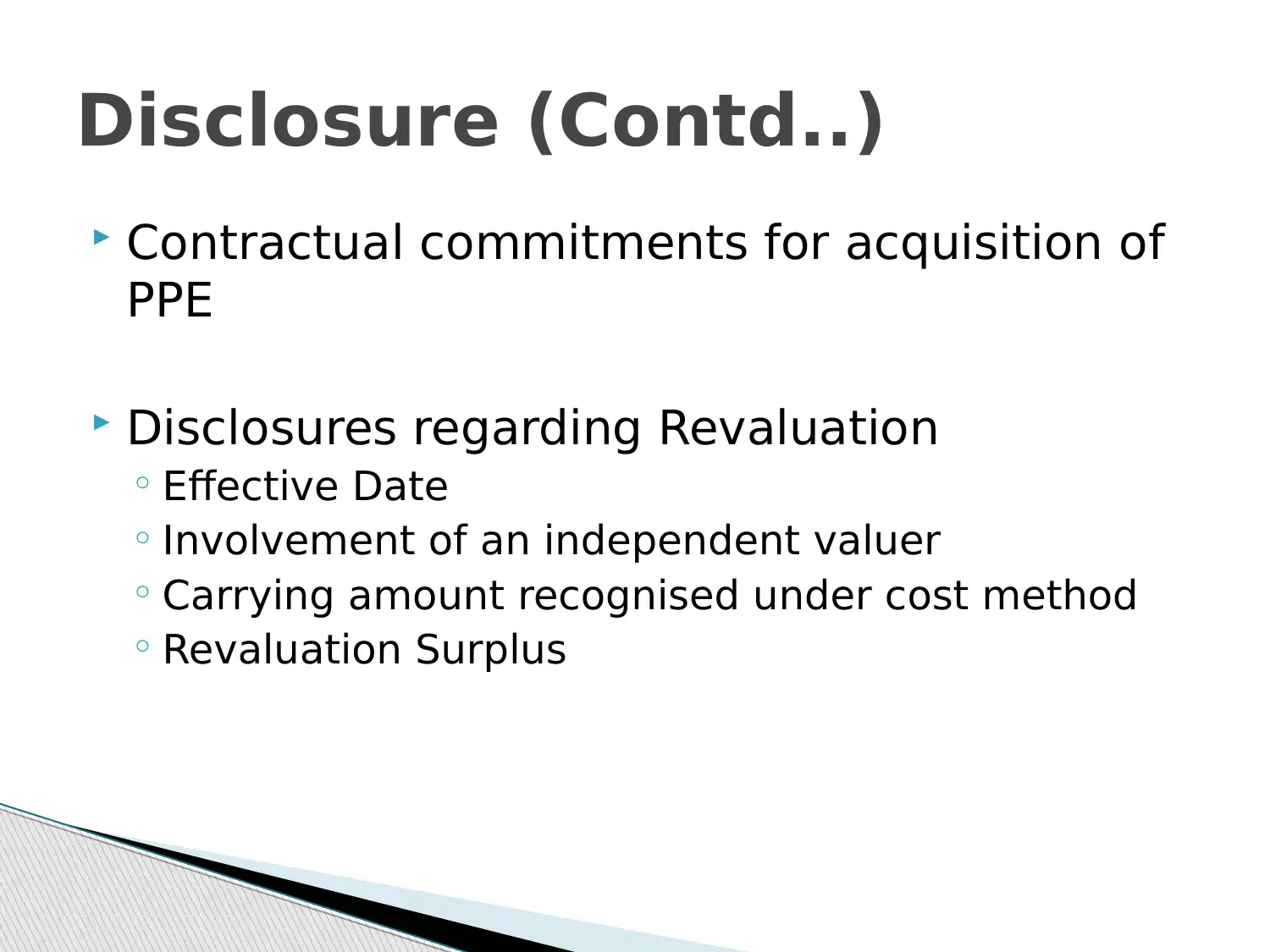

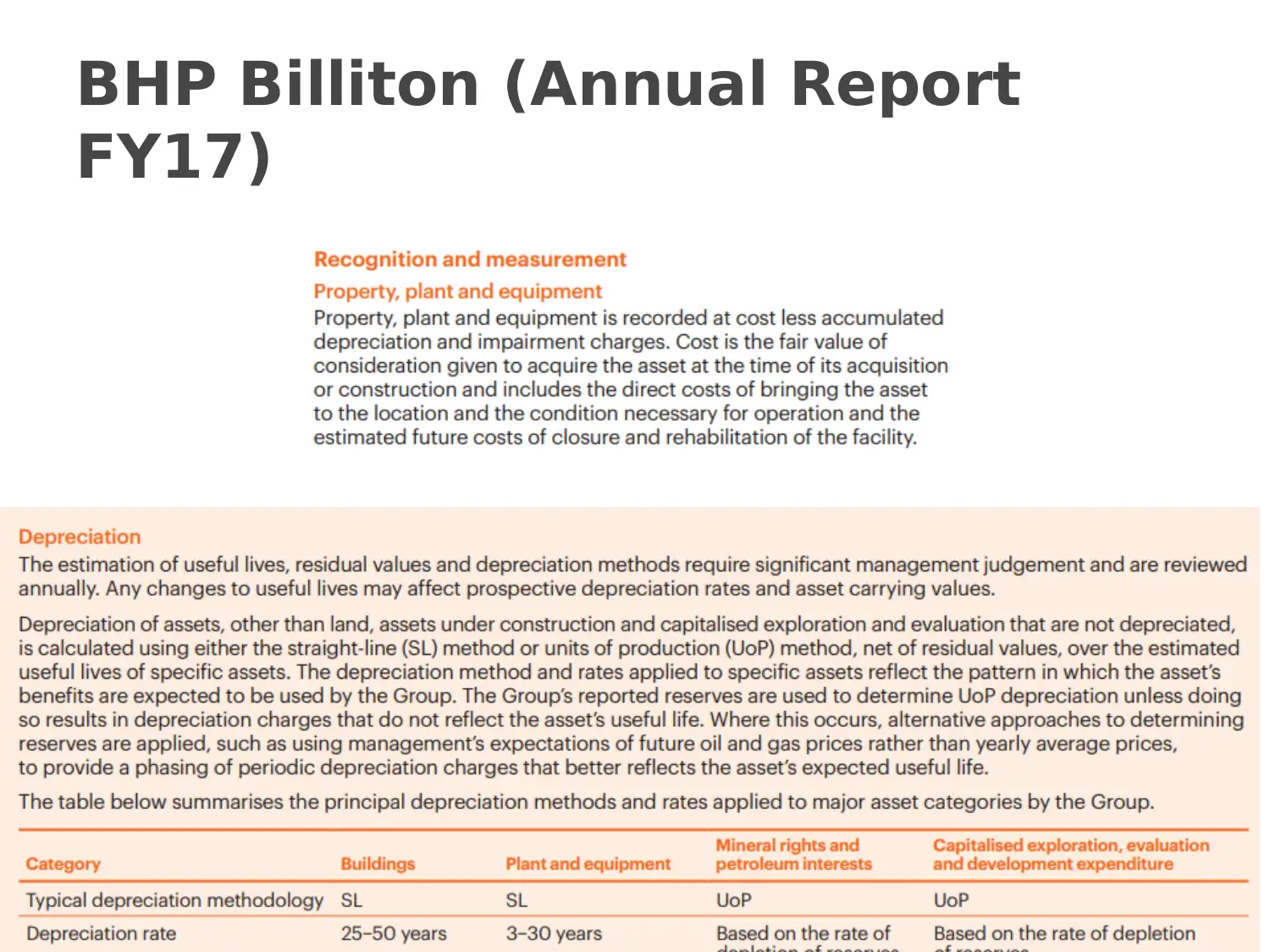

This report provides a comprehensive overview of accounting for Property, Plant, and Equipment (PPE), adhering to the guidelines of AASB 116. It outlines the conditions for asset recognition, emphasizing probable future economic benefits and reliable cost measurement. The report delves into elements of cost, including purchase price, direct costs, and site restoration, while excluding certain costs like initial operating losses and internal profits. It discusses measurement methods, such as the cost model and revaluation model, and addresses depreciation, including methods, rates, and disclosure requirements. The report also examines revaluation frequency, recognition, and the use of revaluation surplus. Furthermore, it incorporates examples from BHP Billiton's annual reports to illustrate practical applications and concludes with a list of relevant references.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.