Comparative Analysis of Accounting Theories: Qantas & Virgin Australia

VerifiedAdded on 2020/03/01

|16

|2251

|223

Report

AI Summary

This report provides a comprehensive comparison of the accounting practices of Qantas Airways and Virgin Australia Airlines. It examines the companies' adherence to accounting standards, particularly AASB and Corporations Act 2001, and the application of the prudence concept. The report analyzes key financial data, including total assets, tangible and intangible assets, and depreciation methods. It also explores the rationale for shareholder investment in both airlines, drawing on information from director's reports and CEO statements. The analysis covers revenue recognition, asset valuation, and the impact of accounting policies on financial performance, providing a detailed overview of the financial reporting frameworks employed by both companies. The report concludes with a summary of the key findings and references relevant literature.

Running head: ACCOUNTING THEORY & CONTEMPORARY ISSUES

Accounting Theory & Contemporary Issues

Name of Student:

Name of University:

Author’s Note:

Accounting Theory & Contemporary Issues

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING THEORY & CONTEMPORARY ISSUES

Executive Summary

The study is intended to important concept which has been seen to be related to the show the

accounting methods adopted by Virgin Australia Airlines and Qantas Airways and various types

of the other notes from the Auditors Report, Remuneration Report and Financial reports. The

final section of the section of the study has been taken into account to discuss on the rationale for

the shareholders to invest. The main accounting standard has been identified with AASB and

Corporations Act 2001. The chief aspect of prudence has been discerned with the delay in the

recognition of the “AASB 15 Revenue from Contracts with Customers (AASB 15)” and “AASB

16 Leases (AASB 16)”. In terms of Qantas Airways Ltd, the assets is categorised as per the

assets held for sale and measured in terms of the fair value less cost of selling. The financial

statements preparation for Virgin Australia Airlines with the assets which are not held for the

assessment based on leases to be categorised at fair value. The important aspect of Qantas Group

has been seen with the decreased recognition as per straight line basis for PPE except for

freehold land. The depreciation and amortisation of the Virgin Airlines is taken into

consideration as per the date they have been classified as being held for sale. The reduction on

the PPE is stated as per cost less “accumulated depreciation and impairment losses”.

Executive Summary

The study is intended to important concept which has been seen to be related to the show the

accounting methods adopted by Virgin Australia Airlines and Qantas Airways and various types

of the other notes from the Auditors Report, Remuneration Report and Financial reports. The

final section of the section of the study has been taken into account to discuss on the rationale for

the shareholders to invest. The main accounting standard has been identified with AASB and

Corporations Act 2001. The chief aspect of prudence has been discerned with the delay in the

recognition of the “AASB 15 Revenue from Contracts with Customers (AASB 15)” and “AASB

16 Leases (AASB 16)”. In terms of Qantas Airways Ltd, the assets is categorised as per the

assets held for sale and measured in terms of the fair value less cost of selling. The financial

statements preparation for Virgin Australia Airlines with the assets which are not held for the

assessment based on leases to be categorised at fair value. The important aspect of Qantas Group

has been seen with the decreased recognition as per straight line basis for PPE except for

freehold land. The depreciation and amortisation of the Virgin Airlines is taken into

consideration as per the date they have been classified as being held for sale. The reduction on

the PPE is stated as per cost less “accumulated depreciation and impairment losses”.

2ACCOUNTING THEORY & CONTEMPORARY ISSUES

Table of Contents

Introduction......................................................................................................................................3

Conceptual framework of Accounting for both the companies.......................................................3

Prudence theory applied in both the companies..............................................................................4

Criteria followed for financial data..................................................................................................5

Rationale for the shareholders investing in the companies.............................................................6

Conclusion.......................................................................................................................................7

List of Appendix..............................................................................................................................8

Reference List................................................................................................................................14

Table of Contents

Introduction......................................................................................................................................3

Conceptual framework of Accounting for both the companies.......................................................3

Prudence theory applied in both the companies..............................................................................4

Criteria followed for financial data..................................................................................................5

Rationale for the shareholders investing in the companies.............................................................6

Conclusion.......................................................................................................................................7

List of Appendix..............................................................................................................................8

Reference List................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING THEORY & CONTEMPORARY ISSUES

Introduction

Qantas Airways owns Jetstar is considered as one of the discount priced airline operator

in Australia. JetStar carries more than 8.5% passenger from Australia itself. It has been further

seen to operate as per the home and the international network from Melbourne Airport. The

primary fleet of the airline operator has been seen to be acknowledged with the A320 and Boeing

787 Dreamliner.

Virgin Australia Airlines is discerned as the second principal airline carrier after Qantas

Airways. The airline company is seen to be based in Bowen Hills in Brisbane. It has been further

seen to be considered in 1999 and operated in one route. The airline carrier is considered to

expand itself in 29 cities in areas such as Brisbane, Adelaide, Melbourne and Sydney.

The objective has been seen to be based on the important concept which has been seen to

be related to the show the methods adopted by both the companies and various types of the other

notes from the Auditors Report, Remuneration Report and Financial reports. The final section of

the segment of the lessons has been further able to discuss on the rational for the shareholders to

invest.

Conceptual framework of Accounting for both the companies

It has been observed that both the companies have been seen with “AASB and

Corporations Act 2001”. It has been seen that financial report of both the companies has been

prepared as the IFRS. This standard is further seen to be issued by the international accounting

board. The important consideration for this has been based on the various types of the

consideration taken from the financial statements of both Jetstar Airways and Virgin Australia

Introduction

Qantas Airways owns Jetstar is considered as one of the discount priced airline operator

in Australia. JetStar carries more than 8.5% passenger from Australia itself. It has been further

seen to operate as per the home and the international network from Melbourne Airport. The

primary fleet of the airline operator has been seen to be acknowledged with the A320 and Boeing

787 Dreamliner.

Virgin Australia Airlines is discerned as the second principal airline carrier after Qantas

Airways. The airline company is seen to be based in Bowen Hills in Brisbane. It has been further

seen to be considered in 1999 and operated in one route. The airline carrier is considered to

expand itself in 29 cities in areas such as Brisbane, Adelaide, Melbourne and Sydney.

The objective has been seen to be based on the important concept which has been seen to

be related to the show the methods adopted by both the companies and various types of the other

notes from the Auditors Report, Remuneration Report and Financial reports. The final section of

the segment of the lessons has been further able to discuss on the rational for the shareholders to

invest.

Conceptual framework of Accounting for both the companies

It has been observed that both the companies have been seen with “AASB and

Corporations Act 2001”. It has been seen that financial report of both the companies has been

prepared as the IFRS. This standard is further seen to be issued by the international accounting

board. The important consideration for this has been based on the various types of the

consideration taken from the financial statements of both Jetstar Airways and Virgin Australia

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING THEORY & CONTEMPORARY ISSUES

Airlines. This is further seen to be considered as per the historical cost evaluation except in

sections of asset and liabilities which needs assessment as per the fair value and other relevant

accounting policies (Steenkamp & Steenkamp, 2016).

The import aspect of the accounting aspect of revenue recognition is seen to be

considered as per “AASB 118 Revenue”, “AASB 111 Construction Contracts and

Interpretation 13 Customer Loyalty Programmes”. The company is yet to implement the

“AASB 15 Revenue from contracts with the customers”, this has been seen to be based on the

existing nature of the standards which has been set to be implemented as per the commence date

of on or after 1st January 2018. The main activities of the company have been further able to

decide if they will be able to swap the “AASB 117 for leases” and able to change the various

considerations of the framework based on AASB 16. “AASB 136: Impairment of Assets”, is

applicable for the recognition of the financial guarantees and the agreement which is seen to be

related to the financial guarantees based on the implementation of “AASB 137 Provisions,

Contingent Liabilities and Contingent Assets” (Marshall et al., 2013).

Prudence theory applied in both the companies

Theoretical application of prudence has been further seen to be based on the fact that

none of the company overestimate of total revenues. Virgin Australia and Jetstar has applied the

prudence concept based on the financial information which is conservative and the recording of

the assets is not underestimated based on the liabilities. It has been further seen that the financial

statements has considered the probable transaction into considerations. A variety of the

important consideration for the prudence has not been applied as per the “AASB 15 Revenue

from Contracts with Customers (AASB 15)” and the application of “AASB 16 Leases (AASB

Airlines. This is further seen to be considered as per the historical cost evaluation except in

sections of asset and liabilities which needs assessment as per the fair value and other relevant

accounting policies (Steenkamp & Steenkamp, 2016).

The import aspect of the accounting aspect of revenue recognition is seen to be

considered as per “AASB 118 Revenue”, “AASB 111 Construction Contracts and

Interpretation 13 Customer Loyalty Programmes”. The company is yet to implement the

“AASB 15 Revenue from contracts with the customers”, this has been seen to be based on the

existing nature of the standards which has been set to be implemented as per the commence date

of on or after 1st January 2018. The main activities of the company have been further able to

decide if they will be able to swap the “AASB 117 for leases” and able to change the various

considerations of the framework based on AASB 16. “AASB 136: Impairment of Assets”, is

applicable for the recognition of the financial guarantees and the agreement which is seen to be

related to the financial guarantees based on the implementation of “AASB 137 Provisions,

Contingent Liabilities and Contingent Assets” (Marshall et al., 2013).

Prudence theory applied in both the companies

Theoretical application of prudence has been further seen to be based on the fact that

none of the company overestimate of total revenues. Virgin Australia and Jetstar has applied the

prudence concept based on the financial information which is conservative and the recording of

the assets is not underestimated based on the liabilities. It has been further seen that the financial

statements has considered the probable transaction into considerations. A variety of the

important consideration for the prudence has not been applied as per the “AASB 15 Revenue

from Contracts with Customers (AASB 15)” and the application of “AASB 16 Leases (AASB

5ACCOUNTING THEORY & CONTEMPORARY ISSUES

16)”. It is seen to be convinced of replacing the existing standards. For testing the viability of the

various types of the methods, the companies have been able to decide on test the new method for

lease only after 01.01.2019. Other considerations of prudence have been depicted with the

regular review of the assets and in terms of assessment of the decreasing values of these assets.

The most important consideration for prudence is evident among both the companies by writing

off the values in terms of fixed assets (Barker, 2015).

Criteria followed for financial data

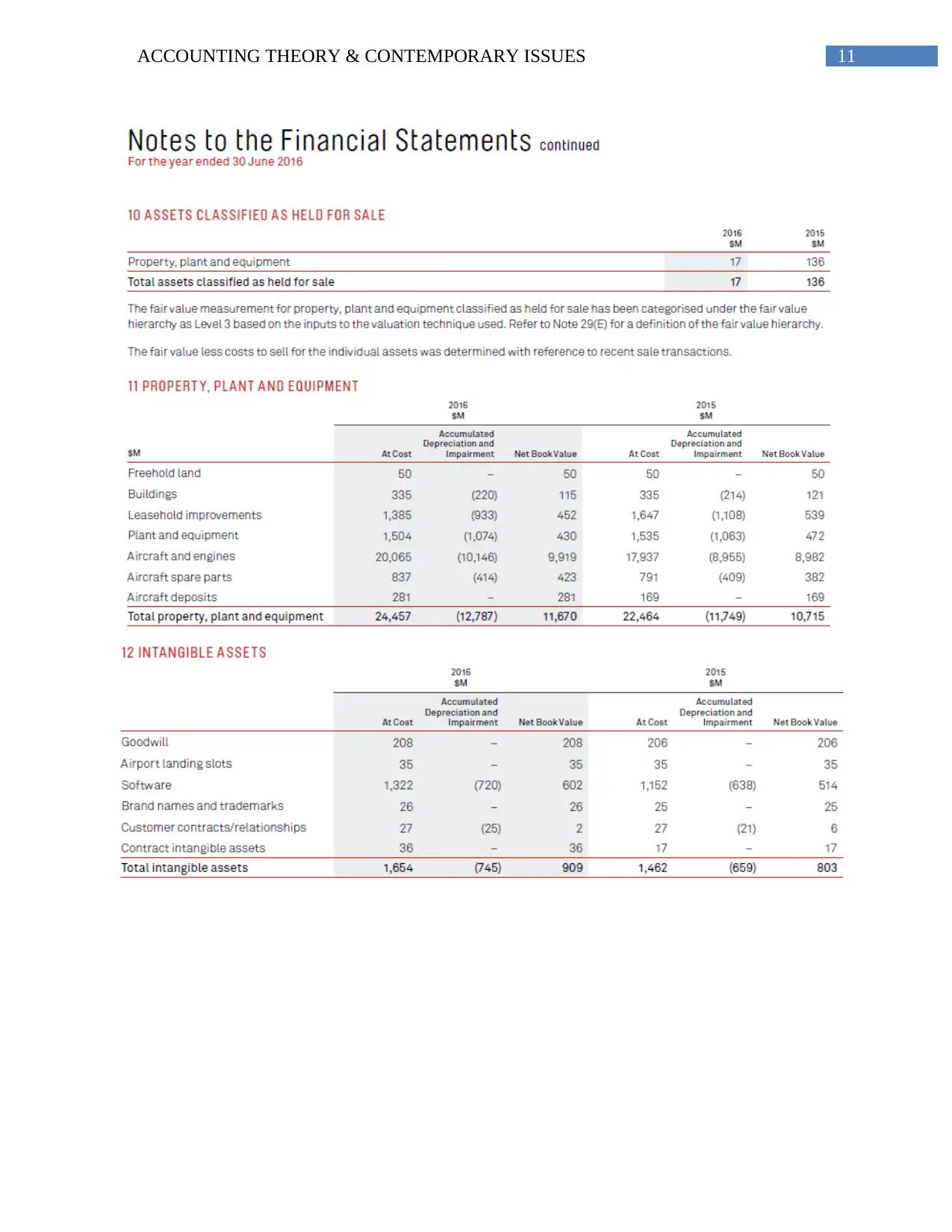

Total Assets- The total asset of Qantas Airways is standing at $ 17708m in 2016; however the

entire asset of virgin Australia is seen to be $ 6886.9 m in 2016. In addition to this, Virgin

Australia is not having any amount of the dependent liabilities as on 30 June 2016. In terms of

Qantas Airways Ltd, the assets have been seen to be categorised as per the assets held for sale

and measured in terms of the fair value less cost of selling. The main benefit of Qantas Airways

is seen with the measurement of “fair value of plan assets less the present value”. The different

types of the other consideration has been further seen to be made with the preparation of

financial statements of Virgin Australia Airlines with the assets which are not held for the

assessment based on financial leases to be recognised at fair value (Wan Norhishamuddinet al.,

2015).

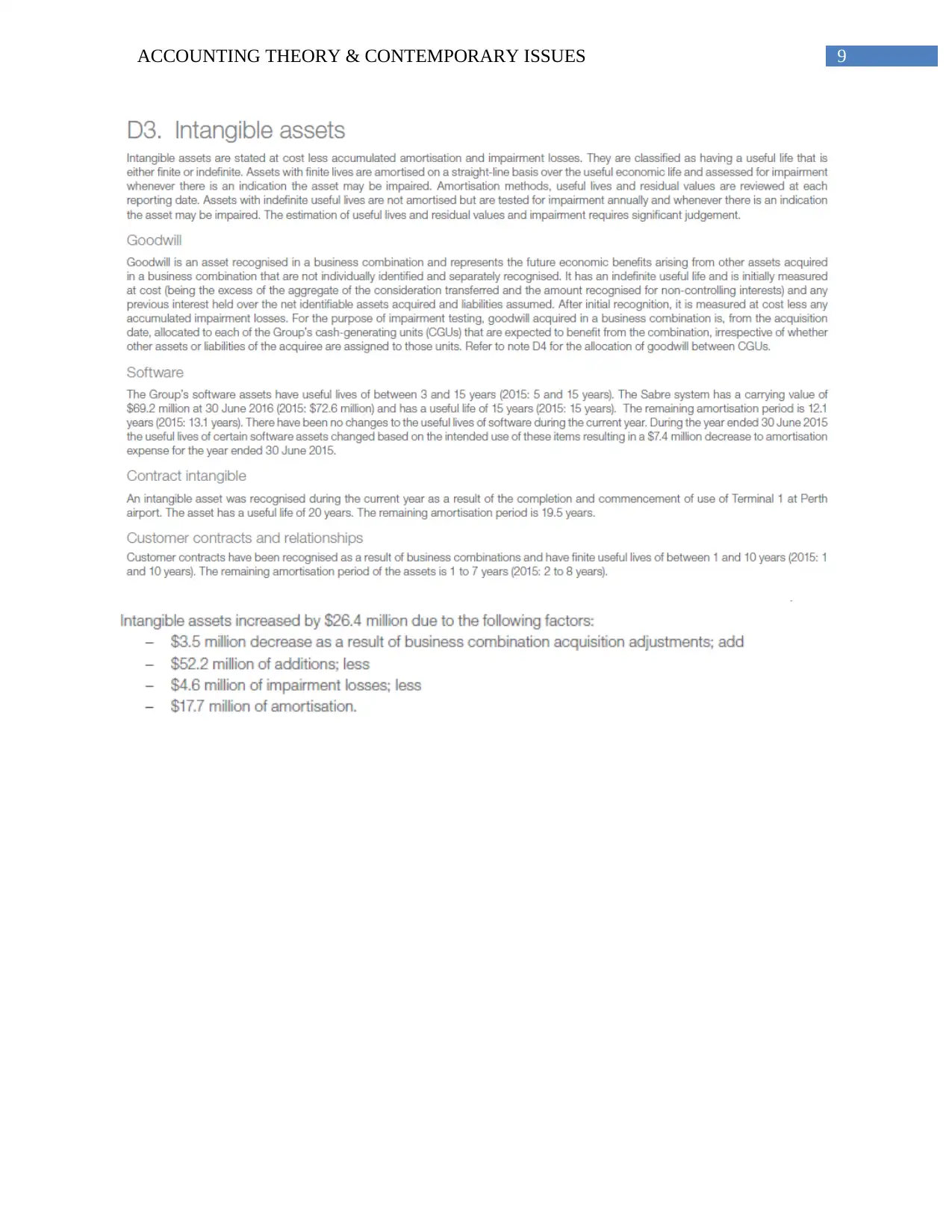

Tangible Assets and Intangible Assets- It has been depicted with the recognition of the

intangible and the intangible assets, with the consideration of “non-current tangible assets”,

which are further seen to be regarded for revenue as per the recoverable amount of the assets.

The amortisation is considered as per residual life and useful life as per the date of reporting

(Guthrie & Pang, 2013).

16)”. It is seen to be convinced of replacing the existing standards. For testing the viability of the

various types of the methods, the companies have been able to decide on test the new method for

lease only after 01.01.2019. Other considerations of prudence have been depicted with the

regular review of the assets and in terms of assessment of the decreasing values of these assets.

The most important consideration for prudence is evident among both the companies by writing

off the values in terms of fixed assets (Barker, 2015).

Criteria followed for financial data

Total Assets- The total asset of Qantas Airways is standing at $ 17708m in 2016; however the

entire asset of virgin Australia is seen to be $ 6886.9 m in 2016. In addition to this, Virgin

Australia is not having any amount of the dependent liabilities as on 30 June 2016. In terms of

Qantas Airways Ltd, the assets have been seen to be categorised as per the assets held for sale

and measured in terms of the fair value less cost of selling. The main benefit of Qantas Airways

is seen with the measurement of “fair value of plan assets less the present value”. The different

types of the other consideration has been further seen to be made with the preparation of

financial statements of Virgin Australia Airlines with the assets which are not held for the

assessment based on financial leases to be recognised at fair value (Wan Norhishamuddinet al.,

2015).

Tangible Assets and Intangible Assets- It has been depicted with the recognition of the

intangible and the intangible assets, with the consideration of “non-current tangible assets”,

which are further seen to be regarded for revenue as per the recoverable amount of the assets.

The amortisation is considered as per residual life and useful life as per the date of reporting

(Guthrie & Pang, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING THEORY & CONTEMPORARY ISSUES

Depreciation – The important aspect of Qantas Group has been seen with the depreciation

recognition as per “straight line basis for PPE except for freehold land”. The rate of

depreciation of the assets is calculated by total assessment cost is estimated as per the residual

values for the various types the useful life of the assets. In a similar way the depreciation and

amortisation of the Virgin Airlines is taken into consideration as per the date on which they are

classified as held for sale. The depreciation on the PPE is stated as per cost less “accumulated

depreciation and impairment losses”. Same as Qantas, Virgin Airlines recognises the

depreciation of the assets with the straight line and estimate the same, with the useful life of the

residual value (Microsoft, 2015).

Rationale for the shareholders investing in the companies

The different types of the considerations made from the director’s report has been able to

state on the various implication on the shareholders investing in both Qantas Airline and Virgin

Airlines. Based on the report of Virgin Airlines, the revenue of the company has been observed

to rise from $4,749.2 million to $5,021.0 million. The comparative period has been able to reflect

on the total equity which is accounted as 60% of the equity from Tigerair Australia in 16 October

2014. The investor need to further consider on increasing the net operating expenditure from

$4,802.7 million to $5,278.7 million. This particular aspect has been seen to be negative for

Qantas. The increasing equity has been considered to be conducive for investing in Virgin

Airlines (Kober, Lee, & Ng, 2013).

As per the CEO statement as per the annual report of 2016, is seen to significantly

contribute with high figures in 2015-16. The total add to in financial performance is also obvious

with the growing operating margin recognised with the increasing EBIT for “Jetstar Group,

Depreciation – The important aspect of Qantas Group has been seen with the depreciation

recognition as per “straight line basis for PPE except for freehold land”. The rate of

depreciation of the assets is calculated by total assessment cost is estimated as per the residual

values for the various types the useful life of the assets. In a similar way the depreciation and

amortisation of the Virgin Airlines is taken into consideration as per the date on which they are

classified as held for sale. The depreciation on the PPE is stated as per cost less “accumulated

depreciation and impairment losses”. Same as Qantas, Virgin Airlines recognises the

depreciation of the assets with the straight line and estimate the same, with the useful life of the

residual value (Microsoft, 2015).

Rationale for the shareholders investing in the companies

The different types of the considerations made from the director’s report has been able to

state on the various implication on the shareholders investing in both Qantas Airline and Virgin

Airlines. Based on the report of Virgin Airlines, the revenue of the company has been observed

to rise from $4,749.2 million to $5,021.0 million. The comparative period has been able to reflect

on the total equity which is accounted as 60% of the equity from Tigerair Australia in 16 October

2014. The investor need to further consider on increasing the net operating expenditure from

$4,802.7 million to $5,278.7 million. This particular aspect has been seen to be negative for

Qantas. The increasing equity has been considered to be conducive for investing in Virgin

Airlines (Kober, Lee, & Ng, 2013).

As per the CEO statement as per the annual report of 2016, is seen to significantly

contribute with high figures in 2015-16. The total add to in financial performance is also obvious

with the growing operating margin recognised with the increasing EBIT for “Jetstar Group,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING THEORY & CONTEMPORARY ISSUES

Qantas Loyalty, Qantas International and Qantas Domestic”. It has been further discerned that

over two thirds of the total remuneration of Qantas has been measured with the international

operations, strategy of the portfolio and loyalty business. It needs to be considered by the

investors the increasing in the profit before tax from $ 975 m in 2015 to $ 1532 in 2016. As per

the financial examination it has been observed that Jetstar (Qantas) is not only in better position

than Virgin Airlines and the operating expenses is lower, which makes it a better contender than

the latter (Menegatti, 2014).

Conclusion

The main aspects of the study have able to highlight the present framework of accounting

for both Qantas Airways and Virgin Airlines. The a variety of aspect of the study has been able

to check for the compliance of the financial report as per the prescribed standard. The conceptual

framework of the report has been further seen to be considered as per the “AASB and

Corporations Act 2001”. It has been further discerned from the financial statements that the

main accounting framework is seen to be based IFRS. This standard is issued by the international

board of accounts. The main consideration of the financial statement has been based on previous

cost evaluation, except in some of the areas where the possessions and liabilities needs

assessment based on fair value and the relevant accounting policies.

Qantas Loyalty, Qantas International and Qantas Domestic”. It has been further discerned that

over two thirds of the total remuneration of Qantas has been measured with the international

operations, strategy of the portfolio and loyalty business. It needs to be considered by the

investors the increasing in the profit before tax from $ 975 m in 2015 to $ 1532 in 2016. As per

the financial examination it has been observed that Jetstar (Qantas) is not only in better position

than Virgin Airlines and the operating expenses is lower, which makes it a better contender than

the latter (Menegatti, 2014).

Conclusion

The main aspects of the study have able to highlight the present framework of accounting

for both Qantas Airways and Virgin Airlines. The a variety of aspect of the study has been able

to check for the compliance of the financial report as per the prescribed standard. The conceptual

framework of the report has been further seen to be considered as per the “AASB and

Corporations Act 2001”. It has been further discerned from the financial statements that the

main accounting framework is seen to be based IFRS. This standard is issued by the international

board of accounts. The main consideration of the financial statement has been based on previous

cost evaluation, except in some of the areas where the possessions and liabilities needs

assessment based on fair value and the relevant accounting policies.

8ACCOUNTING THEORY & CONTEMPORARY ISSUES

List of Appendix

Virgin Australia Group

List of Appendix

Virgin Australia Group

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING THEORY & CONTEMPORARY ISSUES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING THEORY & CONTEMPORARY ISSUES

Qantas Airways

Qantas Airways

11ACCOUNTING THEORY & CONTEMPORARY ISSUES

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.