Analysis of Accounting Records and Financial Statements for Conga

VerifiedAdded on 2020/10/05

|24

|4948

|210

Homework Assignment

AI Summary

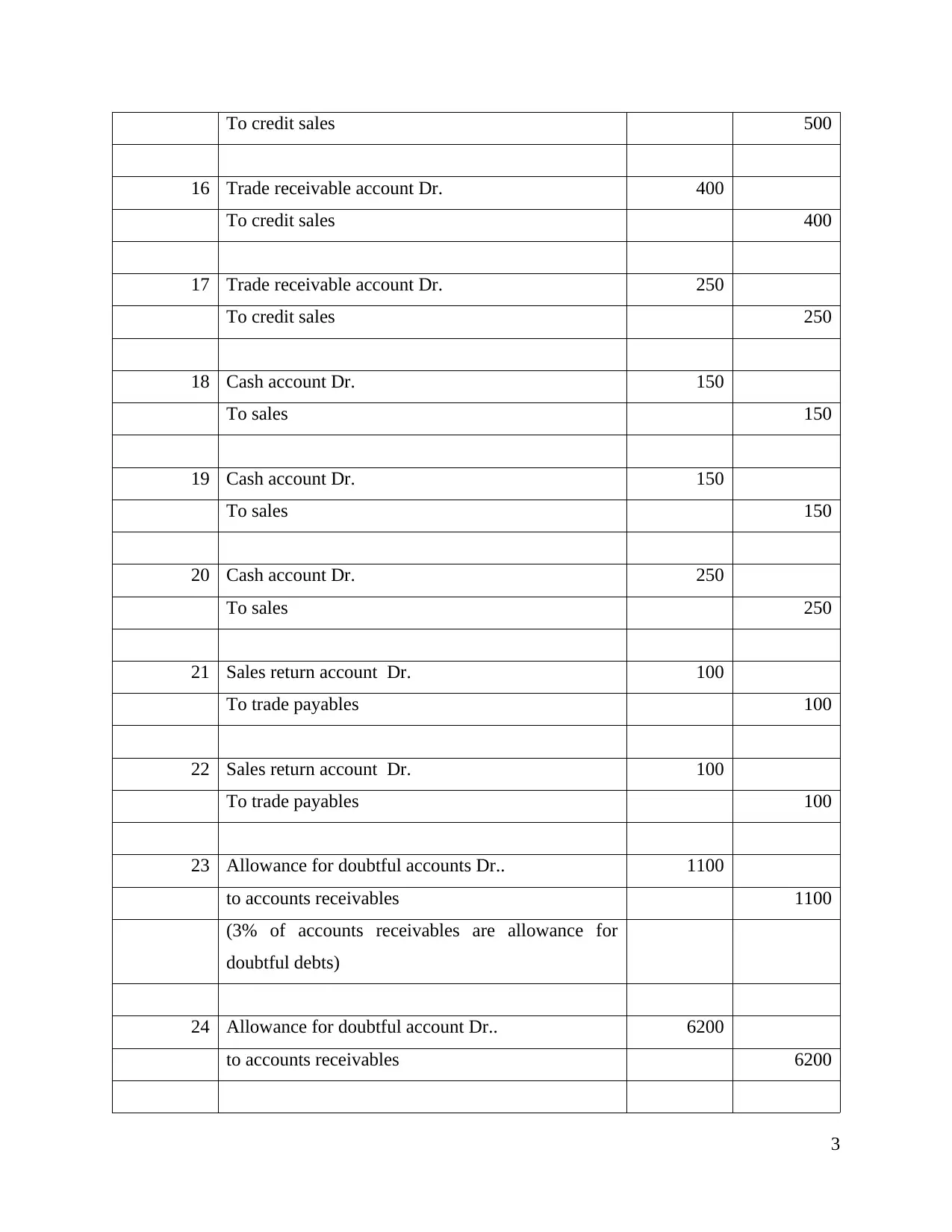

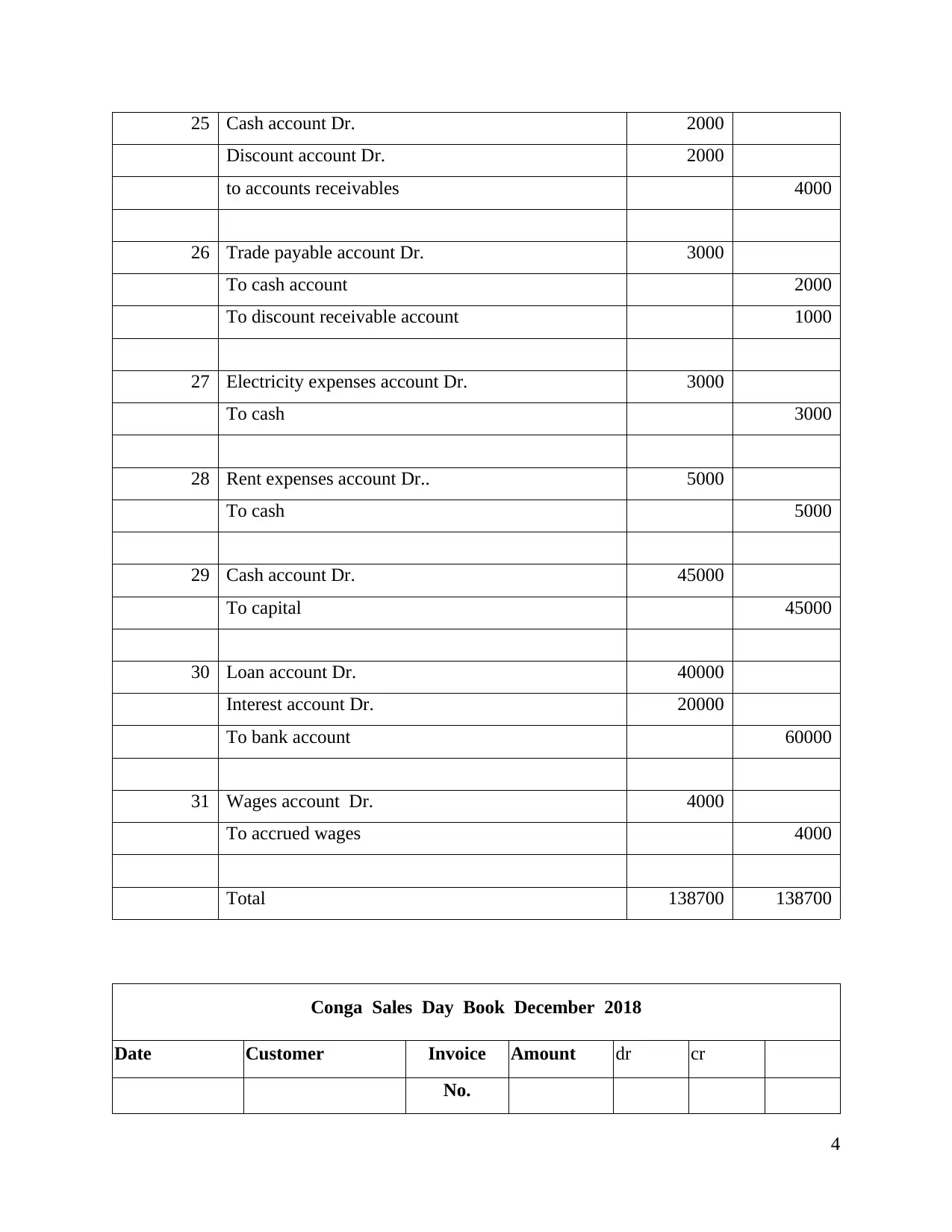

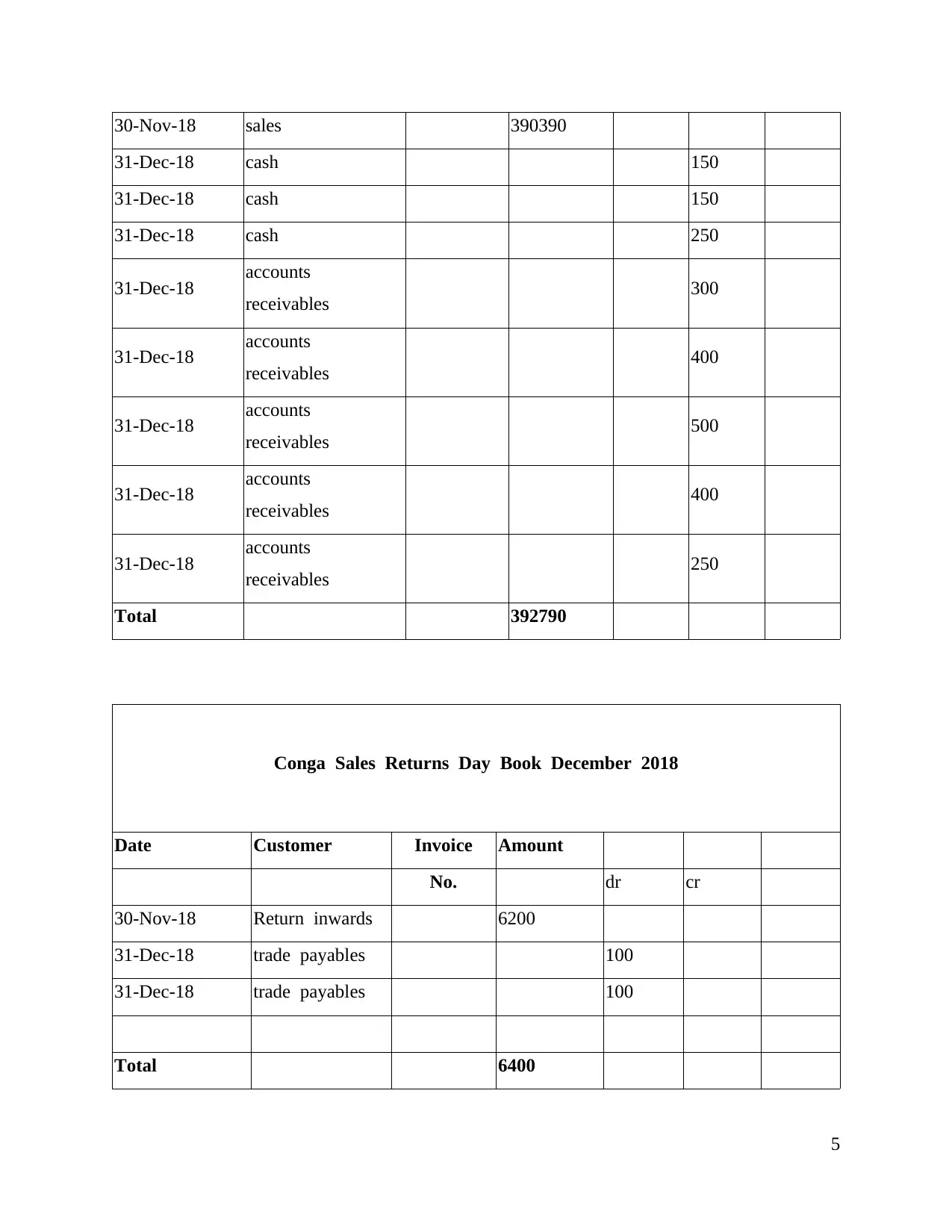

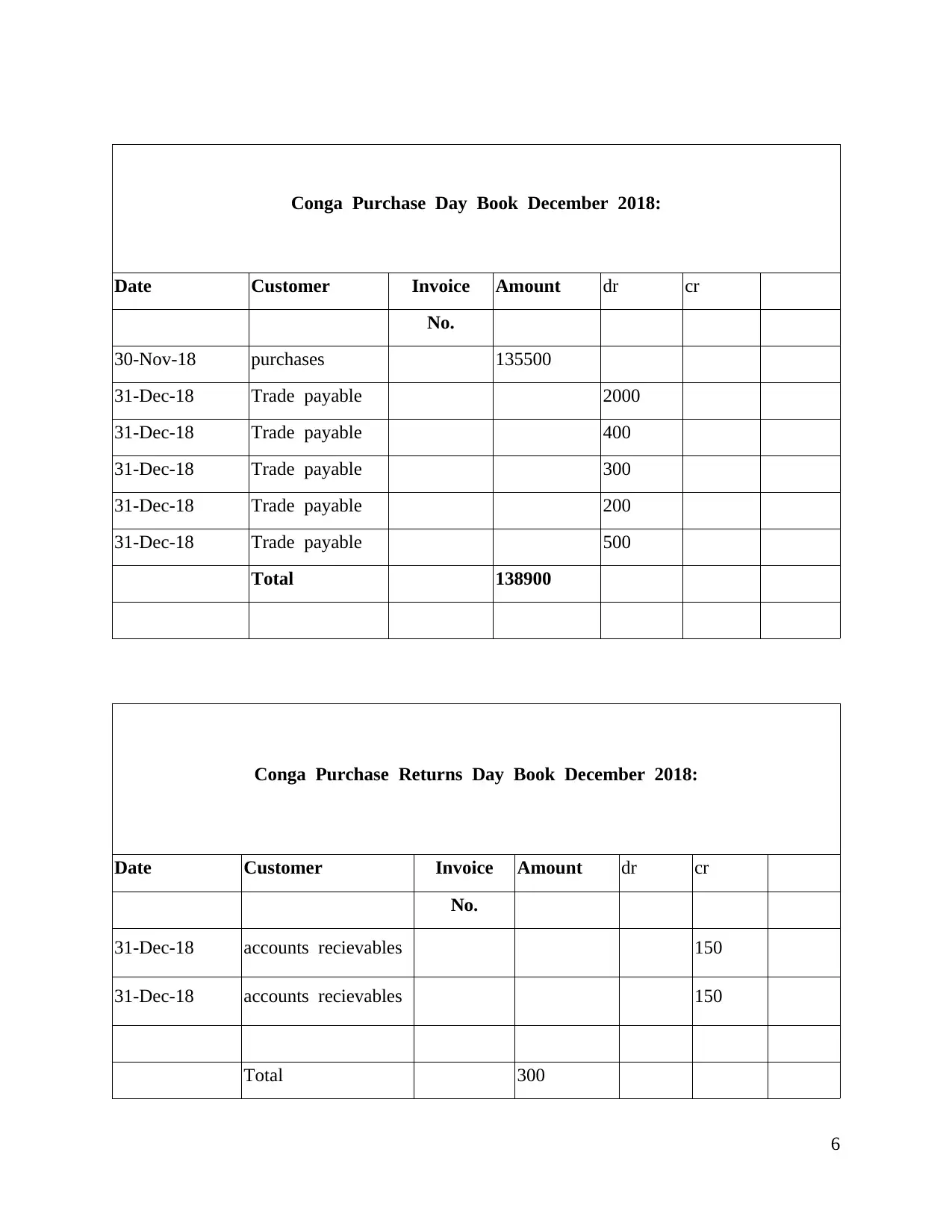

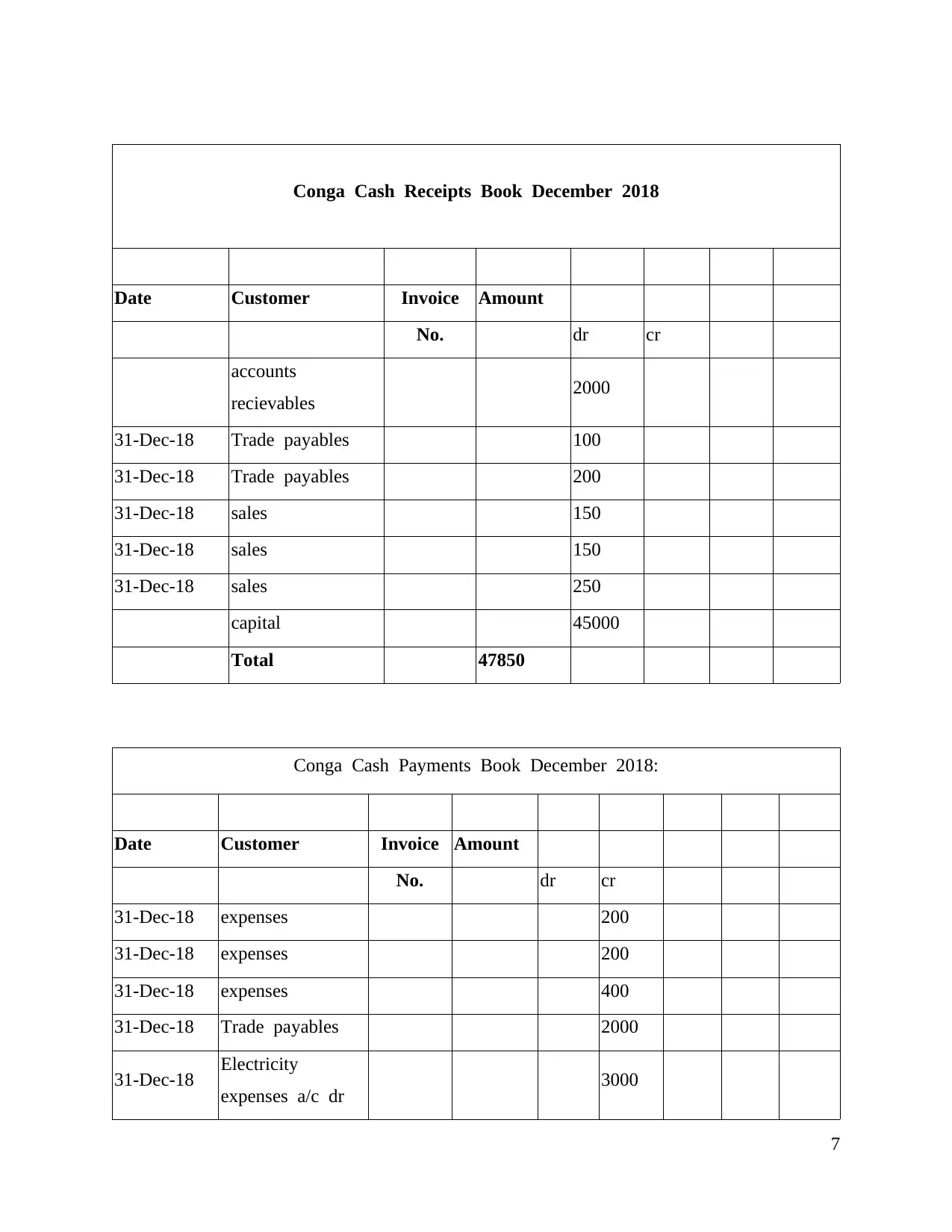

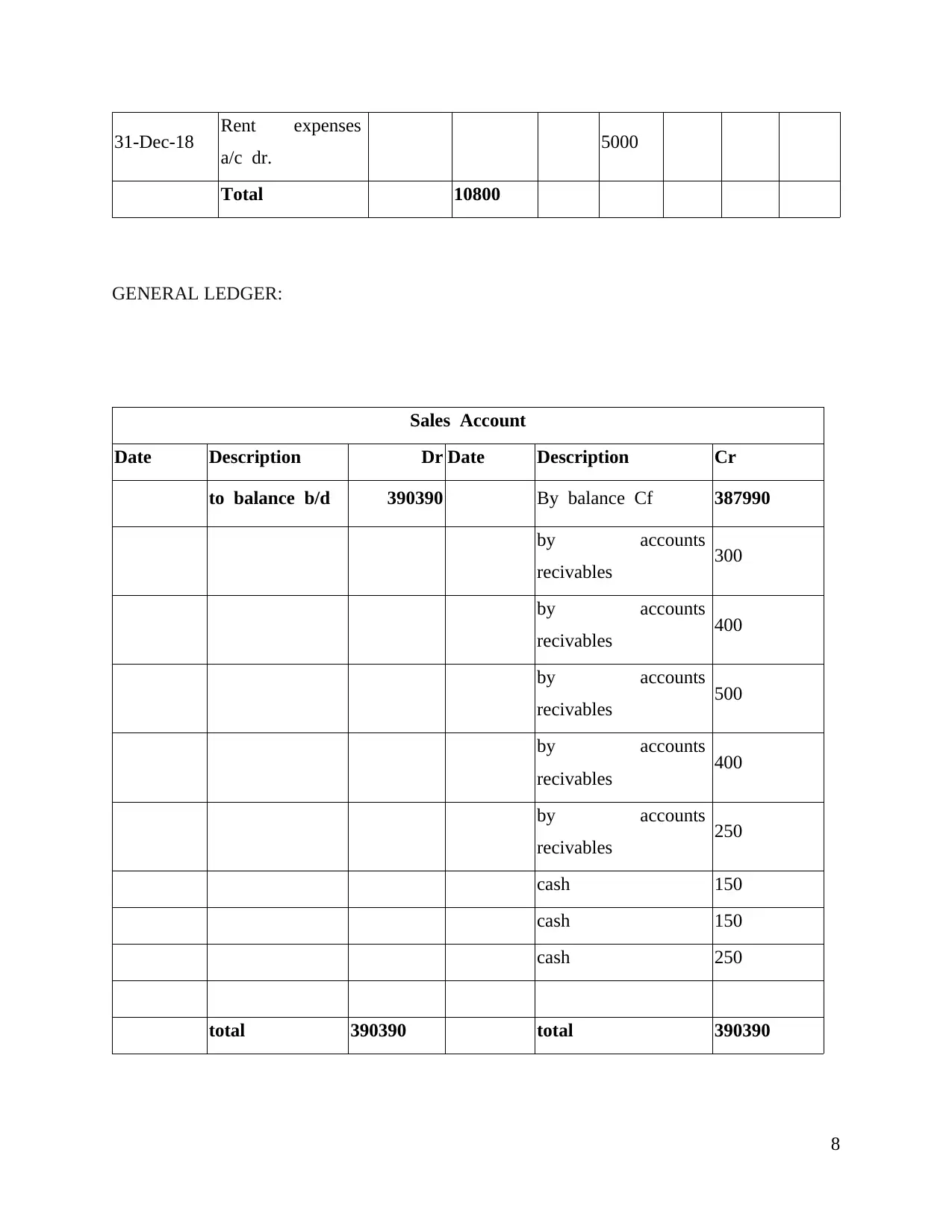

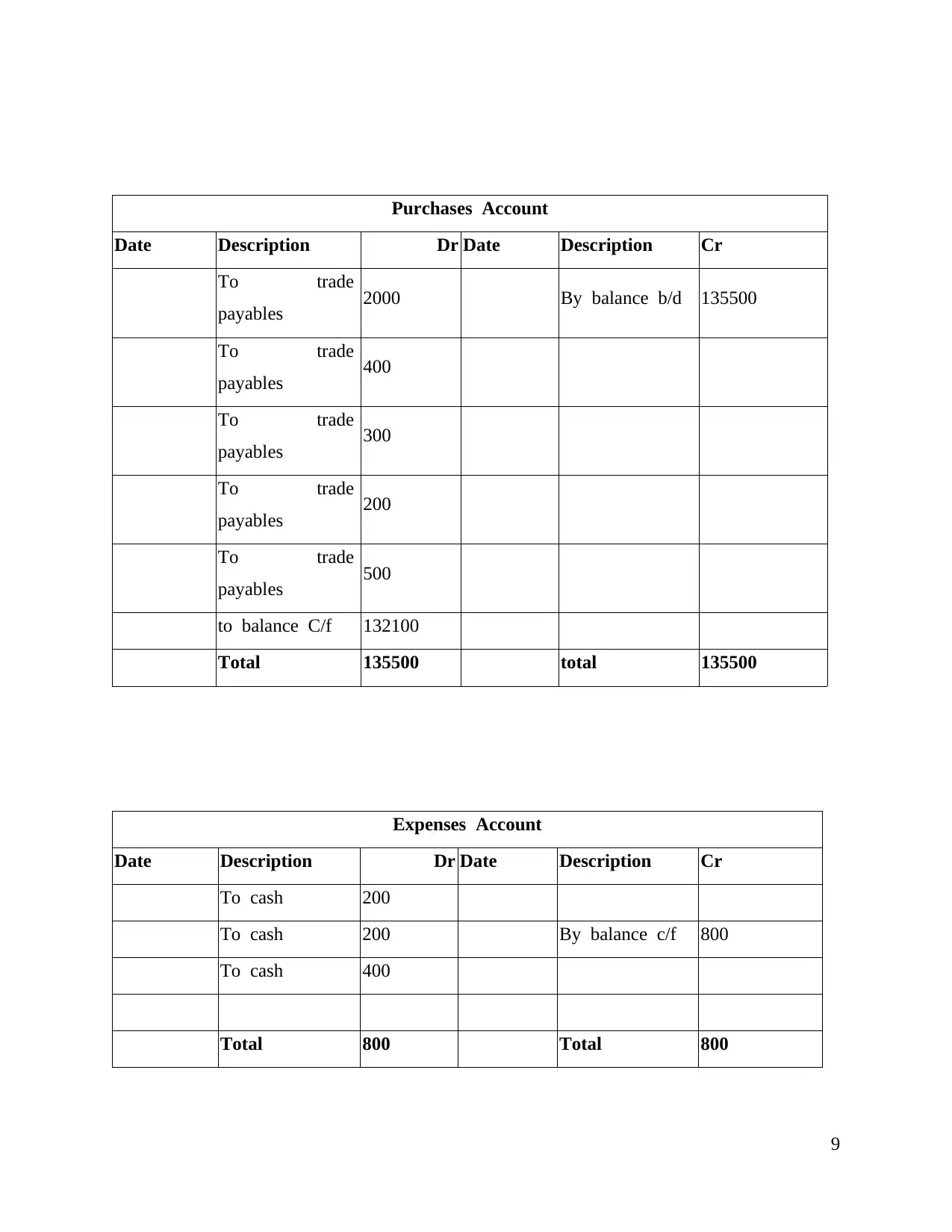

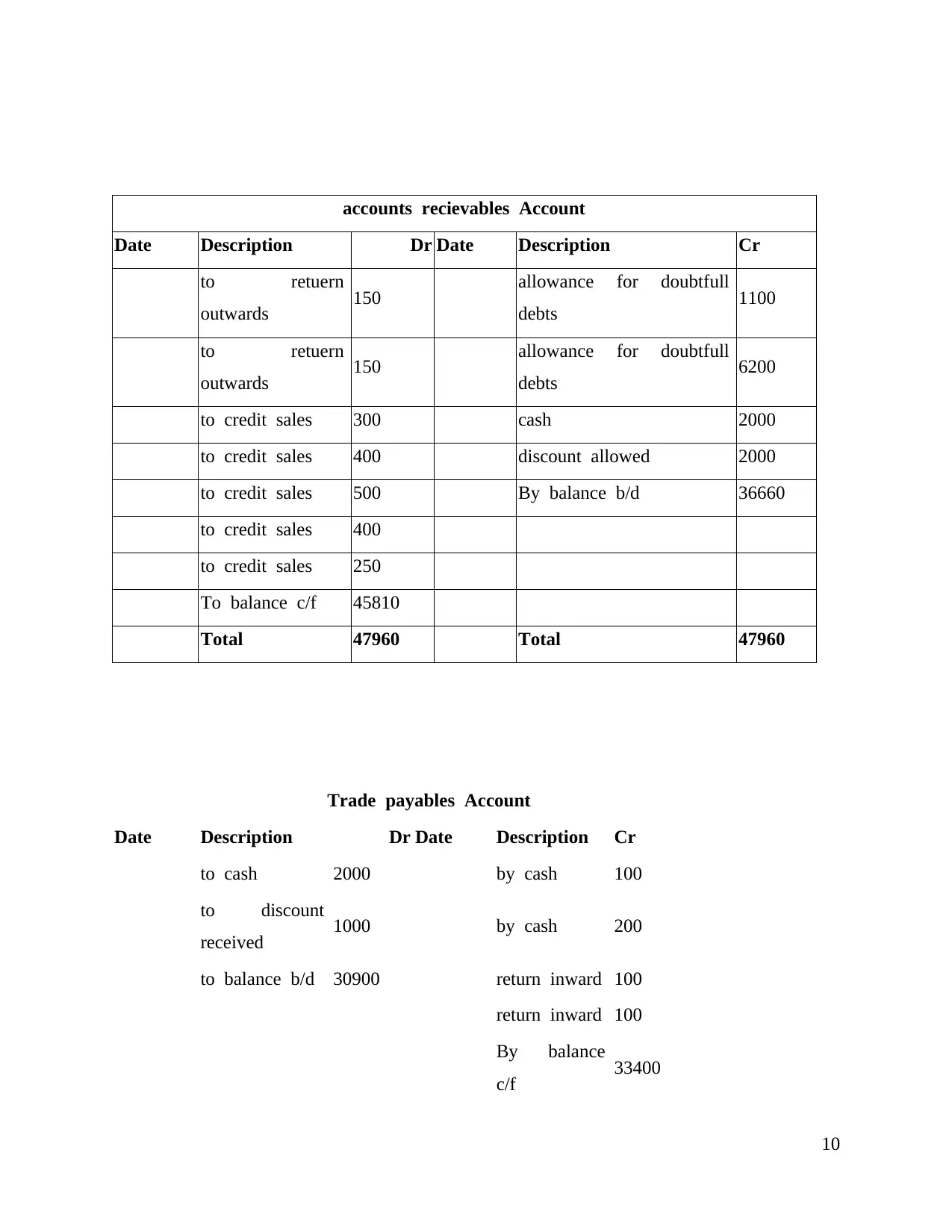

This assignment focuses on preparing and analyzing the accounting records and financial statements for Conga, a sole trader toy retailer. The assignment includes detailed journal entries for various transactions, such as credit purchases, sales, expenses, and loan activities. It also covers the preparation of sales day book, purchase day book, cash receipts and payments books, and general ledger accounts like sales, purchases, and expenses. Furthermore, the assignment addresses key accounting concepts like the prudent and accrual concepts. The solution also considers the potential impact of value-added tax (VAT) on Conga's accounting reports. The provided solution includes all the necessary financial statements and accounting records for the company. This assignment is contributed by a student to be published on the website Desklib. Desklib is a platform which provides all the necessary AI based study tools for students.

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.