Accounting Principles, Financial Analysis, and UK Regulatory Framework

VerifiedAdded on 2021/06/22

|17

|3289

|256

Homework Assignment

AI Summary

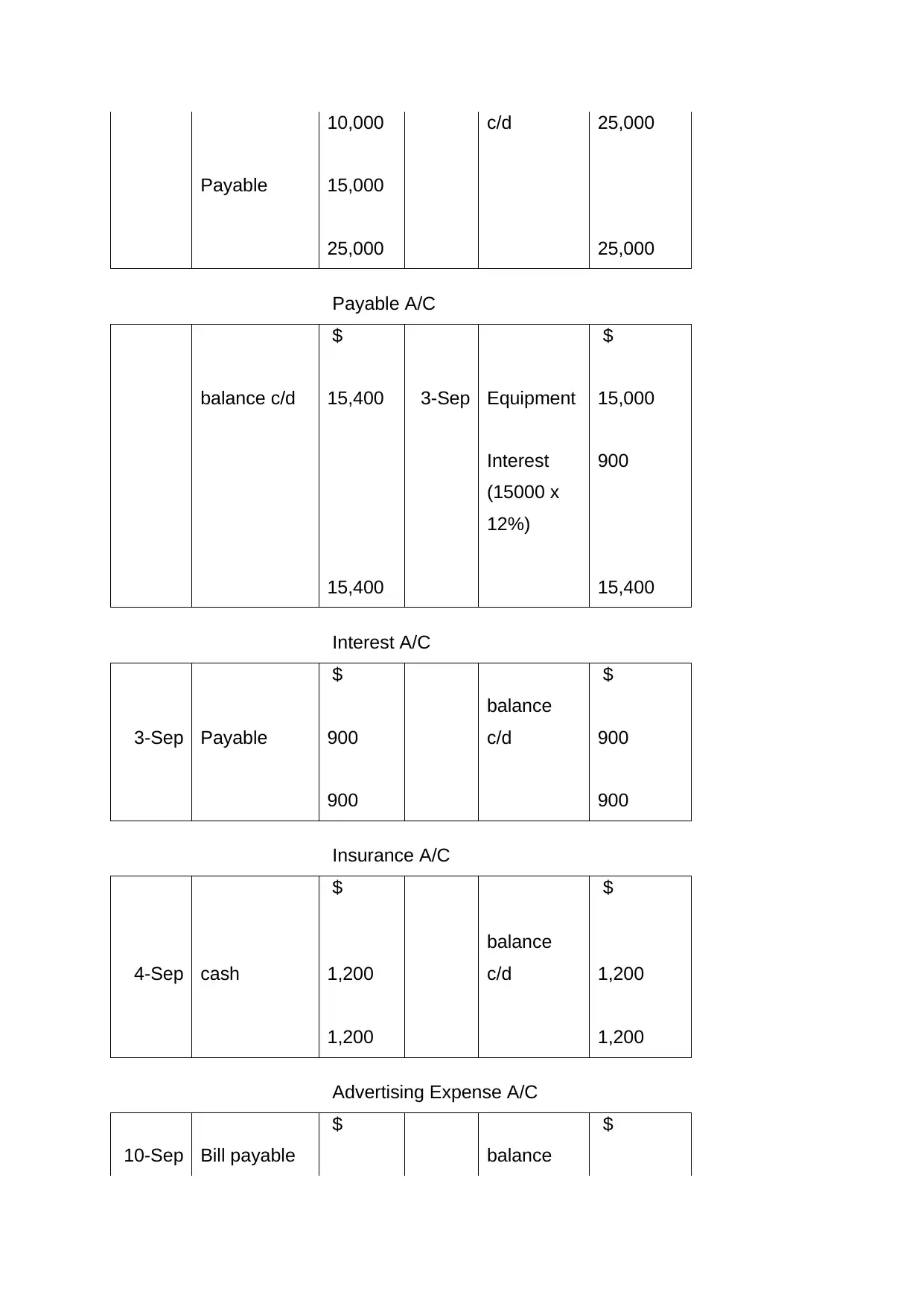

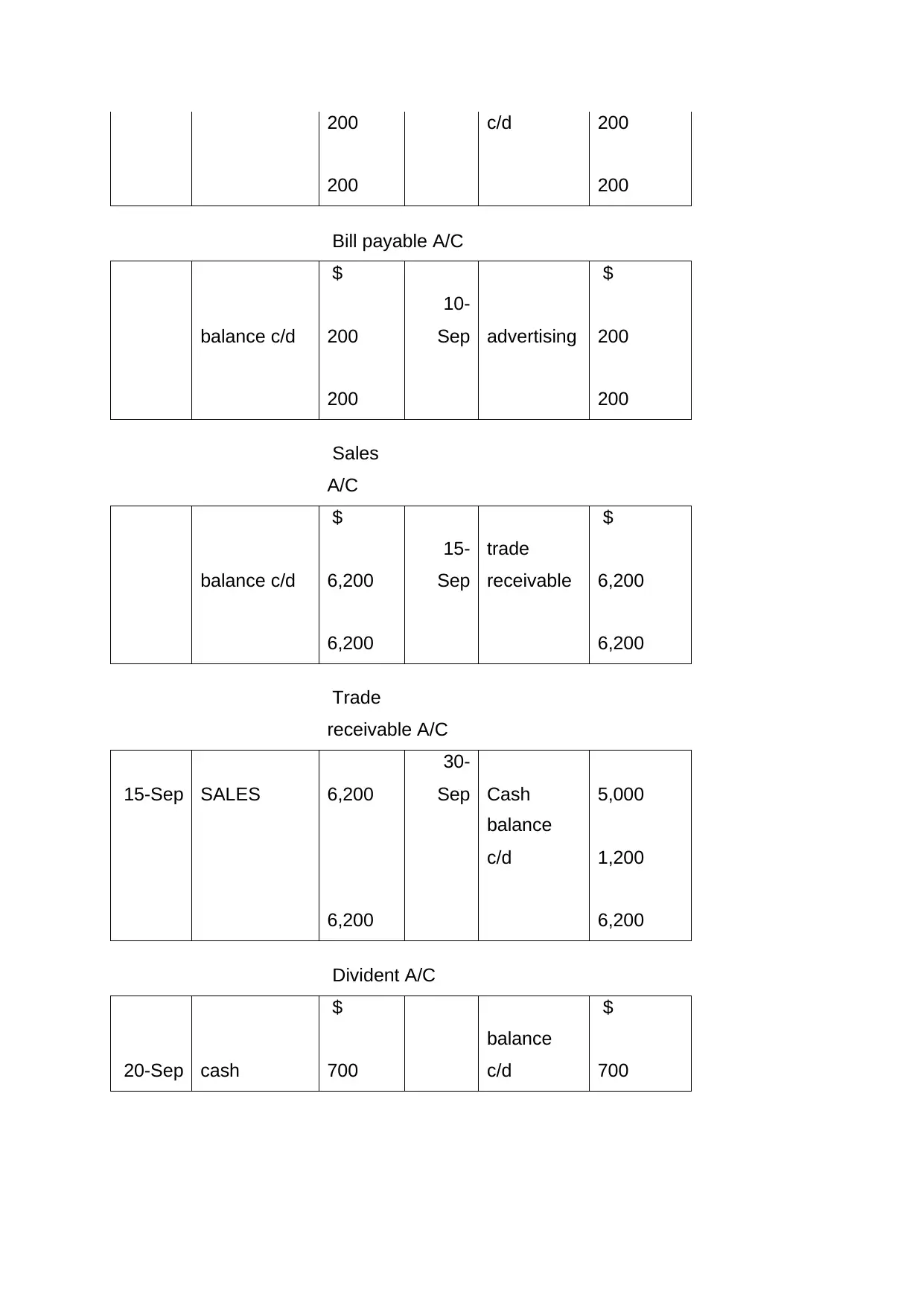

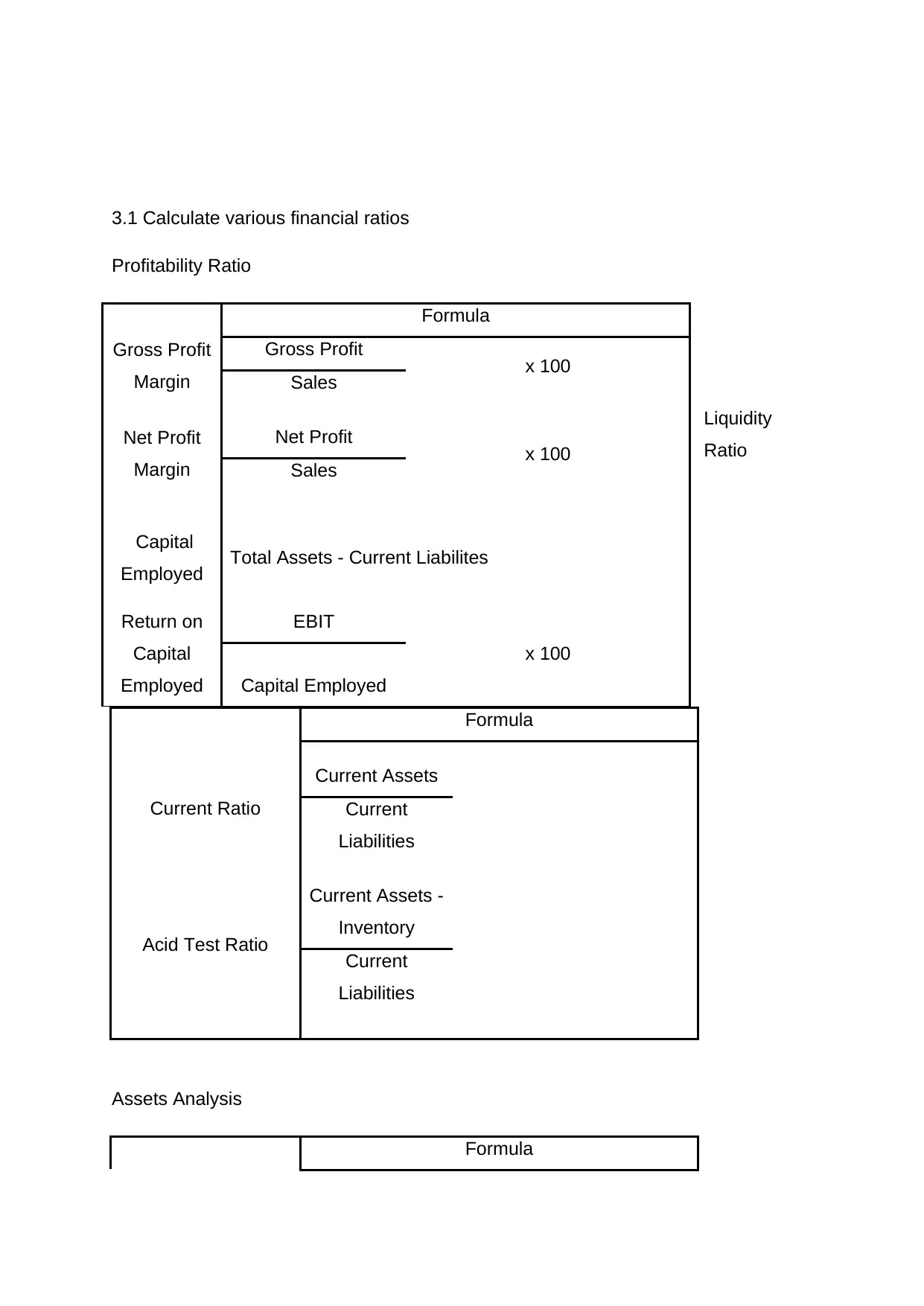

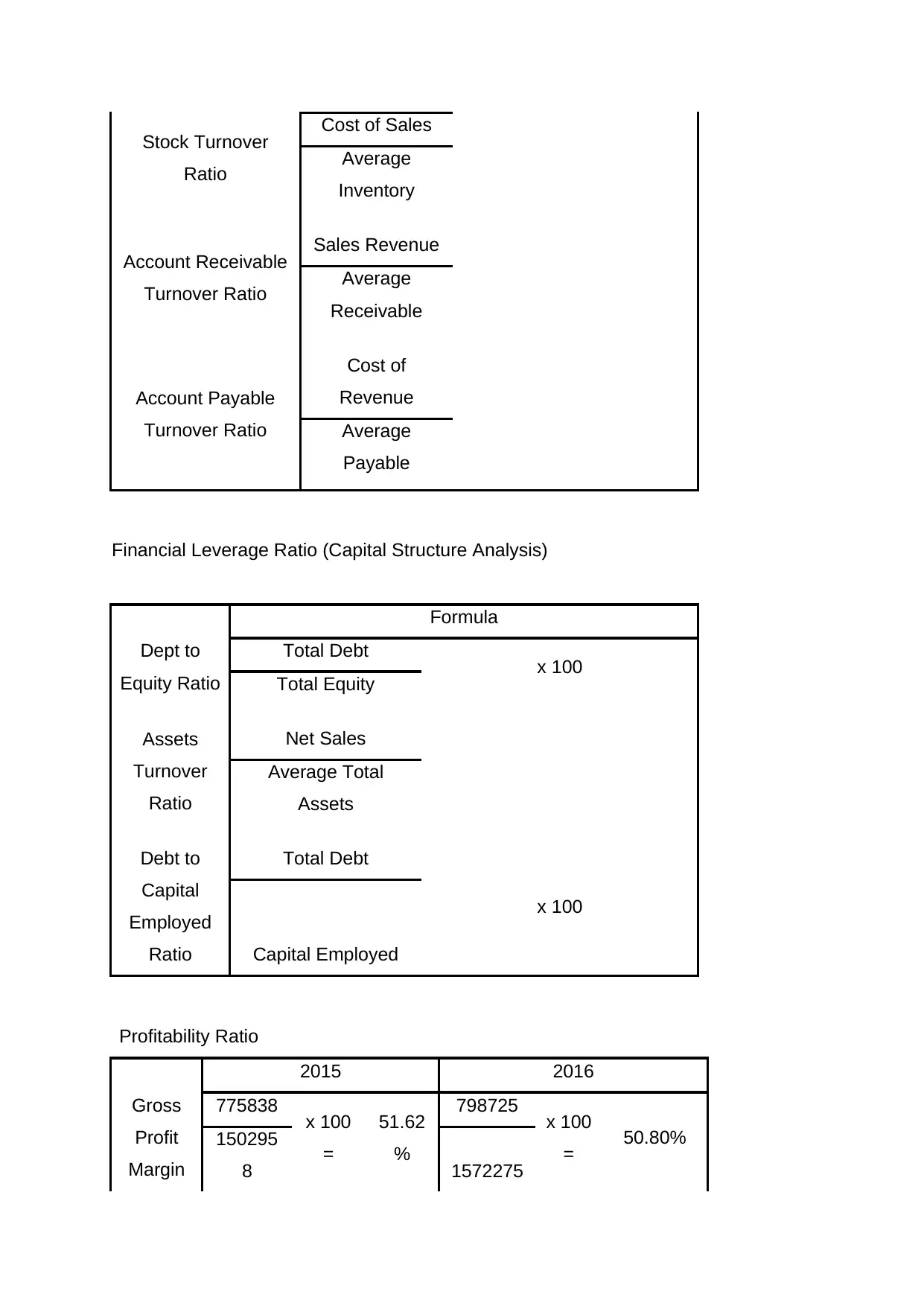

This accounting assignment solution covers several key areas within financial accounting. It begins by defining the purposes, aims, and regulations of financial and management accounting, as well as identifying different users of accounting information and the types of businesses. The solution then prepares books of original entry, a profit and loss account, and a balance sheet. It includes the construction of final accounts, adjustments for bookkeeping, and the preparation of cash flow statements. Furthermore, the assignment calculates various financial ratios, including profitability, liquidity, and asset analysis ratios, with a focus on the interpretation of these ratios. Finally, it explores the UK regulatory framework for accounting, providing a comprehensive overview of the topic.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.