Current Developments in Accounting Thought: Analysis Report

VerifiedAdded on 2020/03/16

|22

|3656

|394

Report

AI Summary

This report delves into current developments in accounting thought, examining the Financial Accounting Standards Board (FASB) and its exposure drafts related to employee share-based payments and stock compensation. It analyzes comment letters from various entities, including Heiskell and MacGillivray and Associates, Raytheon Company, and the American Bankers Association. The report outlines major issues covered in the exposure draft, assesses the behavior of regulators through the lens of public interest theory, and compares agreements and disagreements among the parties submitting comment letters. It further evaluates the arguments for and against regulation used by the authors of the comment letters and applies theories of regulation (Public interest, Capture theory, and Private interest) to the issues. The report also critically evaluates the underlying assumptions of these regulatory theories in the context of the exposure draft and comment letters. Furthermore, the report uses a case study of the KPMG audit of Rolls Royce, investigating bribery allegations, to illustrate the application of accounting regulations and theories.

Running head: CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

Current developments in accounting thought

Name of the Student:

Name of the University:

Author Note:

Current developments in accounting thought

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

Table of Contents

Question 1........................................................................................................................................4

Question 2........................................................................................................................................7

Executive Summary.........................................................................................................................7

Introduction......................................................................................................................................7

Part A...............................................................................................................................................9

Copy of Four selected Comment Letters.........................................................................................9

Heiskell and MacGillivray and Associates..............................................................................9

Raytheon Company................................................................................................................10

American Bankers Association..............................................................................................12

Part B.............................................................................................................................................12

Outlining the major issues covered in the Exposure Draft............................................................12

Part C.............................................................................................................................................13

Providing an in-depth assessment whether the behavior of regulator in introducing the Exposure

Draft can be explained by public interest theory...........................................................................13

Part D.............................................................................................................................................14

Describing in depth where there is agreement or disagreement between the parties who have

submitted Comment Letters...........................................................................................................14

Part E.............................................................................................................................................15

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

Table of Contents

Question 1........................................................................................................................................4

Question 2........................................................................................................................................7

Executive Summary.........................................................................................................................7

Introduction......................................................................................................................................7

Part A...............................................................................................................................................9

Copy of Four selected Comment Letters.........................................................................................9

Heiskell and MacGillivray and Associates..............................................................................9

Raytheon Company................................................................................................................10

American Bankers Association..............................................................................................12

Part B.............................................................................................................................................12

Outlining the major issues covered in the Exposure Draft............................................................12

Part C.............................................................................................................................................13

Providing an in-depth assessment whether the behavior of regulator in introducing the Exposure

Draft can be explained by public interest theory...........................................................................13

Part D.............................................................................................................................................14

Describing in depth where there is agreement or disagreement between the parties who have

submitted Comment Letters...........................................................................................................14

Part E.............................................................................................................................................15

3

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

Assessing whether the authors of the Comment Letters are utilizing the arguments for or against

regulation.......................................................................................................................................15

Part F..............................................................................................................................................15

Applying each of the theories of regulation (Public interest, Capture theory and Private interest)

to the various issues in the four selected comment letter and justifying which theory of regulation

best explains the comment on the issues.......................................................................................15

Part G.............................................................................................................................................17

Critically evaluate the underlying assumptions and assumptions of the theories of regulation with

regard to their application to the issues identified in the Exposure Draft and Comment Letters..17

Heiskell and MacGillivray and Associates................................................................................17

Raytheon Company...................................................................................................................17

Visa Inc......................................................................................................................................18

American Bankers Association..................................................................................................18

References and Bibliography.........................................................................................................20

Appendix........................................................................................................................................22

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

Assessing whether the authors of the Comment Letters are utilizing the arguments for or against

regulation.......................................................................................................................................15

Part F..............................................................................................................................................15

Applying each of the theories of regulation (Public interest, Capture theory and Private interest)

to the various issues in the four selected comment letter and justifying which theory of regulation

best explains the comment on the issues.......................................................................................15

Part G.............................................................................................................................................17

Critically evaluate the underlying assumptions and assumptions of the theories of regulation with

regard to their application to the issues identified in the Exposure Draft and Comment Letters..17

Heiskell and MacGillivray and Associates................................................................................17

Raytheon Company...................................................................................................................17

Visa Inc......................................................................................................................................18

American Bankers Association..................................................................................................18

References and Bibliography.........................................................................................................20

Appendix........................................................................................................................................22

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

Question 1

For this particular question, article is selected from “The Guardian” and the title is

“Accounting watchdog to investigate KPMG over Rolls-Royce audit”. The article is published

recently on 4th of May 2017. It is well understood that other articles are available that highlights

theoretical issues that leads to prohibited practices of some audit business that have an

undesirable effect on linked stakeholders of the specified business. The current article clearly

explains how accounting watchdog had investigated audit firms (KPMG) while auditing for

Rolls Royce (Zhang et al., 2016).

It is important to understand the fact that mainstream of business functioning in the

global market that have intention to increase the levels of profits. It requires implementation of

various company strategies that wins the confidence and trust of different stakeholders (Zeff,

2016). It is essential to win confidence and trust over the stakeholders that lead to enhancement

of business operations in the international business enterprise. This will lead to increasing the

growth rates as well as future cash flows at the same time. In this article, there was clear mention

about the process of Financial Reporting Council for reviewing the deal of Rolls Royce with

Serious Fraud Office that incurs £ 671 million for settling the allegations that leads to corruptive

activities. The issue had reached the public where FRC (Accounting watchdog of UK) had

properly takes initiatives for investigating into the KPMG audit with Rolls Royce (Ball, Grubnic

& Birchall, 2014). It was needed for investigating the case as there is involvement of engineering

group that sets for a bribery case with Serious Fraud Office for the year 2017.

On analysis, it is noted that Rolls Royce had made an agreement to incur £ 671 million

for settling long-term allegations of corruptions that is well-defined at the time of deferred

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

Question 1

For this particular question, article is selected from “The Guardian” and the title is

“Accounting watchdog to investigate KPMG over Rolls-Royce audit”. The article is published

recently on 4th of May 2017. It is well understood that other articles are available that highlights

theoretical issues that leads to prohibited practices of some audit business that have an

undesirable effect on linked stakeholders of the specified business. The current article clearly

explains how accounting watchdog had investigated audit firms (KPMG) while auditing for

Rolls Royce (Zhang et al., 2016).

It is important to understand the fact that mainstream of business functioning in the

global market that have intention to increase the levels of profits. It requires implementation of

various company strategies that wins the confidence and trust of different stakeholders (Zeff,

2016). It is essential to win confidence and trust over the stakeholders that lead to enhancement

of business operations in the international business enterprise. This will lead to increasing the

growth rates as well as future cash flows at the same time. In this article, there was clear mention

about the process of Financial Reporting Council for reviewing the deal of Rolls Royce with

Serious Fraud Office that incurs £ 671 million for settling the allegations that leads to corruptive

activities. The issue had reached the public where FRC (Accounting watchdog of UK) had

properly takes initiatives for investigating into the KPMG audit with Rolls Royce (Ball, Grubnic

& Birchall, 2014). It was needed for investigating the case as there is involvement of engineering

group that sets for a bribery case with Serious Fraud Office for the year 2017.

On analysis, it is noted that Rolls Royce had made an agreement to incur £ 671 million

for settling long-term allegations of corruptions that is well-defined at the time of deferred

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

examination (Miller & Power, 2013). Due to Brexit effect, there was high cost of settlement as

well as depreciation of pound value and this issues leads to yearly loss of more than 4.6 billion.

The loss incurred was the highest one for this business organization. FRC had taken initiation to

evaluate the KPMG audit in association with the financial statements for the company (Rolls

Royce) for the year 2010 and 2013. It was stated by the owner of KPMG that regulators have to

evaluate the issues that relates with public interest (Ball, Grubnic & Birchall, 2014). After

looking at the demand of KPMG, it can be stated that the audit work of Rolls Royce need to

carry out effectively with full care as well as due diligence that assures overall audit quality. It is

important to understand the fact that an apology had been made by Rolls Royce where they had

bribed the middlepersons for securing the orders in countries such as India, Indonesia, Nigeria as

well as China and Thailand. For instance, the company had paid £28 million to the

middlepersons in Thailand for getting access to few contracts (Meyer et al., 2013).

On evaluating the case, it is noted that Rolls Royce had bribed the SFO for settling the

fraud charges (Dillard, 2014). This action leads to contravention of public interest where SFO

concentrate mainly on defensive the events of business enterprise. Furthermore, the

middlepersons of the various nations had undertaken bribes in order to secure contracts of the

organization. Rolls Royce wanted that their competitors should not enter in the market and this

was treated as unscrupulous measures. There is direct intervention of FRC who was responsible

for investigating the market due to allegations and applied stringest regulations on the audit

business for evaluating as well as disclosing the financial statements in an effective way

(Klinglmair, Sala & Brandão, 2014).

The reputational theory explains the fact where the investors prefer in dealing with such

business enterprise that has strong reputation in the market and aligns with the efficient growth

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

examination (Miller & Power, 2013). Due to Brexit effect, there was high cost of settlement as

well as depreciation of pound value and this issues leads to yearly loss of more than 4.6 billion.

The loss incurred was the highest one for this business organization. FRC had taken initiation to

evaluate the KPMG audit in association with the financial statements for the company (Rolls

Royce) for the year 2010 and 2013. It was stated by the owner of KPMG that regulators have to

evaluate the issues that relates with public interest (Ball, Grubnic & Birchall, 2014). After

looking at the demand of KPMG, it can be stated that the audit work of Rolls Royce need to

carry out effectively with full care as well as due diligence that assures overall audit quality. It is

important to understand the fact that an apology had been made by Rolls Royce where they had

bribed the middlepersons for securing the orders in countries such as India, Indonesia, Nigeria as

well as China and Thailand. For instance, the company had paid £28 million to the

middlepersons in Thailand for getting access to few contracts (Meyer et al., 2013).

On evaluating the case, it is noted that Rolls Royce had bribed the SFO for settling the

fraud charges (Dillard, 2014). This action leads to contravention of public interest where SFO

concentrate mainly on defensive the events of business enterprise. Furthermore, the

middlepersons of the various nations had undertaken bribes in order to secure contracts of the

organization. Rolls Royce wanted that their competitors should not enter in the market and this

was treated as unscrupulous measures. There is direct intervention of FRC who was responsible

for investigating the market due to allegations and applied stringest regulations on the audit

business for evaluating as well as disclosing the financial statements in an effective way

(Klinglmair, Sala & Brandão, 2014).

The reputational theory explains the fact where the investors prefer in dealing with such

business enterprise that has strong reputation in the market and aligns with the efficient growth

6

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

financials. In addition, the cost-benefit analysis over long-term shows dishonest actions that does

not take place that aligns with the organizational interests (Ball, Grubnic & Birchall, 2014).

Some long-term actions take place where dishonest behavior is likely to occur for obtaining

short-term benefits. As far as Rolls Royce is concerned, the business has made a corrupt practice

with SFO for resolving its bribery compulsion. Furthermore, the main purpose was to maintain

the faith levels with the shareholder for accumulating greater funds especially at the time of

funding capital projects. From the annual report of Rolls Royce for the year 2010 to 2013, it is

noted that the figures are misstated that enables the company for gathering sufficient funds from

the investors to undertake new contracts (Deegan, 2016).

It is recommended to the company to carry out their operational progress in the short-run.

It was due to this reason why the company incurs loss as there was loss in the confidence of the

investors. Furthermore, the allegations imposes the company to be identical with reputational as

well as public interest theories that explains the requirements for applying stringest regulations

for given audit business enterprise (Deegan, 2013).

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

financials. In addition, the cost-benefit analysis over long-term shows dishonest actions that does

not take place that aligns with the organizational interests (Ball, Grubnic & Birchall, 2014).

Some long-term actions take place where dishonest behavior is likely to occur for obtaining

short-term benefits. As far as Rolls Royce is concerned, the business has made a corrupt practice

with SFO for resolving its bribery compulsion. Furthermore, the main purpose was to maintain

the faith levels with the shareholder for accumulating greater funds especially at the time of

funding capital projects. From the annual report of Rolls Royce for the year 2010 to 2013, it is

noted that the figures are misstated that enables the company for gathering sufficient funds from

the investors to undertake new contracts (Deegan, 2016).

It is recommended to the company to carry out their operational progress in the short-run.

It was due to this reason why the company incurs loss as there was loss in the confidence of the

investors. Furthermore, the allegations imposes the company to be identical with reputational as

well as public interest theories that explains the requirements for applying stringest regulations

for given audit business enterprise (Deegan, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

Question 2

Executive Summary

The main aim of the assignment is to assess the development application about Financial

Accounting Standards Board that relates directly with employee payment share-based accounting

as well as stock of compensation. In addition, there are main four respondents who are

responsible for providing comments on the exposure draft. Furthermore, the study of this section

highlights that the excess tax benefits and realizes the shortage as mentioned in the income

statement that are not undertaken. Therefore, the balanced fairness approach introduces facts that

minimize the volatility expenses that are mentioned in the income statement. The main objective

of the assignment is to reduce cost as well as complexity for bringing improvements in the

accounting for share-based payments that are issued to employees mainly for the public as well

as private companies. FASB affirms with the proposed changes that aligns with the accounting

for share-based payments as issued to employees in areas such as accounting for income taxes

that gets along with vesting or resolution of awards, presenting excess tax benefits as shown in

the cash flow statement, accounting for forfeitures, presenting employee taxes paid as shown in

the cash flow statement when an employer withholds shares for meeting minimum legislative

necessities as well as minimum statutory requirements.

Introduction

This section deals with introducing FASB and recommending different accounting

standards that allows exposure drafts and comments that are published by industries and

corporate business enterprises (Ball, Grubnic & Birchall, 2014). This particular proposal takes

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

Question 2

Executive Summary

The main aim of the assignment is to assess the development application about Financial

Accounting Standards Board that relates directly with employee payment share-based accounting

as well as stock of compensation. In addition, there are main four respondents who are

responsible for providing comments on the exposure draft. Furthermore, the study of this section

highlights that the excess tax benefits and realizes the shortage as mentioned in the income

statement that are not undertaken. Therefore, the balanced fairness approach introduces facts that

minimize the volatility expenses that are mentioned in the income statement. The main objective

of the assignment is to reduce cost as well as complexity for bringing improvements in the

accounting for share-based payments that are issued to employees mainly for the public as well

as private companies. FASB affirms with the proposed changes that aligns with the accounting

for share-based payments as issued to employees in areas such as accounting for income taxes

that gets along with vesting or resolution of awards, presenting excess tax benefits as shown in

the cash flow statement, accounting for forfeitures, presenting employee taxes paid as shown in

the cash flow statement when an employer withholds shares for meeting minimum legislative

necessities as well as minimum statutory requirements.

Introduction

This section deals with introducing FASB and recommending different accounting

standards that allows exposure drafts and comments that are published by industries and

corporate business enterprises (Ball, Grubnic & Birchall, 2014). This particular proposal takes

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

into account accounting standards for updating the stock-based compensation and it has the topic

number of 718. The mentioned standard title is Improvements of Non-employee share-based

payment accounting (Klinglmair, Sala & Brandão, 2014). It is important to bring improvements

in the non-staff share payment that assures proper reduction of cost. Furthermore, there are

different complexities present that maintain accurate information of financial users that are

mentioned in the financial statements of business enterprise. Therefore, the section mainly

concentrates upon different agreed and non-agreed comments for initiating such standard for

bringing improvements in the procedure of accounting in the most appropriate way. This section

mainly emphasizes upon facts after recommending various important accounting standards as it

updates stock based compensation for improving the procedure of accounting for ascertaining its

idealness (Christ & Burritt, 2015).

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

into account accounting standards for updating the stock-based compensation and it has the topic

number of 718. The mentioned standard title is Improvements of Non-employee share-based

payment accounting (Klinglmair, Sala & Brandão, 2014). It is important to bring improvements

in the non-staff share payment that assures proper reduction of cost. Furthermore, there are

different complexities present that maintain accurate information of financial users that are

mentioned in the financial statements of business enterprise. Therefore, the section mainly

concentrates upon different agreed and non-agreed comments for initiating such standard for

bringing improvements in the procedure of accounting in the most appropriate way. This section

mainly emphasizes upon facts after recommending various important accounting standards as it

updates stock based compensation for improving the procedure of accounting for ascertaining its

idealness (Christ & Burritt, 2015).

9

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

Part A

Copy of Four selected Comment Letters

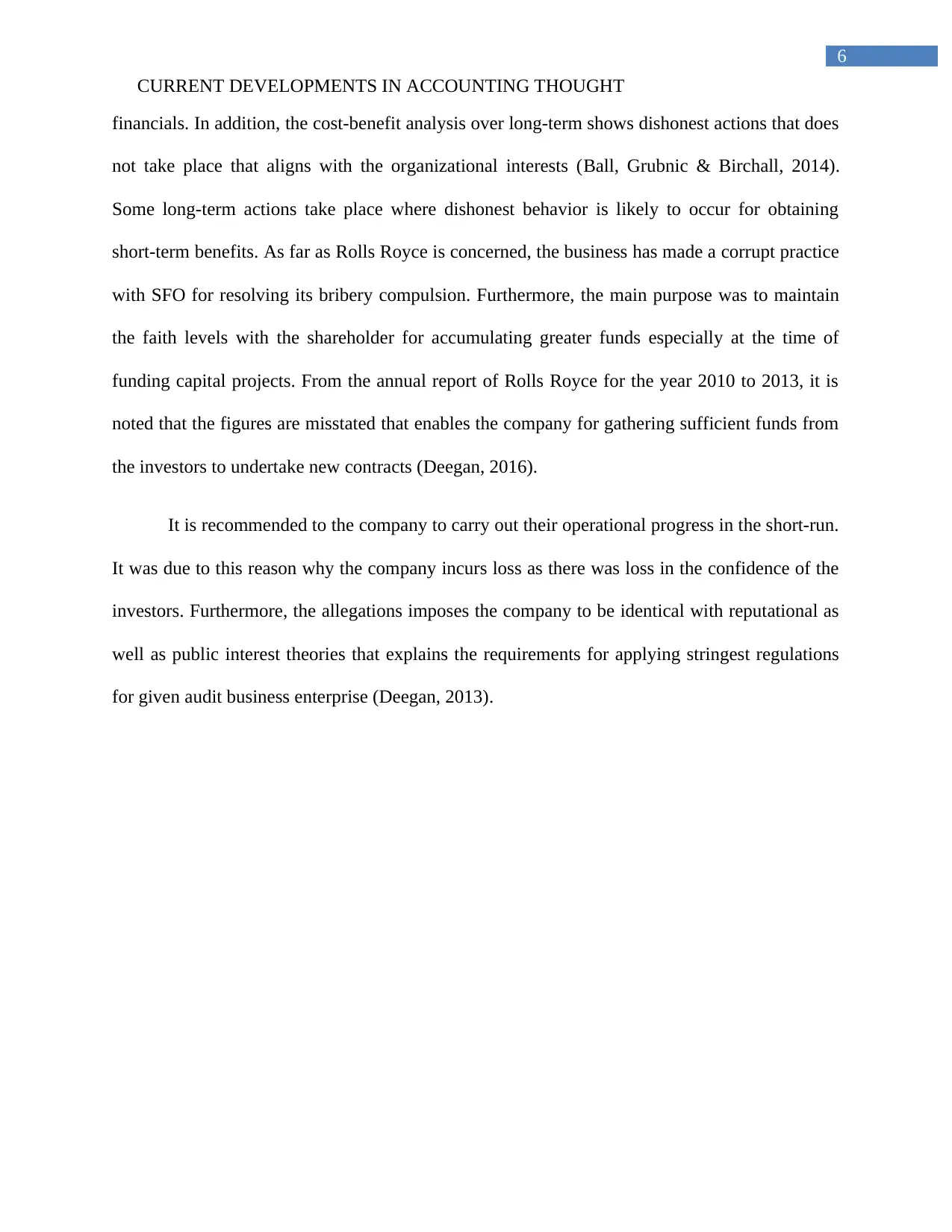

Heiskell and MacGillivray and Associates

Figure: Comment Letters (Financial Accounting Standards Board) of Heiskell and

MacGillivray and Associates

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

Part A

Copy of Four selected Comment Letters

Heiskell and MacGillivray and Associates

Figure: Comment Letters (Financial Accounting Standards Board) of Heiskell and

MacGillivray and Associates

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

Raytheon Company

Figure: Exposure Draft- Stock Compensation Topic 718- Improvements to Employee

Share-Based Payment Accounting

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

Raytheon Company

Figure: Exposure Draft- Stock Compensation Topic 718- Improvements to Employee

Share-Based Payment Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

Visa Inc

Figure: Request for comments on Exposure Draft of Proposed Accounting Standards

Update on Compensation – Stock Compensation (Topic 718), or “the proposed update”

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

Visa Inc

Figure: Request for comments on Exposure Draft of Proposed Accounting Standards

Update on Compensation – Stock Compensation (Topic 718), or “the proposed update”

12

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

American Bankers Association

Figure: IASB Exposure Draft 2015/3 - Conceptual Framework for Financial Reporting

Association

Part B

Outlining the major issues covered in the Exposure Draft

From the IASB and Conceptual Framework, it properly explains about measurement

bases in the Chapter 6. It discuss about various measurement bases and information that it

provided with relevant benefits and limitations. The section even determines the factors that need

to be considered at the time of selecting based on measurement. In the Exposure Draft, there is

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

American Bankers Association

Figure: IASB Exposure Draft 2015/3 - Conceptual Framework for Financial Reporting

Association

Part B

Outlining the major issues covered in the Exposure Draft

From the IASB and Conceptual Framework, it properly explains about measurement

bases in the Chapter 6. It discuss about various measurement bases and information that it

provided with relevant benefits and limitations. The section even determines the factors that need

to be considered at the time of selecting based on measurement. In the Exposure Draft, there is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.