Introduction to Accounting and Finance Report: Analysis and Evaluation

VerifiedAdded on 2023/01/07

|17

|4144

|22

Report

AI Summary

This report provides an overview of key accounting and finance concepts. It begins with the preparation of financial statements, including an income statement and balance sheet, for Collins Colman Limited. The report then delves into break-even analysis and margin of safety calculations for Parksmead Limited, examining the impact of changes in selling price and quantity. Finally, the report assesses investment appraisal techniques, such as payback period, accounting rate of return (ARR), and net present value (NPV), to determine whether Skipsey Clifford Plc. should purchase new machinery, along with the merits and demerits of each technique and the benefits and limitations of budgeting for strategic planning. The report concludes with a recommendation based on the analysis and evaluation of the investment appraisal techniques.

Introduction to Accounting and Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Part A – Collins Colman Limited....................................................................................................1

a. Income statement.....................................................................................................................1

b. Balance sheet...........................................................................................................................2

Part B – Parks mead Limited...........................................................................................................3

a. Calculate the contribution of each microwave.........................................................................3

b. Calculate the break-even point and margin of safety..............................................................4

c. Calculate the profit of Parks mead Limited.............................................................................5

d. Selling price increased by 8% and quantity 15%....................................................................5

e. Explain the underpinning assumptions attached to the break-even model..............................6

Part C – Skipsey Clifford Plc...........................................................................................................6

a. By using investment appraisal technique, calculate several aspect and recommend that

company should purchase this machinery or not.........................................................................6

b. Explain and analyse the key merits or demerits of different investment appraisal technique.9

c. Explain the key benefits or limitations of using budgeting as a tool for strategic planning..11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

MAIN BODY..................................................................................................................................1

Part A – Collins Colman Limited....................................................................................................1

a. Income statement.....................................................................................................................1

b. Balance sheet...........................................................................................................................2

Part B – Parks mead Limited...........................................................................................................3

a. Calculate the contribution of each microwave.........................................................................3

b. Calculate the break-even point and margin of safety..............................................................4

c. Calculate the profit of Parks mead Limited.............................................................................5

d. Selling price increased by 8% and quantity 15%....................................................................5

e. Explain the underpinning assumptions attached to the break-even model..............................6

Part C – Skipsey Clifford Plc...........................................................................................................6

a. By using investment appraisal technique, calculate several aspect and recommend that

company should purchase this machinery or not.........................................................................6

b. Explain and analyse the key merits or demerits of different investment appraisal technique.9

c. Explain the key benefits or limitations of using budgeting as a tool for strategic planning..11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Accounting is a method of tracking and documenting a firm's financial transactions. Finance

is the concept behind a company's asset control. Financial accounting, cost accounting, expense

control, tax planning etc. is the branches of accounting (Aiken, Lu and Ji, 2013). The distinction

among accounting and finance is that accounting deals on the daily basis movement of funds

inside and beyond a company or entity, while finance is a wider concept for wealth and liabilities

strategy and innovation successful marketing. Investors will use financial reports to gain useful

knowledge that has been used in businesses' assessment and debt research. Accounting

information allows analysts to assess the worth of an asset, identify the financing streams of a

company, measure performance, and quantify risks inherent in a balance sheet of a company.

This report based on several concepts of accounting and finance, this assessment classify in

three parts. First part is based on the preparation of income statement or balance sheet of Collins

Colman Ltd, another one is about calculating breakeven point or margin or safety of Parksmead

Limited Company. In addition, last part of this report based on the assessment of investment

appraisal techniques which helps the Skipsey Plc to identify whether they purchase new

machinery or not.

MAIN BODY

Part A – Collins Colman Limited

a. Income statement

This is also defined as the declaration of benefit and loss or the declaration of profits and

cost, the statement of income generally reflects on the sales and expenditures of the company

over a given period (Ainsworth and Deines, 2019). Below mention income statement provide

better understanding.

Income statement for the year ended

Particulars Details Amount

Sales revenues £759600

Less: cost of sale -£356400

£403200

1

Accounting is a method of tracking and documenting a firm's financial transactions. Finance

is the concept behind a company's asset control. Financial accounting, cost accounting, expense

control, tax planning etc. is the branches of accounting (Aiken, Lu and Ji, 2013). The distinction

among accounting and finance is that accounting deals on the daily basis movement of funds

inside and beyond a company or entity, while finance is a wider concept for wealth and liabilities

strategy and innovation successful marketing. Investors will use financial reports to gain useful

knowledge that has been used in businesses' assessment and debt research. Accounting

information allows analysts to assess the worth of an asset, identify the financing streams of a

company, measure performance, and quantify risks inherent in a balance sheet of a company.

This report based on several concepts of accounting and finance, this assessment classify in

three parts. First part is based on the preparation of income statement or balance sheet of Collins

Colman Ltd, another one is about calculating breakeven point or margin or safety of Parksmead

Limited Company. In addition, last part of this report based on the assessment of investment

appraisal techniques which helps the Skipsey Plc to identify whether they purchase new

machinery or not.

MAIN BODY

Part A – Collins Colman Limited

a. Income statement

This is also defined as the declaration of benefit and loss or the declaration of profits and

cost, the statement of income generally reflects on the sales and expenditures of the company

over a given period (Ainsworth and Deines, 2019). Below mention income statement provide

better understanding.

Income statement for the year ended

Particulars Details Amount

Sales revenues £759600

Less: cost of sale -£356400

£403200

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

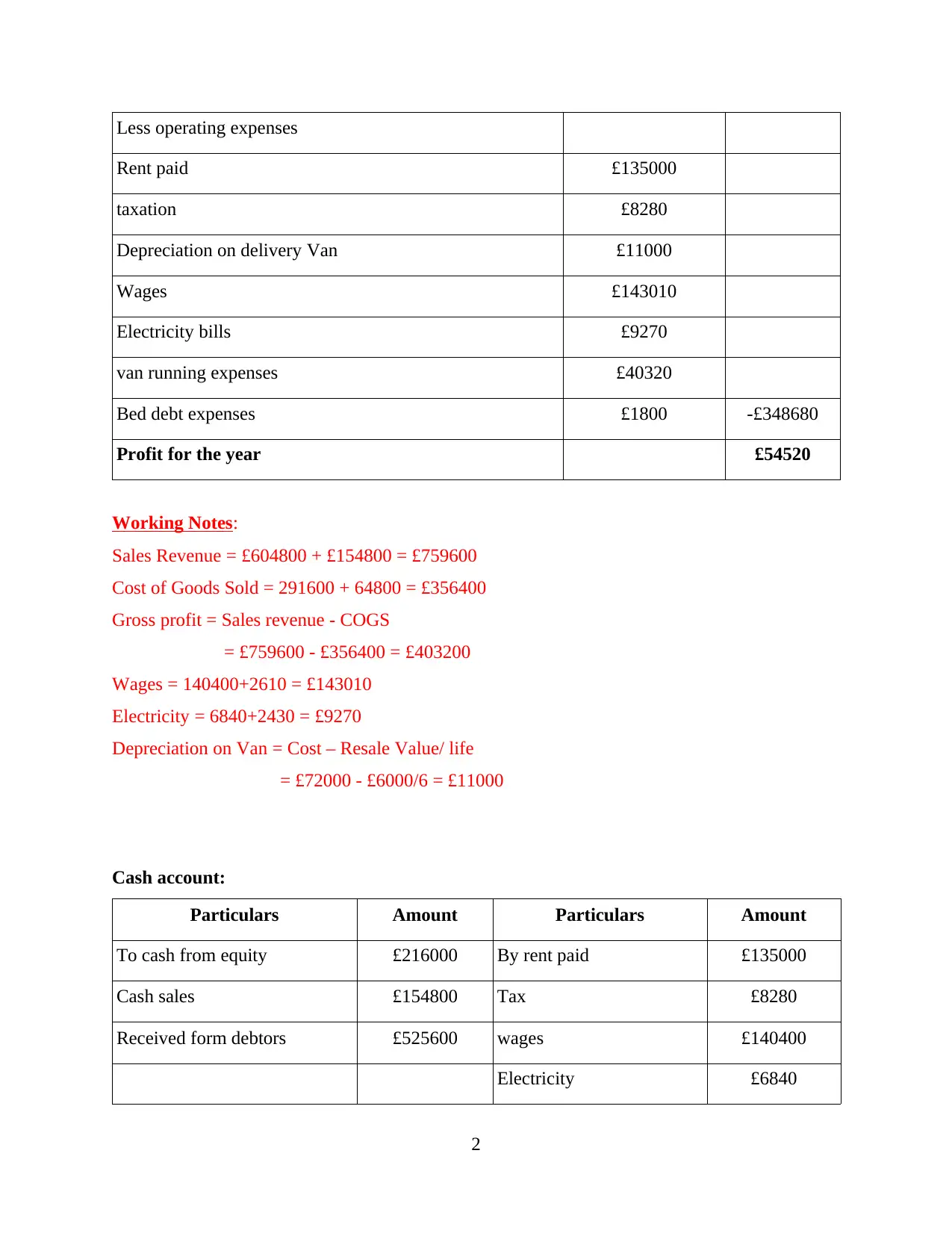

Less operating expenses

Rent paid £135000

taxation £8280

Depreciation on delivery Van £11000

Wages £143010

Electricity bills £9270

van running expenses £40320

Bed debt expenses £1800 -£348680

Profit for the year £54520

Working Notes:

Sales Revenue = £604800 + £154800 = £759600

Cost of Goods Sold = 291600 + 64800 = £356400

Gross profit = Sales revenue - COGS

= £759600 - £356400 = £403200

Wages = 140400+2610 = £143010

Electricity = 6840+2430 = £9270

Depreciation on Van = Cost – Resale Value/ life

= £72000 - £6000/6 = £11000

Cash account:

Particulars Amount Particulars Amount

To cash from equity £216000 By rent paid £135000

Cash sales £154800 Tax £8280

Received form debtors £525600 wages £140400

Electricity £6840

2

Rent paid £135000

taxation £8280

Depreciation on delivery Van £11000

Wages £143010

Electricity bills £9270

van running expenses £40320

Bed debt expenses £1800 -£348680

Profit for the year £54520

Working Notes:

Sales Revenue = £604800 + £154800 = £759600

Cost of Goods Sold = 291600 + 64800 = £356400

Gross profit = Sales revenue - COGS

= £759600 - £356400 = £403200

Wages = 140400+2610 = £143010

Electricity = 6840+2430 = £9270

Depreciation on Van = Cost – Resale Value/ life

= £72000 - £6000/6 = £11000

Cash account:

Particulars Amount Particulars Amount

To cash from equity £216000 By rent paid £135000

Cash sales £154800 Tax £8280

Received form debtors £525600 wages £140400

Electricity £6840

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

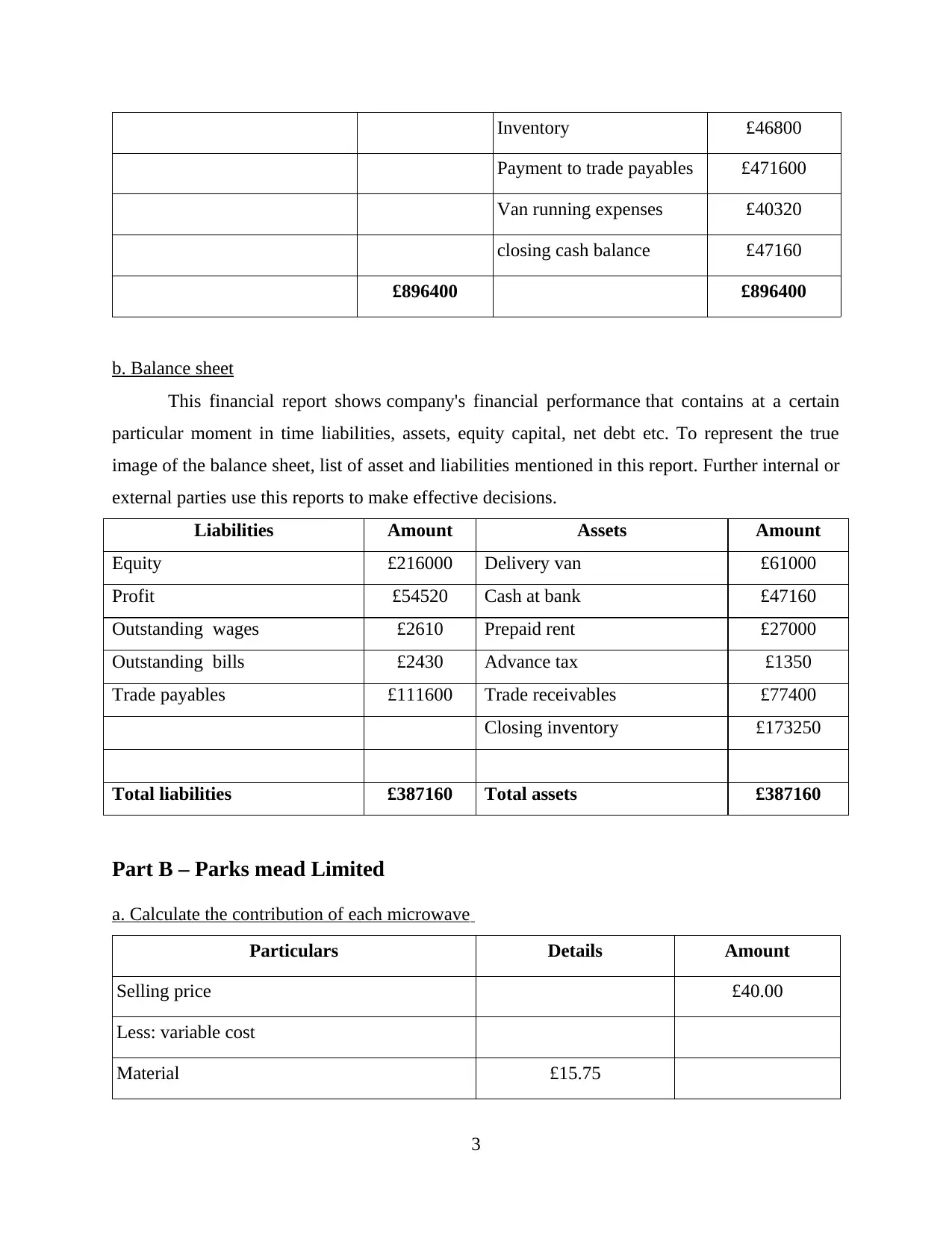

Inventory £46800

Payment to trade payables £471600

Van running expenses £40320

closing cash balance £47160

£896400 £896400

b. Balance sheet

This financial report shows company's financial performance that contains at a certain

particular moment in time liabilities, assets, equity capital, net debt etc. To represent the true

image of the balance sheet, list of asset and liabilities mentioned in this report. Further internal or

external parties use this reports to make effective decisions.

Liabilities Amount Assets Amount

Equity £216000 Delivery van £61000

Profit £54520 Cash at bank £47160

Outstanding wages £2610 Prepaid rent £27000

Outstanding bills £2430 Advance tax £1350

Trade payables £111600 Trade receivables £77400

Closing inventory £173250

Total liabilities £387160 Total assets £387160

Part B – Parks mead Limited

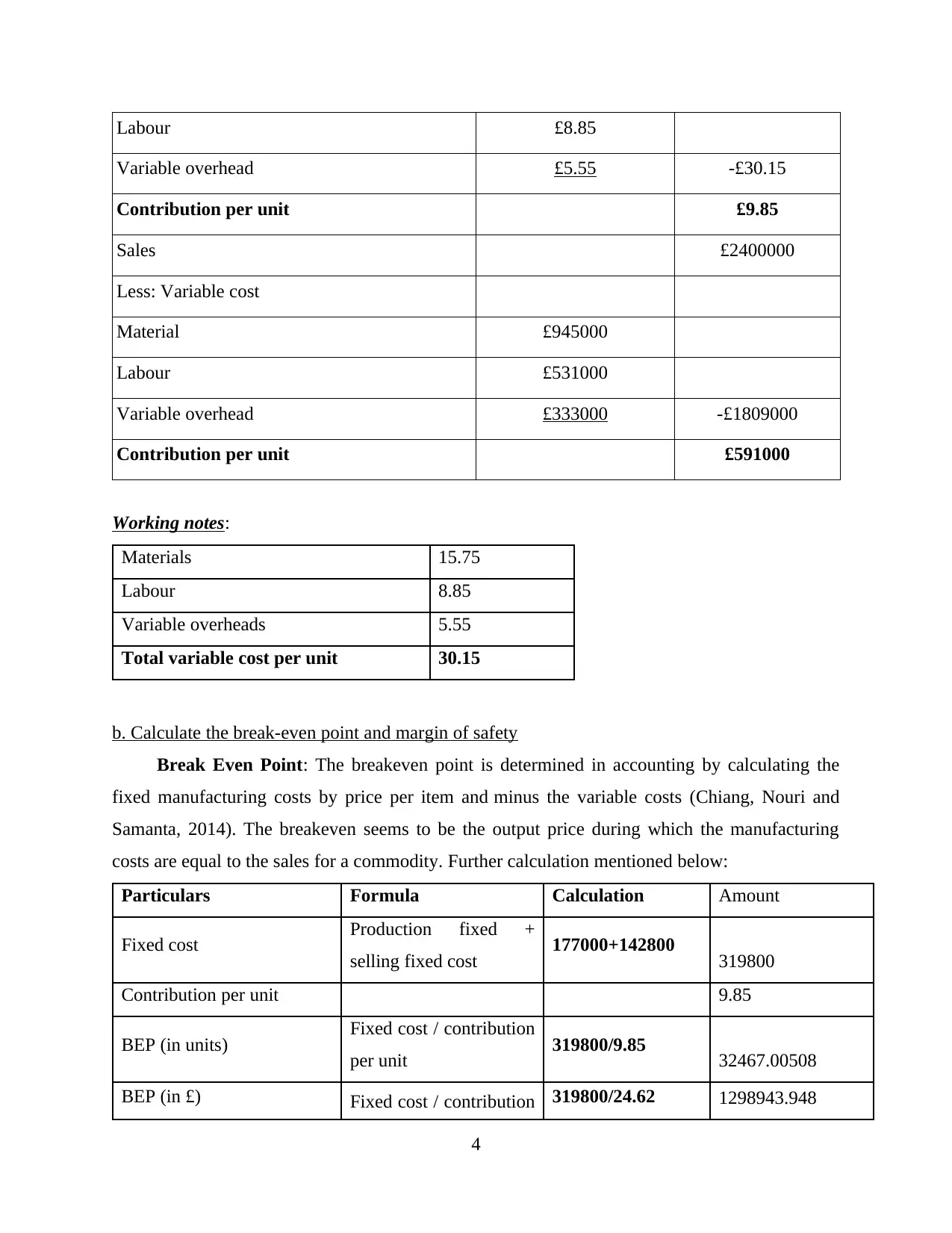

a. Calculate the contribution of each microwave

Particulars Details Amount

Selling price £40.00

Less: variable cost

Material £15.75

3

Payment to trade payables £471600

Van running expenses £40320

closing cash balance £47160

£896400 £896400

b. Balance sheet

This financial report shows company's financial performance that contains at a certain

particular moment in time liabilities, assets, equity capital, net debt etc. To represent the true

image of the balance sheet, list of asset and liabilities mentioned in this report. Further internal or

external parties use this reports to make effective decisions.

Liabilities Amount Assets Amount

Equity £216000 Delivery van £61000

Profit £54520 Cash at bank £47160

Outstanding wages £2610 Prepaid rent £27000

Outstanding bills £2430 Advance tax £1350

Trade payables £111600 Trade receivables £77400

Closing inventory £173250

Total liabilities £387160 Total assets £387160

Part B – Parks mead Limited

a. Calculate the contribution of each microwave

Particulars Details Amount

Selling price £40.00

Less: variable cost

Material £15.75

3

Labour £8.85

Variable overhead £5.55 -£30.15

Contribution per unit £9.85

Sales £2400000

Less: Variable cost

Material £945000

Labour £531000

Variable overhead £333000 -£1809000

Contribution per unit £591000

Working notes:

Materials 15.75

Labour 8.85

Variable overheads 5.55

Total variable cost per unit 30.15

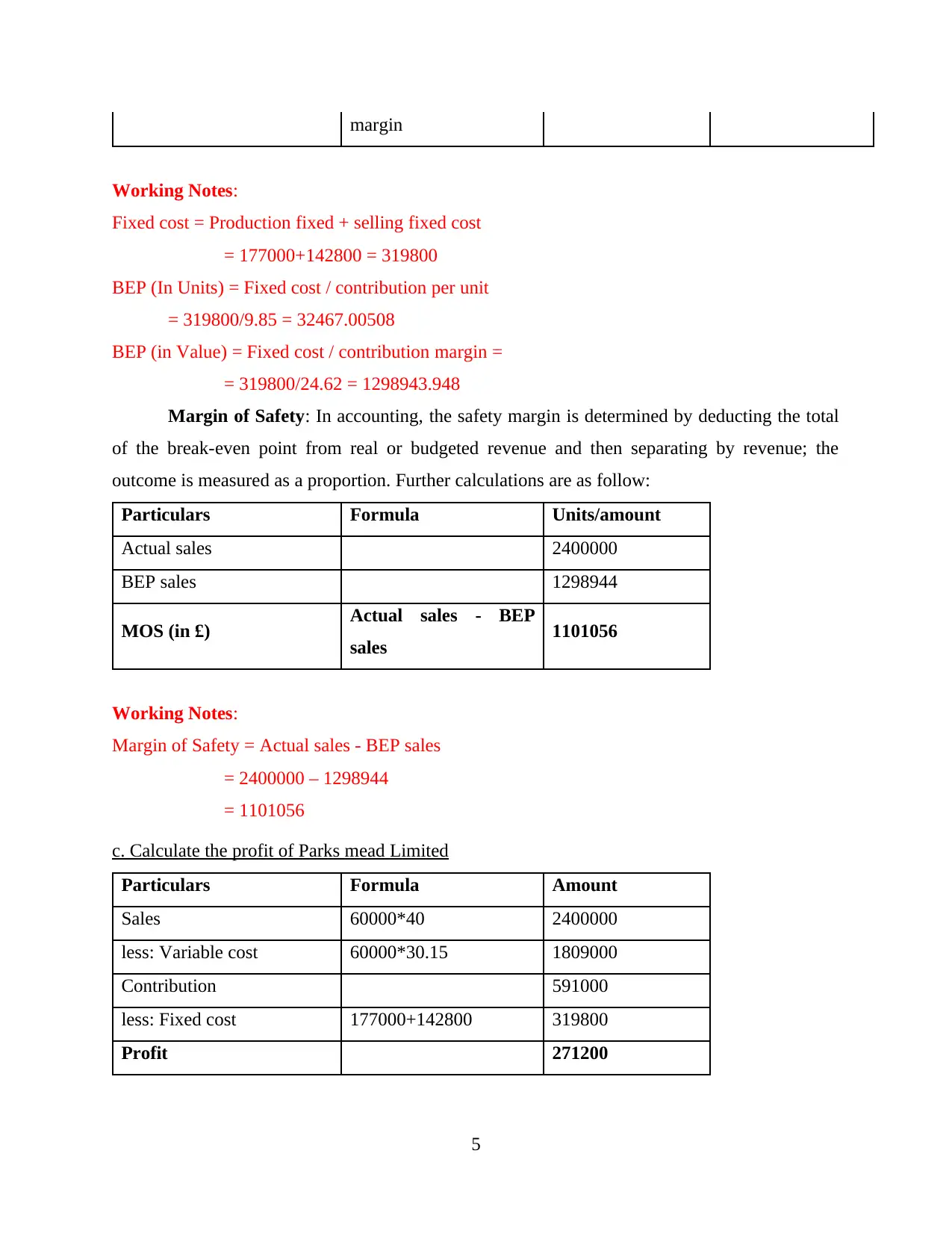

b. Calculate the break-even point and margin of safety

Break Even Point: The breakeven point is determined in accounting by calculating the

fixed manufacturing costs by price per item and minus the variable costs (Chiang, Nouri and

Samanta, 2014). The breakeven seems to be the output price during which the manufacturing

costs are equal to the sales for a commodity. Further calculation mentioned below:

Particulars Formula Calculation Amount

Fixed cost Production fixed +

selling fixed cost 177000+142800 319800

Contribution per unit 9.85

BEP (in units) Fixed cost / contribution

per unit 319800/9.85 32467.00508

BEP (in £) Fixed cost / contribution 319800/24.62 1298943.948

4

Variable overhead £5.55 -£30.15

Contribution per unit £9.85

Sales £2400000

Less: Variable cost

Material £945000

Labour £531000

Variable overhead £333000 -£1809000

Contribution per unit £591000

Working notes:

Materials 15.75

Labour 8.85

Variable overheads 5.55

Total variable cost per unit 30.15

b. Calculate the break-even point and margin of safety

Break Even Point: The breakeven point is determined in accounting by calculating the

fixed manufacturing costs by price per item and minus the variable costs (Chiang, Nouri and

Samanta, 2014). The breakeven seems to be the output price during which the manufacturing

costs are equal to the sales for a commodity. Further calculation mentioned below:

Particulars Formula Calculation Amount

Fixed cost Production fixed +

selling fixed cost 177000+142800 319800

Contribution per unit 9.85

BEP (in units) Fixed cost / contribution

per unit 319800/9.85 32467.00508

BEP (in £) Fixed cost / contribution 319800/24.62 1298943.948

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

margin

Working Notes:

Fixed cost = Production fixed + selling fixed cost

= 177000+142800 = 319800

BEP (In Units) = Fixed cost / contribution per unit

= 319800/9.85 = 32467.00508

BEP (in Value) = Fixed cost / contribution margin =

= 319800/24.62 = 1298943.948

Margin of Safety: In accounting, the safety margin is determined by deducting the total

of the break-even point from real or budgeted revenue and then separating by revenue; the

outcome is measured as a proportion. Further calculations are as follow:

Particulars Formula Units/amount

Actual sales 2400000

BEP sales 1298944

MOS (in £) Actual sales - BEP

sales 1101056

Working Notes:

Margin of Safety = Actual sales - BEP sales

= 2400000 – 1298944

= 1101056

c. Calculate the profit of Parks mead Limited

Particulars Formula Amount

Sales 60000*40 2400000

less: Variable cost 60000*30.15 1809000

Contribution 591000

less: Fixed cost 177000+142800 319800

Profit 271200

5

Working Notes:

Fixed cost = Production fixed + selling fixed cost

= 177000+142800 = 319800

BEP (In Units) = Fixed cost / contribution per unit

= 319800/9.85 = 32467.00508

BEP (in Value) = Fixed cost / contribution margin =

= 319800/24.62 = 1298943.948

Margin of Safety: In accounting, the safety margin is determined by deducting the total

of the break-even point from real or budgeted revenue and then separating by revenue; the

outcome is measured as a proportion. Further calculations are as follow:

Particulars Formula Units/amount

Actual sales 2400000

BEP sales 1298944

MOS (in £) Actual sales - BEP

sales 1101056

Working Notes:

Margin of Safety = Actual sales - BEP sales

= 2400000 – 1298944

= 1101056

c. Calculate the profit of Parks mead Limited

Particulars Formula Amount

Sales 60000*40 2400000

less: Variable cost 60000*30.15 1809000

Contribution 591000

less: Fixed cost 177000+142800 319800

Profit 271200

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

d. Selling price increased by 8% and quantity 15%

Particulars Formula Amount

Sales 69000*43.2 2980800

less: variable cost 69000*30.15 2080350

contribution Sales – variable cost 900450

less: fixed cost 454800

Profits 445650

Working notes:

Particulars Increase 8% in selling price

Sales price 40

% increase 3.2

New sales 43.2

Particulars Increase in sales by 15 %

Old sales £60,000

% increase £9,000

New sales £69,000

e. Explain the underpinning assumptions attached to the break-even model

Assessment of break-even is vitally important when assessing the utility of value variables.

It depends heavily on various factors such as output quantity, quality, and benefit (Fischer-

Pauzenberger and Schwaiger, 2017). This is supposed to clarify the difficult connection among

total annual investment and productivity. For break-even analysis listed below, a number of

concerns have arisen:

It is important to define fixed as well as variable costs benefit of the entire, where all

semi-variable effects are overlooked.

Linear price and benefit feature stay, and the cost of manufacturing are assumed to

remain stable.

Research break-even implies steady rate of maximization of variable cost.

6

Particulars Formula Amount

Sales 69000*43.2 2980800

less: variable cost 69000*30.15 2080350

contribution Sales – variable cost 900450

less: fixed cost 454800

Profits 445650

Working notes:

Particulars Increase 8% in selling price

Sales price 40

% increase 3.2

New sales 43.2

Particulars Increase in sales by 15 %

Old sales £60,000

% increase £9,000

New sales £69,000

e. Explain the underpinning assumptions attached to the break-even model

Assessment of break-even is vitally important when assessing the utility of value variables.

It depends heavily on various factors such as output quantity, quality, and benefit (Fischer-

Pauzenberger and Schwaiger, 2017). This is supposed to clarify the difficult connection among

total annual investment and productivity. For break-even analysis listed below, a number of

concerns have arisen:

It is important to define fixed as well as variable costs benefit of the entire, where all

semi-variable effects are overlooked.

Linear price and benefit feature stay, and the cost of manufacturing are assumed to

remain stable.

Research break-even implies steady rate of maximization of variable cost.

6

This anticipates continuous development and not indispensable for enhancing labour

performance.

The price of the good in this system is believed to be fixed.

Changes in commodity prices or fluctuations are left out.

Part C – Skipsey Clifford Plc.

a. By using investment appraisal technique, calculate several aspect and recommend that

company should purchase this machinery or not

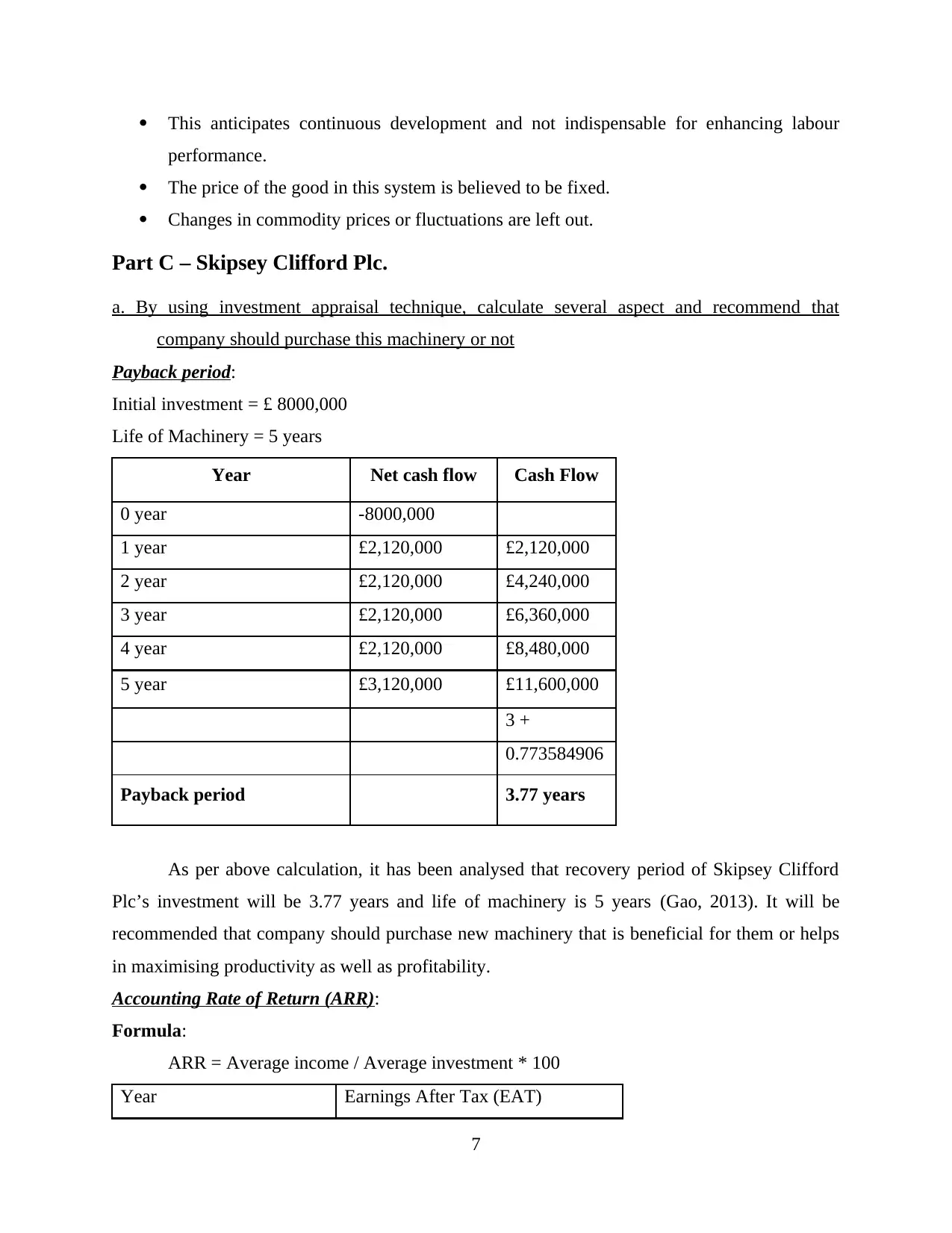

Payback period:

Initial investment = £ 8000,000

Life of Machinery = 5 years

Year Net cash flow Cash Flow

0 year -8000,000

1 year £2,120,000 £2,120,000

2 year £2,120,000 £4,240,000

3 year £2,120,000 £6,360,000

4 year £2,120,000 £8,480,000

5 year £3,120,000 £11,600,000

3 +

0.773584906

Payback period 3.77 years

As per above calculation, it has been analysed that recovery period of Skipsey Clifford

Plc’s investment will be 3.77 years and life of machinery is 5 years (Gao, 2013). It will be

recommended that company should purchase new machinery that is beneficial for them or helps

in maximising productivity as well as profitability.

Accounting Rate of Return (ARR):

Formula:

ARR = Average income / Average investment * 100

Year Earnings After Tax (EAT)

7

performance.

The price of the good in this system is believed to be fixed.

Changes in commodity prices or fluctuations are left out.

Part C – Skipsey Clifford Plc.

a. By using investment appraisal technique, calculate several aspect and recommend that

company should purchase this machinery or not

Payback period:

Initial investment = £ 8000,000

Life of Machinery = 5 years

Year Net cash flow Cash Flow

0 year -8000,000

1 year £2,120,000 £2,120,000

2 year £2,120,000 £4,240,000

3 year £2,120,000 £6,360,000

4 year £2,120,000 £8,480,000

5 year £3,120,000 £11,600,000

3 +

0.773584906

Payback period 3.77 years

As per above calculation, it has been analysed that recovery period of Skipsey Clifford

Plc’s investment will be 3.77 years and life of machinery is 5 years (Gao, 2013). It will be

recommended that company should purchase new machinery that is beneficial for them or helps

in maximising productivity as well as profitability.

Accounting Rate of Return (ARR):

Formula:

ARR = Average income / Average investment * 100

Year Earnings After Tax (EAT)

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

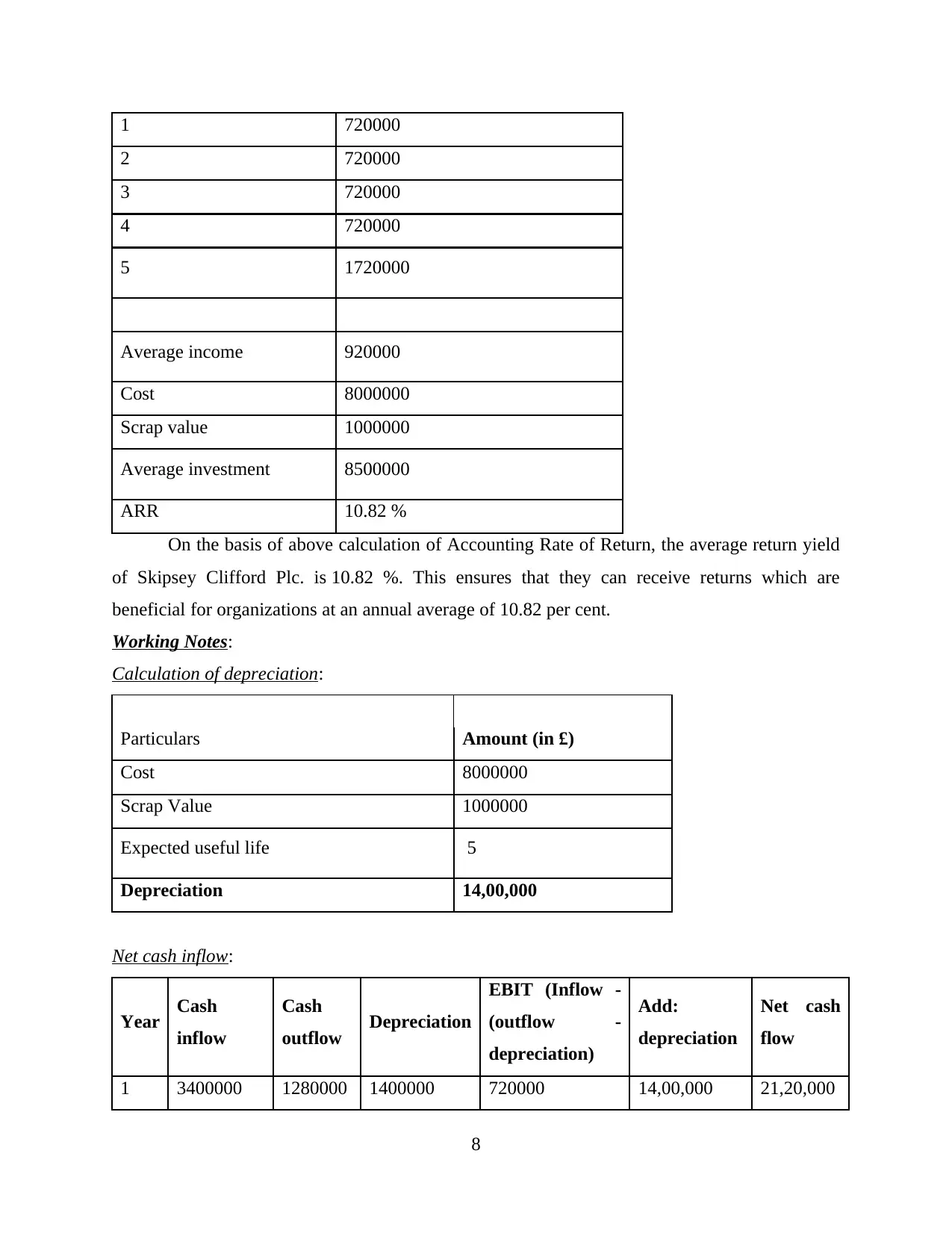

1 720000

2 720000

3 720000

4 720000

5 1720000

Average income 920000

Cost 8000000

Scrap value 1000000

Average investment 8500000

ARR 10.82 %

On the basis of above calculation of Accounting Rate of Return, the average return yield

of Skipsey Clifford Plc. is 10.82 %. This ensures that they can receive returns which are

beneficial for organizations at an annual average of 10.82 per cent.

Working Notes:

Calculation of depreciation:

Particulars Amount (in £)

Cost 8000000

Scrap Value 1000000

Expected useful life 5

Depreciation 14,00,000

Net cash inflow:

Year Cash

inflow

Cash

outflow Depreciation

EBIT (Inflow -

(outflow -

depreciation)

Add:

depreciation

Net cash

flow

1 3400000 1280000 1400000 720000 14,00,000 21,20,000

8

2 720000

3 720000

4 720000

5 1720000

Average income 920000

Cost 8000000

Scrap value 1000000

Average investment 8500000

ARR 10.82 %

On the basis of above calculation of Accounting Rate of Return, the average return yield

of Skipsey Clifford Plc. is 10.82 %. This ensures that they can receive returns which are

beneficial for organizations at an annual average of 10.82 per cent.

Working Notes:

Calculation of depreciation:

Particulars Amount (in £)

Cost 8000000

Scrap Value 1000000

Expected useful life 5

Depreciation 14,00,000

Net cash inflow:

Year Cash

inflow

Cash

outflow Depreciation

EBIT (Inflow -

(outflow -

depreciation)

Add:

depreciation

Net cash

flow

1 3400000 1280000 1400000 720000 14,00,000 21,20,000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

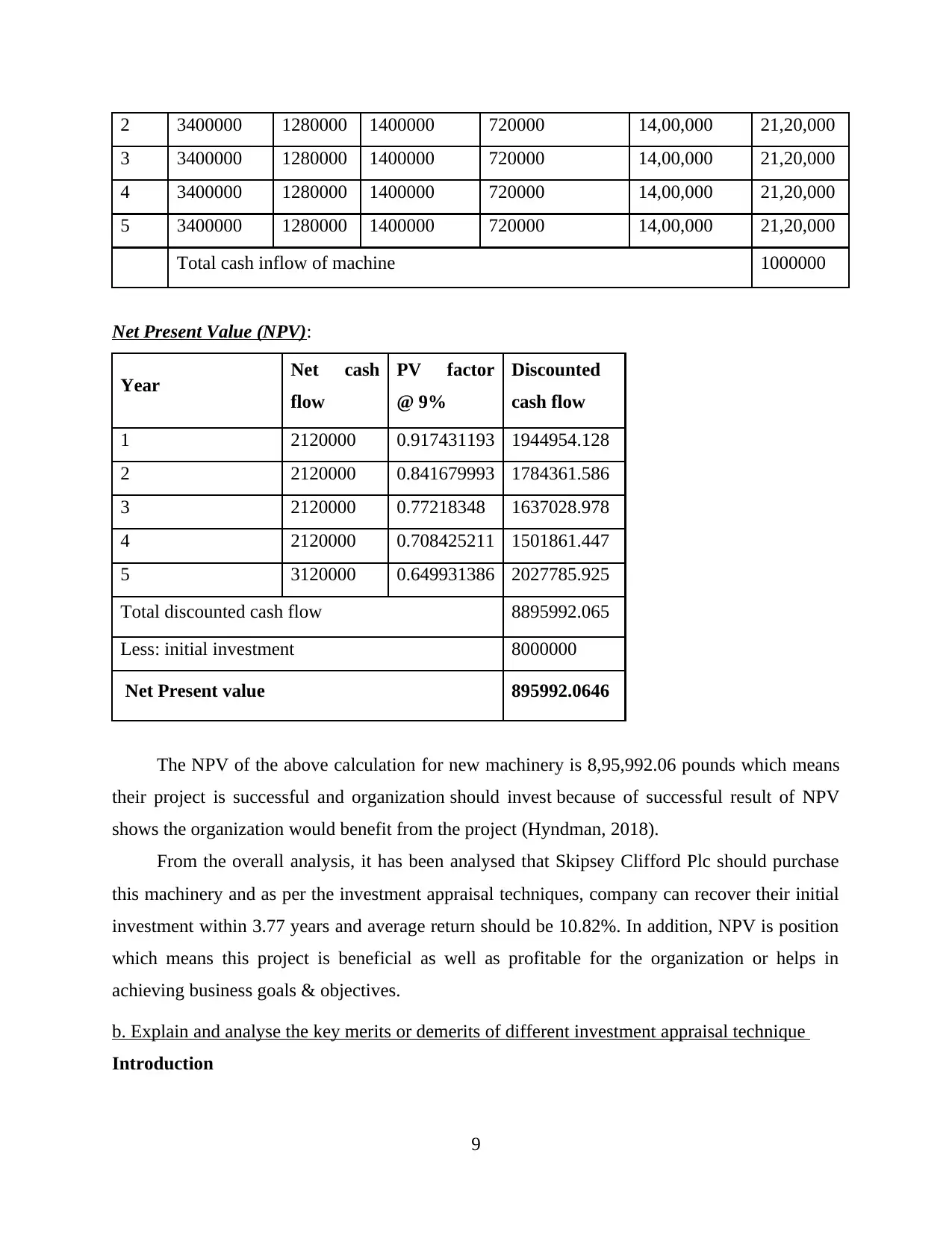

2 3400000 1280000 1400000 720000 14,00,000 21,20,000

3 3400000 1280000 1400000 720000 14,00,000 21,20,000

4 3400000 1280000 1400000 720000 14,00,000 21,20,000

5 3400000 1280000 1400000 720000 14,00,000 21,20,000

Total cash inflow of machine 1000000

Net Present Value (NPV):

Year Net cash

flow

PV factor

@ 9%

Discounted

cash flow

1 2120000 0.917431193 1944954.128

2 2120000 0.841679993 1784361.586

3 2120000 0.77218348 1637028.978

4 2120000 0.708425211 1501861.447

5 3120000 0.649931386 2027785.925

Total discounted cash flow 8895992.065

Less: initial investment 8000000

Net Present value 895992.0646

The NPV of the above calculation for new machinery is 8,95,992.06 pounds which means

their project is successful and organization should invest because of successful result of NPV

shows the organization would benefit from the project (Hyndman, 2018).

From the overall analysis, it has been analysed that Skipsey Clifford Plc should purchase

this machinery and as per the investment appraisal techniques, company can recover their initial

investment within 3.77 years and average return should be 10.82%. In addition, NPV is position

which means this project is beneficial as well as profitable for the organization or helps in

achieving business goals & objectives.

b. Explain and analyse the key merits or demerits of different investment appraisal technique

Introduction

9

3 3400000 1280000 1400000 720000 14,00,000 21,20,000

4 3400000 1280000 1400000 720000 14,00,000 21,20,000

5 3400000 1280000 1400000 720000 14,00,000 21,20,000

Total cash inflow of machine 1000000

Net Present Value (NPV):

Year Net cash

flow

PV factor

@ 9%

Discounted

cash flow

1 2120000 0.917431193 1944954.128

2 2120000 0.841679993 1784361.586

3 2120000 0.77218348 1637028.978

4 2120000 0.708425211 1501861.447

5 3120000 0.649931386 2027785.925

Total discounted cash flow 8895992.065

Less: initial investment 8000000

Net Present value 895992.0646

The NPV of the above calculation for new machinery is 8,95,992.06 pounds which means

their project is successful and organization should invest because of successful result of NPV

shows the organization would benefit from the project (Hyndman, 2018).

From the overall analysis, it has been analysed that Skipsey Clifford Plc should purchase

this machinery and as per the investment appraisal techniques, company can recover their initial

investment within 3.77 years and average return should be 10.82%. In addition, NPV is position

which means this project is beneficial as well as profitable for the organization or helps in

achieving business goals & objectives.

b. Explain and analyse the key merits or demerits of different investment appraisal technique

Introduction

9

Investment appraisal techniques include several methods which help the manager to make

strategic decisions such as payback period, IRR, NPV, ARR etc. It helps in evaluating

profitability of the particular project. This part consist merits or demerits of different investment

appraisal techniques.

Payback period: This method determined that how many years it requires to recoup the

original investment. The method is to develop out the original investment and split by annual

cash balance. Lower the payback period is accepted and higher one rejected because

organizations wants to recover their initial investment as soon as possible. Followings are the

merits and demerits of this approach:

Merits: The payback method's greatest single benefit is its ease. Comparing many

projects and only choosing something that has fastest payback period is a simple way to

do so (Leauby and Wentzel, 2012). It helps the manager to make quick decisions on the

basis of low recovery period. In addition, by using this investment appraisal techniques

organization able to minimise the risk of losses.

Demerits: The far more serious drawback of this method is that, it does not accept the

time value of money. Investment returns obtained throughout a proposal's early days get

a larger weight just like cash flows earned in final decades. Two tasks might have

similar payback period, but one proposal in the early days has the most cash flow, while

another proposal has higher revenues in the later life. The payback period method in this

case will not provide a thorough description about which proposal to choose.

Accounting Rate of Return (ARR): It is one of the effective methods of capital budgeting

which are used for evaluating different options of investment. Overall findings helps the

managers to make their decisions whether to invest or not in the particular project. It is a

calculation that represents the estimated profit margin of return on initial investment, or asset,

relative to the value of the original investment. The ARR equation splits the total profit of an

asset by the original cost of the business in order to calculate the amount or profit one would

assume over the lifespan of the asset or associated project. There are some merits or demerits

which are discussed below:

Merits: This approach aims to equate a proposed project with those of cost-effective

programs, and with profitable projects. The payback time is easier to comprehend, and

quantify. This takes into account the gains or the gains that exist over the entire financial

10

strategic decisions such as payback period, IRR, NPV, ARR etc. It helps in evaluating

profitability of the particular project. This part consist merits or demerits of different investment

appraisal techniques.

Payback period: This method determined that how many years it requires to recoup the

original investment. The method is to develop out the original investment and split by annual

cash balance. Lower the payback period is accepted and higher one rejected because

organizations wants to recover their initial investment as soon as possible. Followings are the

merits and demerits of this approach:

Merits: The payback method's greatest single benefit is its ease. Comparing many

projects and only choosing something that has fastest payback period is a simple way to

do so (Leauby and Wentzel, 2012). It helps the manager to make quick decisions on the

basis of low recovery period. In addition, by using this investment appraisal techniques

organization able to minimise the risk of losses.

Demerits: The far more serious drawback of this method is that, it does not accept the

time value of money. Investment returns obtained throughout a proposal's early days get

a larger weight just like cash flows earned in final decades. Two tasks might have

similar payback period, but one proposal in the early days has the most cash flow, while

another proposal has higher revenues in the later life. The payback period method in this

case will not provide a thorough description about which proposal to choose.

Accounting Rate of Return (ARR): It is one of the effective methods of capital budgeting

which are used for evaluating different options of investment. Overall findings helps the

managers to make their decisions whether to invest or not in the particular project. It is a

calculation that represents the estimated profit margin of return on initial investment, or asset,

relative to the value of the original investment. The ARR equation splits the total profit of an

asset by the original cost of the business in order to calculate the amount or profit one would

assume over the lifespan of the asset or associated project. There are some merits or demerits

which are discussed below:

Merits: This approach aims to equate a proposed project with those of cost-effective

programs, and with profitable projects. The payback time is easier to comprehend, and

quantify. This takes into account the gains or the gains that exist over the entire financial

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.