Comprehensive Management Accounting Report for Azio - Finance

VerifiedAdded on 2020/01/07

|16

|5541

|175

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on their application to Azio, a manufacturer of gaming accessories. It begins with an introduction to management accounting, emphasizing its role in decision-making, financial planning, and cost control. The report then delves into the concept of management accounting and its essential requirements, exploring various systems such as cost accounting, job costing, inventory management, and price optimization. Different management accounting reporting methods, including job cost reports, inventory management reports, operating budget reports, accounts receivable aging reports, and performance reports, are also examined. The report then explores cost calculation techniques, specifically absorption and marginal costing, highlighting their advantages and disadvantages. Furthermore, it discusses planning tools within budgetary control and how Azio should adapt its management accounting system to address financial problems. The report concludes with a summary of key findings and recommendations, providing a valuable resource for understanding and applying management accounting principles in a practical business context.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................4

P1 Concept of management accounting and essential requirements of management accounting

system..........................................................................................................................................4

P2 Different methods for the management accounting reporting which can be used by Azio...6

M1...............................................................................................................................................7

D1................................................................................................................................................8

TASK 2............................................................................................................................................8

P3 & M2 Calculation of cost using different tools and techniques.............................................8

D2..............................................................................................................................................11

TASK 3..........................................................................................................................................12

P4 Different planning tools which are included in budgetary control and its advantages and

disadvantages............................................................................................................................12

M3.............................................................................................................................................13

P6 How organisation should adapt the management accounting system which assist in

responding to the financial problems........................................................................................13

M4.............................................................................................................................................14

D3..............................................................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................4

P1 Concept of management accounting and essential requirements of management accounting

system..........................................................................................................................................4

P2 Different methods for the management accounting reporting which can be used by Azio...6

M1...............................................................................................................................................7

D1................................................................................................................................................8

TASK 2............................................................................................................................................8

P3 & M2 Calculation of cost using different tools and techniques.............................................8

D2..............................................................................................................................................11

TASK 3..........................................................................................................................................12

P4 Different planning tools which are included in budgetary control and its advantages and

disadvantages............................................................................................................................12

M3.............................................................................................................................................13

P6 How organisation should adapt the management accounting system which assist in

responding to the financial problems........................................................................................13

M4.............................................................................................................................................14

D3..............................................................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Managerial accounting processes which helps in attaining the economic information

which is to be used by the supervising to make the appropriate and relevant decisions.

Management accounting put a greater focus on the cost accounting, financial planning as well as

management issues. Along with this employees of the business entity have to fulfil the

responsibility (Baldvinsdottir, Mitchell and Nørreklit, 2010). Management accounting helps the

staff members to do best planning as well as organising by collecting the information related to

the finance and operations of a business. Managerial accounting having the different functions

which includes the marginal analysis, break even analysis, target costing, inventory valuation etc.

They have to warn the managers for the impending issues as well as they have to put their proper

attention so that they can gain the opportunities so that they can earn maximum profits (Cost-

Volume Profit Analysis, 2017). They have to record the appropriate data so that workers can do

accounting transactions in a good manner which helps in attaining the goals and objectives. The

main objective of management accounting is that this assist the supervising and also aid in

making the quality decision so that they can control the business activities in a effective manner.

The present report is focused on Azio which is manufacturer or producer of keyboards, mice etc.

along with the mobile accessories in the style of gaming and vision (Marginal cost, 2017). In the

below assignment, discussion based upon the concept of management accounting and the

different system of management accounting. Along with this determination of absorption and

marginal costing.

TASK 1

P1 Concept of management accounting and essential requirements of management accounting

system

Management accounting is a combination of accounting, finance as well as

administration with the leading edge technique so that they become the successful business.

Management accounting is a profession which involves the partnering in the management

decision making, devise the planning so that they can manage their performance. Along with this

they have to take advice from the experts so that they can manage the data in the financial

reporting and they have to do proper control in the formulation and implementation of the

strategy of Azio which the employees are following (Bennett, Schaltegger and Zvezdov, 2013).

Managerial accounting processes which helps in attaining the economic information

which is to be used by the supervising to make the appropriate and relevant decisions.

Management accounting put a greater focus on the cost accounting, financial planning as well as

management issues. Along with this employees of the business entity have to fulfil the

responsibility (Baldvinsdottir, Mitchell and Nørreklit, 2010). Management accounting helps the

staff members to do best planning as well as organising by collecting the information related to

the finance and operations of a business. Managerial accounting having the different functions

which includes the marginal analysis, break even analysis, target costing, inventory valuation etc.

They have to warn the managers for the impending issues as well as they have to put their proper

attention so that they can gain the opportunities so that they can earn maximum profits (Cost-

Volume Profit Analysis, 2017). They have to record the appropriate data so that workers can do

accounting transactions in a good manner which helps in attaining the goals and objectives. The

main objective of management accounting is that this assist the supervising and also aid in

making the quality decision so that they can control the business activities in a effective manner.

The present report is focused on Azio which is manufacturer or producer of keyboards, mice etc.

along with the mobile accessories in the style of gaming and vision (Marginal cost, 2017). In the

below assignment, discussion based upon the concept of management accounting and the

different system of management accounting. Along with this determination of absorption and

marginal costing.

TASK 1

P1 Concept of management accounting and essential requirements of management accounting

system

Management accounting is a combination of accounting, finance as well as

administration with the leading edge technique so that they become the successful business.

Management accounting is a profession which involves the partnering in the management

decision making, devise the planning so that they can manage their performance. Along with this

they have to take advice from the experts so that they can manage the data in the financial

reporting and they have to do proper control in the formulation and implementation of the

strategy of Azio which the employees are following (Bennett, Schaltegger and Zvezdov, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting have to do best designing and they are intended which is used by the

managers within the organisation and they are intended to use for shareholders, creditors as well

as public regulators. It also helps in monitoring the spending along with the financial control and

also have to conduct the business audits. Along with this management accounting having a

impact on the competitive advantage. Management accounting includes the different systems

which helps the employees of Azio in attaining the targets as well as goals and objectives (What

is Budgetary control?, 2017).

Different system Description

Cost accounting system The employees of Azio have to adopt the system so that they

can manage the cost of the product while producing the

products and services as it aid in increasing productivity as well

as performance of the company in the market. Cost accounting

system is divided into two parts that is job order costing and the

process costing (Busco and Scapens, 2011). This also helps in

doing the appropriate measurement and the improvement of

efficiency and fixation of prices. It provides the detail

information for the cost data that needs the management to

control its current operations along with the plans for the future.

Job costing system It is a form of specific order which helps in analysing and

identifying the cost which are associated while completing the

order so that they can record them in a proper manner. It

includes the cost of material, labour along with the overheads

which is used to manage the job. It is used in the different type

of business where the merchandise should be produce in a

unique nature for each individual consumer.

Inventory management system It is a part of the management accounting system as it helps in

managing as well as analysing the inventory of Azio. It

combines the different use of desktop software, printer as well

as barcode scanner which assist in supervising the inventory

(Christ and Burritt, 2013). The staff members of Azio have to

managers within the organisation and they are intended to use for shareholders, creditors as well

as public regulators. It also helps in monitoring the spending along with the financial control and

also have to conduct the business audits. Along with this management accounting having a

impact on the competitive advantage. Management accounting includes the different systems

which helps the employees of Azio in attaining the targets as well as goals and objectives (What

is Budgetary control?, 2017).

Different system Description

Cost accounting system The employees of Azio have to adopt the system so that they

can manage the cost of the product while producing the

products and services as it aid in increasing productivity as well

as performance of the company in the market. Cost accounting

system is divided into two parts that is job order costing and the

process costing (Busco and Scapens, 2011). This also helps in

doing the appropriate measurement and the improvement of

efficiency and fixation of prices. It provides the detail

information for the cost data that needs the management to

control its current operations along with the plans for the future.

Job costing system It is a form of specific order which helps in analysing and

identifying the cost which are associated while completing the

order so that they can record them in a proper manner. It

includes the cost of material, labour along with the overheads

which is used to manage the job. It is used in the different type

of business where the merchandise should be produce in a

unique nature for each individual consumer.

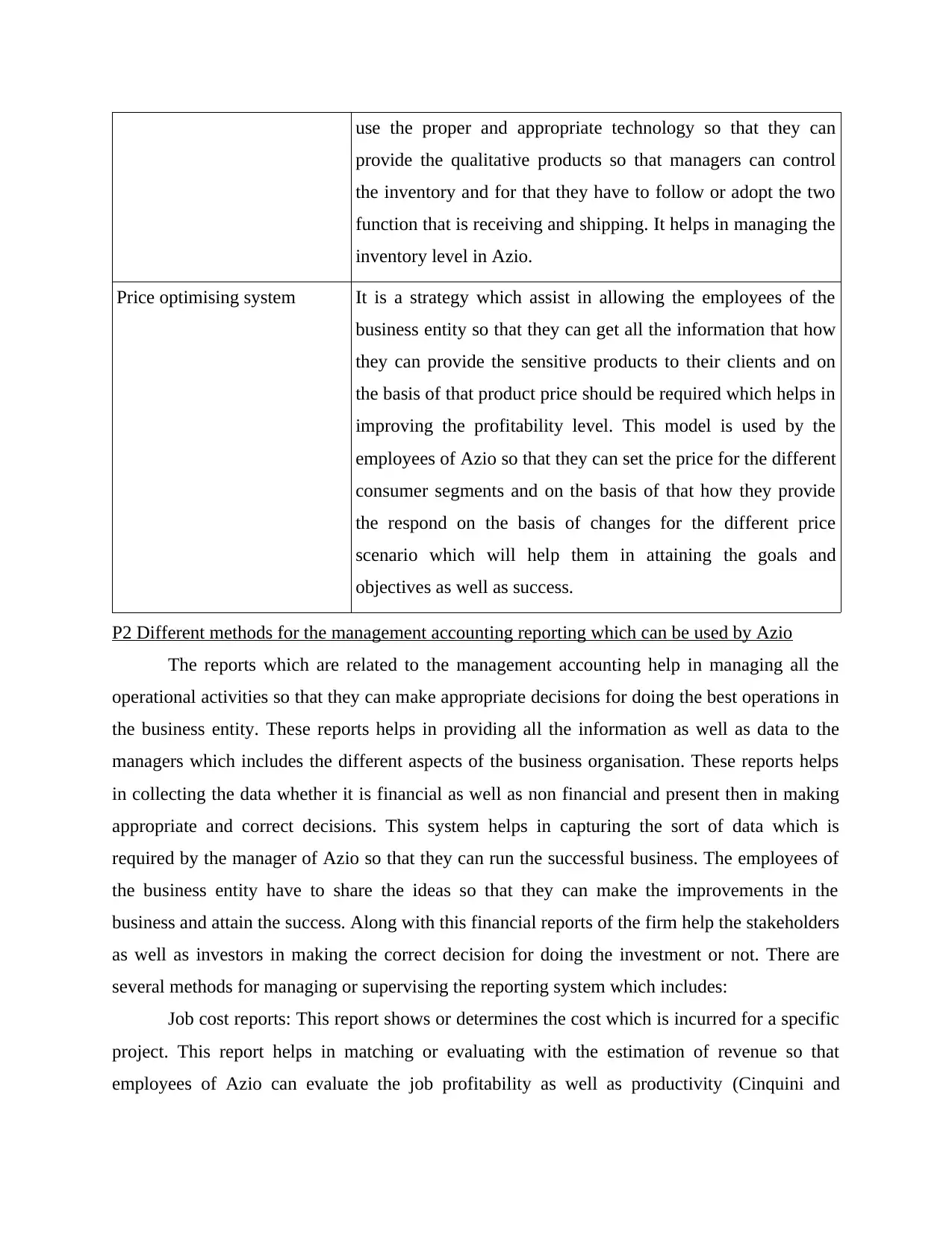

Inventory management system It is a part of the management accounting system as it helps in

managing as well as analysing the inventory of Azio. It

combines the different use of desktop software, printer as well

as barcode scanner which assist in supervising the inventory

(Christ and Burritt, 2013). The staff members of Azio have to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

use the proper and appropriate technology so that they can

provide the qualitative products so that managers can control

the inventory and for that they have to follow or adopt the two

function that is receiving and shipping. It helps in managing the

inventory level in Azio.

Price optimising system It is a strategy which assist in allowing the employees of the

business entity so that they can get all the information that how

they can provide the sensitive products to their clients and on

the basis of that product price should be required which helps in

improving the profitability level. This model is used by the

employees of Azio so that they can set the price for the different

consumer segments and on the basis of that how they provide

the respond on the basis of changes for the different price

scenario which will help them in attaining the goals and

objectives as well as success.

P2 Different methods for the management accounting reporting which can be used by Azio

The reports which are related to the management accounting help in managing all the

operational activities so that they can make appropriate decisions for doing the best operations in

the business entity. These reports helps in providing all the information as well as data to the

managers which includes the different aspects of the business organisation. These reports helps

in collecting the data whether it is financial as well as non financial and present then in making

appropriate and correct decisions. This system helps in capturing the sort of data which is

required by the manager of Azio so that they can run the successful business. The employees of

the business entity have to share the ideas so that they can make the improvements in the

business and attain the success. Along with this financial reports of the firm help the stakeholders

as well as investors in making the correct decision for doing the investment or not. There are

several methods for managing or supervising the reporting system which includes:

Job cost reports: This report shows or determines the cost which is incurred for a specific

project. This report helps in matching or evaluating with the estimation of revenue so that

employees of Azio can evaluate the job profitability as well as productivity (Cinquini and

provide the qualitative products so that managers can control

the inventory and for that they have to follow or adopt the two

function that is receiving and shipping. It helps in managing the

inventory level in Azio.

Price optimising system It is a strategy which assist in allowing the employees of the

business entity so that they can get all the information that how

they can provide the sensitive products to their clients and on

the basis of that product price should be required which helps in

improving the profitability level. This model is used by the

employees of Azio so that they can set the price for the different

consumer segments and on the basis of that how they provide

the respond on the basis of changes for the different price

scenario which will help them in attaining the goals and

objectives as well as success.

P2 Different methods for the management accounting reporting which can be used by Azio

The reports which are related to the management accounting help in managing all the

operational activities so that they can make appropriate decisions for doing the best operations in

the business entity. These reports helps in providing all the information as well as data to the

managers which includes the different aspects of the business organisation. These reports helps

in collecting the data whether it is financial as well as non financial and present then in making

appropriate and correct decisions. This system helps in capturing the sort of data which is

required by the manager of Azio so that they can run the successful business. The employees of

the business entity have to share the ideas so that they can make the improvements in the

business and attain the success. Along with this financial reports of the firm help the stakeholders

as well as investors in making the correct decision for doing the investment or not. There are

several methods for managing or supervising the reporting system which includes:

Job cost reports: This report shows or determines the cost which is incurred for a specific

project. This report helps in matching or evaluating with the estimation of revenue so that

employees of Azio can evaluate the job profitability as well as productivity (Cinquini and

Tenucci, 2010). Along with this it helps in identifying the areas which are included in the high

earning of the business so that employees of the firm can focus on that and put more efforts to

improve those areas rather than wasting time along with the money on the jobs which having the

low profit margins. Moreover, this report helps in analysing or identifying the various costs

which are putting in the progress or improvements of the products and services which assist in

reducing the waste.

Inventory management report: This report helps in managing the inventory of the

business so that they can do the proper operations which helps the business entity in attaining the

success as well as goals and objectives. It assist in determining the levels which they have to

maintain or when the stock should be replenished.

Operating budget report: This report helps the business entity in analysing as well as

identifying the performance in the market as well as in the company also. In each and every

department they have to enable monitor as well as they have to control the cost while doing the

operations. Management of Azio have to use or adopt operating budget which helps in providing

the incentives to the employees (Contrafatto and Burns, 2013).

Accounts receivable aging report: It is a tool which enables the management of Azio so

that they can manage its cash flow in providing the proper credit to their consumers. Along with

this it helps in break down the consumer balance that how they can manage the business as well

as operational activities which helps in attaining the targets.

Performance report: This report help the staff members of Azio in identifying the

performance of them that is how much products and services they are producing. They have to

do proper segments of the market so that they can do proper operations. It aid in attaining the

success as well as generating profitability and improving the productivity. Moreover, for

controlling the cost they have to take corrective measures so that they can manage all the work of

the staff members as well as it helps in bring out the efficiency in a effective manner (Dillard

and Roslender, 2011).

M1

There are different type of management accounting system and they have their benefits.

Cost accounting system helps in determining the cost of the merchandise as well as helps in

making the marketing decisions. They have to determine the selling price of the product and

meet the competition so that they can analyse the profitability. Inventory management system

earning of the business so that employees of the firm can focus on that and put more efforts to

improve those areas rather than wasting time along with the money on the jobs which having the

low profit margins. Moreover, this report helps in analysing or identifying the various costs

which are putting in the progress or improvements of the products and services which assist in

reducing the waste.

Inventory management report: This report helps in managing the inventory of the

business so that they can do the proper operations which helps the business entity in attaining the

success as well as goals and objectives. It assist in determining the levels which they have to

maintain or when the stock should be replenished.

Operating budget report: This report helps the business entity in analysing as well as

identifying the performance in the market as well as in the company also. In each and every

department they have to enable monitor as well as they have to control the cost while doing the

operations. Management of Azio have to use or adopt operating budget which helps in providing

the incentives to the employees (Contrafatto and Burns, 2013).

Accounts receivable aging report: It is a tool which enables the management of Azio so

that they can manage its cash flow in providing the proper credit to their consumers. Along with

this it helps in break down the consumer balance that how they can manage the business as well

as operational activities which helps in attaining the targets.

Performance report: This report help the staff members of Azio in identifying the

performance of them that is how much products and services they are producing. They have to

do proper segments of the market so that they can do proper operations. It aid in attaining the

success as well as generating profitability and improving the productivity. Moreover, for

controlling the cost they have to take corrective measures so that they can manage all the work of

the staff members as well as it helps in bring out the efficiency in a effective manner (Dillard

and Roslender, 2011).

M1

There are different type of management accounting system and they have their benefits.

Cost accounting system helps in determining the cost of the merchandise as well as helps in

making the marketing decisions. They have to determine the selling price of the product and

meet the competition so that they can analyse the profitability. Inventory management system

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

helps in making the changes in the demand for the finished products. Another system is job

costing system and it helps in gathering the data so that they can find actual cost for the job. In

addition to this price optimisation system which having a advantage that is can be organisation to

tailor its pricing for the different consumer segments which is based on the changes of the price

scenario.

D1

The employees and managers of Azio have to use proper management accounting system

along with the reporting so that they can not face any issues in managing all the operational

activities and by that they can attain the goals and objectives (Fullerton, Kennedy and Widener,

2014). Along with this it helps the stakeholders and investors to make the appropriate judgement

for doing the investment in the business entity so that they can accomplish the targets. They have

to present the information in a specified time and also it should be up to date so that investors

can not face any obstacles and by that they can maintain their brand image in the market as well

as assist in reaping the success in the marketplace at the time of high competition.

TASK 2

P3 & M2 Calculation of cost using different tools and techniques

There are different tools and techniques which can be used by the employees of Azio so

that they can calculate the cost along with the profit and they includes:

Absorption Costing: This method helps in calculating the cost of the product whether it is direct

or indirect which will aid in generating the maximum profit. This method of costing assist in

identifying the centre which is related to the individual cost so that indirect cost can be identified

easily. It is a principle which succour in allocating the cost on the basis of production cost so that

employees of the company can do proper functioning and by that they can attain their targets

(Håkansson, Kraus and Lind, 2010).

Income statement on the basis of Absorption costing method:

Selling Price £35

Unit costs

Direct materials £6

Direct Labour £5

costing system and it helps in gathering the data so that they can find actual cost for the job. In

addition to this price optimisation system which having a advantage that is can be organisation to

tailor its pricing for the different consumer segments which is based on the changes of the price

scenario.

D1

The employees and managers of Azio have to use proper management accounting system

along with the reporting so that they can not face any issues in managing all the operational

activities and by that they can attain the goals and objectives (Fullerton, Kennedy and Widener,

2014). Along with this it helps the stakeholders and investors to make the appropriate judgement

for doing the investment in the business entity so that they can accomplish the targets. They have

to present the information in a specified time and also it should be up to date so that investors

can not face any obstacles and by that they can maintain their brand image in the market as well

as assist in reaping the success in the marketplace at the time of high competition.

TASK 2

P3 & M2 Calculation of cost using different tools and techniques

There are different tools and techniques which can be used by the employees of Azio so

that they can calculate the cost along with the profit and they includes:

Absorption Costing: This method helps in calculating the cost of the product whether it is direct

or indirect which will aid in generating the maximum profit. This method of costing assist in

identifying the centre which is related to the individual cost so that indirect cost can be identified

easily. It is a principle which succour in allocating the cost on the basis of production cost so that

employees of the company can do proper functioning and by that they can attain their targets

(Håkansson, Kraus and Lind, 2010).

Income statement on the basis of Absorption costing method:

Selling Price £35

Unit costs

Direct materials £6

Direct Labour £5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

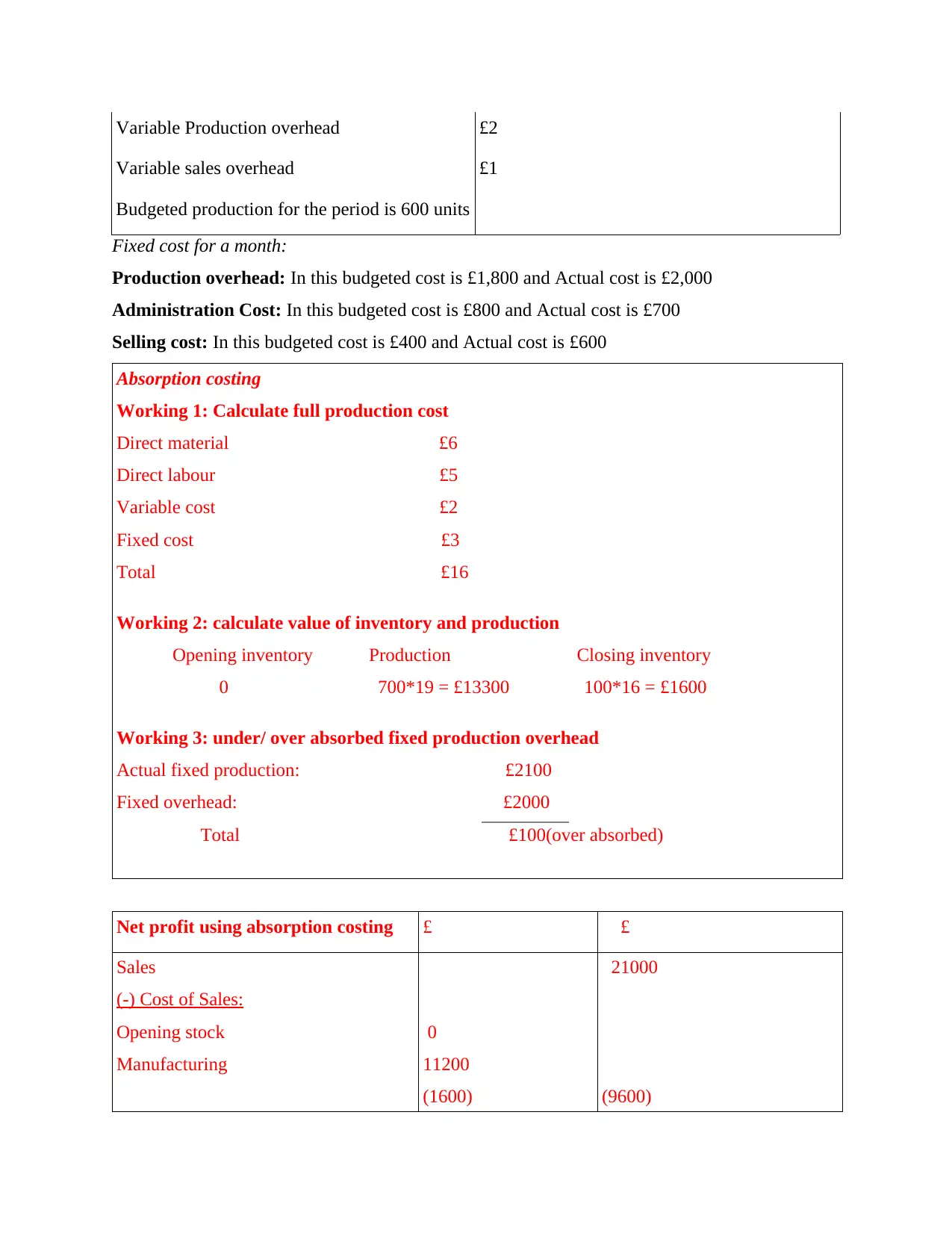

Variable Production overhead £2

Variable sales overhead £1

Budgeted production for the period is 600 units

Fixed cost for a month:

Production overhead: In this budgeted cost is £1,800 and Actual cost is £2,000

Administration Cost: In this budgeted cost is £800 and Actual cost is £700

Selling cost: In this budgeted cost is £400 and Actual cost is £600

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £2

Fixed cost £3

Total £16

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*16 = £1600

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £2100

Fixed overhead: £2000

Total £100(over absorbed)

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

0

11200

(1600)

21000

(9600)

Variable sales overhead £1

Budgeted production for the period is 600 units

Fixed cost for a month:

Production overhead: In this budgeted cost is £1,800 and Actual cost is £2,000

Administration Cost: In this budgeted cost is £800 and Actual cost is £700

Selling cost: In this budgeted cost is £400 and Actual cost is £600

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £2

Fixed cost £3

Total £16

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*16 = £1600

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £2100

Fixed overhead: £2000

Total £100(over absorbed)

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

0

11200

(1600)

21000

(9600)

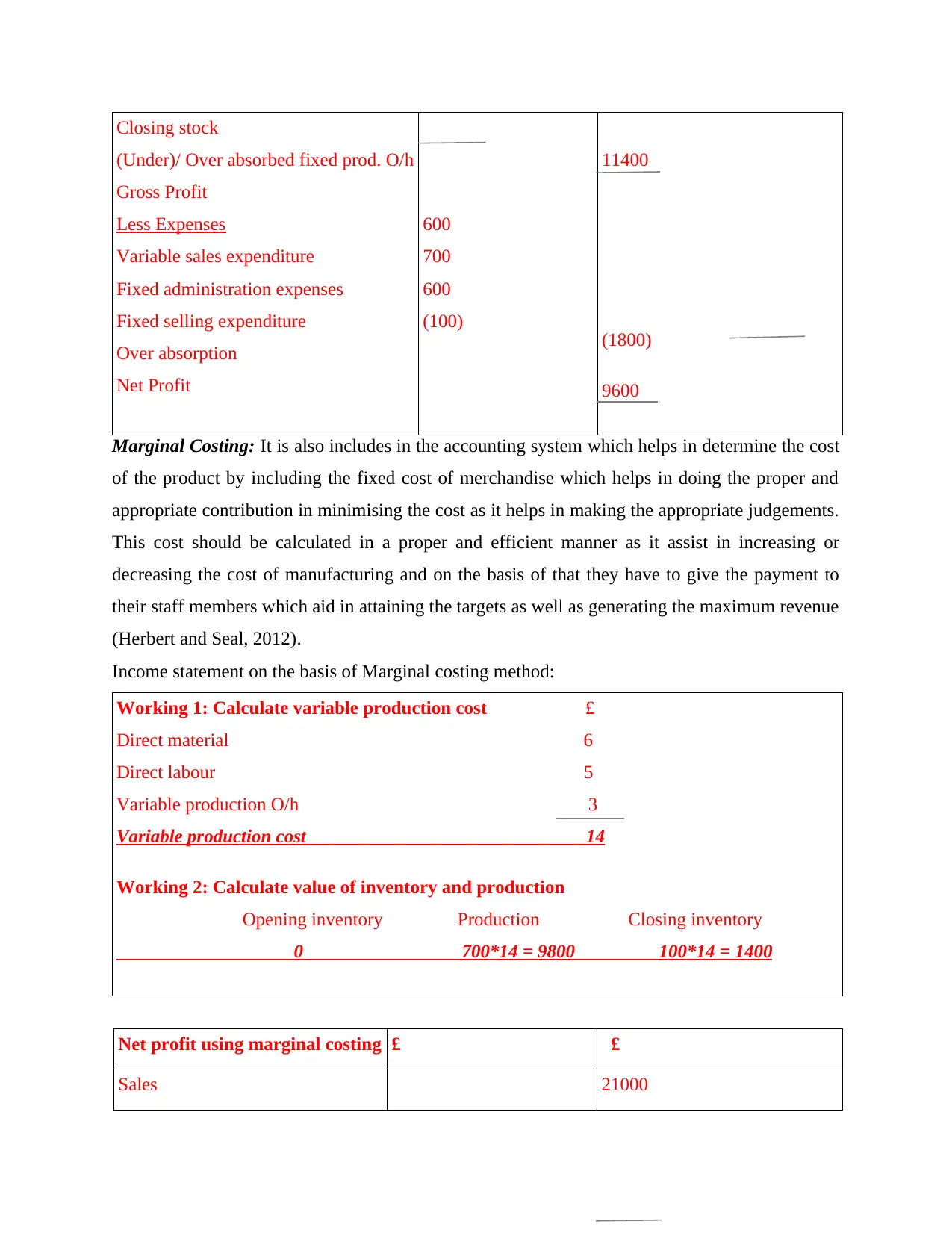

Closing stock

(Under)/ Over absorbed fixed prod. O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed administration expenses

Fixed selling expenditure

Over absorption

Net Profit

600

700

600

(100)

11400

(1800)

9600

Marginal Costing: It is also includes in the accounting system which helps in determine the cost

of the product by including the fixed cost of merchandise which helps in doing the proper and

appropriate contribution in minimising the cost as it helps in making the appropriate judgements.

This cost should be calculated in a proper and efficient manner as it assist in increasing or

decreasing the cost of manufacturing and on the basis of that they have to give the payment to

their staff members which aid in attaining the targets as well as generating the maximum revenue

(Herbert and Seal, 2012).

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Net profit using marginal costing £ £

Sales 21000

(Under)/ Over absorbed fixed prod. O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed administration expenses

Fixed selling expenditure

Over absorption

Net Profit

600

700

600

(100)

11400

(1800)

9600

Marginal Costing: It is also includes in the accounting system which helps in determine the cost

of the product by including the fixed cost of merchandise which helps in doing the proper and

appropriate contribution in minimising the cost as it helps in making the appropriate judgements.

This cost should be calculated in a proper and efficient manner as it assist in increasing or

decreasing the cost of manufacturing and on the basis of that they have to give the payment to

their staff members which aid in attaining the targets as well as generating the maximum revenue

(Herbert and Seal, 2012).

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Net profit using marginal costing £ £

Sales 21000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

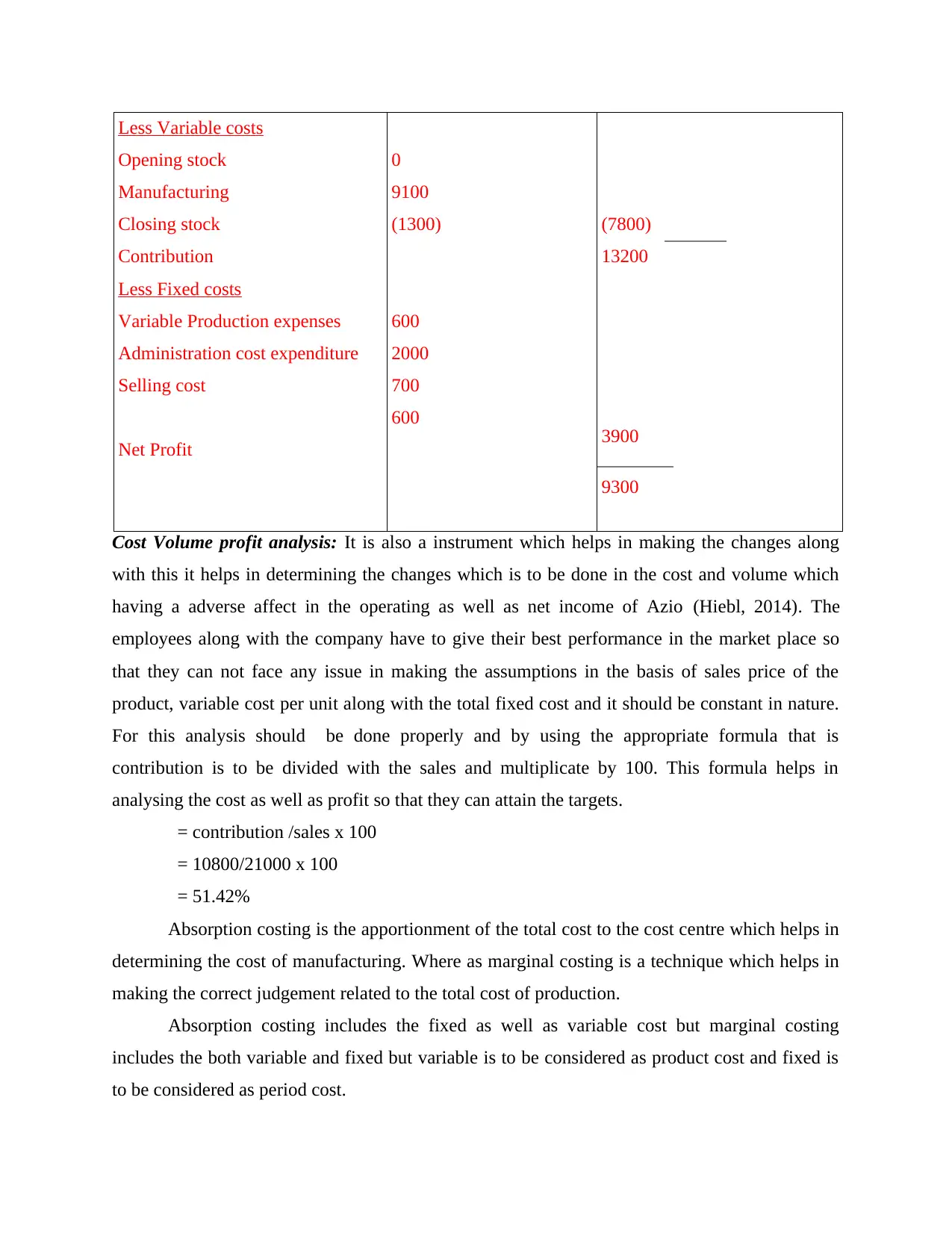

Less Variable costs

Opening stock

Manufacturing

Closing stock

Contribution

Less Fixed costs

Variable Production expenses

Administration cost expenditure

Selling cost

Net Profit

0

9100

(1300)

600

2000

700

600

(7800)

13200

3900

9300

Cost Volume profit analysis: It is also a instrument which helps in making the changes along

with this it helps in determining the changes which is to be done in the cost and volume which

having a adverse affect in the operating as well as net income of Azio (Hiebl, 2014). The

employees along with the company have to give their best performance in the market place so

that they can not face any issue in making the assumptions in the basis of sales price of the

product, variable cost per unit along with the total fixed cost and it should be constant in nature.

For this analysis should be done properly and by using the appropriate formula that is

contribution is to be divided with the sales and multiplicate by 100. This formula helps in

analysing the cost as well as profit so that they can attain the targets.

= contribution /sales x 100

= 10800/21000 x 100

= 51.42%

Absorption costing is the apportionment of the total cost to the cost centre which helps in

determining the cost of manufacturing. Where as marginal costing is a technique which helps in

making the correct judgement related to the total cost of production.

Absorption costing includes the fixed as well as variable cost but marginal costing

includes the both variable and fixed but variable is to be considered as product cost and fixed is

to be considered as period cost.

Opening stock

Manufacturing

Closing stock

Contribution

Less Fixed costs

Variable Production expenses

Administration cost expenditure

Selling cost

Net Profit

0

9100

(1300)

600

2000

700

600

(7800)

13200

3900

9300

Cost Volume profit analysis: It is also a instrument which helps in making the changes along

with this it helps in determining the changes which is to be done in the cost and volume which

having a adverse affect in the operating as well as net income of Azio (Hiebl, 2014). The

employees along with the company have to give their best performance in the market place so

that they can not face any issue in making the assumptions in the basis of sales price of the

product, variable cost per unit along with the total fixed cost and it should be constant in nature.

For this analysis should be done properly and by using the appropriate formula that is

contribution is to be divided with the sales and multiplicate by 100. This formula helps in

analysing the cost as well as profit so that they can attain the targets.

= contribution /sales x 100

= 10800/21000 x 100

= 51.42%

Absorption costing is the apportionment of the total cost to the cost centre which helps in

determining the cost of manufacturing. Where as marginal costing is a technique which helps in

making the correct judgement related to the total cost of production.

Absorption costing includes the fixed as well as variable cost but marginal costing

includes the both variable and fixed but variable is to be considered as product cost and fixed is

to be considered as period cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D2

The employees as well as manager of Azio have to provide the financial report in a

attractive way as it helps the investors in making the correct judgement. If the employees of the

business entity is using absorption costing then they get net profit is 6700 and if they are using

marginal costing then they are getting 7500 that means by using both techniques net profit of the

business entity is different and by that they can improve the performance in the market.

TASK 3

P4 Different planning tools which are included in budgetary control and its advantages and

disadvantages

There are different tools which help in doing planning which helps in doing the budgetary

control and they have to do the formal statement of the different resources which are related to

finance so that they carry out the different activities in a specific period of time. The employees

of Azio have to coordinate the different activities so that they can monitor the organisational

functions which are distinctive in nature. They have to maintain the standard by using the

appropriate control system (Jansen, 2011). There are different type of planning tools which can

be used by the company which includes:

Cash budget: It is also a type of budget which helps in doing the estimation of the inflow

and outflow of the cash for a business in a specific time. They have to analyse the different

things and they have to check that whether Azio have the sufficient cash or not to do all the

business operations. The main advantage of this budget is to identify or analyse the amount of

cash as they require to fulfil the needs and wants without the utilisation of the overdraft

protection. The employees of the business entity have to make the plans for the optimum

utilisation of the cash.

Capital Expenditure budget: This budget helps in maintaining the expenditure and also

they have to use the appropriate funds and resources which are used by the business entity so that

they acquire and upgrade the physical assets such as property, industrial buildings and

equipments. They have to use the appropriate budgets so that they can make the investments.

The employees have to do the appropriate calculations which help in doing the determination so

that they can make the correct investment decisions. This method helps in saving the time as well

as money so that every staff members can not face any issues (Kaplan and Atkinson, 2015).

The employees as well as manager of Azio have to provide the financial report in a

attractive way as it helps the investors in making the correct judgement. If the employees of the

business entity is using absorption costing then they get net profit is 6700 and if they are using

marginal costing then they are getting 7500 that means by using both techniques net profit of the

business entity is different and by that they can improve the performance in the market.

TASK 3

P4 Different planning tools which are included in budgetary control and its advantages and

disadvantages

There are different tools which help in doing planning which helps in doing the budgetary

control and they have to do the formal statement of the different resources which are related to

finance so that they carry out the different activities in a specific period of time. The employees

of Azio have to coordinate the different activities so that they can monitor the organisational

functions which are distinctive in nature. They have to maintain the standard by using the

appropriate control system (Jansen, 2011). There are different type of planning tools which can

be used by the company which includes:

Cash budget: It is also a type of budget which helps in doing the estimation of the inflow

and outflow of the cash for a business in a specific time. They have to analyse the different

things and they have to check that whether Azio have the sufficient cash or not to do all the

business operations. The main advantage of this budget is to identify or analyse the amount of

cash as they require to fulfil the needs and wants without the utilisation of the overdraft

protection. The employees of the business entity have to make the plans for the optimum

utilisation of the cash.

Capital Expenditure budget: This budget helps in maintaining the expenditure and also

they have to use the appropriate funds and resources which are used by the business entity so that

they acquire and upgrade the physical assets such as property, industrial buildings and

equipments. They have to use the appropriate budgets so that they can make the investments.

The employees have to do the appropriate calculations which help in doing the determination so

that they can make the correct investment decisions. This method helps in saving the time as well

as money so that every staff members can not face any issues (Kaplan and Atkinson, 2015).

Cost plus pricing method: It is also a cost method which helps in identifying the cost and

that is related to the direct material, direct labour as well as overheads of that product and

according to that they can determine the price of the product. It helps in finding out the exact

amount the expenditure as it helps in accomplishing the desired revenue. But this method having

a disadvantage also that is they have to take into account for the future demand of the products

and services and also have to decide the price of the product accordingly (Setthasakko, 2010).

Target cost pricing method: This approach helps in determining the cost and that is

determined in the product life cycle. Along with this it is sufficient to develop the functions of

the business entity along with the quality so that they can generate the maximum profits. They

have to target the cost by subtracting the desired profit margin so that they can get the

competitive price of the product which helps in attaining the success at the time of high

competition. It helps in creating the management which helps in identifying the desires and on

the basis of that they can make design along with the manufacturing products so that they can

meet the price and on the basis of that they can attain the success (Lee, 2011).

Market led pricing method: The employees of Azio have to use the appropriate marketing

strategy so that they can determine the price of the product. If the price of the merchandise is

high then consumer shift to the other and move to the another. They have to do the proper market

research so that they can provide the best products to their consumers. The employees of Azio

have to maintain the standards in the industry as well as they have to set the price which is

related to their life cycle (Sánchez-Rodríguez and Spraakman, 2012). The employees have to

manage the price so that they can attain the success in the market but this having a disadvantage

also that is based on pricing which is based on the price of the merchandise of the business

entity.

M3

There are different planning tools which can be used by the employees of Azio so that

they can put the proper control on their budgets as it helps in doing the expenditure for

purchasing the material which are used for them and on the basis of that they can provide the

best services and by that they can attain the goals and objectives as well as targets (Luft and

Shields, 2010). Along with this to maintain these budgets they have to manage all the data as it

succour in improving the performance along with the productivity of the company in the market

when they are facing high competition.

that is related to the direct material, direct labour as well as overheads of that product and

according to that they can determine the price of the product. It helps in finding out the exact

amount the expenditure as it helps in accomplishing the desired revenue. But this method having

a disadvantage also that is they have to take into account for the future demand of the products

and services and also have to decide the price of the product accordingly (Setthasakko, 2010).

Target cost pricing method: This approach helps in determining the cost and that is

determined in the product life cycle. Along with this it is sufficient to develop the functions of

the business entity along with the quality so that they can generate the maximum profits. They

have to target the cost by subtracting the desired profit margin so that they can get the

competitive price of the product which helps in attaining the success at the time of high

competition. It helps in creating the management which helps in identifying the desires and on

the basis of that they can make design along with the manufacturing products so that they can

meet the price and on the basis of that they can attain the success (Lee, 2011).

Market led pricing method: The employees of Azio have to use the appropriate marketing

strategy so that they can determine the price of the product. If the price of the merchandise is

high then consumer shift to the other and move to the another. They have to do the proper market

research so that they can provide the best products to their consumers. The employees of Azio

have to maintain the standards in the industry as well as they have to set the price which is

related to their life cycle (Sánchez-Rodríguez and Spraakman, 2012). The employees have to

manage the price so that they can attain the success in the market but this having a disadvantage

also that is based on pricing which is based on the price of the merchandise of the business

entity.

M3

There are different planning tools which can be used by the employees of Azio so that

they can put the proper control on their budgets as it helps in doing the expenditure for

purchasing the material which are used for them and on the basis of that they can provide the

best services and by that they can attain the goals and objectives as well as targets (Luft and

Shields, 2010). Along with this to maintain these budgets they have to manage all the data as it

succour in improving the performance along with the productivity of the company in the market

when they are facing high competition.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.