Management Accounting Report: Financial Analysis of IKEA's Operations

VerifiedAdded on 2022/11/25

|15

|4514

|242

Report

AI Summary

This report delves into the application of management accounting principles within IKEA, a multinational conglomerate. It begins with an introduction to management accounting, its core concepts, and different types, including traditional and lean accounting, and transfer pricing. The report then examines management accounting reporting, focusing on budget reports, account receivable aging reports, cost managerial accounting reports, and performance reporting. The analysis includes the advantages and disadvantages of various planning tools. The report provides calculation techniques and explores marginal and absorption costing methods. Overall, the report offers a comprehensive analysis of IKEA's financial strategies and operations, highlighting the significance of management accounting in achieving organizational goals and making informed decisions. Finally, the report concludes with a summary of the findings and references.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................2

Concept of management accounting and types...........................................................................2

Management accounting reporting..............................................................................................4

Analysis of cost............................................................................................................................6

Advantage and disadvantages of different planning tools.........................................................10

Management accounting system................................................................................................11

Conclusion.....................................................................................................................................12

Reference.......................................................................................................................................13

1

Introduction......................................................................................................................................2

Concept of management accounting and types...........................................................................2

Management accounting reporting..............................................................................................4

Analysis of cost............................................................................................................................6

Advantage and disadvantages of different planning tools.........................................................10

Management accounting system................................................................................................11

Conclusion.....................................................................................................................................12

Reference.......................................................................................................................................13

1

Introduction

Management Accounting status about the ongoing procedure of identifying recognising

interpreting and coordinating virus information to different managers at all the level of

organisation (Abdelmoneim and et.al 2021). This will help the organisation to attain its

predetermined goals. IKEA is a multinational conglomerate which deals in ready-to-assemble

furniture kitchen appliances and home accessories. This company operates in most of the

countries in the world such as Europe Middle East South Asia North America etc. In this report

Management Accounting and different types of Management Accounting system has been

mentioned for this company. Calculation using appropriate technique and marginal absorption

costing is also mentioned in this report. Various planning tools which is used for budgetary

reporting is being discussed in this report.

Concept of management accounting and types

Management Accounting often known as managerial accounting and cost accounting because it

provides all the relevant information of financial and non financial factor to the management of

the organisation. As every manager needs different information at all levels of Management

Accounting provides them various information which is being needed by each and every

manager at their level therefore management accounting is very necessary for the organisation.

Management Accounting known as the provision for financial and non financial factors and

information which is used by the management so that they may take accurate decisions and their

decision making process gets success. Management Accounting plays a great role in every

organisation. Management Accounting provides all the necessary information about the expenses

and income of IKEA the managers can take for the decisions in the favour of company. Main

objective of using Management accounting is that it provides accurate information to the

management and helps them to know the credit risk of the company and also it helps them in

making budget so that in future company do not lose any money. Management accounting also

give information to the lowest level of management of the organisation so that each department

gets their desired information and as per the information they can take further steps. Another

management accounting definition is that it analyse, summarise and communicate all the

financial information to the management.

Types of Management accounting

2

Management Accounting status about the ongoing procedure of identifying recognising

interpreting and coordinating virus information to different managers at all the level of

organisation (Abdelmoneim and et.al 2021). This will help the organisation to attain its

predetermined goals. IKEA is a multinational conglomerate which deals in ready-to-assemble

furniture kitchen appliances and home accessories. This company operates in most of the

countries in the world such as Europe Middle East South Asia North America etc. In this report

Management Accounting and different types of Management Accounting system has been

mentioned for this company. Calculation using appropriate technique and marginal absorption

costing is also mentioned in this report. Various planning tools which is used for budgetary

reporting is being discussed in this report.

Concept of management accounting and types

Management Accounting often known as managerial accounting and cost accounting because it

provides all the relevant information of financial and non financial factor to the management of

the organisation. As every manager needs different information at all levels of Management

Accounting provides them various information which is being needed by each and every

manager at their level therefore management accounting is very necessary for the organisation.

Management Accounting known as the provision for financial and non financial factors and

information which is used by the management so that they may take accurate decisions and their

decision making process gets success. Management Accounting plays a great role in every

organisation. Management Accounting provides all the necessary information about the expenses

and income of IKEA the managers can take for the decisions in the favour of company. Main

objective of using Management accounting is that it provides accurate information to the

management and helps them to know the credit risk of the company and also it helps them in

making budget so that in future company do not lose any money. Management accounting also

give information to the lowest level of management of the organisation so that each department

gets their desired information and as per the information they can take further steps. Another

management accounting definition is that it analyse, summarise and communicate all the

financial information to the management.

Types of Management accounting

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Traditional Management Accounting

Traditional Management Accounting helps in tracking the cost and reduced job costing in

process costing method. Each and every method of this determines how a company can

differentiate cost which is related with the different posts such as direct labour manufacturing

and direct materials. Job order costing is basically used for those companies who have large

projects and all cost impact on project. The four big industries and companies use traditional

Management Accounting system so that they make it accurate result about the overall cost in

expenses. As the name suggests it is oldest method of Management Accounting which is used in

past years and still some companies follow traditional Management Accounting system. Its mean

m is to determine and analyse the way in which company distributes various cost such as

material, labour and overhead. Traditional Management Accounting provides all the information

about the cost and expenses to the company so that as per the expenses they may set profit

margin and generate good return.

Lean accounting

Lean accounting is one of the most usable techniques in the management accounting. It does not

focus on single cost but it refers to creating various strategies so that management can eliminate

waste from the organisation by minimising cost of each and every expenses (El 2021). Apart

from this lean Management Accounting provides immediate financial information to the

management so that they can make various decisions and strategies to overcome cost. This is

another method of Management Accounting system which is quite popular among all the

companies and forms. This method do not provide single information about single coast of any

product but it produces various strategies in front of the management which is related to the

overall costing and how management can mitigate the costing of production is being explain by

this accounting system. It also focuses on providing financial information so that management

can create proper strategies and increase the profitability of company.

Transfer pricing

Transfer pricing is also common Management Accounting system this method states that each

cost of goods are different from other goods because each product has to go through various

departments. Therefore the cost of each product should be different from other product because it

totally depends on the manufacturing process. The overall cost of each and every product at the

management to decide the prices of every product so that they may provide flexibility to the

3

Traditional Management Accounting helps in tracking the cost and reduced job costing in

process costing method. Each and every method of this determines how a company can

differentiate cost which is related with the different posts such as direct labour manufacturing

and direct materials. Job order costing is basically used for those companies who have large

projects and all cost impact on project. The four big industries and companies use traditional

Management Accounting system so that they make it accurate result about the overall cost in

expenses. As the name suggests it is oldest method of Management Accounting which is used in

past years and still some companies follow traditional Management Accounting system. Its mean

m is to determine and analyse the way in which company distributes various cost such as

material, labour and overhead. Traditional Management Accounting provides all the information

about the cost and expenses to the company so that as per the expenses they may set profit

margin and generate good return.

Lean accounting

Lean accounting is one of the most usable techniques in the management accounting. It does not

focus on single cost but it refers to creating various strategies so that management can eliminate

waste from the organisation by minimising cost of each and every expenses (El 2021). Apart

from this lean Management Accounting provides immediate financial information to the

management so that they can make various decisions and strategies to overcome cost. This is

another method of Management Accounting system which is quite popular among all the

companies and forms. This method do not provide single information about single coast of any

product but it produces various strategies in front of the management which is related to the

overall costing and how management can mitigate the costing of production is being explain by

this accounting system. It also focuses on providing financial information so that management

can create proper strategies and increase the profitability of company.

Transfer pricing

Transfer pricing is also common Management Accounting system this method states that each

cost of goods are different from other goods because each product has to go through various

departments. Therefore the cost of each product should be different from other product because it

totally depends on the manufacturing process. The overall cost of each and every product at the

management to decide the prices of every product so that they may provide flexibility to the

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

consumer as well. As the name amplifies this Management Accounting system helps the

management to decide various cost of each and every product. This system believes that every

product has to go through from different departments for the manufacturing and therefore the

value of each product is different from other. So it is the responsibility of management that they

must make sure prices of each and every product and as per the prices organisation can attend

good income and profit. These are the popular methods of Management Accounting system

which helps the management to determine cost and also manage the expenses.

Management accounting reporting

Management accounting system is useful for tracking all the financial information and efficiency

of internal management to attain the objective of the organisation.

Management Accounting reports are basically used to gather the inside information of the

organisation. Management accounting report helps the management for making plants setting

regulations and measuring the overall performance of the organisation. These reports are

generated throughout the accounting year of the organisation so that management can make for

the decisions in the favour of the company. Main objective of management accounting is to

provide insight and detailed information about the factors whether they are financial or

nonfinancial to the management of organisation. To provide these details information there are

various management reports have been generated so that accurate information can be shared.

Budget report

Budget reporting plays a critical role in the entire organisation because it helps in measuring the

overall performance of the company for the accounting period (Möller and et.al 2020). Budget

provides all the relevant information to the management for the cost and expenses of the

company along with this whatever income which is being generated by the company is also

mentioned in the budget. Management of the organisation can take help from the previous

budget reports as well so that they will get guidance how to prepare it budget for the company.

Budget plays a critical role in the overall development of any organisation because at assist the

management so that they may measure entire performance of the company. This report only

becomes impossible on the size and income level of organisation. Budget report can be prepared

on the basis of departments because each department has different work from others and

therefore they need different budget as well. The main objective of preparing budget is to face

uncertain situations (Ardiansyah and et.al 2017). In the uncertain situation completely not face

4

management to decide various cost of each and every product. This system believes that every

product has to go through from different departments for the manufacturing and therefore the

value of each product is different from other. So it is the responsibility of management that they

must make sure prices of each and every product and as per the prices organisation can attend

good income and profit. These are the popular methods of Management Accounting system

which helps the management to determine cost and also manage the expenses.

Management accounting reporting

Management accounting system is useful for tracking all the financial information and efficiency

of internal management to attain the objective of the organisation.

Management Accounting reports are basically used to gather the inside information of the

organisation. Management accounting report helps the management for making plants setting

regulations and measuring the overall performance of the organisation. These reports are

generated throughout the accounting year of the organisation so that management can make for

the decisions in the favour of the company. Main objective of management accounting is to

provide insight and detailed information about the factors whether they are financial or

nonfinancial to the management of organisation. To provide these details information there are

various management reports have been generated so that accurate information can be shared.

Budget report

Budget reporting plays a critical role in the entire organisation because it helps in measuring the

overall performance of the company for the accounting period (Möller and et.al 2020). Budget

provides all the relevant information to the management for the cost and expenses of the

company along with this whatever income which is being generated by the company is also

mentioned in the budget. Management of the organisation can take help from the previous

budget reports as well so that they will get guidance how to prepare it budget for the company.

Budget plays a critical role in the overall development of any organisation because at assist the

management so that they may measure entire performance of the company. This report only

becomes impossible on the size and income level of organisation. Budget report can be prepared

on the basis of departments because each department has different work from others and

therefore they need different budget as well. The main objective of preparing budget is to face

uncertain situations (Ardiansyah and et.al 2017). In the uncertain situation completely not face

4

any kind of loss that for management focuses on preparing budget. In some organisation

management take help from previous budget as well so that they will know better options. Apart

from this budget report is useful for the company because it provides the necessary details about

the overall production and sales to the organisation. With the help of budget company can know

how much profit they have earned in the previous years and how much efforts they have to put

more so that they can increase the overall profitability in the upcoming years as well. As per the

budget company can estimated that how much earning they will go to have in the near future and

how much expenses they have to put more so that Limited high profitability.

Account receivable aging report

Account receivable aging report is necessary for those business who do not put cash an

investment in the business but they totally depends on the credit. In this situation account aging

report is necessary to calculate the amount of credit (Assunção and et.al 2020). When the

company totally depends on the credit then the chances of default also increases and the

management of the company need to prepare various strategies to overcome the default and also

them make some policies for bad debts. This report only works on those businesses which totally

dependent on credit. It helps the management to identify bad debts that will not pay the amount

on time to the company. This report will help to find out defaulters and by knowing who are the

defaulters? organisation can reduce defaulters and prepare strong Strategies and policies for the

recovery of bad debts.

Cost managerial accounting report

Cost managerial accounting reports provide necessary information about the material cost

overheads labour and other type of cost which is being imposed on the organisation. This report

provides necessary information about whatever inventory is has been wasted in the production

and also the costing of labour and other expenses such as promotional marketing for the

organisation. As the name indicates this report provides all the necessary information about the

cost of products. It provides all the necessary information about the various raw materials and

other equipments which is used by the company in the process of production. This cost also

provides necessary information about the wages and salary of employees and workers so that by

deciding accurate profit margin company can attend good profit. This report plays a very

essential role in the overall development and growth of the organisation. As it provides very

important details about cost so that company can know how much expenses they have put to

5

management take help from previous budget as well so that they will know better options. Apart

from this budget report is useful for the company because it provides the necessary details about

the overall production and sales to the organisation. With the help of budget company can know

how much profit they have earned in the previous years and how much efforts they have to put

more so that they can increase the overall profitability in the upcoming years as well. As per the

budget company can estimated that how much earning they will go to have in the near future and

how much expenses they have to put more so that Limited high profitability.

Account receivable aging report

Account receivable aging report is necessary for those business who do not put cash an

investment in the business but they totally depends on the credit. In this situation account aging

report is necessary to calculate the amount of credit (Assunção and et.al 2020). When the

company totally depends on the credit then the chances of default also increases and the

management of the company need to prepare various strategies to overcome the default and also

them make some policies for bad debts. This report only works on those businesses which totally

dependent on credit. It helps the management to identify bad debts that will not pay the amount

on time to the company. This report will help to find out defaulters and by knowing who are the

defaulters? organisation can reduce defaulters and prepare strong Strategies and policies for the

recovery of bad debts.

Cost managerial accounting report

Cost managerial accounting reports provide necessary information about the material cost

overheads labour and other type of cost which is being imposed on the organisation. This report

provides necessary information about whatever inventory is has been wasted in the production

and also the costing of labour and other expenses such as promotional marketing for the

organisation. As the name indicates this report provides all the necessary information about the

cost of products. It provides all the necessary information about the various raw materials and

other equipments which is used by the company in the process of production. This cost also

provides necessary information about the wages and salary of employees and workers so that by

deciding accurate profit margin company can attend good profit. This report plays a very

essential role in the overall development and growth of the organisation. As it provides very

important details about cost so that company can know how much expenses they have put to

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

generate a product or services. Along with this with the help of knowing proper cost of the

product company may take appropriate prices from their loyal customers so that customers will

not have to face any kind of issues in paying the appropriate prices of the product and services.

On the other hand this report also helps the company to determine the prices as per the market

needs and demands if the demand of the product is low in the market then they provide some

discounts and cut down the prices of the products that company can increase the overall demand

of the product in the market.

Performance reporting

This is one of the important reporting which every organisation maintained no matter that they

are small medium and large business but every organisation wants to check their performance.

Performance reporting helps the management to create key strategies for the organisation so that

in future they do not under perform and they give tough competition to other companies (Pepple,

and et.al 2021). This report also provides detailed information about the weaknesses of the

company as well. the company for the given time duration. This report will state that is the

company performing as per the Expectations of the management or not. If the company is not

meeting the Expectations then management has to change Strategies and they have to put more

focus on promotion and marketing activities. On the other hand if the company is performing

well then it is the responsibility of management that company should follow the same Strategies

and earn more profitability in the near future. With the help of proper performance report

organisation can easily know that performance and position in the market. By preparing

performance report organisation can get to know that they are ahead of competitors or not and

what are the strategies have been employed by their competitors to gain the market share.

Another reason of preparing performance report is that coming in easily know their drawbacks

and take input changes and efforts so that they can easily overcome from such drawbacks and

convert their weaknesses into strength.

Analysis of cost

Absorption cost

Absorption costing talks about various methods of costing which provides detailed information

about the overall cost of manufacture. Absorption costing method is quite popular among

manufacturers because it provides all the information about the cost of each and every product

which is being produced by the manufacturer (Rudnäs, 2019). Absorption costing includes direct

6

product company may take appropriate prices from their loyal customers so that customers will

not have to face any kind of issues in paying the appropriate prices of the product and services.

On the other hand this report also helps the company to determine the prices as per the market

needs and demands if the demand of the product is low in the market then they provide some

discounts and cut down the prices of the products that company can increase the overall demand

of the product in the market.

Performance reporting

This is one of the important reporting which every organisation maintained no matter that they

are small medium and large business but every organisation wants to check their performance.

Performance reporting helps the management to create key strategies for the organisation so that

in future they do not under perform and they give tough competition to other companies (Pepple,

and et.al 2021). This report also provides detailed information about the weaknesses of the

company as well. the company for the given time duration. This report will state that is the

company performing as per the Expectations of the management or not. If the company is not

meeting the Expectations then management has to change Strategies and they have to put more

focus on promotion and marketing activities. On the other hand if the company is performing

well then it is the responsibility of management that company should follow the same Strategies

and earn more profitability in the near future. With the help of proper performance report

organisation can easily know that performance and position in the market. By preparing

performance report organisation can get to know that they are ahead of competitors or not and

what are the strategies have been employed by their competitors to gain the market share.

Another reason of preparing performance report is that coming in easily know their drawbacks

and take input changes and efforts so that they can easily overcome from such drawbacks and

convert their weaknesses into strength.

Analysis of cost

Absorption cost

Absorption costing talks about various methods of costing which provides detailed information

about the overall cost of manufacture. Absorption costing method is quite popular among

manufacturers because it provides all the information about the cost of each and every product

which is being produced by the manufacturer (Rudnäs, 2019). Absorption costing includes direct

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cost of material labour and other overheads so that it can produce accurate result to the

organisation. The biggest advantage of using absorption costing is that it accurately tracks all the

profit which is being imposed to the company by variable costing. Variable costing status about

all account of production cost and various table cost aspects that at the and Organisation can get

to know the accurate pricing of each and every product. Another advantage of absorption costing

is that it assists the management to create such Strategies and policies through which the

operating income of the company can be increased within a given time duration. It also assist the

management to increase the overall production so that company can easily fulfil the market

demand and specific needs of their customer (Vijaya, 2020). Absorption costing also recognises

the value of fixed production cost in establishing the pricing policy. It provides detailed

information to the management so that with the help of absorption costing all the pricing of each

and every product can be recorded. Absorption costing provides benefit to the organisation in the

long run because it provides margin profit to the organisation and cover all the fixed cost of the

company. Absorption costing also helps the organisation to know the level of sales in the future

as well so that as per the need of future demand off market company can provide proper supply

in the market. Along with this if company faces any kind of loss then it is also being covered by

absorption costing. Another main purpose of using absorption costing is that it provides external

reports for the stock valuation to the company. Absorption costing also provides information

about and absorption and over absorption of various factory overheads. Absorption costing it is

useful for various managers of different departments because it allocates fixed factory overheads

to different departments so that the company may know how much department is spending how

much amount on the production.

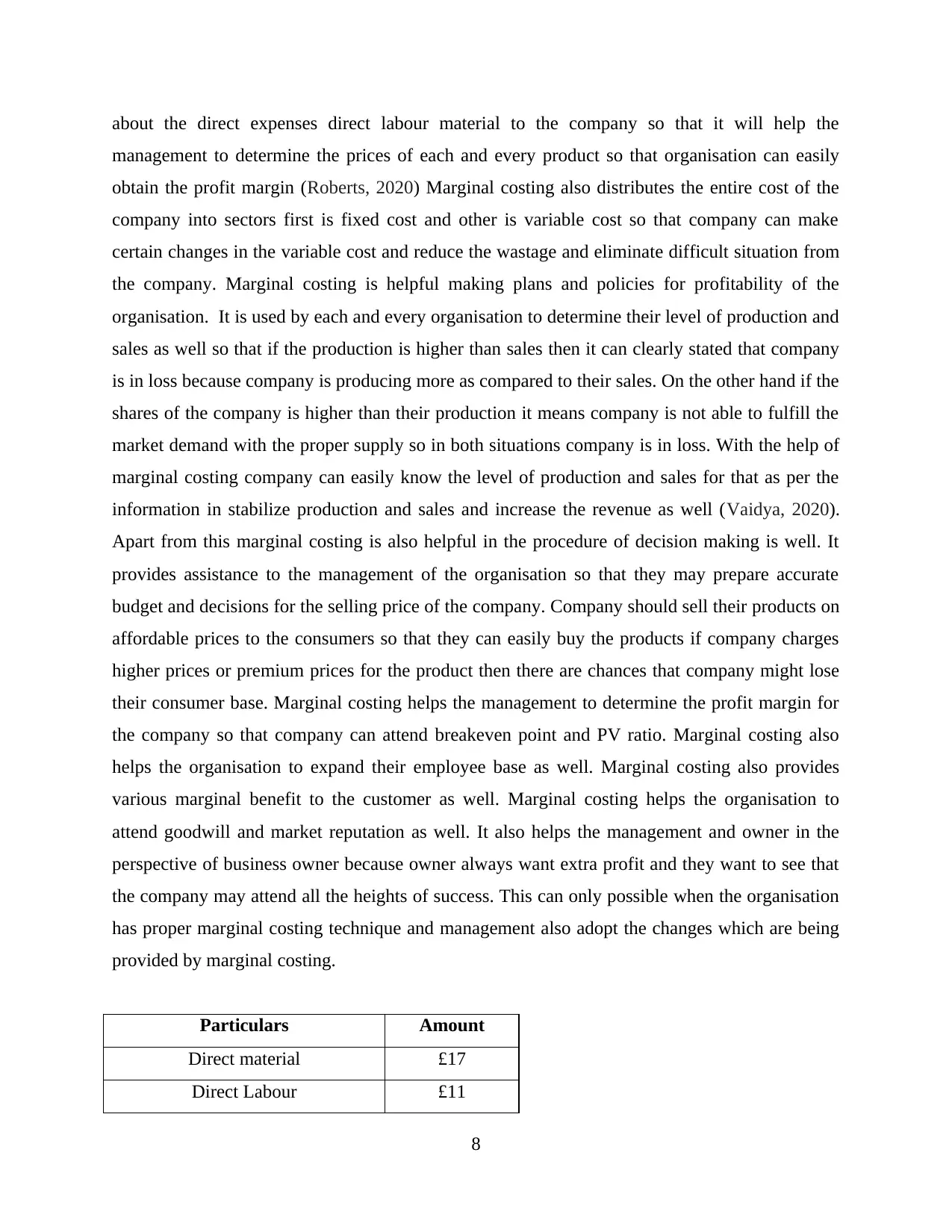

Marginal costing

Marginal costing refers to the techniques of defining the marginal cost such as variable cost is

getting changed with the units of cost on the other hand fixed cost of the units can get written off

against different contributions (Priyatmo and et. al2019). Marginal costing also implies about the

buffer and additional cost involved in the production of extra units. Marginal Costing includes

direct material direct labour and where is a direct expense to provide accurate results to the

organisation. Marginal costing is helpful for the valuation of the stock of the organisation so that

they may know the market price of the products and services of the company apart from this it

also measure the profitability for the organisation. As marginal costing provides all the details

7

organisation. The biggest advantage of using absorption costing is that it accurately tracks all the

profit which is being imposed to the company by variable costing. Variable costing status about

all account of production cost and various table cost aspects that at the and Organisation can get

to know the accurate pricing of each and every product. Another advantage of absorption costing

is that it assists the management to create such Strategies and policies through which the

operating income of the company can be increased within a given time duration. It also assist the

management to increase the overall production so that company can easily fulfil the market

demand and specific needs of their customer (Vijaya, 2020). Absorption costing also recognises

the value of fixed production cost in establishing the pricing policy. It provides detailed

information to the management so that with the help of absorption costing all the pricing of each

and every product can be recorded. Absorption costing provides benefit to the organisation in the

long run because it provides margin profit to the organisation and cover all the fixed cost of the

company. Absorption costing also helps the organisation to know the level of sales in the future

as well so that as per the need of future demand off market company can provide proper supply

in the market. Along with this if company faces any kind of loss then it is also being covered by

absorption costing. Another main purpose of using absorption costing is that it provides external

reports for the stock valuation to the company. Absorption costing also provides information

about and absorption and over absorption of various factory overheads. Absorption costing it is

useful for various managers of different departments because it allocates fixed factory overheads

to different departments so that the company may know how much department is spending how

much amount on the production.

Marginal costing

Marginal costing refers to the techniques of defining the marginal cost such as variable cost is

getting changed with the units of cost on the other hand fixed cost of the units can get written off

against different contributions (Priyatmo and et. al2019). Marginal costing also implies about the

buffer and additional cost involved in the production of extra units. Marginal Costing includes

direct material direct labour and where is a direct expense to provide accurate results to the

organisation. Marginal costing is helpful for the valuation of the stock of the organisation so that

they may know the market price of the products and services of the company apart from this it

also measure the profitability for the organisation. As marginal costing provides all the details

7

about the direct expenses direct labour material to the company so that it will help the

management to determine the prices of each and every product so that organisation can easily

obtain the profit margin (Roberts, 2020) Marginal costing also distributes the entire cost of the

company into sectors first is fixed cost and other is variable cost so that company can make

certain changes in the variable cost and reduce the wastage and eliminate difficult situation from

the company. Marginal costing is helpful making plans and policies for profitability of the

organisation. It is used by each and every organisation to determine their level of production and

sales as well so that if the production is higher than sales then it can clearly stated that company

is in loss because company is producing more as compared to their sales. On the other hand if the

shares of the company is higher than their production it means company is not able to fulfill the

market demand with the proper supply so in both situations company is in loss. With the help of

marginal costing company can easily know the level of production and sales for that as per the

information in stabilize production and sales and increase the revenue as well (Vaidya, 2020).

Apart from this marginal costing is also helpful in the procedure of decision making is well. It

provides assistance to the management of the organisation so that they may prepare accurate

budget and decisions for the selling price of the company. Company should sell their products on

affordable prices to the consumers so that they can easily buy the products if company charges

higher prices or premium prices for the product then there are chances that company might lose

their consumer base. Marginal costing helps the management to determine the profit margin for

the company so that company can attend breakeven point and PV ratio. Marginal costing also

helps the organisation to expand their employee base as well. Marginal costing also provides

various marginal benefit to the customer as well. Marginal costing helps the organisation to

attend goodwill and market reputation as well. It also helps the management and owner in the

perspective of business owner because owner always want extra profit and they want to see that

the company may attend all the heights of success. This can only possible when the organisation

has proper marginal costing technique and management also adopt the changes which are being

provided by marginal costing.

Particulars Amount

Direct material £17

Direct Labour £11

8

management to determine the prices of each and every product so that organisation can easily

obtain the profit margin (Roberts, 2020) Marginal costing also distributes the entire cost of the

company into sectors first is fixed cost and other is variable cost so that company can make

certain changes in the variable cost and reduce the wastage and eliminate difficult situation from

the company. Marginal costing is helpful making plans and policies for profitability of the

organisation. It is used by each and every organisation to determine their level of production and

sales as well so that if the production is higher than sales then it can clearly stated that company

is in loss because company is producing more as compared to their sales. On the other hand if the

shares of the company is higher than their production it means company is not able to fulfill the

market demand with the proper supply so in both situations company is in loss. With the help of

marginal costing company can easily know the level of production and sales for that as per the

information in stabilize production and sales and increase the revenue as well (Vaidya, 2020).

Apart from this marginal costing is also helpful in the procedure of decision making is well. It

provides assistance to the management of the organisation so that they may prepare accurate

budget and decisions for the selling price of the company. Company should sell their products on

affordable prices to the consumers so that they can easily buy the products if company charges

higher prices or premium prices for the product then there are chances that company might lose

their consumer base. Marginal costing helps the management to determine the profit margin for

the company so that company can attend breakeven point and PV ratio. Marginal costing also

helps the organisation to expand their employee base as well. Marginal costing also provides

various marginal benefit to the customer as well. Marginal costing helps the organisation to

attend goodwill and market reputation as well. It also helps the management and owner in the

perspective of business owner because owner always want extra profit and they want to see that

the company may attend all the heights of success. This can only possible when the organisation

has proper marginal costing technique and management also adopt the changes which are being

provided by marginal costing.

Particulars Amount

Direct material £17

Direct Labour £11

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

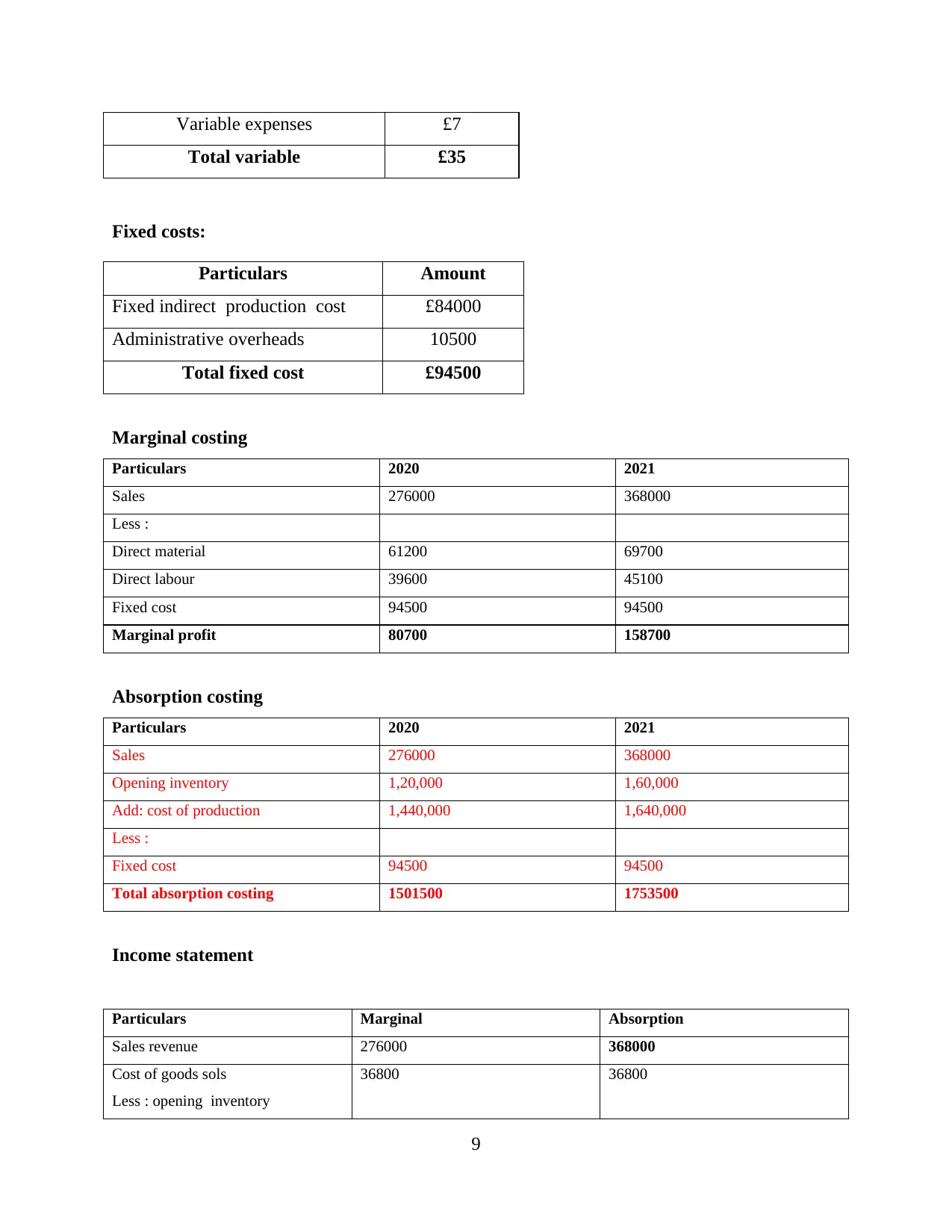

Variable expenses £7

Total variable £35

Fixed costs:

Particulars Amount

Fixed indirect production cost £84000

Administrative overheads 10500

Total fixed cost £94500

Marginal costing

Particulars 2020 2021

Sales 276000 368000

Less :

Direct material 61200 69700

Direct labour 39600 45100

Fixed cost 94500 94500

Marginal profit 80700 158700

Absorption costing

Particulars 2020 2021

Sales 276000 368000

Opening inventory 1,20,000 1,60,000

Add: cost of production 1,440,000 1,640,000

Less :

Fixed cost 94500 94500

Total absorption costing 1501500 1753500

Income statement

Particulars Marginal Absorption

Sales revenue 276000 368000

Cost of goods sols

Less : opening inventory

36800 36800

9

Total variable £35

Fixed costs:

Particulars Amount

Fixed indirect production cost £84000

Administrative overheads 10500

Total fixed cost £94500

Marginal costing

Particulars 2020 2021

Sales 276000 368000

Less :

Direct material 61200 69700

Direct labour 39600 45100

Fixed cost 94500 94500

Marginal profit 80700 158700

Absorption costing

Particulars 2020 2021

Sales 276000 368000

Opening inventory 1,20,000 1,60,000

Add: cost of production 1,440,000 1,640,000

Less :

Fixed cost 94500 94500

Total absorption costing 1501500 1753500

Income statement

Particulars Marginal Absorption

Sales revenue 276000 368000

Cost of goods sols

Less : opening inventory

36800 36800

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

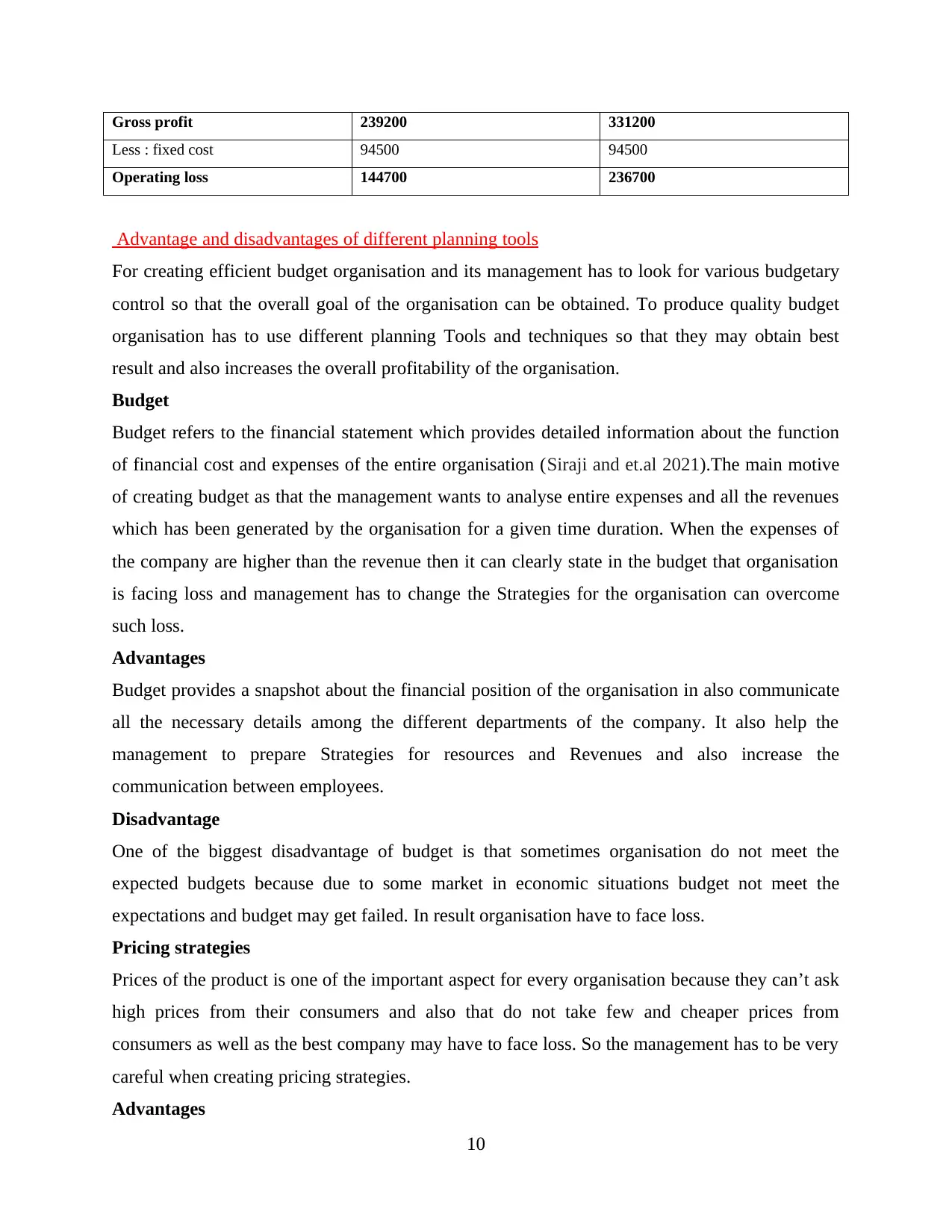

Gross profit 239200 331200

Less : fixed cost 94500 94500

Operating loss 144700 236700

Advantage and disadvantages of different planning tools

For creating efficient budget organisation and its management has to look for various budgetary

control so that the overall goal of the organisation can be obtained. To produce quality budget

organisation has to use different planning Tools and techniques so that they may obtain best

result and also increases the overall profitability of the organisation.

Budget

Budget refers to the financial statement which provides detailed information about the function

of financial cost and expenses of the entire organisation (Siraji and et.al 2021).The main motive

of creating budget as that the management wants to analyse entire expenses and all the revenues

which has been generated by the organisation for a given time duration. When the expenses of

the company are higher than the revenue then it can clearly state in the budget that organisation

is facing loss and management has to change the Strategies for the organisation can overcome

such loss.

Advantages

Budget provides a snapshot about the financial position of the organisation in also communicate

all the necessary details among the different departments of the company. It also help the

management to prepare Strategies for resources and Revenues and also increase the

communication between employees.

Disadvantage

One of the biggest disadvantage of budget is that sometimes organisation do not meet the

expected budgets because due to some market in economic situations budget not meet the

expectations and budget may get failed. In result organisation have to face loss.

Pricing strategies

Prices of the product is one of the important aspect for every organisation because they can’t ask

high prices from their consumers and also that do not take few and cheaper prices from

consumers as well as the best company may have to face loss. So the management has to be very

careful when creating pricing strategies.

Advantages

10

Less : fixed cost 94500 94500

Operating loss 144700 236700

Advantage and disadvantages of different planning tools

For creating efficient budget organisation and its management has to look for various budgetary

control so that the overall goal of the organisation can be obtained. To produce quality budget

organisation has to use different planning Tools and techniques so that they may obtain best

result and also increases the overall profitability of the organisation.

Budget

Budget refers to the financial statement which provides detailed information about the function

of financial cost and expenses of the entire organisation (Siraji and et.al 2021).The main motive

of creating budget as that the management wants to analyse entire expenses and all the revenues

which has been generated by the organisation for a given time duration. When the expenses of

the company are higher than the revenue then it can clearly state in the budget that organisation

is facing loss and management has to change the Strategies for the organisation can overcome

such loss.

Advantages

Budget provides a snapshot about the financial position of the organisation in also communicate

all the necessary details among the different departments of the company. It also help the

management to prepare Strategies for resources and Revenues and also increase the

communication between employees.

Disadvantage

One of the biggest disadvantage of budget is that sometimes organisation do not meet the

expected budgets because due to some market in economic situations budget not meet the

expectations and budget may get failed. In result organisation have to face loss.

Pricing strategies

Prices of the product is one of the important aspect for every organisation because they can’t ask

high prices from their consumers and also that do not take few and cheaper prices from

consumers as well as the best company may have to face loss. So the management has to be very

careful when creating pricing strategies.

Advantages

10

This is in the hands of Management to create suitable pricing strategy for the organisation so that

they may get profitability (TUAN, 2020). Another advantage of pricing strategy is that it can

increase the sales and revenue for the company if the prices of the product are suitable.

Disadvantages

The management set high prices for the product then the overall profitability will get decreased

and it also damages the goodwill and reputation of the organisation.

This organisation is going to adopt budget planning tool which will help the company to prepare

proper budgets for the upcoming year. This is one of the biggest advantage of this planning tool

that organisation can clearly attain the goal.

Management accounting system

Every organisation uses various accounting system because it helps the management to predict

the profitability and various difficulties which is concerned with the financial and non financial

factors of the organisation (Nan, 2019). Management Accounting system identify these factors so

that they do not put any damage and impact on the financial position and profitability of the

organisation.

Liquidity ratio

Liquidity ratio is one of the important aspect for every organisation because it provides snapshot

of overall financial health of the organisation and how company is able to meet their long-term

and short-term obligations. This will also help the organisation to determine proper availability

of cash so that they may meet the specific short term goals of the organisation.

Profitability ratio

As the name implies profitability ratio is used to measure the overall profit of the organisation

and also it provides in-depth information about the ability to generate earnings for the company.

Apart from this profitability ratio also produce quality information about the revenue of the

companies of that their shareholders can put more money in the company and by using that

Money Company can go for further investment.

Non financial factors

Human resources

Human resources are the important factor for every organisation because with the help of human

resources company can produce quality products and services and also they can provide best

11

they may get profitability (TUAN, 2020). Another advantage of pricing strategy is that it can

increase the sales and revenue for the company if the prices of the product are suitable.

Disadvantages

The management set high prices for the product then the overall profitability will get decreased

and it also damages the goodwill and reputation of the organisation.

This organisation is going to adopt budget planning tool which will help the company to prepare

proper budgets for the upcoming year. This is one of the biggest advantage of this planning tool

that organisation can clearly attain the goal.

Management accounting system

Every organisation uses various accounting system because it helps the management to predict

the profitability and various difficulties which is concerned with the financial and non financial

factors of the organisation (Nan, 2019). Management Accounting system identify these factors so

that they do not put any damage and impact on the financial position and profitability of the

organisation.

Liquidity ratio

Liquidity ratio is one of the important aspect for every organisation because it provides snapshot

of overall financial health of the organisation and how company is able to meet their long-term

and short-term obligations. This will also help the organisation to determine proper availability

of cash so that they may meet the specific short term goals of the organisation.

Profitability ratio

As the name implies profitability ratio is used to measure the overall profit of the organisation

and also it provides in-depth information about the ability to generate earnings for the company.

Apart from this profitability ratio also produce quality information about the revenue of the

companies of that their shareholders can put more money in the company and by using that

Money Company can go for further investment.

Non financial factors

Human resources

Human resources are the important factor for every organisation because with the help of human

resources company can produce quality products and services and also they can provide best

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.