Financial Accounting Report: Linda's Business Transaction Analysis

VerifiedAdded on 2022/12/26

|20

|2774

|34

Report

AI Summary

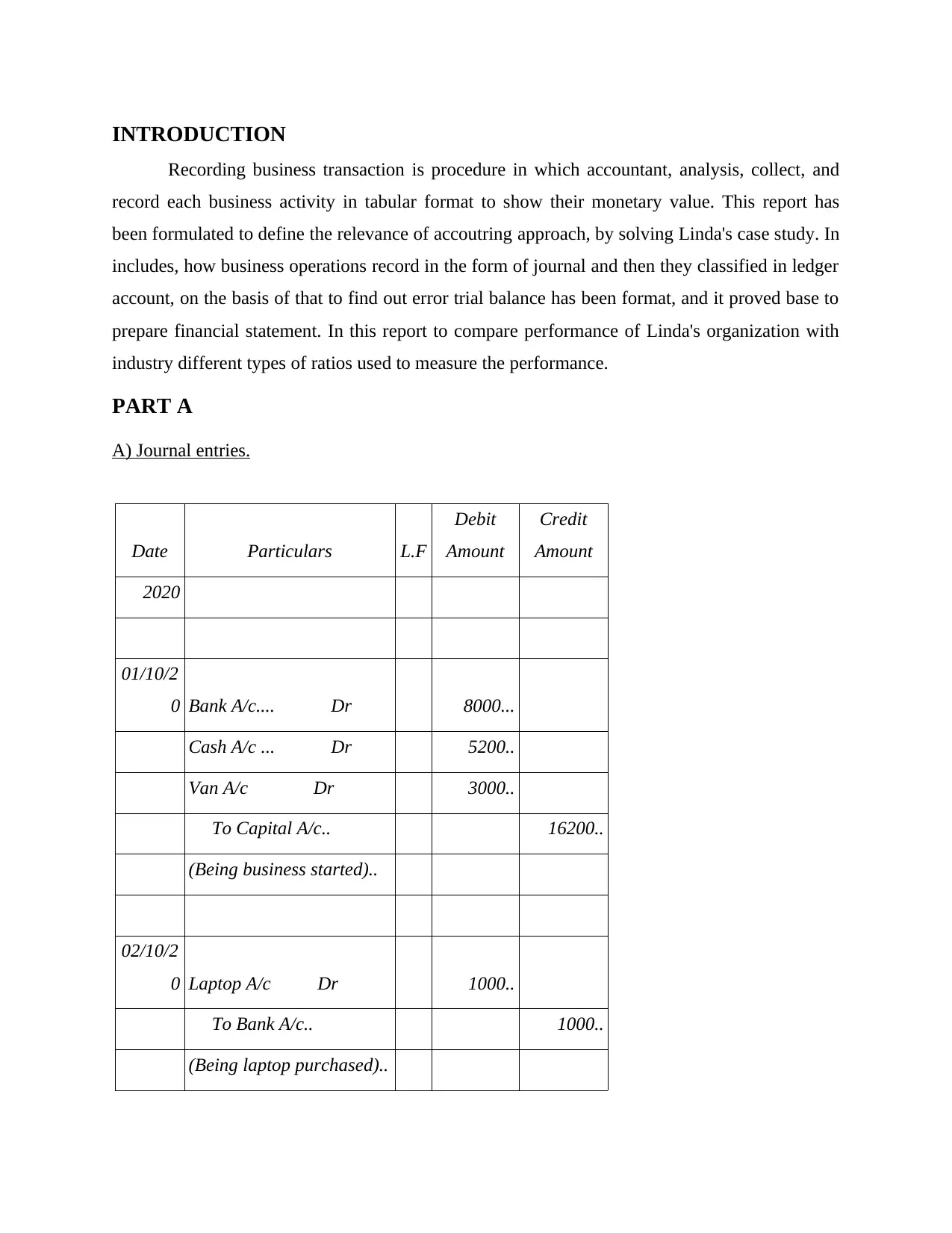

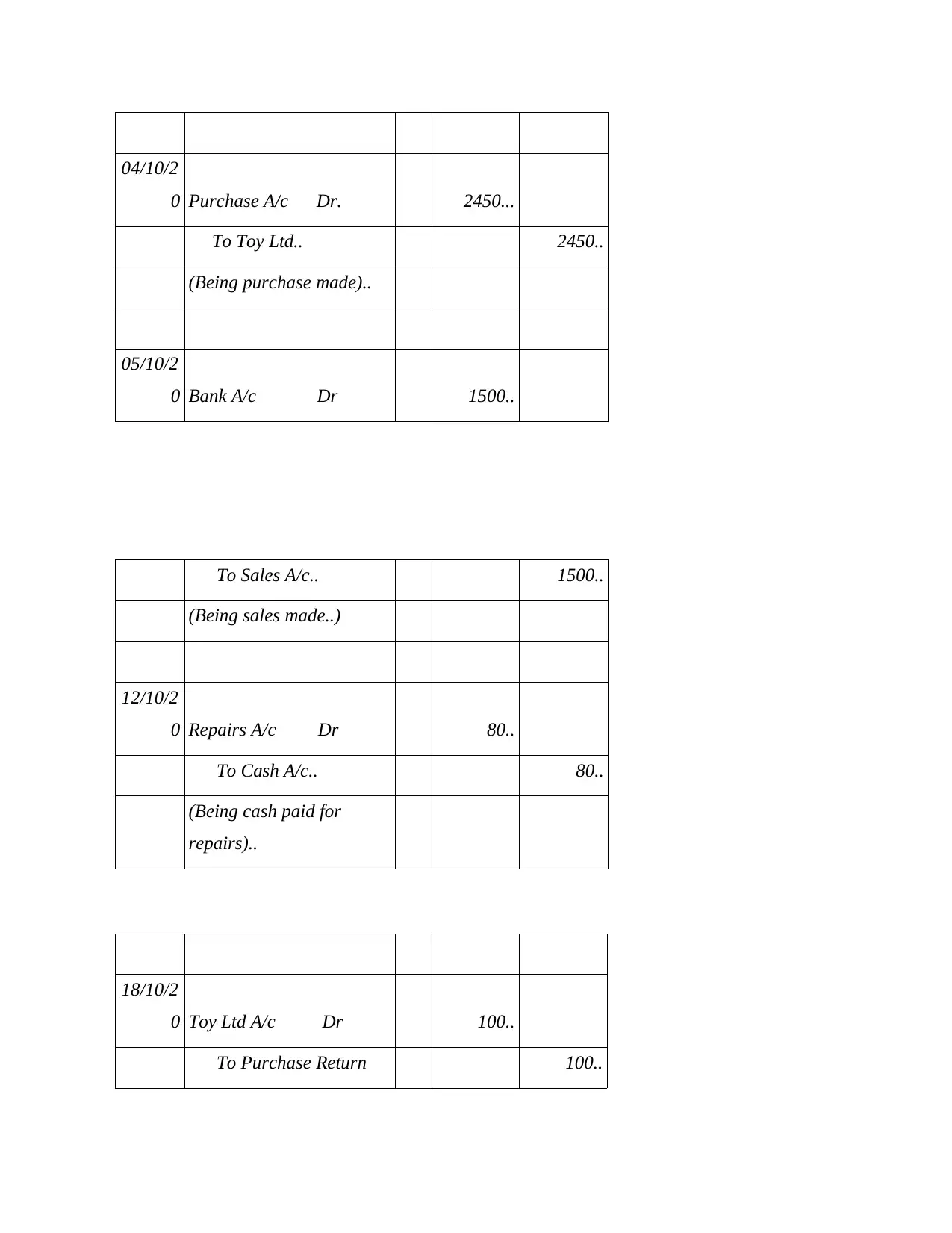

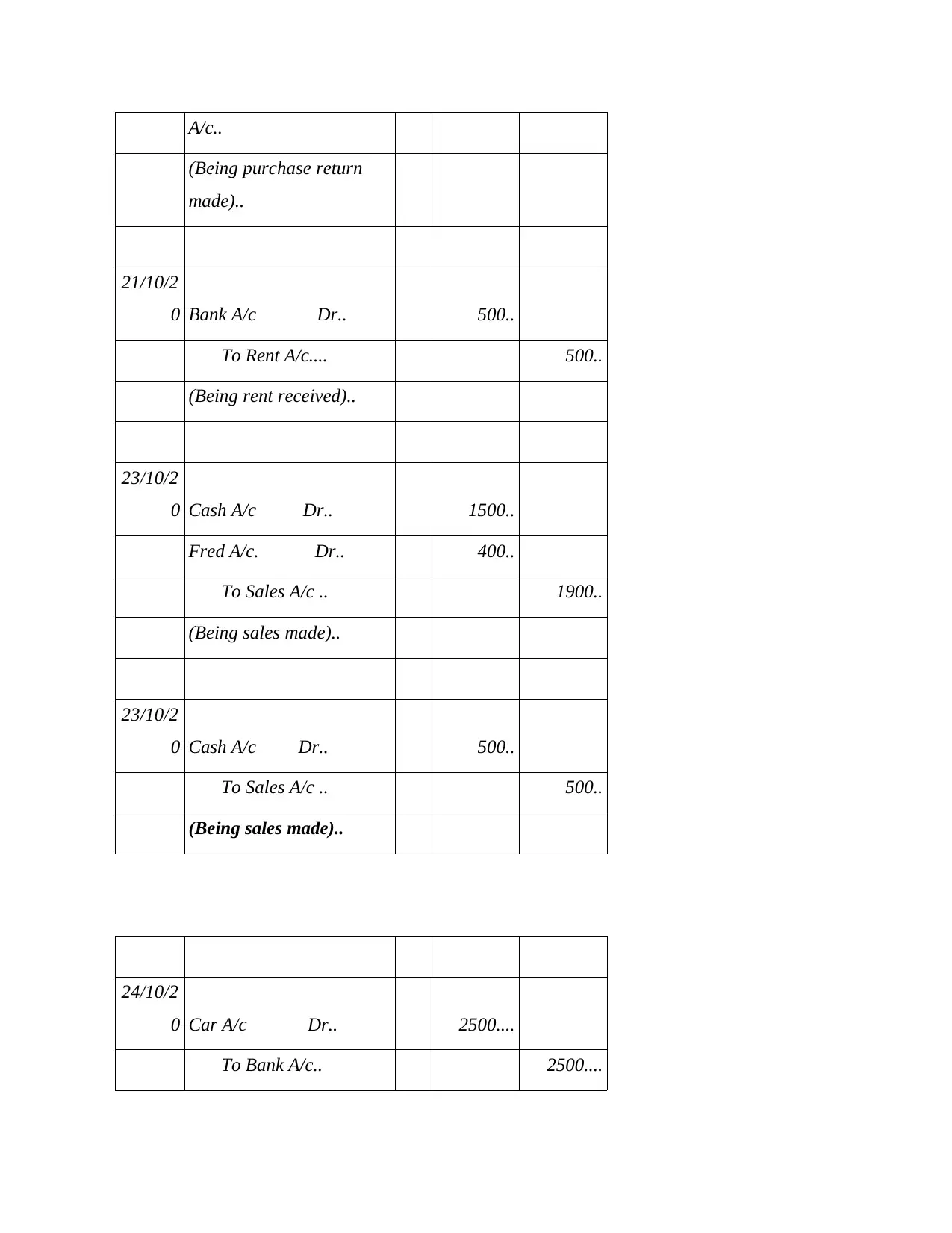

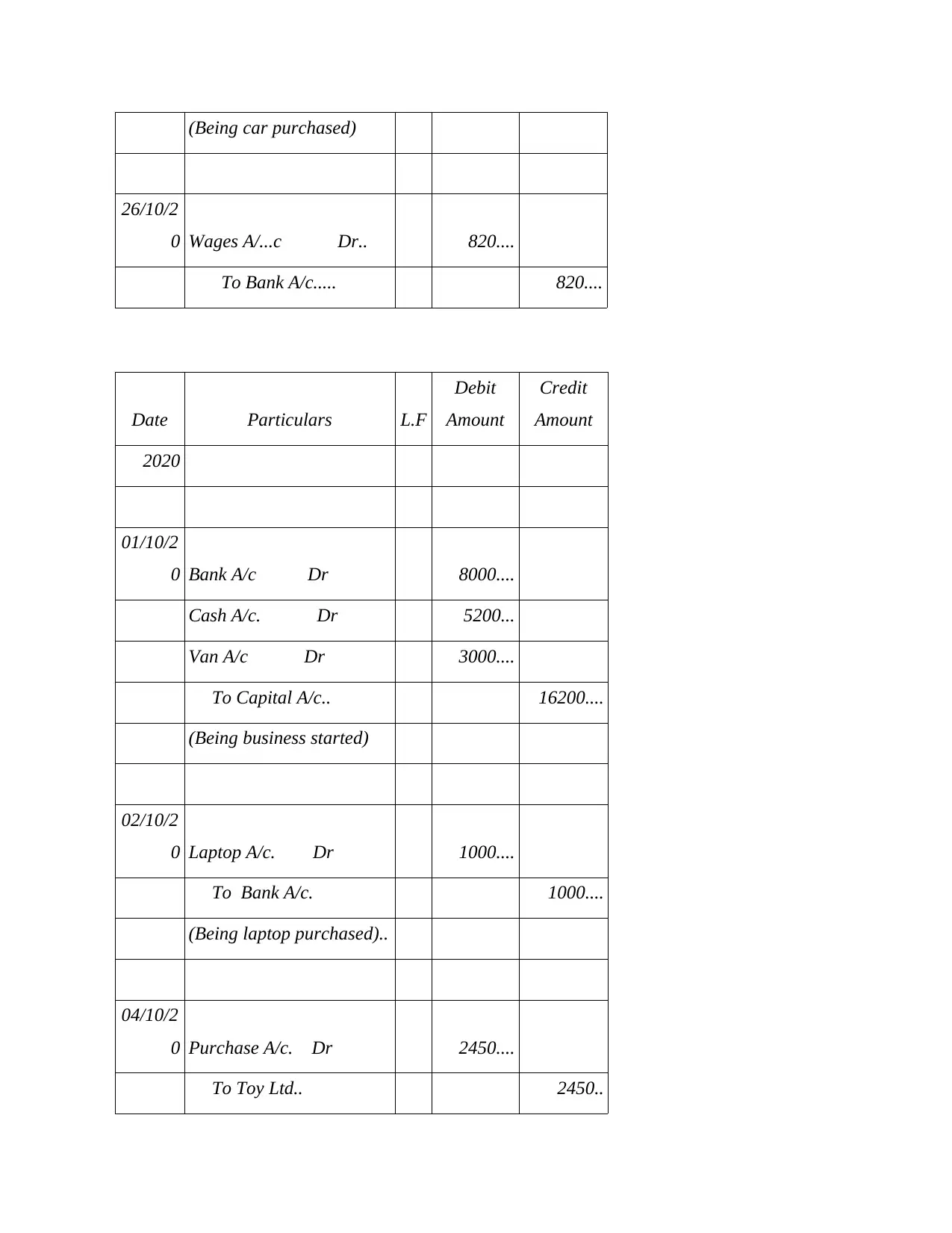

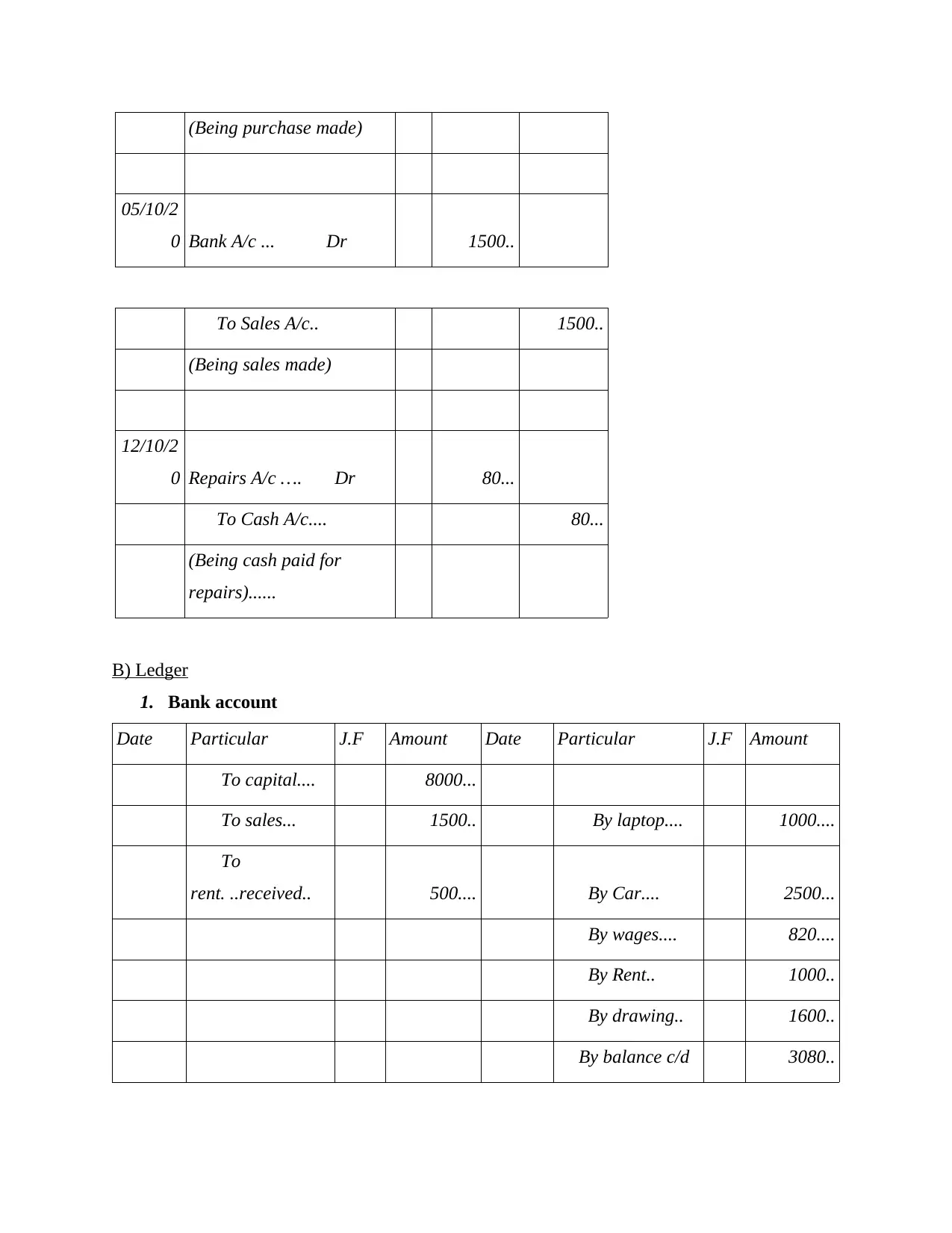

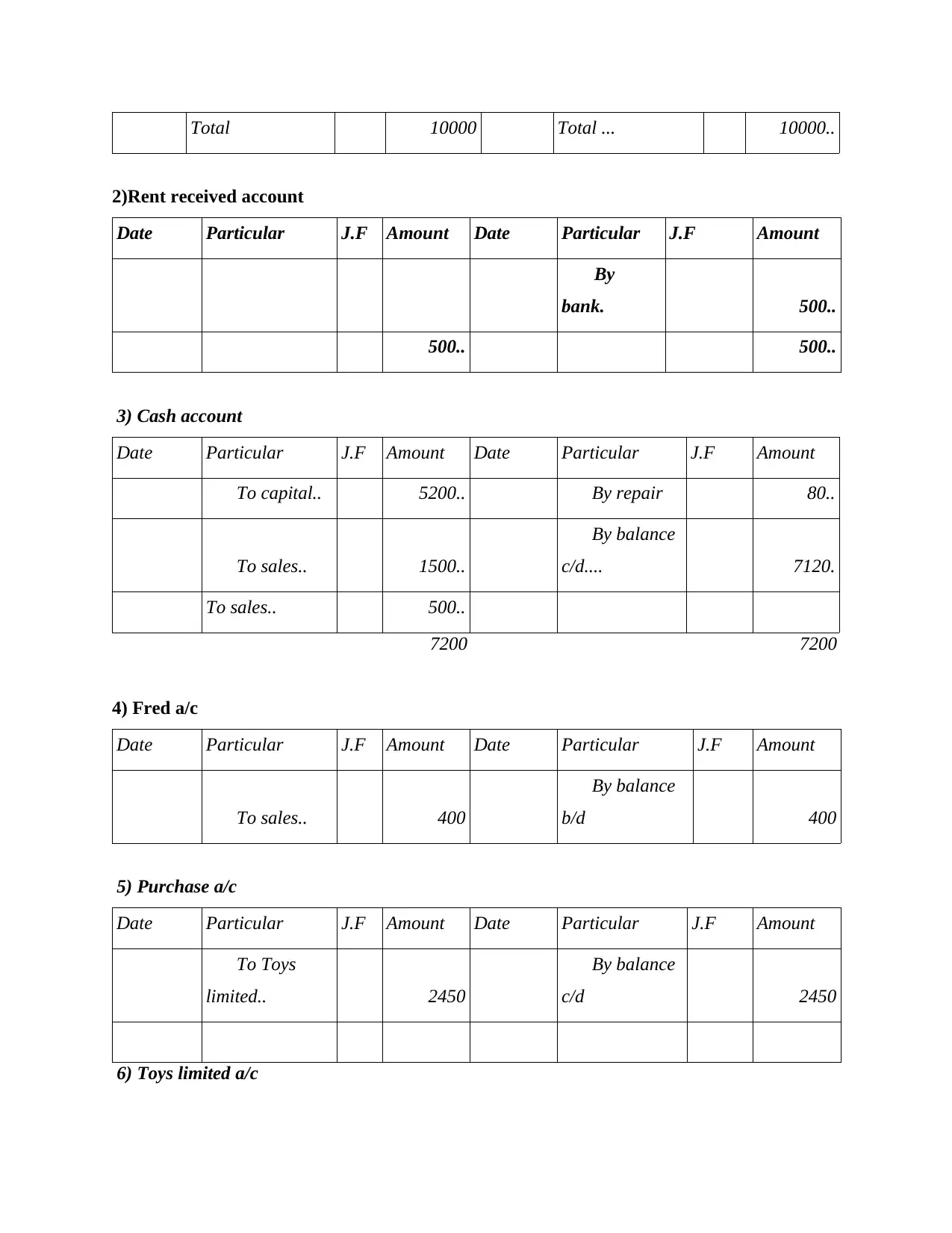

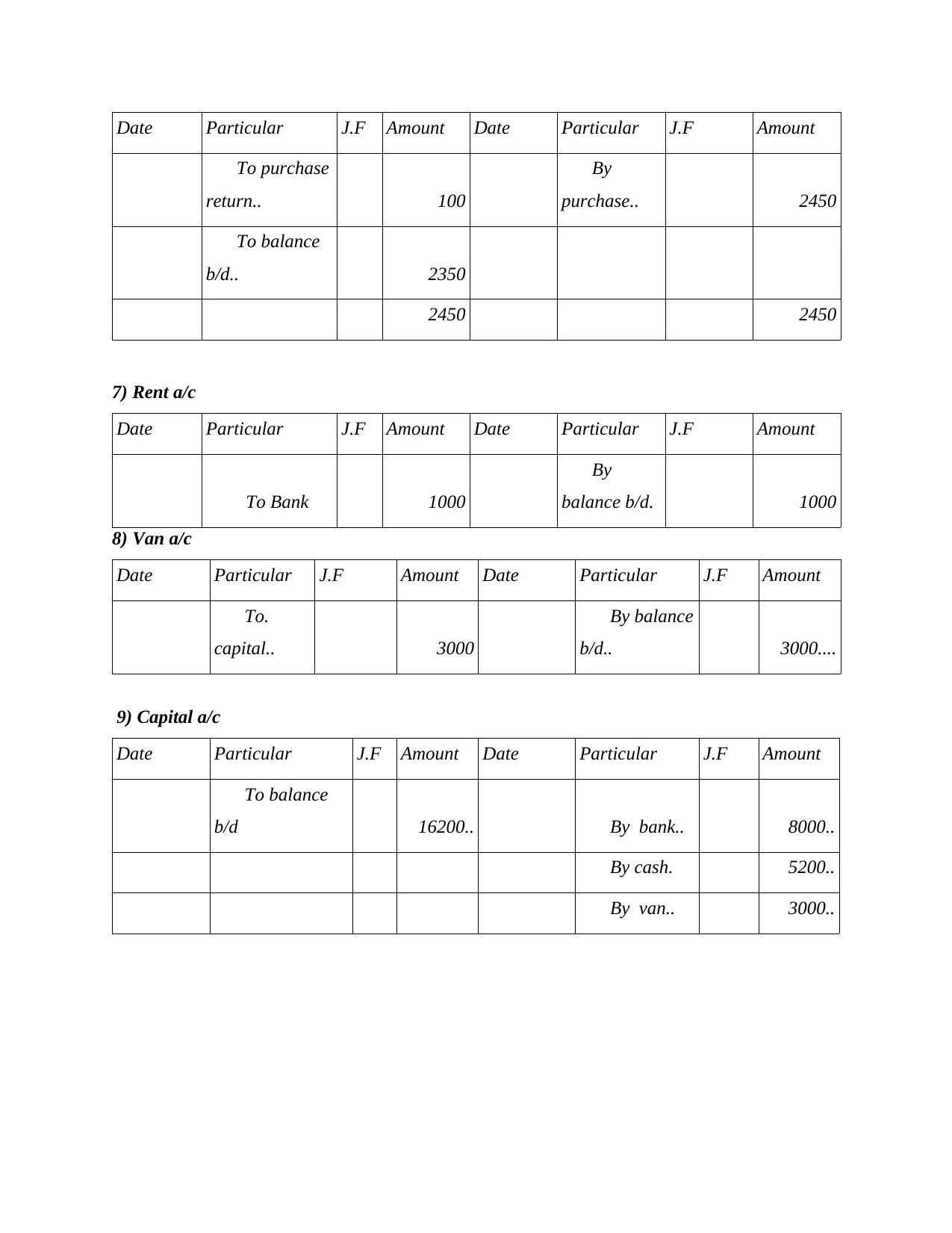

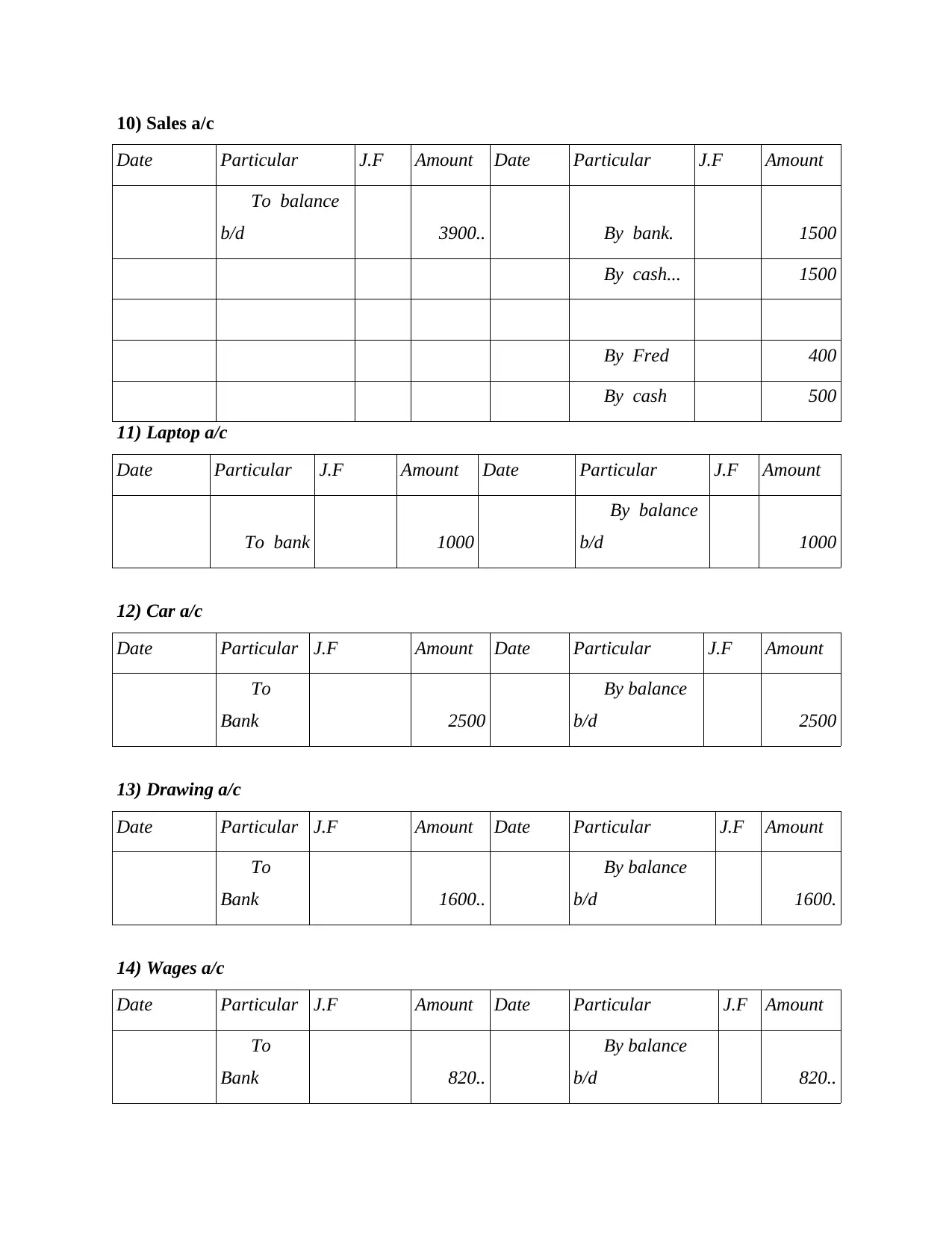

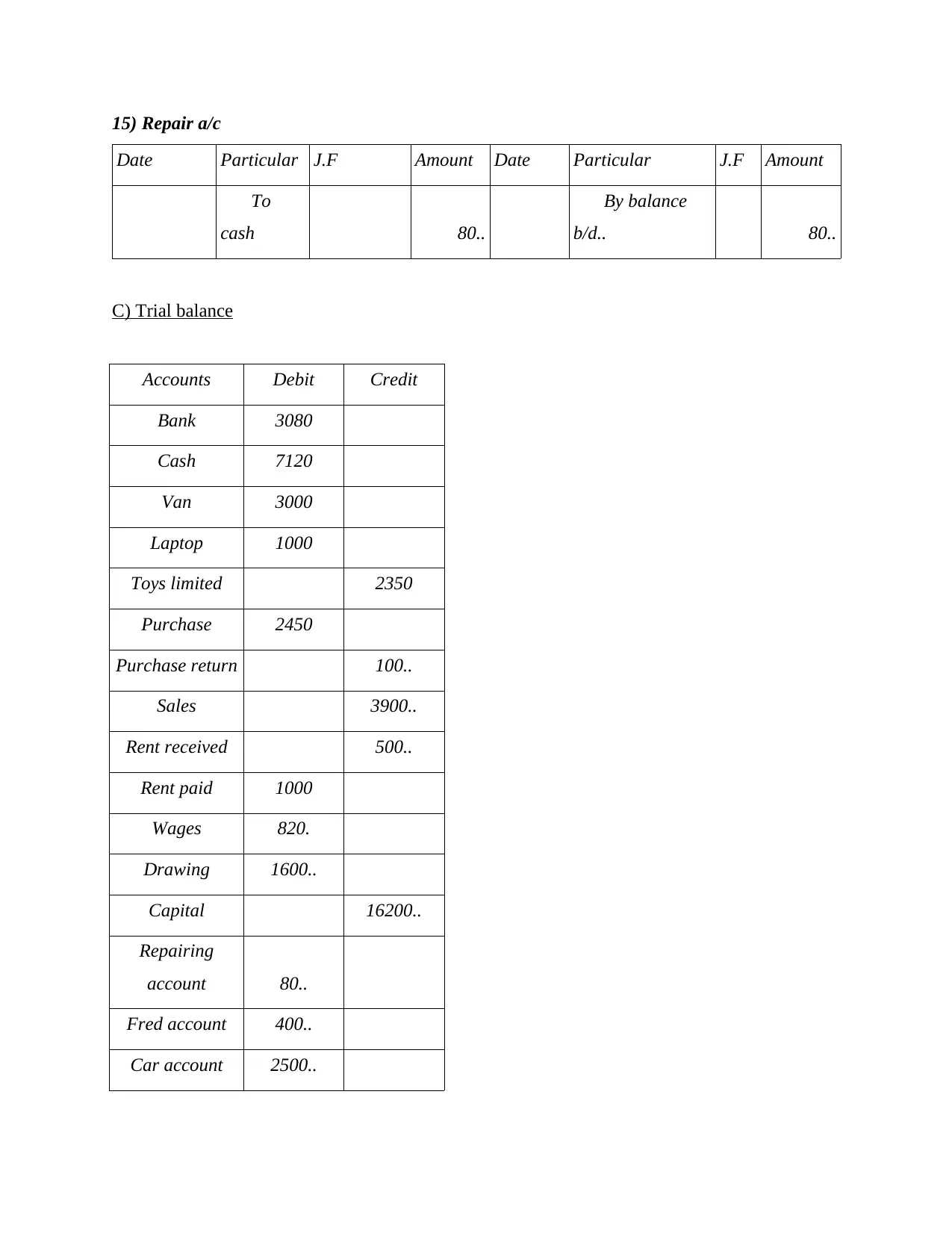

This report presents a comprehensive analysis of Linda's business transactions, employing fundamental accounting principles to assess her financial performance. The analysis begins with detailed journal entries, meticulously recording each transaction in a tabular format. These entries are then classified and summarized in ledger accounts, providing a clear overview of each account's activity. A trial balance is constructed to verify the accuracy of the ledger, serving as the foundation for preparing the financial statements. The report includes an income statement, evaluating Linda's profitability, and a balance sheet, presenting her assets, liabilities, and equity. Furthermore, the report addresses the impact of drawings on capital. Part B of the report delves into ratio analysis, comparing Linda's financial performance against industry benchmarks. It calculates and interprets key ratios, including net profit ratio, gross profit ratio, current ratio, quick ratio, accounts receivable collection period, and accounts payable ratio. The analysis highlights Linda's strengths and weaknesses, offering insights into her financial management and providing recommendations for improvement.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.