Management Accounting Report: Analysis of Nisa Retail's Operations

VerifiedAdded on 2020/02/03

|16

|5055

|38

Report

AI Summary

This report examines management accounting practices within Nisa Retail, a small UK-based retail business. It begins with an introduction to management accounting, its core functions, and its importance in organizational decision-making, covering financial transactions, resource allocation, and financial stability. Task 1 explains management accounting systems, including inventory accounting, ABC costing, accounting for lean, LIFO, FIFO, weighted average, cost accounting, job costing, batch costing, and price optimization. Task 2 focuses on the types of methods used to create management accounting reports, such as budget reports, payroll reports, manufacturing reports, accounts receivable reports, and job cost reports. Task 3 delves into the calculation of cost and net yield using marginal and absorption costing approaches, comparing their outcomes. Task 4 explores the use of various planning tools along with their merits and demerits. Task 5 compares management accounting systems and their role in responding to financial constraints. The report concludes with a summary of the findings and references.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION.......................................................................................................................3

TASK 1.......................................................................................................................................3

P1 Explanation of management accounting as well as essential requirements of various

systems of it............................................................................................................................3

P2 Explanation of different types of methods which are used in order to make management

accounting report....................................................................................................................4

TASK 2.......................................................................................................................................5

P3 Calculation of cost and net yield with the help of marginal absorption costing

approaches..............................................................................................................................5

TASK 3.......................................................................................................................................8

P4 Explaining uses of various kinds of planning tools along with merits and demerits .......8

TASK 4.....................................................................................................................................11

P5 Comparison between management accounting systems and there role in order to

respond financial constraints................................................................................................11

CONCLUSION.........................................................................................................................12

REFERENCES..........................................................................................................................13

INTRODUCTION.......................................................................................................................3

TASK 1.......................................................................................................................................3

P1 Explanation of management accounting as well as essential requirements of various

systems of it............................................................................................................................3

P2 Explanation of different types of methods which are used in order to make management

accounting report....................................................................................................................4

TASK 2.......................................................................................................................................5

P3 Calculation of cost and net yield with the help of marginal absorption costing

approaches..............................................................................................................................5

TASK 3.......................................................................................................................................8

P4 Explaining uses of various kinds of planning tools along with merits and demerits .......8

TASK 4.....................................................................................................................................11

P5 Comparison between management accounting systems and there role in order to

respond financial constraints................................................................................................11

CONCLUSION.........................................................................................................................12

REFERENCES..........................................................................................................................13

INTRODUCTION

Management accounting is an approach which give accounting information which is

useful to the management(Wajeetongratana, 2016). So that management accounting is a core

function of any organisation. In this all the managerial decisions are taken such as policies

framing, deciding the techniques and using appropriate strategy, which are beneficial for the

success of business growth. In management accounting, company can identify, measures,

prepare and monitor each and every financial tractions and elements related to the

organisation. In this way every organisation can use such kind of managerial activity because

it helps the managers to effective allocation of resources and funds and make the firm more

financially stable. In this case study, Nisa retail store is selected which operate there retail

industry in UK and it is also a small business enterprise. Nisa operates and provides there

products and services in local level such as in UK. This report explain the management

accounting and there different management accounting system which are suitable to the Nisa

retail stores. It also explain the different methods which are used for making effective

management accounting reports. It also describes the different types of planning tools which

can used in effective budgetary control.

TASK 1

P1 Explanation of management accounting as well as essential requirements of various

systems of it

Management accounting is the process which help to record each and every

transaction which show the financial position of the organisation, it includes income

statement, cash flow statements, balance sheet etc.(Vosselman, 2014). Management

accounting provides all the sufficient information which provide clear, accurate and reliable

information as per the time for the Nisa retailer stores. If the finance managers have accurate

and reliable data or information they can make use such information for allocating the

resources in a right manner so that organisation can achieve there major goals in future. Nisa

retail stores is a small business enterprise which follow several kinds of systems and

approaches so that they can effectively allocate there resources, they are:

Inventory Accounting- Inventory management is a process by which inventory or stock

in an organisation can be managed effectively. By using such kind of approaches Nisa can

manage there stock and utilize it effectively for the production of there products and services.

If there is higher level of stock in an organisation it means that workplace is not in a good

Management accounting is an approach which give accounting information which is

useful to the management(Wajeetongratana, 2016). So that management accounting is a core

function of any organisation. In this all the managerial decisions are taken such as policies

framing, deciding the techniques and using appropriate strategy, which are beneficial for the

success of business growth. In management accounting, company can identify, measures,

prepare and monitor each and every financial tractions and elements related to the

organisation. In this way every organisation can use such kind of managerial activity because

it helps the managers to effective allocation of resources and funds and make the firm more

financially stable. In this case study, Nisa retail store is selected which operate there retail

industry in UK and it is also a small business enterprise. Nisa operates and provides there

products and services in local level such as in UK. This report explain the management

accounting and there different management accounting system which are suitable to the Nisa

retail stores. It also explain the different methods which are used for making effective

management accounting reports. It also describes the different types of planning tools which

can used in effective budgetary control.

TASK 1

P1 Explanation of management accounting as well as essential requirements of various

systems of it

Management accounting is the process which help to record each and every

transaction which show the financial position of the organisation, it includes income

statement, cash flow statements, balance sheet etc.(Vosselman, 2014). Management

accounting provides all the sufficient information which provide clear, accurate and reliable

information as per the time for the Nisa retailer stores. If the finance managers have accurate

and reliable data or information they can make use such information for allocating the

resources in a right manner so that organisation can achieve there major goals in future. Nisa

retail stores is a small business enterprise which follow several kinds of systems and

approaches so that they can effectively allocate there resources, they are:

Inventory Accounting- Inventory management is a process by which inventory or stock

in an organisation can be managed effectively. By using such kind of approaches Nisa can

manage there stock and utilize it effectively for the production of there products and services.

If there is higher level of stock in an organisation it means that workplace is not in a good

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

condition, so that it is necessary to Nisa retailer to manage there stock effectively so that they

can enhance there profitability.

ABC costing- It is a process in which expenses and cost are determined in each and

every stage, which are essential for the Nisa retailer to manage there cost and expenses and

also determined that such cost and expenses are effectively managed or not.

Accounting for lean- This approach is based on such that in an organisation all waste

and unused expenses can be removed so that it can maintain the quality of services and

products. As per in Nisa retailer,company can eliminate all the unused expenses so that it help

them to make best quality of products and services. It is way by which management can

reduce there cost which make no impact in production or called unproductive and which not

give any kind of return in such production.

LIFO- It refers to last in first out rules, in this Nisa retail stores can sell all such

inventories which comes at the last time rather than using new level of stock. It is very rarely

used by the firm because this approach is less effective and does not give any kind of support

for earning the profits.

FIFO- It represent first in first out rule, in this stock and inventory are sold in first

time when they comes into the business(Tappura, Sievänen, Heikkilä, Jussila and Nenonen,

2015). It is considered as most usable approach which are adopted by every organisation. As

comparing with the LIFO method, FIFO method is better and it gives actual or appropriate

value of stock in Nisa retail stores.

Weighted average- In this approach, stock are valued in every organisation as per

there average value. In this way weighted average method is used to determine the average

value of stock with the help of LIFO and FIFO. So that weighted average method helps the

Nisa retailer stores to examined there average value of stock which are required in there

operational activity.

Cost accounting system- It is a framework which is used by the firm so that manager

can estimate the actual cost or cost per unit. It include profitability analysis, valuation of

inventory, cost control techniques, so that cost are managed by the manager effectively. For

example: Nisa retail store manage their cost by using appropriate techniques and determine

the requirement of cost in each departments.

Job costing system- It helps to identify and assign manufacturing costs to an individual

product. This system are use when product are produced which are different with each other.

can enhance there profitability.

ABC costing- It is a process in which expenses and cost are determined in each and

every stage, which are essential for the Nisa retailer to manage there cost and expenses and

also determined that such cost and expenses are effectively managed or not.

Accounting for lean- This approach is based on such that in an organisation all waste

and unused expenses can be removed so that it can maintain the quality of services and

products. As per in Nisa retailer,company can eliminate all the unused expenses so that it help

them to make best quality of products and services. It is way by which management can

reduce there cost which make no impact in production or called unproductive and which not

give any kind of return in such production.

LIFO- It refers to last in first out rules, in this Nisa retail stores can sell all such

inventories which comes at the last time rather than using new level of stock. It is very rarely

used by the firm because this approach is less effective and does not give any kind of support

for earning the profits.

FIFO- It represent first in first out rule, in this stock and inventory are sold in first

time when they comes into the business(Tappura, Sievänen, Heikkilä, Jussila and Nenonen,

2015). It is considered as most usable approach which are adopted by every organisation. As

comparing with the LIFO method, FIFO method is better and it gives actual or appropriate

value of stock in Nisa retail stores.

Weighted average- In this approach, stock are valued in every organisation as per

there average value. In this way weighted average method is used to determine the average

value of stock with the help of LIFO and FIFO. So that weighted average method helps the

Nisa retailer stores to examined there average value of stock which are required in there

operational activity.

Cost accounting system- It is a framework which is used by the firm so that manager

can estimate the actual cost or cost per unit. It include profitability analysis, valuation of

inventory, cost control techniques, so that cost are managed by the manager effectively. For

example: Nisa retail store manage their cost by using appropriate techniques and determine

the requirement of cost in each departments.

Job costing system- It helps to identify and assign manufacturing costs to an individual

product. This system are use when product are produced which are different with each other.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

For example: Nisa use the job costing accounting system by which firm can make appropriate

recording of cost which are related to manufacturing of products.

Batch costing system- It is a type of specific order costing techniques in which

numbers of units are products, but the produced units are different from the batch. For

example: Nisa company produced number of same products but all are not same in the

distributive areas like US, UK etc.

Price optimisation system- It is mathematical tool which help to analysis the

customers responses as per the change in price of products. By using this techniques, Nisa

identify the customer's demand and preferences as per the changes of the price of products.

For example: Nisa company launch 30 new household products which are not same as peer

their price. Hence, company focus to the demand of the customers that in which price they

will agree to pay for the products.

P2 Explanation of different types of methods which are used in order to make management

accounting report

For ever business it is essential to prepare a financial statements such as income

statements, cash flow statements, balance sheet etc. By using such statements all the data and

informations are collected and record which help the managers to make an effective business

accounting report. In management accounting reports, all the information which help the

business to make an effective decision plan, policy can be made in the report which is based

on the accounting period. In Nisa retail stores there various methods which are used in to

managing the there accounting reports, they are:

Budget Report- Budget report are such report which include all the information and

data related to the fund which are required for the organisation. In Nisa retail stores, budget

report are prepared to estimate the fund requirement that how much money are required in

future for effective running of the business. So that budget report help to examine the future

performance and effective fund allocation for fulfilment of such performance in

future(Schaltegger, Gibassier and Zvezdov, 2013).

Payroll report- Payroll report includes all the expenditure which are paid by the

organisation to there employee in a form of wages, salary, bonus etc. So that all such kind of

expenses which increase the employee work-performance can recorded in this type of report.

In this way, all such expenditure can be treated as expenses account and take difference by

making income statements.

recording of cost which are related to manufacturing of products.

Batch costing system- It is a type of specific order costing techniques in which

numbers of units are products, but the produced units are different from the batch. For

example: Nisa company produced number of same products but all are not same in the

distributive areas like US, UK etc.

Price optimisation system- It is mathematical tool which help to analysis the

customers responses as per the change in price of products. By using this techniques, Nisa

identify the customer's demand and preferences as per the changes of the price of products.

For example: Nisa company launch 30 new household products which are not same as peer

their price. Hence, company focus to the demand of the customers that in which price they

will agree to pay for the products.

P2 Explanation of different types of methods which are used in order to make management

accounting report

For ever business it is essential to prepare a financial statements such as income

statements, cash flow statements, balance sheet etc. By using such statements all the data and

informations are collected and record which help the managers to make an effective business

accounting report. In management accounting reports, all the information which help the

business to make an effective decision plan, policy can be made in the report which is based

on the accounting period. In Nisa retail stores there various methods which are used in to

managing the there accounting reports, they are:

Budget Report- Budget report are such report which include all the information and

data related to the fund which are required for the organisation. In Nisa retail stores, budget

report are prepared to estimate the fund requirement that how much money are required in

future for effective running of the business. So that budget report help to examine the future

performance and effective fund allocation for fulfilment of such performance in

future(Schaltegger, Gibassier and Zvezdov, 2013).

Payroll report- Payroll report includes all the expenditure which are paid by the

organisation to there employee in a form of wages, salary, bonus etc. So that all such kind of

expenses which increase the employee work-performance can recorded in this type of report.

In this way, all such expenditure can be treated as expenses account and take difference by

making income statements.

Manufacturing Report- In this type of report, it include all the expenses which are

spend in the manufacturing activity. In this way Nisa retailer can make complete record of all

the expenses which they are spend in there manufacturing activity such as providing products

and services. In this way, if it also includes various records such expenses which are done to

meet the raw material from suppliers, expenditure in regards to labour charges, techniques

changes etc. In this way all the cost are treated as manufacturing expenditure(Renz, 2016).

Report of account receivables- As per such report, it included all the information in

which Nisa can received the money at end of the accounting period. In this way, if a company

can receive higher receivables than the profit earning capacity of the company will also be

higher but in opposite if the receivables rate is lower than company is not is a position to earn

profit more. So that the profit rate is also lower in this condition. A company can receive there

receivables in the from of money received by debtors, sale on credit, or sales by cash etc.

Job cost report- There is another accounting report which is used by the Nisa retailer

is the report of job costing. In this report which is related to the job are recorded in it. It

require the company's financial position so that manager can determine that in which position

company can stand, is it good or not. In this way, each and every task are allotted in different

departments, and such all the information related to each task can be recorded in this report.

This report also include the total expenses which are occurred to make an effective task from

each department(Otley and Emmanuel, 2013).

TASK 2

P3 Calculation of cost and net yield with the help of marginal absorption costing approaches

To analysis the company's financial position, every business can prepare there

financial statements such as profit and loss account, balance sheet, cash flow statement etc. In

this way, Nisa retailer stores can also prepare such kind of financial statements to estimate

there actual performance at the end of the accounting period. To determine the cost and net

profit Nisa retailer stores can follow two type of approaches such as marginal costing

approach and absorption costing approach. In this methods, all the expenditure and income

can be listed in a proper form so that it can help to identify that the company is in profit

condition or not(Lavia López and Hiebl, 2014). So that to analysis the cost d net profit Nisa

can used two methods. In marginal costing method only direct and variable cost are

considered but in absorption costing method, it include all the expenses which are used in to

determine the net profit in the company. Calculation of net profit by using marginal and

absorption methods are as follow:

spend in the manufacturing activity. In this way Nisa retailer can make complete record of all

the expenses which they are spend in there manufacturing activity such as providing products

and services. In this way, if it also includes various records such expenses which are done to

meet the raw material from suppliers, expenditure in regards to labour charges, techniques

changes etc. In this way all the cost are treated as manufacturing expenditure(Renz, 2016).

Report of account receivables- As per such report, it included all the information in

which Nisa can received the money at end of the accounting period. In this way, if a company

can receive higher receivables than the profit earning capacity of the company will also be

higher but in opposite if the receivables rate is lower than company is not is a position to earn

profit more. So that the profit rate is also lower in this condition. A company can receive there

receivables in the from of money received by debtors, sale on credit, or sales by cash etc.

Job cost report- There is another accounting report which is used by the Nisa retailer

is the report of job costing. In this report which is related to the job are recorded in it. It

require the company's financial position so that manager can determine that in which position

company can stand, is it good or not. In this way, each and every task are allotted in different

departments, and such all the information related to each task can be recorded in this report.

This report also include the total expenses which are occurred to make an effective task from

each department(Otley and Emmanuel, 2013).

TASK 2

P3 Calculation of cost and net yield with the help of marginal absorption costing approaches

To analysis the company's financial position, every business can prepare there

financial statements such as profit and loss account, balance sheet, cash flow statement etc. In

this way, Nisa retailer stores can also prepare such kind of financial statements to estimate

there actual performance at the end of the accounting period. To determine the cost and net

profit Nisa retailer stores can follow two type of approaches such as marginal costing

approach and absorption costing approach. In this methods, all the expenditure and income

can be listed in a proper form so that it can help to identify that the company is in profit

condition or not(Lavia López and Hiebl, 2014). So that to analysis the cost d net profit Nisa

can used two methods. In marginal costing method only direct and variable cost are

considered but in absorption costing method, it include all the expenses which are used in to

determine the net profit in the company. Calculation of net profit by using marginal and

absorption methods are as follow:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

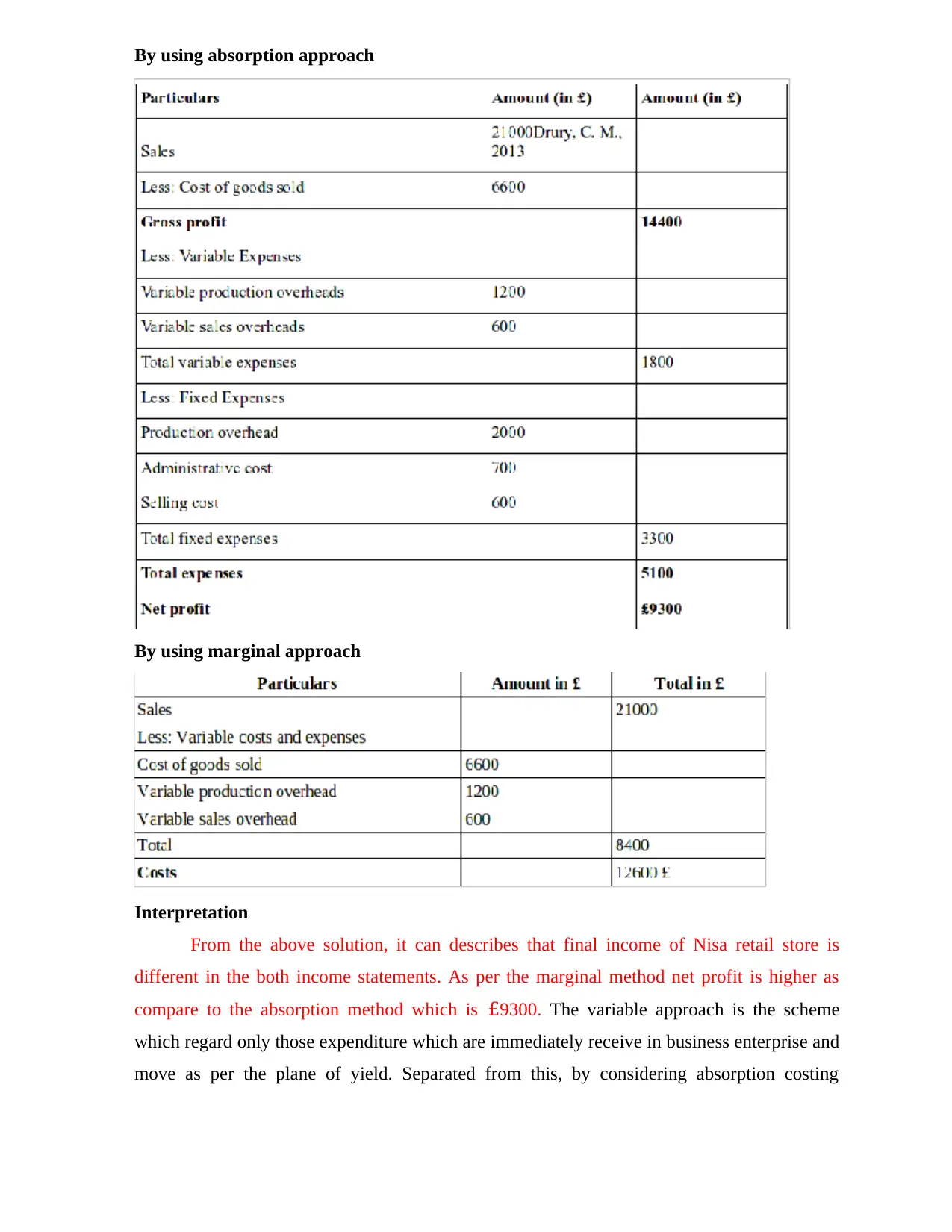

By using absorption approach

By using marginal approach

Interpretation

From the above solution, it can describes that final income of Nisa retail store is

different in the both income statements. As per the marginal method net profit is higher as

compare to the absorption method which is £9300. The variable approach is the scheme

which regard only those expenditure which are immediately receive in business enterprise and

move as per the plane of yield. Separated from this, by considering absorption costing

By using marginal approach

Interpretation

From the above solution, it can describes that final income of Nisa retail store is

different in the both income statements. As per the marginal method net profit is higher as

compare to the absorption method which is £9300. The variable approach is the scheme

which regard only those expenditure which are immediately receive in business enterprise and

move as per the plane of yield. Separated from this, by considering absorption costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

approach Nisa retail store having fewer net profit which track to bring down gain point in the

whole retail industry of UK.

In most of the business organisation enterpriser exercise absorption costing method

rather than marginal approach of costing to measure fiscal execution in the sector where it

doing economic activities (Kaplan and Atkinson, 2015). The rational motive backside that it

consider absorption system is that, Nisa retail store can ascertain actual profit by deducting all

kind of expenditures which at the workplace. Marginal costing is less uses because here the

management can not deduct actual position of the firm. Hence, it can be said that when Nisa

retail store uses both the methods then value of net profit take issue.

Difference between above two mentioned costing approaches

Basis For Comparison Marginal Costing Absorption Costing

Meaning Marginal costing is

techniques by which it can

use to ascertained the total

cost of production in an

organization.

It includes the apportionment

of the total costs to the cost

centre so that it can assess or

determine the total cost of

production in an

organisation(Morales and

Lambert, 2013).

Cost Recognition In this method, variable cost

is take into the consideration

to calculate the product cost

and fixed cost is used to

calculate the period cost in

the organisation.

In this method both fixed and

variable cost are to be taken

into consideration to

calculates product cost.

Classification of overheads In marginal costing fixed and

variable both overheads are to

be taken.

In absorption method,

production, administration

and selling & distribution

overheads are to be taken in

any calculations.

Profitability In this method, profitability is

measured by using profit

volume ratio.

In this method, by making

inclusion of fixed cost,

profitability of any

whole retail industry of UK.

In most of the business organisation enterpriser exercise absorption costing method

rather than marginal approach of costing to measure fiscal execution in the sector where it

doing economic activities (Kaplan and Atkinson, 2015). The rational motive backside that it

consider absorption system is that, Nisa retail store can ascertain actual profit by deducting all

kind of expenditures which at the workplace. Marginal costing is less uses because here the

management can not deduct actual position of the firm. Hence, it can be said that when Nisa

retail store uses both the methods then value of net profit take issue.

Difference between above two mentioned costing approaches

Basis For Comparison Marginal Costing Absorption Costing

Meaning Marginal costing is

techniques by which it can

use to ascertained the total

cost of production in an

organization.

It includes the apportionment

of the total costs to the cost

centre so that it can assess or

determine the total cost of

production in an

organisation(Morales and

Lambert, 2013).

Cost Recognition In this method, variable cost

is take into the consideration

to calculate the product cost

and fixed cost is used to

calculate the period cost in

the organisation.

In this method both fixed and

variable cost are to be taken

into consideration to

calculates product cost.

Classification of overheads In marginal costing fixed and

variable both overheads are to

be taken.

In absorption method,

production, administration

and selling & distribution

overheads are to be taken in

any calculations.

Profitability In this method, profitability is

measured by using profit

volume ratio.

In this method, by making

inclusion of fixed cost,

profitability of any

organisation may be affected.

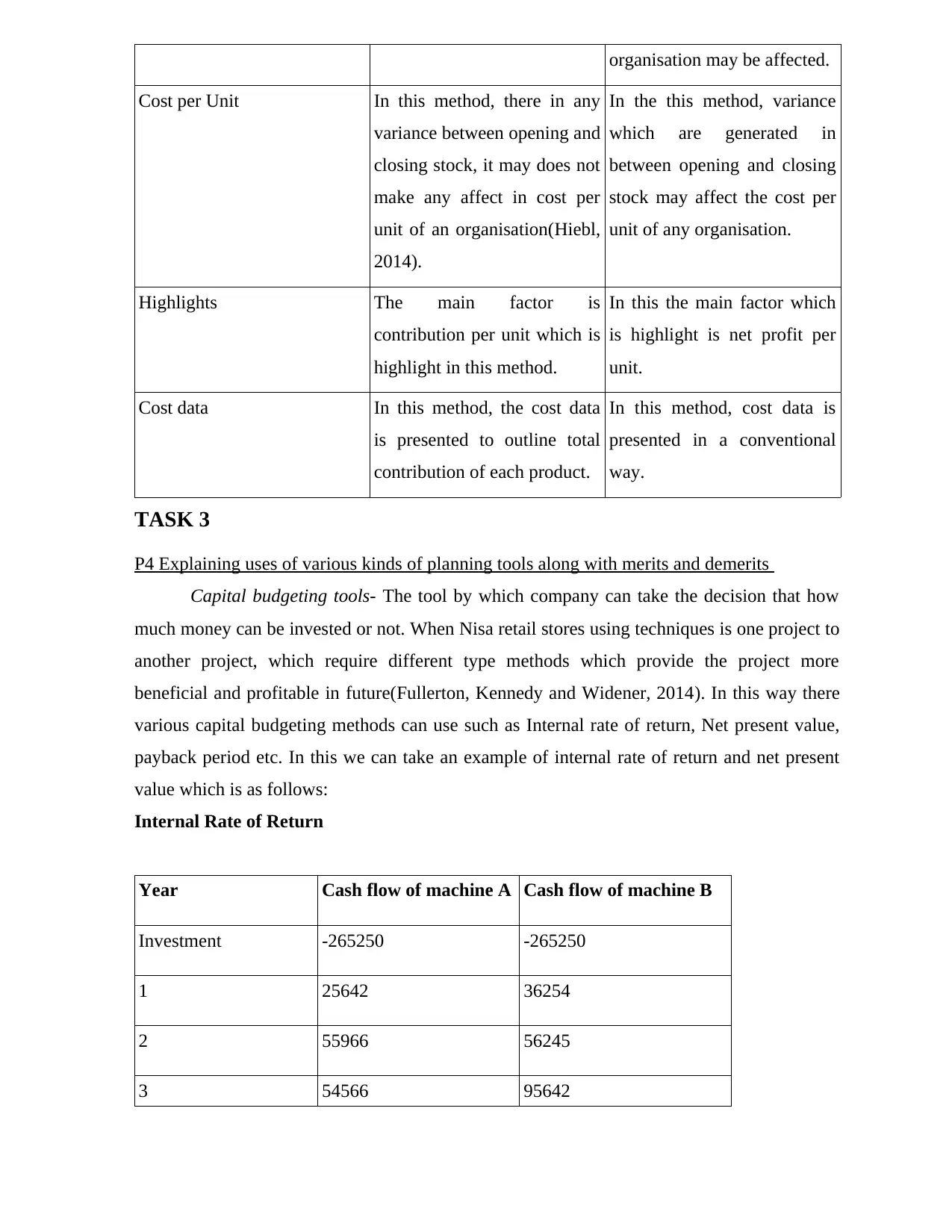

Cost per Unit In this method, there in any

variance between opening and

closing stock, it may does not

make any affect in cost per

unit of an organisation(Hiebl,

2014).

In the this method, variance

which are generated in

between opening and closing

stock may affect the cost per

unit of any organisation.

Highlights The main factor is

contribution per unit which is

highlight in this method.

In this the main factor which

is highlight is net profit per

unit.

Cost data In this method, the cost data

is presented to outline total

contribution of each product.

In this method, cost data is

presented in a conventional

way.

TASK 3

P4 Explaining uses of various kinds of planning tools along with merits and demerits

Capital budgeting tools- The tool by which company can take the decision that how

much money can be invested or not. When Nisa retail stores using techniques is one project to

another project, which require different type methods which provide the project more

beneficial and profitable in future(Fullerton, Kennedy and Widener, 2014). In this way there

various capital budgeting methods can use such as Internal rate of return, Net present value,

payback period etc. In this we can take an example of internal rate of return and net present

value which is as follows:

Internal Rate of Return

Year Cash flow of machine A Cash flow of machine B

Investment -265250 -265250

1 25642 36254

2 55966 56245

3 54566 95642

Cost per Unit In this method, there in any

variance between opening and

closing stock, it may does not

make any affect in cost per

unit of an organisation(Hiebl,

2014).

In the this method, variance

which are generated in

between opening and closing

stock may affect the cost per

unit of any organisation.

Highlights The main factor is

contribution per unit which is

highlight in this method.

In this the main factor which

is highlight is net profit per

unit.

Cost data In this method, the cost data

is presented to outline total

contribution of each product.

In this method, cost data is

presented in a conventional

way.

TASK 3

P4 Explaining uses of various kinds of planning tools along with merits and demerits

Capital budgeting tools- The tool by which company can take the decision that how

much money can be invested or not. When Nisa retail stores using techniques is one project to

another project, which require different type methods which provide the project more

beneficial and profitable in future(Fullerton, Kennedy and Widener, 2014). In this way there

various capital budgeting methods can use such as Internal rate of return, Net present value,

payback period etc. In this we can take an example of internal rate of return and net present

value which is as follows:

Internal Rate of Return

Year Cash flow of machine A Cash flow of machine B

Investment -265250 -265250

1 25642 36254

2 55966 56245

3 54566 95642

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4 145632 136524

5 165914 189526

IRR 15.12% 20.18%

Advantage and disadvantages: The main advantage of capital budgeting is that it help to

take the profitable decision so that it can generate higher return from the potential investment.

In this way Nisa can assess there return and profitability by using capital budgeting. The

another advantage of financial ratio analysis is that it helps in comparing the companies of

different size with each other. Main limitation of capital budgeting is that in capital budgeting,

cash discounting factor is not considered in a firm. Another drawback of ratio analysis is that

accounting standards allow different accounting policies so that in this way ratio analysis is

less useful in such conditions.

Analysis of financial ration- By analysing the financial ratio Nisa retail stores can

estimate the financial position of the company. By using financial ratio, company can also

determine liquidity position, current ratio, net asset turnover etc. in a company(Fullerton,

Kennedy and Widener, 2013). There are various ration used in analysis of financial ratio such

as profitability, solvency, liquidity, investor etc. Some of the example are:

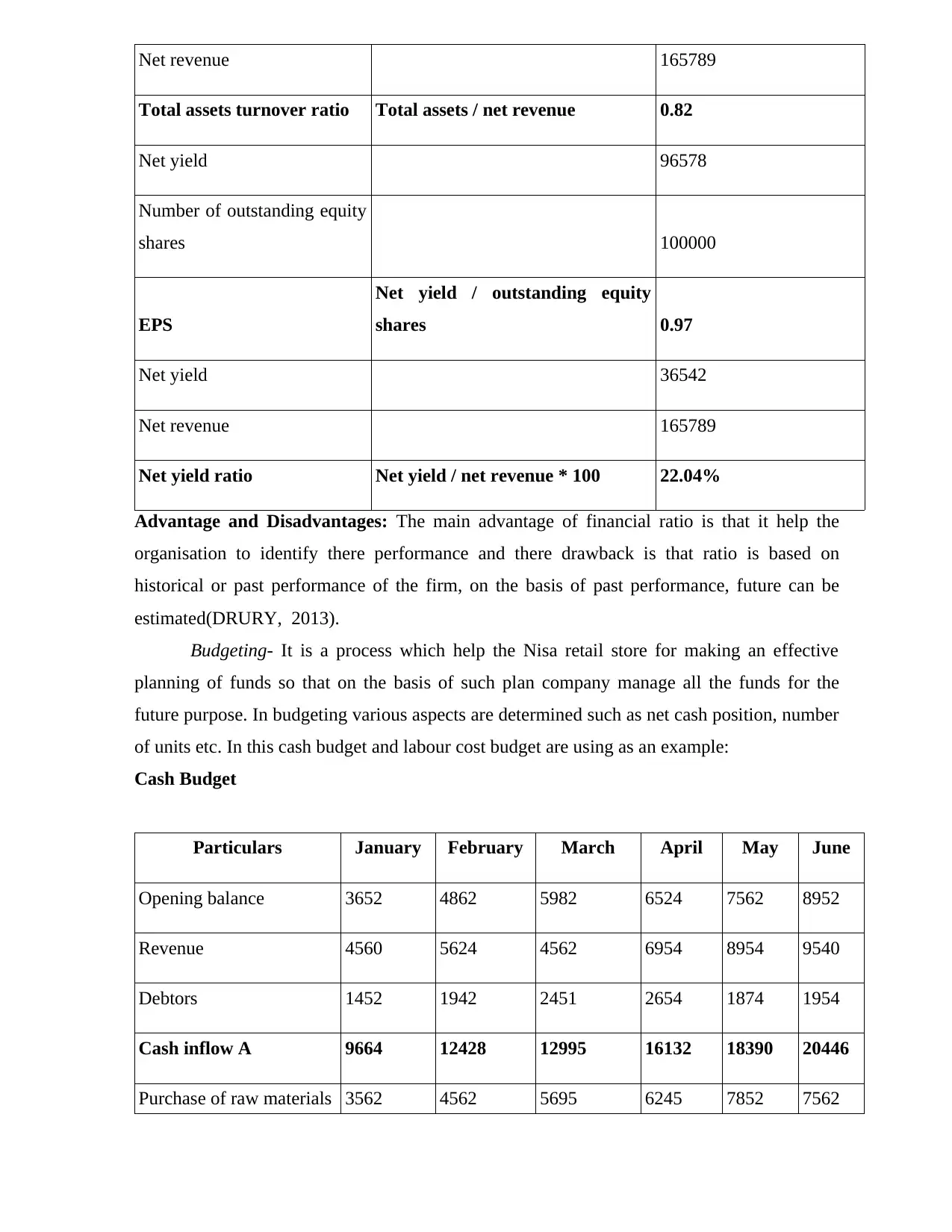

Name of financial ratios Formula to calculate ratios Value and outcomes

Stock at the end of year 65841

Net revenue 165789

Stock turnover ratio stock / net revenue 0.40

Fixed assets 114568

Net revenue 165789

Fixed assets turnover ratio Fixed assets / net revenue 0.69

Total assets 135897

5 165914 189526

IRR 15.12% 20.18%

Advantage and disadvantages: The main advantage of capital budgeting is that it help to

take the profitable decision so that it can generate higher return from the potential investment.

In this way Nisa can assess there return and profitability by using capital budgeting. The

another advantage of financial ratio analysis is that it helps in comparing the companies of

different size with each other. Main limitation of capital budgeting is that in capital budgeting,

cash discounting factor is not considered in a firm. Another drawback of ratio analysis is that

accounting standards allow different accounting policies so that in this way ratio analysis is

less useful in such conditions.

Analysis of financial ration- By analysing the financial ratio Nisa retail stores can

estimate the financial position of the company. By using financial ratio, company can also

determine liquidity position, current ratio, net asset turnover etc. in a company(Fullerton,

Kennedy and Widener, 2013). There are various ration used in analysis of financial ratio such

as profitability, solvency, liquidity, investor etc. Some of the example are:

Name of financial ratios Formula to calculate ratios Value and outcomes

Stock at the end of year 65841

Net revenue 165789

Stock turnover ratio stock / net revenue 0.40

Fixed assets 114568

Net revenue 165789

Fixed assets turnover ratio Fixed assets / net revenue 0.69

Total assets 135897

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net revenue 165789

Total assets turnover ratio Total assets / net revenue 0.82

Net yield 96578

Number of outstanding equity

shares 100000

EPS

Net yield / outstanding equity

shares 0.97

Net yield 36542

Net revenue 165789

Net yield ratio Net yield / net revenue * 100 22.04%

Advantage and Disadvantages: The main advantage of financial ratio is that it help the

organisation to identify there performance and there drawback is that ratio is based on

historical or past performance of the firm, on the basis of past performance, future can be

estimated(DRURY, 2013).

Budgeting- It is a process which help the Nisa retail store for making an effective

planning of funds so that on the basis of such plan company manage all the funds for the

future purpose. In budgeting various aspects are determined such as net cash position, number

of units etc. In this cash budget and labour cost budget are using as an example:

Cash Budget

Particulars January February March April May June

Opening balance 3652 4862 5982 6524 7562 8952

Revenue 4560 5624 4562 6954 8954 9540

Debtors 1452 1942 2451 2654 1874 1954

Cash inflow A 9664 12428 12995 16132 18390 20446

Purchase of raw materials 3562 4562 5695 6245 7852 7562

Total assets turnover ratio Total assets / net revenue 0.82

Net yield 96578

Number of outstanding equity

shares 100000

EPS

Net yield / outstanding equity

shares 0.97

Net yield 36542

Net revenue 165789

Net yield ratio Net yield / net revenue * 100 22.04%

Advantage and Disadvantages: The main advantage of financial ratio is that it help the

organisation to identify there performance and there drawback is that ratio is based on

historical or past performance of the firm, on the basis of past performance, future can be

estimated(DRURY, 2013).

Budgeting- It is a process which help the Nisa retail store for making an effective

planning of funds so that on the basis of such plan company manage all the funds for the

future purpose. In budgeting various aspects are determined such as net cash position, number

of units etc. In this cash budget and labour cost budget are using as an example:

Cash Budget

Particulars January February March April May June

Opening balance 3652 4862 5982 6524 7562 8952

Revenue 4560 5624 4562 6954 8954 9540

Debtors 1452 1942 2451 2654 1874 1954

Cash inflow A 9664 12428 12995 16132 18390 20446

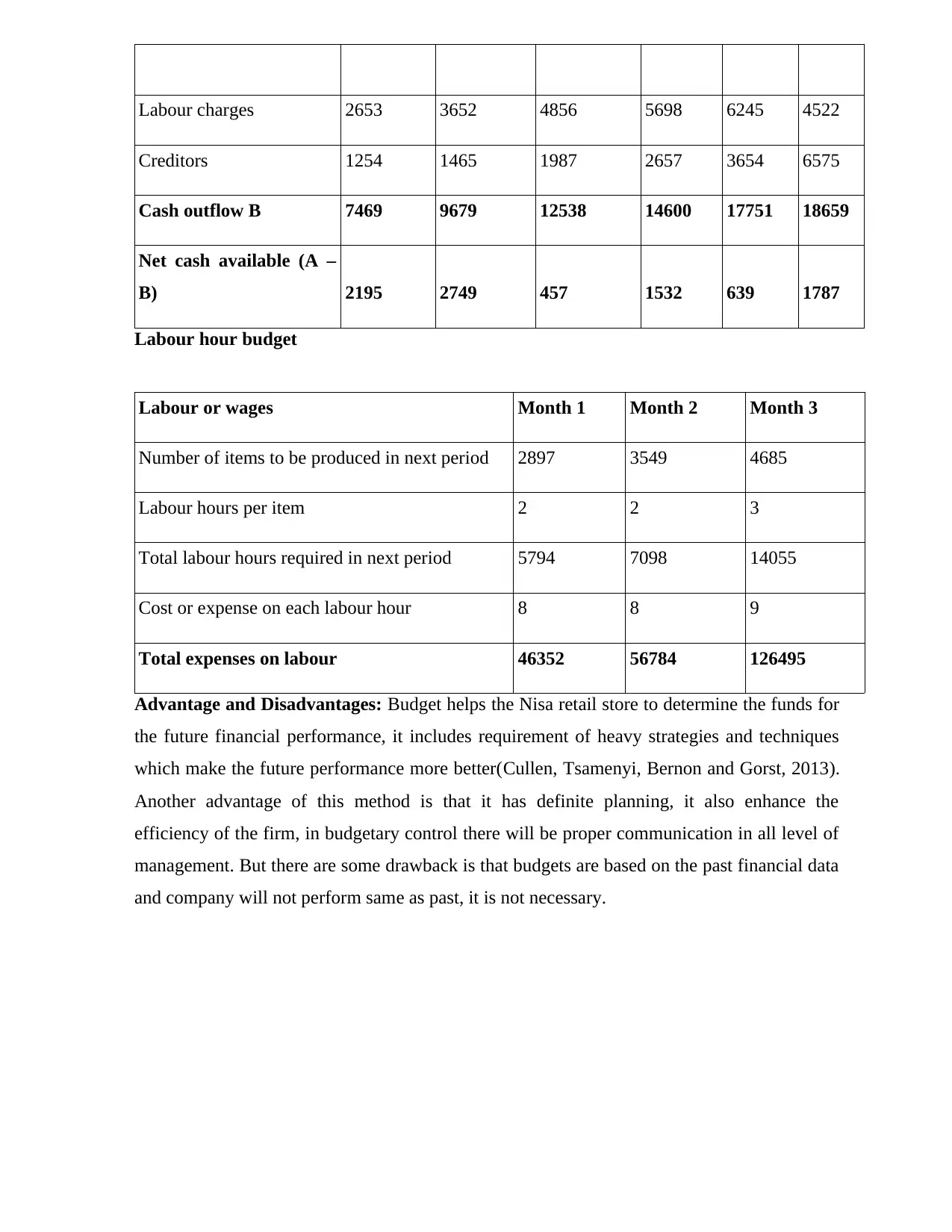

Purchase of raw materials 3562 4562 5695 6245 7852 7562

Labour charges 2653 3652 4856 5698 6245 4522

Creditors 1254 1465 1987 2657 3654 6575

Cash outflow B 7469 9679 12538 14600 17751 18659

Net cash available (A –

B) 2195 2749 457 1532 639 1787

Labour hour budget

Labour or wages Month 1 Month 2 Month 3

Number of items to be produced in next period 2897 3549 4685

Labour hours per item 2 2 3

Total labour hours required in next period 5794 7098 14055

Cost or expense on each labour hour 8 8 9

Total expenses on labour 46352 56784 126495

Advantage and Disadvantages: Budget helps the Nisa retail store to determine the funds for

the future financial performance, it includes requirement of heavy strategies and techniques

which make the future performance more better(Cullen, Tsamenyi, Bernon and Gorst, 2013).

Another advantage of this method is that it has definite planning, it also enhance the

efficiency of the firm, in budgetary control there will be proper communication in all level of

management. But there are some drawback is that budgets are based on the past financial data

and company will not perform same as past, it is not necessary.

Creditors 1254 1465 1987 2657 3654 6575

Cash outflow B 7469 9679 12538 14600 17751 18659

Net cash available (A –

B) 2195 2749 457 1532 639 1787

Labour hour budget

Labour or wages Month 1 Month 2 Month 3

Number of items to be produced in next period 2897 3549 4685

Labour hours per item 2 2 3

Total labour hours required in next period 5794 7098 14055

Cost or expense on each labour hour 8 8 9

Total expenses on labour 46352 56784 126495

Advantage and Disadvantages: Budget helps the Nisa retail store to determine the funds for

the future financial performance, it includes requirement of heavy strategies and techniques

which make the future performance more better(Cullen, Tsamenyi, Bernon and Gorst, 2013).

Another advantage of this method is that it has definite planning, it also enhance the

efficiency of the firm, in budgetary control there will be proper communication in all level of

management. But there are some drawback is that budgets are based on the past financial data

and company will not perform same as past, it is not necessary.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.